JCU LB5235 Applied Research Project: AIS Evolution Report and Analysis

VerifiedAdded on 2022/12/14

|16

|3312

|92

Report

AI Summary

This report examines the evolution of Accounting Information Systems (AIS) and its impact on organizational effectiveness. The research employs a quantitative methodology, utilizing questionnaire surveys with business managers and interviews with accountants. Data analysis techniques, including correlation and regression, are applied to assess the relationship between AIS and task efficiency, with auditing and controlling identified as key independent variables. The study identifies barriers to AIS implementation, such as strategy formulation, environment, and organizational structure. The findings reveal a positive correlation between AIS and organizational effectiveness, suggesting that improvements in AIS can enhance auditing and controlling functions. The report also provides a timeline of the research activities and discusses risk management considerations. The study concludes that AIS is crucial for all types of business organizations and offers significant benefits, including enhanced financial transaction management and improved decision-making processes, while also acknowledging the limitations of AIS such as risk of data loss and the complexity of implementation.

1The Evolution of Accounting Information System

Running head: THE EVOLUTION OF ACCOUNTING INFORMATION SYSTEM

The Evolution of Accounting Information System

Author’s Name

Institutional Affiliation

Running head: THE EVOLUTION OF ACCOUNTING INFORMATION SYSTEM

The Evolution of Accounting Information System

Author’s Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2The Evolution of Accounting Information System

The Evolution of Accounting Information System

Assessment Task 3: Data Analysis

Methods

An accounting information system (AIS) is considered as a formal procedure to collect

relevant data. It plays a critical function in processing raw information and distributing the

same to the respective users. The main aim of AIS is to collect financial as well as accounting

data that are distributed to the managers in terms of informational reports (accountingedu.org,

n.d.). It is believed that proper recognition and monitoring AIS may support the business

corporations of this present day context to develop their respective internal functions by an

extensive level. According to the given subject matter related to accounting, an ideal data has

been mainly collected and analyzed for this particular research. Conceptually, an ideal data

can be defined as the appropriate data, which has valuable information regarding a specific

topic. This ideal data can help in performing data analysis, which promotes organizational

effectiveness.

In general, there are three types of research methodology that comprise qualitative,

mixed and quantitative. In this study, quantitative methodology has been mainly utilized in

order to draw valid inferences and reach into pertinent conclusions. Qualitative research is a

procedure of natural policy, which enhances in-depth understanding of any particular subject.

It generally aims at “why” rather than “what” and deals with direct experiences of human

beings.. On the other hand, quantitative research deals with the measurement and the

numbers, which enables the researchers to study on the selected issues by addressing the

predetermined study aim along with objectives. Finally, mixed research approach is the

combination of qualitative as well as quantitative researches, which also supports into

drawing valid inferences (University of Utah, n.d.).

The Evolution of Accounting Information System

Assessment Task 3: Data Analysis

Methods

An accounting information system (AIS) is considered as a formal procedure to collect

relevant data. It plays a critical function in processing raw information and distributing the

same to the respective users. The main aim of AIS is to collect financial as well as accounting

data that are distributed to the managers in terms of informational reports (accountingedu.org,

n.d.). It is believed that proper recognition and monitoring AIS may support the business

corporations of this present day context to develop their respective internal functions by an

extensive level. According to the given subject matter related to accounting, an ideal data has

been mainly collected and analyzed for this particular research. Conceptually, an ideal data

can be defined as the appropriate data, which has valuable information regarding a specific

topic. This ideal data can help in performing data analysis, which promotes organizational

effectiveness.

In general, there are three types of research methodology that comprise qualitative,

mixed and quantitative. In this study, quantitative methodology has been mainly utilized in

order to draw valid inferences and reach into pertinent conclusions. Qualitative research is a

procedure of natural policy, which enhances in-depth understanding of any particular subject.

It generally aims at “why” rather than “what” and deals with direct experiences of human

beings.. On the other hand, quantitative research deals with the measurement and the

numbers, which enables the researchers to study on the selected issues by addressing the

predetermined study aim along with objectives. Finally, mixed research approach is the

combination of qualitative as well as quantitative researches, which also supports into

drawing valid inferences (University of Utah, n.d.).

3The Evolution of Accounting Information System

From the perspective of data collection method, primary information has been mainly

gathered for this specific research by conducting questionnaire survey with the business

managers of varied organizations and interview with the accountants in particular. In this

case, primary data refers to the information, which is mainly collected by the researchers

themselves. This kind of data is information oriented, which supports into deriving favorable

outcomes (Lotame Solutions, 2019). A total of ten (10) close-ended questions have been

designed for this particular quantitative research with the intention of addressing the issue

identified for this research. In relation to the study, the entire results have been presented in

SPSS format that are analyzed through correlation and regression.

