Evaluation of Evolution in Mining Industry Practices

VerifiedAdded on 2020/05/28

|14

|3184

|112

AI Summary

The mining industry has undergone substantial evolution over recent decades, especially concerning safety practices, social responsibility initiatives, and stakeholder engagement efforts. Initially focused primarily on resource extraction with minimal consideration for environmental or community impact, contemporary mining operations now prioritize comprehensive safety protocols designed to protect workers and reduce accidents. These improvements are driven by stringent regulatory standards and technological advancements in equipment and training. In parallel, there has been a marked shift towards greater corporate social responsibility (CSR), where companies actively engage in environmentally sustainable practices and contribute positively to local communities. This evolution reflects an increased awareness of the long-term impacts of mining activities on ecosystems and societal structures. Moreover, stakeholder engagement has transformed from a peripheral activity to a central strategic element, ensuring that the voices of affected communities, environmental groups, and other relevant stakeholders are heard and considered in decision-making processes. The integration of these practices not only enhances the industry's reputation but also ensures sustainable growth by aligning business operations with broader societal expectations. Overall, the mining sector continues to evolve, striving for a balance between resource extraction and its social and environmental responsibilities.

Accounting Theory and Issues 1

ACCOUNTING THEORY AND ISSUES

by(Student’s Name)

Professor’s Name

Institution

Location of Institution

Course

Date

ACCOUNTING THEORY AND ISSUES

by(Student’s Name)

Professor’s Name

Institution

Location of Institution

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Issues 2

Executive Summary

The conceptual accounting framework is considered as objectives and ideas which result

in the development of a consistent set of standards and rules. The primary objective of the

conceptual framework is, therefore, to guide accountants on the procedures and policies for the

preparation of accounting financial information in the various company. This paper seeks to give

insight into the accounting system of Evolution Mining Company.

It discusses how the company has complied with the fundamental qualitative characteristics

of financial information including those features which enhances the qualitative characteristics

such as timeliness, understandability and comparability. The other focus of the paper is on the

accounting problems faced by the Evolution Mining Company as discussed in the paper below.

Moreover, the paper has highlighted on the key recommendations to be used by the company

to prevent accounting problems and such recommendations entail, the enhancement of the

qualitative characteristics of accounting information. The paper concludes by giving an overview

of whether the company has complied with the qualitative characteristics of accounting

information or not as required by the Australian Security Exchange.

Introduction

Evolution Mining Limited is an Australian gold miner company established in 2011 as a mid-tier

gold producer with the merging of Conquest Mining Ltd and Catalpa Resources Ltd as well as

the concurrent acquisition of Newcrest Mining's interests in the Cracow and Mt Rawdon mines.

Since its establishment, the company has grown through acquisition; acquiring Cowal and

Mungari in July and August of 2015 respectively as well as Ernest Henry in November 2016.

Having created a reputation for consistency and reliability Evolution has won several accolades

such as Craig Oliver Award, 2016 Miner of the Year to mention a few (Piper, 2018 p.33).

Executive Summary

The conceptual accounting framework is considered as objectives and ideas which result

in the development of a consistent set of standards and rules. The primary objective of the

conceptual framework is, therefore, to guide accountants on the procedures and policies for the

preparation of accounting financial information in the various company. This paper seeks to give

insight into the accounting system of Evolution Mining Company.

It discusses how the company has complied with the fundamental qualitative characteristics

of financial information including those features which enhances the qualitative characteristics

such as timeliness, understandability and comparability. The other focus of the paper is on the

accounting problems faced by the Evolution Mining Company as discussed in the paper below.

Moreover, the paper has highlighted on the key recommendations to be used by the company

to prevent accounting problems and such recommendations entail, the enhancement of the

qualitative characteristics of accounting information. The paper concludes by giving an overview

of whether the company has complied with the qualitative characteristics of accounting

information or not as required by the Australian Security Exchange.

Introduction

Evolution Mining Limited is an Australian gold miner company established in 2011 as a mid-tier

gold producer with the merging of Conquest Mining Ltd and Catalpa Resources Ltd as well as

the concurrent acquisition of Newcrest Mining's interests in the Cracow and Mt Rawdon mines.

