Comparative Analysis of Executive Remuneration: Saracen vs Newcrest

VerifiedAdded on 2023/06/07

|11

|1764

|149

Report

AI Summary

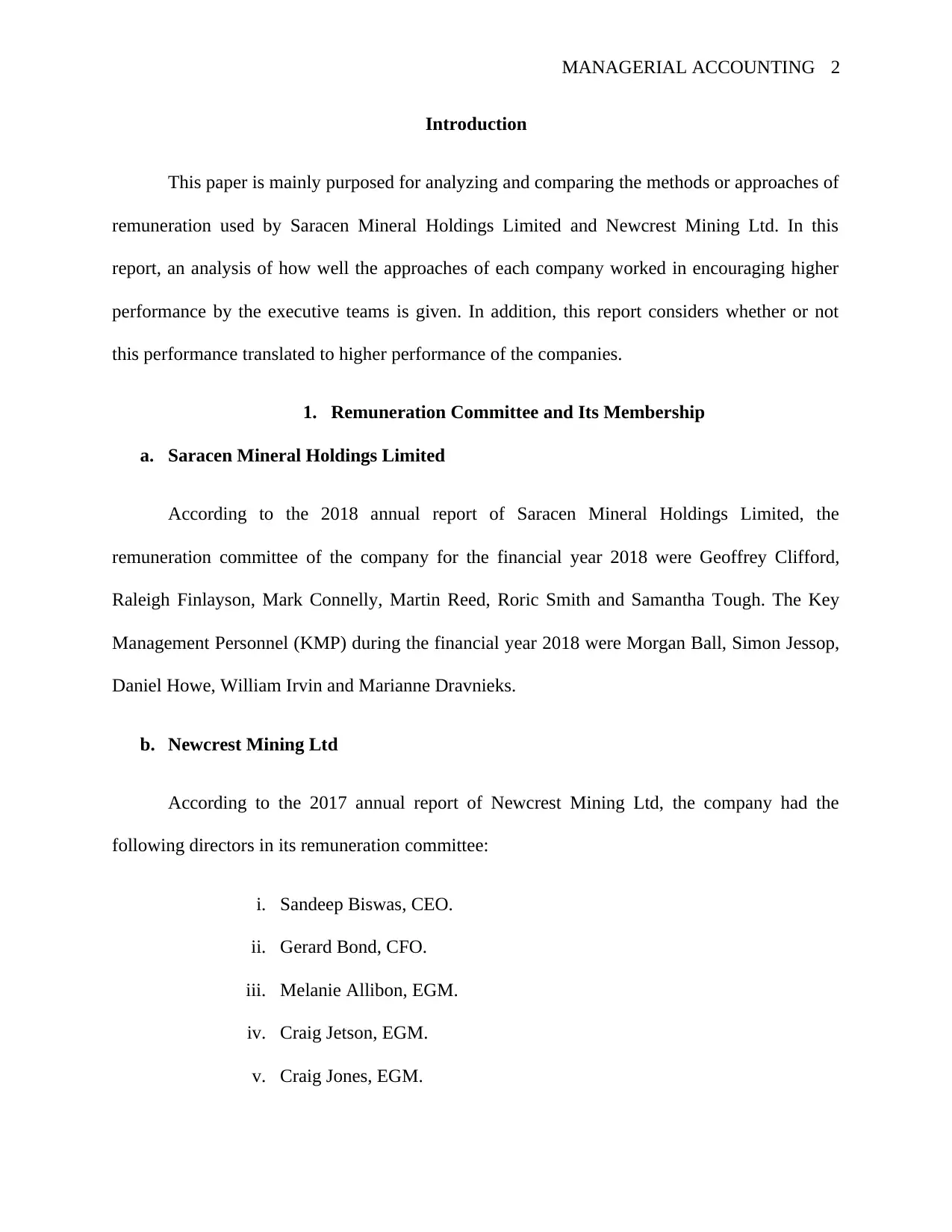