Correlation is viewed to be a statistical tool of measuring the association existing

between two variables. These two variables are independent and dependent. The value of a

correlation coefficient can be differed from the value minus one to plus one. Conceptually, a

minus one value signifies an ideal negative correlation. On the other hand, a plus one

represents an ideal positive correlation. However, a correlation value of zero indicates there is

no relation between two variables. Negative correlation defines that if the value of one

variable increases, the value of the other variable tends to decrease. Conversely, a positive

correlation value indicates the fact that when the value of one variable increases, the value of

the other variable also enlarges as well (StatPac Inc, 2017). Similarly, regression analysis

enables to gain comprehensive insights that can be applied for the improvement of products

and/or services. In relation to the given study, this analysis enables to understand and

determine the strength of the relationship existing amid the two variables. To be precise,

regression analysis helps to understand the organizations to establish the degree in which

specific independent variables influencing dependent variables (Gallo, 2015).

In this study, “task efficiency” is considered as the dependent variable, whereas

“auditing and controlling” is termed as the independent variable. Thus, increasing in the task

From the perspective of data collection method, primary information has been mainly

gathered for this specific research by conducting questionnaire survey with the business

managers of varied organizations and interview with the accountants in particular. In this

case, primary data refers to the information, which is mainly collected by the researchers

themselves. This kind of data is information oriented, which supports into deriving favorable

outcomes (Lotame Solutions, 2019). A total of ten (10) close-ended questions have been

designed for this particular quantitative research with the intention of addressing the issue

identified for this research. In relation to the study, the entire results have been presented in

SPSS format that are analyzed through correlation and regression.

Correlation is viewed to be a statistical tool of measuring the association existing

between two variables. These two variables are independent and dependent. The value of a

correlation coefficient can be differed from the value minus one to plus one. Conceptually, a

minus one value signifies an ideal negative correlation. On the other hand, a plus one

represents an ideal positive correlation. However, a correlation value of zero indicates there is

no relation between two variables. Negative correlation defines that if the value of one

variable increases, the value of the other variable tends to decrease. Conversely, a positive

correlation value indicates the fact that when the value of one variable increases, the value of

the other variable also enlarges as well (StatPac Inc, 2017). Similarly, regression analysis

enables to gain comprehensive insights that can be applied for the improvement of products

and/or services. In relation to the given study, this analysis enables to understand and

determine the strength of the relationship existing amid the two variables. To be precise,

regression analysis helps to understand the organizations to establish the degree in which

specific independent variables influencing dependent variables (Gallo, 2015).

In this study, “task efficiency” is considered as the dependent variable, whereas

“auditing and controlling” is termed as the independent variable. Thus, increasing in the task

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4The Evolution of Accounting Information System

efficiency can raise the auditing and the task controlling levels at large. Based on the

questionnaire designed for this particular research, it has been apparent that both

demographic and qualitative based questions have been prepared in order to generate suitable

results. A 5 point Likert Scale method has been utilized for this research, which is coded in

the forms of 1, 2, 3 , 4 and 5. These coded forms signify ‘strongly agree’, ‘agree’, ‘neutral’,

‘disagree’ and ‘strongly disagree’ respectively.

There are certain barriers of implementation that have been identified with respect to

the issue identified for this research. The issue in this context is identified as investigating the

relationship existing amid AIS and organizational effectiveness. One of such barriers is

Strategy Formulation, which involves the decision to shape the path of an organization. The

implementation stage is generally considered to be the realization process of strategy, which

is mainly developed in the formulation phase. It is argued that if the formulation stage is not

evaluated well, it will adversely impact the implementation phase, creating barriers for

smooth execution in the procedure of generating relevant data. In case of implementation and

formulation procedures, there is a tendency to perform different activities related to a

research separately by the different groups of the people. Moreover, many people within the

organizations play a major role in the businesses. Furthermore, there is possibility of unaware

of the efforts and the information that basically deal with the formulation process.

Apart from Strategy Formulation, Environment can be duly considered as the other

implementation barrier for any specific research. It is obvious that the changes in the

environment are considered to be the organizational transformation. Thus, the organizations

are needed to assess the suitable implementation strategies. These should be applicable when

there is a change in the environment. Thus, it should be keep in mind that organizations

should be aware of the things that are going on within the environment. If crucial changes are

observed then an organization should react to these changes promptly and therefore apply

efficiency can raise the auditing and the task controlling levels at large. Based on the

questionnaire designed for this particular research, it has been apparent that both

demographic and qualitative based questions have been prepared in order to generate suitable

results. A 5 point Likert Scale method has been utilized for this research, which is coded in

the forms of 1, 2, 3 , 4 and 5. These coded forms signify ‘strongly agree’, ‘agree’, ‘neutral’,

‘disagree’ and ‘strongly disagree’ respectively.

There are certain barriers of implementation that have been identified with respect to

the issue identified for this research. The issue in this context is identified as investigating the

relationship existing amid AIS and organizational effectiveness. One of such barriers is

Strategy Formulation, which involves the decision to shape the path of an organization. The

implementation stage is generally considered to be the realization process of strategy, which

is mainly developed in the formulation phase. It is argued that if the formulation stage is not

evaluated well, it will adversely impact the implementation phase, creating barriers for

smooth execution in the procedure of generating relevant data. In case of implementation and

formulation procedures, there is a tendency to perform different activities related to a

research separately by the different groups of the people. Moreover, many people within the

organizations play a major role in the businesses. Furthermore, there is possibility of unaware

of the efforts and the information that basically deal with the formulation process.

