ACCT20074: Event Hospitality and Tsogo Sun Analysis Report

VerifiedAdded on 2023/01/20

|17

|3794

|64

Report

AI Summary

This report provides a comprehensive analysis of Event Hospitality (EVT) and Tsogo Sun Holdings Ltd (TSH), focusing on the application of the conceptual framework in financial reporting. The report begins with an overview of the history and development of the conceptual framework in the USA, UK, Australia, and globally under the IASB. It then discusses the Australian accounting profession's concerns regarding the application of the IASB/IFRS Conceptual Framework. The analysis extends to a critical discussion of academics' concerns regarding the quality, benefits, and limitations of the conceptual framework. Part A focuses on the conceptual framework, including its history, the accounting profession's perspective, academic concerns, and its application to Event Hospitality. Part B analyzes the sustainability and integrated reporting of Tsogo Sun Holdings Ltd. The report examines the financial positions of Event Hospitality based on the conceptual framework. It explores recognition principles, measurement bases for revenue, assets, and liabilities and the qualitative characteristics of information exhibited in the company's financial reports. The report makes a comparison between the Australian and South African companies and evaluates the financial statements against the conceptual framework.

Running Head: EVENT HOSPITALITY AND TSOGO ANALYSIS 1

Event Hospitality and Tsogo Analysis

Name

Institution

Event Hospitality and Tsogo Analysis

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Event Hospitality and Tsogo Analysis 2

Executive Summary

In this paper the main idea is centered on the enactment of the conceptual framework that is

significantly utilized in accounting of companies statements. The major concept identified in

this is that these financial statements are utilized in effectively making essential decisions of a

specific company. Thus the focus of the paper is assisting organization is acquiring and

evaluating the financial condition of various companies. Hence the conceptual framework

utilization and applicability within the ASX aligned companies will assess the Event

Hospitality (EVT), and methods the company has employed in making sure those financial

statements, and processes. Therefore, in section B there will be a rational of international

reporting frameworks against effective accounting measures which entirely relate to the

strengths and restriction of the conceptual framework (CF) (Ahmad, & Arshad, 2014).

Additionally, in the paper there will be an analysis of a South African firm which is Tsogo

Sun Holdings Ltd. The analysis of the South African based company will be compared to the

Australian company stated in initially.

Executive Summary

In this paper the main idea is centered on the enactment of the conceptual framework that is

significantly utilized in accounting of companies statements. The major concept identified in

this is that these financial statements are utilized in effectively making essential decisions of a

specific company. Thus the focus of the paper is assisting organization is acquiring and

evaluating the financial condition of various companies. Hence the conceptual framework

utilization and applicability within the ASX aligned companies will assess the Event

Hospitality (EVT), and methods the company has employed in making sure those financial

statements, and processes. Therefore, in section B there will be a rational of international

reporting frameworks against effective accounting measures which entirely relate to the

strengths and restriction of the conceptual framework (CF) (Ahmad, & Arshad, 2014).

Additionally, in the paper there will be an analysis of a South African firm which is Tsogo

Sun Holdings Ltd. The analysis of the South African based company will be compared to the

Australian company stated in initially.

Event Hospitality and Tsogo Analysis 3

Introduction

The main objective of this paper is stating fundamental financial guidelines which are

important and take into account various processes and rules used in evaluating firm’s

financial records and economic appraisal. Taking into account the financial statements it

enables stakeholders in creating effective decisions using the conceptual framework that is

also applicable for both Event hospitality and the Tsogo Sun Holdings limited respectively.

Consequently, the CF is useful in evaluating the IASB during the implementation of

standardized accounting rules and guidelines which are pertinent for the application of

financial statements and procedures. Based on Event Hospitality, the conceptual framework

will entirely look into the application and relevancy stating how various financial statements

have been outlined. Lastly, part B will analyze how sustainability and integral reporting have

been employed with the aid of the conceptual framework by Tsogo Sun Holding Limited.

