Ethics and Governance: Analysis of a Corporate Case Study

VerifiedAdded on 2022/10/07

|15

|3781

|20

Case Study

AI Summary

This case study delves into the ethical failings within a corporation, focusing on the behaviors of key figures like Mr. Goodrich and Arnold. It examines the application of ethical theories such as egoism, utilitarianism, and deontology to analyze their decision-making processes. The assignment assesses Mr. Goodrich's leadership style, particularly his 'whatever it takes' approach, and its impact on subordinates. It scrutinizes Arnold's inaccurate financial reporting and its consequences for stakeholders. The analysis incorporates ethical decision-making models, including the AAA model, to evaluate the ethical dilemmas and recommend appropriate actions. The case study also applies the APES 110 code of ethics to advise Arnold on proper conduct. The paper highlights the importance of ethical leadership, the consequences of unethical practices, and the need for robust ethical frameworks to ensure responsible corporate behavior. This case study provides insights into the complexities of ethical decision-making and the importance of upholding ethical standards within organizations.

Running head: ETHICS AND GOVERNANCE

ETHICS AND GOVERNANCE

Name of the Student:

Name of the University:

Author note:

ETHICS AND GOVERNANCE

Name of the Student:

Name of the University:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ETHICS AND GOVERNANCE

Executive Summary

Management serves imperative role in inculcating workplace ethics in workplace. Top

management necessitates inaugurating proper instances for their dependents. Management

requires to acts as a foundation of stimulus and enthusiasm for the workforces. It is normally

perceived that team managers, frontrunners or top hierarchical leaders tend to guide their

underlings to unlimited point. Superiors strictly necessitate obeying to rules and regulations

of the organization in provision of their workforces to follow the same. It has noted that the

opinion that as corporations progresses or advances their external operations, intend to

decentralize their business functions and empower their workforce, it is vital for the top

management level to progress ethical practices which proposition the essential training and

mechanisms to promise that their employees can make ethical decisions. The following paper

have analysed the case of an organization where ethical situation regarding top hierarchical

leaders have deteriorated strictly resulting to unethical decision making practices with the

organization.

Executive Summary

Management serves imperative role in inculcating workplace ethics in workplace. Top

management necessitates inaugurating proper instances for their dependents. Management

requires to acts as a foundation of stimulus and enthusiasm for the workforces. It is normally

perceived that team managers, frontrunners or top hierarchical leaders tend to guide their

underlings to unlimited point. Superiors strictly necessitate obeying to rules and regulations

of the organization in provision of their workforces to follow the same. It has noted that the

opinion that as corporations progresses or advances their external operations, intend to

decentralize their business functions and empower their workforce, it is vital for the top

management level to progress ethical practices which proposition the essential training and

mechanisms to promise that their employees can make ethical decisions. The following paper

have analysed the case of an organization where ethical situation regarding top hierarchical

leaders have deteriorated strictly resulting to unethical decision making practices with the

organization.

2ETHICS AND GOVERNANCE

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Implementation of ethical theories.........................................................................................4

Analysis of Mr. Goodrich’s behaviour using theory of egoism.............................................4

Analysis of Mr. Goodrich’s behaviour using theory of Utilitarianism..................................5

Analysis of Arnold’s behaviour using theory of Utilitarianism.............................................6

Analysis of Arnold’s behaviour using theory of Deontology................................................6

Understanding Ethical decision-making model.....................................................................7

Using APES 110 to Advice Arnold’s Appropriate Actions...................................................8

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Implementation of ethical theories.........................................................................................4

Analysis of Mr. Goodrich’s behaviour using theory of egoism.............................................4

Analysis of Mr. Goodrich’s behaviour using theory of Utilitarianism..................................5

Analysis of Arnold’s behaviour using theory of Utilitarianism.............................................6

Analysis of Arnold’s behaviour using theory of Deontology................................................6

Understanding Ethical decision-making model.....................................................................7

Using APES 110 to Advice Arnold’s Appropriate Actions...................................................8

Conclusion................................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ETHICS AND GOVERNANCE

Introduction

Management plays decisive role in inculcating workplace ethics in workplace. Top

management requires establishing proper examples for their subordinates. Management

requires to acts as a source of inspiration and enthusiasm for the employees. It is typically

observed that team managers, leaders or top hierarchical leaders tend to influence their

subordinates to great degree. Superiors strictly require adhering to rules and regulations of

the organization in support of their employees to pursue the same. Shin et al. (2015) are of

the opinion that as companies develop or improve their overseas operations, intend to

decentralize their business functions and empower their workforce, it is essential for the top

management level to develop ethical practices which offer the essential training and

mechanisms to guarantee that their employees can make ethical decisions. Such strategies

will decrease organization’s vulnerability to misconduct and the harm it might cause to

revenue making, profitability, company image and management focus. However, Melé,

