Comprehensive Analysis of IAS 16 and IAS 37 in Financial Reporting

VerifiedAdded on 2020/06/06

|13

|3712

|66

Report

AI Summary

This report offers a detailed analysis of International Accounting Standards (IAS) 16 and 37. It begins with a critical evaluation of IAS 16, focusing on property, plant, and equipment, including asset recognition, valuation using cost and revaluation models, depreciation, and impairment losses. The report highlights the complexities of determining fair value and discount rates, as well as the limitations of the revaluation model. The valuation of ships is then presented using both cost and revaluation models, with detailed calculations and tables. The report also evaluates IAS 37 concerning provisions, contingent liabilities, and contingent assets, identifying potential for earnings manipulation and challenges in understanding the guidelines. It discusses limitations related to recognition criteria, measurement requirements, and consistency in application. The report concludes by emphasizing the need for improvements in IAS 37 to ensure accurate and consistent accounting practices.

INTERNATIONAL FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

1Critical evaluation of IAS 16 Property, plant and equipment...................................................1

2Valuation of ship........................................................................................................................2

Question 2........................................................................................................................................5

1Critical evaluation of IAS 37 provisions...................................................................................5

2.a Treatment of provision in books of accounts.........................................................................6

2.b Case of contingent assets.......................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

1Critical evaluation of IAS 16 Property, plant and equipment...................................................1

2Valuation of ship........................................................................................................................2

Question 2........................................................................................................................................5

1Critical evaluation of IAS 37 provisions...................................................................................5

2.a Treatment of provision in books of accounts.........................................................................6

2.b Case of contingent assets.......................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting is the one of the important branch of commerce discipline. Over past couple

of years many changes are made in the IAS that are followed across the globe. In current report

IAS 15 property, plant and equipment is reviewed and along with this, IAS 37 of contingent

assets and liability is also applied on relevant cases to develop broad understanding about them.

Apart from this, valuation of assets is done by following cost model and revaluation model. In

this regard discount rate is taken in to account and at same rate cash flows present value is

calculated. At end of the report conclusion section is prepared and in this research work is

carried out in report.

Question 1

1Critical evaluation of IAS 16 Property, plant and equipment

IAS 16 is the one of the main accounting standard that is followed by most of business

firms across the globe. This is because it contain provisions that must be followed to do

accounting in systematic manner for property, plant and equipment. IAS 16 primarily was

prepared to develop accounting treatment that must be followed in respect to property, plant and

equipment (Cairns and et.al., 2011). There are some of the issus that are closely associated with

the mentioned principle. Mainly these issues are related to recognizing assets, determining

carrying amount, depreciation charges and impairment lossess that are related to assets. In the

last paragraph 7 it is clearly stated that an asset must be recognized at its historical value. As per

rules historical cost can be recognized only in case it is possible that cost of an item can be

measured reliably. Second important condition is that future economic benefit will be associated

with entity. Means that asset will generate future cash inflows (Rattenbacher and et.al, 2010).

Thereafter firm need to determine apporach by using which fair value of an asset can be

computed for its entire life.

At this point issue is mainly faced by the busines firms as they need to compute fair value

of an asset. Fair value have nothing to do with current market price. Under this simply discount

rate is determined and by using same cash flows are discounted to compute fair value of asset.

Means that first of all cash flows from asset that will be earned in future are estimated and then

by using discount rate same is discounted and added to calculate value of asset (Aljinović Barać

and Šodan, 2011). One of main difficult task is to determine accurate discount rate. If discount

rate will be estimated wrongly then in that case wrong value of asset will be computed as fair

1 | P a g e

Accounting is the one of the important branch of commerce discipline. Over past couple

of years many changes are made in the IAS that are followed across the globe. In current report

IAS 15 property, plant and equipment is reviewed and along with this, IAS 37 of contingent

assets and liability is also applied on relevant cases to develop broad understanding about them.

Apart from this, valuation of assets is done by following cost model and revaluation model. In

this regard discount rate is taken in to account and at same rate cash flows present value is

calculated. At end of the report conclusion section is prepared and in this research work is

carried out in report.

Question 1

1Critical evaluation of IAS 16 Property, plant and equipment

IAS 16 is the one of the main accounting standard that is followed by most of business

firms across the globe. This is because it contain provisions that must be followed to do

accounting in systematic manner for property, plant and equipment. IAS 16 primarily was

prepared to develop accounting treatment that must be followed in respect to property, plant and

equipment (Cairns and et.al., 2011). There are some of the issus that are closely associated with

the mentioned principle. Mainly these issues are related to recognizing assets, determining

carrying amount, depreciation charges and impairment lossess that are related to assets. In the

last paragraph 7 it is clearly stated that an asset must be recognized at its historical value. As per

rules historical cost can be recognized only in case it is possible that cost of an item can be

measured reliably. Second important condition is that future economic benefit will be associated

with entity. Means that asset will generate future cash inflows (Rattenbacher and et.al, 2010).

Thereafter firm need to determine apporach by using which fair value of an asset can be

computed for its entire life.

At this point issue is mainly faced by the busines firms as they need to compute fair value

of an asset. Fair value have nothing to do with current market price. Under this simply discount

rate is determined and by using same cash flows are discounted to compute fair value of asset.

Means that first of all cash flows from asset that will be earned in future are estimated and then

by using discount rate same is discounted and added to calculate value of asset (Aljinović Barać

and Šodan, 2011). One of main difficult task is to determine accurate discount rate. If discount

rate will be estimated wrongly then in that case wrong value of asset will be computed as fair

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

value and wrong decisions will be made. Thus, it is very important to ensure that appropriate

discount rate is taken in to account to measure fair value of asset.

After determining cost of asset next year business firm have to choose either cost or

revaluation. There is difference between both models and also have some limitations. In IAS 16

it is clearly stated that asset must be valued at amount equal to value of asset minus depreciation

and impairment loss. Impairment loss reflect to value of asset that is reduced. Apart from cost

model there is another model which is known as revaluation model. There are some limitations

of revaluation model and one of them is that same is very complex in nature and difficult to

apply (Boterashvili and et.al., 2012). It is also not necessary that accurately value of asset is

predicted.

