Evaluating Murray Goulburn's Financial Standing-Financial Reports

VerifiedAdded on 2023/06/12

|5

|833

|418

Report

AI Summary

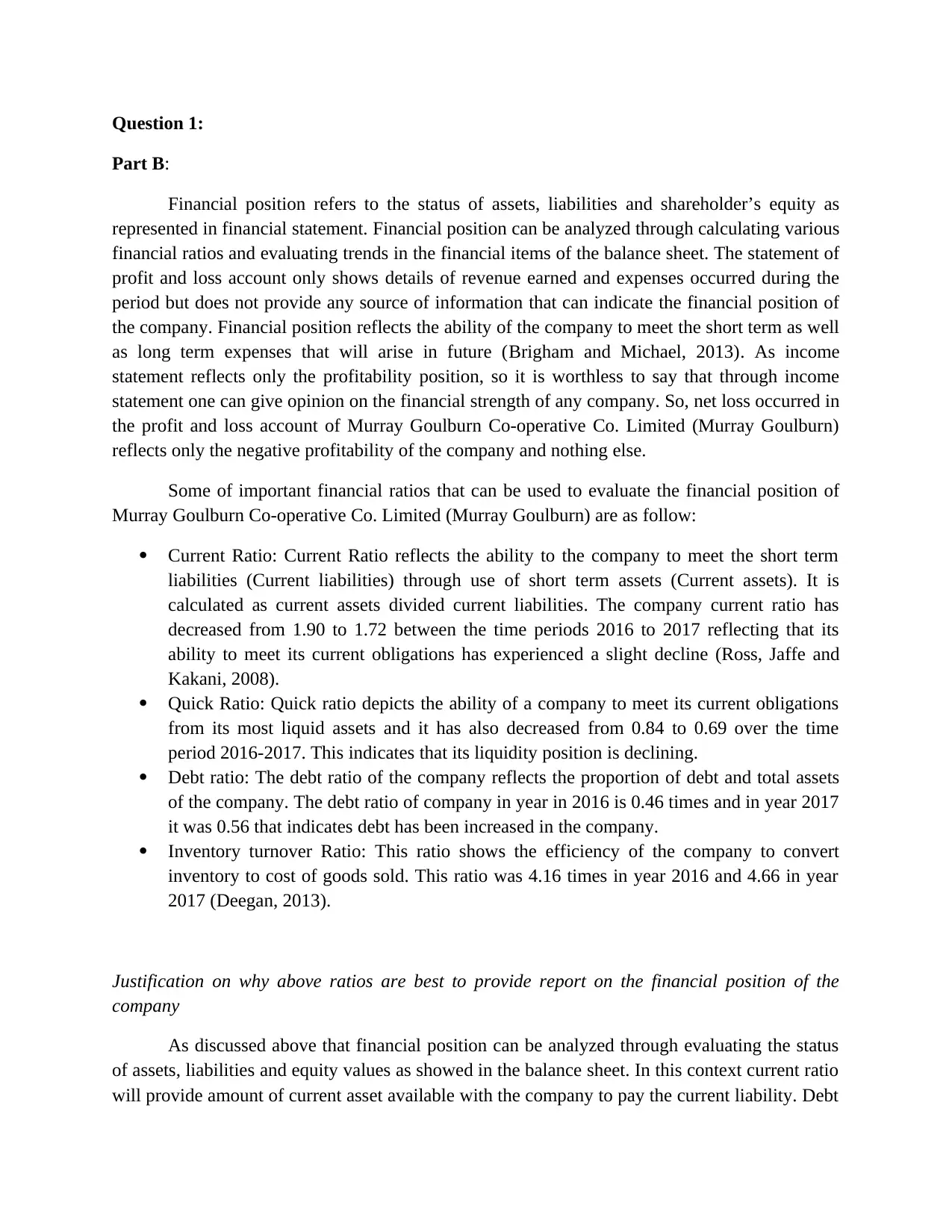

This report analyzes the financial position of Murray Goulburn Co-operative Co. Limited using financial ratios. It discusses the limitations of using only the profit and loss account to assess financial health, emphasizing the importance of balance sheet analysis. Key ratios like current ratio, quick ratio, debt ratio, and inventory turnover ratio are calculated and interpreted to evaluate the company's liquidity, debt levels, and efficiency in managing inventory. The report justifies the selection of these ratios based on their relevance in assessing assets, liabilities, and equity, providing insights into the company's ability to meet short-term obligations and overall financial stability. Desklib offers a platform to explore similar financial reports and solved assignments for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.