Rosanas and Fontrodona (2017) have claimed that while CEOs, COOs or top hierarchical

business leaders tend to establish an ethical workplace culture, forming proper foundation

provides correct direction and employees must show the accountability to follow it. The

following paper will analyse the case of an organization where ethical situation concerning

top hierarchical leaders have deteriorated severely resulting to unethical decision making

practices with the organization.

Introduction

Management plays decisive role in inculcating workplace ethics in workplace. Top

management requires establishing proper examples for their subordinates. Management

requires to acts as a source of inspiration and enthusiasm for the employees. It is typically

observed that team managers, leaders or top hierarchical leaders tend to influence their

subordinates to great degree. Superiors strictly require adhering to rules and regulations of

the organization in support of their employees to pursue the same. Shin et al. (2015) are of

the opinion that as companies develop or improve their overseas operations, intend to

decentralize their business functions and empower their workforce, it is essential for the top

management level to develop ethical practices which offer the essential training and

mechanisms to guarantee that their employees can make ethical decisions. Such strategies

will decrease organization’s vulnerability to misconduct and the harm it might cause to

revenue making, profitability, company image and management focus. However, Melé,

Rosanas and Fontrodona (2017) have claimed that while CEOs, COOs or top hierarchical

business leaders tend to establish an ethical workplace culture, forming proper foundation

provides correct direction and employees must show the accountability to follow it. The

following paper will analyse the case of an organization where ethical situation concerning

top hierarchical leaders have deteriorated severely resulting to unethical decision making

practices with the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ETHICS AND GOVERNANCE

Discussion

Implementation of ethical theories

Analysis of Mr. Goodrich’s behaviour using theory of egoism

One management ethics theoretical issue can be explained as the difference between

two alternate theoretical perspectives namely managerial moral monism and managerial

limited moral pluralism (Mill, 2016). Chan et al. (2016) have noted that moral monism

upholds that managerial moral performance is assured by the reliable and influential

understanding of a single management theory with a single ethics theory. For example, top

hierarchical leaders exhibiting ethical egoism depending on balanced goal management

theory tend to suggest that optimal managerial moral performance must be determined by the

extent which will eventually upsurge his individual success and wealth. Moreover, lack of

sufficiency related to theoretical deliberation of other management theories in addition to the

roles of moral constraint, character as well as perspective related to leaders’ decision-making

show a tendency to incentivize egoistic managers in order to continue to using unlawful

approaches and strategies to obtain individualistic accomplishments. By means of such

procedure, egoistic organizational leaders raised viciousness within the organizational culture

instead of following integration and commitment further creating corrupted culture which

propagates utmost insatiability and self-indulgence. However, drawing insights from the case

of ethical decision making, Mr. Goodrich’s behavioural approach towards his subordinates

did not exhibit any advocacy of selfishness or harming others. Furthermore, his ‘whatever it

takes guys’ approach aided his company to meet crucial targets and acquire reputation of a

successful achiever. Thus, considering ethical egoism in the case of Mr. Goodrich, there can

be found several underlying factors to suppose that showing stringency to subordinates

results to enduring self-interest (Bell, Dyck & Neubert, 2017). Consequently, such egoist

Discussion

Implementation of ethical theories

Analysis of Mr. Goodrich’s behaviour using theory of egoism

One management ethics theoretical issue can be explained as the difference between

two alternate theoretical perspectives namely managerial moral monism and managerial

limited moral pluralism (Mill, 2016). Chan et al. (2016) have noted that moral monism

upholds that managerial moral performance is assured by the reliable and influential

understanding of a single management theory with a single ethics theory. For example, top

hierarchical leaders exhibiting ethical egoism depending on balanced goal management

theory tend to suggest that optimal managerial moral performance must be determined by the

extent which will eventually upsurge his individual success and wealth. Moreover, lack of

sufficiency related to theoretical deliberation of other management theories in addition to the

roles of moral constraint, character as well as perspective related to leaders’ decision-making

show a tendency to incentivize egoistic managers in order to continue to using unlawful

approaches and strategies to obtain individualistic accomplishments. By means of such