This is the major shortoming of the IAS 16 as it does not give completely reliable value

of asset. It can be said that revaluation model is very complex and it can be employed only when

fair value of an asset can be determined with reasonable reliability. As per this model one need to

compute real value of asset on date of revaluation and from same depreciation amount as well as

loss that is identified on performnace of impairment process must be removed. In such kind of

proces if fair value is wrongly determined asset can be valued at wrong amount (Damian and

et.al., 2014). In IAS clear procedure that must be followed for computing fair value is not given

which is major limitation of IAS 16.

However, positive side of IAS 16 is that it clearly instruct firms to carry out revaluation

of assets time to time so that real value of asset can be carried out in proper manner. In

mentioned accounting standard steps that firms must follow for revaluation of asset is clearly

defined. Hence, No firm can value asset at its own discretion.

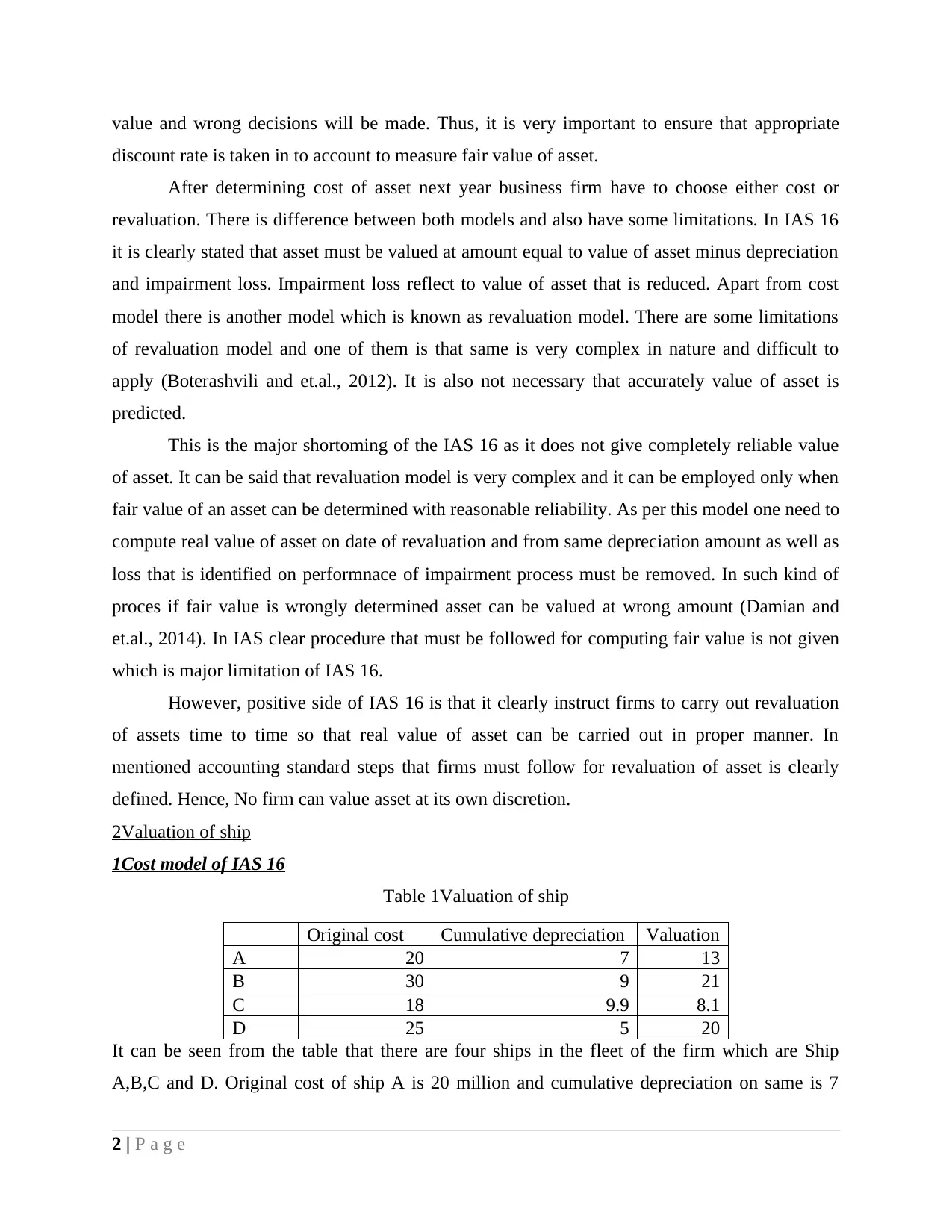

2Valuation of ship

1Cost model of IAS 16

Table 1Valuation of ship

Original cost Cumulative depreciation Valuation

A 20 7 13

B 30 9 21

C 18 9.9 8.1

D 25 5 20

It can be seen from the table that there are four ships in the fleet of the firm which are Ship

A,B,C and D. Original cost of ship A is 20 million and cumulative depreciation on same is 7

2 | P a g e

discount rate is taken in to account to measure fair value of asset.

After determining cost of asset next year business firm have to choose either cost or

revaluation. There is difference between both models and also have some limitations. In IAS 16

it is clearly stated that asset must be valued at amount equal to value of asset minus depreciation

and impairment loss. Impairment loss reflect to value of asset that is reduced. Apart from cost

model there is another model which is known as revaluation model. There are some limitations

of revaluation model and one of them is that same is very complex in nature and difficult to

apply (Boterashvili and et.al., 2012). It is also not necessary that accurately value of asset is

predicted.

This is the major shortoming of the IAS 16 as it does not give completely reliable value

of asset. It can be said that revaluation model is very complex and it can be employed only when

fair value of an asset can be determined with reasonable reliability. As per this model one need to

compute real value of asset on date of revaluation and from same depreciation amount as well as

loss that is identified on performnace of impairment process must be removed. In such kind of

proces if fair value is wrongly determined asset can be valued at wrong amount (Damian and

et.al., 2014). In IAS clear procedure that must be followed for computing fair value is not given

which is major limitation of IAS 16.

