Ethics and Governance Case Study: Ethical Theories and Practices

VerifiedAdded on 2022/10/11

|15

|3756

|9

Case Study

AI Summary

This case study examines ethical issues within a corporate setting, focusing on the actions of Mr. Goodrich, Arnold, and Amanda. The report analyzes the behavior of the involved parties through the lens of ethical theories such as egoism, utilitarianism, and deontology, exploring how these theories influence decision-making. It also applies the AAA decision-making model to guide ethical choices. Additionally, the case study discusses the CPA's code of ethics, highlighting potential threats and safeguards for CPA members. The analysis covers various aspects of ethical leadership, decision-making, and corporate governance, offering insights into the complexities of ethical dilemmas in business and provides recommendations for ethical practices.

Ethics and Governance

Running Head: BUSINESS AND CORPORATION LAW 0

8 / 1 6 / 2 0 1 9

Student’s Name

Running Head: BUSINESS AND CORPORATION LAW 0

8 / 1 6 / 2 0 1 9

Student’s Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ethics and Governance

1

Executive Summary

The reports started with a section of introduction that provides an outline of the whole

report. The report developed finding on the behavior of parties to the case using different ethical

theories in its first part. In conjunction with the relationship of theories and behavior of parties,

the basic understanding of theories been provided. The second part of the report discussed each

step involved in AAA decision-making model and how Mr. Goodrich can seek ethical decision

using this model. The last of the report developed the focus on APE 110 code of ethics, which

provides guidelines, and standards of behavior to members of Certified Professional Accountants

Australia. This part summarized the threats that Arnold may have being a CPA member and the

safeguard available to him. The report ended with a conclusion that consist of the main finding

of the report.

1

Executive Summary

The reports started with a section of introduction that provides an outline of the whole

report. The report developed finding on the behavior of parties to the case using different ethical

theories in its first part. In conjunction with the relationship of theories and behavior of parties,

the basic understanding of theories been provided. The second part of the report discussed each

step involved in AAA decision-making model and how Mr. Goodrich can seek ethical decision

using this model. The last of the report developed the focus on APE 110 code of ethics, which

provides guidelines, and standards of behavior to members of Certified Professional Accountants

Australia. This part summarized the threats that Arnold may have being a CPA member and the

safeguard available to him. The report ended with a conclusion that consist of the main finding

of the report.

Ethics and Governance

2

Contents

Introduction......................................................................................................................................2

Part A...............................................................................................................................................3

Theory of Egoism: reflection in Goodrich’s behavior 3

Theory of Utilitarianism: reflection in Goodrich’s behavior 4

Theory of Utilitarianism: reflection in Arnold’s behavior 4

Theory of deontology: reflection in Arnold’s behavior 5

Part B...............................................................................................................................................6

Part C...............................................................................................................................................7

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Contents

Introduction......................................................................................................................................2

Part A...............................................................................................................................................3

Theory of Egoism: reflection in Goodrich’s behavior 3

Theory of Utilitarianism: reflection in Goodrich’s behavior 4

Theory of Utilitarianism: reflection in Arnold’s behavior 4

Theory of deontology: reflection in Arnold’s behavior 5

Part B...............................................................................................................................................6

Part C...............................................................................................................................................7

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ethics and Governance

3

Introduction

One may not separate ethics from a business, as it is an essential part of each business.

Decision-makers of business have different ideologies that they use while taking business

decisions. These ideologies are influenced by one or more ethical theories. The report is divided

into three parts namely Part A, B and C. Part will examine the behavior of parties to the case in

the context of different ethical theories. Part B will discuss AAA decision-making model and

will help Mr. Goodrich to take an ethical decision and lastly, part C of the report will make the

focus on fundamental principles, threats, and safeguard relevant to Arnold’s situation. A

conclusion summarizing key point of the report will be presented at the end of the report.