Apart from Strategy Formulation, Environment can be duly considered as the other

implementation barrier for any specific research. It is obvious that the changes in the

environment are considered to be the organizational transformation. Thus, the organizations

are needed to assess the suitable implementation strategies. These should be applicable when

there is a change in the environment. Thus, it should be keep in mind that organizations

should be aware of the things that are going on within the environment. If crucial changes are

observed then an organization should react to these changes promptly and therefore apply

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5The Evolution of Accounting Information System

relevant strategies to raise organizational effectiveness. The importance of environment to an

organization mainly portrays the actions through which the underlying environment gets

affected during the operations (Tan, 2004).

However, organization structure is also one of the barriers, which is faced by the

organizations during the conduct of operations. This barrier is related to the dimension of

strategic management and is thus considered to be a vital variable for a study. It is worth

mentioning that organization structure is defined as one of those variables, which leads

towards the attainment of desired goals. There is a huge scope for the organizations to use

AIS in their respective businesses so that they can keep their accounting records safe and

maintain the workflow as per the expectation level. The database of the system is basically

secured compared to the other system. This accounting system is used in various steps. It

mainly deals with the financial transactions of a business concern. Also, the accounting

system i.e. AIS is necessary for all types of business organizations operating in this present

day context. Moreover, it is also useful for the individuals and the families as well

(VanBarenm, 2017).

One of the major functions of accounting is to keep the accounts updated with the

financial transactions. In addition, all the financial activities of the individuals, business

concerns and semi government organizations appear under the scope of accounting.

Financial transactions have major importance in the domain of AIS, which has some

limitations as well. For instance, there is a risk of losing the information through the power

outage. An accounting information system is complicated to set up because every

organization has a different set up and follow diverse procedures in order to generate positive

outcomes (VanBarenm, 2017).

relevant strategies to raise organizational effectiveness. The importance of environment to an

organization mainly portrays the actions through which the underlying environment gets

affected during the operations (Tan, 2004).

However, organization structure is also one of the barriers, which is faced by the

organizations during the conduct of operations. This barrier is related to the dimension of

strategic management and is thus considered to be a vital variable for a study. It is worth

mentioning that organization structure is defined as one of those variables, which leads

towards the attainment of desired goals. There is a huge scope for the organizations to use

AIS in their respective businesses so that they can keep their accounting records safe and

maintain the workflow as per the expectation level. The database of the system is basically

secured compared to the other system. This accounting system is used in various steps. It

mainly deals with the financial transactions of a business concern. Also, the accounting

system i.e. AIS is necessary for all types of business organizations operating in this present

day context. Moreover, it is also useful for the individuals and the families as well

(VanBarenm, 2017).

One of the major functions of accounting is to keep the accounts updated with the

financial transactions. In addition, all the financial activities of the individuals, business

concerns and semi government organizations appear under the scope of accounting.

Financial transactions have major importance in the domain of AIS, which has some

limitations as well. For instance, there is a risk of losing the information through the power

outage. An accounting information system is complicated to set up because every

organization has a different set up and follow diverse procedures in order to generate positive

outcomes (VanBarenm, 2017).

6The Evolution of Accounting Information System

Results

The questionnaire survey had been performed with fifty (50) business managers of

different organizations that follow AIS in their respective operations. On the other hand,

interviews were conducted with 5 accountants who carry out accounting related activities on

behalf of varied business corporations. In this particular section of the research, initially, the

qualitative results obtained through interviews have been discussed, followed by the

outcomes generated via survey questionnaire. According to the interview question number 1

(see Appendix 2), Respondent 1 stated that he has been following and using the traditional

AIS method to conduct the accounting operations since the last 3-4 years. On the other hand,

Respondent 2 did not provide any response. Similarly, Respondent 3 stated the same thing as

similar to Respondent 2. However, Respondents 4 and 5 mentioned that they are new to the

organization and yet not started to follow and use the traditional AIS method to perform the

respective accounting functions.

The second interview question number 2 (see Appendix 2) was framed in order to

determine the reasons for which the traditional AIS procedure is executed in the accounting

practices. In response, Interviewee 1 stated that the reason was to achieve the sales goals.

However, Respondent 2 stated that AIS simplifies the information, which enhances

organizational efficiency. Interviewee 3 also agreed on the response provided by Respondent

2. On the other hand, Respondents 4 and 5 agreed on the fact and stated that the accounting

system (AIS) helps in controlling the internal functions of the firm. The third interview

question (see Appendix 2) was based on how traditional AIS can support an individual to

determine and improve organizational effectiveness. In this case, Respondent 1 stated that it

is useful for making right decisions, whereas Respondent 2 stated that it helps in making

financial transactions successfully. However, Respondent 3 agreed on the fact and stated that

Results

The questionnaire survey had been performed with fifty (50) business managers of

different organizations that follow AIS in their respective operations. On the other hand,

interviews were conducted with 5 accountants who carry out accounting related activities on

behalf of varied business corporations. In this particular section of the research, initially, the

qualitative results obtained through interviews have been discussed, followed by the

outcomes generated via survey questionnaire. According to the interview question number 1

(see Appendix 2), Respondent 1 stated that he has been following and using the traditional

AIS method to conduct the accounting operations since the last 3-4 years. On the other hand,

Respondent 2 did not provide any response. Similarly, Respondent 3 stated the same thing as

similar to Respondent 2. However, Respondents 4 and 5 mentioned that they are new to the

organization and yet not started to follow and use the traditional AIS method to perform the

respective accounting functions.

