Capstone Report: Ethics and Governance of Metrics Company

VerifiedAdded on 2023/03/17

|15

|4653

|65

Report

AI Summary

This capstone report provides a comprehensive analysis of Metrics, a non-bank financial lender, focusing on its corporate governance practices, ethical outlook, and stakeholder relationships. The report begins with an executive summary outlining the purpose and scope of the analysis, followed by an introduction detailing Metrics' corporate history, industry context, and board composition. The core of the report delves into Metrics' corporate governance, including board structure, director remuneration, and the company's adherence to corporate governance principles. A significant portion of the report examines the board's orientation through the lens of various theories, including the Agency Theory, Resource Dependency Theory, Ethical Theory, and Stakeholder-Managerial Branch Theory, concluding that Metrics aligns with the Agency Theory. The report concludes by exploring Metrics' communication and disclosures in relation to the Legitimacy Theory of corporate governance, providing insights into the company's engagement with stakeholders and its role in the community.

ETHICS AND GOVERNACE

MANAGEMENT

5/19/2019

[Type the company name]

XXXXXX

Executive Summary

MANAGEMENT

5/19/2019

[Type the company name]

XXXXXX

Executive Summary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The capstone assignment’s aim is to explain the what, why and how of the corporate governance

practices of the chosen company Metrics. The purpose of this paper is to give a detailed report of

the company’s ethical and moral outlook and determine whether the company is fulfilling its

moral obligations to society. The company’s stakeholders are the ones who decide if the

company is ethical or not. But all efforts have been made in this report to explain to the readers if

and what is the view of the company regarding its role in the community and what part it plays

for the benefit of all of its stakeholders. Our purpose here is to simply present the desired

information. No judgments have been made regarding the company’s corporate governance

practices.

The introduction of the paper is a continuation of this summary of what the purpose of this report

is. The corporate history of the company and what industry it belongs to have been explained.

The composition of its board of directors along with the ration and remuneration of directors

have also been discussed. The orientation of the board with respect to the different theories of

board orientation has been discussed. At last, an effort has been made to explain the stance of the

company regarding communication with the stakeholders and its acceptance by society.

practices of the chosen company Metrics. The purpose of this paper is to give a detailed report of

the company’s ethical and moral outlook and determine whether the company is fulfilling its

moral obligations to society. The company’s stakeholders are the ones who decide if the

company is ethical or not. But all efforts have been made in this report to explain to the readers if

and what is the view of the company regarding its role in the community and what part it plays

for the benefit of all of its stakeholders. Our purpose here is to simply present the desired

information. No judgments have been made regarding the company’s corporate governance

practices.

The introduction of the paper is a continuation of this summary of what the purpose of this report

is. The corporate history of the company and what industry it belongs to have been explained.

The composition of its board of directors along with the ration and remuneration of directors

have also been discussed. The orientation of the board with respect to the different theories of

board orientation has been discussed. At last, an effort has been made to explain the stance of the

company regarding communication with the stakeholders and its acceptance by society.

Introduction

The capstone project aims to find out the research is done and the interpretations regarding the

social and ethical outlook of the chosen company. The purpose of this report is to explain in

detail the outlook of the company and its stakeholders regarding corporate governance practices.

Our purpose is not to make judgments about the social and ethical role of the company – the

purpose is to explain the current trends and practices followed by the company regarding the

problem at hand. The company chosen is Metrics. It is a non-bank financial lender and has an

asset management division for the management of the investment portfolios of its clients. The

company manages the securities of the company with the help of one of its kind wholesale asset

management funds which are registered on the Australian Stock Exchange.

The report of the company is given below – it has been divided into four different sections. The

first section gives a detailed introduction about the company. It explains the origin of the

company, information about the industry to which the company belongs to and the recent history

and developments with regard to the company. The second part of the company report explains

the corporate governance practices at the company – the composition of the board of directors of

the company, the CEO’s and the Chairperson’s reports, and the remuneration report. The third

and the most significant part of the report explains the orientation of the board of Metrics along

with support from the different theories of board orientation. It also explains that the company

follows the Agency Theory of board orientation. The last part of the report explains the

communications and disclosures of the company with respect to the Legitimacy Theory of

corporate governance.

Metrics - Company Report

I. Introduction to the Company

The chosen company for the purpose of this report is Metrics. It is a non – banking

financial lending corporation. The company also has an asset management division

– it is engaged in the management of credit for the private sector, equity, and capital

investments, and fixed income management (“Metrics – Who We Are”, n.d.). The

company manages the high value of portfolio investments for its clients, most of

The capstone project aims to find out the research is done and the interpretations regarding the

social and ethical outlook of the chosen company. The purpose of this report is to explain in

detail the outlook of the company and its stakeholders regarding corporate governance practices.