However, positive side of IAS 16 is that it clearly instruct firms to carry out revaluation

of assets time to time so that real value of asset can be carried out in proper manner. In

mentioned accounting standard steps that firms must follow for revaluation of asset is clearly

defined. Hence, No firm can value asset at its own discretion.

2Valuation of ship

1Cost model of IAS 16

Table 1Valuation of ship

Original cost Cumulative depreciation Valuation

A 20 7 13

B 30 9 21

C 18 9.9 8.1

D 25 5 20

It can be seen from the table that there are four ships in the fleet of the firm which are Ship

A,B,C and D. Original cost of ship A is 20 million and cumulative depreciation on same is 7

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

million which means that by considering cost model fair value of ship A is 13. On other hand, in

case of ship B original cost is 30 and value of depreciation is 9. On subtraction of depreciation

from asset computed value identified is 21 million. Same approach of cost model is followed for

ship C and its valuation is equal to 8.1 million which is very low in comparison to other ships. In

case of ship D original cost is 25 million and on subtraction of cumulative depreciation obtained

value is 20 million. It can be said that cost model is simple to apply as anyone can apply that

method easily.

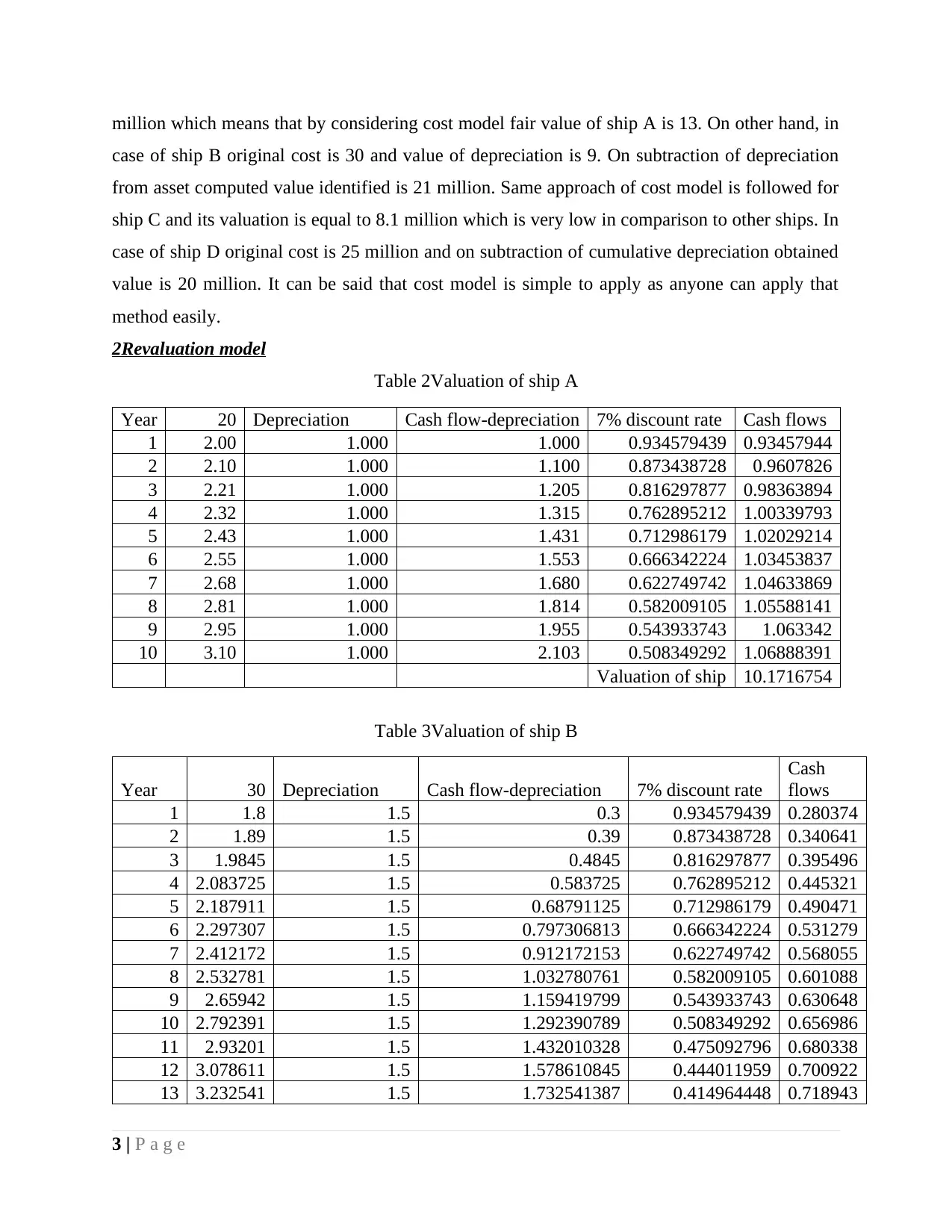

2Revaluation model

Table 2Valuation of ship A

Year 20 Depreciation Cash flow-depreciation 7% discount rate Cash flows

1 2.00 1.000 1.000 0.934579439 0.93457944

2 2.10 1.000 1.100 0.873438728 0.9607826

3 2.21 1.000 1.205 0.816297877 0.98363894

4 2.32 1.000 1.315 0.762895212 1.00339793

5 2.43 1.000 1.431 0.712986179 1.02029214

6 2.55 1.000 1.553 0.666342224 1.03453837

7 2.68 1.000 1.680 0.622749742 1.04633869

8 2.81 1.000 1.814 0.582009105 1.05588141

9 2.95 1.000 1.955 0.543933743 1.063342

10 3.10 1.000 2.103 0.508349292 1.06888391

Valuation of ship 10.1716754

Table 3Valuation of ship B

Year 30 Depreciation Cash flow-depreciation 7% discount rate

Cash

flows

1 1.8 1.5 0.3 0.934579439 0.280374

2 1.89 1.5 0.39 0.873438728 0.340641

3 1.9845 1.5 0.4845 0.816297877 0.395496

4 2.083725 1.5 0.583725 0.762895212 0.445321

5 2.187911 1.5 0.68791125 0.712986179 0.490471

6 2.297307 1.5 0.797306813 0.666342224 0.531279

7 2.412172 1.5 0.912172153 0.622749742 0.568055

8 2.532781 1.5 1.032780761 0.582009105 0.601088

9 2.65942 1.5 1.159419799 0.543933743 0.630648

10 2.792391 1.5 1.292390789 0.508349292 0.656986

11 2.93201 1.5 1.432010328 0.475092796 0.680338

12 3.078611 1.5 1.578610845 0.444011959 0.700922

13 3.232541 1.5 1.732541387 0.414964448 0.718943

3 | P a g e

case of ship B original cost is 30 and value of depreciation is 9. On subtraction of depreciation