Part A

Theory of Egoism: reflection in Goodrich’s behavior

The theory of ethical egoism is one of the significant theories of ethics, which states that

moral agents are required to do the actions in self-interest (Österberg, 2012). It is concerned with

the manner one should behave. The theory believes that only a person is responsible for his/her

happiness and not the other people and therefore people must think their interest over and above

others. By reviewing the given scenario in the context of this theory this is to state that the

behavior of Mr. Goodrich seems to be affected and influenced by this theory. He did not consider

himself liable for the happiness and future of Amanda and Arnold and only though of about his

position and reputation. During the whole case, he was saving his place. He fired Amanda and

also instructed Arnold to not to share the situation with anyone else as it could bring adverse

impact to his situation in the organization. He threatened Arnold that he will ruin his career if

3

Introduction

One may not separate ethics from a business, as it is an essential part of each business.

Decision-makers of business have different ideologies that they use while taking business

decisions. These ideologies are influenced by one or more ethical theories. The report is divided

into three parts namely Part A, B and C. Part will examine the behavior of parties to the case in

the context of different ethical theories. Part B will discuss AAA decision-making model and

will help Mr. Goodrich to take an ethical decision and lastly, part C of the report will make the

focus on fundamental principles, threats, and safeguard relevant to Arnold’s situation. A

conclusion summarizing key point of the report will be presented at the end of the report.

Part A

Theory of Egoism: reflection in Goodrich’s behavior

The theory of ethical egoism is one of the significant theories of ethics, which states that

moral agents are required to do the actions in self-interest (Österberg, 2012). It is concerned with

the manner one should behave. The theory believes that only a person is responsible for his/her

happiness and not the other people and therefore people must think their interest over and above

others. By reviewing the given scenario in the context of this theory this is to state that the

behavior of Mr. Goodrich seems to be affected and influenced by this theory. He did not consider

himself liable for the happiness and future of Amanda and Arnold and only though of about his

position and reputation. During the whole case, he was saving his place. He fired Amanda and

also instructed Arnold to not to share the situation with anyone else as it could bring adverse

impact to his situation in the organization. He threatened Arnold that he will ruin his career if

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ethics and Governance

4

anything related to payment error would leak in the market. He did not think about the

professional career of Amanda and Arnold as ethical egoism puts thee focus on self-interest. At

each stage of the case, he was trying to keep himself free from every liability irrespective of

others' happiness. Apart from hiding the situation from stakeholders, he also decided to delete all

the records related to the payment error and instructed Arnold to do so. Again, he provided

safeguard to himself hence to say that he applied the theory of egoism in his behavior.

Theory of Utilitarianism: reflection in Goodrich’s behavior

The theory of Utilitarianism decides an action as right or wrong based on its outcome

(Ethicsunwrapped, 2019). It means if the outcome of an act is good for a large group of people

then it considers as ethical under this theory, the theory believes that people must pursue those

acts that lead greater benefits (Mandal, 2010). In the given case, Mr., Goodrich seems to use this

theory in his behavior at few of the incident where he considered the goodness of company i.e. a

larger group of people. As an ultimate decision, Mr. Goodrich decided to not to share the

incident with anyone else as he was considering the result of it on the company at last. He

believed that the company did not have any chances to get the funds from business and the

incident if reported, had the potential to ruin the company. Being on the position of COO, this is

to assume that he had reason to believe in it. Stake and interest of various stakeholder groups

were involved with the company and closure of the same could lead to an adverse situation for

them. In such a situation, Mr., Goodrich found ethical to not to share the information with

anyone which seems to be a correct action as per the principles and beliefs of the theory of

utilitarianism. This action could be negative for a few working groups but consist of the idea of

the greater good.

4

anything related to payment error would leak in the market. He did not think about the

professional career of Amanda and Arnold as ethical egoism puts thee focus on self-interest. At

each stage of the case, he was trying to keep himself free from every liability irrespective of

others' happiness. Apart from hiding the situation from stakeholders, he also decided to delete all

the records related to the payment error and instructed Arnold to do so. Again, he provided

safeguard to himself hence to say that he applied the theory of egoism in his behavior.

