Finance for International Business: Euro Jet's UK Strategy

VerifiedAdded on 2020/06/05

|13

|2887

|36

Report

AI Summary

This report provides a comprehensive financial analysis of Euro Jet, an airline facing challenges due to Brexit. The report examines the airline's contingency plans, focusing on leasing aircraft and establishing a UK subsidiary. It delves into key financial aspects, including the Net Present Value (NPV) and Weighted Average Cost of Capital (WACC) calculations, assessing the profitability of the proposed investments. Furthermore, the report addresses the Foreign Exchange (FOREX) risks associated with the project, explaining relevant theories such as Balance of Payment, Interest Rate Parity, International Fisher Effect, and Purchasing Power Parity. The analysis includes data on yield rates, share prices, and corporate tax rates in both the UK and Ireland. The report concludes with recommendations on the best financial strategy for Euro Jet's expansion and offers insights into the challenges and opportunities in the international business landscape, particularly in the context of Brexit and the airline industry. This document, contributed by a student, is available on Desklib, a platform offering AI-based study tools.

Finance for International

Business

Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION..............................................................................................................1

Overview of Euro jet and its financial proposal........................................................1

Advising the board:..................................................................................................2

FOREX and its theories:..........................................................................................3

Analysing the NPV measurements for Euro jet plc..................................................5

Analysing the WACC for Euro jet UK plc.................................................................7

CONCLUSION................................................................................................................. 8

REFERENCES...............................................................................................................10

INTRODUCTION..............................................................................................................1

Overview of Euro jet and its financial proposal........................................................1

Advising the board:..................................................................................................2

FOREX and its theories:..........................................................................................3

Analysing the NPV measurements for Euro jet plc..................................................5

Analysing the WACC for Euro jet UK plc.................................................................7

CONCLUSION................................................................................................................. 8

REFERENCES...............................................................................................................10

INTRODUCTION

Euro jet is a registered airline in Ireland and is listed in Dublin Stock Exchange

and was founded in the year 1980 and is a small airline. Euro jet is having very

ambitious future growth plan for coming years and relatively it is low cost no frill

airline. The present report will be covering how this airline will be growing in the

coming year and is having the future plan of year 2028. There are number of issues

which are related to future development of the airline and this require making

decisions. After UK's decision to leave the European Union by early 2019, Euro jet is

likely to lose right to free access to UK and its aviation market.

Overview of Euro jet and its financial proposal

Euro jet is facing many problems and issues regarding the future development

of the airline and board of directors of the airline need to make certain important

decision about it (Euro Jet, 2017). This was set up in 1980 and till the time, it is the

largest European airline in terms of seat miles flown per annum and is serving about

200 destinations of EU and North Africa. The major cities which the airline is

operating in are Dublin, Milan, Brussels, Stansted and Düsseldorf. Among these

cities, Stansted is the most important as 40% of the total aeroplanes are travelling

here only. Euro jet is very low-cost and low-price airlines by attracting a larger

customer base and higher market share to firm. The service quality of Euro jet is

very good and all the rivals are wanting to defend its market share. In the year 1992,

Europe deregulated the airspace giving the airline companies right to operate in

other countries of Europe (Ilushchenko and Onashchenko, 2017). After this

deregulation of airspace in Europe, many small and low-cost airline in Europe was

set up. But none of them can give challenge or defend Euro jet in terms of low price

and good quality of services.

Euro jet was earning about 40% of its revenue from passengers of UK and

this was certainly affected by UK's decision to leave EU till mid of 2019. However,

Euro jet lost the access of free market in the UK's aviation market and this greatly

risked 40% of total revenue of the company from UK (Euro Jet, 2017). Once UK

leave EU by mid of 2019, Euro jet and its revenue would be very hardly hit by this

decision as UK can have restricted the access to market of UK. At present time, the

airline is working under the European regulation having airworthiness certificate,

aircraft maintenance schedule, aircrew licences and airline operator certificate are

1

Euro jet is a registered airline in Ireland and is listed in Dublin Stock Exchange

and was founded in the year 1980 and is a small airline. Euro jet is having very

ambitious future growth plan for coming years and relatively it is low cost no frill

airline. The present report will be covering how this airline will be growing in the

coming year and is having the future plan of year 2028. There are number of issues

which are related to future development of the airline and this require making

decisions. After UK's decision to leave the European Union by early 2019, Euro jet is

likely to lose right to free access to UK and its aviation market.

Overview of Euro jet and its financial proposal

Euro jet is facing many problems and issues regarding the future development

of the airline and board of directors of the airline need to make certain important

decision about it (Euro Jet, 2017). This was set up in 1980 and till the time, it is the

largest European airline in terms of seat miles flown per annum and is serving about

200 destinations of EU and North Africa. The major cities which the airline is

operating in are Dublin, Milan, Brussels, Stansted and Düsseldorf. Among these

cities, Stansted is the most important as 40% of the total aeroplanes are travelling

here only. Euro jet is very low-cost and low-price airlines by attracting a larger

customer base and higher market share to firm. The service quality of Euro jet is

very good and all the rivals are wanting to defend its market share. In the year 1992,

Europe deregulated the airspace giving the airline companies right to operate in

other countries of Europe (Ilushchenko and Onashchenko, 2017). After this

deregulation of airspace in Europe, many small and low-cost airline in Europe was

set up. But none of them can give challenge or defend Euro jet in terms of low price

and good quality of services.

Euro jet was earning about 40% of its revenue from passengers of UK and

this was certainly affected by UK's decision to leave EU till mid of 2019. However,

Euro jet lost the access of free market in the UK's aviation market and this greatly

risked 40% of total revenue of the company from UK (Euro Jet, 2017). Once UK

leave EU by mid of 2019, Euro jet and its revenue would be very hardly hit by this

decision as UK can have restricted the access to market of UK. At present time, the

airline is working under the European regulation having airworthiness certificate,

aircraft maintenance schedule, aircrew licences and airline operator certificate are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issued by EU only. EU also check that 50% of ownership of any airline must be with

citizen of Europe and once UK is separated from the union, it will be having its own

rules and regulation of airline operations.

