Auditing 12 Report: Analyzing Executive Performance and Remuneration

VerifiedAdded on 2021/05/31

|13

|2885

|78

Report

AI Summary

This report, prepared for an Auditing 12 assignment, evaluates executive performance and remuneration in public companies, focusing on the National Australia Bank (NAB). The report begins with an introduction to the topic and a review of relevant literature on short-term and long-term incentive (STI and LTI) methods, including bonus schemes, share options, and non-financial measures. The report then analyzes NAB's remuneration practices, examining its STI and LTI plans, performance measures (such as cash return on equity and total shareholder return), and the allocation methodologies used. Findings reveal differences between methods discussed in literature and practical applications. The report concludes with recommendations for improving performance measures and a focus on aligning employee performance with compensation plans. This report is a comprehensive analysis of executive compensation strategies.

Running head: ACCOUNTING

Accounting

University Name

Student Name

Authors’ Note

Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDITING

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................5

Review of literature:...................................................................................................................5

Company review:.......................................................................................................................6

Summary of findings:.................................................................................................................8

Analysis of remuneration method used:.....................................................................................8

Recommendation:....................................................................................................................12

Conclusion:..............................................................................................................................12

References lists:.......................................................................................................................14

AUDITING

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................5

Review of literature:...................................................................................................................5

Company review:.......................................................................................................................6

Summary of findings:.................................................................................................................8

Analysis of remuneration method used:.....................................................................................8

Recommendation:....................................................................................................................12

Conclusion:..............................................................................................................................12

References lists:.......................................................................................................................14

3

AUDITING

Introduction:

The report is prepared for evaluating the performance of executives and remuneration

in public companies. Research on this particular topic is conducted by reviewing the literature

on the method used for measuring the performance of management. The purpose of report is

to analyze the available information on literature review on the several methods used by

public companies to calculate the performance pay. In addition to this, research is also

conducted on the annual report of chosen organition for reviewing the management

performance measures used. Chosen organization for analyzing the method used for

remuneration is National Australia Bank (NAB) that is one of the largest financial institutions

operating in Australia in terms of earning generated, market capitalization and total number

of customers served (Armstrong and Taylor 2014). The method used for computing long term

incentive and short term incentive for measuring the performance used by NAB are evaluated

by reviewing the annual report of organization.

Discussion:

Review of literature:

Short term incentives are referred to as incentive schemes where the payments are

done in cash such as gain share, profit share, bonus scheme and commission and the

measurement period is around one year. Some of the methods that are used by organization in

plan of short term incentives are bonus scheme, gain sharing scheme and profit sharing

scheme. The nature of these performance criteria can be qualitative, quantitative, financial

and non financial. The plan of profit sharing helps employees to become acquainted with

profit margin and focus on bottom line. A portion of pre tax profit is put by organization that

is distributed among employees. A larger percentage of profits are received by employees

with higher percentage profits (Demerouti et al. 2014). However, such type of plan results in

AUDITING

Introduction:

The report is prepared for evaluating the performance of executives and remuneration

in public companies. Research on this particular topic is conducted by reviewing the literature

on the method used for measuring the performance of management. The purpose of report is

to analyze the available information on literature review on the several methods used by

public companies to calculate the performance pay. In addition to this, research is also

conducted on the annual report of chosen organition for reviewing the management

performance measures used. Chosen organization for analyzing the method used for

remuneration is National Australia Bank (NAB) that is one of the largest financial institutions

operating in Australia in terms of earning generated, market capitalization and total number

of customers served (Armstrong and Taylor 2014). The method used for computing long term

incentive and short term incentive for measuring the performance used by NAB are evaluated

by reviewing the annual report of organization.

Discussion:

Review of literature:

Short term incentives are referred to as incentive schemes where the payments are

done in cash such as gain share, profit share, bonus scheme and commission and the

measurement period is around one year. Some of the methods that are used by organization in

plan of short term incentives are bonus scheme, gain sharing scheme and profit sharing

scheme. The nature of these performance criteria can be qualitative, quantitative, financial

and non financial. The plan of profit sharing helps employees to become acquainted with

profit margin and focus on bottom line. A portion of pre tax profit is put by organization that

is distributed among employees. A larger percentage of profits are received by employees

with higher percentage profits (Demerouti et al. 2014). However, such type of plan results in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDITING

higher labour cost in event of better performance of organization and lower labour cost when

organization is facing economic downturn.

The long term incentive (LTI) plans are often based on options and stock. In such

plants, the rights of executive to obtain stocks or exercise or receive options are associated

with measure of performance. Executives are granted with options or stock when the target

values are achieved by executives for the specified measure of performance. Operations of

long tem incentive plans are done especially for executives as an incentive for improving

incentive. Furthermore, it also provides the opportunity to reduce the fixed costs. The

schemes that is generally used by organization bonus linked to long term performance for

encouraging focus on long term goals (Pepper and Gore 2015). It also involves share option

plans for promoting the convergence of interest of executives and stakeholders. LTI are

offered to incentives for increasing long term focus of organization and thereby aligning the

interest of shareholder of companies and interest of executives. The LTI is faced with the

challenge is associated with the extent to which it is felt by employees that their performance

are associated with the level of reward. The link between LTI and individual performance

may be regarded potentially weaker than other form of compensation as such plan are

generally limited to higher level of employees who arguably directly impact the performance

of firms (Beer et al. 2015). Moreover, employees who are provided with LTI are not able to

derive immediate value as it generally has restriction on cash.

