Tax Analysis and Corporate Accounting Report - Eureka Group Holdings

VerifiedAdded on 2020/05/16

|12

|2265

|54

Report

AI Summary

This report presents a tax analysis and corporate accounting review of Eureka Group Holdings Limited. The analysis delves into the company's equity structure, highlighting the common stock and retained earnings. It examines the company's tax obligations, revealing that Eureka Group Holdings Limited is exempt from paying taxes. The report explores the differences between accounting and tax rules, explaining why the income tax expense shown in the income statement differs from the tax rate times the computed amount. It discusses deferred tax assets and liabilities, noting that the company has no deferred tax liabilities. Furthermore, the report compares current tax expenses and payable amounts, as well as the discrepancies between income tax expenses in the income statement and income tax paid in the cash flow statement. The report concludes by reflecting on the interesting, surprising, and difficult aspects of the company's tax recording practices, offering new insights into the governance structure and the impact of tax exemptions.

RUNNING HEAD: Tax analysis and corporate accounting

1

Name of the student-

Topic- Tax analysis and corporate accounting

University name

1

Name of the student-

Topic- Tax analysis and corporate accounting

University name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax analysis and corporate accounting

2

Table of Contents

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................5

Answer to question no-3........................................................................................................................5

Answer to question no-4........................................................................................................................7

Answer to question no-5........................................................................................................................8

Answer to question no-6........................................................................................................................9

Answer to question no-7........................................................................................................................9

References...........................................................................................................................................12

.

2

Table of Contents

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................5

Answer to question no-3........................................................................................................................5

Answer to question no-4........................................................................................................................7

Answer to question no-5........................................................................................................................8

Answer to question no-6........................................................................................................................9

Answer to question no-7........................................................................................................................9

References...........................................................................................................................................12

.

Tax analysis and corporate accounting

3

This report has reflected the key understanding on Tax analysis and corporate

accounting of Eureka group holdings limited. This report has reflected the tax recording of

Eureka group holdings limited and how this recording differ in accounting and tax rules and

regulation.

