Evaluating Divisional Performance Using Cost Accounting: Tyndall

VerifiedAdded on 2023/04/08

|8

|762

|305

Case Study

AI Summary

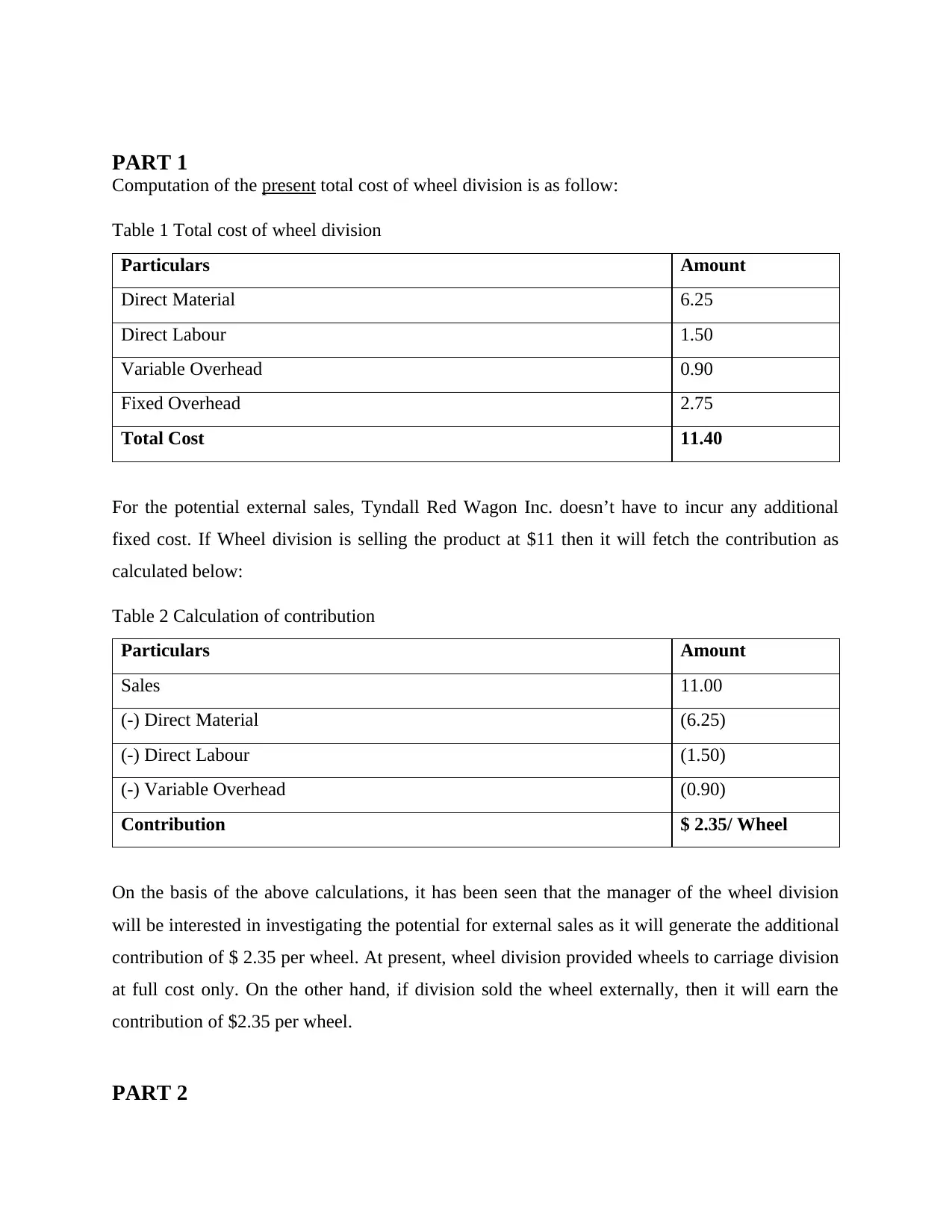

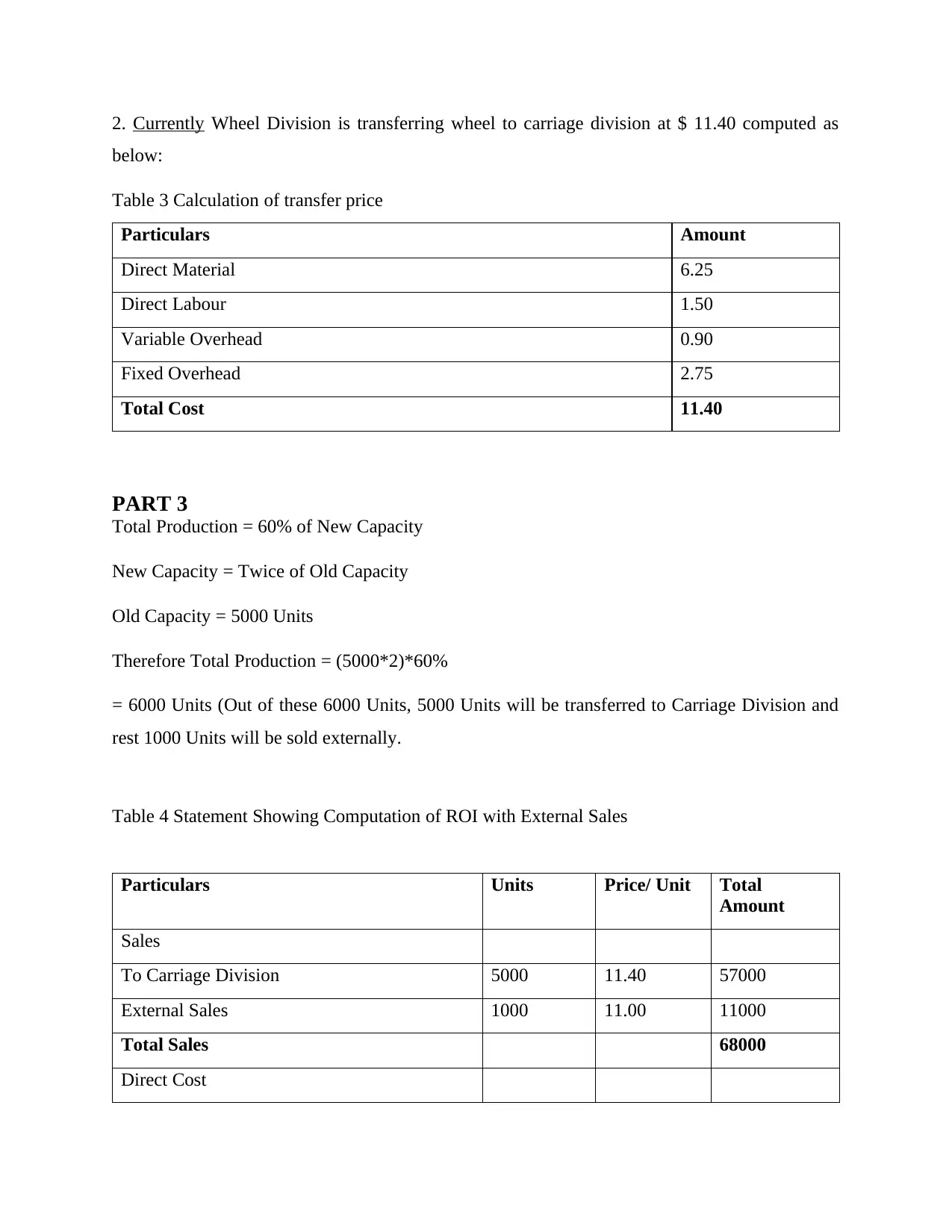

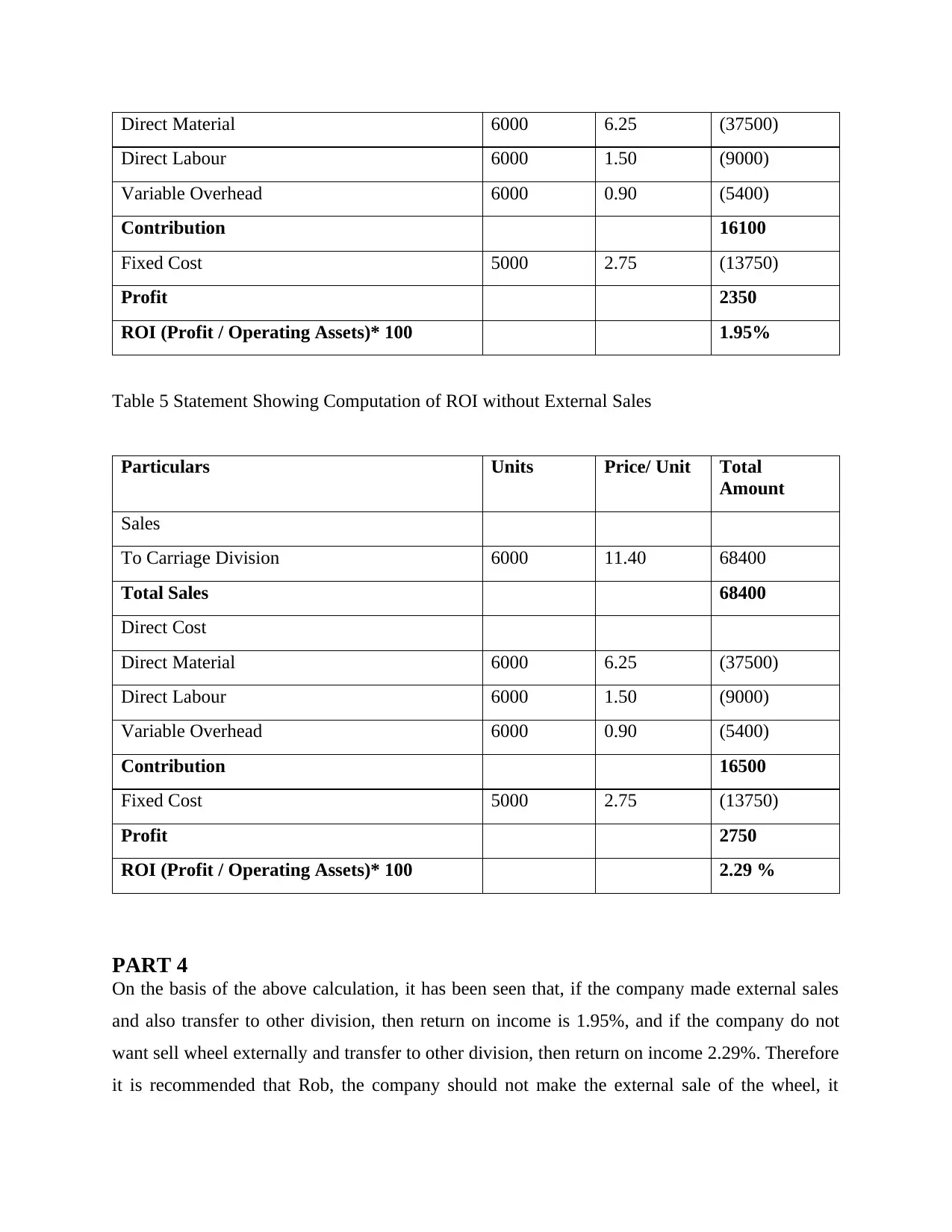

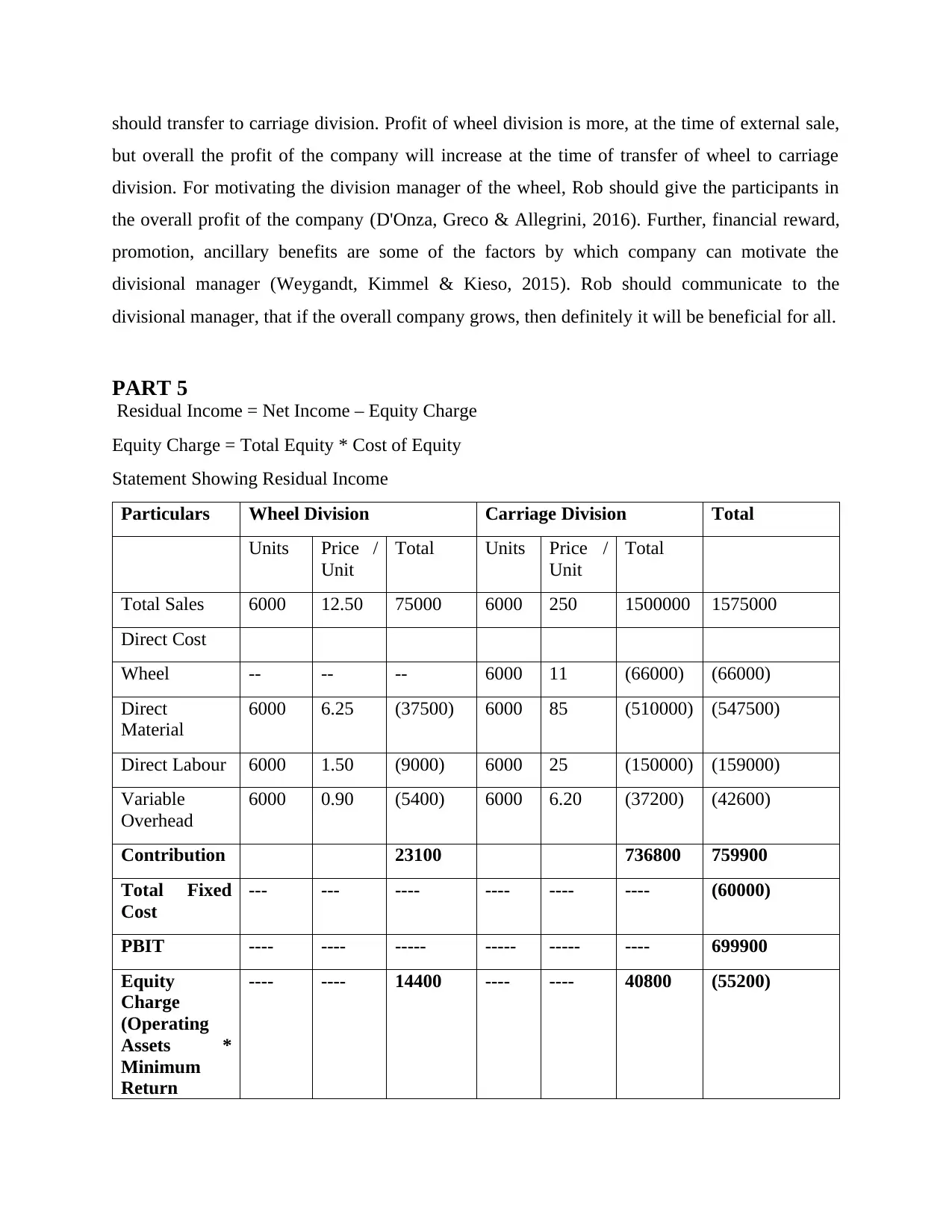

This case study provides a comprehensive cost accounting analysis of Tyndall Red Wagon Inc., focusing on the Wheel Division's performance and its potential for external sales. It examines the current total cost of the wheel division, calculates the contribution margin from potential external sales, and analyzes the return on investment (ROI) with and without external sales. The study recommends against external sales based on ROI and suggests strategies for motivating the divisional manager. Furthermore, it calculates residual income for both the Wheel and Carriage Divisions to assess their economic profitability. The analysis includes detailed calculations of direct costs, fixed costs, and equity charges to provide a holistic view of the company's financial performance. Desklib offers similar solved assignments.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.