Since its establishment, the company has grown through acquisition; acquiring Cowal and

Mungari in July and August of 2015 respectively as well as Ernest Henry in November 2016.

Having created a reputation for consistency and reliability Evolution has won several accolades

such as Craig Oliver Award, 2016 Miner of the Year to mention a few (Piper, 2018 p.33).

Accounting Theory and Issues 3

Conceptual Framework

The conceptual framework for financial reporting creates the concepts that lie in financial

reporting. Financing reporting provides information useful to both the potential and existing

investors, creditors and others in the making decisions on resource allocation and investments. It

is also useful in evaluating prospects of cash flow and the provision of information on resources

of a business organization including claims. The key conceptual framework elements include

relevance, faithful representation, understandability and comparability. An information should be

relevant in decisions relating to allocation of resources, investment and credit allocation.

An information which is relevant can make a difference in the decisions of users by helping them

in the evaluation of potential past, present and future transaction effects on future cash flows. A

faithful representation of the real world economic phenomena is useful in investing, credit

resource allocation decisions.

Thus the information must be verifiable, neutral and complete. Comparability enhances the

financial reporting information usefulness in making investment, credit and resource allocation

decisions (Piper, 2018 p.33). Understandability enables users having a reasonable knowledge of

business and economic activities and financial accounting to study the information and

comprehend its meaning. The critical requirements for a general purpose financial reporting are

that one a company must comply with the accounting standards and such a report has to be

prepared in accordance with the Australian Accounting Standards.

The other requirement is that the general purpose financial reporting should offer an accurate

representation of the financial position, cash flows and financial performance of a particular

Conceptual Framework

The conceptual framework for financial reporting creates the concepts that lie in financial

reporting. Financing reporting provides information useful to both the potential and existing

investors, creditors and others in the making decisions on resource allocation and investments. It

is also useful in evaluating prospects of cash flow and the provision of information on resources

of a business organization including claims. The key conceptual framework elements include

relevance, faithful representation, understandability and comparability. An information should be

relevant in decisions relating to allocation of resources, investment and credit allocation.

An information which is relevant can make a difference in the decisions of users by helping them

in the evaluation of potential past, present and future transaction effects on future cash flows. A

faithful representation of the real world economic phenomena is useful in investing, credit

resource allocation decisions.

Thus the information must be verifiable, neutral and complete. Comparability enhances the

financial reporting information usefulness in making investment, credit and resource allocation

decisions (Piper, 2018 p.33). Understandability enables users having a reasonable knowledge of

business and economic activities and financial accounting to study the information and

comprehend its meaning. The critical requirements for a general purpose financial reporting are

that one a company must comply with the accounting standards and such a report has to be

prepared in accordance with the Australian Accounting Standards.

The other requirement is that the general purpose financial reporting should offer an accurate

representation of the financial position, cash flows and financial performance of a particular

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Issues 4

company in a structured manner. Moreover, the general purpose financial reporting should also

be in a position to provide relevant information which is useful to a variety of users to enable

them to make viable economic decisions. Lastly, it is required of the general purpose financial

reporting to indicate the results of the stewardship of management of the resources which have

been allocated in a particular company. However, to comply and meet the requirements, the

financial statements must be prepared on the basis of measurement and recognition criteria

which would represent the financial position and performance of an entity faithfully.

Critical Analysis

Stakeholder Theory

According to the theory, the primary aim of the business entity is the creation of value for

the key stakeholders of the company. The executive members of the company should ensure

therefore that the various interests of the stakeholders such as employees, customers,

shareholders, customers and suppliers are aligned and therefore go together in the same

particular direction (Piper, 2018 p.33). The stakeholder theory has however been criticized by

different individuals especially in relation to the fiduciary obligations. According to the critics of

the theory, they argue that the theory results in the breakage of the fiduciary duties which the

managers of the company have on shareholders and this has been considered as unethical.

However, there are several benefits which have been obtained by the company due to the use of

the stakeholder approach.