To avoid all sorts of risk and uncertainty, board of Euro jet has prepared two

possible contingency plans (Agnihotri, Hu and Krush, 2016). The aim of these plans

is to secure its business in UK and to avoid the outcome of EU-UK relationship on

their business.

Contingency plan 1

According to this plan, Euro jet would be leasing out 10 Boeing 737 aircraft

and creating a mini UK airline which would be called Euro jet (UK) plc. All the rules

and regulations of this airline will be regulated by UK only (Euro Jet, 2017). The

regulations include airworthiness certificate, aircraft maintenance schedule, aircrew

licences and airline operator certificate which are presently under EU.

Contingency plan 2

If the scenario relationship between UK and EU became the worst then Euro

jet would be buying the ready-made UK airlines. This will be helping the airline in

rapidly expanding its business in UK and handling all Euro jet business in UK.

Advising the board:

From both these plans, Euro jet will be preferring the contingency plan of

leasing out Boeing 737 aircraft and creation of mini UK airline known as Euro jet

(UK) plc (O'Halloran, Robinson and Brock, 2017). Now the question in front of board

of Euro jet is whether this plan is best suited for growing business in UK or not. The

company is planning to come under the agreement to lease out 10 Boeing 737

aircraft for almost 10 years starting from 2019 to 2028. $403 million is estimated as

the fixed annual cost for each year from 2019 to 2028. This aircraft will be situated in

Stansted and at the end of 2024, Euro jet (UK) plc will be renovating all its 10 Boeing

737 aircraft at the cost of £12 million per aircraft. As per the annual cost and revenue

projection for the year 2019 which will be the first year of its operations as Euro jet

(UK) plc is estimated to £676 million (Euro Jet. 2017). The expected annual growth

after 2019 till 2028 in schedule revenues will be about 1.02%. At the starting of the

contingency plan of leasing out 10 Boeing 737 aircraft, initial establishment cost will

be about £60 million to start the business in 2019.

2

citizen of Europe and once UK is separated from the union, it will be having its own

rules and regulation of airline operations.

To avoid all sorts of risk and uncertainty, board of Euro jet has prepared two

possible contingency plans (Agnihotri, Hu and Krush, 2016). The aim of these plans

is to secure its business in UK and to avoid the outcome of EU-UK relationship on

their business.

Contingency plan 1

According to this plan, Euro jet would be leasing out 10 Boeing 737 aircraft

and creating a mini UK airline which would be called Euro jet (UK) plc. All the rules

and regulations of this airline will be regulated by UK only (Euro Jet, 2017). The

regulations include airworthiness certificate, aircraft maintenance schedule, aircrew

licences and airline operator certificate which are presently under EU.

Contingency plan 2

If the scenario relationship between UK and EU became the worst then Euro

jet would be buying the ready-made UK airlines. This will be helping the airline in

rapidly expanding its business in UK and handling all Euro jet business in UK.

Advising the board:

From both these plans, Euro jet will be preferring the contingency plan of

leasing out Boeing 737 aircraft and creation of mini UK airline known as Euro jet

(UK) plc (O'Halloran, Robinson and Brock, 2017). Now the question in front of board

of Euro jet is whether this plan is best suited for growing business in UK or not. The

company is planning to come under the agreement to lease out 10 Boeing 737

aircraft for almost 10 years starting from 2019 to 2028. $403 million is estimated as

the fixed annual cost for each year from 2019 to 2028. This aircraft will be situated in

Stansted and at the end of 2024, Euro jet (UK) plc will be renovating all its 10 Boeing

737 aircraft at the cost of £12 million per aircraft. As per the annual cost and revenue

projection for the year 2019 which will be the first year of its operations as Euro jet

(UK) plc is estimated to £676 million (Euro Jet. 2017). The expected annual growth

after 2019 till 2028 in schedule revenues will be about 1.02%. At the starting of the

contingency plan of leasing out 10 Boeing 737 aircraft, initial establishment cost will

be about £60 million to start the business in 2019.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the year 2016, Euro jet (UK) plc was set as inactive business organisation

and thereafter Euro jet will be holding 55% of shares which is offered by financial

institution of UK. The initial public offer of shares was raised to £780000 with the

share capital and sale of 156 million shares each at 0.5 pence. Euro jet (UK) plc

issued £320 million maturing in 2026 at par of 4% loan stock. And this share of Euro

jet (UK) plc is now trading at £9.68 per share and the loan stock trading value is

£100.51 on the London Stock Exchange (Zablah and Brown, 2016). The yield of the

stock of Euro jet (UK) plc at London stock exchange are:

1.6% on UK Treasury Bond,

12.5% on Corporate tax rate in Ireland,

19% on Corporate tax rate in UK, and

β by bank is around 0.947.

According to the meeting of the board of directors of Euro jet (UK) plc, the above

said proposal is very convenient and profitable for the company. The next coming

year of 2018 will be full of challenges for the company so, it must quickly decide what

should be done in reference to UK. As per the financial perspective and looking at

the upcoming year, the proposal of leasing out 10 Boeing 737 aircraft for 10 years is

regarded as the best contingency plan (Matthews, 2018). But there is some forex

risk of above said project which have been explained in next section with the help of

relevant theories and calculations.