procedure, egoistic organizational leaders raised viciousness within the organizational culture

instead of following integration and commitment further creating corrupted culture which

propagates utmost insatiability and self-indulgence. However, drawing insights from the case

of ethical decision making, Mr. Goodrich’s behavioural approach towards his subordinates

did not exhibit any advocacy of selfishness or harming others. Furthermore, his ‘whatever it

takes guys’ approach aided his company to meet crucial targets and acquire reputation of a

successful achiever. Thus, considering ethical egoism in the case of Mr. Goodrich, there can

be found several underlying factors to suppose that showing stringency to subordinates

results to enduring self-interest (Bell, Dyck & Neubert, 2017). Consequently, such egoist

5ETHICS AND GOVERNANCE

leaders as per theoretical explanation of ethical egoism show tendency to act diligently for

acquiring organizational aims rather than posing self-harm. Schminke, Arnaud and Taylor

(2015). have claimed that ethical egoism aligns with principles of rational morality related to

deference, morality, and benevolence. Drawing relevance to theoretical understanding of

egoism it can be asserted that Mr. Goodrich organizational decision-making abilities may

outlawed acts of self-regard in highly blameworthy sense, it has resulted his subordinates to

attain motivational focus in order to establish on individualistic interests or organizational

benefit.

Analysis of Mr. Goodrich’s behaviour using theory of Utilitarianism

Comprehensive studies have explained that management’s best result is not

necessarily driven towards the greatest good for the greatest number (Vitell & Hunt, 2015). It

primarily focuses on products delivering on return of investment. Thus, considering Mr.

Goodrich decision making approach has principally shed light on the very contradiction of

the Happiness Principle. Schminke, Arnaud and Taylor (2015) have mentioned that

utilitarianism as a moral theory considers that only thing relevant to determine an action to be

right or wrong must be determined from the outcome of the action. Thus, outcomes of actions

show great decisiveness while analysing leadership skills of top hierarchical leaders.

Considering the approach of Mr. Goodrich, it can be asserted that his decision making

strategies and leadership abilities exhibit showed robust connotation towards

consequentialism outcomes. His strategic decisions focused on side-tracking the motives of

his actions and essentially focused on the outcome. Drawing relevance to these factors, it can

be noted that Goodrich’s management strategies aligned greatly to consequentialism rather

than utilitarianism. According to Zeni and Griffith (2016), as consequentialism management

measures results rather than shedding light on intentions and moral motives related to the

action derived from Kantian theory of ethics. Moreover, managerial dimensions often fail to

leaders as per theoretical explanation of ethical egoism show tendency to act diligently for

acquiring organizational aims rather than posing self-harm. Schminke, Arnaud and Taylor

(2015). have claimed that ethical egoism aligns with principles of rational morality related to

deference, morality, and benevolence. Drawing relevance to theoretical understanding of

egoism it can be asserted that Mr. Goodrich organizational decision-making abilities may

outlawed acts of self-regard in highly blameworthy sense, it has resulted his subordinates to

attain motivational focus in order to establish on individualistic interests or organizational

benefit.

Analysis of Mr. Goodrich’s behaviour using theory of Utilitarianism

Comprehensive studies have explained that management’s best result is not

necessarily driven towards the greatest good for the greatest number (Vitell & Hunt, 2015). It

primarily focuses on products delivering on return of investment. Thus, considering Mr.

Goodrich decision making approach has principally shed light on the very contradiction of

the Happiness Principle. Schminke, Arnaud and Taylor (2015) have mentioned that

utilitarianism as a moral theory considers that only thing relevant to determine an action to be

right or wrong must be determined from the outcome of the action. Thus, outcomes of actions

show great decisiveness while analysing leadership skills of top hierarchical leaders.

Considering the approach of Mr. Goodrich, it can be asserted that his decision making

strategies and leadership abilities exhibit showed robust connotation towards

consequentialism outcomes. His strategic decisions focused on side-tracking the motives of

his actions and essentially focused on the outcome. Drawing relevance to these factors, it can

be noted that Goodrich’s management strategies aligned greatly to consequentialism rather

than utilitarianism. According to Zeni and Griffith (2016), as consequentialism management

measures results rather than shedding light on intentions and moral motives related to the

action derived from Kantian theory of ethics. Moreover, managerial dimensions often fail to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ETHICS AND GOVERNANCE

be constructively associated with the Happiness Principle. Consequently, most management

ethics of Goodrich do not align to considerations of consequentialism or utilitarianism.