Generally, the primary activity of any particular business entity is not to make profits for

the shareholders, but rather it entails the enhancement of the state of the world including the

company in a structured manner. Moreover, the general purpose financial reporting should also

be in a position to provide relevant information which is useful to a variety of users to enable

them to make viable economic decisions. Lastly, it is required of the general purpose financial

reporting to indicate the results of the stewardship of management of the resources which have

been allocated in a particular company. However, to comply and meet the requirements, the

financial statements must be prepared on the basis of measurement and recognition criteria

which would represent the financial position and performance of an entity faithfully.

Critical Analysis

Stakeholder Theory

According to the theory, the primary aim of the business entity is the creation of value for

the key stakeholders of the company. The executive members of the company should ensure

therefore that the various interests of the stakeholders such as employees, customers,

shareholders, customers and suppliers are aligned and therefore go together in the same

particular direction (Piper, 2018 p.33). The stakeholder theory has however been criticized by

different individuals especially in relation to the fiduciary obligations. According to the critics of

the theory, they argue that the theory results in the breakage of the fiduciary duties which the

managers of the company have on shareholders and this has been considered as unethical.

However, there are several benefits which have been obtained by the company due to the use of

the stakeholder approach.

Generally, the primary activity of any particular business entity is not to make profits for

the shareholders, but rather it entails the enhancement of the state of the world including the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Issues 5

creation of value for the stakeholders which form the critical benefit which has been obtained by

the company (Baur, 2014 p.174). Moreover, when the right thing is done for the customer, the

company would gain financially. Thus it is vital to focus on the various stakeholders of the

company.

Accounting Problems

There are a variety of accounting problems and issues faced by the company. One of the

key problems is that of fraudulent reporting activity which entails the reporting of certain false

figures with the aim of making the company appear as if it is financially stable. However, this

has damaged the image of the firm including its reputation leading to criminal charges. The other

fraudulent activity which had earlier been committed by the company is that of deferring the

gross profit by use of revenue recognition system which is unacceptable by the General Accepted

Accounting Principles (Henderson et al.2015 p.10).

Another accounting problem the company faces is that of the use of varying accounting

methods in every particular financial year. The use of different accounting techniques in the

company has created a lot of confusion resulting in miscommunication among various

employees (Herman, 2016 p.40). It is therefore essential for the company to comprehend the

various accounting techniques which should be used to avoid such an accounting issue.

Measurement Requirements

According to the annual report of the company, Evolution Mining Limited often complies

with the measurement requirements of the conceptual framework. One of the key measurement

requirements is that the measurement cost in the often justified by certain benefits which are as a

result of the information which is available for the potential, investors and creditors who rely on

the information for decision-making purposes (Kroeger and Weber, 2014 p.520). The other

creation of value for the stakeholders which form the critical benefit which has been obtained by

the company (Baur, 2014 p.174). Moreover, when the right thing is done for the customer, the

company would gain financially. Thus it is vital to focus on the various stakeholders of the

company.

Accounting Problems

There are a variety of accounting problems and issues faced by the company. One of the

key problems is that of fraudulent reporting activity which entails the reporting of certain false

figures with the aim of making the company appear as if it is financially stable. However, this

has damaged the image of the firm including its reputation leading to criminal charges. The other

fraudulent activity which had earlier been committed by the company is that of deferring the

gross profit by use of revenue recognition system which is unacceptable by the General Accepted

Accounting Principles (Henderson et al.2015 p.10).

Another accounting problem the company faces is that of the use of varying accounting

methods in every particular financial year. The use of different accounting techniques in the

company has created a lot of confusion resulting in miscommunication among various

employees (Herman, 2016 p.40). It is therefore essential for the company to comprehend the

various accounting techniques which should be used to avoid such an accounting issue.

Measurement Requirements

According to the annual report of the company, Evolution Mining Limited often complies

with the measurement requirements of the conceptual framework. One of the key measurement

requirements is that the measurement cost in the often justified by certain benefits which are as a

result of the information which is available for the potential, investors and creditors who rely on

the information for decision-making purposes (Kroeger and Weber, 2014 p.520). The other

Accounting Theory and Issues 6

measurement requirement which has been complied with by the company is that of a faithful

representation of relevant information on the economic resources, the efficiency of the

management, utilization of resources of the company by the board and various claims levelled

against the Evolution mining company.