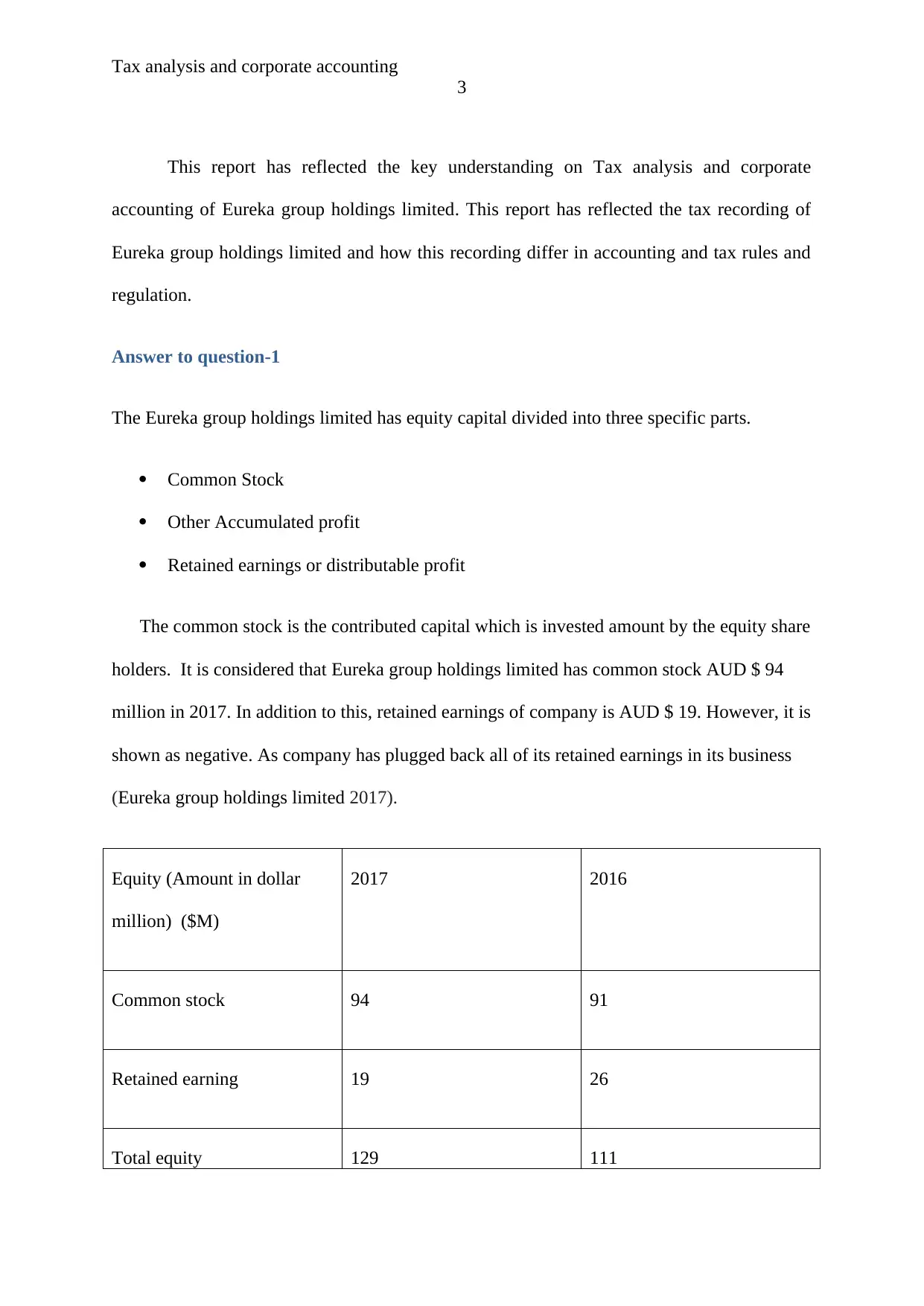

Answer to question-1

The Eureka group holdings limited has equity capital divided into three specific parts.

Common Stock

Other Accumulated profit

Retained earnings or distributable profit

The common stock is the contributed capital which is invested amount by the equity share

holders. It is considered that Eureka group holdings limited has common stock AUD $ 94

million in 2017. In addition to this, retained earnings of company is AUD $ 19. However, it is

shown as negative. As company has plugged back all of its retained earnings in its business

(Eureka group holdings limited 2017).

Equity (Amount in dollar

million) ($M)

2017 2016

Common stock 94 91

Retained earning 19 26

Total equity 129 111

3

This report has reflected the key understanding on Tax analysis and corporate

accounting of Eureka group holdings limited. This report has reflected the tax recording of

Eureka group holdings limited and how this recording differ in accounting and tax rules and

regulation.

Answer to question-1

The Eureka group holdings limited has equity capital divided into three specific parts.

Common Stock

Other Accumulated profit

Retained earnings or distributable profit

The common stock is the contributed capital which is invested amount by the equity share

holders. It is considered that Eureka group holdings limited has common stock AUD $ 94

million in 2017. In addition to this, retained earnings of company is AUD $ 19. However, it is

shown as negative. As company has plugged back all of its retained earnings in its business

(Eureka group holdings limited 2017).

Equity (Amount in dollar

million) ($M)

2017 2016

Common stock 94 91

Retained earning 19 26

Total equity 129 111

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax analysis and corporate accounting