FOREX and its theories:

Forex is the acronym which is popularly known as Foreign exchange market

or the trading or exchange of foreign currency in market. This is that type of market

which is decentralized global market and all currency of countries are traded in the

market according to set global currency (Economic theory found in Forex market,

2017). This is the best and most liquid market for currency trading where about $5

trillion is traded on an average basis. If the value of the currency in which the trader

is trading goes down then they can sell out that currency and if value in market is

been increased then it could be bought. US dollar is regarded as the base for

exchange of all currency in market and all the other country's currency are traded

according to it only. As Euro jet is about to lease out its 10 Boeing 737 aircraft for

about 10 years, there are also some forex risk which concern with the project. For

3

and thereafter Euro jet will be holding 55% of shares which is offered by financial

institution of UK. The initial public offer of shares was raised to £780000 with the

share capital and sale of 156 million shares each at 0.5 pence. Euro jet (UK) plc

issued £320 million maturing in 2026 at par of 4% loan stock. And this share of Euro

jet (UK) plc is now trading at £9.68 per share and the loan stock trading value is

£100.51 on the London Stock Exchange (Zablah and Brown, 2016). The yield of the

stock of Euro jet (UK) plc at London stock exchange are:

1.6% on UK Treasury Bond,

12.5% on Corporate tax rate in Ireland,

19% on Corporate tax rate in UK, and

β by bank is around 0.947.

According to the meeting of the board of directors of Euro jet (UK) plc, the above

said proposal is very convenient and profitable for the company. The next coming

year of 2018 will be full of challenges for the company so, it must quickly decide what

should be done in reference to UK. As per the financial perspective and looking at

the upcoming year, the proposal of leasing out 10 Boeing 737 aircraft for 10 years is

regarded as the best contingency plan (Matthews, 2018). But there is some forex

risk of above said project which have been explained in next section with the help of

relevant theories and calculations.

FOREX and its theories:

Forex is the acronym which is popularly known as Foreign exchange market

or the trading or exchange of foreign currency in market. This is that type of market

which is decentralized global market and all currency of countries are traded in the

market according to set global currency (Economic theory found in Forex market,

2017). This is the best and most liquid market for currency trading where about $5

trillion is traded on an average basis. If the value of the currency in which the trader

is trading goes down then they can sell out that currency and if value in market is

been increased then it could be bought. US dollar is regarded as the base for

exchange of all currency in market and all the other country's currency are traded

according to it only. As Euro jet is about to lease out its 10 Boeing 737 aircraft for

about 10 years, there are also some forex risk which concern with the project. For

3

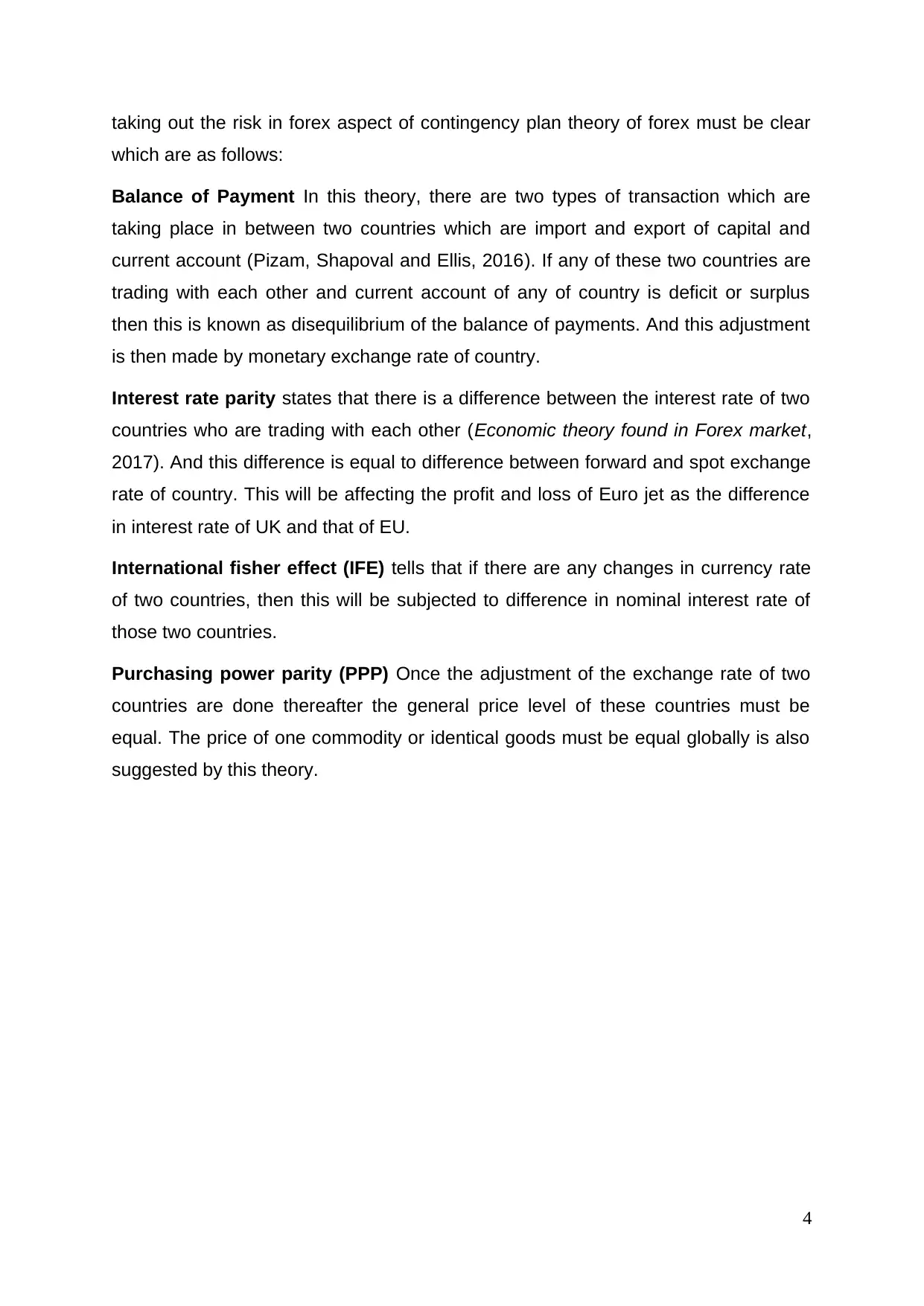

taking out the risk in forex aspect of contingency plan theory of forex must be clear

which are as follows:

Balance of Payment In this theory, there are two types of transaction which are

taking place in between two countries which are import and export of capital and

current account (Pizam, Shapoval and Ellis, 2016). If any of these two countries are

trading with each other and current account of any of country is deficit or surplus

then this is known as disequilibrium of the balance of payments. And this adjustment

is then made by monetary exchange rate of country.

