Sunshine Ltd: Ethical and Governance Issues in Financial Accounting

VerifiedAdded on 2020/05/28

|9

|2519

|467

Report

AI Summary

This report analyzes the financial accounting practices of Sunshine Ltd, focusing on ethical and governance issues stemming from the general manager's request to manipulate profits. The report details the ethical breaches, particularly concerning integrity, transparency, and objectivity, and examines the accountant's role in changing depreciation methods from straight-line to sum-of-years-digit, along with the impact on financial statements. It identifies key stakeholders, including customers, shareholders, and creditors, and explores the implications of these actions under AASB116. The report concludes that the actions of both the general manager and the accountant violated core ethical principles and highlights the importance of adhering to accounting standards for accurate financial reporting and stakeholder trust.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Executive Summary

The main aim of this report is to analyze and evaluate various aspect of ethics and governance in

the actions of Sunshine Limited. The first part of the report shows the analysis of major ethical

and governance issues in the company. The second part comprises the role of the accountant in

charging deprecation. The third part of the report shows the description of major stakeholders of

the company. The last part of the report analyzes various aspect of AASB116 for changing

deprecation.

Executive Summary

The main aim of this report is to analyze and evaluate various aspect of ethics and governance in

the actions of Sunshine Limited. The first part of the report shows the analysis of major ethical

and governance issues in the company. The second part comprises the role of the accountant in

charging deprecation. The third part of the report shows the description of major stakeholders of

the company. The last part of the report analyzes various aspect of AASB116 for changing

deprecation.

2FINANCIAL ACCOUNTING

Introduction

The provided information is on the company named Sunshine Ltd and the general

manager of the company Kam Sunshine went to the accountant, Maria Mars for reduction in

profit. The major motive of Kam is to do some modification in the upcoming profit of the

company. This aspect has created an ethical dilemma on Maria Mars due to her concern for the

renewal of her contract with the company1. This has led to Maria to change the method of

depreciation from straight-line method to sum-of-year-digit method in spite of knowing the

unethical nature of this action. In this particular case, the major stakeholders are shareholders of

the company, local community, government, employees, customers, suppliers, accountant,

general manager and creditors. With the action of Maria, she has breached three major ethical

principles; they are Integrity, Transparency and Violation of Objectivity.

Ethics and Governance

Ethics and Governance is highly related with morality and they are not compelled to

anyone. In the presence of ethics and governance, the confidence of the stakeholders uses to

increase on the quality of the work of the company. Following are the major ethical and

governance related issues related with Sunshine Ltd:

Lack of Integrity and Transparency: It is the authority of the shareholders of the companies to

get information about the profitability of their investments in the company. According to the

change in the profitability of their investments in the company, they use to take decisions

whether they will keep the shares of the company or not. In order to provide satisfaction to the

shareholders, the general manager of Sunshine Ltd has taken the way to change the method of

depreciation in order to create illusion to reduce the level of profit. It shows the lack of integrity

and transparency from the side of Sunshine Ltd for the depiction of accurate financial

information to the users of financial statements2.

Breach of Objectivity: It can be observed that the general manager of Sunshine Ltd has used the

management of the company in order to be personally benefitted and the accountant of Sunshine

Ltd, Maria Mars has assisted him to achieve it. The use of different method of depreciation can

be seen in Sunshine Ltd I order to devalue the assets so that the company can become beneficial

from future benefits. Variance in the timing of depreciation can be seen as Maria has changed the

method of depreciation. It is the responsibility of the accountants to disclose accounting

information in the most truthful way to the stakeholders. For this reason, the work of Maria has

violated the principles of objectivity of accounting ethics and governance3.

1 Lo, Bernard. Resolving ethical dilemmas: a guide for clinicians. Lippincott Williams &

Wilkins, 2012.

2 Carey, Peter John, Gary S. Monroe, and Greg Shailer. "Review of Post‐CLERP 9 Australian

Auditor Independence Research." Australian Accounting Review 24.4 (2014): 370-380.

3 Han Fan, Ying, Gordon Woodbine, and Wei Cheng. "A study of Australian and Chinese

accountants’ attitudes towards independence issues and the impact on ethical judgements." Asian

Review of Accounting 21.3 (2013): 205-222.