Our purpose is not to make judgments about the social and ethical role of the company – the

purpose is to explain the current trends and practices followed by the company regarding the

problem at hand. The company chosen is Metrics. It is a non-bank financial lender and has an

asset management division for the management of the investment portfolios of its clients. The

company manages the securities of the company with the help of one of its kind wholesale asset

management funds which are registered on the Australian Stock Exchange.

The report of the company is given below – it has been divided into four different sections. The

first section gives a detailed introduction about the company. It explains the origin of the

company, information about the industry to which the company belongs to and the recent history

and developments with regard to the company. The second part of the company report explains

the corporate governance practices at the company – the composition of the board of directors of

the company, the CEO’s and the Chairperson’s reports, and the remuneration report. The third

and the most significant part of the report explains the orientation of the board of Metrics along

with support from the different theories of board orientation. It also explains that the company

follows the Agency Theory of board orientation. The last part of the report explains the

communications and disclosures of the company with respect to the Legitimacy Theory of

corporate governance.

Metrics - Company Report

I. Introduction to the Company

The chosen company for the purpose of this report is Metrics. It is a non – banking

financial lending corporation. The company also has an asset management division

– it is engaged in the management of credit for the private sector, equity, and capital

investments, and fixed income management (“Metrics – Who We Are”, n.d.). The

company manages the high value of portfolio investments for its clients, most of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which are high net-worth individuals. Along with the individuals, Metrics has a client

base in institutional investors as well.Metrics launched its first fund for the purpose of

investment in 2012. It then launched the MCP Master Income Trust (ASX: MTX)

and was successfully listed on the ASX in 2017. Its second such vehicle for

investment was listed on the ASX in 2019 – this was called the MCP Income

Opportunities Trust (ASX: MOT). While the MCP Master Income Trust focusses

on delivering monthly cash income to its clients and investors, the MCP Income

Opportunities Trust aims to give to the investors an opportunity to invest in private

credit instruments (“Metrics – Investment Agility”, n.d.). Along with these wholesale

funds, the company promises to provide credit to all corporate investors from all

industries and across all credit risk categories (“Metrics – Borrowing Power”, n.d.).

The company belongs to the financial sector in Australia and its main focus is on the

corporate and individual lending sphere as well as the management of assets and

investments for its customers. As of 2017, the fund management industry in

Australia is the largest financial and asset management industry in the Asia –

Pacific Region and included in the top ten in the world (Tang, 2017). Metrics forms a

large part of this industry. It has provided the industry with a sophisticated investor

base and with a mature market for investment. Due to the presence of Metrics, the

financial industry in Australia boasts of a one of its kind regulatory environment and

an educated labor force.

The company has had a long history associated with it. The company was one of the

first of its kind to launch two wholesale funds (as explained above). Metrics have

been confirmed as one of the major lending partners for the refinance of Origin

– an energy giant in Australia looking to refinance its operations for the purpose of

expansion. The refinance is worth A$550 Million (“Origin completes A$550 million

refinancing – Metrics increases commitment”, 2018). Also, the company, in March

2019, has been assigned as one of the prime lenders for the refinancing of Patrick,

the largest provider of container services in Australia. The refinancing amount is

worth a total sum of A$1 billion. The refinance was conducted as a bidding process

out of which the company emerged as one of the most successful bidders. Patrick,

base in institutional investors as well.Metrics launched its first fund for the purpose of

investment in 2012. It then launched the MCP Master Income Trust (ASX: MTX)

and was successfully listed on the ASX in 2017. Its second such vehicle for

investment was listed on the ASX in 2019 – this was called the MCP Income

Opportunities Trust (ASX: MOT). While the MCP Master Income Trust focusses

on delivering monthly cash income to its clients and investors, the MCP Income

Opportunities Trust aims to give to the investors an opportunity to invest in private

credit instruments (“Metrics – Investment Agility”, n.d.). Along with these wholesale

funds, the company promises to provide credit to all corporate investors from all

industries and across all credit risk categories (“Metrics – Borrowing Power”, n.d.).

The company belongs to the financial sector in Australia and its main focus is on the

corporate and individual lending sphere as well as the management of assets and

investments for its customers. As of 2017, the fund management industry in

Australia is the largest financial and asset management industry in the Asia –

Pacific Region and included in the top ten in the world (Tang, 2017). Metrics forms a

large part of this industry. It has provided the industry with a sophisticated investor

base and with a mature market for investment. Due to the presence of Metrics, the

financial industry in Australia boasts of a one of its kind regulatory environment and

an educated labor force.