Theory of Utilitarianism: reflection in Goodrich’s behavior

The theory of Utilitarianism decides an action as right or wrong based on its outcome

(Ethicsunwrapped, 2019). It means if the outcome of an act is good for a large group of people

then it considers as ethical under this theory, the theory believes that people must pursue those

acts that lead greater benefits (Mandal, 2010). In the given case, Mr., Goodrich seems to use this

theory in his behavior at few of the incident where he considered the goodness of company i.e. a

larger group of people. As an ultimate decision, Mr. Goodrich decided to not to share the

incident with anyone else as he was considering the result of it on the company at last. He

believed that the company did not have any chances to get the funds from business and the

incident if reported, had the potential to ruin the company. Being on the position of COO, this is

to assume that he had reason to believe in it. Stake and interest of various stakeholder groups

were involved with the company and closure of the same could lead to an adverse situation for

them. In such a situation, Mr., Goodrich found ethical to not to share the information with

anyone which seems to be a correct action as per the principles and beliefs of the theory of

utilitarianism. This action could be negative for a few working groups but consist of the idea of

the greater good.

Ethics and Governance

5

Theory of Utilitarianism: reflection in Arnold’s behavior

Arnold had chances to hide the situation from Mr. Goodrich nevertheless; he has shared

the whole situation with him knowing the danger to his job. He considered the interest of the

company and its stakeholders over the self-interest. His lead focus was on the ultimate goodness

of the company. He also made Amanda believe that it is right to let the Goodrich know about this

situation. He spent his whole night in searching for options to deal with the situation. Both of the

options searched by him were expected to bring better outcomes for the company. He wanted to

bring the best results to the company and considering the goodness of various stakeholders he

suggested Mr. Goodrich ask for the help of bankers and unions, as he was aware of the risk of

insolvency. Further, by doing so, the company also could escape situations like damage to

goodwill in the future. In his other option, he has suggested to not to share the incident with

anymore else and to hope that no one notices the same. Nevertheless, this option does not seems

to be ethical but as could save the company hence Arnold developed the same. He was putting all

the efforts to bring the best outcomes for the company and the theory of utilitarianism reflects in

his performance.

Theory of deontology: reflection in Arnold’s behavior

Theory of deontology is just the opposite of the Utilitarianism theory. As Utilitarianism

theory develops its focus on consequences, deontology focuses on actions (Philosophybasics,

2019). The theory states that one must do the actions that are ethical irrespective of the

consequences. In the given cases, sometimes Arnold behaved according to the principles of this

theory. The theory can be seen at the moment when he made the focus on the latter option that is

to ask the help of unions and bankers. Arnold was trying to carry the best results for the company

but also wanted to keep the environment ethical. He was aware of the fact that the company

5

Theory of Utilitarianism: reflection in Arnold’s behavior

Arnold had chances to hide the situation from Mr. Goodrich nevertheless; he has shared

the whole situation with him knowing the danger to his job. He considered the interest of the

company and its stakeholders over the self-interest. His lead focus was on the ultimate goodness

of the company. He also made Amanda believe that it is right to let the Goodrich know about this

situation. He spent his whole night in searching for options to deal with the situation. Both of the

options searched by him were expected to bring better outcomes for the company. He wanted to

bring the best results to the company and considering the goodness of various stakeholders he

suggested Mr. Goodrich ask for the help of bankers and unions, as he was aware of the risk of

insolvency. Further, by doing so, the company also could escape situations like damage to

goodwill in the future. In his other option, he has suggested to not to share the incident with

anymore else and to hope that no one notices the same. Nevertheless, this option does not seems

to be ethical but as could save the company hence Arnold developed the same. He was putting all

the efforts to bring the best outcomes for the company and the theory of utilitarianism reflects in

his performance.

