Analysis of Inventory Management at Evolution Mining Under AASB 102

VerifiedAdded on 2023/04/26

|7

|1339

|207

Essay

AI Summary

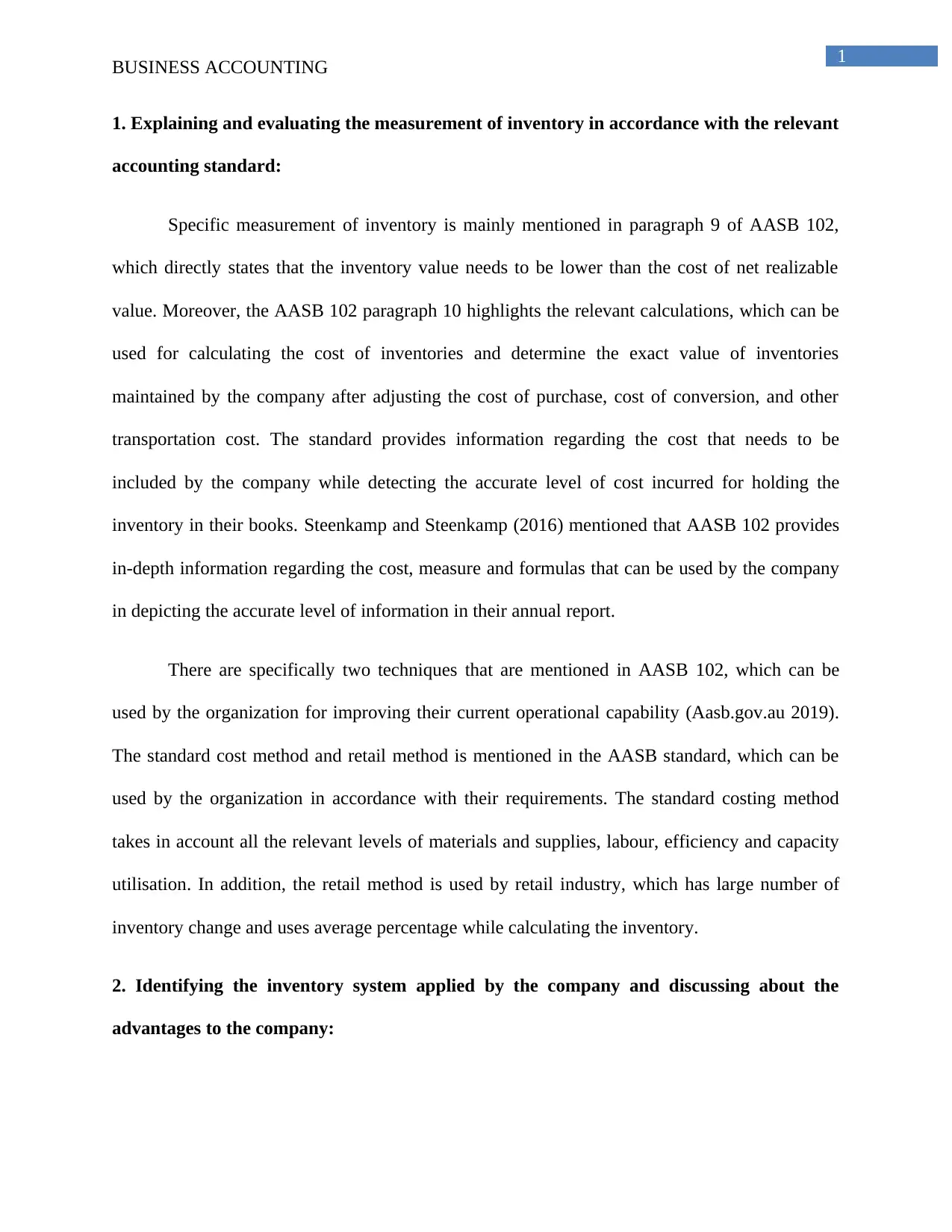

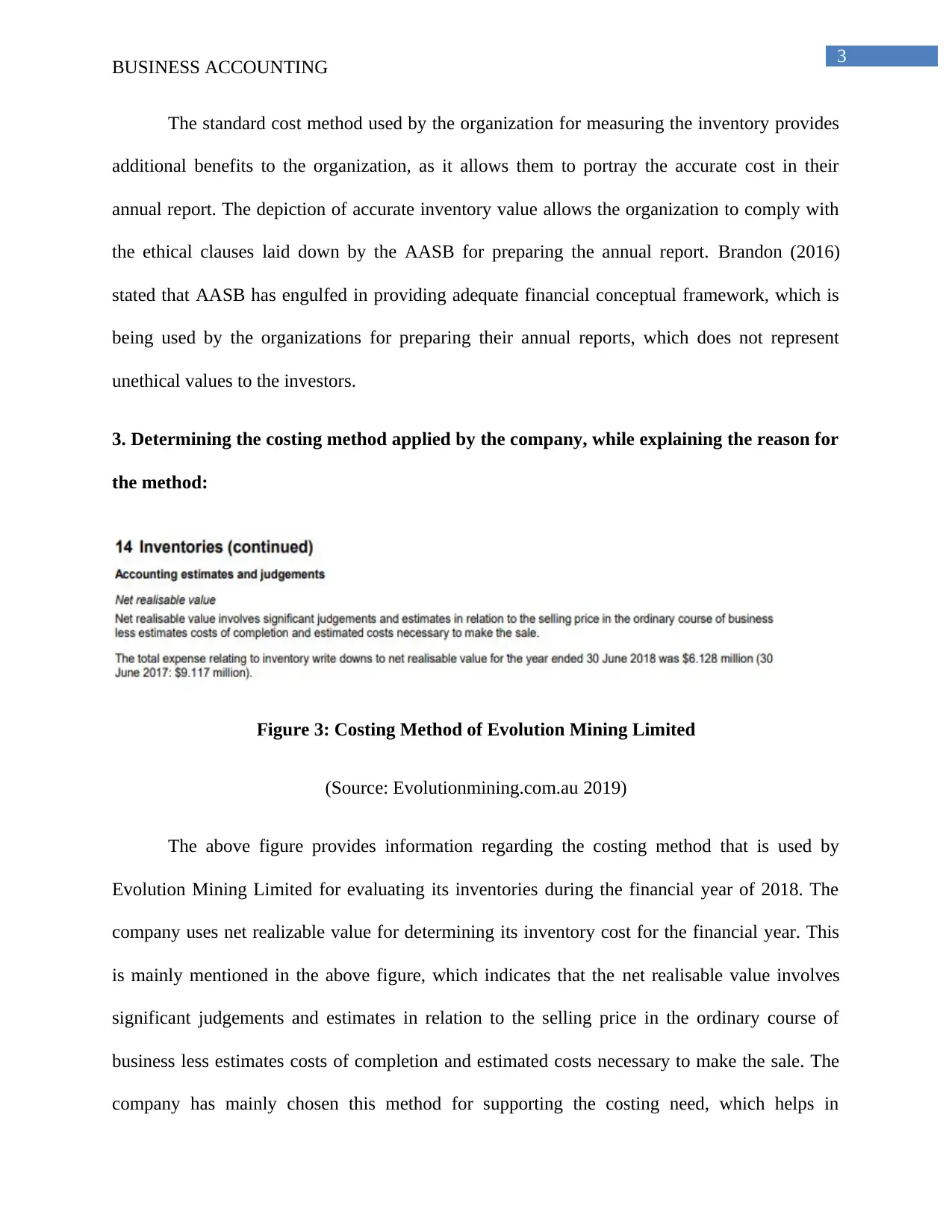

This essay provides an in-depth analysis of inventory measurement and accounting standards, specifically focusing on Evolution Mining Limited and its application of AASB 102. It explains and evaluates the measurement of inventory according to relevant accounting standards, identifies the inventory system applied by the company, and discusses the advantages of their chosen system. Furthermore, the essay determines the costing method used by Evolution Mining, explaining the rationale behind it, and estimates the impact of different costing methods on the company's financial statements. The analysis incorporates references from the AASB Conceptual Framework to support the discussions, highlighting the company's use of the standard cost method and net realizable value for inventory valuation, ultimately concluding that this approach allows for accurate financial reporting in the mining industry.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.