Analysis of Arnold’s behaviour using theory of Utilitarianism

Contemporary businesses require applying utilitarianism to distinguish rightness or

wrongness of actions being executed (Dörr & Hollnbuchner, 2017). Considering case study,

it has been noted that Arnold serving the role of management accountant showed utmost

incompetence in providing accurate financial report to Mr. Goodrich. Schminke, Arnaud and

Taylor (2015) have mentioned that inaccurate financial reporting tends to be the result of lack

of diligence, misinterpretation and dishonesty. Drawing insights from the case study, it has

been noted that Arnold faulty financial reporting has posed threats to the company’s

stakeholders and further impacted company’s credibility with the COO and investors. At this

juncture, Arnold failed to draw relevance to welfarism is the understanding that inequality or

correctness of operations mainly relies on conceptions of benefits. As per the study of Zeni

and Griffith (2016), welfarism principally aims at capitalizing on services and benefits of

every individual. While, the challenge that utilitarianism poses to other interpretations

depends on the probability of the consequences of disrupting the moral rules and regulations.

Analysis of Arnold’s behaviour using theory of Deontology

Ethics is regarded as the study of morality and the way to reliably practice impeccable

character formation and behaviour. Theory of deontology implies on the way individuals

judge the morality of others on the basis of set of principles and rules. Meanwhile, in the

domain of economics, deontology is understood as the foundation of any decision taken by

the employee and is considered as the fundament of any organizational milieu. Similarly,

drawing relevance to the insights gathered from the case of Arnold, engaged to the role of

management accountant, it has been observed that employees must balance ‘the means of an

be constructively associated with the Happiness Principle. Consequently, most management

ethics of Goodrich do not align to considerations of consequentialism or utilitarianism.

Analysis of Arnold’s behaviour using theory of Utilitarianism

Contemporary businesses require applying utilitarianism to distinguish rightness or

wrongness of actions being executed (Dörr & Hollnbuchner, 2017). Considering case study,

it has been noted that Arnold serving the role of management accountant showed utmost

incompetence in providing accurate financial report to Mr. Goodrich. Schminke, Arnaud and

Taylor (2015) have mentioned that inaccurate financial reporting tends to be the result of lack

of diligence, misinterpretation and dishonesty. Drawing insights from the case study, it has

been noted that Arnold faulty financial reporting has posed threats to the company’s

stakeholders and further impacted company’s credibility with the COO and investors. At this

juncture, Arnold failed to draw relevance to welfarism is the understanding that inequality or

correctness of operations mainly relies on conceptions of benefits. As per the study of Zeni

and Griffith (2016), welfarism principally aims at capitalizing on services and benefits of

every individual. While, the challenge that utilitarianism poses to other interpretations

depends on the probability of the consequences of disrupting the moral rules and regulations.

Analysis of Arnold’s behaviour using theory of Deontology

Ethics is regarded as the study of morality and the way to reliably practice impeccable

character formation and behaviour. Theory of deontology implies on the way individuals

judge the morality of others on the basis of set of principles and rules. Meanwhile, in the

domain of economics, deontology is understood as the foundation of any decision taken by

the employee and is considered as the fundament of any organizational milieu. Similarly,

drawing relevance to the insights gathered from the case of Arnold, engaged to the role of

management accountant, it has been observed that employees must balance ‘the means of an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ETHICS AND GOVERNANCE

end’ with the vital ‘moral duty’ and accomplish the said duty. According to authors,

employees engaged in any domain of economy have shown certain degree of susceptibility to

deontological dilemma. Considering the case of Arnold, he encountered deontological

dilemma during decision-making situation of making financial reporting. Furthermore, as per

the view of Schminke, Arnaud and Taylor (2015), any employee associated with an economic

process tends to admit that on any particular decision-making in which he has been involved

in front of a deontological dilemma by unalloyed reflex, without considering roles and

responsibilities expected from him as well as relevant consequences.

Understanding Ethical decision-making model

Decision-making models provide systematic framework in order to attain most

effective course of action. Zeni and Griffith (2016) have noted that decision to increase or not

to elevate production to perfectly align to organizations’ demand acts as a critical decision,

yet has been considerably routine as well as structured. Considering Mr. Goodrich showing

interest in Arnold’s financial report and aiming to derive most effective outcome from it, he

must apply AAA decision making model which will enable him to take ongoing ethical issues

in the company into consideration. According to authors, many business decisions have

ethical factors attached to them. It is typically due to the impacts of those decisions and the

fact that effects show potential to impact stakeholders in various ways and will articulate

varied ethical values and perceptions. Analysing the case study, it can be understood that Mr.