Theory of deontology: reflection in Arnold’s behavior

Theory of deontology is just the opposite of the Utilitarianism theory. As Utilitarianism

theory develops its focus on consequences, deontology focuses on actions (Philosophybasics,

2019). The theory states that one must do the actions that are ethical irrespective of the

consequences. In the given cases, sometimes Arnold behaved according to the principles of this

theory. The theory can be seen at the moment when he made the focus on the latter option that is

to ask the help of unions and bankers. Arnold was trying to carry the best results for the company

but also wanted to keep the environment ethical. He was aware of the fact that the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ethics and Governance

6

consists of many of the stakeholders that have an interest in the business of the company and

hiding anything from them is not ethical. He recommended Mr. Goodrich to declare the error to

the industrial regulator and to ask time to fix the problem. By suggesting this option, Arnold was

trying to ensure transparency and good governance in an organization. He believed there is no

good to put the company into the danger of insolvency and in such a situation; the company

should ask the help of banks and workers. He was not happy with the decision of Goodrich

regarding keeping the information secret and it shows that he believed in ethics in actions and

followed deontology theory of ethics.

Part B

The lead issues which often business manages faces is related to the way in which they

take ethical decisions. They do not understand how to reach up to an ethical conclusion of a

situation. AAA decision-making model helps the managers and decision-makers in such a

situation. This model consists of 7 steps, following which an ethical decision can be attained

(BPP Learning Media, 2013). In the following discussion, the discussion in respect to these 7

steps and their implication to the given case study scenario will be discussed. Starting from the

very first step, this is to state that the same is related to the formation of facts of the case. As the

title of the step implies, Mr. Goodrich will check and review the facts of the whole situation. The

second step requires decision-makers to identify the ethical issues involved in a case (Goza,

2013). Here Mr. Goodrich would check what exact issues related to ethics he may face or facing.

Under the third step of the model, one is required to identify values, norms, and principles of a

case. Under this step all the related principles and rule of law are is to check. Mr. Goodrich will

evaluate different laws applicable to the incident.

6

consists of many of the stakeholders that have an interest in the business of the company and

hiding anything from them is not ethical. He recommended Mr. Goodrich to declare the error to

the industrial regulator and to ask time to fix the problem. By suggesting this option, Arnold was

trying to ensure transparency and good governance in an organization. He believed there is no

good to put the company into the danger of insolvency and in such a situation; the company

should ask the help of banks and workers. He was not happy with the decision of Goodrich

regarding keeping the information secret and it shows that he believed in ethics in actions and

followed deontology theory of ethics.

Part B

The lead issues which often business manages faces is related to the way in which they

take ethical decisions. They do not understand how to reach up to an ethical conclusion of a

situation. AAA decision-making model helps the managers and decision-makers in such a

situation. This model consists of 7 steps, following which an ethical decision can be attained

(BPP Learning Media, 2013). In the following discussion, the discussion in respect to these 7

steps and their implication to the given case study scenario will be discussed. Starting from the

very first step, this is to state that the same is related to the formation of facts of the case. As the

title of the step implies, Mr. Goodrich will check and review the facts of the whole situation. The

second step requires decision-makers to identify the ethical issues involved in a case (Goza,

2013). Here Mr. Goodrich would check what exact issues related to ethics he may face or facing.

Under the third step of the model, one is required to identify values, norms, and principles of a

case. Under this step all the related principles and rule of law are is to check. Mr. Goodrich will

evaluate different laws applicable to the incident.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ethics and Governance

7

In conjunction with he would also evaluate expectations associated with his role in the

company Once he would be done with the identification of the norms, he will move towards the

next step i.e. step 4. From this step, the work of decision-making gets starts in actual. This step

involves preparing a rough draft of all the alternative available to reach up to the decision. Here

this is necessary to state that this step does not consider any norms or principles identified under

step 3. In step 4, Mr. Goodrich would collect all the alternatives available to address the issue

without considering any expectations attached to his role or the law related to the area of issue.

These alternatives may be anything such as hiding the issue from everyone or to announce the

same or anything else. The next step i.e. step 5 can be seen as a good combination of step 3 and 4

where alternatives of step 4 are required to be review considering norms identified under step 3

(Cartlidge, 2011). Mr. Goodrich here would be expected to check the various alternatives as per

the applicable principles. This step helps to understand elements of each alternative and their

capability to resolve the ethical issue. Step 6 develops its focus on the consequences of each

alternative. It is obvious that different alternatives consist of different results hence under this

step, Mr. Goodrich would review what results different alternative would bring to the company

as well as to different stakeholders. It means the pros and cons of various options are used to be

discussed in this step. The seventh step is the final step of this model that lead to the decision

(Verbeke, Roberts, Delaney, Zámborský, Nagar, & Enderwick, 2019). Under this step, Mr.