Introduction

The provided information is on the company named Sunshine Ltd and the general

manager of the company Kam Sunshine went to the accountant, Maria Mars for reduction in

profit. The major motive of Kam is to do some modification in the upcoming profit of the

company. This aspect has created an ethical dilemma on Maria Mars due to her concern for the

renewal of her contract with the company1. This has led to Maria to change the method of

depreciation from straight-line method to sum-of-year-digit method in spite of knowing the

unethical nature of this action. In this particular case, the major stakeholders are shareholders of

the company, local community, government, employees, customers, suppliers, accountant,

general manager and creditors. With the action of Maria, she has breached three major ethical

principles; they are Integrity, Transparency and Violation of Objectivity.

Ethics and Governance

Ethics and Governance is highly related with morality and they are not compelled to

anyone. In the presence of ethics and governance, the confidence of the stakeholders uses to

increase on the quality of the work of the company. Following are the major ethical and

governance related issues related with Sunshine Ltd:

Lack of Integrity and Transparency: It is the authority of the shareholders of the companies to

get information about the profitability of their investments in the company. According to the

change in the profitability of their investments in the company, they use to take decisions

whether they will keep the shares of the company or not. In order to provide satisfaction to the

shareholders, the general manager of Sunshine Ltd has taken the way to change the method of

depreciation in order to create illusion to reduce the level of profit. It shows the lack of integrity

and transparency from the side of Sunshine Ltd for the depiction of accurate financial

information to the users of financial statements2.

Breach of Objectivity: It can be observed that the general manager of Sunshine Ltd has used the

management of the company in order to be personally benefitted and the accountant of Sunshine

Ltd, Maria Mars has assisted him to achieve it. The use of different method of depreciation can

be seen in Sunshine Ltd I order to devalue the assets so that the company can become beneficial

from future benefits. Variance in the timing of depreciation can be seen as Maria has changed the

method of depreciation. It is the responsibility of the accountants to disclose accounting

information in the most truthful way to the stakeholders. For this reason, the work of Maria has

violated the principles of objectivity of accounting ethics and governance3.

1 Lo, Bernard. Resolving ethical dilemmas: a guide for clinicians. Lippincott Williams &

Wilkins, 2012.

2 Carey, Peter John, Gary S. Monroe, and Greg Shailer. "Review of Post‐CLERP 9 Australian

Auditor Independence Research." Australian Accounting Review 24.4 (2014): 370-380.

3 Han Fan, Ying, Gordon Woodbine, and Wei Cheng. "A study of Australian and Chinese

accountants’ attitudes towards independence issues and the impact on ethical judgements." Asian

Review of Accounting 21.3 (2013): 205-222.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