The company has had a long history associated with it. The company was one of the

first of its kind to launch two wholesale funds (as explained above). Metrics have

been confirmed as one of the major lending partners for the refinance of Origin

– an energy giant in Australia looking to refinance its operations for the purpose of

expansion. The refinance is worth A$550 Million (“Origin completes A$550 million

refinancing – Metrics increases commitment”, 2018). Also, the company, in March

2019, has been assigned as one of the prime lenders for the refinancing of Patrick,

the largest provider of container services in Australia. The refinancing amount is

worth a total sum of A$1 billion. The refinance was conducted as a bidding process

out of which the company emerged as one of the most successful bidders. Patrick,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with the help of Metrics, will be benefited with a higher rate of productivity due to

this lending (“Metrics involved in A$1 billion debt refinancing for Patrick

Terminals”, 2019).

II. Corporate Governance of the Company

As per the annual reports of Metrics published in 2018 (available at the official

webpage of the Australian Stock Exchange – MXT: MCP Master Income Trust), the

following have discussed below:

The company is based on the principles of corporate governance and it follows

these with utmost sincerity. The company lays a solid foundation for its management

and oversight of all operations and aims to structure the Board of the company in

such a manner that it adds to the value of the company. The corporate governance

principles of the company include – promoting ethical and timely disclosures,

safeguarding the integrity of the financial reports, etc.

The Board of the company includes the Chairman, the Independent Directors, the

Non – Independent Directors, and the Partners. The directors of the company include

both independent and non – independent directors. Metrics has a total of 10

directors out of which 4 are currently non – independent directors whereas the

remaining act as independent directors. The ratio of independent to non – independent

directors is 6:4 or 3:2. All the directors have been a part of the company in the given

period of the annual reports of the company (except if otherwise stated in it). The

Chairperson of the Board is a Non – Independent Director.

According to the Director’s Report, the company seeks to deliver to its investors a

high quality of investment opportunities. The MCP is the primary lending fund of the

company and its basic reason for listing on the ASX is to give the investors an

opportunity to invest in a diversified portfolio. The report informs that during the last

financial accounting period, Metrics has been able to fulfill its goals and the MCP has

exceeded its original expectations of delivering good returns to its investors. Through

the management of risk, the company has been able to balance the delivery of returns

this lending (“Metrics involved in A$1 billion debt refinancing for Patrick

Terminals”, 2019).

II. Corporate Governance of the Company

As per the annual reports of Metrics published in 2018 (available at the official

webpage of the Australian Stock Exchange – MXT: MCP Master Income Trust), the

following have discussed below:

The company is based on the principles of corporate governance and it follows

these with utmost sincerity. The company lays a solid foundation for its management

and oversight of all operations and aims to structure the Board of the company in

such a manner that it adds to the value of the company. The corporate governance

principles of the company include – promoting ethical and timely disclosures,

safeguarding the integrity of the financial reports, etc.

The Board of the company includes the Chairman, the Independent Directors, the

Non – Independent Directors, and the Partners. The directors of the company include

both independent and non – independent directors. Metrics has a total of 10

directors out of which 4 are currently non – independent directors whereas the

remaining act as independent directors. The ratio of independent to non – independent

directors is 6:4 or 3:2. All the directors have been a part of the company in the given

period of the annual reports of the company (except if otherwise stated in it). The

Chairperson of the Board is a Non – Independent Director.

According to the Director’s Report, the company seeks to deliver to its investors a

high quality of investment opportunities. The MCP is the primary lending fund of the

company and its basic reason for listing on the ASX is to give the investors an

opportunity to invest in a diversified portfolio. The report informs that during the last

financial accounting period, Metrics has been able to fulfill its goals and the MCP has

exceeded its original expectations of delivering good returns to its investors. Through

the management of risk, the company has been able to balance the delivery of returns

along with investment in a number of options. There were no significant changes in

the Fund during the period.

While the remuneration payable to the directors of the company is not mentioned

in the Annual reports, the directors have declared that all requirements of the law

have been fulfilled by them while preparing the financial statements and these

represent a true and fair picture of the company’s position during the given period.

The annual report of the company provides the basic information regarding any

changes made in the financial position of the company and states that the Fund has

been managed with utmost dedication. There have not been any significant changes

in the investment procedures or the management of the wholesale funds of the

company. The fund earned an operating profit of more than A$ 21,00,000in the

previous financial year. The financial statements of the company have explained the

collective information regarding the auditor’s remuneration, the fees paid or payable

during the current and the subsequent financial year, the interests paid or payable, the

environmental regulations followed, the accounting principles followed by the

company, among all other significant things. Rest assured by the auditors KPMG

International, the statements give a true and fair picture of the financial position of

the company during the given period.