Goodrich would finally take the decision, which will be an ethical one as this model only

supports to ethical decision making. In this way, by following the studied steps, Mr., Goodrich

will reach up to an ethical decision.

7

In conjunction with he would also evaluate expectations associated with his role in the

company Once he would be done with the identification of the norms, he will move towards the

next step i.e. step 4. From this step, the work of decision-making gets starts in actual. This step

involves preparing a rough draft of all the alternative available to reach up to the decision. Here

this is necessary to state that this step does not consider any norms or principles identified under

step 3. In step 4, Mr. Goodrich would collect all the alternatives available to address the issue

without considering any expectations attached to his role or the law related to the area of issue.

These alternatives may be anything such as hiding the issue from everyone or to announce the

same or anything else. The next step i.e. step 5 can be seen as a good combination of step 3 and 4

where alternatives of step 4 are required to be review considering norms identified under step 3

(Cartlidge, 2011). Mr. Goodrich here would be expected to check the various alternatives as per

the applicable principles. This step helps to understand elements of each alternative and their

capability to resolve the ethical issue. Step 6 develops its focus on the consequences of each

alternative. It is obvious that different alternatives consist of different results hence under this

step, Mr. Goodrich would review what results different alternative would bring to the company

as well as to different stakeholders. It means the pros and cons of various options are used to be

discussed in this step. The seventh step is the final step of this model that lead to the decision

(Verbeke, Roberts, Delaney, Zámborský, Nagar, & Enderwick, 2019). Under this step, Mr.

Goodrich would finally take the decision, which will be an ethical one as this model only

supports to ethical decision making. In this way, by following the studied steps, Mr., Goodrich

will reach up to an ethical decision.

Ethics and Governance

8

Part C

Every professional accountant is required to behave in a standard and ethical manner.

Certified professional accountants (CPA) Australia is a body that consists of and regulates

accounting professional. These accountants are known as CPA members and have to comply

with the code and guidelines provided by a professional accountant. Accounting Professional and

Ethical Standards Board have developed certain code of ethics for CPA members, which are well

known as APES 110 Code of Ethics for Professional Accountants (Moroney, Campbell, &

Hamilton, 2012). This code outlines the standard manner of decision making and working for

CPA members. Now, this is to state that some of the professional accountants remain in business

whereas some of them remain in employment hence the subjective code has three parts. These

parts apply differently to the members in business and members in services. Part A has common

applicability whereas Part B is there for members in public practice and Part c guides members

in business (Cpaaustralia.Com, 2019). Part A, which applies to all members, has a different

significance when it comes to ethics and governance as the same grants fundamental principles.

These principles can be understood as elements, which are required to be there in the behavior of

every CPA member. As Arnold is a CPA member, the following principles would apply to him:-