Besides the above mentioned measurement requirement which has been adhered to by the

company, the other typical requirement is that of preparation of financial information on the

basis of a measurement technique which would have an impact on the statement of

comprehensive income including the notes to the financial statements and the statement of the

cash flows. During the process of establishing the measurement requirements, the company often

takes into account various factors such as the cost incurred in the use of measurement of a

particular item in a statement of financial position which later provides another measure in the

notes of the financial statements (Baumgartner, 2014 p.260).

According to Chatburn et al. (2018 p.20), the other factor which it considers is the losses

and gains which are reported in the financial statements. Such a factor is looked into due to the

changes which may occur as a result of the use of one particular measurement technique to

another which could mislead the various users of financial statements. Furthermore, there is the

consideration of the number of various measures used since there is an assumption that with a

minimum number of measures, it becomes easier to offer relevant information to the various

stakeholders of the company.

Compliance of Evolution Mining Company with the Fundamental Qualitative

Characteristics

According to the annual reports of the company, it has complied with the fundamental

qualitative characteristics. For example, in its financial reporting, it faithfully represents

measurement requirement which has been complied with by the company is that of a faithful

representation of relevant information on the economic resources, the efficiency of the

management, utilization of resources of the company by the board and various claims levelled

against the Evolution mining company.

Besides the above mentioned measurement requirement which has been adhered to by the

company, the other typical requirement is that of preparation of financial information on the

basis of a measurement technique which would have an impact on the statement of

comprehensive income including the notes to the financial statements and the statement of the

cash flows. During the process of establishing the measurement requirements, the company often

takes into account various factors such as the cost incurred in the use of measurement of a

particular item in a statement of financial position which later provides another measure in the

notes of the financial statements (Baumgartner, 2014 p.260).

According to Chatburn et al. (2018 p.20), the other factor which it considers is the losses

and gains which are reported in the financial statements. Such a factor is looked into due to the

changes which may occur as a result of the use of one particular measurement technique to

another which could mislead the various users of financial statements. Furthermore, there is the

consideration of the number of various measures used since there is an assumption that with a

minimum number of measures, it becomes easier to offer relevant information to the various

stakeholders of the company.

Compliance of Evolution Mining Company with the Fundamental Qualitative

Characteristics

According to the annual reports of the company, it has complied with the fundamental

qualitative characteristics. For example, in its financial reporting, it faithfully represents

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Issues 7

information by ensuring that the reports are free from material error, complete and neutral. The

faithful representation has been enhanced by the company by the use of estimates and

assumptions which are closely related to the underlying standards and economic constructs

(Kythreotis, 2014 p.15). The common proxies used by the company in the measurement of the

faithful representation include corporate governance statement, neutrality, freedom from bias and

unqualified audit report.

The other way through which the firm has complied with the fundamental qualitative

characteristics is by providing information which is relevant which can make a difference in the

decisions made by the different users. The relevance of the information is based on the

confirmatory and predictive value (Birt, Muthusamy and Bir, 2017 p.118). The company

measures the predictive value on the basis of the use of fair value, provision of forward-looking

statements by the annual reports and the disclosure of information on the basis of risks and

business opportunities in the annual reports. Moreover, the financial reports of the company

entail both the financial and non-financial information which are considered as relevant to the

different users of the firm.

Apart from the above mentioned ways through which the company has complied with the

fundamental qualitative characteristics, Evolution Company provides understandable information

which is an essential qualitative characteristic. Generally, understandability increases due to

characterization, classification and presentation of information in a clear and precise manner to

allow various users to understand their meanings (Al-dmour et al.2017 p.10). To measure

understandability, the company uses various items such as the organization of information in the

annual report in a proper manner, the inclusion of a glossary of unfamiliar terminologies, the

disclosure of information in the notes of the financial statements and provision of information in

information by ensuring that the reports are free from material error, complete and neutral. The

faithful representation has been enhanced by the company by the use of estimates and

assumptions which are closely related to the underlying standards and economic constructs

(Kythreotis, 2014 p.15). The common proxies used by the company in the measurement of the

faithful representation include corporate governance statement, neutrality, freedom from bias and

unqualified audit report.