III. Board Orientation

The Orientation of the Board of a company refers to the way that it has been

composed – that means the composition of the board and the dependency on the

internal and external directors of the company. A Board of a company may be formed

of a majority independent or a majority of non – independent directors (Wang and

Dewhirst, 2010). There are various theories which have been propounded by

experts in order to determine the board orientation and the effect that this orientation

has on the shareholders, the resources and the communications strategy of the board.

The different theories which help explain the orientation of the board have been given

the Fund during the period.

While the remuneration payable to the directors of the company is not mentioned

in the Annual reports, the directors have declared that all requirements of the law

have been fulfilled by them while preparing the financial statements and these

represent a true and fair picture of the company’s position during the given period.

The annual report of the company provides the basic information regarding any

changes made in the financial position of the company and states that the Fund has

been managed with utmost dedication. There have not been any significant changes

in the investment procedures or the management of the wholesale funds of the

company. The fund earned an operating profit of more than A$ 21,00,000in the

previous financial year. The financial statements of the company have explained the

collective information regarding the auditor’s remuneration, the fees paid or payable

during the current and the subsequent financial year, the interests paid or payable, the

environmental regulations followed, the accounting principles followed by the

company, among all other significant things. Rest assured by the auditors KPMG

International, the statements give a true and fair picture of the financial position of

the company during the given period.

III. Board Orientation

The Orientation of the Board of a company refers to the way that it has been

composed – that means the composition of the board and the dependency on the

internal and external directors of the company. A Board of a company may be formed

of a majority independent or a majority of non – independent directors (Wang and

Dewhirst, 2010). There are various theories which have been propounded by

experts in order to determine the board orientation and the effect that this orientation

has on the shareholders, the resources and the communications strategy of the board.

The different theories which help explain the orientation of the board have been given

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

below so as to give way to the understanding of the board orientation of Metrics, the

company currently under discussion.

1. Agency Theory of the Board

This theory states that there is a separation between ownership and management

of the company and that the managers act as agents working on behalf of the

owners of the company. This separation of ownership and management leads to

what is known as agency costs and these agency costs can be controlled with the

help of the principles of corporate governance (Bathala and Rao, 2010). In the

formation of the Board of Directors of a company, the theory states that the

majority of directors are independent and are employed for the benefit of the

shareholders. The main motives of the shareholders are profits and dividends. The

financial statements as per this theory include the remuneration report, the

Balance Sheet and the Income Statement.

2. Resource Dependency Theory

The resource dependency theory of the firm must have control over all its external

resources if it wants to be successful. The board of the company is important in

this case as it is responsible for the management of all external resources of the

company (Hamid, 2011). As per this theory, the board composition is not that

important but the skill of the board is much more important. How easily the

directors can exert control over the board is of prime importance.

3. Ethical Theory

This theory of the orientation of the board of a company states that there should

be equal focus on all the stakeholders of the company and not just the

shareholders. The number of independent directors is more than any other

directors in order to present the needs of all stakeholders of the company. The

company gives out voluntary disclosures along with its accounting statements in

this case (Abdullah and Valentine, 2019).

4. Stakeholder-Managerial Branch Theory

This theory of corporate governance states that the board of the company is

formed in such a manner that it helps to satisfy the needs and demands of the most

powerful of the stakeholders of the company and not all. The board is formed of

company currently under discussion.

1. Agency Theory of the Board

This theory states that there is a separation between ownership and management

of the company and that the managers act as agents working on behalf of the

owners of the company. This separation of ownership and management leads to

what is known as agency costs and these agency costs can be controlled with the

help of the principles of corporate governance (Bathala and Rao, 2010). In the

formation of the Board of Directors of a company, the theory states that the

majority of directors are independent and are employed for the benefit of the

shareholders. The main motives of the shareholders are profits and dividends. The

financial statements as per this theory include the remuneration report, the

Balance Sheet and the Income Statement.

2. Resource Dependency Theory

The resource dependency theory of the firm must have control over all its external

resources if it wants to be successful. The board of the company is important in

this case as it is responsible for the management of all external resources of the

company (Hamid, 2011). As per this theory, the board composition is not that

important but the skill of the board is much more important. How easily the

directors can exert control over the board is of prime importance.

3. Ethical Theory

This theory of the orientation of the board of a company states that there should

be equal focus on all the stakeholders of the company and not just the

shareholders. The number of independent directors is more than any other

directors in order to present the needs of all stakeholders of the company. The

company gives out voluntary disclosures along with its accounting statements in

this case (Abdullah and Valentine, 2019).