The second interview question number 2 (see Appendix 2) was framed in order to

determine the reasons for which the traditional AIS procedure is executed in the accounting

practices. In response, Interviewee 1 stated that the reason was to achieve the sales goals.

However, Respondent 2 stated that AIS simplifies the information, which enhances

organizational efficiency. Interviewee 3 also agreed on the response provided by Respondent

2. On the other hand, Respondents 4 and 5 agreed on the fact and stated that the accounting

system (AIS) helps in controlling the internal functions of the firm. The third interview

question (see Appendix 2) was based on how traditional AIS can support an individual to

determine and improve organizational effectiveness. In this case, Respondent 1 stated that it

is useful for making right decisions, whereas Respondent 2 stated that it helps in making

financial transactions successfully. However, Respondent 3 agreed on the fact and stated that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7The Evolution of Accounting Information System

it increases the organizational performance. Moreover, Respondents 4 and 5 stated that this

approach enhances the knowledge management.

As per question number 4 of the interview (see appendix 2), interviewee 1 responded

that AIS is a new approach for enhancing the effectiveness of the organization. On the other

hand, Respondent 2 agreed on the opinion of Respondent 1. Respondent 3 stated that AIS

system has association with the computer assisted auditing tools and techniques. Moreover,

Respondent 4 stated that AIS system is useful for forecasting. Respondent 5 stated that AIS

system enables the business intelligence, which helps in raising organizational effectiveness.

In accordance with question number 5 of the interview (see appendix 2), Respondent 1 stated

that by innovating new approaches, AIS will contribute to the organizational effectiveness.

Respondent 2 also agreed on the opinion of respondent 1. However, Respondent 3 stated that

big data model can be approached to the AIS system for enhancing the organizational

effectiveness. Lastly, Respondents 4 and 5 mentioned about the cloud computing approach,

which can be used in the AIS system.

The correlation and regression results obtained for this study have been portrayed

hereunder.

it increases the organizational performance. Moreover, Respondents 4 and 5 stated that this

approach enhances the knowledge management.

As per question number 4 of the interview (see appendix 2), interviewee 1 responded

that AIS is a new approach for enhancing the effectiveness of the organization. On the other

hand, Respondent 2 agreed on the opinion of Respondent 1. Respondent 3 stated that AIS

system has association with the computer assisted auditing tools and techniques. Moreover,

Respondent 4 stated that AIS system is useful for forecasting. Respondent 5 stated that AIS

system enables the business intelligence, which helps in raising organizational effectiveness.

In accordance with question number 5 of the interview (see appendix 2), Respondent 1 stated

that by innovating new approaches, AIS will contribute to the organizational effectiveness.

Respondent 2 also agreed on the opinion of respondent 1. However, Respondent 3 stated that

big data model can be approached to the AIS system for enhancing the organizational

effectiveness. Lastly, Respondents 4 and 5 mentioned about the cloud computing approach,

which can be used in the AIS system.

The correlation and regression results obtained for this study have been portrayed

hereunder.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8The Evolution of Accounting Information System