Interest rate parity states that there is a difference between the interest rate of two

countries who are trading with each other (Economic theory found in Forex market,

2017). And this difference is equal to difference between forward and spot exchange

rate of country. This will be affecting the profit and loss of Euro jet as the difference

in interest rate of UK and that of EU.

International fisher effect (IFE) tells that if there are any changes in currency rate

of two countries, then this will be subjected to difference in nominal interest rate of

those two countries.

Purchasing power parity (PPP) Once the adjustment of the exchange rate of two

countries are done thereafter the general price level of these countries must be

equal. The price of one commodity or identical goods must be equal globally is also

suggested by this theory.

4

which are as follows:

Balance of Payment In this theory, there are two types of transaction which are

taking place in between two countries which are import and export of capital and

current account (Pizam, Shapoval and Ellis, 2016). If any of these two countries are

trading with each other and current account of any of country is deficit or surplus

then this is known as disequilibrium of the balance of payments. And this adjustment

is then made by monetary exchange rate of country.

Interest rate parity states that there is a difference between the interest rate of two

countries who are trading with each other (Economic theory found in Forex market,

2017). And this difference is equal to difference between forward and spot exchange

rate of country. This will be affecting the profit and loss of Euro jet as the difference

in interest rate of UK and that of EU.

International fisher effect (IFE) tells that if there are any changes in currency rate

of two countries, then this will be subjected to difference in nominal interest rate of

those two countries.

Purchasing power parity (PPP) Once the adjustment of the exchange rate of two

countries are done thereafter the general price level of these countries must be

equal. The price of one commodity or identical goods must be equal globally is also

suggested by this theory.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

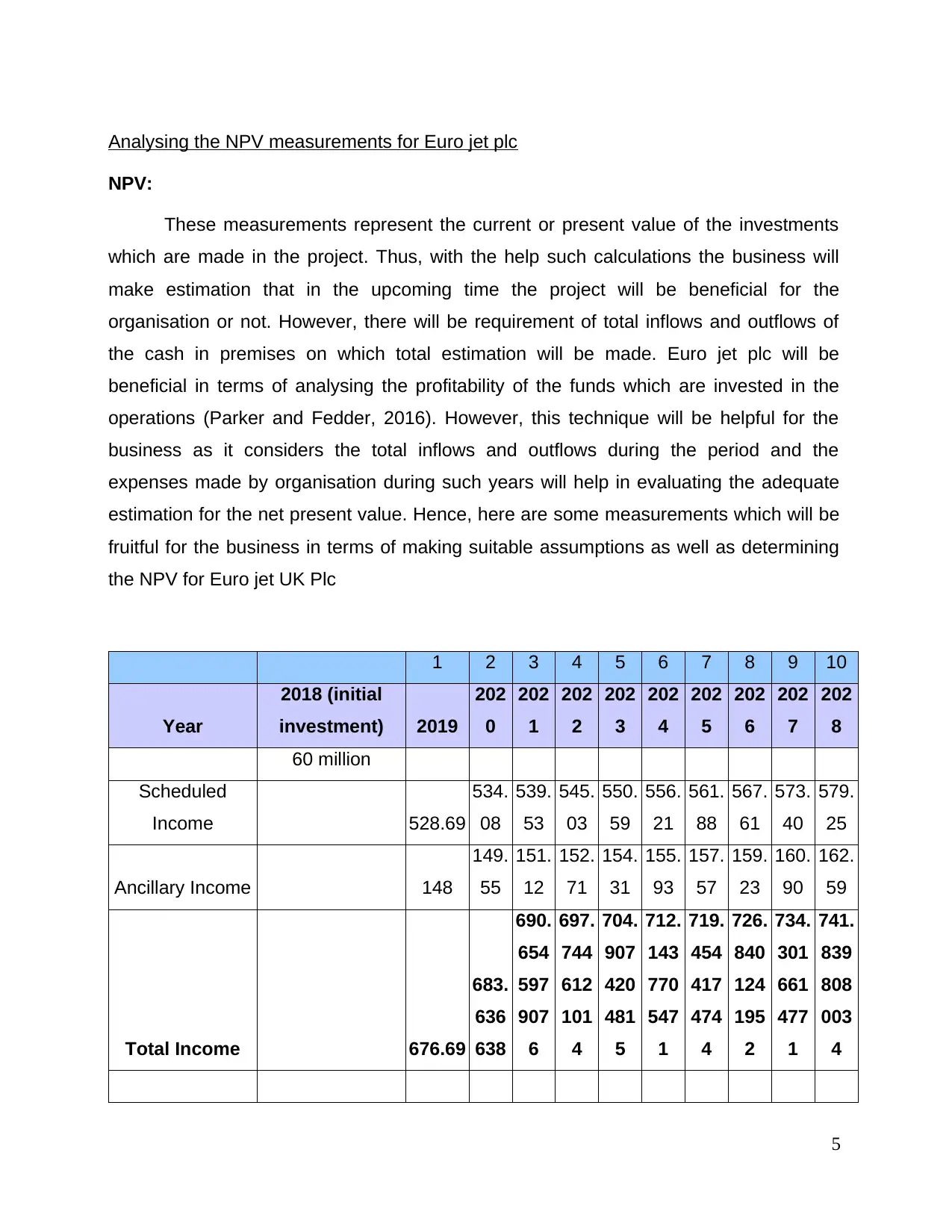

Analysing the NPV measurements for Euro jet plc

NPV:

These measurements represent the current or present value of the investments

which are made in the project. Thus, with the help such calculations the business will

make estimation that in the upcoming time the project will be beneficial for the

organisation or not. However, there will be requirement of total inflows and outflows of

the cash in premises on which total estimation will be made. Euro jet plc will be

beneficial in terms of analysing the profitability of the funds which are invested in the

operations (Parker and Fedder, 2016). However, this technique will be helpful for the

business as it considers the total inflows and outflows during the period and the

expenses made by organisation during such years will help in evaluating the adequate

estimation for the net present value. Hence, here are some measurements which will be

fruitful for the business in terms of making suitable assumptions as well as determining

the NPV for Euro jet UK Plc

1 2 3 4 5 6 7 8 9 10

Year

2018 (initial

investment) 2019

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

60 million

Scheduled

Income 528.69

534.

08

539.

53

545.

03

550.

59

556.

21

561.

88

567.

61

573.

40

579.

25

Ancillary Income 148

149.

55

151.

12

152.

71

154.

31

155.

93

157.

57

159.

23

160.

90

162.

59

Total Income 676.69

683.

636

638

690.

654

597

907

6

697.

744

612

101

4

704.

907

420

481

5

712.

143

770

547

1

719.

454

417

474

4

726.

840

124

195

2

734.

301

661

477

1

741.

839

808

003

4

5

NPV:

These measurements represent the current or present value of the investments

which are made in the project. Thus, with the help such calculations the business will

make estimation that in the upcoming time the project will be beneficial for the

organisation or not. However, there will be requirement of total inflows and outflows of

the cash in premises on which total estimation will be made. Euro jet plc will be

beneficial in terms of analysing the profitability of the funds which are invested in the

operations (Parker and Fedder, 2016). However, this technique will be helpful for the

business as it considers the total inflows and outflows during the period and the

expenses made by organisation during such years will help in evaluating the adequate

estimation for the net present value. Hence, here are some measurements which will be

fruitful for the business in terms of making suitable assumptions as well as determining

the NPV for Euro jet UK Plc

1 2 3 4 5 6 7 8 9 10

Year

2018 (initial

investment) 2019

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

60 million

Scheduled

Income 528.69

534.

08

539.

53

545.

03

550.

59

556.

21

561.

88

567.

61

573.

40

579.

25

Ancillary Income 148

149.

55

151.

12

152.

71

154.

31

155.

93

157.

57

159.

23

160.

90

162.

59

Total Income 676.69

683.

636

638

690.

654

597

907

6

697.

744

612

101

4

704.

907

420

481

5

712.

143

770

547

1

719.

454

417

474

4

726.

840

124

195

2

734.

301

661

477

1

741.

839

808

003

4

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fuel and oil 152.47

154.

07

155.

69

157.

32

158.

98

160.

64

162.

33

164.

04

165.

76

167.

50

Staff costs 35.15 35.5 37.3 39.2 41.1 43.2 45.3 47.6 50.0 52.5

Airport and

handling charges 49.37

49.8

7

50.3

8

50.9

0

51.4

2

51.9

4

52.4

7

53.0

0

53.5

5

54.0

9

Maintenance and

repairs 9.78 9.9 10.0 10.1 10.2 10.3 10.4 10.5 10.6 10.7

Marketing &

administration

costs 1 16

16.1

6

16.3

3

16.5

0

16.6

7

16.8

4

17.0

1

17.1

9

17.3

7

17.5

5

Route charges 39.2

39.6

0

40.0

0

40.4

1

40.8

2

41.2

4

41.6

6

42.0

9

42.5

2

42.9

5

Refurbishment 120

Lease cost 310 310 310 310 310 310 310 310 310 310

Total expenses 611.97

615.

101

928

619.

676

172

890

5

624.

368

256

198

8

629.

182

918

697

4

754.

125

126

243

5

639.

200

080

909

2

644.

413

232

666

2

649.

770

291

655

655.

277

241

064

3

Profit (Income -

expenses) 64.7 68.5 71.0 73.4 75.7

-

42.0 80.3 82.4 84.5 86.6

0.978

0.95

7

0.93

7

0.91

7

0.89

7

0.87

8

0.85

9

0.84

0

0.82

2

0.80

4

63.33

65.6

2

66.4

9

67.2

6

67.9

2

-

36.8

4

68.9

1

69.2

6

69.5

0

69.6

3

Total revenue 571.07

Initial investment 60

NPV 511.07

6

154.

07

155.

69

157.

32

158.

98

160.

64

162.

33

164.

04

165.

76

167.

50

Staff costs 35.15 35.5 37.3 39.2 41.1 43.2 45.3 47.6 50.0 52.5

Airport and

handling charges 49.37

49.8

7

50.3

8

50.9

0

51.4

2

51.9

4

52.4

7

53.0

0

53.5

5

54.0

9

Maintenance and

repairs 9.78 9.9 10.0 10.1 10.2 10.3 10.4 10.5 10.6 10.7

Marketing &

administration

costs 1 16

16.1

6

16.3

3

16.5

0

16.6

7

16.8

4

17.0

1

17.1

9

17.3

7

17.5

5

Route charges 39.2

39.6

0

40.0

0

40.4

1

40.8

2

41.2

4

41.6

6

42.0

9

42.5

2

42.9

5

Refurbishment 120

Lease cost 310 310 310 310 310 310 310 310 310 310

Total expenses 611.97

615.

101

928

619.

676

172

890

5

624.

368

256

198

8

629.

182

918

697

4

754.

125

126

243

5

639.

200

080

909

2

644.

413

232

666

2

649.

770

291

655

655.