4. Stakeholder-Managerial Branch Theory

This theory of corporate governance states that the board of the company is

formed in such a manner that it helps to satisfy the needs and demands of the most

powerful of the stakeholders of the company and not all. The board is formed of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximum independent directors so that the external stakeholder's needs can be

satisfied. The voluntary disclosures of the company are a must.

5. Stewardship Theory

The main focus is on the growth of the company. The directors are mostly non –

independent so that their only focus is on the maximization of profit of the

company. The disclosures include the chairperson’s report, the cash flow

statement, etc. (Flynn, 2018).

Conclusion – Agency theory is the theory which is most applicable to the

company. It has been explained below:

After having discussed the different basis of forming the board orientation,

the goal is now to understand the orientation of the company Metrics. The

company, as discussed above, has a ratio of 3:2 of independent to non –

independent directors. The annual report of the company presents the

Chairperson’s and the CEO’s reports, the cash flow statement, the income

statement, and the balance sheet. Accordingly, the theory of board orientation

that Metrics is following is Agency Theory. The company has employed the

Board of directors to act as agents on behalf of the firm and diligently carry

out the operations of the firm in such a manner that it maximizes the growth

and the profits of the company (McColgan, 2010). There is an agency

relationship between the owners of the company (The Trust Company – RE Services

Ltd.) and the managers. Also, the focus is on the maximization of returns to the

shareholders.

The annual report of the company presents the cash flow statement and the

balance sheet in order to highlight to the readers that the focus of the board

composition is on the maximization of the return to the owners of the

firm.The firm has earned a considerable profit (about A$ 21,00,000) and has

distributed the vast majority of it as returns to the shareholders (about A$

20,872,000). The agents of the firm, as stated in the annual reports, are

satisfied. The voluntary disclosures of the company are a must.

5. Stewardship Theory

The main focus is on the growth of the company. The directors are mostly non –

independent so that their only focus is on the maximization of profit of the

company. The disclosures include the chairperson’s report, the cash flow

statement, etc. (Flynn, 2018).

Conclusion – Agency theory is the theory which is most applicable to the

company. It has been explained below:

After having discussed the different basis of forming the board orientation,

the goal is now to understand the orientation of the company Metrics. The

company, as discussed above, has a ratio of 3:2 of independent to non –

independent directors. The annual report of the company presents the

Chairperson’s and the CEO’s reports, the cash flow statement, the income

statement, and the balance sheet. Accordingly, the theory of board orientation

that Metrics is following is Agency Theory. The company has employed the

Board of directors to act as agents on behalf of the firm and diligently carry

out the operations of the firm in such a manner that it maximizes the growth

and the profits of the company (McColgan, 2010). There is an agency

relationship between the owners of the company (The Trust Company – RE Services

Ltd.) and the managers. Also, the focus is on the maximization of returns to the

shareholders.

The annual report of the company presents the cash flow statement and the

balance sheet in order to highlight to the readers that the focus of the board

composition is on the maximization of the return to the owners of the

firm.The firm has earned a considerable profit (about A$ 21,00,000) and has

distributed the vast majority of it as returns to the shareholders (about A$

20,872,000). The agents of the firm, as stated in the annual reports, are

working with the main motive of investment and getting a good return on

that investment. This justifies that the Agency Theory is the most applicable one.

The annual report of Metrics states that the performance of the agents has been

and will continue to be affected by a number of factors including the performance

of investment markets, and the fund in which the investments have been made.

These motives of the board of Metrics might give rise to what is termed as the

agency costs – the costs of the managers performing the tasks on behalf of the

owners. These costs have the potential of becoming a deterrent in the way of the

growth of the company – but can be measured with the help of the corporate

governance principles (Bonazzi and Islam, 2017).

As Bathala and Rao have stated in their paper, the agency configuration of the

board is the most suitable, especially in case of financial companies as it helps to

control the costs of management of the company and can help in maximizing the

value and the return to the shareholders. Also, the company can make appropriate

disclosures in its annual reports and give a genuine commitment to the principles

of corporate governance. The only drawback of the company following this

orientation for its board is that it might lead to a conflict of interest between

the other stakeholders of the firm – the clients, the related parties, etc.

