Market Fluctuation and Forecast Report

VerifiedAdded on 2019/09/26

|7

|1118

|431

Report

AI Summary

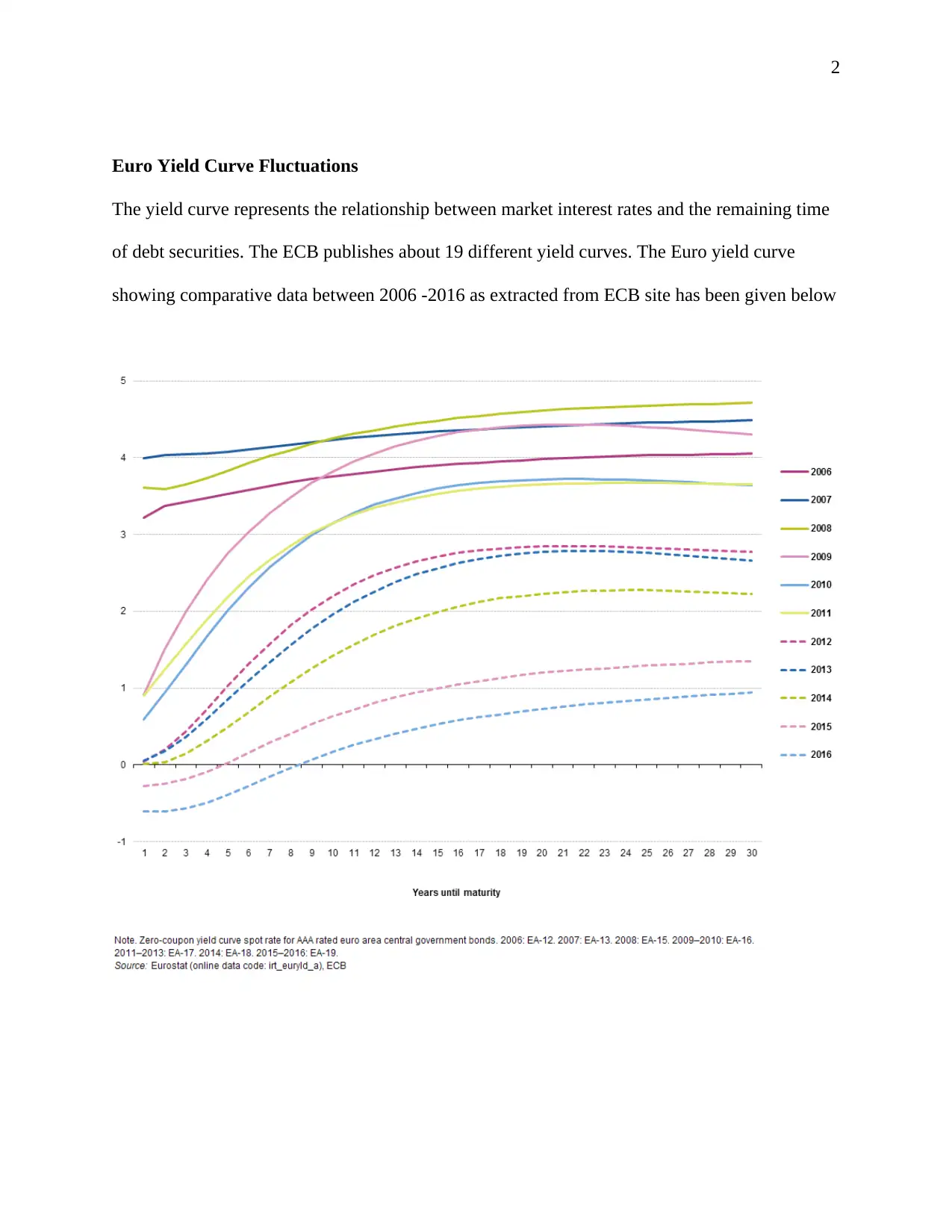

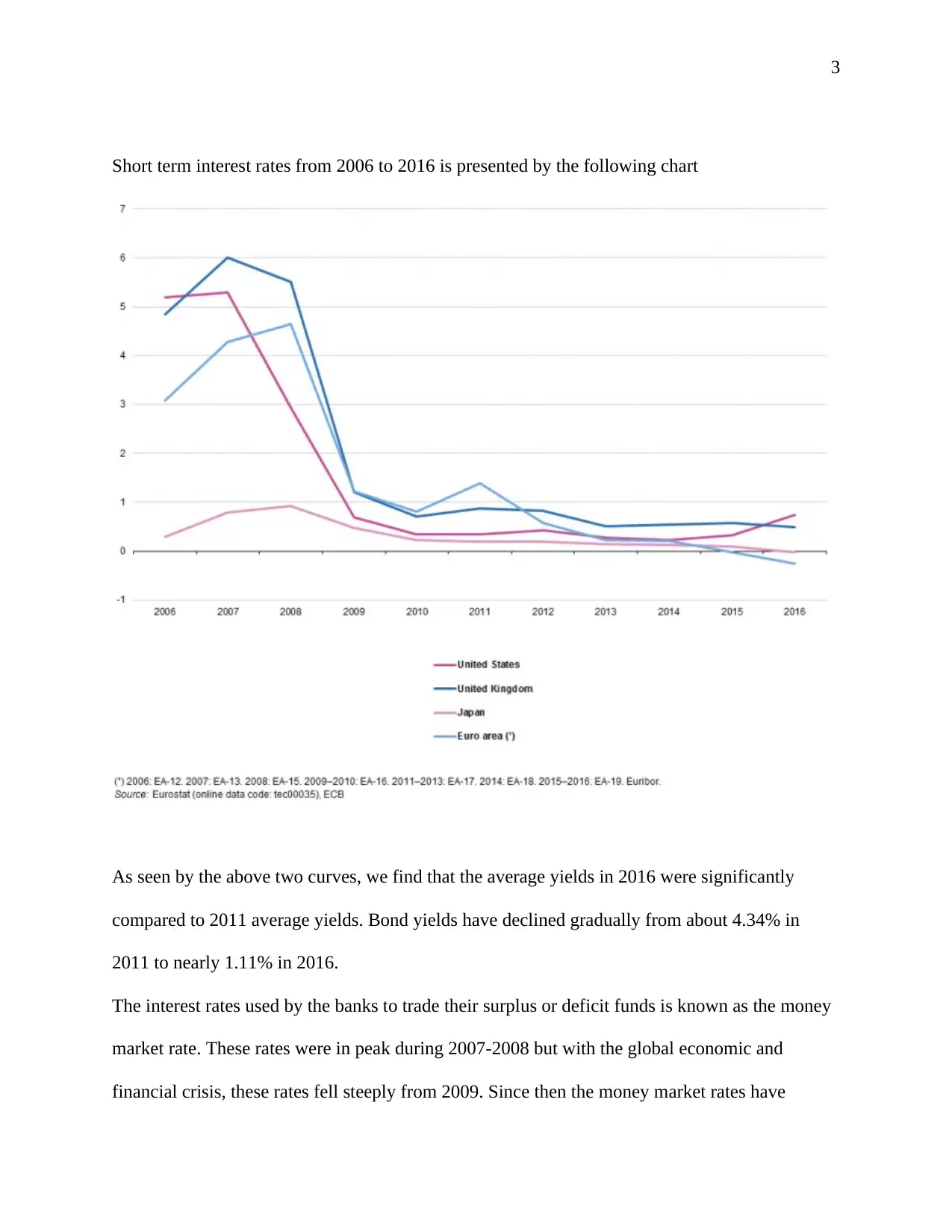

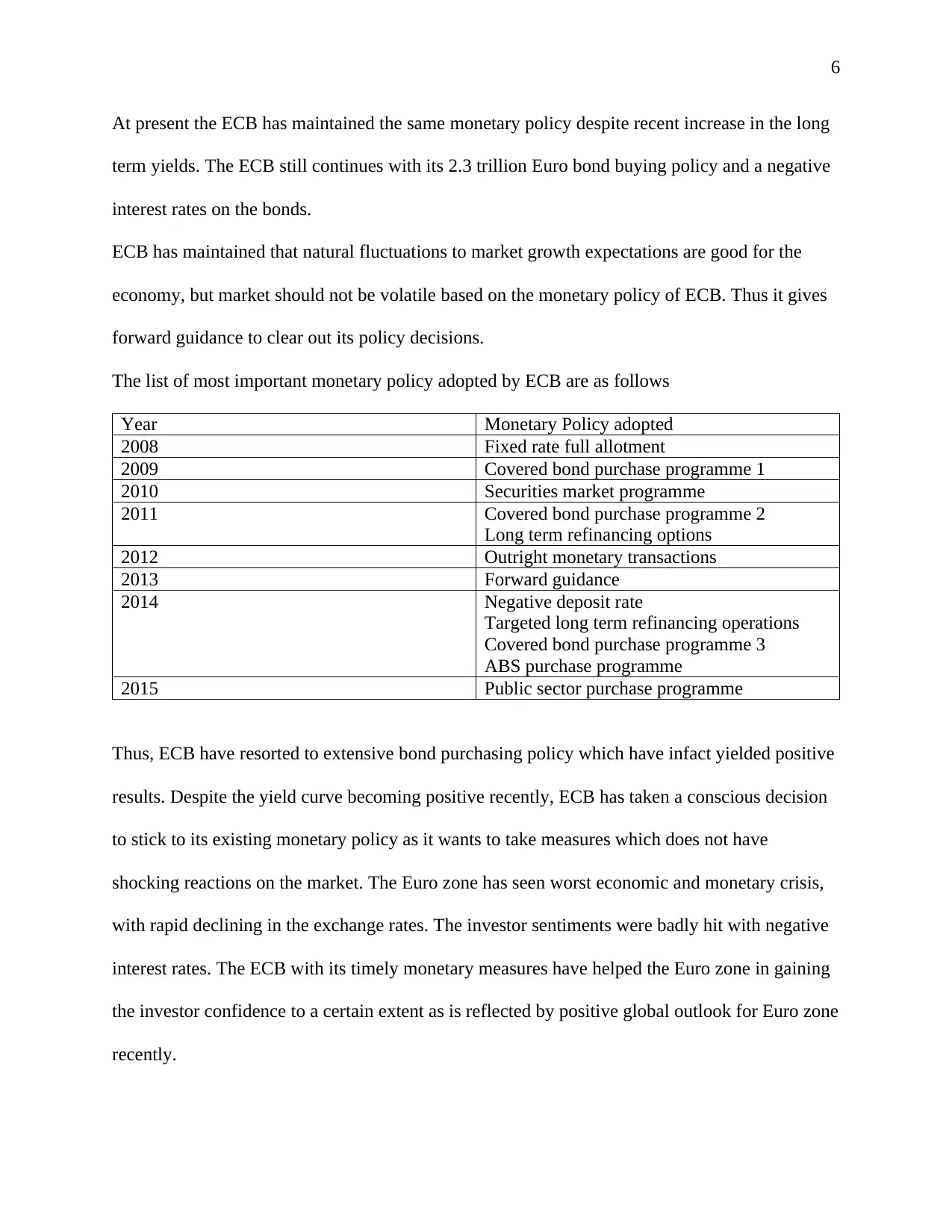

This report analyzes the fluctuations in the Euro yield curve from 2006 to 2016, focusing on the impact of the European Central Bank's (ECB) monetary policies. It examines the relationship between market interest rates and the time to maturity of debt securities, highlighting the significant decline in bond yields from 2011 to 2016, including the emergence of negative interest rates. The report discusses the ECB's use of various monetary policy tools, such as the main refinancing operations, marginal lending facility, and deposit facility, to maintain price stability and control inflation. The analysis includes the role of overnight index swaps and Bund curves in policy formulation, and the impact of the ECB's forward guidance and asset purchase programs on both short-term and long-term yields. The report concludes by summarizing the ECB's monetary policy measures and their effectiveness in managing the Eurozone's economic and monetary crisis, emphasizing the importance of maintaining investor confidence and avoiding market volatility.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.