Goodrich can undergo 7 step-process of AAA model to generate most effective outcome for

his organization. At the first juncture, while evaluating Arnold’s financial report, COO

Goodrich must determine the facts related to past financial position of the company and

investments. It can be noted as there is less ambiguity in the first step of AAA model;

Goodrich can be responsive to Arnold’s report and then scrutinize the data and figures of the

particular financial reporting. This is the 2nd step of the AAA model where ethical issues are

end’ with the vital ‘moral duty’ and accomplish the said duty. According to authors,

employees engaged in any domain of economy have shown certain degree of susceptibility to

deontological dilemma. Considering the case of Arnold, he encountered deontological

dilemma during decision-making situation of making financial reporting. Furthermore, as per

the view of Schminke, Arnaud and Taylor (2015), any employee associated with an economic

process tends to admit that on any particular decision-making in which he has been involved

in front of a deontological dilemma by unalloyed reflex, without considering roles and

responsibilities expected from him as well as relevant consequences.

Understanding Ethical decision-making model

Decision-making models provide systematic framework in order to attain most

effective course of action. Zeni and Griffith (2016) have noted that decision to increase or not

to elevate production to perfectly align to organizations’ demand acts as a critical decision,

yet has been considerably routine as well as structured. Considering Mr. Goodrich showing

interest in Arnold’s financial report and aiming to derive most effective outcome from it, he

must apply AAA decision making model which will enable him to take ongoing ethical issues

in the company into consideration. According to authors, many business decisions have

ethical factors attached to them. It is typically due to the impacts of those decisions and the

fact that effects show potential to impact stakeholders in various ways and will articulate

varied ethical values and perceptions. Analysing the case study, it can be understood that Mr.

Goodrich can undergo 7 step-process of AAA model to generate most effective outcome for

his organization. At the first juncture, while evaluating Arnold’s financial report, COO

Goodrich must determine the facts related to past financial position of the company and

investments. It can be noted as there is less ambiguity in the first step of AAA model;

Goodrich can be responsive to Arnold’s report and then scrutinize the data and figures of the

particular financial reporting. This is the 2nd step of the AAA model where ethical issues are

8ETHICS AND GOVERNANCE

principally been distinguished. While, analysing the case study, it has been found that Arnold

tried to explain his COO about paying factory workers from inaccurate staff award for last

two years. Furthermore, COO Goodrich should evaluate fact whether Arnold was involved in

any illegal monetary transaction (Curtis et al., 2017). The third step of AAA model is related

to an identification of norms, values and standards of the case. At this juncture, COO

Goodrich must place his decision in utmost professional context by upholding ethical norms

of company. Considering Goodrich’s aggressive response to Arnold’s report could have been

mitigated to maintain basic professional behaviour context of the company. As the report

contained assets, liabilities, investment, income, and expense of the company, these should

have been taken as relevant determinant to consider in such scenario.

Furthermore, Mr. Goodrich must propose alternative action to Arnold if he has been

indulged in any acceptance of bribe. Moreover, to generate best outcome for his company

COO Goodrich must update Arnold about severe consequences of acceptance of bribe where

he encounter risk of both legal and professional issues. Joshi and Li (2016) have mentioned

that the fundamental aim of AAA model is to mention the implications of each outcome in

explicit manner in order to produce comprehensive decision with proper acknowledgement of

each employee. By implementing AAA decision making model, COO might consider

shifting responsibilities to evade Arnold from becoming entrenched in his position.

Furthermore, he should focus on provide legal clauses all staffs who have fiduciary

accountability of protecting the company from any form of employee theft.

Using APES 110 to Advice Arnold’s Appropriate Actions

APES 110 the Accounting Professional and Ethical Standards Board (APESB) has

issued Code of Ethics for Professional Accountants (Code). APESB is known as an

autonomous entity established in 2006 as an initiative of CPA Australia and Chartered

Accountants in Australia and New Zealand. Considering the case study if Arnold is assumed

principally been distinguished. While, analysing the case study, it has been found that Arnold

tried to explain his COO about paying factory workers from inaccurate staff award for last

two years. Furthermore, COO Goodrich should evaluate fact whether Arnold was involved in

any illegal monetary transaction (Curtis et al., 2017). The third step of AAA model is related

to an identification of norms, values and standards of the case. At this juncture, COO

Goodrich must place his decision in utmost professional context by upholding ethical norms

of company. Considering Goodrich’s aggressive response to Arnold’s report could have been

mitigated to maintain basic professional behaviour context of the company. As the report

contained assets, liabilities, investment, income, and expense of the company, these should

have been taken as relevant determinant to consider in such scenario.