4

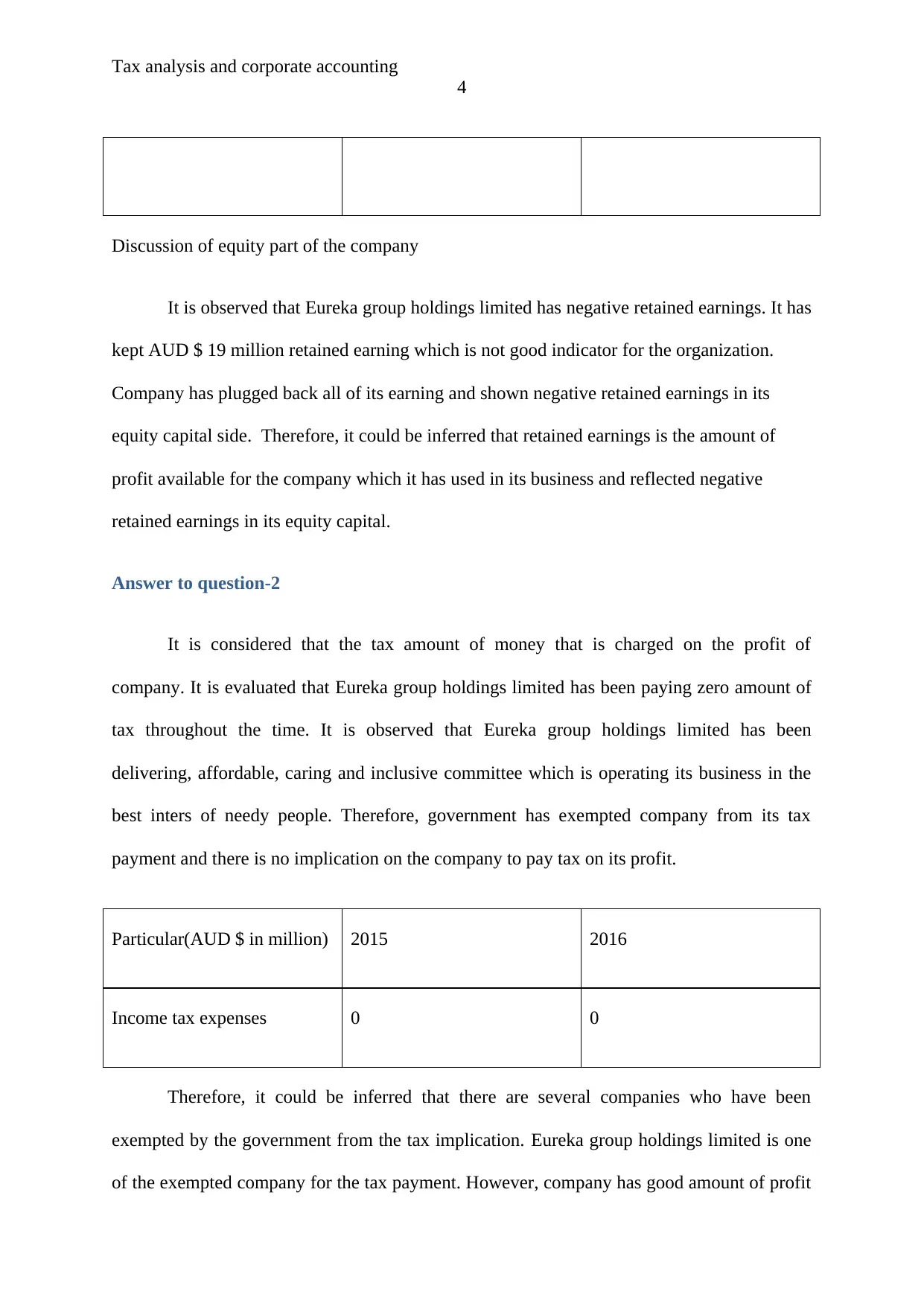

Discussion of equity part of the company

It is observed that Eureka group holdings limited has negative retained earnings. It has

kept AUD $ 19 million retained earning which is not good indicator for the organization.

Company has plugged back all of its earning and shown negative retained earnings in its

equity capital side. Therefore, it could be inferred that retained earnings is the amount of

profit available for the company which it has used in its business and reflected negative

retained earnings in its equity capital.

Answer to question-2

It is considered that the tax amount of money that is charged on the profit of

company. It is evaluated that Eureka group holdings limited has been paying zero amount of

tax throughout the time. It is observed that Eureka group holdings limited has been

delivering, affordable, caring and inclusive committee which is operating its business in the

best inters of needy people. Therefore, government has exempted company from its tax

payment and there is no implication on the company to pay tax on its profit.