Part A: The Conceptual Framework Analysis

a. Analysis of the Conceptual Framework History (CF)

Initially the formulation of the conceptual framework both in US, UK, and Australia was

initiated by Sprouse and Moonitz based on probable accounting techniques and processes in

1962. Thus in 1965, Grady created a theory explaining the CF based on the evaluation of

present accounting methods which led to the establishment of the APB (Accounting

Principles Board). Hence later, there was effective formulation of an actual committee which

implemented the true blood report in 1972. Thus the main constituents of the report were:

Stating 7 qualitative features of financial data and 12 aims linked to accounting

Aim 1: focused on the necessities of financial statements of the clients

Aim 2: must met customer’s having limited ability of accessing financial data

Introduction

The main objective of this paper is stating fundamental financial guidelines which are

important and take into account various processes and rules used in evaluating firm’s

financial records and economic appraisal. Taking into account the financial statements it

enables stakeholders in creating effective decisions using the conceptual framework that is

also applicable for both Event hospitality and the Tsogo Sun Holdings limited respectively.

Consequently, the CF is useful in evaluating the IASB during the implementation of

standardized accounting rules and guidelines which are pertinent for the application of

financial statements and procedures. Based on Event Hospitality, the conceptual framework

will entirely look into the application and relevancy stating how various financial statements

have been outlined. Lastly, part B will analyze how sustainability and integral reporting have

been employed with the aid of the conceptual framework by Tsogo Sun Holding Limited.

Part A: The Conceptual Framework Analysis

a. Analysis of the Conceptual Framework History (CF)

Initially the formulation of the conceptual framework both in US, UK, and Australia was

initiated by Sprouse and Moonitz based on probable accounting techniques and processes in

1962. Thus in 1965, Grady created a theory explaining the CF based on the evaluation of

present accounting methods which led to the establishment of the APB (Accounting

Principles Board). Hence later, there was effective formulation of an actual committee which

implemented the true blood report in 1972. Thus the main constituents of the report were:

Stating 7 qualitative features of financial data and 12 aims linked to accounting

Aim 1: focused on the necessities of financial statements of the clients

Aim 2: must met customer’s having limited ability of accessing financial data

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Event Hospitality and Tsogo Analysis 4

In 1974, there was replacement of the accounting principle board with the FASB which

specifically aimed at analyzing the conceptual framework components. Based on this fact,

about 6 of the statements were thus enacted in 1985. Primarily, the foremost SFACS to be

formulated was considered to be normative but the SFAC had been associated to

identification and acknowledgement of current accounting practices. Based on this fact much

reproaches were witnessed in 2005 which made the IASB initiate brand new techniques used

in improving the reviewed conceptual framework that would be used by the entire committee

referred as a joint project. On the other hand, the UK advanced in taking into action the

objectives and documentations of customer’s data availed from the corporate statements.

Thus the major components of the reports entailed the below factors, they include:

Highlighting society privileges and positions of evaluating financial information

Entirely, data is not recommended by the accounting professionals.

Additionally, the IASC was adopted in 1991 which specifically assessed the conceptual

framework. Thus the current accounting policies met the Australian and the US framework

thus was generally known as the IASB framework. Thus considering the Australian

accounting systems, the progress levels of the country’s economy is stagnating five

accounting records were introduced which were:

SFAC 1 – reporting entity explanation

SFAC 2 – financial reporting objectives

SFAC 3 – financial data qualitative factors

SFAC 4 – recognition and explanation of specific financial characteristics

SFAC 5 – having measurements that had not yet been released

In 1974, there was replacement of the accounting principle board with the FASB which

specifically aimed at analyzing the conceptual framework components. Based on this fact,

about 6 of the statements were thus enacted in 1985. Primarily, the foremost SFACS to be

formulated was considered to be normative but the SFAC had been associated to

identification and acknowledgement of current accounting practices. Based on this fact much

reproaches were witnessed in 2005 which made the IASB initiate brand new techniques used

in improving the reviewed conceptual framework that would be used by the entire committee

referred as a joint project. On the other hand, the UK advanced in taking into action the

objectives and documentations of customer’s data availed from the corporate statements.