Organization can also make use of some non financial measure for measuring the

performance of employees. Some of the non financial measures involve development of

workforce, customer satisfaction, product quality, employee satisfaction, productivity and

efficiency. The length of long term inventive plan varies from one year to six years

(Friedman 2017).

AUDITING

higher labour cost in event of better performance of organization and lower labour cost when

organization is facing economic downturn.

The long term incentive (LTI) plans are often based on options and stock. In such

plants, the rights of executive to obtain stocks or exercise or receive options are associated

with measure of performance. Executives are granted with options or stock when the target

values are achieved by executives for the specified measure of performance. Operations of

long tem incentive plans are done especially for executives as an incentive for improving

incentive. Furthermore, it also provides the opportunity to reduce the fixed costs. The

schemes that is generally used by organization bonus linked to long term performance for

encouraging focus on long term goals (Pepper and Gore 2015). It also involves share option

plans for promoting the convergence of interest of executives and stakeholders. LTI are

offered to incentives for increasing long term focus of organization and thereby aligning the

interest of shareholder of companies and interest of executives. The LTI is faced with the

challenge is associated with the extent to which it is felt by employees that their performance

are associated with the level of reward. The link between LTI and individual performance

may be regarded potentially weaker than other form of compensation as such plan are

generally limited to higher level of employees who arguably directly impact the performance

of firms (Beer et al. 2015). Moreover, employees who are provided with LTI are not able to

derive immediate value as it generally has restriction on cash.

Organization can also make use of some non financial measure for measuring the

performance of employees. Some of the non financial measures involve development of

workforce, customer satisfaction, product quality, employee satisfaction, productivity and

efficiency. The length of long term inventive plan varies from one year to six years

(Friedman 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDITING

Company review:

National Australia bank is the financial service providers of Australia that intend to

achieve their business objectives by building relationship in segments such as medium and

small businesses and deliver greater customer experience. The remuneration decision within

the organization is supported by way of easing leaders and lead to embedding and

introduction of a new market based pay range methodology. Remuneration policy of

company is built around creating linkage for rewarding value of shareholders and retaining

and attracting high performing employees.

Long term incentives plan of NAB takes the form of performance rights that assist in

aligning the long term performance of group with decision of management by using

challenging performance hurdles. Senior executives across the group are awarded with

executive LTI program. Maximum opportunity of LTI is set with reference to external and

internal relativities for executives who must meet the minimum conduct and performance

threshold (Shields et al. 2015). The performance measure that is used for awarding LTI is the

total shareholder return and cash return on equity growth. Allocation of LTI is done under the

LTI program of group in the form of performance rights. The performance right associated

with LTI is a performance right that is granted under the plan and is subjected to long term

performance hurdles. For grant of year 2017, the allocation methodology for LTI has been

changes from fair value to face value that helps in determining the number of performance

rights. LTI is based on minimum grant value of 130% of fixed remuneration.

AUDITING

Company review:

National Australia bank is the financial service providers of Australia that intend to

achieve their business objectives by building relationship in segments such as medium and

small businesses and deliver greater customer experience. The remuneration decision within

the organization is supported by way of easing leaders and lead to embedding and

introduction of a new market based pay range methodology. Remuneration policy of

company is built around creating linkage for rewarding value of shareholders and retaining

and attracting high performing employees.

Long term incentives plan of NAB takes the form of performance rights that assist in

aligning the long term performance of group with decision of management by using

challenging performance hurdles. Senior executives across the group are awarded with

executive LTI program. Maximum opportunity of LTI is set with reference to external and

internal relativities for executives who must meet the minimum conduct and performance

threshold (Shields et al. 2015). The performance measure that is used for awarding LTI is the

total shareholder return and cash return on equity growth. Allocation of LTI is done under the

LTI program of group in the form of performance rights. The performance right associated

with LTI is a performance right that is granted under the plan and is subjected to long term

performance hurdles. For grant of year 2017, the allocation methodology for LTI has been

changes from fair value to face value that helps in determining the number of performance

rights. LTI is based on minimum grant value of 130% of fixed remuneration.