Particular(AUD $ in million) 2015 2016

Income tax expenses 0 0

Therefore, it could be inferred that there are several companies who have been

exempted by the government from the tax implication. Eureka group holdings limited is one

of the exempted company for the tax payment. However, company has good amount of profit

4

Discussion of equity part of the company

It is observed that Eureka group holdings limited has negative retained earnings. It has

kept AUD $ 19 million retained earning which is not good indicator for the organization.

Company has plugged back all of its earning and shown negative retained earnings in its

equity capital side. Therefore, it could be inferred that retained earnings is the amount of

profit available for the company which it has used in its business and reflected negative

retained earnings in its equity capital.

Answer to question-2

It is considered that the tax amount of money that is charged on the profit of

company. It is evaluated that Eureka group holdings limited has been paying zero amount of

tax throughout the time. It is observed that Eureka group holdings limited has been

delivering, affordable, caring and inclusive committee which is operating its business in the

best inters of needy people. Therefore, government has exempted company from its tax

payment and there is no implication on the company to pay tax on its profit.

Particular(AUD $ in million) 2015 2016

Income tax expenses 0 0

Therefore, it could be inferred that there are several companies who have been

exempted by the government from the tax implication. Eureka group holdings limited is one

of the exempted company for the tax payment. However, company has good amount of profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax analysis and corporate accounting

5

in its business which is plugged back by company in its business operations for the

betterment of society and people at large. It has reduced the income tax burden of company in

determined approach.

Answer to question no-3

It is observed that tax expenses of Eureka group holdings limited has been shown in

the income statement as zero. Company is having zero level of tax implication due to the

exemption granted to it. The Eureka group a holding limited is wholly owned Australian

resident entity that have formed tax-consolidation group with effect from 1st July 2003. On

the other hand, company has not paid any tax in any of its financial year. However, in order

to answer the fact whether the income tax charged is equal to the tax rate times computed on

the net profit following information could be drawn. The tax rate 30% is the standard tax rate

which is determined with a view to determine the tax rate of income in determined approach.

The tax charged on the profit of company which is implicated as per the rules and

regulations of income tax.

In addition to this, tax rate times is computed by using accounting income* 30% tax

rate, i.e. 6538*30%. This amount is AUD $ 1961.4 million. Therefore, due to the difference

in accounting rules and income tax rules, tax amount shown in the income statement would

be differ from the tax rate times computed.

Explain why this

The main reason for this is based on the difference in accounting rules and income tax

rules applicable on the company.

5

in its business which is plugged back by company in its business operations for the

betterment of society and people at large. It has reduced the income tax burden of company in

determined approach.

Answer to question no-3

It is observed that tax expenses of Eureka group holdings limited has been shown in

the income statement as zero. Company is having zero level of tax implication due to the

exemption granted to it. The Eureka group a holding limited is wholly owned Australian

resident entity that have formed tax-consolidation group with effect from 1st July 2003. On

the other hand, company has not paid any tax in any of its financial year. However, in order

to answer the fact whether the income tax charged is equal to the tax rate times computed on

the net profit following information could be drawn. The tax rate 30% is the standard tax rate

which is determined with a view to determine the tax rate of income in determined approach.

The tax charged on the profit of company which is implicated as per the rules and

regulations of income tax.

In addition to this, tax rate times is computed by using accounting income* 30% tax

rate, i.e. 6538*30%. This amount is AUD $ 1961.4 million. Therefore, due to the difference

in accounting rules and income tax rules, tax amount shown in the income statement would

be differ from the tax rate times computed.

Explain why this

The main reason for this is based on the difference in accounting rules and income tax

rules applicable on the company.

Tax analysis and corporate accounting

6

The treatment of charging tax on the net profit is completely different as per the

accounting rules and income tax rules.

The tax expenses shown in the income statement is completely based on the income

tax rules and regulations. On the other hand, tax rate times is determined as per the

accounting rules and charged on the profit earned by company.

The main reasons are given as below.

The main first difference is related to recording of revenue and expenses recorded in the

profit and loss account such as recording of depreciation, bed debts and treatment of revenue

and expenses of company.