277

241

064

3

Profit (Income -

expenses) 64.7 68.5 71.0 73.4 75.7

-

42.0 80.3 82.4 84.5 86.6

0.978

0.95

7

0.93

7

0.91

7

0.89

7

0.87

8

0.85

9

0.84

0

0.82

2

0.80

4

63.33

65.6

2

66.4

9

67.2

6

67.9

2

-

36.8

4

68.9

1

69.2

6

69.5

0

69.6

3

Total revenue 571.07

Initial investment 60

NPV 511.07

6

Interpretation: In consideration with the above-mentioned report, the business

will be beneficial in terms of making suitable assumption that the NPV of Euro jet is

511.07 million. Thus, it can be said that the project will be beneficial for the company in

terms of obtaining satisfactory profits. However, in the year 2018 the business has made

initial investments for 60 million which was the capital for the respective years in the

project till 2028. Thus, these 10 years of investment will be helpful for this aviation

industry in terms of attaining the adequate profits each year. Thus, the payment for

refurbishments of aircraft in the year 2024 amounted to 120 million which in turn

negatively affect the revenue gathering of the business and present the deficit balance

for -42.0 million.

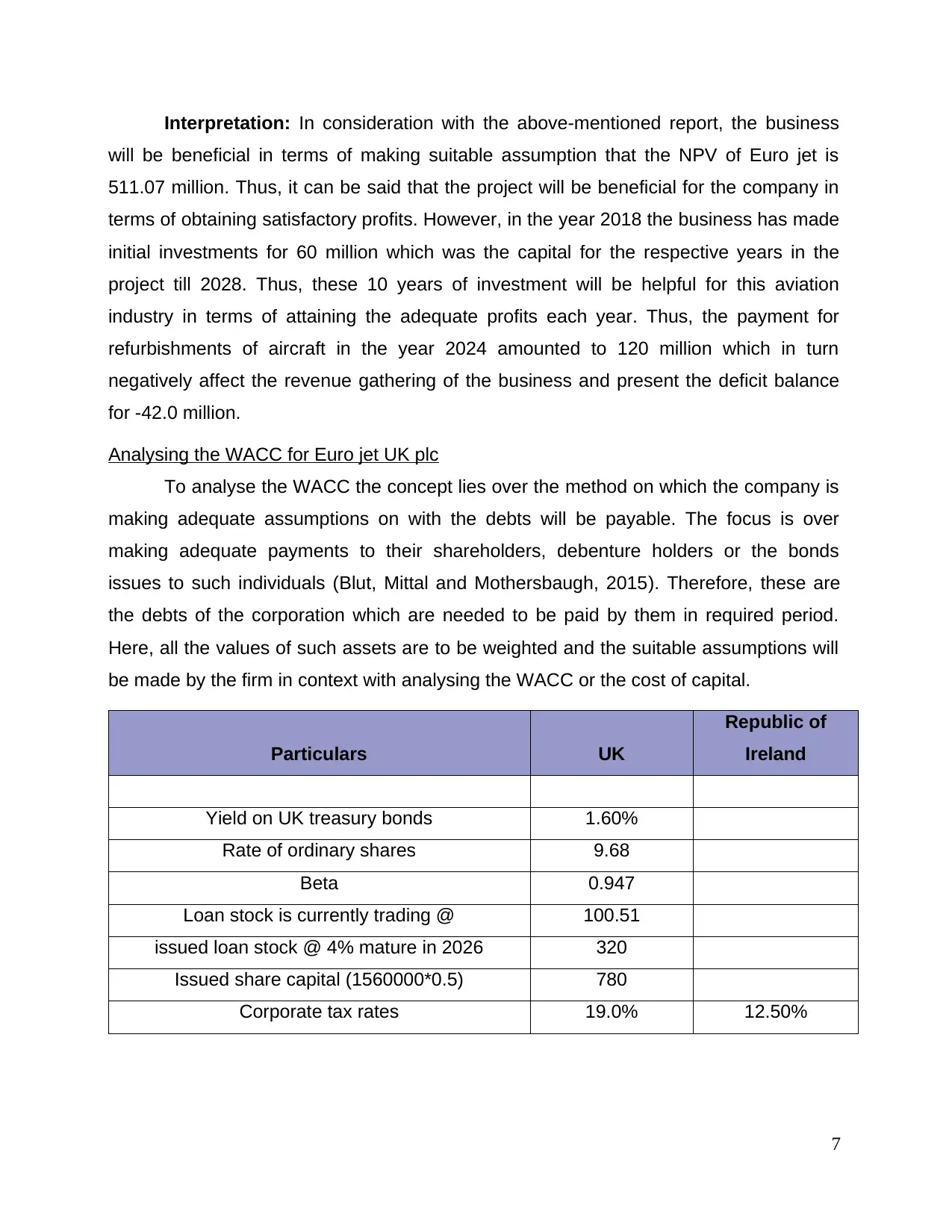

Analysing the WACC for Euro jet UK plc

To analyse the WACC the concept lies over the method on which the company is

making adequate assumptions on with the debts will be payable. The focus is over

making adequate payments to their shareholders, debenture holders or the bonds

issues to such individuals (Blut, Mittal and Mothersbaugh, 2015). Therefore, these are

the debts of the corporation which are needed to be paid by them in required period.

Here, all the values of such assets are to be weighted and the suitable assumptions will

be made by the firm in context with analysing the WACC or the cost of capital.

Particulars UK

Republic of

Ireland

Yield on UK treasury bonds 1.60%

Rate of ordinary shares 9.68

Beta 0.947

Loan stock is currently trading @ 100.51

issued loan stock @ 4% mature in 2026 320

Issued share capital (1560000*0.5) 780

Corporate tax rates 19.0% 12.50%

7

will be beneficial in terms of making suitable assumption that the NPV of Euro jet is

511.07 million. Thus, it can be said that the project will be beneficial for the company in

terms of obtaining satisfactory profits. However, in the year 2018 the business has made

initial investments for 60 million which was the capital for the respective years in the

project till 2028. Thus, these 10 years of investment will be helpful for this aviation

industry in terms of attaining the adequate profits each year. Thus, the payment for

refurbishments of aircraft in the year 2024 amounted to 120 million which in turn

negatively affect the revenue gathering of the business and present the deficit balance

for -42.0 million.