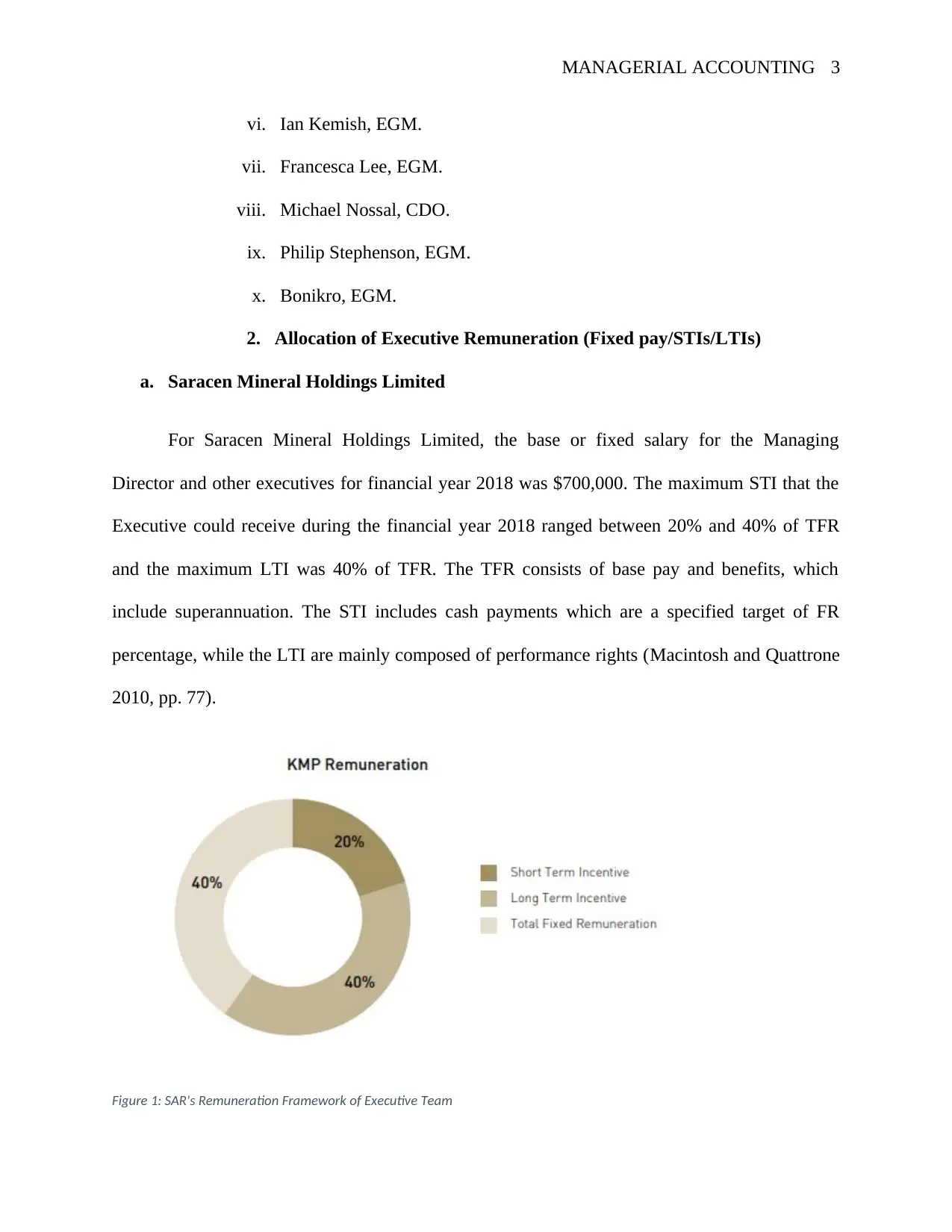

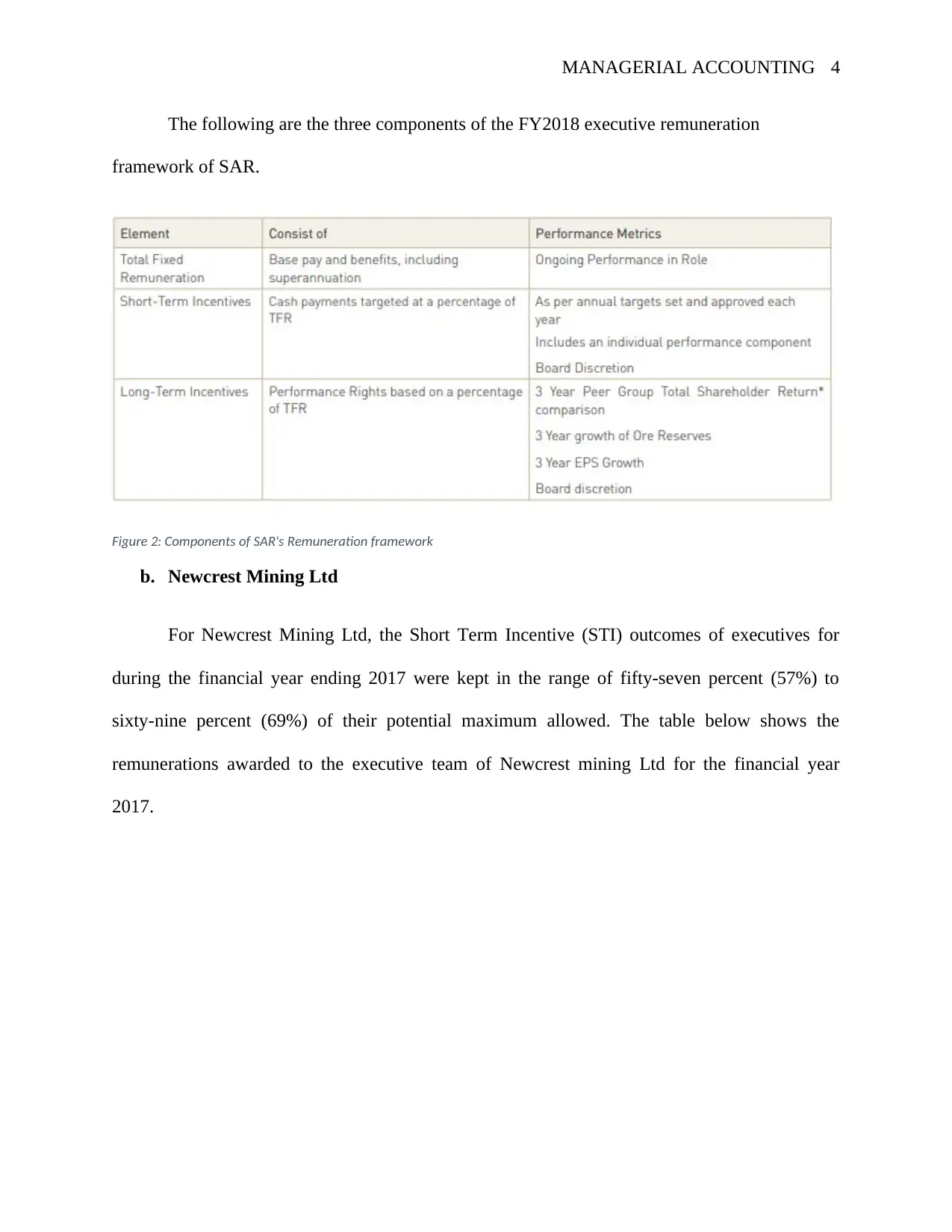

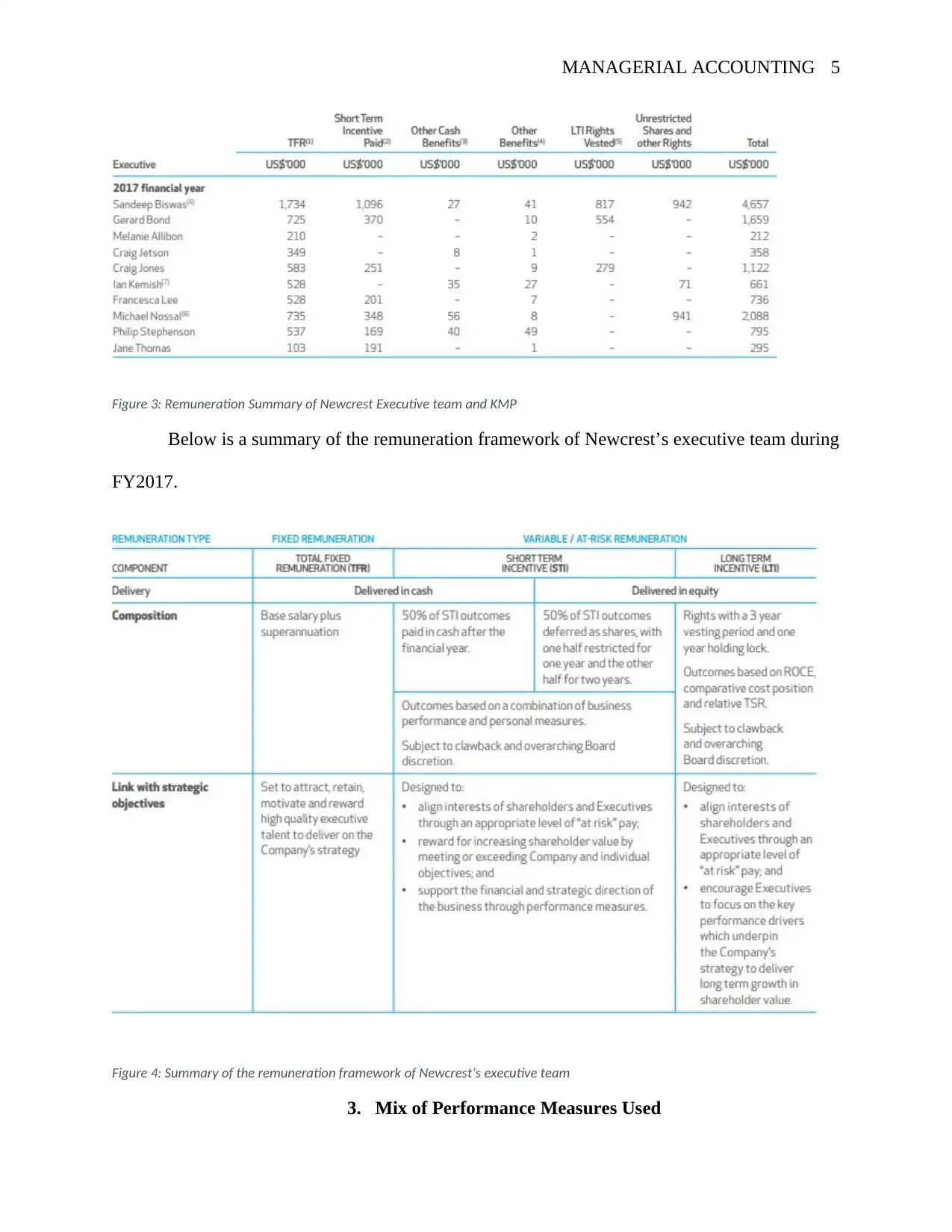

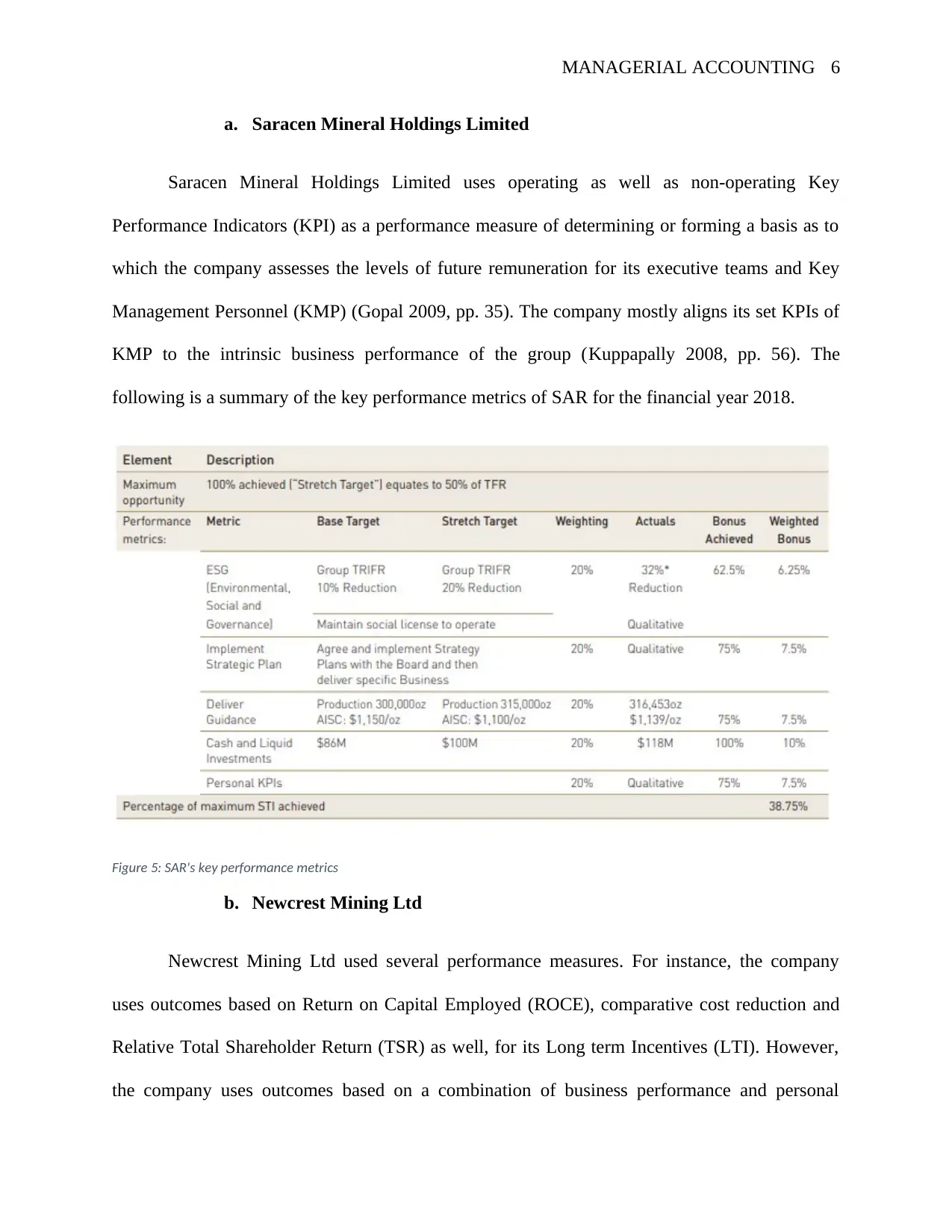

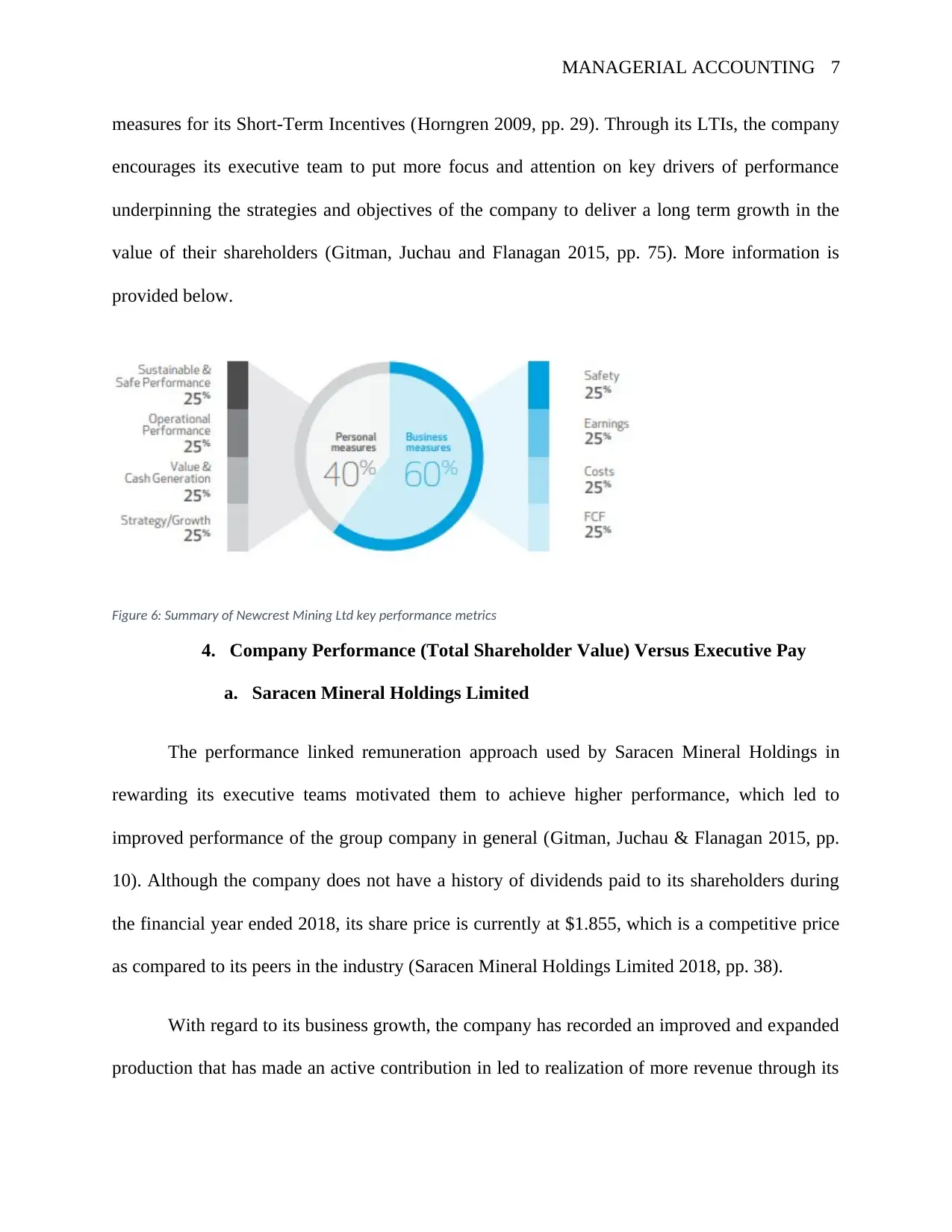

