Analysis of European Financial Market and Trilemma Issues

VerifiedAdded on 2019/10/31

|6

|1042

|184

Report

AI Summary

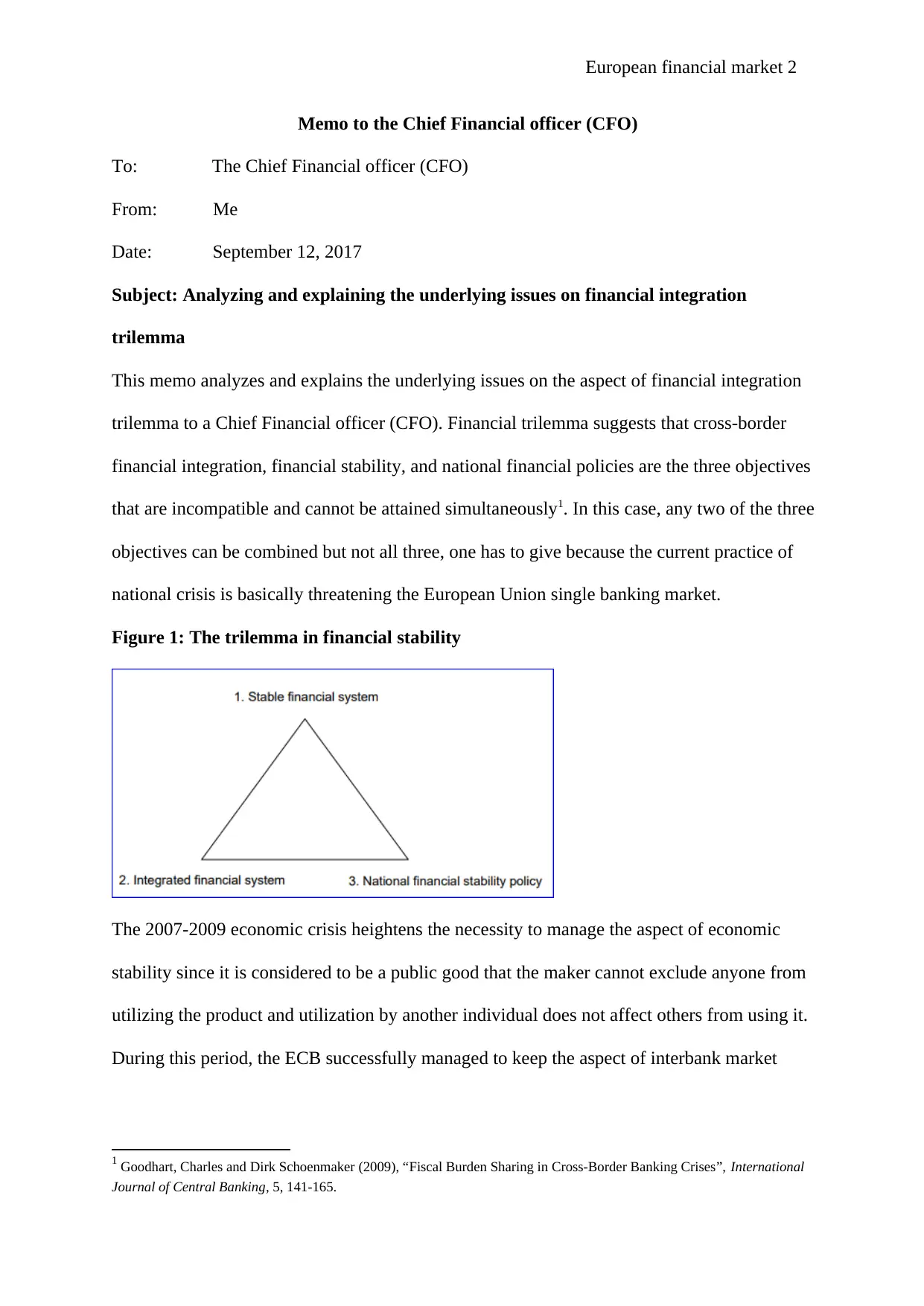

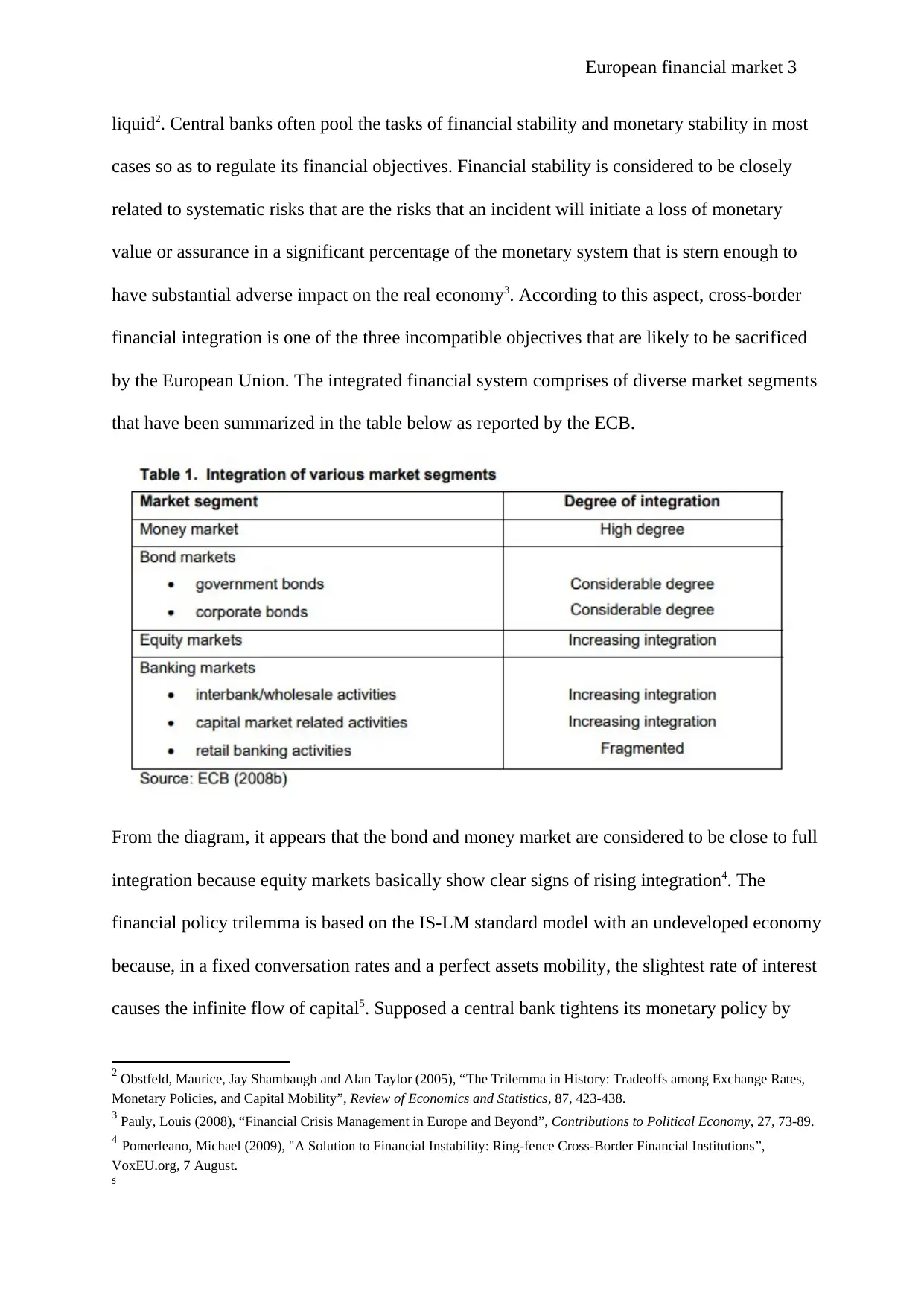

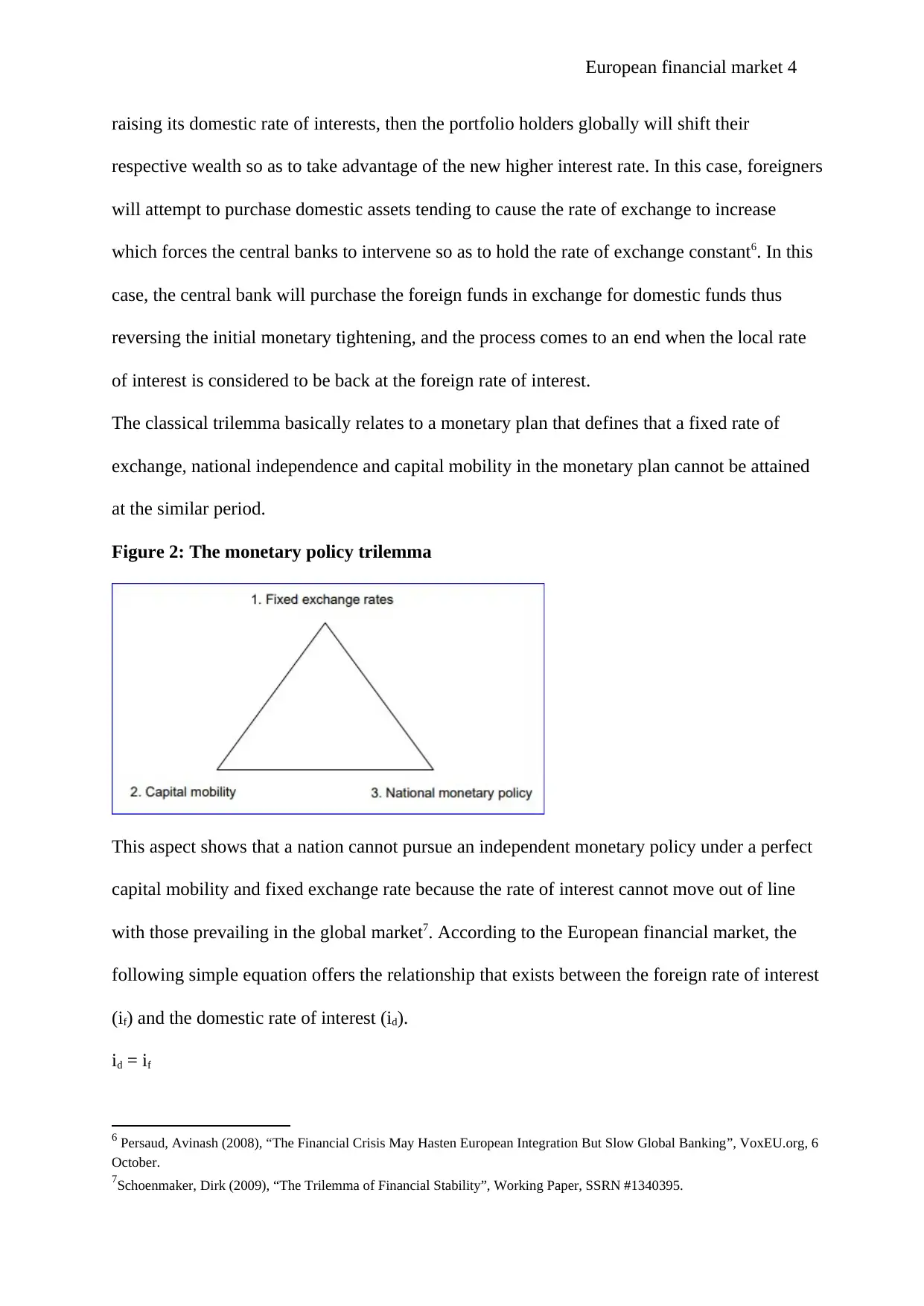

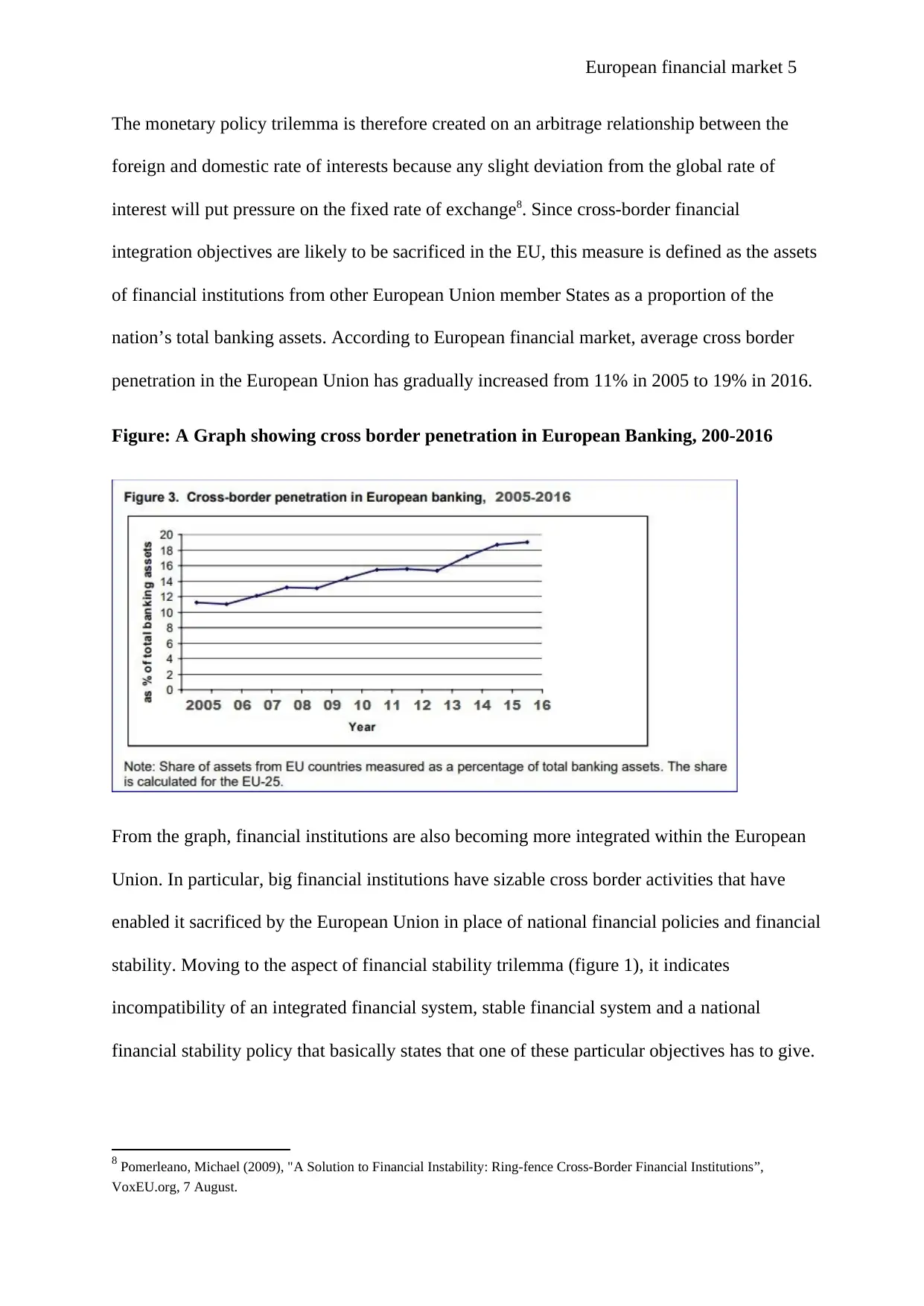

This report provides an analysis of the European financial market, specifically focusing on the financial integration trilemma. It explains the incompatibility of cross-border financial integration, financial stability, and national financial policies, highlighting the challenges faced by the European Union. The report discusses the 2007-2009 economic crisis and its impact on financial stability, the role of the ECB, and the concept of systematic risks. It examines the financial policy trilemma based on the IS-LM model and discusses the relationship between domestic and foreign interest rates. Furthermore, the report analyzes the increasing cross-border penetration in the European banking sector and the integration of financial institutions, particularly large ones. The report concludes by emphasizing the sacrifices that must be made in the European Union in order to maintain financial stability and national financial policies. The report also includes relevant bibliography for further reading.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.