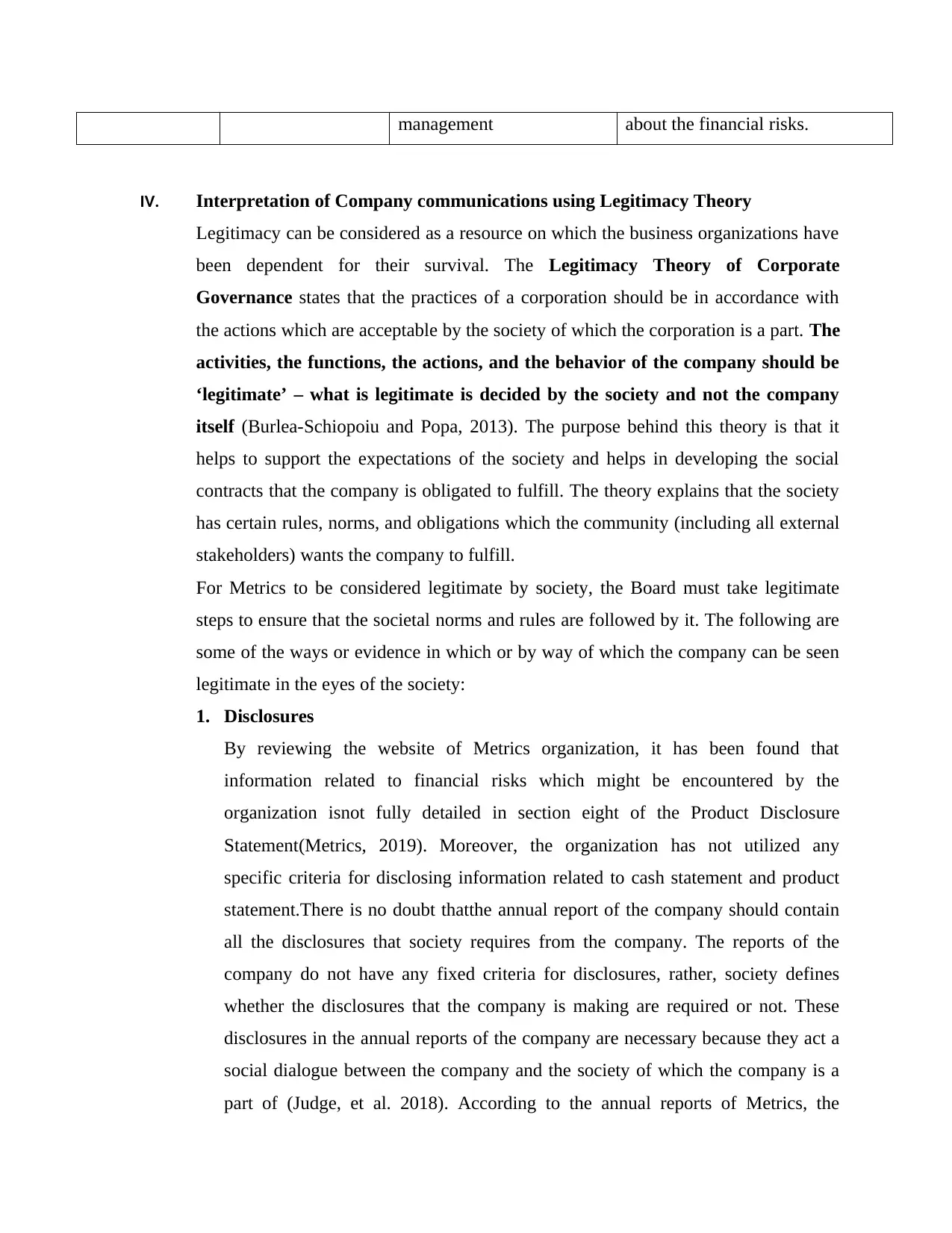

Orientation Board composition Board focus Key communications

Stakeholder –

Managerial

branch

a majority of

independent

directors

Business risks related to

investment

Livewire interview, income

statement (Metrics, 2019)

Shareholder –

Metrics

Managing

branch

Independent

partners

Low risk of capital loss and

portfolio diversification

deliver monthly cash

Details of capital raising, SMCP

income opportunities trust (ASX:

MOT), current cash income (5.8%

p.a.)(Metrics, 2019)

Resources Board has a mix of

skills

Capital management, cash

flow management, team

Product Disclosure Statement

(PDS) containing information

that investment. This justifies that the Agency Theory is the most applicable one.

The annual report of Metrics states that the performance of the agents has been

and will continue to be affected by a number of factors including the performance

of investment markets, and the fund in which the investments have been made.

These motives of the board of Metrics might give rise to what is termed as the

agency costs – the costs of the managers performing the tasks on behalf of the

owners. These costs have the potential of becoming a deterrent in the way of the

growth of the company – but can be measured with the help of the corporate

governance principles (Bonazzi and Islam, 2017).