Analysing the WACC for Euro jet UK plc

To analyse the WACC the concept lies over the method on which the company is

making adequate assumptions on with the debts will be payable. The focus is over

making adequate payments to their shareholders, debenture holders or the bonds

issues to such individuals (Blut, Mittal and Mothersbaugh, 2015). Therefore, these are

the debts of the corporation which are needed to be paid by them in required period.

Here, all the values of such assets are to be weighted and the suitable assumptions will

be made by the firm in context with analysing the WACC or the cost of capital.

Particulars UK

Republic of

Ireland

Yield on UK treasury bonds 1.60%

Rate of ordinary shares 9.68

Beta 0.947

Loan stock is currently trading @ 100.51

issued loan stock @ 4% mature in 2026 320

Issued share capital (1560000*0.5) 780

Corporate tax rates 19.0% 12.50%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

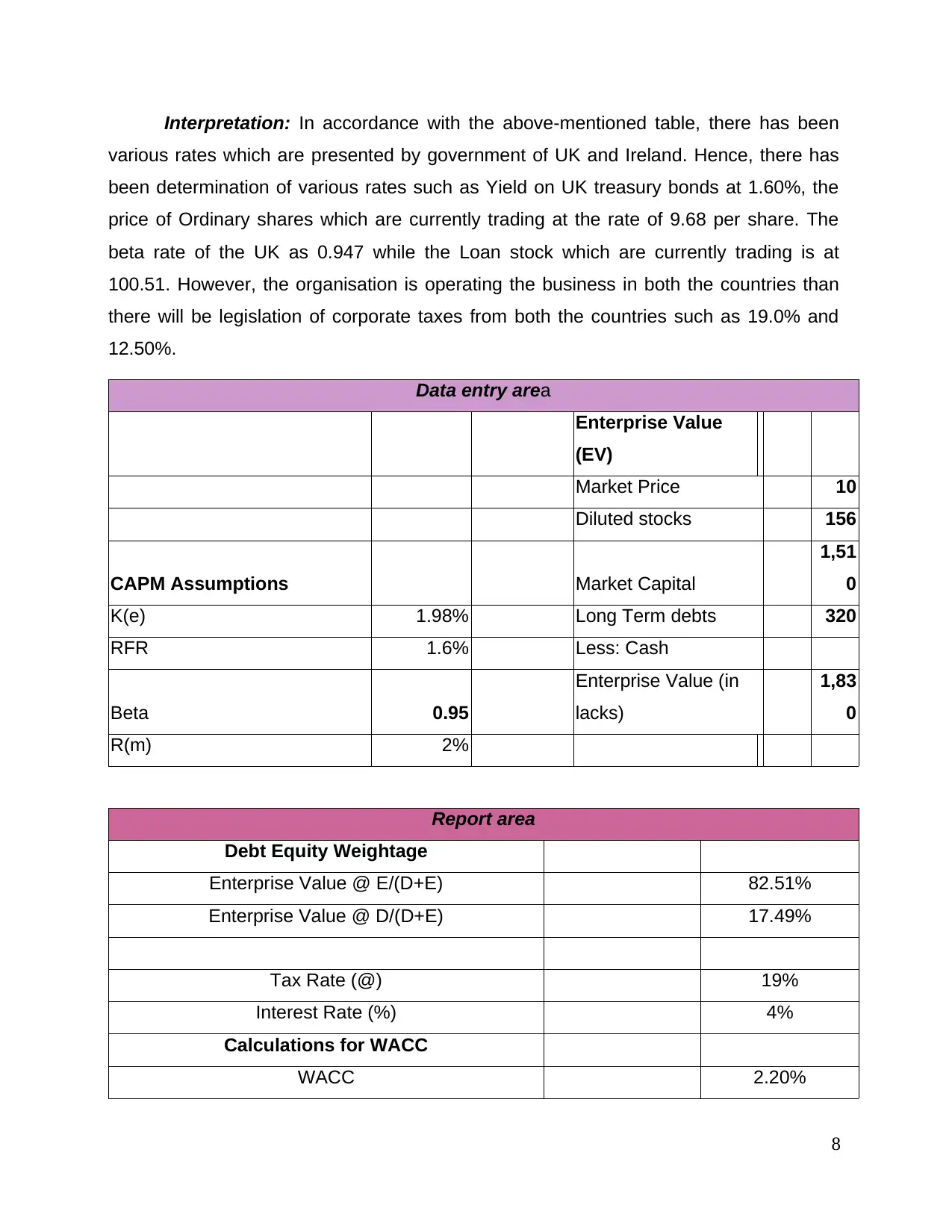

Interpretation: In accordance with the above-mentioned table, there has been

various rates which are presented by government of UK and Ireland. Hence, there has

been determination of various rates such as Yield on UK treasury bonds at 1.60%, the

price of Ordinary shares which are currently trading at the rate of 9.68 per share. The

beta rate of the UK as 0.947 while the Loan stock which are currently trading is at

100.51. However, the organisation is operating the business in both the countries than

there will be legislation of corporate taxes from both the countries such as 19.0% and

12.50%.

Data entry area

Enterprise Value

(EV)

Market Price 10

Diluted stocks 156

CAPM Assumptions Market Capital

1,51

0

K(e) 1.98% Long Term debts 320

RFR 1.6% Less: Cash

Beta 0.95

Enterprise Value (in

lacks)

1,83

0

R(m) 2%

Report area

Debt Equity Weightage

Enterprise Value @ E/(D+E) 82.51%

Enterprise Value @ D/(D+E) 17.49%

Tax Rate (@) 19%

Interest Rate (%) 4%

Calculations for WACC

WACC 2.20%

8

various rates which are presented by government of UK and Ireland. Hence, there has

been determination of various rates such as Yield on UK treasury bonds at 1.60%, the

price of Ordinary shares which are currently trading at the rate of 9.68 per share. The

beta rate of the UK as 0.947 while the Loan stock which are currently trading is at

100.51. However, the organisation is operating the business in both the countries than

there will be legislation of corporate taxes from both the countries such as 19.0% and

12.50%.