Thus the major components of the reports entailed the below factors, they include:

Highlighting society privileges and positions of evaluating financial information

Entirely, data is not recommended by the accounting professionals.

Additionally, the IASC was adopted in 1991 which specifically assessed the conceptual

framework. Thus the current accounting policies met the Australian and the US framework

thus was generally known as the IASB framework. Thus considering the Australian

accounting systems, the progress levels of the country’s economy is stagnating five

accounting records were introduced which were:

SFAC 1 – reporting entity explanation

SFAC 2 – financial reporting objectives

SFAC 3 – financial data qualitative factors

SFAC 4 – recognition and explanation of specific financial characteristics

SFAC 5 – having measurements that had not yet been released

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Event Hospitality and Tsogo Analysis 5

Therefore, centered on the history of the Australian accounting system it was nearly similar

to the US conceptual framework. Thus the IASB framework was enacted which was used in

performing the IAS and the IFRS financial reporting.

a. Accounting Profession explanation

Generally, the quasi legislation significantly entails the anxiety of state-focused CF within the

Australian accounting systems which is always not conceivable in ascertaining that

accounting rules are precise and steady and thus been outlined in an accurate way

(Bellantuono, Pontrandolfo, & Scozzi, 2016). Despite the fact that accounting fundamentals

can be very hard in accessing, certain objectives of the stated accounting records, have been

claimed by researchers to be inefficient considering the Australian accounting standards

which further highlights the stated accounting challenges. Due to this fact, there are more

focus in assessing the conceptual framework operations unlike its stated aims and objective

used in the evaluation of different entities within the financial statements. It implies that

many experts are not in compliance with various accounting rules and basic assessment of the

conceptual framework considering the aims and objectives of various financial accounting

records. The basic reason behind this is due to the fact that the under-laid accounting systems

convey limited accounting objectives.

a. Academic concerns

There prospective benefits and restrictions when relating the conceptual framework to the

various accounting professions. Based on this fact, certain advantages are noticeable within

the accounting industry such as.

Due to the establishment of the conceptual framework by many countries worldwide,

then all countries must uphold international compatibility considering the various

accounting standards and methods. Therefore, matters on quality of accounting

Therefore, centered on the history of the Australian accounting system it was nearly similar

to the US conceptual framework. Thus the IASB framework was enacted which was used in

performing the IAS and the IFRS financial reporting.

a. Accounting Profession explanation

Generally, the quasi legislation significantly entails the anxiety of state-focused CF within the

Australian accounting systems which is always not conceivable in ascertaining that

accounting rules are precise and steady and thus been outlined in an accurate way

(Bellantuono, Pontrandolfo, & Scozzi, 2016). Despite the fact that accounting fundamentals

can be very hard in accessing, certain objectives of the stated accounting records, have been

claimed by researchers to be inefficient considering the Australian accounting standards

which further highlights the stated accounting challenges. Due to this fact, there are more

focus in assessing the conceptual framework operations unlike its stated aims and objective

used in the evaluation of different entities within the financial statements. It implies that

many experts are not in compliance with various accounting rules and basic assessment of the

conceptual framework considering the aims and objectives of various financial accounting

records. The basic reason behind this is due to the fact that the under-laid accounting systems

convey limited accounting objectives.

a. Academic concerns

There prospective benefits and restrictions when relating the conceptual framework to the

various accounting professions. Based on this fact, certain advantages are noticeable within

the accounting industry such as.