The recording of revenue and expenses shown in the financial statement differ due to the

difference between accounting and income tax rules AASB-122 (Devereux, Griffith and

Klemm, 2012).

Answer to question no-4

After evaluating the annual report of Eureka group holdings limited it is determined

that company is having zero amount of tax payment. It is considered that deferred tax is

recognized by using balance sheet method. This method is provided for temporary difference

between the carrying value of the assets and liabilities of company and amount used for

taxation purpose. For instance, if company pays higher income tax due to the difference

between accounting an income tax then it will mark the excess amount of money as deferred

tax assets in the books of account of company. On the other hand, if company paid less

amount of tax as per the taxation rules and regulations, as compared to accounting rules and

regulations then it will have to books the fewer amounts in its books of account as deferred

tax liabilities (Eureka group holdings limited 2017). The deferred tax amount is not recorded

6

The treatment of charging tax on the net profit is completely different as per the

accounting rules and income tax rules.

The tax expenses shown in the income statement is completely based on the income

tax rules and regulations. On the other hand, tax rate times is determined as per the

accounting rules and charged on the profit earned by company.

The main reasons are given as below.

The main first difference is related to recording of revenue and expenses recorded in the

profit and loss account such as recording of depreciation, bed debts and treatment of revenue

and expenses of company.

The recording of revenue and expenses shown in the financial statement differ due to the

difference between accounting and income tax rules AASB-122 (Devereux, Griffith and

Klemm, 2012).

Answer to question no-4

After evaluating the annual report of Eureka group holdings limited it is determined

that company is having zero amount of tax payment. It is considered that deferred tax is

recognized by using balance sheet method. This method is provided for temporary difference

between the carrying value of the assets and liabilities of company and amount used for

taxation purpose. For instance, if company pays higher income tax due to the difference

between accounting an income tax then it will mark the excess amount of money as deferred

tax assets in the books of account of company. On the other hand, if company paid less

amount of tax as per the taxation rules and regulations, as compared to accounting rules and

regulations then it will have to books the fewer amounts in its books of account as deferred

tax liabilities (Eureka group holdings limited 2017). The deferred tax amount is not recorded

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax analysis and corporate accounting

7

in the books account of company. It shows that company has no deferred tax liabilities in the

books of account of company which reflects that company need not to pay any amount to

government in future.

The deferred tax is not realised in the books of accounts of Eureka group holdings

limited so it is not booked in the financial statement of accounts.

Particular (AUD $ million) 2017 2016

Deferred tax assets 0 0

7

in the books account of company. It shows that company has no deferred tax liabilities in the

books of account of company which reflects that company need not to pay any amount to

government in future.

The deferred tax is not realised in the books of accounts of Eureka group holdings

limited so it is not booked in the financial statement of accounts.

Particular (AUD $ million) 2017 2016

Deferred tax assets 0 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax analysis and corporate accounting

8

Answer to question no-5

Current tax payable and current tax expenses of Eureka group holdings limited

It is evaluated that current tax is charged on the profit of Eureka group holdings

limited. However, due to the tax exemption, company has paid zero amount of tax to

government. Therefore, there is no amount of tax payable by company to government. The

current tax is charged as per the taxation rules and regulations given under AASB 112. The

current tax reflects the amount of tax charged on the profit of company in current year. On

the other hand, current tax payable is the amount of overall tax payable by company to

government. The current tax payment is shown in income statement and tax payable amount

is recorded in the liabilities side of financial statement of company (Garrett, Hoitash and

Prawitt, 2014). Therefore, it could be inferred that company has not current tax expenses nor

any tax payable. It has showcased no liabilities on company.

Deferred tax payment of Eureka group holdings limited is also zero.

Particular(AUD $ in million) 2016 2017

Income tax Expenses 0 0

Why income tax expenses is not same as the income tax payable

There are several reasons which have resulted to differences between tax expenses

and tax payable company.

