ETT Infrastructure Upgrade: Managerial Finance Report Analysis

VerifiedAdded on 2023/03/23

|4

|1634

|36

Report

AI Summary

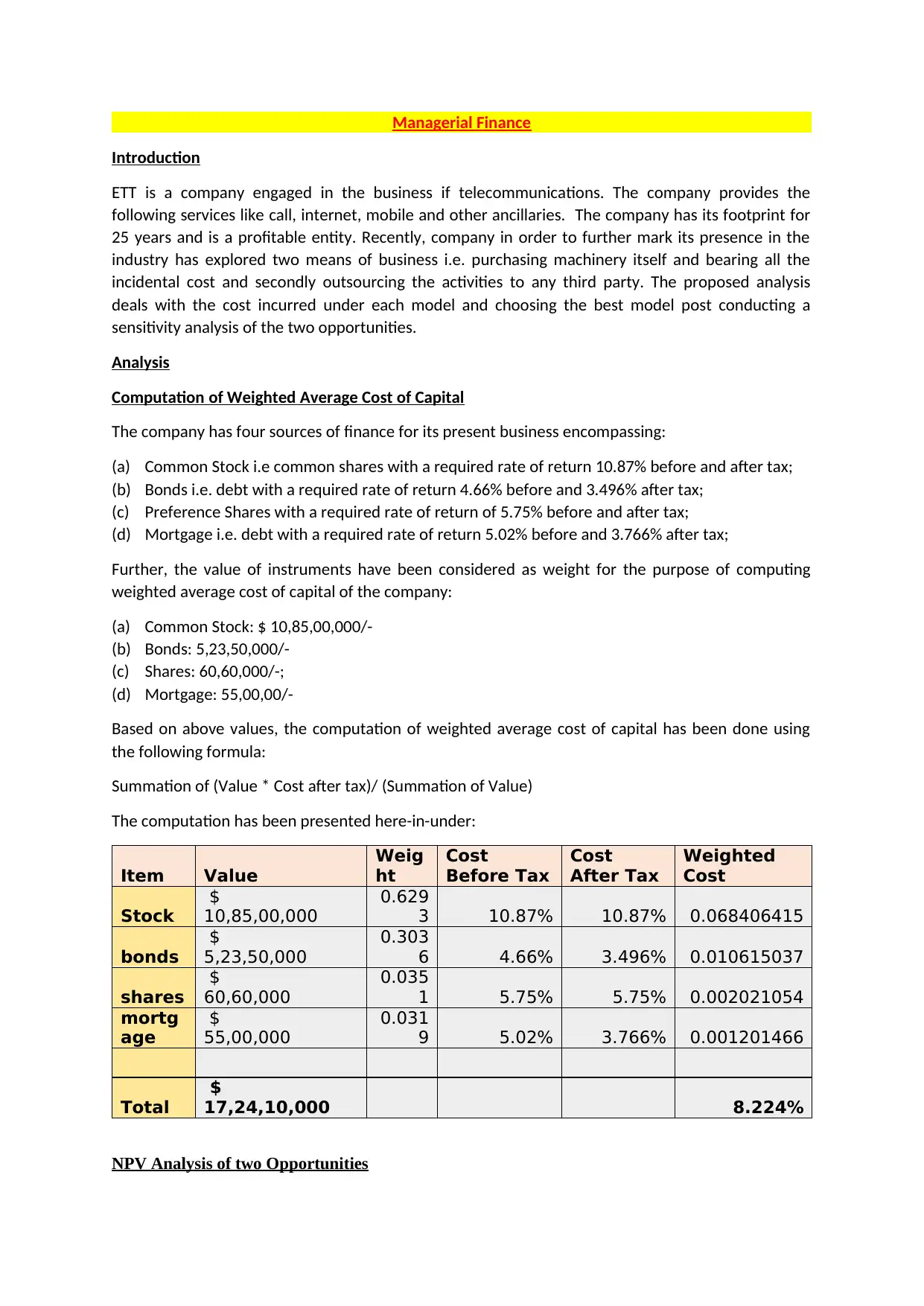

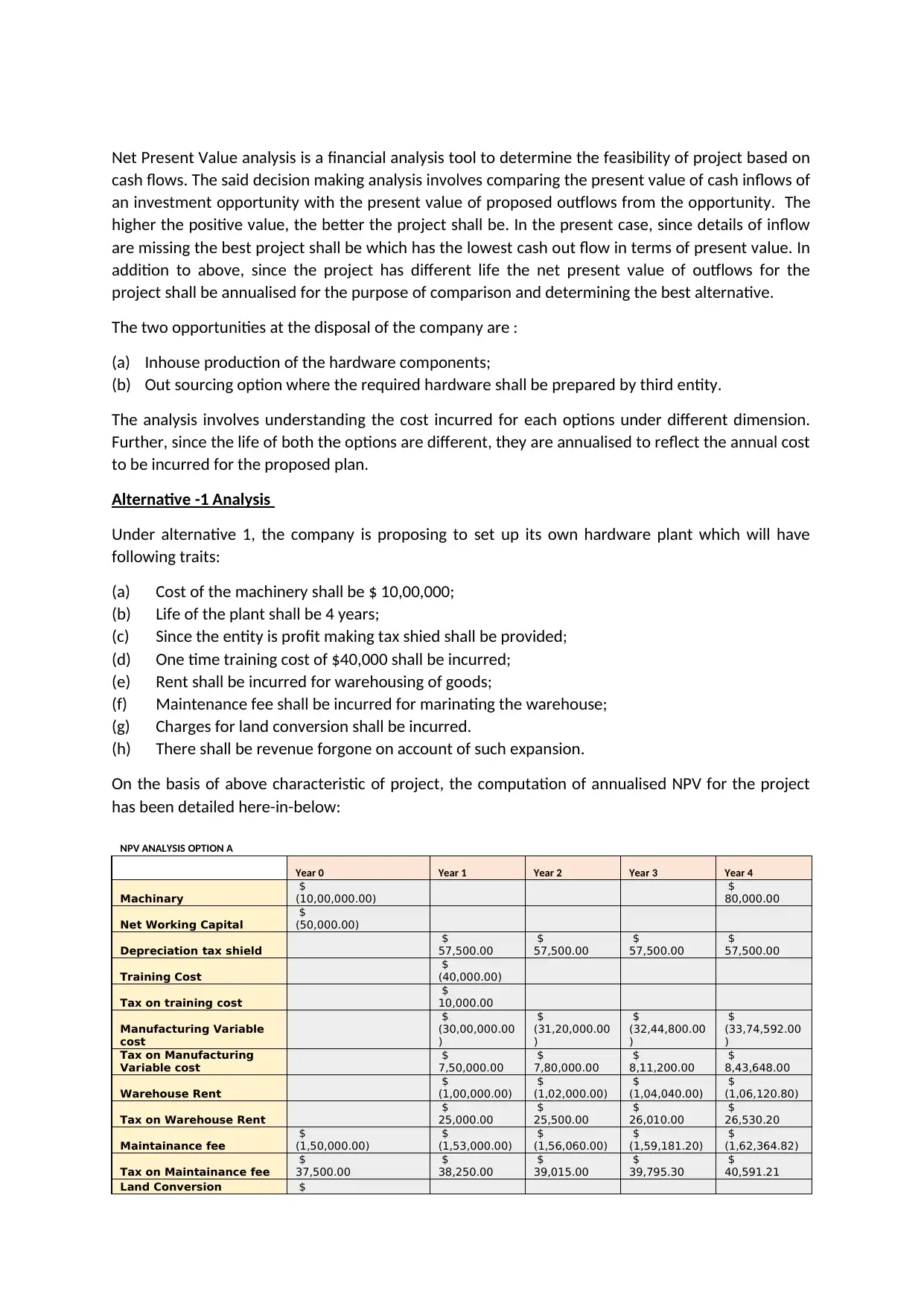

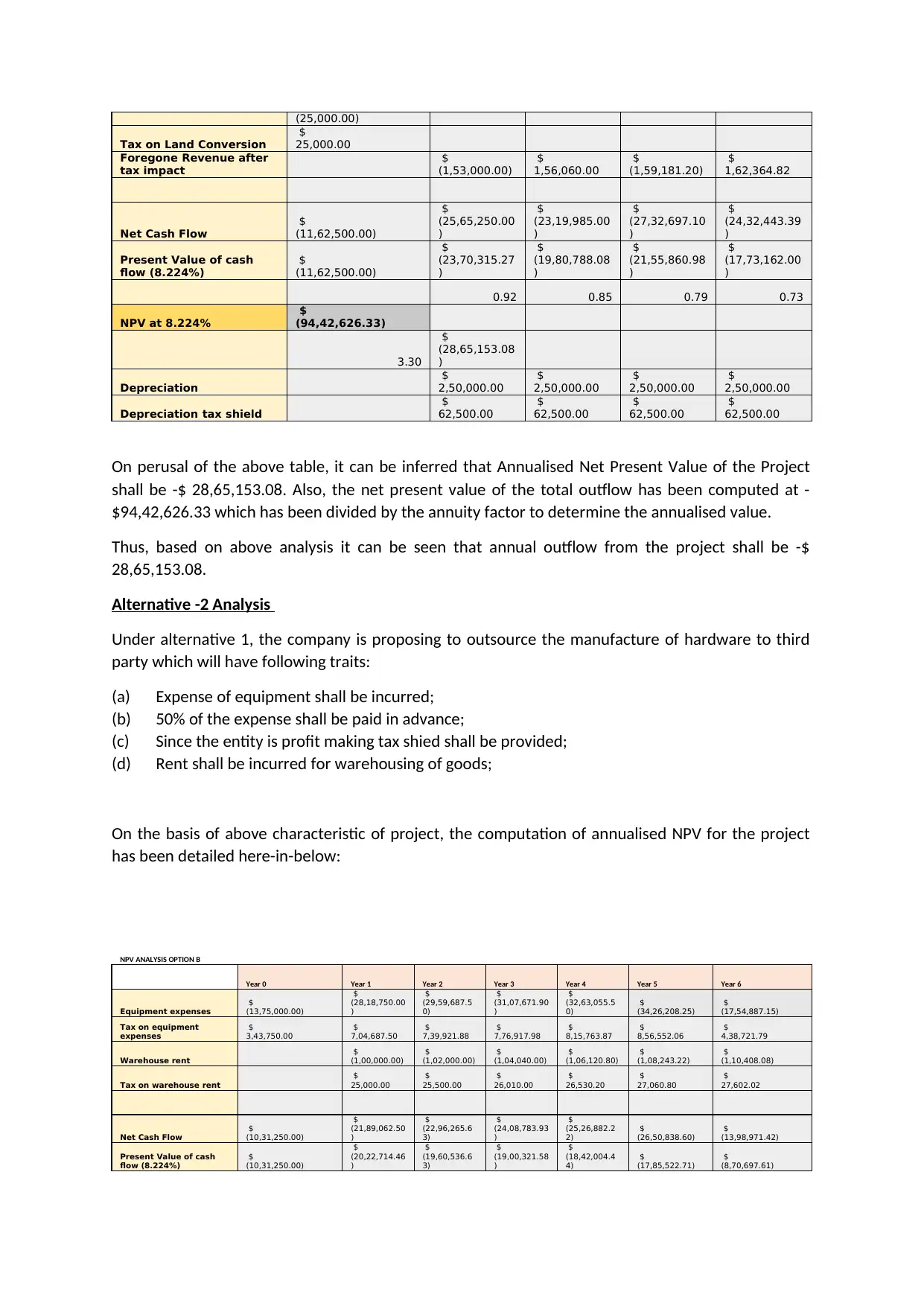

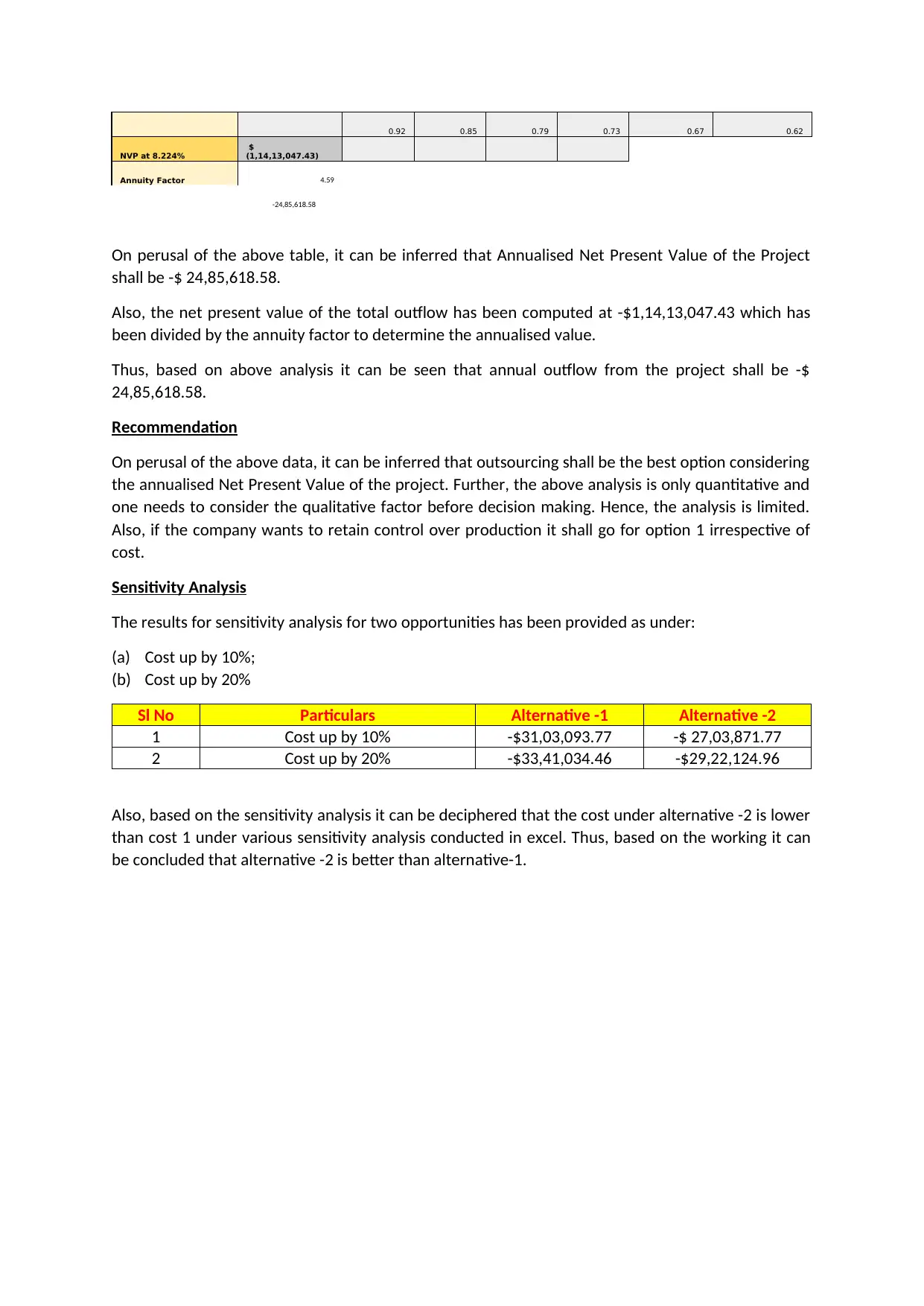

This report analyzes the financial aspects of Excellent Telecommunication Technologies Limited (ETT)'s infrastructure upgrade, comparing two options: in-house production of hardware components and outsourcing to a third party. The analysis includes the computation of ETT's Weighted Average Cost of Capital (WACC), using the values of common stock, bonds, preference shares, and mortgage. The core of the report is a Net Present Value (NPV) analysis, which evaluates the costs associated with each option over their respective lifespans, considering factors like machinery costs, training, variable costs, warehouse rent, and tax implications. Sensitivity analysis is conducted to assess the impact of cost variations on the financial outcomes. The report concludes with a recommendation based on the annualised NPV, suggesting the preferred option, and acknowledges the limitations of a purely quantitative analysis, emphasizing the importance of qualitative factors and control considerations. The analysis reveals that outsourcing appears to be the better option.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.