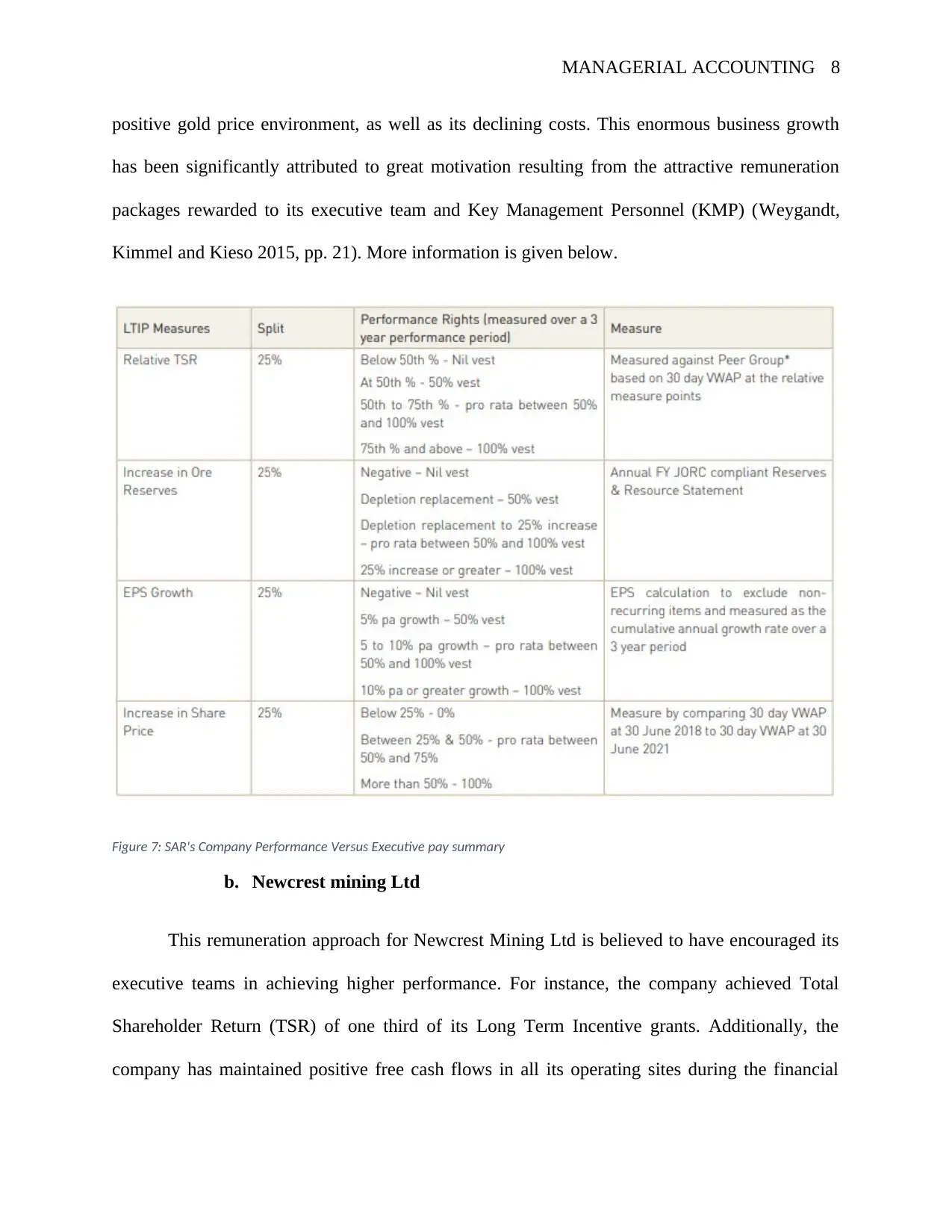

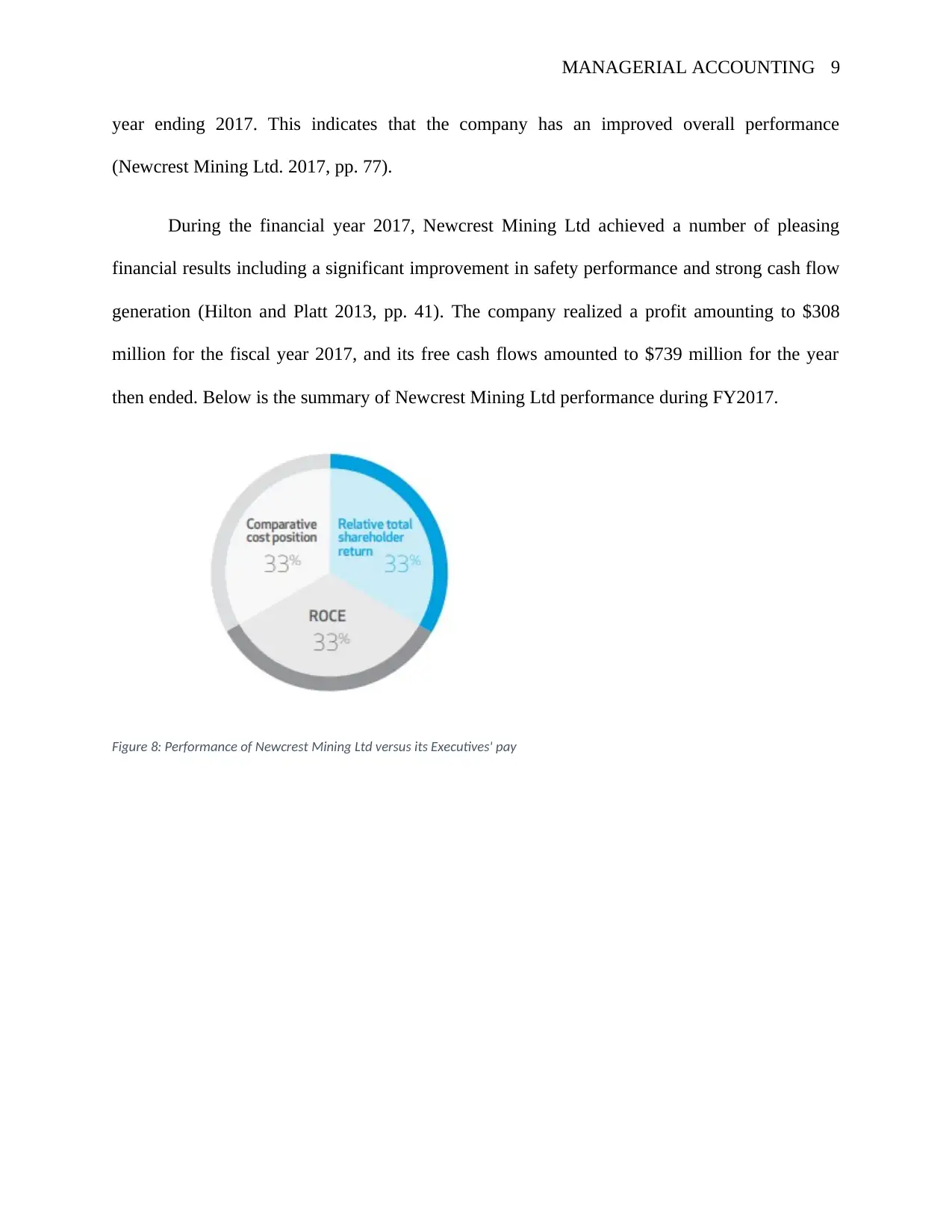

This report analyzes and compares the remuneration methods used by Saracen Mineral Holdings Limited and Newcrest Mining Ltd, evaluating their effectiveness in incentivizing executive performance and contributing to overall company success. It examines the composition of remuneration committees, the allocation of fixed pay, short-term incentives (STIs), and long-term incentives (LTIs), and the specific performance measures employed by each company, including both operating and non-operating KPIs. The report further assesses the correlation between company performance, measured by total shareholder value, and executive pay, highlighting instances where performance-linked remuneration motivated improved results. Ultimately, the study concludes that while the approaches of the two companies are similar, they differ in the specifics of incentive structures and performance metrics, both aiming to align executive interests with shareholder value.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.