The other way through which the firm has complied with the fundamental qualitative

characteristics is by providing information which is relevant which can make a difference in the

decisions made by the different users. The relevance of the information is based on the

confirmatory and predictive value (Birt, Muthusamy and Bir, 2017 p.118). The company

measures the predictive value on the basis of the use of fair value, provision of forward-looking

statements by the annual reports and the disclosure of information on the basis of risks and

business opportunities in the annual reports. Moreover, the financial reports of the company

entail both the financial and non-financial information which are considered as relevant to the

different users of the firm.

Apart from the above mentioned ways through which the company has complied with the

fundamental qualitative characteristics, Evolution Company provides understandable information

which is an essential qualitative characteristic. Generally, understandability increases due to

characterization, classification and presentation of information in a clear and precise manner to

allow various users to understand their meanings (Al-dmour et al.2017 p.10). To measure

understandability, the company uses various items such as the organization of information in the

annual report in a proper manner, the inclusion of a glossary of unfamiliar terminologies, the

disclosure of information in the notes of the financial statements and provision of information in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Issues 8

graphs and tables. Additionally, the company usually takes into account the comparability

qualitative characteristics of information. The comparability feature of information has enabled

the users of the company to recognize differences and similarities in various sets of economic

phenomena.

According to Mbobo and Ekpo (2016 p.188), the firm measures comparability of

information using a number of items. Such include, the presentation of ratios and financial index

numbers in the annual reports, provision of comparable results of the previous accounting

periods and those of the current accounting periods. The others are notes to the revisions of the

accounting judgments and estimates which explains the effect of the changes and the

comparability of information of the company with those of the other organization in the same

mining industry.

The last qualitative characteristics which Evolution Mining Company has complied with

is that of timeliness. Generally, the company makes available the information to the different

users at a time which it has not lost its capacity to influence the decisions made (Zheng and

Chen, 2017 p.3). The timeliness of the information is estimated by the company on the basis of

the number of days taken by the company’s auditor in signing the books of account.

Compliance of Evolution Mining Company with Enhancing Qualitative Characteristics of

Information

Evolution Mining Company has indeed complied with the enhancement of the qualitative

characteristics of information, and this is according to the annual financial reports. Some of the

qualitative characteristics which have been complied by the company include verifiability such

that the financial information produced by the company is provided in the same assumptions and

graphs and tables. Additionally, the company usually takes into account the comparability

qualitative characteristics of information. The comparability feature of information has enabled

the users of the company to recognize differences and similarities in various sets of economic

phenomena.

According to Mbobo and Ekpo (2016 p.188), the firm measures comparability of

information using a number of items. Such include, the presentation of ratios and financial index

numbers in the annual reports, provision of comparable results of the previous accounting

periods and those of the current accounting periods. The others are notes to the revisions of the

accounting judgments and estimates which explains the effect of the changes and the

comparability of information of the company with those of the other organization in the same

mining industry.

The last qualitative characteristics which Evolution Mining Company has complied with

is that of timeliness. Generally, the company makes available the information to the different

users at a time which it has not lost its capacity to influence the decisions made (Zheng and

Chen, 2017 p.3). The timeliness of the information is estimated by the company on the basis of

the number of days taken by the company’s auditor in signing the books of account.

Compliance of Evolution Mining Company with Enhancing Qualitative Characteristics of

Information

Evolution Mining Company has indeed complied with the enhancement of the qualitative

characteristics of information, and this is according to the annual financial reports. Some of the

qualitative characteristics which have been complied by the company include verifiability such

that the financial information produced by the company is provided in the same assumptions and

Accounting Theory and Issues 9

data. Thus the information is made verifiable by the key financial users for decision making

(Lee, 2017 p.215).

The other enhanced qualitative characteristics of the financial information which is

adhered to by the company are the comparability where the policies and accounting standards

applied by the company are used consistently in various financial periods (Yakovleva, 2017

p.100). The users of the financial information of the firm can, therefore, gather insightful

conclusions in relation to the performance and trends of Evolution Mining Limited for a

particular period. The financial information provided in the annual reports of the company is

clear and thus can be understood by the average user, which forms a way in which the

organization enhances the qualitative characteristics of information (Ly et al.2015 p.220).