6

AUDITING

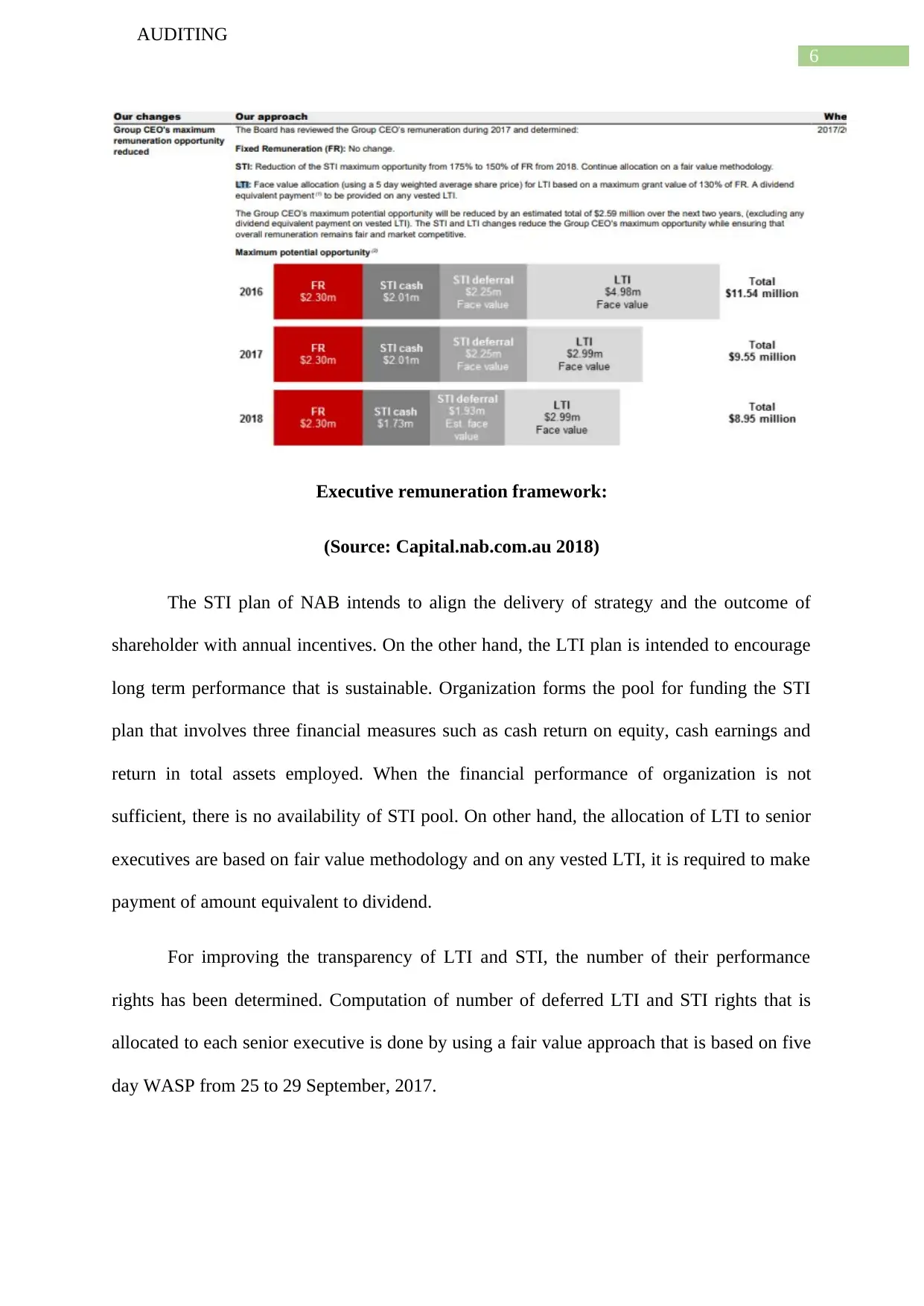

Executive remuneration framework:

(Source: Capital.nab.com.au 2018)

The STI plan of NAB intends to align the delivery of strategy and the outcome of

shareholder with annual incentives. On the other hand, the LTI plan is intended to encourage

long term performance that is sustainable. Organization forms the pool for funding the STI

plan that involves three financial measures such as cash return on equity, cash earnings and

return in total assets employed. When the financial performance of organization is not

sufficient, there is no availability of STI pool. On other hand, the allocation of LTI to senior

executives are based on fair value methodology and on any vested LTI, it is required to make

payment of amount equivalent to dividend.

For improving the transparency of LTI and STI, the number of their performance

rights has been determined. Computation of number of deferred LTI and STI rights that is

allocated to each senior executive is done by using a fair value approach that is based on five

day WASP from 25 to 29 September, 2017.

AUDITING

Executive remuneration framework:

(Source: Capital.nab.com.au 2018)

The STI plan of NAB intends to align the delivery of strategy and the outcome of

shareholder with annual incentives. On the other hand, the LTI plan is intended to encourage

long term performance that is sustainable. Organization forms the pool for funding the STI

plan that involves three financial measures such as cash return on equity, cash earnings and

return in total assets employed. When the financial performance of organization is not

sufficient, there is no availability of STI pool. On other hand, the allocation of LTI to senior

executives are based on fair value methodology and on any vested LTI, it is required to make

payment of amount equivalent to dividend.