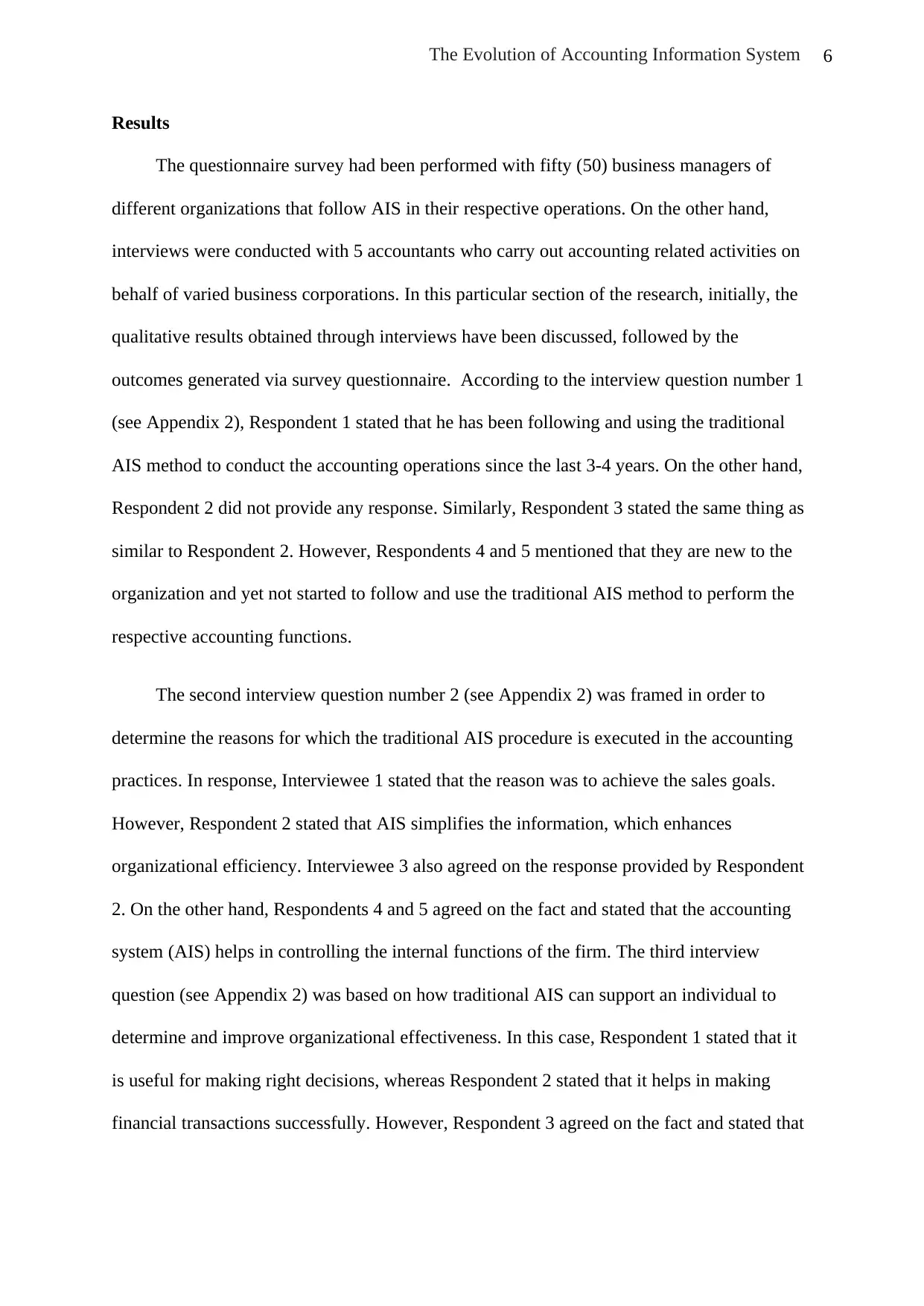

Figure 1: Correlation Results

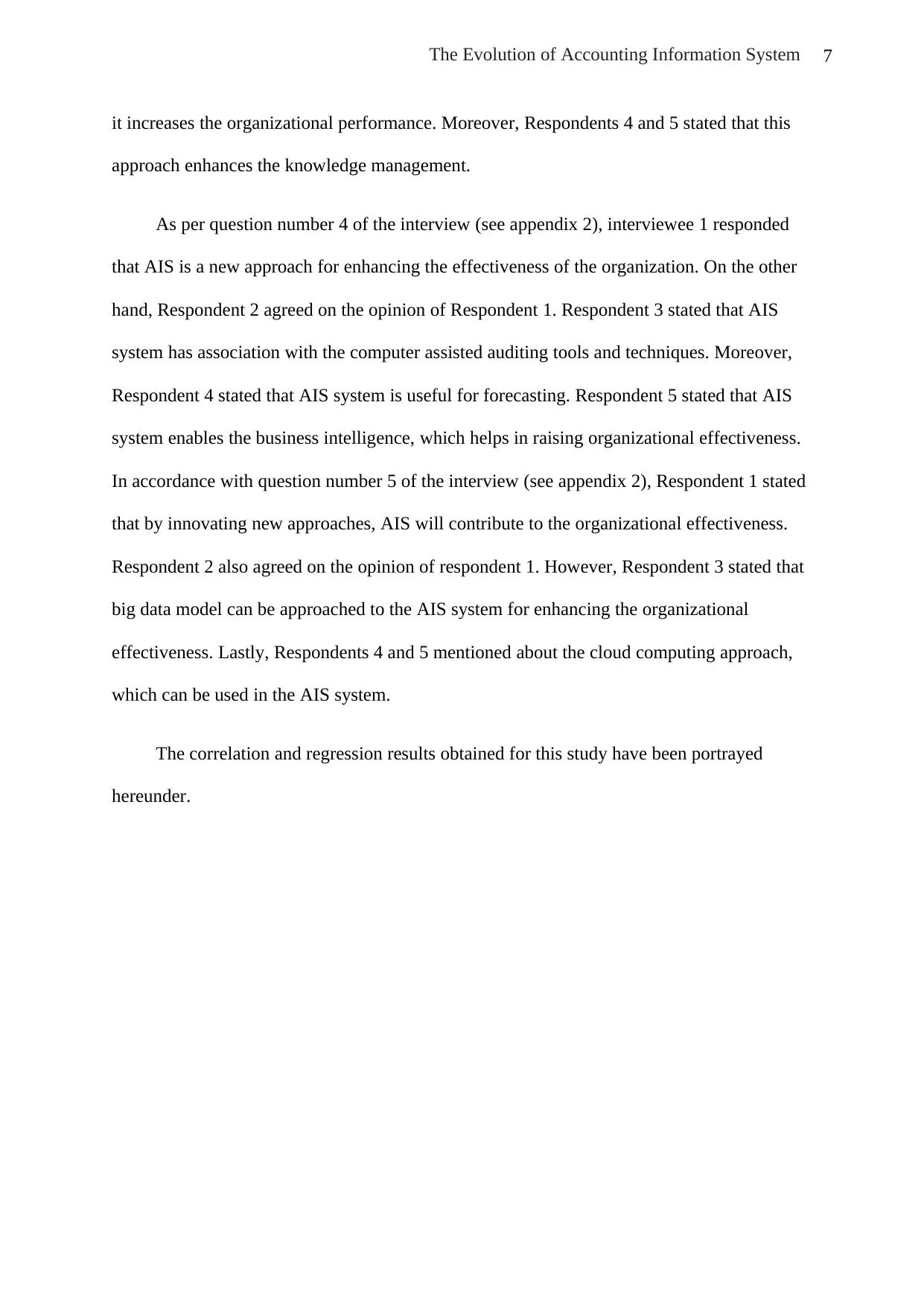

Figure 2: Regression Results

Based on the above two figures wherein the correlation and the R-square values stood

positive and less than 1, it can be affirmed that there exists a direct as well as a strong

relationship amid AIS and organizational effectiveness. By evaluating the regression mode, it

has been observed that the R-square value stood near about 0.910. It entails positive

relationship between the two variables. In simple words, increase in the efficiency of AIS

system can develop auditing and controlling activities of the organizations at large.

Figure 1: Correlation Results