Consequently, the financial performance of the company can easily be established.

Timeliness is another enhancing qualitative characteristics which the company has complied

with in its preparation of annual financial reports (Zhu et al.2014 p.4). Evolution Company often

avails financial information to the users for proper decision making. The company values its

stakeholders. Thus it ensures that it avails financial information promptly.

The users of financial reports that is lenders, creditors and investors are therefore able to

use the reports to make viable decisions because, the information contained in the reports all

complies with the qualitative characteristics of information such as understandability,

comparability and relevance among others. Based on the information contained in the annual

reports of the company, the basic knowledge of accounting has been provided and therefore the

users of the information do not need much than that which has been provided to evaluate the

company. Moreover all the requirements for the general purpose financial reporting has been met

data. Thus the information is made verifiable by the key financial users for decision making

(Lee, 2017 p.215).

The other enhanced qualitative characteristics of the financial information which is

adhered to by the company are the comparability where the policies and accounting standards

applied by the company are used consistently in various financial periods (Yakovleva, 2017

p.100). The users of the financial information of the firm can, therefore, gather insightful

conclusions in relation to the performance and trends of Evolution Mining Limited for a

particular period. The financial information provided in the annual reports of the company is

clear and thus can be understood by the average user, which forms a way in which the

organization enhances the qualitative characteristics of information (Ly et al.2015 p.220).

Consequently, the financial performance of the company can easily be established.

Timeliness is another enhancing qualitative characteristics which the company has complied

with in its preparation of annual financial reports (Zhu et al.2014 p.4). Evolution Company often

avails financial information to the users for proper decision making. The company values its

stakeholders. Thus it ensures that it avails financial information promptly.

The users of financial reports that is lenders, creditors and investors are therefore able to

use the reports to make viable decisions because, the information contained in the reports all

complies with the qualitative characteristics of information such as understandability,

comparability and relevance among others. Based on the information contained in the annual

reports of the company, the basic knowledge of accounting has been provided and therefore the

users of the information do not need much than that which has been provided to evaluate the

company. Moreover all the requirements for the general purpose financial reporting has been met