from asset computed value identified is 21 million. Same approach of cost model is followed for

ship C and its valuation is equal to 8.1 million which is very low in comparison to other ships. In

case of ship D original cost is 25 million and on subtraction of cumulative depreciation obtained

value is 20 million. It can be said that cost model is simple to apply as anyone can apply that

method easily.

2Revaluation model

Table 2Valuation of ship A

Year 20 Depreciation Cash flow-depreciation 7% discount rate Cash flows

1 2.00 1.000 1.000 0.934579439 0.93457944

2 2.10 1.000 1.100 0.873438728 0.9607826

3 2.21 1.000 1.205 0.816297877 0.98363894

4 2.32 1.000 1.315 0.762895212 1.00339793

5 2.43 1.000 1.431 0.712986179 1.02029214

6 2.55 1.000 1.553 0.666342224 1.03453837

7 2.68 1.000 1.680 0.622749742 1.04633869

8 2.81 1.000 1.814 0.582009105 1.05588141

9 2.95 1.000 1.955 0.543933743 1.063342

10 3.10 1.000 2.103 0.508349292 1.06888391

Valuation of ship 10.1716754

Table 3Valuation of ship B

Year 30 Depreciation Cash flow-depreciation 7% discount rate

Cash

flows

1 1.8 1.5 0.3 0.934579439 0.280374

2 1.89 1.5 0.39 0.873438728 0.340641

3 1.9845 1.5 0.4845 0.816297877 0.395496

4 2.083725 1.5 0.583725 0.762895212 0.445321

5 2.187911 1.5 0.68791125 0.712986179 0.490471

6 2.297307 1.5 0.797306813 0.666342224 0.531279

7 2.412172 1.5 0.912172153 0.622749742 0.568055

8 2.532781 1.5 1.032780761 0.582009105 0.601088

9 2.65942 1.5 1.159419799 0.543933743 0.630648

10 2.792391 1.5 1.292390789 0.508349292 0.656986

11 2.93201 1.5 1.432010328 0.475092796 0.680338

12 3.078611 1.5 1.578610845 0.444011959 0.700922

13 3.232541 1.5 1.732541387 0.414964448 0.718943

3 | P a g e

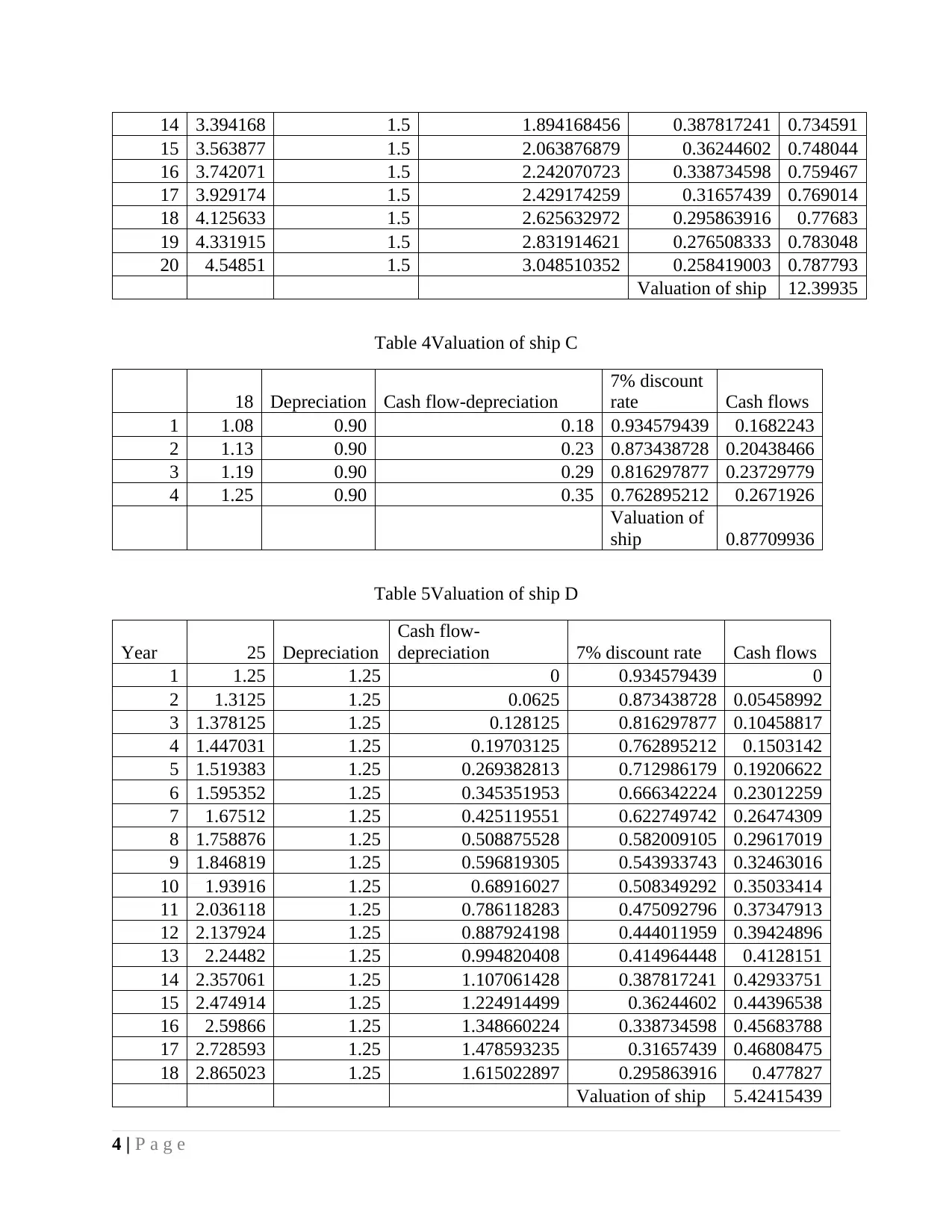

14 3.394168 1.5 1.894168456 0.387817241 0.734591

15 3.563877 1.5 2.063876879 0.36244602 0.748044

16 3.742071 1.5 2.242070723 0.338734598 0.759467

17 3.929174 1.5 2.429174259 0.31657439 0.769014

18 4.125633 1.5 2.625632972 0.295863916 0.77683

19 4.331915 1.5 2.831914621 0.276508333 0.783048

20 4.54851 1.5 3.048510352 0.258419003 0.787793

Valuation of ship 12.39935

Table 4Valuation of ship C

18 Depreciation Cash flow-depreciation

7% discount

rate Cash flows

1 1.08 0.90 0.18 0.934579439 0.1682243

2 1.13 0.90 0.23 0.873438728 0.20438466

3 1.19 0.90 0.29 0.816297877 0.23729779

4 1.25 0.90 0.35 0.762895212 0.2671926

Valuation of

ship 0.87709936

Table 5Valuation of ship D

Year 25 Depreciation

Cash flow-

depreciation 7% discount rate Cash flows

1 1.25 1.25 0 0.934579439 0

2 1.3125 1.25 0.0625 0.873438728 0.05458992

3 1.378125 1.25 0.128125 0.816297877 0.10458817

4 1.447031 1.25 0.19703125 0.762895212 0.1503142

5 1.519383 1.25 0.269382813 0.712986179 0.19206622

6 1.595352 1.25 0.345351953 0.666342224 0.23012259

7 1.67512 1.25 0.425119551 0.622749742 0.26474309