Furthermore, Mr. Goodrich must propose alternative action to Arnold if he has been

indulged in any acceptance of bribe. Moreover, to generate best outcome for his company

COO Goodrich must update Arnold about severe consequences of acceptance of bribe where

he encounter risk of both legal and professional issues. Joshi and Li (2016) have mentioned

that the fundamental aim of AAA model is to mention the implications of each outcome in

explicit manner in order to produce comprehensive decision with proper acknowledgement of

each employee. By implementing AAA decision making model, COO might consider

shifting responsibilities to evade Arnold from becoming entrenched in his position.

Furthermore, he should focus on provide legal clauses all staffs who have fiduciary

accountability of protecting the company from any form of employee theft.

Using APES 110 to Advice Arnold’s Appropriate Actions

APES 110 the Accounting Professional and Ethical Standards Board (APESB) has

issued Code of Ethics for Professional Accountants (Code). APESB is known as an

autonomous entity established in 2006 as an initiative of CPA Australia and Chartered

Accountants in Australia and New Zealand. Considering the case study if Arnold is assumed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ETHICS AND GOVERNANCE

to be member of CPA Australia, he must comply with the Codes unless he is prevented from

complying so by relevant laws or regulations. By adhering to paragraph 100.1, Arnold must

understand that his fundamental accountability as a financial accountant must rely on public

interest.

The official website mentions that Paragraph 100.1 of the Code explains that a

distinctive mark of the accountancy profession depends on its recognition of the

responsibility to serve for public interest (CPAAustralia.com.au, 2019). As a result, Arnold’s

major accountability responsibility is not simply to contend any specific client or employer

but to the public as a whole.

Furthermore, 100.5 paragraph of APES code highlights importance of integrity,

objectivity, professional ability, professional behaviour and confidentiality. While adhering to

this code, Arnold must uphold his professional knowledge and competences as member of

CPA Australia in order to ensure that his organization receives capable professional services

on the basis of ongoing developments in practice, legislation, methods and techniques and

must serve with utmost diligence and in compliance with relevant technical as well as

professional standards. Furthermore, as per the principles of APES 110, employees must

defer to the discretion of information obtained as outcome of professional and business

associations. Taking into Arnold’s case as being member of CPA Australia, Arnold must

conceal any data or information from any third party entity unless there can be seen any

obligation or professional duty to reveal information. He should further take into account that

Arnold as CPA member must not use the information for individual benefit.

In addition to this, APES 110 offers conceptual framework (100.6 to 100.11), which

will help CPA members to use their professional judgement. Considering Arnold as member

of CPA, he must utilize professional decision making strategies to proficiently identify any

risks to compliance with major principles, assess the value of recognized threats and further

to be member of CPA Australia, he must comply with the Codes unless he is prevented from

complying so by relevant laws or regulations. By adhering to paragraph 100.1, Arnold must

understand that his fundamental accountability as a financial accountant must rely on public

interest.

The official website mentions that Paragraph 100.1 of the Code explains that a

distinctive mark of the accountancy profession depends on its recognition of the

responsibility to serve for public interest (CPAAustralia.com.au, 2019). As a result, Arnold’s

major accountability responsibility is not simply to contend any specific client or employer

but to the public as a whole.

Furthermore, 100.5 paragraph of APES code highlights importance of integrity,

objectivity, professional ability, professional behaviour and confidentiality. While adhering to

this code, Arnold must uphold his professional knowledge and competences as member of

CPA Australia in order to ensure that his organization receives capable professional services

on the basis of ongoing developments in practice, legislation, methods and techniques and

must serve with utmost diligence and in compliance with relevant technical as well as

professional standards. Furthermore, as per the principles of APES 110, employees must

defer to the discretion of information obtained as outcome of professional and business

associations. Taking into Arnold’s case as being member of CPA Australia, Arnold must

conceal any data or information from any third party entity unless there can be seen any

obligation or professional duty to reveal information. He should further take into account that

Arnold as CPA member must not use the information for individual benefit.