Data entry area

Enterprise Value

(EV)

Market Price 10

Diluted stocks 156

CAPM Assumptions Market Capital

1,51

0

K(e) 1.98% Long Term debts 320

RFR 1.6% Less: Cash

Beta 0.95

Enterprise Value (in

lacks)

1,83

0

R(m) 2%

Report area

Debt Equity Weightage

Enterprise Value @ E/(D+E) 82.51%

Enterprise Value @ D/(D+E) 17.49%

Tax Rate (@) 19%

Interest Rate (%) 4%

Calculations for WACC

WACC 2.20%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: By considering the above tables, it can be said that the firm is

having adequate WACC such as 2.20% which in turn reflects that the project will be

beneficial for the business in terms of making satisfactory revenue gathering. If the rate

of WACC is higher than there will be increments in the risks and reduction in the market

value of the corporation. Thus, it will be suggested to the managers of this organisation

that they must apply this technique as it reflects that the project will be fruitful for them.

However, the interest will be payable at the rate of 4% while the taxes were made at

19%.

CONCLUSION

To determine the profitability of this project that the business is being able to

make operations in UK and Europe it can be said that there have been positive impacts

of such investment. Euro jet will be beneficial in terms of NPV and WACC measurement.

Thus, it represents that the business will be fruitful for the organisation as it will facilitate

the beneficial returns. Further, the report also has elaborated various Forex theories

which is necessary to be determined by the international organisations as to understand

various policies and procedure of such operational tasks.

9

having adequate WACC such as 2.20% which in turn reflects that the project will be

beneficial for the business in terms of making satisfactory revenue gathering. If the rate

of WACC is higher than there will be increments in the risks and reduction in the market

value of the corporation. Thus, it will be suggested to the managers of this organisation

that they must apply this technique as it reflects that the project will be fruitful for them.

However, the interest will be payable at the rate of 4% while the taxes were made at

19%.

CONCLUSION

To determine the profitability of this project that the business is being able to

make operations in UK and Europe it can be said that there have been positive impacts

of such investment. Euro jet will be beneficial in terms of NPV and WACC measurement.

Thus, it represents that the business will be fruitful for the organisation as it will facilitate

the beneficial returns. Further, the report also has elaborated various Forex theories

which is necessary to be determined by the international organisations as to understand

various policies and procedure of such operational tasks.

9

REFERENCES

Books and Journals:

Agnihotri, R.,Hu, M.Y. and Krush, M.T., 2016. Social media: Influencing customer

satisfaction in B2B sales. Industrial Marketing Management. 53. pp.172-180.

Blut, M., Mittal, V. and Mothersbaugh, D.L., 2015. How procedural, financial and

relational switching costs affect customer satisfaction, repurchase intentions,

and repurchase behavior: A meta-analysis. International Journal of Research in

Marketing. 32(2). pp.226-229.

Ilushchenko, A. F., and Onashchenko, F. E., 2017. Flame spraying of coatings of self-

fluxing alloys. Welding International. 31(11). pp.887-891.

Matthews, R., 2018. European Collaboration in the Development of New Weapon

Systems. In The Emergence of EU Defense Research Policy (pp. 111-130).

Springer, Cham.

O'Halloran, C., Robinson, T. G. and Brock, N., 2017. Verifying cyber attack properties.

Science of Computer Programming. 148. pp.3-25.

Parker, R. and Fedder, G., 2016. Aircraft engines: a proud heritage and an exciting

future. The Aeronautical Journal. 120(1223). pp.131-169.

Pizam, A., Shapoval, V., and Ellis, T., 2016. Customer satisfaction and its measurement

in hospitality enterprises: a revisit and update. International Journal of

Contemporary Hospitality Management. 28(1). pp.2-35.

Zablah, A.R., and Brown, T.J., 2016. A cross-lagged test of the association between

customer satisfaction and employee job satisfaction in a relational context.

Journal of Applied Psychology. 101(5). p.743.

Online

10

Books and Journals:

Agnihotri, R.,Hu, M.Y. and Krush, M.T., 2016. Social media: Influencing customer

satisfaction in B2B sales. Industrial Marketing Management. 53. pp.172-180.

Blut, M., Mittal, V. and Mothersbaugh, D.L., 2015. How procedural, financial and

relational switching costs affect customer satisfaction, repurchase intentions,

and repurchase behavior: A meta-analysis. International Journal of Research in

Marketing. 32(2). pp.226-229.

Ilushchenko, A. F., and Onashchenko, F. E., 2017. Flame spraying of coatings of self-

fluxing alloys. Welding International. 31(11). pp.887-891.

Matthews, R., 2018. European Collaboration in the Development of New Weapon

Systems. In The Emergence of EU Defense Research Policy (pp. 111-130).

Springer, Cham.

O'Halloran, C., Robinson, T. G. and Brock, N., 2017. Verifying cyber attack properties.

Science of Computer Programming. 148. pp.3-25.

Parker, R. and Fedder, G., 2016. Aircraft engines: a proud heritage and an exciting

future. The Aeronautical Journal. 120(1223). pp.131-169.

Pizam, A., Shapoval, V., and Ellis, T., 2016. Customer satisfaction and its measurement

in hospitality enterprises: a revisit and update. International Journal of

Contemporary Hospitality Management. 28(1). pp.2-35.

Zablah, A.R., and Brown, T.J., 2016. A cross-lagged test of the association between

customer satisfaction and employee job satisfaction in a relational context.

Journal of Applied Psychology. 101(5). p.743.

Online

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.