Due to the establishment of the conceptual framework by many countries worldwide,

then all countries must uphold international compatibility considering the various

accounting standards and methods. Therefore, matters on quality of accounting

Event Hospitality and Tsogo Analysis 6

standards and accuracy within the international financial reports will be accurate for

the assessment of far-off investments and cash flows

Additionally, academic are majorly focused on accounting results that are accurate

and logical, thus insinuating that for accounting standards to be formulated

prospective frameworks must be effectively established

On the other hand, the conceptual framework issues out essential functions of the

accounting systems. Due to this fact, regulators are thus prospected to be responsible

for their financial claims. Thus in an event when these decisions are recovered from

essential accounting concerns as assessed within the CF the academic experts are

anticipated to provide vivid explanation and clarity should be outlined during the

implementation process.

On the other hand, the conceptual framework points relevant methods used in

highlighting important ideas and concepts centered on the current financial reports.

Hence, the CF has analyzed probable guide used for entities reporting based on

certain accounting assessments and standards of particular financial matters.

Also accounting regulators encounter less political pressure in the process of creating

the accounting methods and standards such as the aims and objectives of the financial

reports, whereby different criteria to recognition have been prioritized considering the

enactment of the conceptual framework.

Hence a segment of the restrictions has been linked to the accounting CF which are briefly

stated below:

It is contemptible in formulating the CF

There is influence of the CF by government activities. Considering this various

accountant highlight current concerns and claims in which the CF is highly inclined to

political protocols.

standards and accuracy within the international financial reports will be accurate for

the assessment of far-off investments and cash flows

Additionally, academic are majorly focused on accounting results that are accurate

and logical, thus insinuating that for accounting standards to be formulated

prospective frameworks must be effectively established

On the other hand, the conceptual framework issues out essential functions of the

accounting systems. Due to this fact, regulators are thus prospected to be responsible

for their financial claims. Thus in an event when these decisions are recovered from

essential accounting concerns as assessed within the CF the academic experts are

anticipated to provide vivid explanation and clarity should be outlined during the

implementation process.

On the other hand, the conceptual framework points relevant methods used in

highlighting important ideas and concepts centered on the current financial reports.

Hence, the CF has analyzed probable guide used for entities reporting based on

certain accounting assessments and standards of particular financial matters.

Also accounting regulators encounter less political pressure in the process of creating

the accounting methods and standards such as the aims and objectives of the financial

reports, whereby different criteria to recognition have been prioritized considering the

enactment of the conceptual framework.

Hence a segment of the restrictions has been linked to the accounting CF which are briefly

stated below:

It is contemptible in formulating the CF

There is influence of the CF by government activities. Considering this various

accountant highlight current concerns and claims in which the CF is highly inclined to

political protocols.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Event Hospitality and Tsogo Analysis 7

Associated to various restrictions stated in the previous sections, when the conceptual

framework entails the involvement of accounting concerns most often there is arousal

of various financial estimation of a particular asset

Conclusively, the conceptual framework regards more on financial linked concepts.

Considering this, the CF will specifically highlight certain performance processes including

social and ecological features. Additionally, with the assessment of the financial performance

processes, the conceptual framework highly conveys financial assessor concepts based on the

corporate performance processes.

a. The conceptual framework application

i. Explanation of how the conceptual framework has been applied by the selected

Australian Company

In this section there will be an analysis of the number of statements that have been prepare

based on the conceptual framework and its essential components

Associated to various restrictions stated in the previous sections, when the conceptual

framework entails the involvement of accounting concerns most often there is arousal

of various financial estimation of a particular asset

Conclusively, the conceptual framework regards more on financial linked concepts.