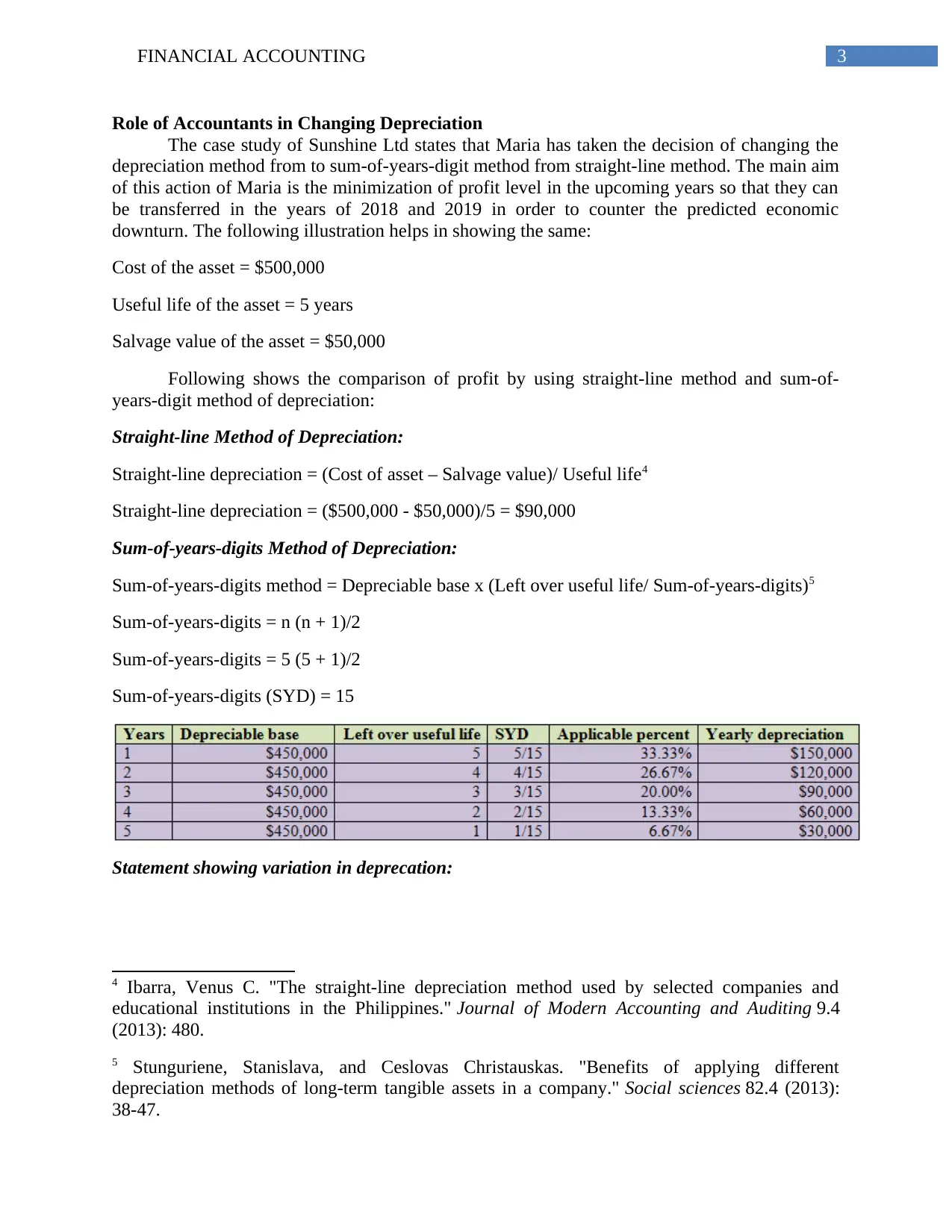

Role of Accountants in Changing Depreciation

The case study of Sunshine Ltd states that Maria has taken the decision of changing the

depreciation method from to sum-of-years-digit method from straight-line method. The main aim

of this action of Maria is the minimization of profit level in the upcoming years so that they can

be transferred in the years of 2018 and 2019 in order to counter the predicted economic

downturn. The following illustration helps in showing the same:

Cost of the asset = $500,000

Useful life of the asset = 5 years

Salvage value of the asset = $50,000

Following shows the comparison of profit by using straight-line method and sum-of-

years-digit method of depreciation:

Straight-line Method of Depreciation:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life4

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits Method of Depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-digits)5