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Issues 10

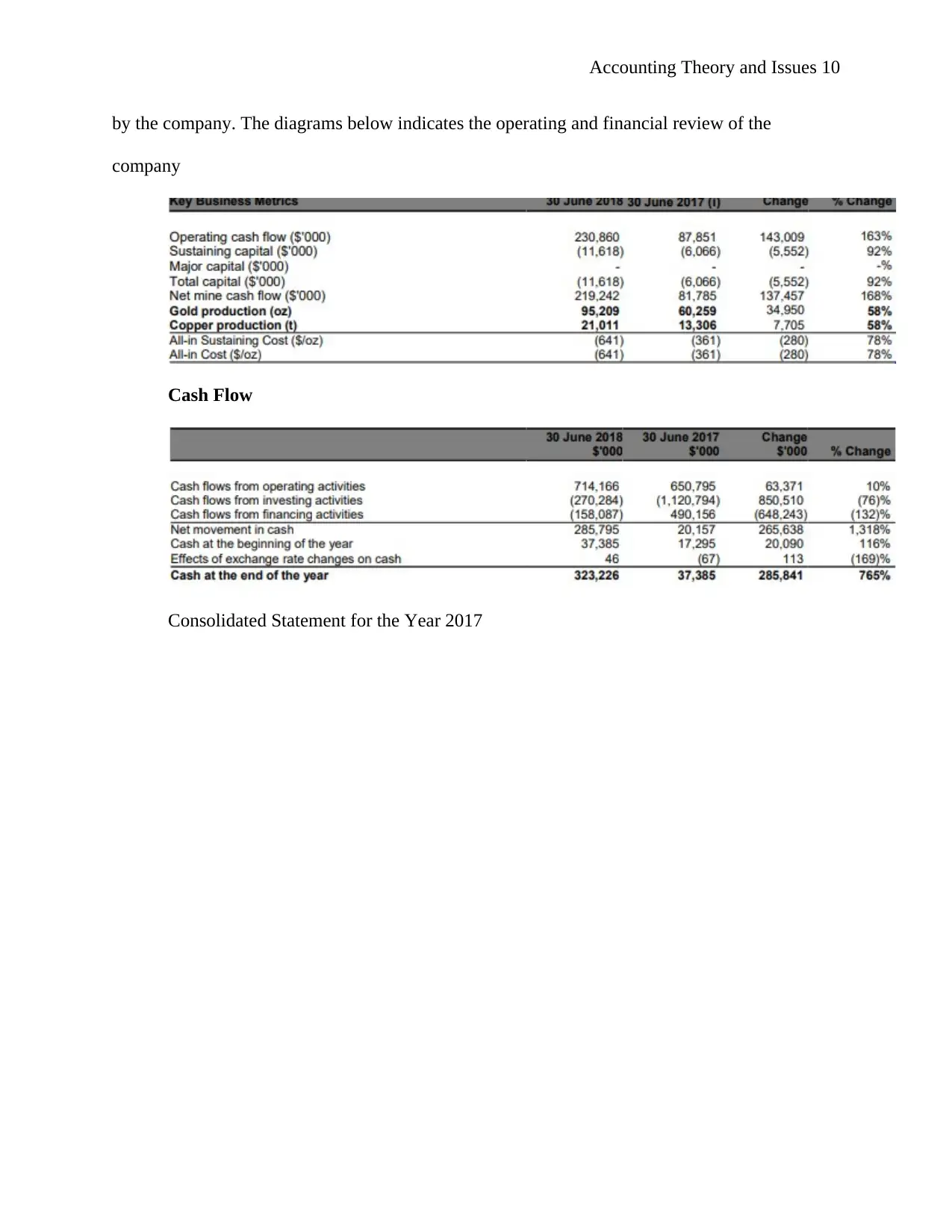

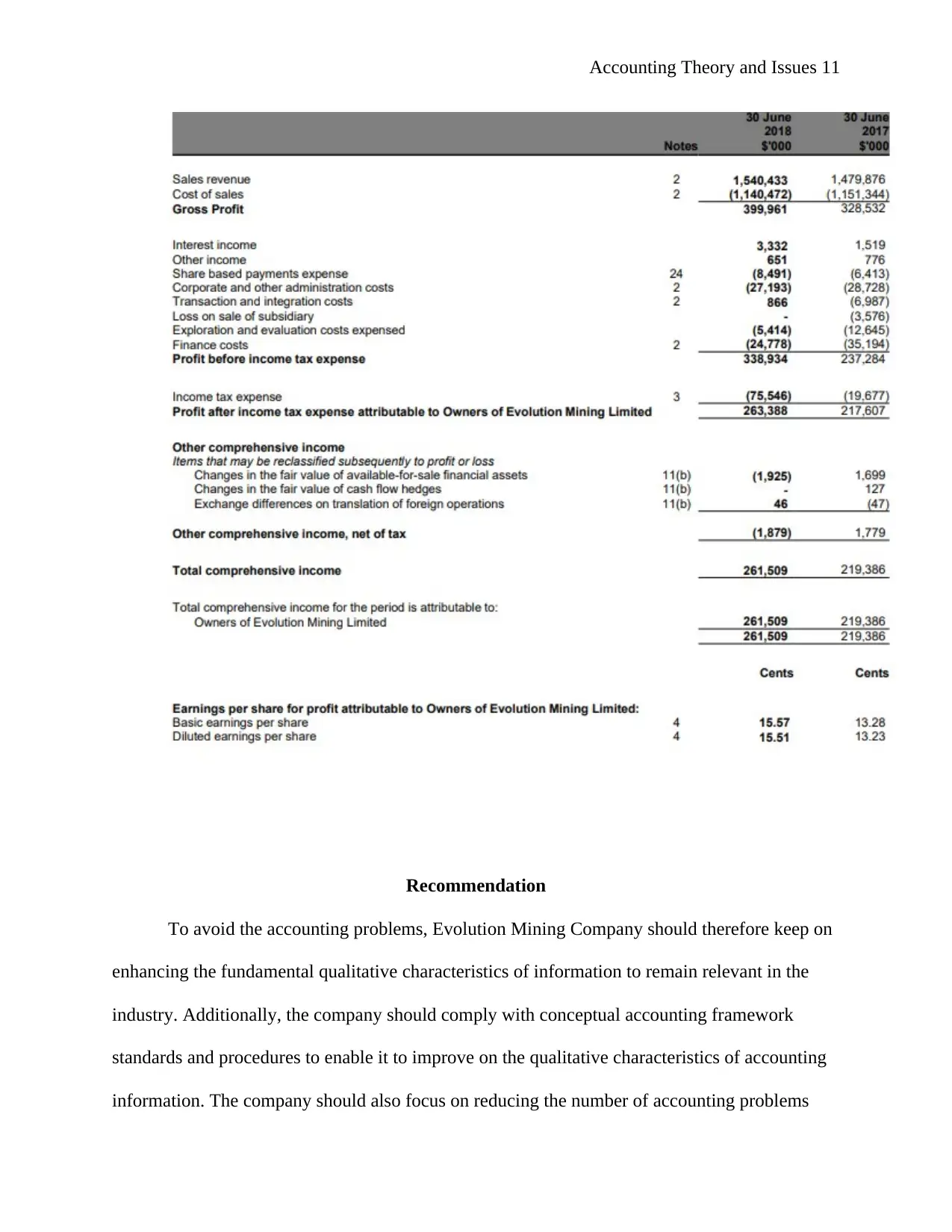

by the company. The diagrams below indicates the operating and financial review of the

company

Cash Flow

Consolidated Statement for the Year 2017

by the company. The diagrams below indicates the operating and financial review of the

company

Cash Flow

Consolidated Statement for the Year 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Issues 11

Recommendation

To avoid the accounting problems, Evolution Mining Company should therefore keep on

enhancing the fundamental qualitative characteristics of information to remain relevant in the

industry. Additionally, the company should comply with conceptual accounting framework

standards and procedures to enable it to improve on the qualitative characteristics of accounting

information. The company should also focus on reducing the number of accounting problems

Recommendation

To avoid the accounting problems, Evolution Mining Company should therefore keep on

enhancing the fundamental qualitative characteristics of information to remain relevant in the

industry. Additionally, the company should comply with conceptual accounting framework

standards and procedures to enable it to improve on the qualitative characteristics of accounting

information. The company should also focus on reducing the number of accounting problems

Accounting Theory and Issues 12

such as fraudulent activities by reporting the correct figures in the financial reports and this will

enhance its image and reputation in the industry.

Conclusion

To conclude, Evolution Mining Company has complied with the conceptual framework