8

Answer to question no-5

Current tax payable and current tax expenses of Eureka group holdings limited

It is evaluated that current tax is charged on the profit of Eureka group holdings

limited. However, due to the tax exemption, company has paid zero amount of tax to

government. Therefore, there is no amount of tax payable by company to government. The

current tax is charged as per the taxation rules and regulations given under AASB 112. The

current tax reflects the amount of tax charged on the profit of company in current year. On

the other hand, current tax payable is the amount of overall tax payable by company to

government. The current tax payment is shown in income statement and tax payable amount

is recorded in the liabilities side of financial statement of company (Garrett, Hoitash and

Prawitt, 2014). Therefore, it could be inferred that company has not current tax expenses nor

any tax payable. It has showcased no liabilities on company.

Deferred tax payment of Eureka group holdings limited is also zero.

Particular(AUD $ in million) 2016 2017

Income tax Expenses 0 0

Why income tax expenses is not same as the income tax payable

There are several reasons which have resulted to differences between tax expenses

and tax payable company.

Tax analysis and corporate accounting

9

Answer to question no-6

Is the income tax expense shown in the income statement same as the income tax paid shown

in the cash flow statement? If not

No, the income tax expenses shown in the income statement is not equal to income tax

amount shown in the cash flow statement of company.

Why are the differences?

It is evaluated that cash flow statement is accompanied with the cash inflow and

outflow from the business in particular year irrespective of the fact that whether it is related

to current year or previous year. The income tax charged on the profit of company is zero as

company is exempted from all tax payment. In addition to this, company has been paying

zero amount of tax to government. Therefore, there is zero amount of tax payment shown in

the books of account of company. Cash flow statement covers all the cash expenses of

company. On the other hand, income statement covers only the amount of tax which is

charged on the current year profit of organization. The recording of tax amount in the books

of account is done by following AASB 112 of the taxation act (Robinson, Stomberg and

Towery, 2015). Therefore, it could be inferred that company need not to worry about the tax

payment to government as it is exempted from the tax implication.

Answer to question no-7

Treatment of tax in the books of accounts of company

Interesting thing about the recorded its entire tax amount

9

Answer to question no-6

Is the income tax expense shown in the income statement same as the income tax paid shown

in the cash flow statement? If not

No, the income tax expenses shown in the income statement is not equal to income tax

amount shown in the cash flow statement of company.

Why are the differences?

It is evaluated that cash flow statement is accompanied with the cash inflow and

outflow from the business in particular year irrespective of the fact that whether it is related

to current year or previous year. The income tax charged on the profit of company is zero as

company is exempted from all tax payment. In addition to this, company has been paying

zero amount of tax to government. Therefore, there is zero amount of tax payment shown in

the books of account of company. Cash flow statement covers all the cash expenses of

company. On the other hand, income statement covers only the amount of tax which is

charged on the current year profit of organization. The recording of tax amount in the books

of account is done by following AASB 112 of the taxation act (Robinson, Stomberg and

Towery, 2015). Therefore, it could be inferred that company need not to worry about the tax

payment to government as it is exempted from the tax implication.

Answer to question no-7

Treatment of tax in the books of accounts of company

Interesting thing about the recorded its entire tax amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax analysis and corporate accounting

10

The main interesting thing about the recording of entire tax amount is based on the

recording of tax as per the accounting rules and regulations. It may results to differences

between accounting profit and profit computed by income tax rules and regulations. This

difference in amount may be recorded as deferred tax assets or deferred tax liabilities in the

financial statement of company. This is really interesting thing about the company which has

shown that company has positive recording of assets in the books of accounts

Surprising thing about the recorded its entire tax amount

The main surprising thing about the recording of entries tax amount in Eureka group

holdings limited is related to its corporate governance. Government of Australia has

exempted various companies and bodies from the tax burden. Eureka group holdings limited

is one of the selected company which is not allowed to pay tax to government. (Eureka group

holdings limited, 2017).