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

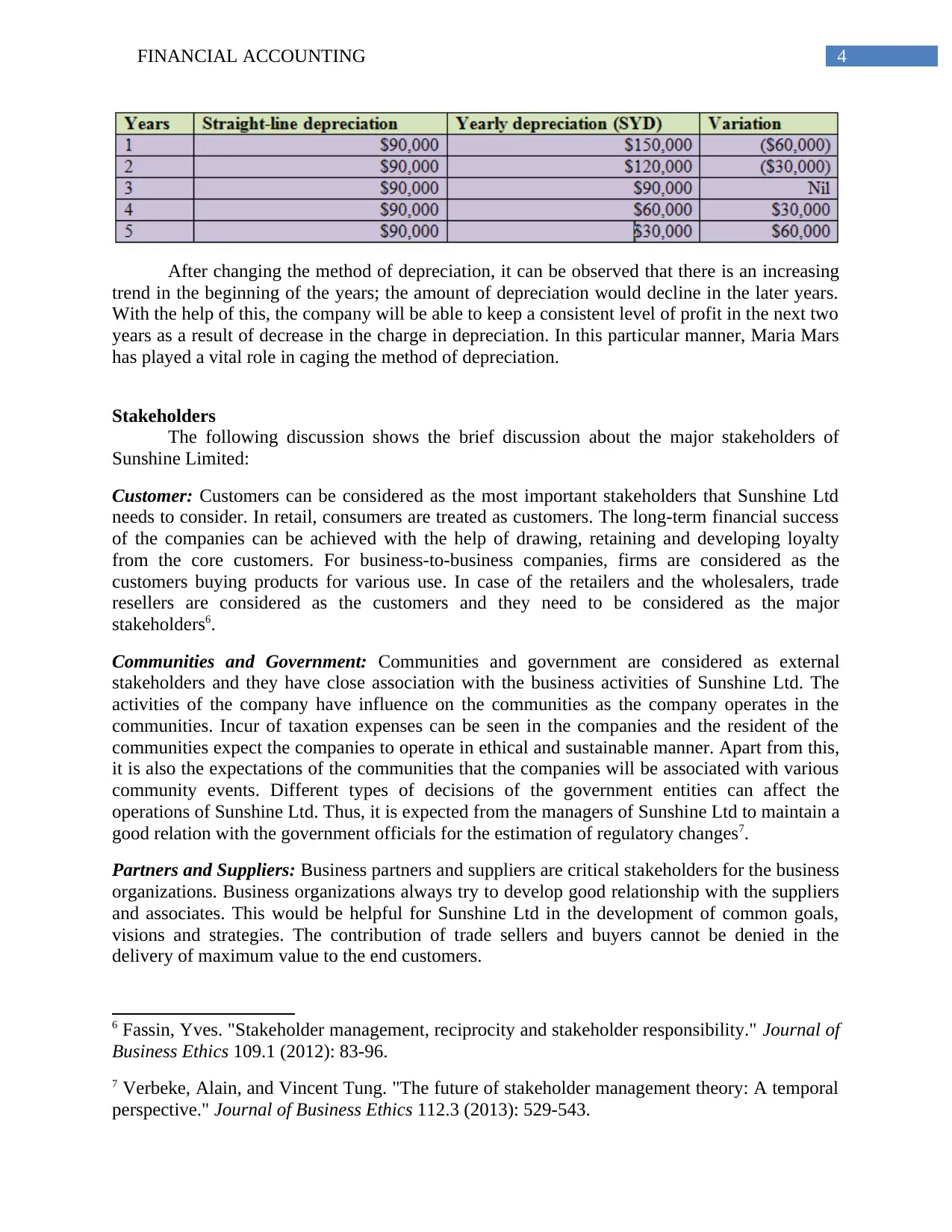

Statement showing variation in deprecation:

4 Ibarra, Venus C. "The straight-line depreciation method used by selected companies and

educational institutions in the Philippines." Journal of Modern Accounting and Auditing 9.4

(2013): 480.

5 Stunguriene, Stanislava, and Ceslovas Christauskas. "Benefits of applying different

depreciation methods of long-term tangible assets in a company." Social sciences 82.4 (2013):

38-47.

Role of Accountants in Changing Depreciation

The case study of Sunshine Ltd states that Maria has taken the decision of changing the

depreciation method from to sum-of-years-digit method from straight-line method. The main aim

of this action of Maria is the minimization of profit level in the upcoming years so that they can

be transferred in the years of 2018 and 2019 in order to counter the predicted economic

downturn. The following illustration helps in showing the same:

Cost of the asset = $500,000

Useful life of the asset = 5 years

Salvage value of the asset = $50,000

Following shows the comparison of profit by using straight-line method and sum-of-

years-digit method of depreciation:

Straight-line Method of Depreciation:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life4

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits Method of Depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-digits)5

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

Statement showing variation in deprecation:

4 Ibarra, Venus C. "The straight-line depreciation method used by selected companies and

educational institutions in the Philippines." Journal of Modern Accounting and Auditing 9.4

(2013): 480.

5 Stunguriene, Stanislava, and Ceslovas Christauskas. "Benefits of applying different

depreciation methods of long-term tangible assets in a company." Social sciences 82.4 (2013):

38-47.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

After changing the method of depreciation, it can be observed that there is an increasing

trend in the beginning of the years; the amount of depreciation would decline in the later years.

With the help of this, the company will be able to keep a consistent level of profit in the next two

years as a result of decrease in the charge in depreciation. In this particular manner, Maria Mars

has played a vital role in caging the method of depreciation.

Stakeholders

The following discussion shows the brief discussion about the major stakeholders of

Sunshine Limited:

Customer: Customers can be considered as the most important stakeholders that Sunshine Ltd

needs to consider. In retail, consumers are treated as customers. The long-term financial success

of the companies can be achieved with the help of drawing, retaining and developing loyalty

from the core customers. For business-to-business companies, firms are considered as the

customers buying products for various use. In case of the retailers and the wholesalers, trade

resellers are considered as the customers and they need to be considered as the major

stakeholders6.