Considering this, the CF will specifically highlight certain performance processes including

social and ecological features. Additionally, with the assessment of the financial performance

processes, the conceptual framework highly conveys financial assessor concepts based on the

corporate performance processes.

a. The conceptual framework application

i. Explanation of how the conceptual framework has been applied by the selected

Australian Company

In this section there will be an analysis of the number of statements that have been prepare

based on the conceptual framework and its essential components

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Event Hospitality and Tsogo Analysis 8

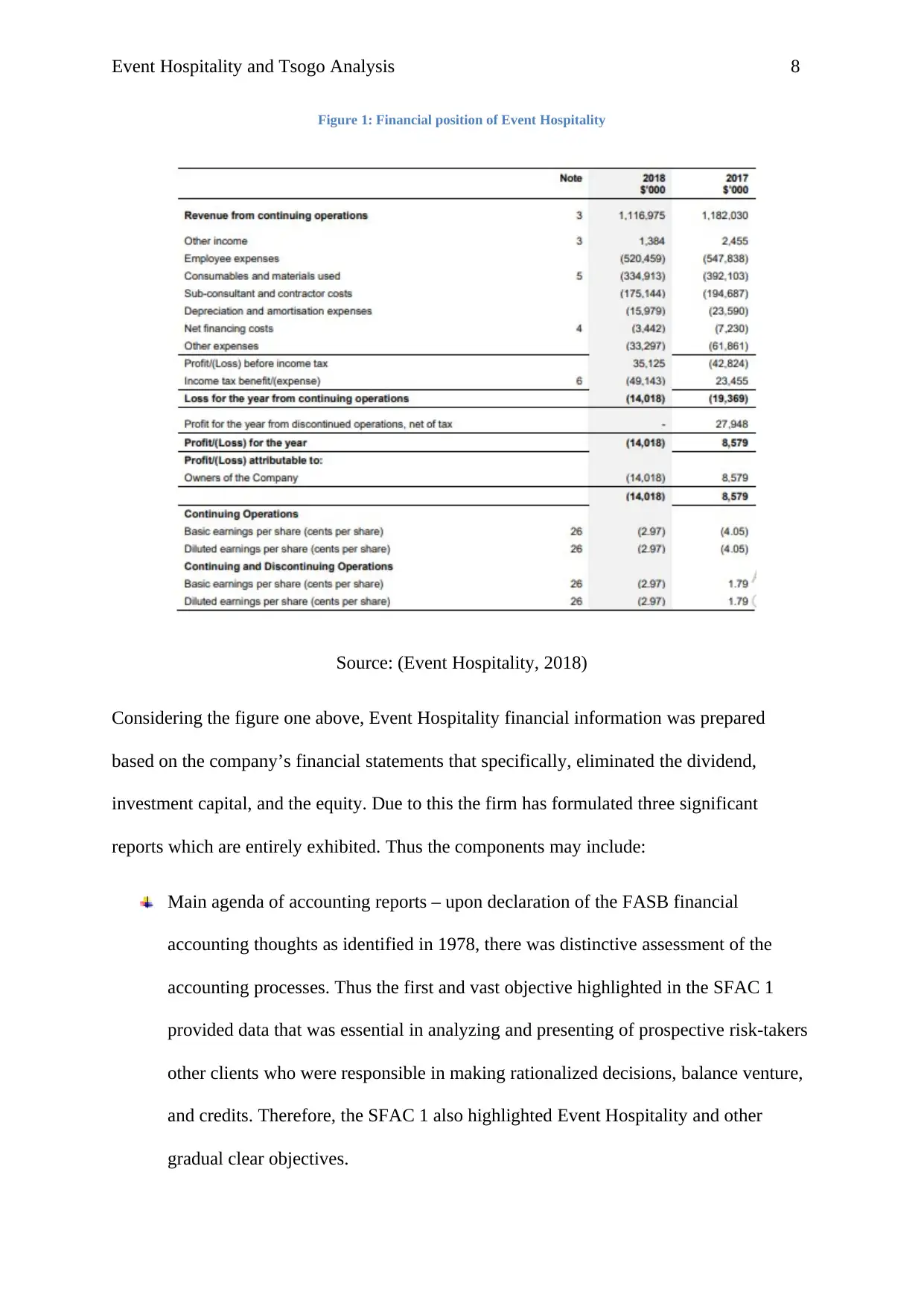

Figure 1: Financial position of Event Hospitality

Source: (Event Hospitality, 2018)