For improving the transparency of LTI and STI, the number of their performance

rights has been determined. Computation of number of deferred LTI and STI rights that is

allocated to each senior executive is done by using a fair value approach that is based on five

day WASP from 25 to 29 September, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDITING

Summary of findings:

Reviewing the literature on the methods used for computing the short and long term

incentives payable to executives provides with the answer that there are several measures that

are available and take into account different concepts. From the analysis of the information

gained from annual report of National Australia bank and literature review on the available

methods and performance measures, it can be inferred that there exist considerable amount of

difference between the methods that are used practically and methods discussed in literature

review. Higher payment is made by company for motivating lower level executives so that

they are able to perform better and thereby contribute to overall performance of company.

Analysis of remuneration method used:

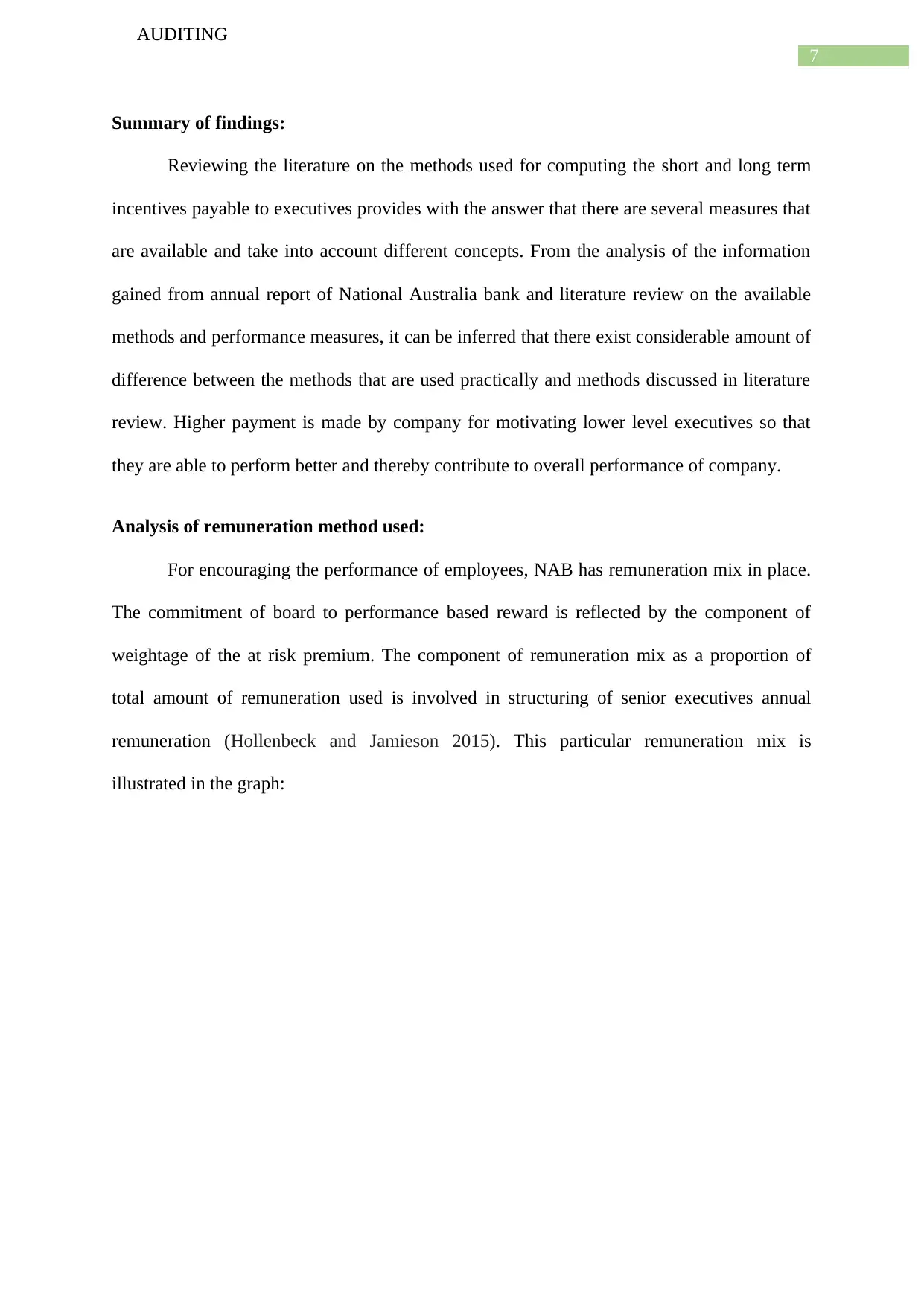

For encouraging the performance of employees, NAB has remuneration mix in place.