8 1.758876 1.25 0.508875528 0.582009105 0.29617019

9 1.846819 1.25 0.596819305 0.543933743 0.32463016

10 1.93916 1.25 0.68916027 0.508349292 0.35033414

11 2.036118 1.25 0.786118283 0.475092796 0.37347913

12 2.137924 1.25 0.887924198 0.444011959 0.39424896

13 2.24482 1.25 0.994820408 0.414964448 0.4128151

14 2.357061 1.25 1.107061428 0.387817241 0.42933751

15 2.474914 1.25 1.224914499 0.36244602 0.44396538

16 2.59866 1.25 1.348660224 0.338734598 0.45683788

17 2.728593 1.25 1.478593235 0.31657439 0.46808475

18 2.865023 1.25 1.615022897 0.295863916 0.477827

Valuation of ship 5.42415439

4 | P a g e

15 3.563877 1.5 2.063876879 0.36244602 0.748044

16 3.742071 1.5 2.242070723 0.338734598 0.759467

17 3.929174 1.5 2.429174259 0.31657439 0.769014

18 4.125633 1.5 2.625632972 0.295863916 0.77683

19 4.331915 1.5 2.831914621 0.276508333 0.783048

20 4.54851 1.5 3.048510352 0.258419003 0.787793

Valuation of ship 12.39935

Table 4Valuation of ship C

18 Depreciation Cash flow-depreciation

7% discount

rate Cash flows

1 1.08 0.90 0.18 0.934579439 0.1682243

2 1.13 0.90 0.23 0.873438728 0.20438466

3 1.19 0.90 0.29 0.816297877 0.23729779

4 1.25 0.90 0.35 0.762895212 0.2671926

Valuation of

ship 0.87709936

Table 5Valuation of ship D

Year 25 Depreciation

Cash flow-

depreciation 7% discount rate Cash flows

1 1.25 1.25 0 0.934579439 0

2 1.3125 1.25 0.0625 0.873438728 0.05458992

3 1.378125 1.25 0.128125 0.816297877 0.10458817

4 1.447031 1.25 0.19703125 0.762895212 0.1503142

5 1.519383 1.25 0.269382813 0.712986179 0.19206622

6 1.595352 1.25 0.345351953 0.666342224 0.23012259

7 1.67512 1.25 0.425119551 0.622749742 0.26474309

8 1.758876 1.25 0.508875528 0.582009105 0.29617019

9 1.846819 1.25 0.596819305 0.543933743 0.32463016

10 1.93916 1.25 0.68916027 0.508349292 0.35033414

11 2.036118 1.25 0.786118283 0.475092796 0.37347913

12 2.137924 1.25 0.887924198 0.444011959 0.39424896

13 2.24482 1.25 0.994820408 0.414964448 0.4128151

14 2.357061 1.25 1.107061428 0.387817241 0.42933751

15 2.474914 1.25 1.224914499 0.36244602 0.44396538

16 2.59866 1.25 1.348660224 0.338734598 0.45683788

17 2.728593 1.25 1.478593235 0.31657439 0.46808475

18 2.865023 1.25 1.615022897 0.295863916 0.477827

Valuation of ship 5.42415439

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On valuation it can be seen that fair value of asset A is 10.17 million, B is valued at 12.39

million,0.87 million and D is valued at 5.42 million.

3 Problem arriving at valuation of ship

There were problem that were faced while doing valuation of ship. Problem was that it

was hard to estimate discount rate. In case wrong discount rate is taken in to account asset may

be valued at wrong value. Hence, it is very important to estimate accurate discount rate to

estimate value of any asset.