Considering the figure one above, Event Hospitality financial information was prepared

based on the company’s financial statements that specifically, eliminated the dividend,

investment capital, and the equity. Due to this the firm has formulated three significant

reports which are entirely exhibited. Thus the components may include:

Main agenda of accounting reports – upon declaration of the FASB financial

accounting thoughts as identified in 1978, there was distinctive assessment of the

accounting processes. Thus the first and vast objective highlighted in the SFAC 1

provided data that was essential in analyzing and presenting of prospective risk-takers

other clients who were responsible in making rationalized decisions, balance venture,

and credits. Therefore, the SFAC 1 also highlighted Event Hospitality and other

gradual clear objectives.

Figure 1: Financial position of Event Hospitality

Source: (Event Hospitality, 2018)

Considering the figure one above, Event Hospitality financial information was prepared

based on the company’s financial statements that specifically, eliminated the dividend,

investment capital, and the equity. Due to this the firm has formulated three significant

reports which are entirely exhibited. Thus the components may include:

Main agenda of accounting reports – upon declaration of the FASB financial

accounting thoughts as identified in 1978, there was distinctive assessment of the

accounting processes. Thus the first and vast objective highlighted in the SFAC 1

provided data that was essential in analyzing and presenting of prospective risk-takers

other clients who were responsible in making rationalized decisions, balance venture,

and credits. Therefore, the SFAC 1 also highlighted Event Hospitality and other

gradual clear objectives.

Event Hospitality and Tsogo Analysis 9

Useful financial information features – in this case the second section in the

conceptual framework is inclusive of the characteristics and financial data established

which is highly valuable in making managerial decisions. According to section 2 of

the SFAC, FASB portrays useful information which is reliable, essential and equal.

On the other hand, all data is appropriate considering the fact that it may have

influence of certain choices. Thus the data may have such characteristics due to the

fact that it may influence prospective choices outcomes and have influence over the

specific decisions.

Elements of financial statements – thus a different progression in structuring the

conceptual framework is deciding on essential components of a report budget. This

will take into account characterizing of various Event Hospitality information

regarding the acquired monetary reports. The FASB financial summaries take into

account the important elements such as liabilities, assets, income, and other additional

costs.

Assessment of financials and recognition – based on the SFAC 3, it entails

approximation of business projects, whereby the FASB has set aside various ideas

used in the selection when different things should have been introduced or professed

within the financial statements, and the methods used in allotting different numbers

within the financial groups.

ii. Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities?

Normally, various data should be perceived as stated by the FASB in attaining certain

objectives, they include:

Position – information concerning this is entitled to have adverse effect on customer

choices

Useful financial information features – in this case the second section in the

conceptual framework is inclusive of the characteristics and financial data established

which is highly valuable in making managerial decisions. According to section 2 of

the SFAC, FASB portrays useful information which is reliable, essential and equal.

On the other hand, all data is appropriate considering the fact that it may have

influence of certain choices. Thus the data may have such characteristics due to the

fact that it may influence prospective choices outcomes and have influence over the

specific decisions.

Elements of financial statements – thus a different progression in structuring the

conceptual framework is deciding on essential components of a report budget. This

will take into account characterizing of various Event Hospitality information

regarding the acquired monetary reports. The FASB financial summaries take into

account the important elements such as liabilities, assets, income, and other additional

costs.

Assessment of financials and recognition – based on the SFAC 3, it entails

approximation of business projects, whereby the FASB has set aside various ideas

used in the selection when different things should have been introduced or professed

within the financial statements, and the methods used in allotting different numbers

within the financial groups.

ii. Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities?