The commitment of board to performance based reward is reflected by the component of

weightage of the at risk premium. The component of remuneration mix as a proportion of

total amount of remuneration used is involved in structuring of senior executives annual

remuneration (Hollenbeck and Jamieson 2015). This particular remuneration mix is

illustrated in the graph:

AUDITING

Summary of findings:

Reviewing the literature on the methods used for computing the short and long term

incentives payable to executives provides with the answer that there are several measures that

are available and take into account different concepts. From the analysis of the information

gained from annual report of National Australia bank and literature review on the available

methods and performance measures, it can be inferred that there exist considerable amount of

difference between the methods that are used practically and methods discussed in literature

review. Higher payment is made by company for motivating lower level executives so that

they are able to perform better and thereby contribute to overall performance of company.

Analysis of remuneration method used:

For encouraging the performance of employees, NAB has remuneration mix in place.

The commitment of board to performance based reward is reflected by the component of

weightage of the at risk premium. The component of remuneration mix as a proportion of

total amount of remuneration used is involved in structuring of senior executives annual

remuneration (Hollenbeck and Jamieson 2015). This particular remuneration mix is

illustrated in the graph:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDITING

Remuneration mix for encouraging performance:

(Source: Capital.nab.com.au 2018)

Chief legal and chief executive officer plays a very important role in maintaining the

oversight of risk and financial performance of employees and group. The reward mix for such

roles is structured that helps in recognizing the responsibilities and supporting the

independence roles by offering higher proportion of fixed amount of remuneration. Great

emphasis is placed on the component of LTI rather than STI of their variable reward. Some

of the financial performance measures used by NAB include statutory return on equity, cash

earnings, net interest margin, average equity, average assets and average interest earning

assets (McKeown et al. 2015).

LTI and performance measures:

AUDITING

Remuneration mix for encouraging performance:

(Source: Capital.nab.com.au 2018)

Chief legal and chief executive officer plays a very important role in maintaining the

oversight of risk and financial performance of employees and group. The reward mix for such

roles is structured that helps in recognizing the responsibilities and supporting the

independence roles by offering higher proportion of fixed amount of remuneration. Great

emphasis is placed on the component of LTI rather than STI of their variable reward. Some

of the financial performance measures used by NAB include statutory return on equity, cash

earnings, net interest margin, average equity, average assets and average interest earning

assets (McKeown et al. 2015).

LTI and performance measures:

9

AUDITING

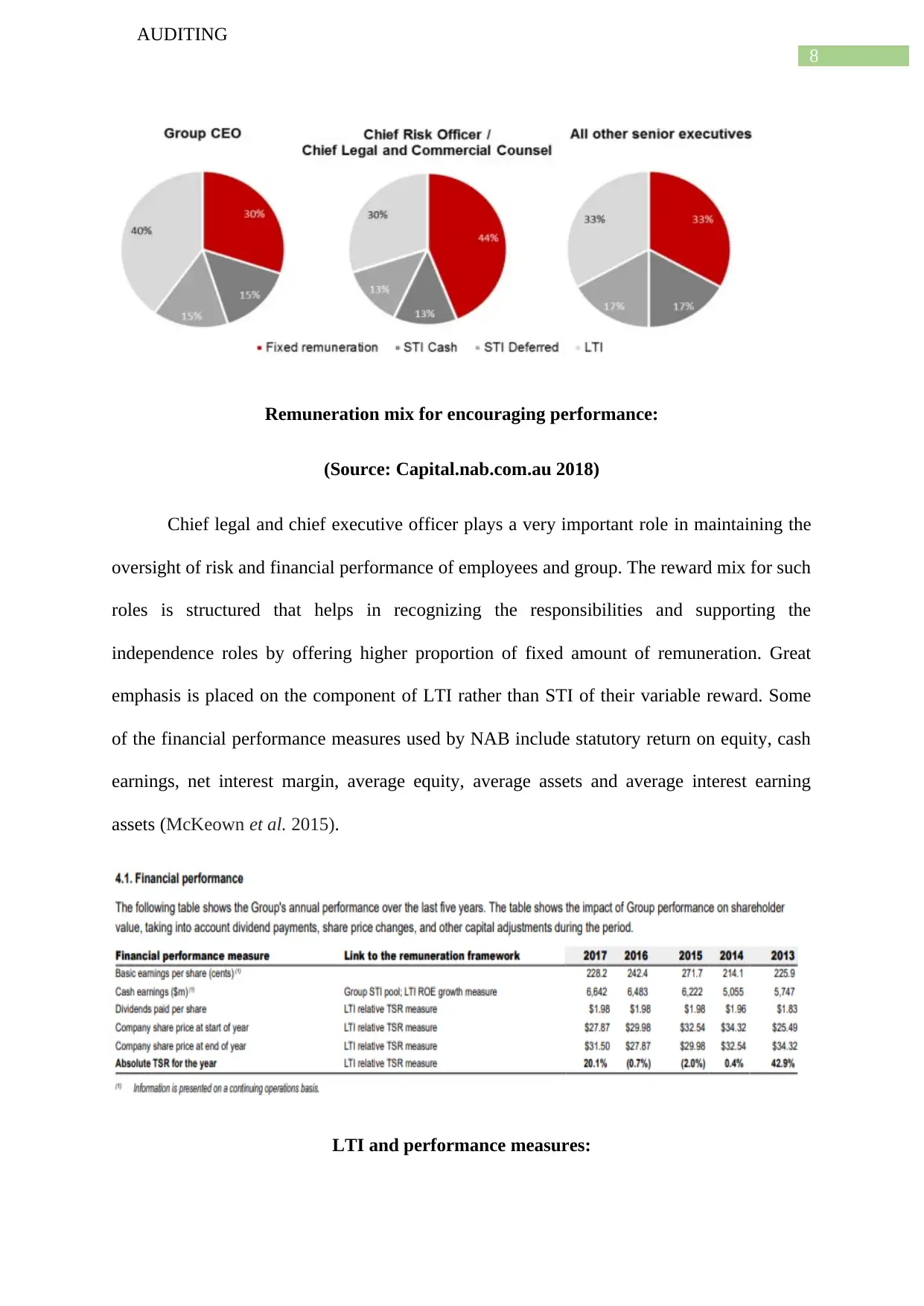

(Source: Capital.nab.com.au 2018)

The above table depicts the annual performance of organization over the last five

years on the value of shareholders by taking into account any changes in share price, dividend

payment and other adjustments in capital.

The allocation methodology used by NAB for short term incentives plan is fair value

for all senior executives. Outcome of STI ranges from 0% to maximum opportunity. 50%

deferred and 50% cash is provided as performance rights and only if the performance and

service conditions are met, then only organization vest into deferred conditions. Depending

on the allocation value, the outcome of LTI may range from 0% to 100%. Under LTI reward,

100% is provided as performance rights (Capital.nab.com.au 2018).

Remuneration of CEO of group is reviewed by the group during year 2017. The fair

value allocation methodology is used in determining the STI and there would be reduction of

maximum opportunity from 175% to 150% if fixed remuneration form year 2018. On other

hand, the LTI is determined by using face value allocation. Such allocation involves using

five day weighted average share price based maximum grant value of 130% of fixed

remuneration. This would lead to reduction of maximum potential opportunity of CEO over

the next two years by an estimated amount of $ 2.59 million. Maximum opportunity of CEO

is reduced by the changes brought in LTI and STI along with ensuring that overall

remuneration remains market competitive and fair (Capital.nab.com.au 2018).

The performance measures that is used for determining the STI incorporates cash

return on equity at the rate of 30%, cash earnings at the rate of 40% and return on total

acquired equity at the rate of 30%. This also includes adjustment based on expectation of

shareholders, risk management and financial results quality. On other hand, the performance

measures that is used for determining LTI incorporates performance period of four years,

AUDITING

(Source: Capital.nab.com.au 2018)

The above table depicts the annual performance of organization over the last five

years on the value of shareholders by taking into account any changes in share price, dividend

payment and other adjustments in capital.

The allocation methodology used by NAB for short term incentives plan is fair value

for all senior executives. Outcome of STI ranges from 0% to maximum opportunity. 50%

deferred and 50% cash is provided as performance rights and only if the performance and

service conditions are met, then only organization vest into deferred conditions. Depending

on the allocation value, the outcome of LTI may range from 0% to 100%. Under LTI reward,

100% is provided as performance rights (Capital.nab.com.au 2018).

Remuneration of CEO of group is reviewed by the group during year 2017. The fair

value allocation methodology is used in determining the STI and there would be reduction of

maximum opportunity from 175% to 150% if fixed remuneration form year 2018. On other

hand, the LTI is determined by using face value allocation. Such allocation involves using

five day weighted average share price based maximum grant value of 130% of fixed

remuneration. This would lead to reduction of maximum potential opportunity of CEO over

the next two years by an estimated amount of $ 2.59 million. Maximum opportunity of CEO

is reduced by the changes brought in LTI and STI along with ensuring that overall

remuneration remains market competitive and fair (Capital.nab.com.au 2018).

The performance measures that is used for determining the STI incorporates cash

return on equity at the rate of 30%, cash earnings at the rate of 40% and return on total

acquired equity at the rate of 30%. This also includes adjustment based on expectation of

shareholders, risk management and financial results quality. On other hand, the performance

measures that is used for determining LTI incorporates performance period of four years,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDITING

measurement against cash return on equity growth of 50% and relative total shareholder