Figure 2: Regression Results

Based on the above two figures wherein the correlation and the R-square values stood

positive and less than 1, it can be affirmed that there exists a direct as well as a strong

relationship amid AIS and organizational effectiveness. By evaluating the regression mode, it

has been observed that the R-square value stood near about 0.910. It entails positive

relationship between the two variables. In simple words, increase in the efficiency of AIS

system can develop auditing and controlling activities of the organizations at large.

9The Evolution of Accounting Information System

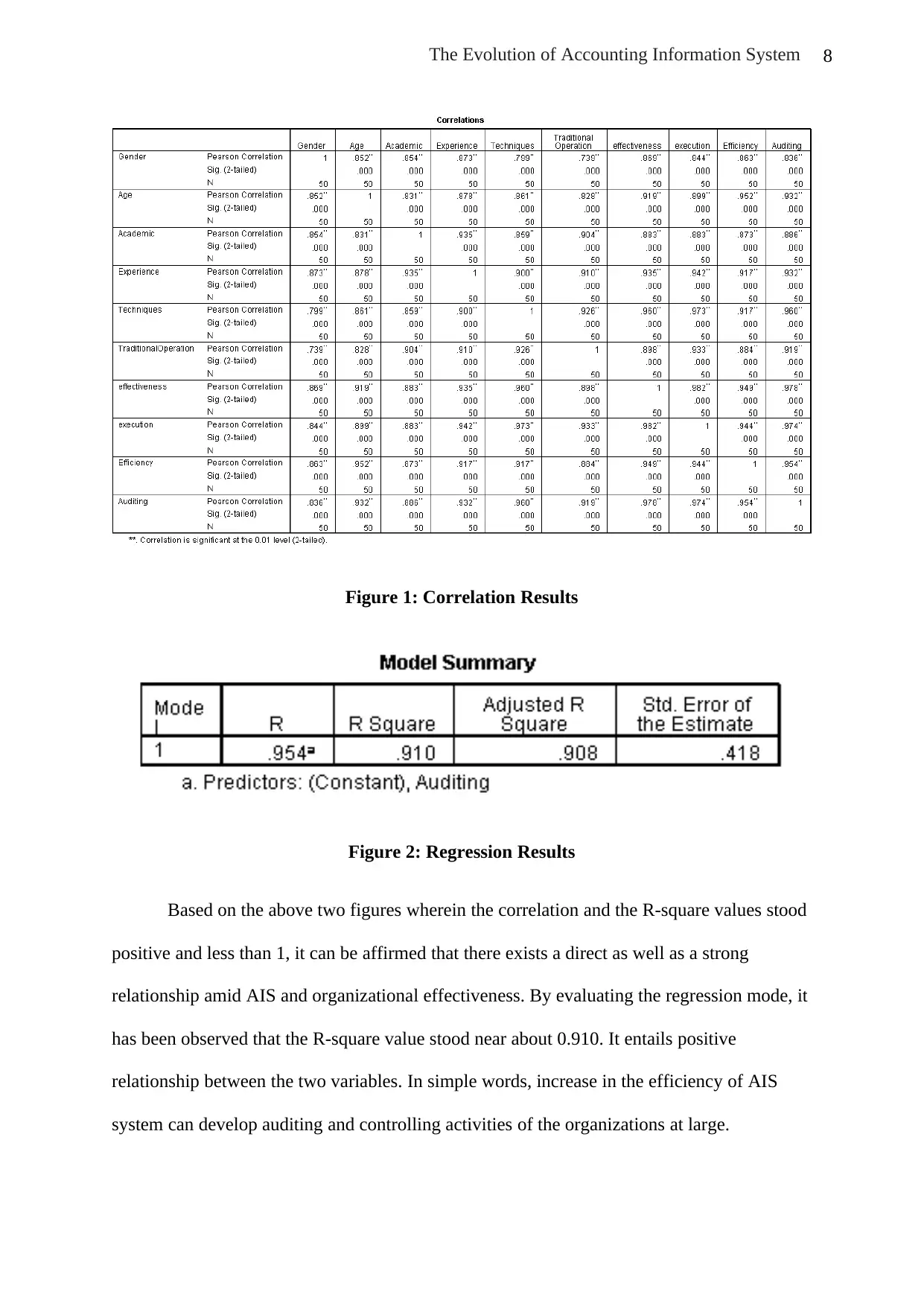

The timeline of the research is provided below:

Activities 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Preliminary Research

Deciding the topic

In depth Research on the topic

Preparation of the proposal

Approval of the proposal

Background search

Writing the introduction chapter

Preparing the literature review

Deciding the methodology

Conducting the question survey

Completing the dissertation

Draft Submission

Getting the feedback of the supervisor

Making required amendment

Final Submission

Figure 3: Timeline

Risk Management

It can be stated that if there is any risk in the accounting information system, it should

be solved initially. At first, the risk should be identified by the researchers or the professional

personnel. After that, it must be analyzed with respect to the outcomes. Modern techniques

should be applied for managing the risks. However, organizations are ought to focus on the

risk response planning. The opportunities for creating the risk mitigation strategies also need

to be analyzed in the study. Risk is considered as a uncertain thing. In this context, risk

management process helps in solving the problems when these emerge at any specific phase.

These problems have been evaluated critically and thereby planned to derive positive

outcomes (Continuing Professional Development, 2014).

Most importantly, a risk can take place within the AIS of an organization, disrupting

its operational efficiency at large. Therefore, the organizations should focus on identifying

the risks and these should be managed before it affects the whole procedure of the accounting

information system. However, the capability of managing the risk may help a company to

raise its operational effectiveness (CareersinAudit.com, 2013).

The timeline of the research is provided below:

Activities 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Preliminary Research

Deciding the topic

In depth Research on the topic

Preparation of the proposal

Approval of the proposal

Background search

Writing the introduction chapter

Preparing the literature review

Deciding the methodology

Conducting the question survey

Completing the dissertation

Draft Submission

Getting the feedback of the supervisor

Making required amendment

Final Submission

Figure 3: Timeline

Risk Management

It can be stated that if there is any risk in the accounting information system, it should

be solved initially. At first, the risk should be identified by the researchers or the professional

personnel. After that, it must be analyzed with respect to the outcomes. Modern techniques

should be applied for managing the risks. However, organizations are ought to focus on the

risk response planning. The opportunities for creating the risk mitigation strategies also need

to be analyzed in the study. Risk is considered as a uncertain thing. In this context, risk

management process helps in solving the problems when these emerge at any specific phase.

These problems have been evaluated critically and thereby planned to derive positive

outcomes (Continuing Professional Development, 2014).

Most importantly, a risk can take place within the AIS of an organization, disrupting

its operational efficiency at large. Therefore, the organizations should focus on identifying

the risks and these should be managed before it affects the whole procedure of the accounting

information system. However, the capability of managing the risk may help a company to

raise its operational effectiveness (CareersinAudit.com, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10The Evolution of Accounting Information System

References

accountingedu.org. (n.d.). What are Accounting Information Systems? Retrieved September 7

2019, from https://www.accountingedu.org/accounting-information-systems.html.

CareersinAudit.com. (2013). The Importance of Risk Management In An Organisation.

Retrieved September 7 2019, from https://www.careersinaudit.com/article/the-

importance-of-risk-management-in-an-organisation

Continuing Professional Development. (2014). What are the 5 Risk Management Steps in a

Sound Risk Management Process? Retrieved September 7 2019, from

https://continuingprofessionaldevelopment.org/risk-management-steps-in-risk-

management-process/

Gallo, A. (2015, November 04). A Refresher on Regression Analysis. Retrieved September 7

2019, from https://hbr.org/2015/11/a-refresher-on-regression-analysis

Lotame Solutions, Inc. (2019, May 13). What Are the Methods of Data Collection? Retrieved

September 7 2019, from https://www.lotame.com/what-are-the-methods-of-data-

collection/#primary

StatPac Inc. (2017). Correlation Types. Retrieved September 7 2019, from

https://www.statpac.com/statistics-calculator/correlation-regression.htm

Tan, Y. T. (2004). Barriers to strategy Implementation: A case study of Air New Zealand.

Auckland University Of technology, 1-177.

University of Utah. (n.d.). What Is Qualitative Research? Retrieved September 7 2019, from

https://nursing.utah.edu/research/qualitative-research/what-is-qualitative-research.php

VanBarenm, J. (2017, September 26). The Disadvantages of Accounting Information

Systems. Retrieved September 7 2019, from https://bizfluent.com/list-6767205-

disadvantages-accounting-information-systems.html

References

accountingedu.org. (n.d.). What are Accounting Information Systems? Retrieved September 7

2019, from https://www.accountingedu.org/accounting-information-systems.html.

CareersinAudit.com. (2013). The Importance of Risk Management In An Organisation.