Normally, various data should be perceived as stated by the FASB in attaining certain

objectives, they include:

Position – information concerning this is entitled to have adverse effect on customer

choices

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Event Hospitality and Tsogo Analysis 10

Characterization – meeting the connotation of various budgetary reports

Dependability – thus EVT information is irrefutable, resolute, and not partial

Measurability – it is significant quality quantifiable using enough dependability

According to the FASB accounting rules there is expression of entire budget summaries

which are wholly explained and shown. Some of the relevant data shown include the profit or

the whole period, money associated positions and entire income salary for the period. Hence

the new thought is diverse compared to profit and takes into account adjustment in

entrepreneur value aside from other that resulted due to transfers noticed by the proprietors.

Various transitions in asset regards are included in this notion although are stripped of from

Event Hospitality revenue.

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?

Generally quantitative characteristic basically highlight firm’s financial statements as shown

below:

Performance of the subjective attributes – in order to come up with an approximation gadget,

previous writings were employed that involved quality considering upgrading and crucial

characteristics that were convenient to the ED (Timbate, & Park, 2018). The primary subject

qualities are essential and tell the amount of funds linked to certain information.

Significance – importance is a characteristic that a company refers based on the capability of

understanding certain matters elevated by customers as contractors of capital within a firm.

Based on previous literatures, the application of various operations inclusive of various

certain accounting features symbolize collaborative and psychic framework. Considering the

analysis in the paper, most accountants assess keenly the financial income quality rather that

the accounting reporting. This concept is limited as non-financial data is neglected and

Characterization – meeting the connotation of various budgetary reports

Dependability – thus EVT information is irrefutable, resolute, and not partial

Measurability – it is significant quality quantifiable using enough dependability

According to the FASB accounting rules there is expression of entire budget summaries

which are wholly explained and shown. Some of the relevant data shown include the profit or

the whole period, money associated positions and entire income salary for the period. Hence

the new thought is diverse compared to profit and takes into account adjustment in

entrepreneur value aside from other that resulted due to transfers noticed by the proprietors.

Various transitions in asset regards are included in this notion although are stripped of from

Event Hospitality revenue.

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?

Generally quantitative characteristic basically highlight firm’s financial statements as shown

below:

Performance of the subjective attributes – in order to come up with an approximation gadget,

previous writings were employed that involved quality considering upgrading and crucial

characteristics that were convenient to the ED (Timbate, & Park, 2018). The primary subject

qualities are essential and tell the amount of funds linked to certain information.

Significance – importance is a characteristic that a company refers based on the capability of

understanding certain matters elevated by customers as contractors of capital within a firm.

Based on previous literatures, the application of various operations inclusive of various

certain accounting features symbolize collaborative and psychic framework. Considering the

analysis in the paper, most accountants assess keenly the financial income quality rather that

the accounting reporting. This concept is limited as non-financial data is neglected and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Event Hospitality and Tsogo Analysis 11

prospective financial information would be accessible to the stakeholders. Thus for

improvement of quality, vast and detailed research of Event Hospitality financial statements

have to be done (Soyka, 2013).

Part B: Sustainability and Integrated Financial Reporting

i. Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Worldwide integrated reporting systems are relevant in the business today. Therefore, the

main role of organizations is expanding considering its underlying commitment of assessing

its financial benefit or recording funds. Hence sustainable accounting reporting rules exhibits

the important gauges appropriate in assisting organizations in creating a competitive based

strategy. Moreover, international integrated reporting Systems improve the company’s repute

hence firm’s productivity can be assessed dependent on worldwide standards and policies.

Therefore, various reporting requires financial specialists to build strong relationship with the

bookkeeping and non-bookkeeping information experts to have the option to viably assess

potential risks. Various associations have vigorously started to get prompt reports in various

designs and each report has been moulded according to the prerequisites of business

properties. Additionally, incorporated declaring gauges and principles have been appropriated

by the international integrated board for the provision of guidance to report various assessors.

ii. Rigor (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strength

Prospective accounting techniques and methods focused on the conceptual framework are

effectively used in making prospective financial statements, thus improving sustainability of

various firms (Cantele, Tsalis, & Nikolaou, 2018). This strength helps in using the conceptual

prospective financial information would be accessible to the stakeholders. Thus for

improvement of quality, vast and detailed research of Event Hospitality financial statements

have to be done (Soyka, 2013).