In addition to this, APES 110 offers conceptual framework (100.6 to 100.11), which

will help CPA members to use their professional judgement. Considering Arnold as member

of CPA, he must utilize professional decision making strategies to proficiently identify any

risks to compliance with major principles, assess the value of recognized threats and further

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ETHICS AND GOVERNANCE

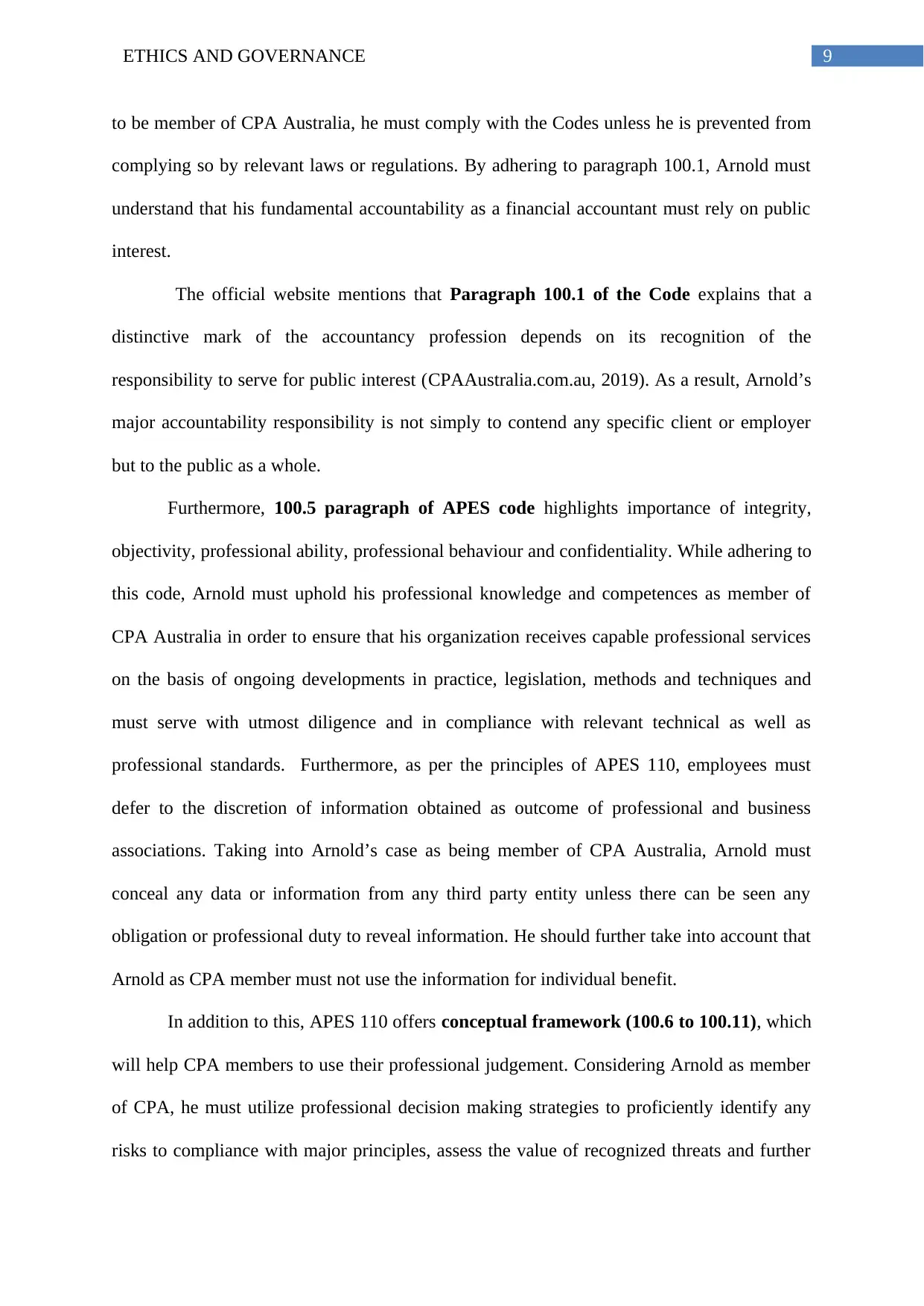

implement safety measures in order to remove or mitigate threats considerably. Authors have

noted that members of CPA in these cases must focus on lessening or suspend professional

service when required. APES 110 Code is primarily based on a conceptual framework that

necessitates dynamic deliberation of problems based on the fundamental principles. The

framework can be functional to contradictory circumstances and be dependent on on

professional judgement rather than on particular rules.