Communities and Government: Communities and government are considered as external

stakeholders and they have close association with the business activities of Sunshine Ltd. The

activities of the company have influence on the communities as the company operates in the

communities. Incur of taxation expenses can be seen in the companies and the resident of the

communities expect the companies to operate in ethical and sustainable manner. Apart from this,

it is also the expectations of the communities that the companies will be associated with various

community events. Different types of decisions of the government entities can affect the

operations of Sunshine Ltd. Thus, it is expected from the managers of Sunshine Ltd to maintain a

good relation with the government officials for the estimation of regulatory changes7.

Partners and Suppliers: Business partners and suppliers are critical stakeholders for the business

organizations. Business organizations always try to develop good relationship with the suppliers

and associates. This would be helpful for Sunshine Ltd in the development of common goals,

visions and strategies. The contribution of trade sellers and buyers cannot be denied in the

delivery of maximum value to the end customers.

6 Fassin, Yves. "Stakeholder management, reciprocity and stakeholder responsibility." Journal of

Business Ethics 109.1 (2012): 83-96.

7 Verbeke, Alain, and Vincent Tung. "The future of stakeholder management theory: A temporal

perspective." Journal of Business Ethics 112.3 (2013): 529-543.

After changing the method of depreciation, it can be observed that there is an increasing

trend in the beginning of the years; the amount of depreciation would decline in the later years.

With the help of this, the company will be able to keep a consistent level of profit in the next two

years as a result of decrease in the charge in depreciation. In this particular manner, Maria Mars

has played a vital role in caging the method of depreciation.

Stakeholders

The following discussion shows the brief discussion about the major stakeholders of

Sunshine Limited:

Customer: Customers can be considered as the most important stakeholders that Sunshine Ltd

needs to consider. In retail, consumers are treated as customers. The long-term financial success

of the companies can be achieved with the help of drawing, retaining and developing loyalty

from the core customers. For business-to-business companies, firms are considered as the

customers buying products for various use. In case of the retailers and the wholesalers, trade

resellers are considered as the customers and they need to be considered as the major

stakeholders6.

Communities and Government: Communities and government are considered as external

stakeholders and they have close association with the business activities of Sunshine Ltd. The

activities of the company have influence on the communities as the company operates in the

communities. Incur of taxation expenses can be seen in the companies and the resident of the

communities expect the companies to operate in ethical and sustainable manner. Apart from this,

it is also the expectations of the communities that the companies will be associated with various

community events. Different types of decisions of the government entities can affect the

operations of Sunshine Ltd. Thus, it is expected from the managers of Sunshine Ltd to maintain a

good relation with the government officials for the estimation of regulatory changes7.

Partners and Suppliers: Business partners and suppliers are critical stakeholders for the business

organizations. Business organizations always try to develop good relationship with the suppliers

and associates. This would be helpful for Sunshine Ltd in the development of common goals,

visions and strategies. The contribution of trade sellers and buyers cannot be denied in the

delivery of maximum value to the end customers.

6 Fassin, Yves. "Stakeholder management, reciprocity and stakeholder responsibility." Journal of

Business Ethics 109.1 (2012): 83-96.

7 Verbeke, Alain, and Vincent Tung. "The future of stakeholder management theory: A temporal

perspective." Journal of Business Ethics 112.3 (2013): 529-543.

5FINANCIAL ACCOUNTING

Creditors: Many times the organizations have to use the lenders in order to fund their businesses,

purchase of assets and the purchase of supplies. It can be seen that the banks lend money to the

firms for the purchase of new buildings. Sometimes, the suppliers provide products on credit

basis and take money later. It would be the expectation of the creditors of Sunshine Ltd to make

the payments within the deadline8.

Accountant: The provided case study of Sunshine Ltd states that Maria Mars is the accountants

of the company and has the reasonability to prepare the financial statements of the company

along with the change in profit from 2016 and 2017 to 2018 and 2019.

General Manager: As per the case study of Sunshine Ltd, Kam Sunshine is the general

managers of Sunshine Ltd and he has the responsibility to take responsible decisions for

improving the business operations of the company.