Part B: Sustainability and Integrated Financial Reporting

i. Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Worldwide integrated reporting systems are relevant in the business today. Therefore, the

main role of organizations is expanding considering its underlying commitment of assessing

its financial benefit or recording funds. Hence sustainable accounting reporting rules exhibits

the important gauges appropriate in assisting organizations in creating a competitive based

strategy. Moreover, international integrated reporting Systems improve the company’s repute

hence firm’s productivity can be assessed dependent on worldwide standards and policies.

Therefore, various reporting requires financial specialists to build strong relationship with the

bookkeeping and non-bookkeeping information experts to have the option to viably assess

potential risks. Various associations have vigorously started to get prompt reports in various

designs and each report has been moulded according to the prerequisites of business

properties. Additionally, incorporated declaring gauges and principles have been appropriated

by the international integrated board for the provision of guidance to report various assessors.

ii. Rigor (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strength

Prospective accounting techniques and methods focused on the conceptual framework are

effectively used in making prospective financial statements, thus improving sustainability of

various firms (Cantele, Tsalis, & Nikolaou, 2018). This strength helps in using the conceptual

Event Hospitality and Tsogo Analysis 12

framework for making accounting standards and global integrated reports, that specifically

point out essential aspects of financial data (Pérez-López, Moreno-Romero, & Barkemeyer,

2013).

Constraints

Incapacitated Fundamental administration: Convectional bookkeeping offers choice boss

little information on an affiliation's claims to fame. This is in light of the fact that the kind of

utilization the arranging method errands is hypothetical and isn't strong for settling on explicit

decisions. This forces boss in governments and affiliations using conventional arranging

methodologies to change their game plans consistently, so as to strengthen their decisions.

i. Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Association budgetary analysists around the world use institutional hypothesis or neo-

institutional hypothesis in their investigation to show that foundations of financial, social,

enlightening, cash related, and political nature keeps up a tremendous effect upon generally

speaking affiliations. Results show that coordinated uncovering is exceedingly connected

with the period of money related improvement, national corporate obligation, countries'

characteristics system, laborer's organizations, the private utilization of tertiary preparing,

ownership dispersing. The arrangement creators fail to show the effect of the political factor,

underlining the abnormality of data as for the years for which information has been

assembled, given the manner in which that the examination does not consider the

presumption of huge changes in the political system.

ii. Preparation of an index (a table or checklist) of various components (criteria) of an

integrated report, and discussion of whether and how the selected South African

Company has disclosed information against each of those components (criteria)

framework for making accounting standards and global integrated reports, that specifically

point out essential aspects of financial data (Pérez-López, Moreno-Romero, & Barkemeyer,

2013).

Constraints

Incapacitated Fundamental administration: Convectional bookkeeping offers choice boss

little information on an affiliation's claims to fame. This is in light of the fact that the kind of

utilization the arranging method errands is hypothetical and isn't strong for settling on explicit

decisions. This forces boss in governments and affiliations using conventional arranging

methodologies to change their game plans consistently, so as to strengthen their decisions.

i. Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Association budgetary analysists around the world use institutional hypothesis or neo-

institutional hypothesis in their investigation to show that foundations of financial, social,

enlightening, cash related, and political nature keeps up a tremendous effect upon generally

speaking affiliations. Results show that coordinated uncovering is exceedingly connected

with the period of money related improvement, national corporate obligation, countries'

characteristics system, laborer's organizations, the private utilization of tertiary preparing,

ownership dispersing. The arrangement creators fail to show the effect of the political factor,

underlining the abnormality of data as for the years for which information has been

assembled, given the manner in which that the examination does not consider the

presumption of huge changes in the political system.

ii. Preparation of an index (a table or checklist) of various components (criteria) of an

integrated report, and discussion of whether and how the selected South African

Company has disclosed information against each of those components (criteria)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.