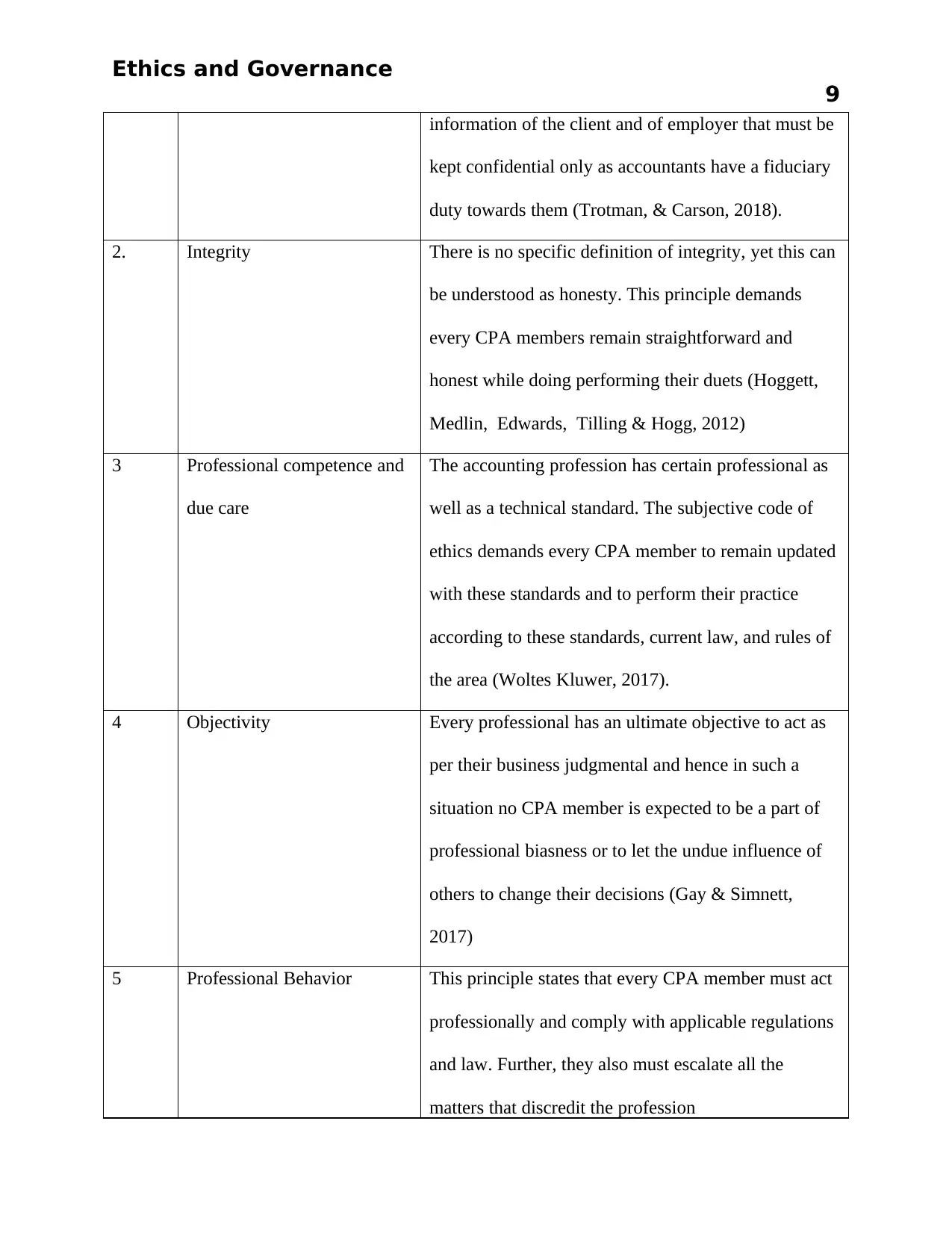

S. No. Title Explanation

1. Confidentiality This is the core and foremost principle applicable. The

Principle states that it is required for CPA members to

keep the confidentiality in their dealing while acting

on behalf of the client (for members in business) or for

client and employer (for members in services). Being

the accountant, they have access to confidential

8

Part C

Every professional accountant is required to behave in a standard and ethical manner.

Certified professional accountants (CPA) Australia is a body that consists of and regulates

accounting professional. These accountants are known as CPA members and have to comply

with the code and guidelines provided by a professional accountant. Accounting Professional and

Ethical Standards Board have developed certain code of ethics for CPA members, which are well

known as APES 110 Code of Ethics for Professional Accountants (Moroney, Campbell, &

Hamilton, 2012). This code outlines the standard manner of decision making and working for

CPA members. Now, this is to state that some of the professional accountants remain in business

whereas some of them remain in employment hence the subjective code has three parts. These

parts apply differently to the members in business and members in services. Part A has common

applicability whereas Part B is there for members in public practice and Part c guides members

in business (Cpaaustralia.Com, 2019). Part A, which applies to all members, has a different

significance when it comes to ethics and governance as the same grants fundamental principles.