APES 110 Conceptual Framework

Source: (CPAAustralia.com.au, 2019).

However, any accountant professional might encounter threats in his professional

career which could be avoided if they comply with fundamental principles of APES 110.

Paragraph 100.12 of APES 110 Code clearly points out that risks might fall into the realm

of self-interest, self-evaluation, advocacy, intimidation or knowledge. Considering Arnold’s

role as CPA member, it can be observed that Arnold in his profession of financial accountant

implement safety measures in order to remove or mitigate threats considerably. Authors have

noted that members of CPA in these cases must focus on lessening or suspend professional

service when required. APES 110 Code is primarily based on a conceptual framework that

necessitates dynamic deliberation of problems based on the fundamental principles. The

framework can be functional to contradictory circumstances and be dependent on on

professional judgement rather than on particular rules.

APES 110 Conceptual Framework

Source: (CPAAustralia.com.au, 2019).

However, any accountant professional might encounter threats in his professional

career which could be avoided if they comply with fundamental principles of APES 110.

Paragraph 100.12 of APES 110 Code clearly points out that risks might fall into the realm

of self-interest, self-evaluation, advocacy, intimidation or knowledge. Considering Arnold’s

role as CPA member, it can be observed that Arnold in his profession of financial accountant

11ETHICS AND GOVERNANCE

might sometimes fail to review financial results with utmost accuracy or investments made

by the employer. Furthermore, often members tend to encounter threats owing to distant or

intimate association with client. However, drawing insights from these categories of threat,

Arnold might experience close association with any of his clients, which can further give rise

to ethical dilemma while offering current service (CPAAustralia.com.au, 2019).

Furthermore, as per the principle of APES 110 in 100.3, safeguard as actions or

measures can be seen as effective which may be eliminate risks or to some extent in

acceptable level. Arnold must take into consideration safeguard measures to avoid any type

of financial threats during his services at an acceptable threat. An acceptable level is

considered as the level where considerable as well as informed third party entity would be

likely to conclude, considering all particular facts and conditions obtainable to the associate

at that time that compliance with the important principles is not cooperated or negotiated.

However, if threats fail to be abolished or abridged to a satisfactory level as the pressures

show great degree of severity or there is lack of precautions or cannot be applied to report the

coercions, in these cases, the context or relationship producing the threats must be

circumvented. Considering Arnold’s role in these circumstances is obligatory to decline or

suspend the professional service and if required a member in public practice is required to

quit from the assignation. In other cases, member in business is required to leave from the

employing organisation.

Meanwhile, taking into consideration the relevant factors of 100.17 to 100.22, CPA

member must determine the appropriate development of action, evaluating the significances

of each likely progression of business operations action and whether any other individuals

and those accused of governance must be referred. However, in compliance with the

fundamental principles of APES 110, Arnold should consider attaining professional

suggestions from appropriate professional entity or any recognized legal consultative further

might sometimes fail to review financial results with utmost accuracy or investments made

by the employer. Furthermore, often members tend to encounter threats owing to distant or

intimate association with client. However, drawing insights from these categories of threat,

Arnold might experience close association with any of his clients, which can further give rise

to ethical dilemma while offering current service (CPAAustralia.com.au, 2019).

Furthermore, as per the principle of APES 110 in 100.3, safeguard as actions or

measures can be seen as effective which may be eliminate risks or to some extent in

acceptable level. Arnold must take into consideration safeguard measures to avoid any type

of financial threats during his services at an acceptable threat. An acceptable level is

considered as the level where considerable as well as informed third party entity would be

likely to conclude, considering all particular facts and conditions obtainable to the associate

at that time that compliance with the important principles is not cooperated or negotiated.

However, if threats fail to be abolished or abridged to a satisfactory level as the pressures

show great degree of severity or there is lack of precautions or cannot be applied to report the

coercions, in these cases, the context or relationship producing the threats must be

circumvented. Considering Arnold’s role in these circumstances is obligatory to decline or

suspend the professional service and if required a member in public practice is required to

quit from the assignation. In other cases, member in business is required to leave from the

employing organisation.

Meanwhile, taking into consideration the relevant factors of 100.17 to 100.22, CPA

member must determine the appropriate development of action, evaluating the significances

of each likely progression of business operations action and whether any other individuals

and those accused of governance must be referred. However, in compliance with the

fundamental principles of APES 110, Arnold should consider attaining professional

suggestions from appropriate professional entity or any recognized legal consultative further

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.