As Bathala and Rao have stated in their paper, the agency configuration of the

board is the most suitable, especially in case of financial companies as it helps to

control the costs of management of the company and can help in maximizing the

value and the return to the shareholders. Also, the company can make appropriate

disclosures in its annual reports and give a genuine commitment to the principles

of corporate governance. The only drawback of the company following this

orientation for its board is that it might lead to a conflict of interest between

the other stakeholders of the firm – the clients, the related parties, etc.

Orientation Board composition Board focus Key communications

Stakeholder –

Managerial

branch

a majority of

independent

directors

Business risks related to

investment

Livewire interview, income

statement (Metrics, 2019)

Shareholder –

Metrics

Managing

branch

Independent

partners

Low risk of capital loss and

portfolio diversification

deliver monthly cash

Details of capital raising, SMCP

income opportunities trust (ASX:

MOT), current cash income (5.8%

p.a.)(Metrics, 2019)

Resources Board has a mix of

skills

Capital management, cash

flow management, team

Product Disclosure Statement

(PDS) containing information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management about the financial risks.

IV. Interpretation of Company communications using Legitimacy Theory

Legitimacy can be considered as a resource on which the business organizations have

been dependent for their survival. The Legitimacy Theory of Corporate

Governance states that the practices of a corporation should be in accordance with

the actions which are acceptable by the society of which the corporation is a part. The

activities, the functions, the actions, and the behavior of the company should be

‘legitimate’ – what is legitimate is decided by the society and not the company

itself (Burlea-Schiopoiu and Popa, 2013). The purpose behind this theory is that it

helps to support the expectations of the society and helps in developing the social

contracts that the company is obligated to fulfill. The theory explains that the society

has certain rules, norms, and obligations which the community (including all external

stakeholders) wants the company to fulfill.

For Metrics to be considered legitimate by society, the Board must take legitimate

steps to ensure that the societal norms and rules are followed by it. The following are

some of the ways or evidence in which or by way of which the company can be seen

legitimate in the eyes of the society:

1. Disclosures

By reviewing the website of Metrics organization, it has been found that

information related to financial risks which might be encountered by the

organization isnot fully detailed in section eight of the Product Disclosure

Statement(Metrics, 2019). Moreover, the organization has not utilized any

specific criteria for disclosing information related to cash statement and product

statement.There is no doubt thatthe annual report of the company should contain

all the disclosures that society requires from the company. The reports of the

company do not have any fixed criteria for disclosures, rather, society defines

whether the disclosures that the company is making are required or not. These

disclosures in the annual reports of the company are necessary because they act a

social dialogue between the company and the society of which the company is a

part of (Judge, et al. 2018). According to the annual reports of Metrics, the

IV. Interpretation of Company communications using Legitimacy Theory

Legitimacy can be considered as a resource on which the business organizations have

been dependent for their survival. The Legitimacy Theory of Corporate

Governance states that the practices of a corporation should be in accordance with

the actions which are acceptable by the society of which the corporation is a part. The

activities, the functions, the actions, and the behavior of the company should be

‘legitimate’ – what is legitimate is decided by the society and not the company

itself (Burlea-Schiopoiu and Popa, 2013). The purpose behind this theory is that it

helps to support the expectations of the society and helps in developing the social

contracts that the company is obligated to fulfill. The theory explains that the society

has certain rules, norms, and obligations which the community (including all external

stakeholders) wants the company to fulfill.

For Metrics to be considered legitimate by society, the Board must take legitimate

steps to ensure that the societal norms and rules are followed by it. The following are

some of the ways or evidence in which or by way of which the company can be seen

legitimate in the eyes of the society:

1. Disclosures

By reviewing the website of Metrics organization, it has been found that

information related to financial risks which might be encountered by the

organization isnot fully detailed in section eight of the Product Disclosure

Statement(Metrics, 2019). Moreover, the organization has not utilized any

specific criteria for disclosing information related to cash statement and product

statement.There is no doubt thatthe annual report of the company should contain

all the disclosures that society requires from the company. The reports of the

company do not have any fixed criteria for disclosures, rather, society defines

whether the disclosures that the company is making are required or not. These

disclosures in the annual reports of the company are necessary because they act a

social dialogue between the company and the society of which the company is a

part of (Judge, et al. 2018). According to the annual reports of Metrics, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company is making routine disclosures but it is not making sufficient disclosures

from the point of view of the society. The society does not just want the

profitability report of the company. It wants a measure of what Metrics is doing

for the benefit of society. For the successful application of the legitimacy theory,

the company should disclose the social work that it carries out for the benefit of

the community as a whole. All the stakeholders of the company should be thought

of while making disclosures in the financial statements of the company. In context

to legitimacy theory, Metrics organization should inform and educate its customer

segment (relevant public) regarding actual changes made by the organization in

its business activities and performance(Metrics, 2019). The organization has

posted very fewer posts (news) on its website about its business operations. It can

utilize its website to target its consumer segment by providing required

(important) information about its business processes.