These principles can be understood as elements, which are required to be there in the behavior of

every CPA member. As Arnold is a CPA member, the following principles would apply to him:-

S. No. Title Explanation

1. Confidentiality This is the core and foremost principle applicable. The

Principle states that it is required for CPA members to

keep the confidentiality in their dealing while acting

on behalf of the client (for members in business) or for

client and employer (for members in services). Being

the accountant, they have access to confidential

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ethics and Governance

9

information of the client and of employer that must be

kept confidential only as accountants have a fiduciary

duty towards them (Trotman, & Carson, 2018).

2. Integrity There is no specific definition of integrity, yet this can

be understood as honesty. This principle demands

every CPA members remain straightforward and

honest while doing performing their duets (Hoggett,

Medlin, Edwards, Tilling & Hogg, 2012)

3 Professional competence and

due care

The accounting profession has certain professional as

well as a technical standard. The subjective code of

ethics demands every CPA member to remain updated

with these standards and to perform their practice

according to these standards, current law, and rules of

the area (Woltes Kluwer, 2017).

4 Objectivity Every professional has an ultimate objective to act as

per their business judgmental and hence in such a

situation no CPA member is expected to be a part of

professional biasness or to let the undue influence of

others to change their decisions (Gay & Simnett,

2017)

5 Professional Behavior This principle states that every CPA member must act

professionally and comply with applicable regulations

and law. Further, they also must escalate all the

matters that discredit the profession

9

information of the client and of employer that must be

kept confidential only as accountants have a fiduciary

duty towards them (Trotman, & Carson, 2018).

2. Integrity There is no specific definition of integrity, yet this can

be understood as honesty. This principle demands

every CPA members remain straightforward and

honest while doing performing their duets (Hoggett,

Medlin, Edwards, Tilling & Hogg, 2012)

3 Professional competence and

due care

The accounting profession has certain professional as

well as a technical standard. The subjective code of

ethics demands every CPA member to remain updated

with these standards and to perform their practice

according to these standards, current law, and rules of

the area (Woltes Kluwer, 2017).

4 Objectivity Every professional has an ultimate objective to act as

per their business judgmental and hence in such a

situation no CPA member is expected to be a part of

professional biasness or to let the undue influence of

others to change their decisions (Gay & Simnett,

2017)

5 Professional Behavior This principle states that every CPA member must act

professionally and comply with applicable regulations

and law. Further, they also must escalate all the

matters that discredit the profession

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ethics and Governance

10

(Publicaccountants, 2018).

Arnold, in this case, would pursue all the above-tabled principles. To discuss the most relevant

principles for Arnold, this is to mention that being a part of the company he was required to

maintain the confidentiality but since the matter was required to inform stakeholder hence he was

now also to liable to maintain integrity and professionalism. In such a situation, professional

behavior, integrity, and professional due care seem to be the most relevant ones for Arnold. This

is to mention that compliance with these principles becomes difficult sometimes as due to the

threat associated with these principles.

Different threats are there that are there according to the facts and other situations of the case.

Intimidation threat is one of the most significant ones for members who are engaged in service.

The threats consist of a risk to take wrong decisions by members after having undue influence

from employers. Arnold in such a case had the same threat as Mr. Goodrich was of influencing

nature. He did the same and forced Arnold to hide the incident from everyone else. Another

threat that fits in the case is an advocacy threat. The threat consists of a risk that to promote the

best result for client or employer, members would compromise with their objectivity. Arnold

faced this threat, as he had to move from Goodrich’s cabin after knowing his final decision,

although he was aware with the ethics involved in the decision of Mr. Goodrich, yet he

comprised with his objectivity. Familiarity threat was also relevant to Arnold's situation as he

was a part of the company. This threat is related to the principle of objectivity and professional

behavior and doubts that Arnold may work in the interest of the company forgetting the

principles applies to him being a member of CPA.

10

(Publicaccountants, 2018).