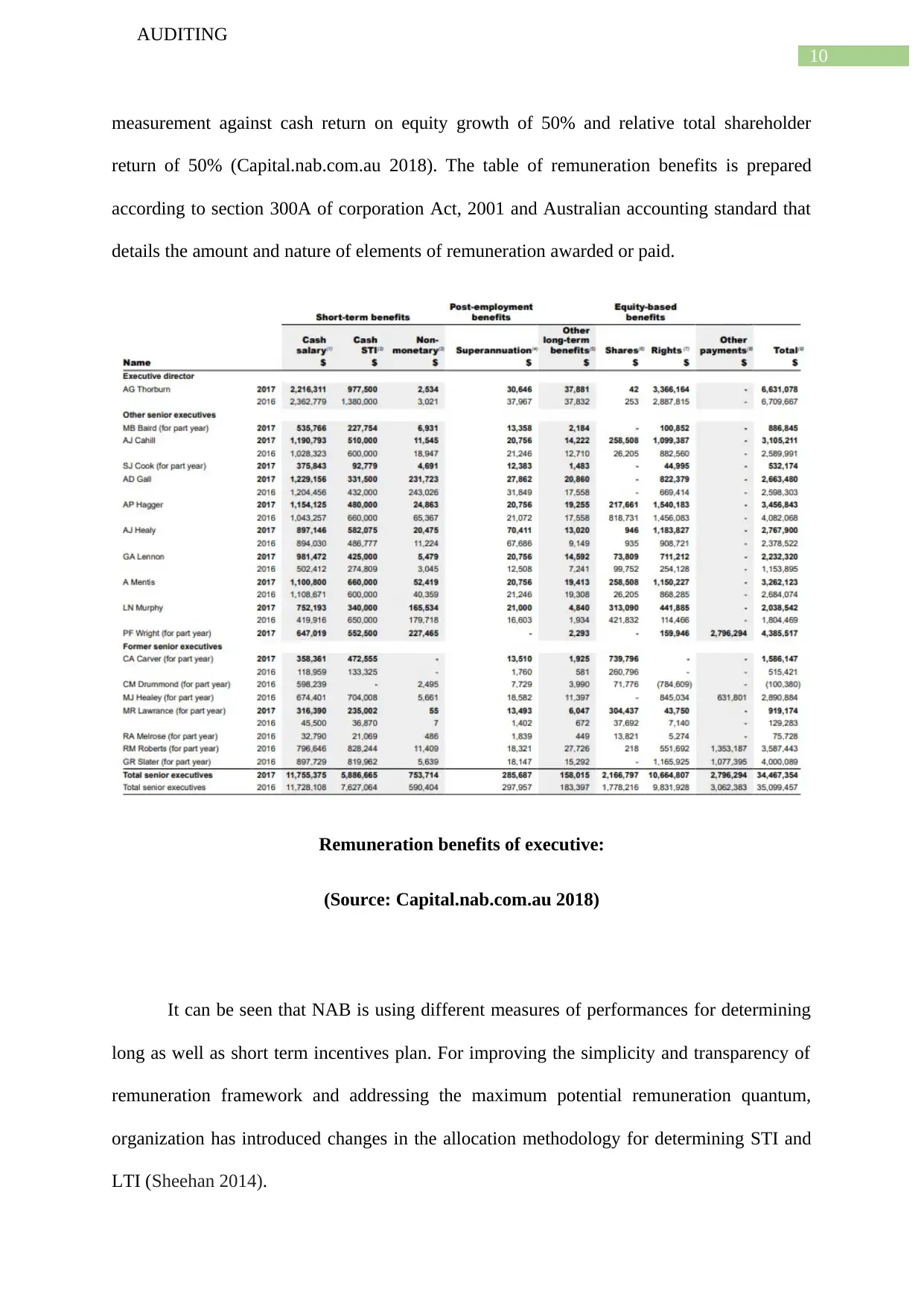

return of 50% (Capital.nab.com.au 2018). The table of remuneration benefits is prepared

according to section 300A of corporation Act, 2001 and Australian accounting standard that

details the amount and nature of elements of remuneration awarded or paid.

Remuneration benefits of executive:

(Source: Capital.nab.com.au 2018)

It can be seen that NAB is using different measures of performances for determining

long as well as short term incentives plan. For improving the simplicity and transparency of

remuneration framework and addressing the maximum potential remuneration quantum,

organization has introduced changes in the allocation methodology for determining STI and

LTI (Sheehan 2014).

AUDITING

measurement against cash return on equity growth of 50% and relative total shareholder

return of 50% (Capital.nab.com.au 2018). The table of remuneration benefits is prepared

according to section 300A of corporation Act, 2001 and Australian accounting standard that

details the amount and nature of elements of remuneration awarded or paid.

Remuneration benefits of executive:

(Source: Capital.nab.com.au 2018)

It can be seen that NAB is using different measures of performances for determining

long as well as short term incentives plan. For improving the simplicity and transparency of

remuneration framework and addressing the maximum potential remuneration quantum,

organization has introduced changes in the allocation methodology for determining STI and

LTI (Sheehan 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUDITING

Recommendation:

One of the important ways to keep track of business is to put the system of

performance management in place. Organizations seeking broadening their performance

measures should broaden their strategic business objectives that help in calculating the inputs

and gauging employee engagement. It is required by organization to develop a

comprehensive reporting strategy and measurement of human resource that should be well

aligned with the overall strategy of business. The performance measures employed by

organization can be improved by setting the benchmark and benchmarking the performance

against performance level. Such benchmarking can either be developed internally or it can be

determined by comparing with other business. Incentive plans of company should be

associated with the overall performance. Most of the research focuses on pay for performance

and whether the performance of employees is affected positively by such incentives.