requirement because it has enhanced all the qualitative characteristics of accounting information

such as comparability, understandability and timeliness among others. The key recommendations

for the company should be reduction of fraudulent activities by reporting right figures in annual

reports. Other recommendations include, compliance with the accounting conceptual framework

and enhancement of the qualitative characteristics of information.

References

Al-dmour, A., Abbod, M.F. and Al-dmour, H.H., 2017. Qualitative Characteristics of Financial

Reporting and Non-Financial Business Performance. International Journal of Corporate

Finance and Accounting (IJCFA), 4(2), pp.1-22.

such as fraudulent activities by reporting the correct figures in the financial reports and this will

enhance its image and reputation in the industry.

Conclusion

To conclude, Evolution Mining Company has complied with the conceptual framework

requirement because it has enhanced all the qualitative characteristics of accounting information

such as comparability, understandability and timeliness among others. The key recommendations

for the company should be reduction of fraudulent activities by reporting right figures in annual

reports. Other recommendations include, compliance with the accounting conceptual framework

and enhancement of the qualitative characteristics of information.

References

Al-dmour, A., Abbod, M.F. and Al-dmour, H.H., 2017. Qualitative Characteristics of Financial

Reporting and Non-Financial Business Performance. International Journal of Corporate

Finance and Accounting (IJCFA), 4(2), pp.1-22.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.