Question 2

1Critical evaluation of IAS 37 provisions

There are few limitations of IAS 37 as it is related to contingent liabilities and contingent

assets. Like it can be seen that in case of accounting standards there are some limitations and in

present case also it is identified that there are some limitations of IAS 37. There is significent

scope of manipulation of earning in the books of accounts if IAS37. For example under

provisions of IAS 37 firms can make provisions for future costs which are not obligation for the

firm in current time period (Firoz and Ansari, 2010). Apart from this, IAS 37 only allows

provisions which meet definition of liability. Such kind of aspects of IAS 37 are not considered

good and there is need to make modification in it. There are many other shortcomings in the IAS

37 and due to this reason IASB is considering to make changes in IAS 37. There are some

guidelines that are given in mentioned standard but same are difficult to understand and it

become hard for one to identify liability. Recogniition that is done in the relevant standard are

also questionable in nature. In other words it can be said that threshold that is determined in

standard are also not clear. This is one of the main limitation of the named standard and need to

be improved on time so that accounting can be done in systematic manner (Jaweher and

Mounira, 2014). Some of measurement requirements are also given in the IASB but same are

very unclear in nature. Hence, it can be said that there are huge limitations of IAS 37 and there

are lots of areas where improvements need to be made in the standard.

There is also lack of consistency in the standard as it can be observed that in case of some

provisions outcomes are uncertain. Hence, different outputs can be obtained by individuals on

application of specific provisions on books of accounts. Provisions that are related to warranty

are best example in this regard where firms at their own discretion take steps to deal with

situation (Jupe, and et.al., 2014). Other main limitation of mentioend standard is that it does not

5 | P a g e

million,0.87 million and D is valued at 5.42 million.

3 Problem arriving at valuation of ship

There were problem that were faced while doing valuation of ship. Problem was that it

was hard to estimate discount rate. In case wrong discount rate is taken in to account asset may

be valued at wrong value. Hence, it is very important to estimate accurate discount rate to

estimate value of any asset.

Question 2

1Critical evaluation of IAS 37 provisions

There are few limitations of IAS 37 as it is related to contingent liabilities and contingent

assets. Like it can be seen that in case of accounting standards there are some limitations and in

present case also it is identified that there are some limitations of IAS 37. There is significent

scope of manipulation of earning in the books of accounts if IAS37. For example under

provisions of IAS 37 firms can make provisions for future costs which are not obligation for the

firm in current time period (Firoz and Ansari, 2010). Apart from this, IAS 37 only allows

provisions which meet definition of liability. Such kind of aspects of IAS 37 are not considered

good and there is need to make modification in it. There are many other shortcomings in the IAS

37 and due to this reason IASB is considering to make changes in IAS 37. There are some

guidelines that are given in mentioned standard but same are difficult to understand and it

become hard for one to identify liability. Recogniition that is done in the relevant standard are

also questionable in nature. In other words it can be said that threshold that is determined in

standard are also not clear. This is one of the main limitation of the named standard and need to

be improved on time so that accounting can be done in systematic manner (Jaweher and

Mounira, 2014). Some of measurement requirements are also given in the IASB but same are

very unclear in nature. Hence, it can be said that there are huge limitations of IAS 37 and there

are lots of areas where improvements need to be made in the standard.

There is also lack of consistency in the standard as it can be observed that in case of some

provisions outcomes are uncertain. Hence, different outputs can be obtained by individuals on

application of specific provisions on books of accounts. Provisions that are related to warranty

are best example in this regard where firms at their own discretion take steps to deal with

situation (Jupe, and et.al., 2014). Other main limitation of mentioend standard is that it does not

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

state whether provisions of IAS 37 must include provisions in respect to legal cost which is

incurred by an individual when settlement of claim happened. It is also observed that in

mentioned standard there is recognition criteria under which main emphasis is given on probable

outflow criterion. Just be considering probability cash flows can not be estimated and same can

not be taken in to accounting. In order to make standard consistent it is very important to make

necessary changes in same so that accurately accounting can be done and items measured at

correct value in books of accounts. In IAS 37 it is clearly stated that risk and uncertainity must

be considered in order to envisage provision. There was need to determine nature of risk that

must be taken in to account for doing necessary adjustments in books of accounts.

It can be said that there are some of limitations of the IAS 37 but there are multiple

positive side of the mentioned standard as it is used by the business firms to keep proper track

record of assets and liabilities in business (Daske and et.al., 2013). There is vast scope of the

mentioned accounting standard and due to this reason it is used regulalrly by the business firms

for accounting purpose. Time to time many changes were made in these standards and due to this

reason IAS 37 get evolved to great extent. It can be said that mentioned standard have both

positive and negative sides.

2.a Treatment of provision in books of accounts

Provision refers to the specific amount that is kept aside by the business firm to meet its

liability. As per rules it is necessary for the business firm to ensure that for most of liabilities it

prepared provision. As part of treatmet actual expenses that are made by the firm in its business

are deducted from provisiion amount. Then remaining amount of provision amount is carry

forward to next year income statement. Means that portion of money that was kept aside is used

next year to meet requirements (Gordon and Gallery, 2012). It can be said that there is great

importance of provision for the business firms because provision help firm in managing risk in

the business and identifying profit amount that can be earned in the business. There are most of

firms that prepare provision in respect to varied liabilities. This reflects that there is huge

importance of preparing provision for business firms.

There are some limitations of provisions as it allow business firms to manipulate profit

amount. Many times business firms show large amount of provision amount in their books of

accounts and actual expenses are very less. Due to this reason less amount of profit is revealed in

the books of accounts and firms have to pay less income tax (Fifield and et.al., 2011). Thus, it

6 | P a g e

incurred by an individual when settlement of claim happened. It is also observed that in

mentioned standard there is recognition criteria under which main emphasis is given on probable

outflow criterion. Just be considering probability cash flows can not be estimated and same can

not be taken in to accounting. In order to make standard consistent it is very important to make

necessary changes in same so that accurately accounting can be done and items measured at

correct value in books of accounts. In IAS 37 it is clearly stated that risk and uncertainity must

be considered in order to envisage provision. There was need to determine nature of risk that

must be taken in to account for doing necessary adjustments in books of accounts.