Difficulty in recorded the entire tax amount

Eureka group holdings limited has been exempted from the tax burden by the

government. It is evaluated that company has not paid any tax in its books of account as per

the AASB-112 income tax rules and regulations. It has increased the complexity in recording

of income tax. As per the accounting rules and regulations, company should pay tax amount

of AUD $ 1491million to government then it will increase the overall outcomes of the

organization (Eureka group holdings limited, 2017).

New insight about the company account for the income tax

The main insight about the income tax recording is related to governance structure of

company. It is evaluated that Eureka group holdings limited is falling under the exemption

10

The main interesting thing about the recording of entire tax amount is based on the

recording of tax as per the accounting rules and regulations. It may results to differences

between accounting profit and profit computed by income tax rules and regulations. This

difference in amount may be recorded as deferred tax assets or deferred tax liabilities in the

financial statement of company. This is really interesting thing about the company which has

shown that company has positive recording of assets in the books of accounts

Surprising thing about the recorded its entire tax amount

The main surprising thing about the recording of entries tax amount in Eureka group

holdings limited is related to its corporate governance. Government of Australia has

exempted various companies and bodies from the tax burden. Eureka group holdings limited

is one of the selected company which is not allowed to pay tax to government. (Eureka group

holdings limited, 2017).

Difficulty in recorded the entire tax amount

Eureka group holdings limited has been exempted from the tax burden by the

government. It is evaluated that company has not paid any tax in its books of account as per

the AASB-112 income tax rules and regulations. It has increased the complexity in recording

of income tax. As per the accounting rules and regulations, company should pay tax amount

of AUD $ 1491million to government then it will increase the overall outcomes of the

organization (Eureka group holdings limited, 2017).

New insight about the company account for the income tax

The main insight about the income tax recording is related to governance structure of

company. It is evaluated that Eureka group holdings limited is falling under the exemption

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax analysis and corporate accounting

11

list of government. It is considered that Eureka group holdings limited has paid zero amount

of tax to government due to the applicable rules and regulation of the income tax act.

However, if any case, existing rules and regulations are changed then company will have to

pay tax to government.

11

list of government. It is considered that Eureka group holdings limited has paid zero amount

of tax to government due to the applicable rules and regulation of the income tax act.

However, if any case, existing rules and regulations are changed then company will have to

pay tax to government.

Tax analysis and corporate accounting

12

References

Bauer, A.M., 2016. Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), pp.449-486.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Devereux, M.P., Griffith, R. and Klemm, A., 2012. Corporate income tax reforms and

international tax competition. Economic policy, 17(35), pp.449-495

Eureka group holdings limited, 2017, annual report, Retrieved on 21st January, 2017 from

http://investor.genworth.com.au/Investor-Centre/?page=reports-and-presentations

Feldstein, M., 2009. Tax avoidance and the deadweight loss of the income tax. The Review of

Economics and Statistics, 81(4), pp.674-680.

Garrett, J., Hoitash, R. and Prawitt, D.F., 2014. Trust and financial reporting quality. Journal

of Accounting Research, 52(5), pp.1087-1125.

Kundakchyan, R.M. and Zulfakarova, L.F., 2014. Current issues of optimal capital structure

based on forecasting financial performance of the company. Life Science Journal, 11(6s),

pp.368-371.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

12

References

Bauer, A.M., 2016. Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), pp.449-486.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Devereux, M.P., Griffith, R. and Klemm, A., 2012. Corporate income tax reforms and

international tax competition. Economic policy, 17(35), pp.449-495

Eureka group holdings limited, 2017, annual report, Retrieved on 21st January, 2017 from

http://investor.genworth.com.au/Investor-Centre/?page=reports-and-presentations

Feldstein, M., 2009. Tax avoidance and the deadweight loss of the income tax. The Review of

Economics and Statistics, 81(4), pp.674-680.

Garrett, J., Hoitash, R. and Prawitt, D.F., 2014. Trust and financial reporting quality. Journal

of Accounting Research, 52(5), pp.1087-1125.

Kundakchyan, R.M. and Zulfakarova, L.F., 2014. Current issues of optimal capital structure

based on forecasting financial performance of the company. Life Science Journal, 11(6s),

pp.368-371.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.