Retrieved September 7 2019, from https://www.careersinaudit.com/article/the-

importance-of-risk-management-in-an-organisation

Continuing Professional Development. (2014). What are the 5 Risk Management Steps in a

Sound Risk Management Process? Retrieved September 7 2019, from

https://continuingprofessionaldevelopment.org/risk-management-steps-in-risk-

management-process/

Gallo, A. (2015, November 04). A Refresher on Regression Analysis. Retrieved September 7

2019, from https://hbr.org/2015/11/a-refresher-on-regression-analysis

Lotame Solutions, Inc. (2019, May 13). What Are the Methods of Data Collection? Retrieved

September 7 2019, from https://www.lotame.com/what-are-the-methods-of-data-

collection/#primary

StatPac Inc. (2017). Correlation Types. Retrieved September 7 2019, from

https://www.statpac.com/statistics-calculator/correlation-regression.htm

Tan, Y. T. (2004). Barriers to strategy Implementation: A case study of Air New Zealand.

Auckland University Of technology, 1-177.

University of Utah. (n.d.). What Is Qualitative Research? Retrieved September 7 2019, from

https://nursing.utah.edu/research/qualitative-research/what-is-qualitative-research.php

VanBarenm, J. (2017, September 26). The Disadvantages of Accounting Information

Systems. Retrieved September 7 2019, from https://bizfluent.com/list-6767205-

disadvantages-accounting-information-systems.html

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11The Evolution of Accounting Information System

Bibliography

AIS - Aplicaciones de Inteligencia Artificial, S.A. (2019). SCACS risk management platform.

Retrieved September 7 2019, from https://www.ais-int.com/en/financial-services/credit-

risk-management/scacs-risk-management-platform/

Anastasia. (2017 February 26,). Overview of Qualitative And Quantitative Data Collection

Methods. Retrieved September 7 2019, from https://www.cleverism.com/qualitative-

and-quantitative-data-collection-methods/

Chatterjee, S. (2019, Jul 22). A Comprehensive Study of Linear vs Logistic Regression to

refresh the Basics. Retrieved September 7 2019, from

https://towardsdatascience.com/a-comprehensive-study-of-linear-vs-logistic-regression-

to-refresh-the-basics-7e526c1d3ebe

MyAccountingCourse.com. (2019). What is an Accounting Information System? Retrieved

September 7 2019, from

https://www.myaccountingcourse.com/accounting-dictionary/accounting-information-

system

Peavler, R. (2019 June 01). The Business Owner's Guide to Accounting Information Systems.

Retrieved September 7 2019, from https://www.thebalancesmb.com/accounting-

information-systems-392953

Statistics Solutions. (2019). Correlation in SPSS. Retrieved September 7 2019

https://www.statisticssolutions.com/correlation-in-spss/

University Of Connecticut (n.d.). Anova, regression, and chi-square Retrieved September 7

2019, from https://researchbasics.education.uconn.edu/anova_regression_and_chi-

square/#

Bibliography

AIS - Aplicaciones de Inteligencia Artificial, S.A. (2019). SCACS risk management platform.

Retrieved September 7 2019, from https://www.ais-int.com/en/financial-services/credit-

risk-management/scacs-risk-management-platform/

Anastasia. (2017 February 26,). Overview of Qualitative And Quantitative Data Collection

Methods. Retrieved September 7 2019, from https://www.cleverism.com/qualitative-

and-quantitative-data-collection-methods/

Chatterjee, S. (2019, Jul 22). A Comprehensive Study of Linear vs Logistic Regression to

refresh the Basics. Retrieved September 7 2019, from

https://towardsdatascience.com/a-comprehensive-study-of-linear-vs-logistic-regression-

to-refresh-the-basics-7e526c1d3ebe

MyAccountingCourse.com. (2019). What is an Accounting Information System? Retrieved

September 7 2019, from

https://www.myaccountingcourse.com/accounting-dictionary/accounting-information-

system

Peavler, R. (2019 June 01). The Business Owner's Guide to Accounting Information Systems.

Retrieved September 7 2019, from https://www.thebalancesmb.com/accounting-

information-systems-392953

Statistics Solutions. (2019). Correlation in SPSS. Retrieved September 7 2019

https://www.statisticssolutions.com/correlation-in-spss/

University Of Connecticut (n.d.). Anova, regression, and chi-square Retrieved September 7

2019, from https://researchbasics.education.uconn.edu/anova_regression_and_chi-

square/#

12The Evolution of Accounting Information System

Appendices

Appendix 1: Survey Questionnaire

Q.1.) Gender

Male [ ]

Female [ ]

Q.2.) Age

20-30 [ ]

30-40 [ ]

40-50 [ ]

Above 50 [ ]

Q.3.) Academic Qualification

Master [ ]

Bachelor [ ]

Diploma [ ]

Other [ ]

Appendices

Appendix 1: Survey Questionnaire

Q.1.) Gender

Male [ ]

Female [ ]

Q.2.) Age

20-30 [ ]

30-40 [ ]

40-50 [ ]

Above 50 [ ]

Q.3.) Academic Qualification

Master [ ]

Bachelor [ ]

Diploma [ ]

Other [ ]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.