Shareholders: Shareholder are the persons investing in the equity shares of Sunshine Ltd in

order to take advantage of the profit of the company. Shareholders are considered as the major

stakeholders of the company.

Impact of AASB116

The provided case study of Sunshine Ltd states that Kam Sunshine has requested Maria

mars to find a way to minimize the profit level for 2016 and 2017 after 30 June 2015. The main

motive of this action was to get consistent amount of profit in two years in order to satisfy the

shareholders. As a result, Maria has changed the deprecation method from straight-line to sum-

of-years-digits method and she has not disclosed this change in depreciation in the notes of

financial statements.

The Australian Accounting Standard Board (AASB) 116 is related with the valuation of

property, plant and equipment and it can be applied for the reporting of mentioned assets starting

on or after 1 July 2009. The main international of AASB116 is to demand for the accounting

treatment of property, plant and equipment in order to provide this information to the readers of

financial statements related to the company’s investment on these kinds of assets and the

investment modification. The major accounting issue related with the calculation of property,

plant and equipment are the realization of the assets, determination of the carrying value of the

assets, process of modification of depreciation and the determination of impairment profits and

losses9.

In case of Sunshine Ltd, Maria Mars has changed the deprecation process from straight-

line to sum-of-years-digit method. In this case, the main idea related with deprecation is the

distribution of the value of assets over the useful lives of the assets. It has been observed that the

business organizations use to determine depreciation on their fixed assets and non-current asset

for both tax and accounting purposes. The impact of former can be seen on the reported net

8 Minoja, Mario. "Stakeholder management theory, firm strategy, and ambidexterity." Journal of

Business Ethics 109.1 (2012): 67-82.

9 Yao, Dai Fei Troy, Majella Percy, and Fang Hu. "Fair value accounting for non-current assets

and audit fees: Evidence from Australian companies." Journal of Contemporary Accounting &

Economics 11.1 (2015): 31-45.

Creditors: Many times the organizations have to use the lenders in order to fund their businesses,

purchase of assets and the purchase of supplies. It can be seen that the banks lend money to the

firms for the purchase of new buildings. Sometimes, the suppliers provide products on credit

basis and take money later. It would be the expectation of the creditors of Sunshine Ltd to make

the payments within the deadline8.

Accountant: The provided case study of Sunshine Ltd states that Maria Mars is the accountants

of the company and has the reasonability to prepare the financial statements of the company

along with the change in profit from 2016 and 2017 to 2018 and 2019.

General Manager: As per the case study of Sunshine Ltd, Kam Sunshine is the general

managers of Sunshine Ltd and he has the responsibility to take responsible decisions for

improving the business operations of the company.

Shareholders: Shareholder are the persons investing in the equity shares of Sunshine Ltd in

order to take advantage of the profit of the company. Shareholders are considered as the major

stakeholders of the company.

Impact of AASB116

The provided case study of Sunshine Ltd states that Kam Sunshine has requested Maria

mars to find a way to minimize the profit level for 2016 and 2017 after 30 June 2015. The main

motive of this action was to get consistent amount of profit in two years in order to satisfy the

shareholders. As a result, Maria has changed the deprecation method from straight-line to sum-

of-years-digits method and she has not disclosed this change in depreciation in the notes of

financial statements.

The Australian Accounting Standard Board (AASB) 116 is related with the valuation of

property, plant and equipment and it can be applied for the reporting of mentioned assets starting

on or after 1 July 2009. The main international of AASB116 is to demand for the accounting

treatment of property, plant and equipment in order to provide this information to the readers of

financial statements related to the company’s investment on these kinds of assets and the

investment modification. The major accounting issue related with the calculation of property,

plant and equipment are the realization of the assets, determination of the carrying value of the

assets, process of modification of depreciation and the determination of impairment profits and

losses9.

In case of Sunshine Ltd, Maria Mars has changed the deprecation process from straight-

line to sum-of-years-digit method. In this case, the main idea related with deprecation is the

distribution of the value of assets over the useful lives of the assets. It has been observed that the

business organizations use to determine depreciation on their fixed assets and non-current asset

for both tax and accounting purposes. The impact of former can be seen on the reported net

8 Minoja, Mario. "Stakeholder management theory, firm strategy, and ambidexterity." Journal of

Business Ethics 109.1 (2012): 67-82.