It can be said that there are some of limitations of the IAS 37 but there are multiple

positive side of the mentioned standard as it is used by the business firms to keep proper track

record of assets and liabilities in business (Daske and et.al., 2013). There is vast scope of the

mentioned accounting standard and due to this reason it is used regulalrly by the business firms

for accounting purpose. Time to time many changes were made in these standards and due to this

reason IAS 37 get evolved to great extent. It can be said that mentioned standard have both

positive and negative sides.

2.a Treatment of provision in books of accounts

Provision refers to the specific amount that is kept aside by the business firm to meet its

liability. As per rules it is necessary for the business firm to ensure that for most of liabilities it

prepared provision. As part of treatmet actual expenses that are made by the firm in its business

are deducted from provisiion amount. Then remaining amount of provision amount is carry

forward to next year income statement. Means that portion of money that was kept aside is used

next year to meet requirements (Gordon and Gallery, 2012). It can be said that there is great

importance of provision for the business firms because provision help firm in managing risk in

the business and identifying profit amount that can be earned in the business. There are most of

firms that prepare provision in respect to varied liabilities. This reflects that there is huge

importance of preparing provision for business firms.

There are some limitations of provisions as it allow business firms to manipulate profit

amount. Many times business firms show large amount of provision amount in their books of

accounts and actual expenses are very less. Due to this reason less amount of profit is revealed in

the books of accounts and firms have to pay less income tax (Fifield and et.al., 2011). Thus, it

6 | P a g e

can be said that provision allow manipulation of values in books of accounts. It is one of major

shortcoming of the mentioned method for the businesss firms. There are two situations under

which there is a firm that consistently receive order from same client. Whereras, there is other

firm that receive order on contractual basis. In present case firm is operating construction

business and it receive order on contractual basis. Hence, in case project get completed in current

time period then in that case amount of provision can not be carry forward to next financial year

because project will be completed in current time period. Hence, in that case firms separately

show unused amount of provision separatrely in books of accounts and add it to profit amount.

Thus, profit amount exaggerated in the income statement of the business firm.

There are number of steps in which accounting for provision is done recognition of

provision, unwinding the discount, utilization of provision, reimbursement. In case of

recognition, provision must be recognized in profit or loss or within cost of another assets (Barbu

and et.al., 2014). In case it is identified that provision is for more then 12 months then in that

case discounting of provision is done and it is recorded at its present value. Means thad even

provision will be used in next year time period but it will be discounted and its value will be

shown for current time period. When any business firm make any sort of expenses that are

related to settlement of obligation then in that case provision can be used. Utilization of

provision is recognized directly when invoice is received from suppliers. In case of any event

any reimbursement takes place then in that case same can not be considered as separate asset.

However, company can net off expenditure that are related to provision with income from

reimbursement.

There are some specific situations in which provisions can be treated in specific manner

like in case of future operating losses and onerous assets. In case of future operating losses one

can not make provision because in association of same no past event occur. Provision can be

preparedn as per rules in case of any specific variable only which there is any relationship

between past and present event (Fifield, and et.al., 2011). It is possible to avoid any future loss

by considering future profit amount. In case of onerous contract also there is specific treatment

of provision. These are those contracts on which loss can be avoided. It can be said that there is

wide scope of provisions and for different sort of situations varied treatement of same is done in

books of accounts.

7 | P a g e

shortcoming of the mentioned method for the businesss firms. There are two situations under

which there is a firm that consistently receive order from same client. Whereras, there is other

firm that receive order on contractual basis. In present case firm is operating construction

business and it receive order on contractual basis. Hence, in case project get completed in current

time period then in that case amount of provision can not be carry forward to next financial year

because project will be completed in current time period. Hence, in that case firms separately

show unused amount of provision separatrely in books of accounts and add it to profit amount.

Thus, profit amount exaggerated in the income statement of the business firm.

There are number of steps in which accounting for provision is done recognition of

provision, unwinding the discount, utilization of provision, reimbursement. In case of

recognition, provision must be recognized in profit or loss or within cost of another assets (Barbu

and et.al., 2014). In case it is identified that provision is for more then 12 months then in that

case discounting of provision is done and it is recorded at its present value. Means thad even

provision will be used in next year time period but it will be discounted and its value will be

shown for current time period. When any business firm make any sort of expenses that are

related to settlement of obligation then in that case provision can be used. Utilization of

provision is recognized directly when invoice is received from suppliers. In case of any event

any reimbursement takes place then in that case same can not be considered as separate asset.

However, company can net off expenditure that are related to provision with income from

reimbursement.

There are some specific situations in which provisions can be treated in specific manner

like in case of future operating losses and onerous assets. In case of future operating losses one

can not make provision because in association of same no past event occur. Provision can be

preparedn as per rules in case of any specific variable only which there is any relationship

between past and present event (Fifield, and et.al., 2011). It is possible to avoid any future loss

by considering future profit amount. In case of onerous contract also there is specific treatment

of provision. These are those contracts on which loss can be avoided. It can be said that there is

wide scope of provisions and for different sort of situations varied treatement of same is done in

books of accounts.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.b Case of contingent assets

Contingenet asset is one under which those assets come that originate suddenly due to

happening of certain event. According to IAS 37 there are some conditions that must be

considered before considering any asset as contingent asset. As per IAS 37 rules claim outcome

that a company made through legal process can be considered as contingent asset when final

outcome of the claim that is made is uncertain. Means that any asset will be considered as

contingent asset when outcome of claim made in uncertain whether claim will result in cash

inflow or not. In such kind of situation if benefit is made then it can be assumed as contingent

asset (Provisions, contingent liabilities and current assets, 2017). There is no specific treatment

of contingent assets because same occurred suddenly and it is not dislosed in the company books

of accounts. Amount of contingent asset need to be shown in reports that are individually

approved by Board of Directors.

CONCLUSION

On the basis of above discussion it is concluded that asset must be valued at fair value

because same are included in the asset. In the balance sheet assets and liability both show firm

financial position. In case an asset valued at greater amount then in that case balance sheet may

show wrong financial position of the business firm. all relevant rules must be followed while

preparing provisions and current assets as well as current liability. By doing so real picture of the

firm financial position can be obtained by the business firm.

