Ethical Decision Making in Finance: AAA Seven-Step Model Case Study

VerifiedAdded on 2022/10/12

|4

|1460

|23

Case Study

AI Summary

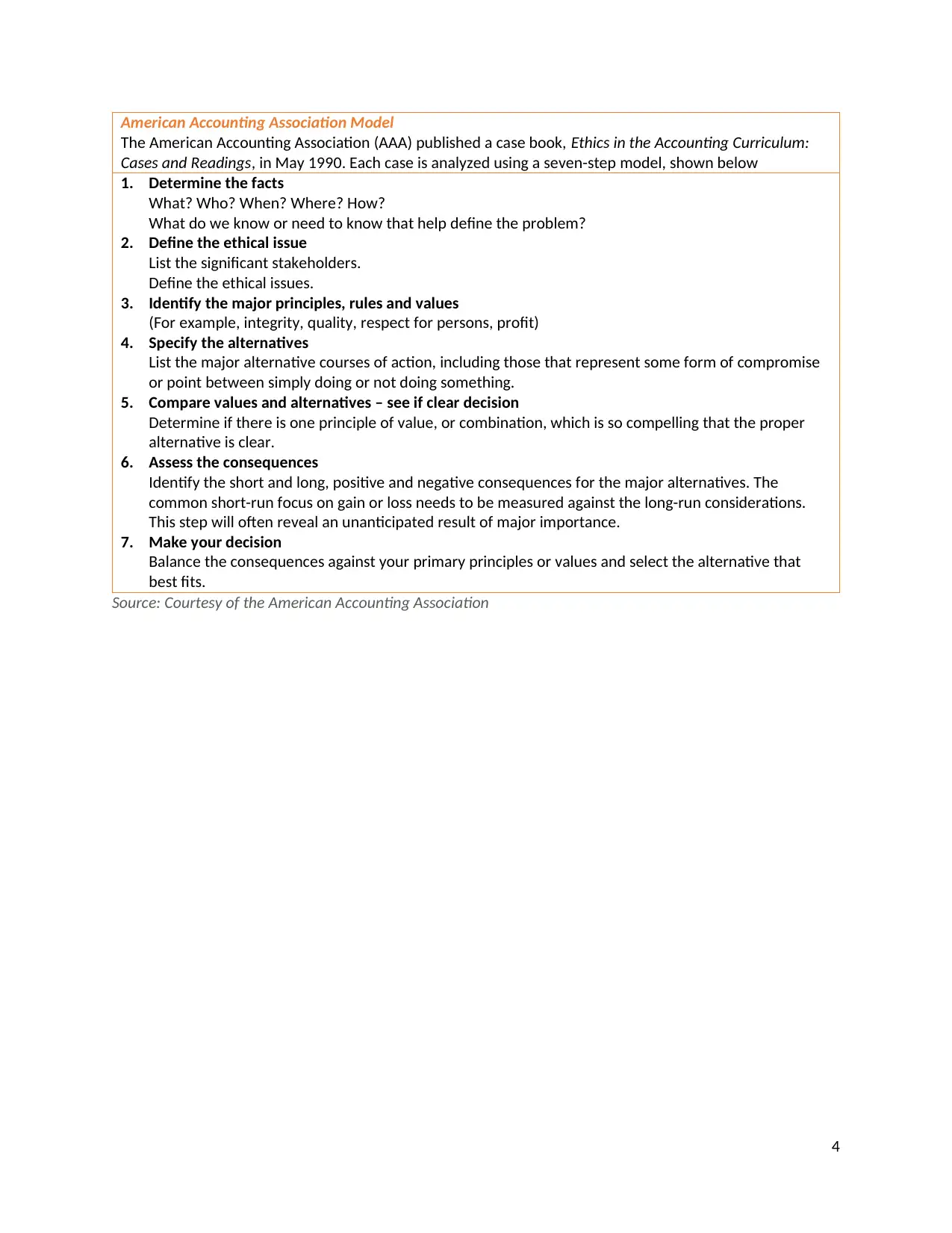

This document presents a detailed case study applying the American Accounting Association (AAA) seven-step model to analyze an ethical dilemma involving a Chartered Accountant associated with a misleading statement. The analysis systematically progresses through the seven steps: establishing facts, identifying ethical issues and stakeholders, determining relevant principles, rules, and values, identifying alternative courses of action, comparing principles to alternatives, analyzing consequences, and finally, making a decision. The case explores various scenarios and potential actions, evaluating their ethical implications and consequences for all stakeholders involved, including the accountant, the employing organization, and other users of the misleading information. The document emphasizes the importance of integrity, professional competence, and due care in ethical decision-making within the finance profession. The solution concludes with a decision based on a well-informed ethical judgment.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.