Comparative Analysis: ABC and Absorption Costing at Golden Casket

VerifiedAdded on 2023/06/10

|8

|1098

|293

Report

AI Summary

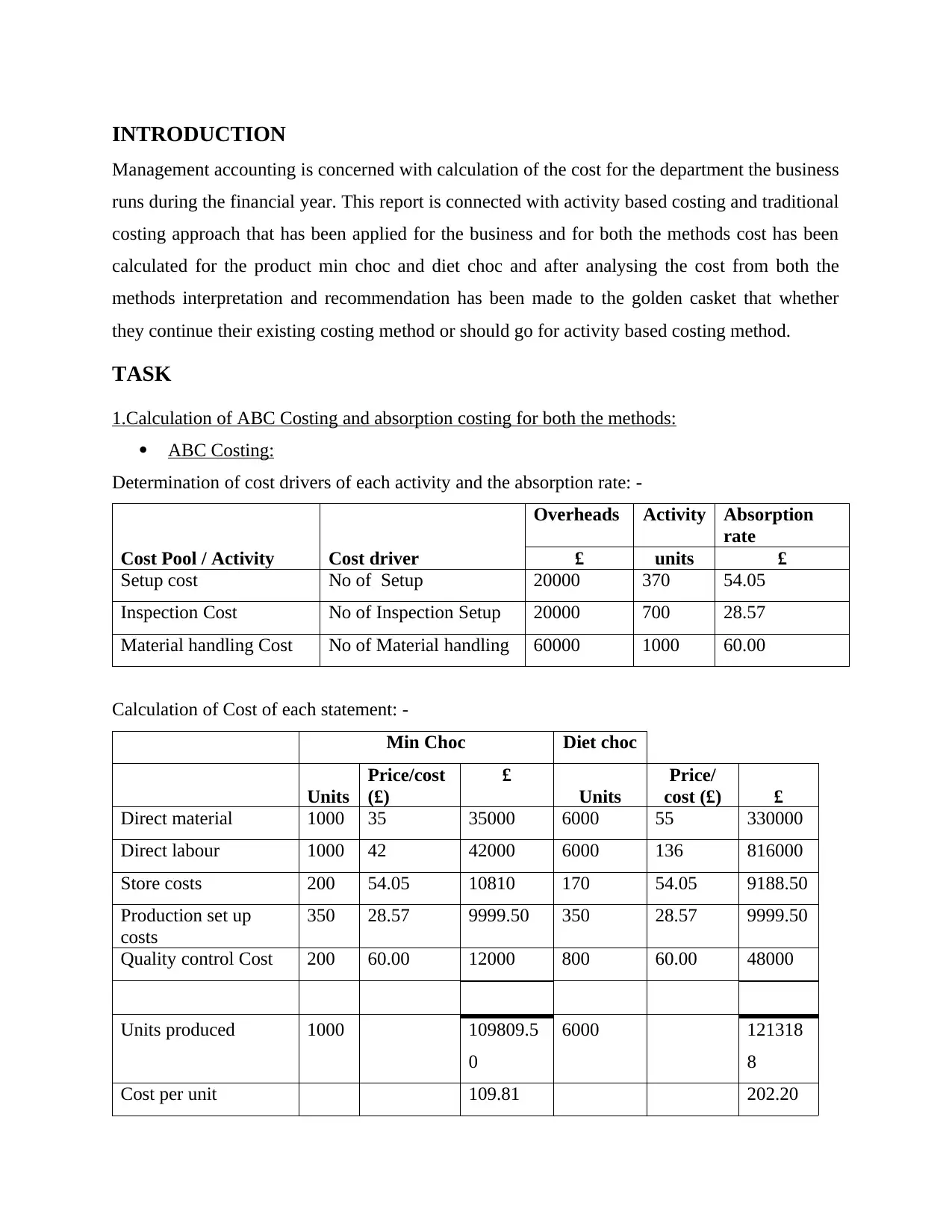

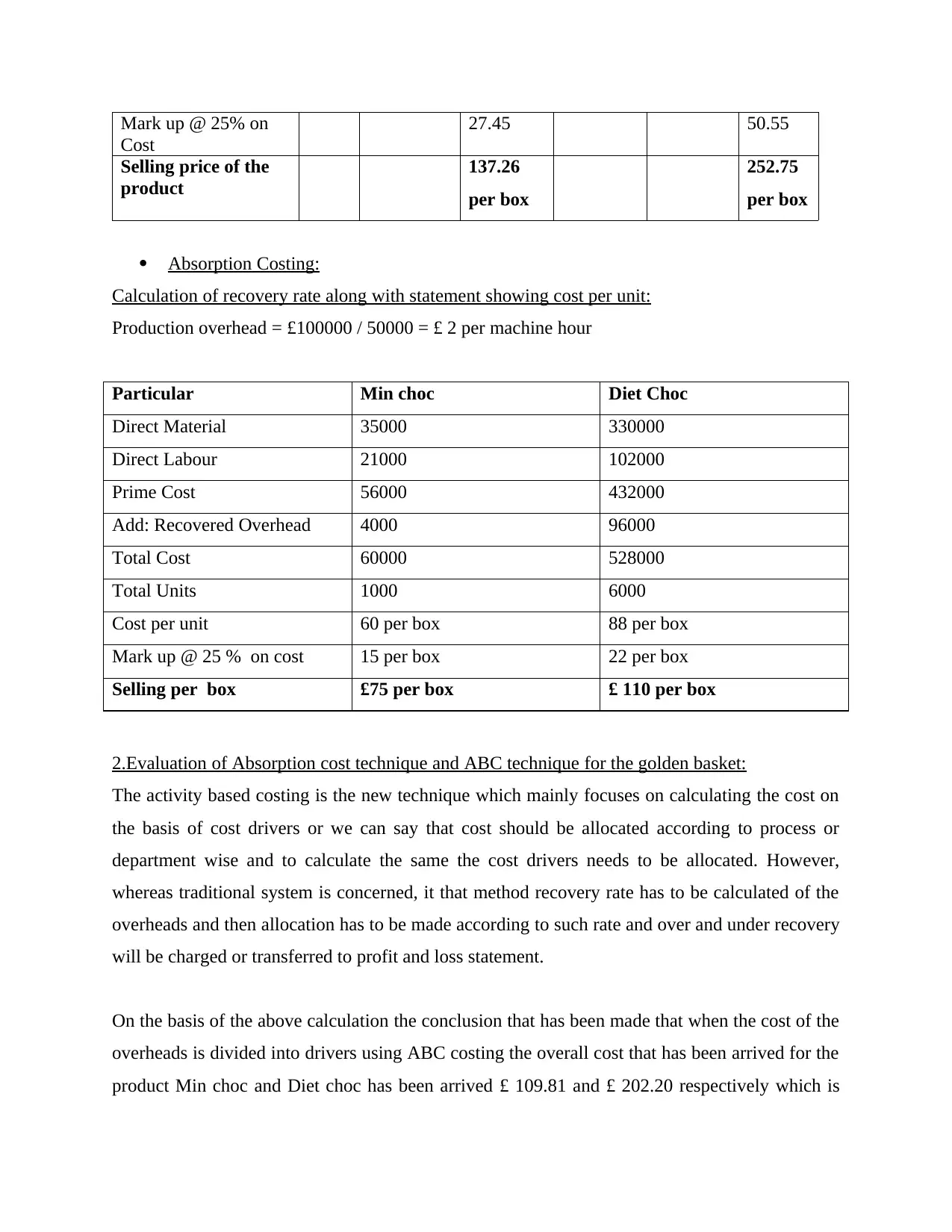

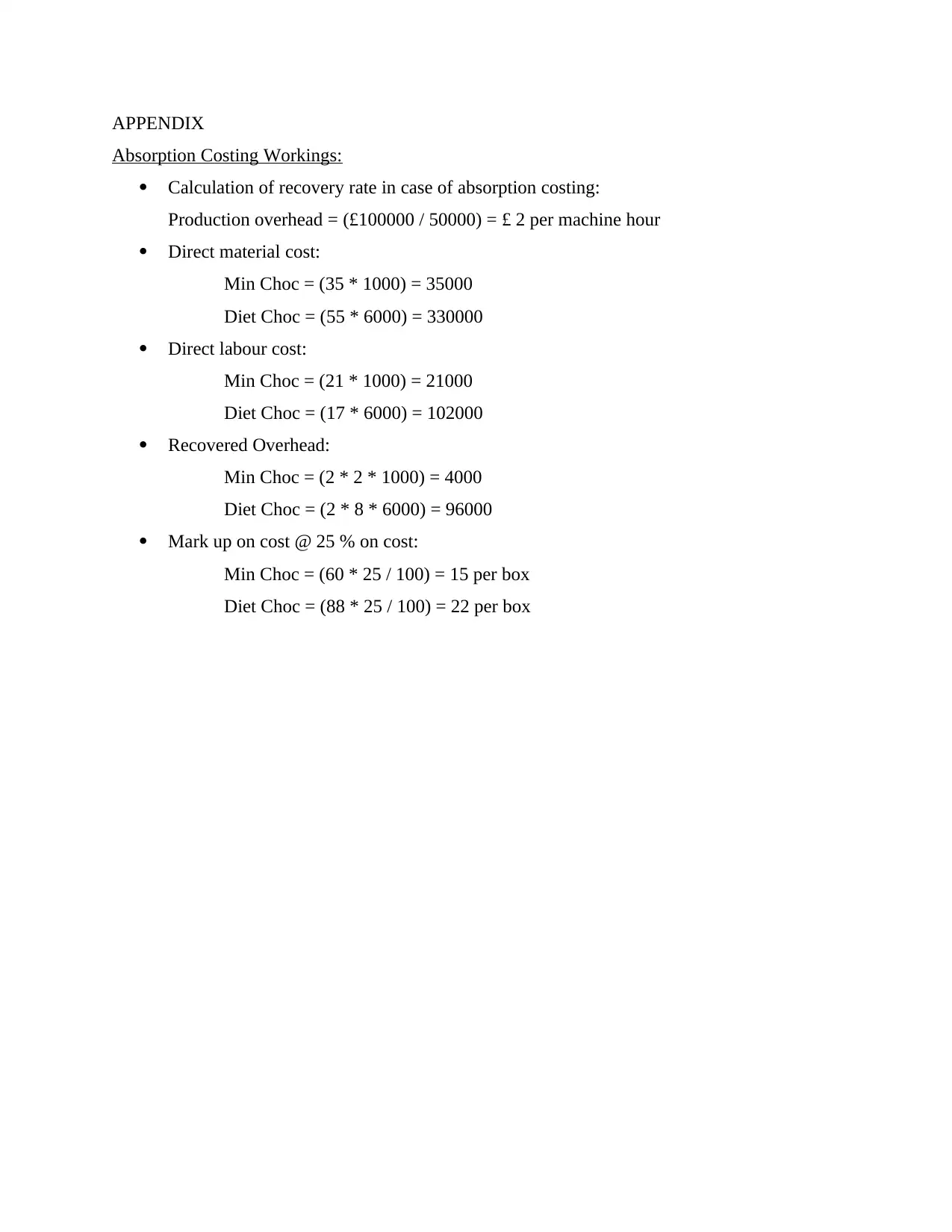

This report analyzes activity-based costing (ABC) and absorption costing methods for Golden Casket, focusing on the products Min Choc and Diet Choc. The analysis involves calculating costs using both methods, evaluating their applicability, and providing recommendations. ABC costing identifies cost drivers for each activity, while absorption costing uses an overhead recovery rate. The report finds that ABC results in higher costs per unit compared to absorption costing. The recommendation is to continue using the traditional absorption costing method to maintain acceptable product costs and sales volume. Appendices provide detailed calculations for both costing methods, including overhead recovery rates, material and labor costs, and markup calculations. The conclusion emphasizes that sticking with traditional costing is more viable for Golden Casket's financial health and consumer acceptance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.