8 | P a g e

Contingenet asset is one under which those assets come that originate suddenly due to

happening of certain event. According to IAS 37 there are some conditions that must be

considered before considering any asset as contingent asset. As per IAS 37 rules claim outcome

that a company made through legal process can be considered as contingent asset when final

outcome of the claim that is made is uncertain. Means that any asset will be considered as

contingent asset when outcome of claim made in uncertain whether claim will result in cash

inflow or not. In such kind of situation if benefit is made then it can be assumed as contingent

asset (Provisions, contingent liabilities and current assets, 2017). There is no specific treatment

of contingent assets because same occurred suddenly and it is not dislosed in the company books

of accounts. Amount of contingent asset need to be shown in reports that are individually

approved by Board of Directors.

CONCLUSION

On the basis of above discussion it is concluded that asset must be valued at fair value

because same are included in the asset. In the balance sheet assets and liability both show firm

financial position. In case an asset valued at greater amount then in that case balance sheet may

show wrong financial position of the business firm. all relevant rules must be followed while

preparing provisions and current assets as well as current liability. By doing so real picture of the

firm financial position can be obtained by the business firm.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Aljinović Barać, Ž. and Šodan, S., 2011. Motives for asset revaluation policy choice in Croatia.

Croatian Operational Research Review. 2(1). pp.60-70.

Barbu, E.M. and et.al., 2014. Mandatory environmental disclosures by companies complying

with IASs/IFRSs: The cases of France, Germany, and the UK. The International Journal of

Accounting. 49(2). pp.231-247.

Boterashvili, M. and et.al., 2012. Integrated and Segregated Au/γ‐Fe2O3 Binary Nanoparticle

Assemblies. Angewandte Chemie International Edition. 51(49). pp.12268-12271.

Cairns, D. and et.al., 2011. IFRS fair value measurement and accounting policy choice in the

United Kingdom and Australia. The British Accounting Review. 43(1). pp.1-21.

Damian, M.I. and et.al., 2014. Bearer plants: Stakeholders' view. Accounting and Management

Information Systems. 13(4). p.719.

Daske, H. and et.al., 2013. Adopting a label: Heterogeneity in the economic consequences

around IAS/IFRS adoptions. Journal of Accounting Research. 51(3). pp.495-547.

Fifield, S. and et.al., 2011. A cross-country analysis of IFRS reconciliation statements. Journal

of Applied Accounting Research. 12(1). pp.26-42.

Fifield, S. and et.al., 2011. A cross-country analysis of IFRS reconciliation statements. Journal

of Applied Accounting Research. 12(1). pp.26-42.

Firoz, C.M. and Ansari, A.A., 2010. Environmental accounting and international financial

reporting standards (IFRS). International Journal of Business and Management. 5(10).

p.105.

Gordon, I. and Gallery, N., 2012. Assessing financial reporting comparability across institutional

settings: The case of pension accounting. The British Accounting Review. 44(1). pp.11-20.

Jaweher, B. and Mounira, B.A., 2014. The effects of mandatory IAS/IFRS regulation on the

properties of earnings’ quality in Australia and Europe. European Journal of Business and

Management. 6(3). pp.92-111.

Jupe, A., Këri, L., Biracaj, R. and Taka, A., 2014. Accounting for Environmental Liabilities–

Case of Albania. Academic Journal of Interdisciplinary Studies. 3(3). p.283.

Rattenbacher, B. and et.al, 2010. Analysis of CUGBP1 targets identifies GU-repeat sequences

that mediate rapid mRNA decay. Molecular and cellular biology. 30(16). pp.3970-3980.

9 | P a g e

Books and Journals

Aljinović Barać, Ž. and Šodan, S., 2011. Motives for asset revaluation policy choice in Croatia.

Croatian Operational Research Review. 2(1). pp.60-70.

Barbu, E.M. and et.al., 2014. Mandatory environmental disclosures by companies complying

with IASs/IFRSs: The cases of France, Germany, and the UK. The International Journal of

Accounting. 49(2). pp.231-247.

Boterashvili, M. and et.al., 2012. Integrated and Segregated Au/γ‐Fe2O3 Binary Nanoparticle

Assemblies. Angewandte Chemie International Edition. 51(49). pp.12268-12271.

Cairns, D. and et.al., 2011. IFRS fair value measurement and accounting policy choice in the

United Kingdom and Australia. The British Accounting Review. 43(1). pp.1-21.

Damian, M.I. and et.al., 2014. Bearer plants: Stakeholders' view. Accounting and Management

Information Systems. 13(4). p.719.

Daske, H. and et.al., 2013. Adopting a label: Heterogeneity in the economic consequences

around IAS/IFRS adoptions. Journal of Accounting Research. 51(3). pp.495-547.

Fifield, S. and et.al., 2011. A cross-country analysis of IFRS reconciliation statements. Journal

of Applied Accounting Research. 12(1). pp.26-42.

Fifield, S. and et.al., 2011. A cross-country analysis of IFRS reconciliation statements. Journal

of Applied Accounting Research. 12(1). pp.26-42.

Firoz, C.M. and Ansari, A.A., 2010. Environmental accounting and international financial

reporting standards (IFRS). International Journal of Business and Management. 5(10).

p.105.

Gordon, I. and Gallery, N., 2012. Assessing financial reporting comparability across institutional

settings: The case of pension accounting. The British Accounting Review. 44(1). pp.11-20.

Jaweher, B. and Mounira, B.A., 2014. The effects of mandatory IAS/IFRS regulation on the

properties of earnings’ quality in Australia and Europe. European Journal of Business and

Management. 6(3). pp.92-111.

Jupe, A., Këri, L., Biracaj, R. and Taka, A., 2014. Accounting for Environmental Liabilities–

Case of Albania. Academic Journal of Interdisciplinary Studies. 3(3). p.283.

Rattenbacher, B. and et.al, 2010. Analysis of CUGBP1 targets identifies GU-repeat sequences

that mediate rapid mRNA decay. Molecular and cellular biology. 30(16). pp.3970-3980.

9 | P a g e

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.