Arnold, in this case, would pursue all the above-tabled principles. To discuss the most relevant

principles for Arnold, this is to mention that being a part of the company he was required to

maintain the confidentiality but since the matter was required to inform stakeholder hence he was

now also to liable to maintain integrity and professionalism. In such a situation, professional

behavior, integrity, and professional due care seem to be the most relevant ones for Arnold. This

is to mention that compliance with these principles becomes difficult sometimes as due to the

threat associated with these principles.

Different threats are there that are there according to the facts and other situations of the case.

Intimidation threat is one of the most significant ones for members who are engaged in service.

The threats consist of a risk to take wrong decisions by members after having undue influence

from employers. Arnold in such a case had the same threat as Mr. Goodrich was of influencing

nature. He did the same and forced Arnold to hide the incident from everyone else. Another

threat that fits in the case is an advocacy threat. The threat consists of a risk that to promote the

best result for client or employer, members would compromise with their objectivity. Arnold

faced this threat, as he had to move from Goodrich’s cabin after knowing his final decision,

although he was aware with the ethics involved in the decision of Mr. Goodrich, yet he

comprised with his objectivity. Familiarity threat was also relevant to Arnold's situation as he

was a part of the company. This threat is related to the principle of objectivity and professional

behavior and doubts that Arnold may work in the interest of the company forgetting the

principles applies to him being a member of CPA.

Ethics and Governance

11

Now after the discussion of threats, safeguards are also required to discuss. As the name implies,

these safeguards provide how identified threats can be addressed. The code itself provides

safeguard to deal with various threats. These safeguards are divided into two categories. First,

those, which are provided by profession, legislation and regulation and others, are those that

developed in the work environment. Arnold many use both kinds of safeguards. To eliminate the

advocacy threat, he may ask for the help of an independent reviewer who would have no

influence from Mr. Goodrich and can provide independent advice. Further, to seek an ethical

decision, he may ask advice from independent audit panel. Another threat i.e. intimidation threat

can be eliminated by informing the whole situation to senior management or compliance head of

the company. To minimize the undue influence of Mr. Goodrich, Arnold can report the issue to

higher authorities than Mr. Goodrich. Few people are there in businesses that have the expertise

of the matter, hence Arnold may seek the assistance of those people and can analyze the way in

which he may maintain confidentially of his organization along with maintaining the dignity of

the profession.

If to discuss the safeguards provided by the work environment, Arnold has the option to take

help of ethics or corporate governance of the company if any. This seems to be the best

safeguard available to Arnold as by using this, he may eliminate any chances of litigations and

can save his time and cost. Further by doing this, he can also act in the best interest of the

organization, which is also his duty in conjunction with compliance of principles of the

profession.

11

Now after the discussion of threats, safeguards are also required to discuss. As the name implies,

these safeguards provide how identified threats can be addressed. The code itself provides

safeguard to deal with various threats. These safeguards are divided into two categories. First,

those, which are provided by profession, legislation and regulation and others, are those that

developed in the work environment. Arnold many use both kinds of safeguards. To eliminate the

advocacy threat, he may ask for the help of an independent reviewer who would have no

influence from Mr. Goodrich and can provide independent advice. Further, to seek an ethical

decision, he may ask advice from independent audit panel. Another threat i.e. intimidation threat

can be eliminated by informing the whole situation to senior management or compliance head of

the company. To minimize the undue influence of Mr. Goodrich, Arnold can report the issue to

higher authorities than Mr. Goodrich. Few people are there in businesses that have the expertise

of the matter, hence Arnold may seek the assistance of those people and can analyze the way in

which he may maintain confidentially of his organization along with maintaining the dignity of

the profession.

If to discuss the safeguards provided by the work environment, Arnold has the option to take

help of ethics or corporate governance of the company if any. This seems to be the best

safeguard available to Arnold as by using this, he may eliminate any chances of litigations and

can save his time and cost. Further by doing this, he can also act in the best interest of the

organization, which is also his duty in conjunction with compliance of principles of the

profession.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.