9 Yao, Dai Fei Troy, Majella Percy, and Fang Hu. "Fair value accounting for non-current assets

and audit fees: Evidence from Australian companies." Journal of Contemporary Accounting &

Economics 11.1 (2015): 31-45.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

income of the companies while the effects of the latter can be seen on the statement of balance

sheet of the companies. Initially, the apportionment of the cost is done in depreciation expenses

form among the asset utilization period10.

Companies use to realize this expense for the purpose of tax and financial reporting.

Divergence can be noticed in the method of depreciation and the years of depreciation between

the kind of asset in the identical businesses along with different tax purposes. Due to the

presence of various standards and laws, variation among them can be seen from country to

country. Different types of methods can be seen for the calculation of deprecation; they are

straight-line method, diminishing balance method, sum-of-years-digit method and others.

The sum-of-years-digit technique for depreciation is considered as an accelerated

technique for the determination of depreciation of the assets. The formula used under sum-of-

years-digit method of deprecation is shown below:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits method)

This method has been developed in order to reflect the consumption pattern of the

fundamental assets. Moreover, in the absence any kind of pattern for the utilization of the asset,

this particular technique of deprecation is used. The uniform change in the cost of asset over the

useful lives can be seen under the straight-line depreciation method. Effective use of this method

can be seen where aim is to realize the value of assets uniformly in the lifetime. The formula of

this is shown below:

Depreciation per year = (Cost – Residual value)/ Useful life

In Sunshine Ltd, it is the responsibility of the management to take decisions for their

business operations. In this context, Kam Sunshine breached the rule of the company by taking

his decisions that has direct effect on the financial statements of the company. In addition, in the

change of depreciation method, the consent of all the shareholders is required. Hence, it can be

observed that Maria Mars has not complied with the requirements of AASB116.

Conclusion

The above discussion shows that the actions of Kam Sunshine and Maria Mars have

violated the major ethical principles of accounting that are transparency, integrity and

subjectivity. It can also be seen that that the accountant of Sunshine Ltd, Maria Mars has

changed the depreciation method from straight-line to sum-of-years-digit method out of the fear

of the not renewal of contract. This particular aspect can affect the financial statements of the

company along with their major stakeholders. As per the above discussion, the major

stakeholders of Sunshine Ltd are creditors, employees, customers, community and government,

shareholders and others. The above discussion also shows the fact that Maria Mars has not

complied with the standards of AASB116 at the time of charging deprecation on the fixed assets.

10 Hodgson, Allan, and Mark Russell. "Comprehending comprehensive income." Australian

Accounting Review 24.2 (2014): 100-110.

income of the companies while the effects of the latter can be seen on the statement of balance

sheet of the companies. Initially, the apportionment of the cost is done in depreciation expenses

form among the asset utilization period10.

Companies use to realize this expense for the purpose of tax and financial reporting.

Divergence can be noticed in the method of depreciation and the years of depreciation between

the kind of asset in the identical businesses along with different tax purposes. Due to the

presence of various standards and laws, variation among them can be seen from country to

country. Different types of methods can be seen for the calculation of deprecation; they are

straight-line method, diminishing balance method, sum-of-years-digit method and others.

The sum-of-years-digit technique for depreciation is considered as an accelerated

technique for the determination of depreciation of the assets. The formula used under sum-of-

years-digit method of deprecation is shown below:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits method)

This method has been developed in order to reflect the consumption pattern of the

fundamental assets. Moreover, in the absence any kind of pattern for the utilization of the asset,

this particular technique of deprecation is used. The uniform change in the cost of asset over the

useful lives can be seen under the straight-line depreciation method. Effective use of this method

can be seen where aim is to realize the value of assets uniformly in the lifetime. The formula of

this is shown below:

Depreciation per year = (Cost – Residual value)/ Useful life

In Sunshine Ltd, it is the responsibility of the management to take decisions for their

business operations. In this context, Kam Sunshine breached the rule of the company by taking

his decisions that has direct effect on the financial statements of the company. In addition, in the

change of depreciation method, the consent of all the shareholders is required. Hence, it can be

observed that Maria Mars has not complied with the requirements of AASB116.