2. Social Work

While the society expects Metrics to make disclosures of the work that it is

performing for its benefit, the company first must have something to show on its

social rooster as well (Morrison, 2014). In simple words, first the social work will

be performed, then it can be disclosed. According to the official media releases of

the company, it has been involved in the refinancing of Patrick Terminal as well

as the Origin Energy Plant. This is for the benefit of society. The question that

arises here is that is this actually sufficient? The answer is no. Metrics should first

find out its legitimacy standards i.e. what the society expects from it. It should

then focus on delivering these results(Metrics, 2019). The disclosures then follow.

Conclusion

No good report can be said to be finished without giving it a just conclusion. The company

chosen for this report is Metrics and all efforts have been made to give a report which explains

the corporate governance practices and principles of the company. For the purpose of easy

understanding of the report, it has been divided into different parts. The parts have been given

bolded heads and within the sections as well certain parts have been highlighted for the clear

from the point of view of the society. The society does not just want the

profitability report of the company. It wants a measure of what Metrics is doing

for the benefit of society. For the successful application of the legitimacy theory,

the company should disclose the social work that it carries out for the benefit of

the community as a whole. All the stakeholders of the company should be thought

of while making disclosures in the financial statements of the company. In context

to legitimacy theory, Metrics organization should inform and educate its customer

segment (relevant public) regarding actual changes made by the organization in

its business activities and performance(Metrics, 2019). The organization has

posted very fewer posts (news) on its website about its business operations. It can

utilize its website to target its consumer segment by providing required

(important) information about its business processes.

2. Social Work

While the society expects Metrics to make disclosures of the work that it is

performing for its benefit, the company first must have something to show on its

social rooster as well (Morrison, 2014). In simple words, first the social work will

be performed, then it can be disclosed. According to the official media releases of

the company, it has been involved in the refinancing of Patrick Terminal as well

as the Origin Energy Plant. This is for the benefit of society. The question that

arises here is that is this actually sufficient? The answer is no. Metrics should first

find out its legitimacy standards i.e. what the society expects from it. It should

then focus on delivering these results(Metrics, 2019). The disclosures then follow.

Conclusion

No good report can be said to be finished without giving it a just conclusion. The company

chosen for this report is Metrics and all efforts have been made to give a report which explains

the corporate governance practices and principles of the company. For the purpose of easy

understanding of the report, it has been divided into different parts. The parts have been given

bolded heads and within the sections as well certain parts have been highlighted for the clear

understanding of the readers. The report explains the company history, its industry, its corporate

governance practices (including the composition of the board, its ratio of independent to non –

independent directors, and the remuneration of the directors), its justification for the orientation

of the board in the way that it is currently, and its communication with the society in order to

fulfill the needs of the different stakeholders. Metrics’ origin and history have been explained

along with the fund – lending and management of assets’ industry that it is a part of. The

composition of the board and the ratio of its directors have also been discussed. The company

follows the Agency theory for the purpose of its board orientation. The managers act as the

agents of the owners of the company and work on its behalf. The company also makes

disclosures for the acceptance and the ‘legitimate’ stamp from the society, albeit not enough

disclosures have been made.

With this report, a sincere effort has been made so as to give a bird’s eye view of the corporate

governance practices at Metrics and interpreting the disclosure requirements of the company.

The findings of this report showed that legitimacy theory is the most applicable as compared to

other theories as it provides useful insights regarding different methods used by the chosen

organization to change views of the community about its business practices. All efforts have

been made that proper sources have been used and referenced in the report.

governance practices (including the composition of the board, its ratio of independent to non –

independent directors, and the remuneration of the directors), its justification for the orientation

of the board in the way that it is currently, and its communication with the society in order to

fulfill the needs of the different stakeholders. Metrics’ origin and history have been explained

along with the fund – lending and management of assets’ industry that it is a part of. The

composition of the board and the ratio of its directors have also been discussed. The company

follows the Agency theory for the purpose of its board orientation. The managers act as the

agents of the owners of the company and work on its behalf. The company also makes

disclosures for the acceptance and the ‘legitimate’ stamp from the society, albeit not enough

disclosures have been made.

With this report, a sincere effort has been made so as to give a bird’s eye view of the corporate

governance practices at Metrics and interpreting the disclosure requirements of the company.

The findings of this report showed that legitimacy theory is the most applicable as compared to

other theories as it provides useful insights regarding different methods used by the chosen

organization to change views of the community about its business practices. All efforts have

been made that proper sources have been used and referenced in the report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.