Conclusion

The above discussion shows that the actions of Kam Sunshine and Maria Mars have

violated the major ethical principles of accounting that are transparency, integrity and

subjectivity. It can also be seen that that the accountant of Sunshine Ltd, Maria Mars has

changed the depreciation method from straight-line to sum-of-years-digit method out of the fear

of the not renewal of contract. This particular aspect can affect the financial statements of the

company along with their major stakeholders. As per the above discussion, the major

stakeholders of Sunshine Ltd are creditors, employees, customers, community and government,

shareholders and others. The above discussion also shows the fact that Maria Mars has not

complied with the standards of AASB116 at the time of charging deprecation on the fixed assets.

10 Hodgson, Allan, and Mark Russell. "Comprehending comprehensive income." Australian

Accounting Review 24.2 (2014): 100-110.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

References

Carey, Peter John, Gary S. Monroe, and Greg Shailer. "Review of Post‐CLERP 9 Australian

Auditor Independence Research." Australian Accounting Review 24.4 (2014): 370-380.

Fassin, Yves. "Stakeholder management, reciprocity and stakeholder responsibility." Journal of

Business Ethics 109.1 (2012): 83-96.

Han Fan, Ying, Gordon Woodbine, and Wei Cheng. "A study of Australian and Chinese

accountants’ attitudes towards independence issues and the impact on ethical judgements." Asian

Review of Accounting 21.3 (2013): 205-222.

Hodgson, Allan, and Mark Russell. "Comprehending comprehensive income." Australian

Accounting Review 24.2 (2014): 100-110.

Ibarra, Venus C. "The straight-line depreciation method used by selected companies and

educational institutions in the Philippines." Journal of Modern Accounting and Auditing 9.4

(2013): 480.

Lo, Bernard. Resolving ethical dilemmas: a guide for clinicians. Lippincott Williams & Wilkins,

2012.

Minoja, Mario. "Stakeholder management theory, firm strategy, and ambidexterity." Journal of

Business Ethics 109.1 (2012): 67-82.

Stunguriene, Stanislava, and Ceslovas Christauskas. "Benefits of applying different depreciation

methods of long-term tangible assets in a company." Social sciences 82.4 (2013): 38-47.

Verbeke, Alain, and Vincent Tung. "The future of stakeholder management theory: A temporal

perspective." Journal of Business Ethics 112.3 (2013): 529-543.

Yao, Dai Fei Troy, Majella Percy, and Fang Hu. "Fair value accounting for non-current assets

and audit fees: Evidence from Australian companies." Journal of Contemporary Accounting &

Economics 11.1 (2015): 31-45.

References

Carey, Peter John, Gary S. Monroe, and Greg Shailer. "Review of Post‐CLERP 9 Australian

Auditor Independence Research." Australian Accounting Review 24.4 (2014): 370-380.

Fassin, Yves. "Stakeholder management, reciprocity and stakeholder responsibility." Journal of

Business Ethics 109.1 (2012): 83-96.

Han Fan, Ying, Gordon Woodbine, and Wei Cheng. "A study of Australian and Chinese

accountants’ attitudes towards independence issues and the impact on ethical judgements." Asian

Review of Accounting 21.3 (2013): 205-222.

Hodgson, Allan, and Mark Russell. "Comprehending comprehensive income." Australian

Accounting Review 24.2 (2014): 100-110.

Ibarra, Venus C. "The straight-line depreciation method used by selected companies and

educational institutions in the Philippines." Journal of Modern Accounting and Auditing 9.4

(2013): 480.

Lo, Bernard. Resolving ethical dilemmas: a guide for clinicians. Lippincott Williams & Wilkins,

2012.

Minoja, Mario. "Stakeholder management theory, firm strategy, and ambidexterity." Journal of

Business Ethics 109.1 (2012): 67-82.

Stunguriene, Stanislava, and Ceslovas Christauskas. "Benefits of applying different depreciation

methods of long-term tangible assets in a company." Social sciences 82.4 (2013): 38-47.

Verbeke, Alain, and Vincent Tung. "The future of stakeholder management theory: A temporal

perspective." Journal of Business Ethics 112.3 (2013): 529-543.

Yao, Dai Fei Troy, Majella Percy, and Fang Hu. "Fair value accounting for non-current assets

and audit fees: Evidence from Australian companies." Journal of Contemporary Accounting &

Economics 11.1 (2015): 31-45.

8FINANCIAL ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.