Employees are motivated to perform in a better way by creating a greater link of employee

performance and rewards with compensation plan (Klettner et al. 2014).

Conclusion:

Many researchers have focused on the relationship between performance of company

and compensation of executive. Usage of executive compensation for increasing the value of

firms comes with both positive as well as negative side. In order for designing the effective

pay performance plan, the crucial factor that should be taken into by account by organization

is compensation plan characteristics impacting the future performance of company. From the

analysis of annual report of NAB, it has been found that the methodology used for

determination of incentive plans of executives have been changed during the year 2017. This

change has been introduced to bring simplicity and transparency into the remuneration

framework. However, it is required by NAB to broaden their performance measures for

improving the reporting of remuneration framework.

AUDITING

Recommendation:

One of the important ways to keep track of business is to put the system of

performance management in place. Organizations seeking broadening their performance

measures should broaden their strategic business objectives that help in calculating the inputs

and gauging employee engagement. It is required by organization to develop a

comprehensive reporting strategy and measurement of human resource that should be well

aligned with the overall strategy of business. The performance measures employed by

organization can be improved by setting the benchmark and benchmarking the performance

against performance level. Such benchmarking can either be developed internally or it can be

determined by comparing with other business. Incentive plans of company should be

associated with the overall performance. Most of the research focuses on pay for performance

and whether the performance of employees is affected positively by such incentives.

Employees are motivated to perform in a better way by creating a greater link of employee

performance and rewards with compensation plan (Klettner et al. 2014).

Conclusion:

Many researchers have focused on the relationship between performance of company

and compensation of executive. Usage of executive compensation for increasing the value of

firms comes with both positive as well as negative side. In order for designing the effective

pay performance plan, the crucial factor that should be taken into by account by organization

is compensation plan characteristics impacting the future performance of company. From the

analysis of annual report of NAB, it has been found that the methodology used for

determination of incentive plans of executives have been changed during the year 2017. This

change has been introduced to bring simplicity and transparency into the remuneration

framework. However, it is required by NAB to broaden their performance measures for

improving the reporting of remuneration framework.

12

AUDITING

References lists:

Armstrong, M. and Taylor, S., 2014. Armstrong's handbook of human resource management

practice. Kogan Page Publishers.

Beer, M., Boselie, P. and Brewster, C., 2015. Back to the future: Implications for the field of

HRM of the multistakeholder perspective proposed 30 years ago. Human Resource

Management, 54(3), pp.427-438.

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Buettner, R., 2015, January. A systematic literature review of crowdsourcing research from a

human resource management perspective. In System Sciences (HICSS), 2015 48th Hawaii

International Conference on (pp. 4609-4618). IEEE.

Capital.nab.com.au. (2018). [online] Available at: https://capital.nab.com.au/docs/NAB-

2017-annual-financial-report.pdf [Accessed 7 May 2018].

Demerouti, E., Bakker, A.B. and Leiter, M., 2014. Burnout and job performance: The

moderating role of selection, optimization, and compensation strategies. Journal of

occupational health psychology, 19(1), p.96.

Friedman, S.D., 2017. Succession systems in large corporations: Characteristics and

correlates of performance. In Leadership succession (pp. 15-38). Routledge.

Gupta, N. and Shaw, J.D., 2014. Employee compensation: The neglected area of HRM

research. Human Resource Management Review, 24(1), pp.1-4.

Hollenbeck, J.R. and Jamieson, B.B., 2015. Human capital, social capital, and social network

analysis: Implications for strategic human resource management. The Academy of

Management Perspectives, 29(3), pp.370-385.

AUDITING

References lists:

Armstrong, M. and Taylor, S., 2014. Armstrong's handbook of human resource management

practice. Kogan Page Publishers.

Beer, M., Boselie, P. and Brewster, C., 2015. Back to the future: Implications for the field of

HRM of the multistakeholder perspective proposed 30 years ago. Human Resource

Management, 54(3), pp.427-438.

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Buettner, R., 2015, January. A systematic literature review of crowdsourcing research from a

human resource management perspective. In System Sciences (HICSS), 2015 48th Hawaii

International Conference on (pp. 4609-4618). IEEE.

Capital.nab.com.au. (2018). [online] Available at: https://capital.nab.com.au/docs/NAB-

2017-annual-financial-report.pdf [Accessed 7 May 2018].

Demerouti, E., Bakker, A.B. and Leiter, M., 2014. Burnout and job performance: The

moderating role of selection, optimization, and compensation strategies. Journal of

occupational health psychology, 19(1), p.96.

Friedman, S.D., 2017. Succession systems in large corporations: Characteristics and

correlates of performance. In Leadership succession (pp. 15-38). Routledge.

Gupta, N. and Shaw, J.D., 2014. Employee compensation: The neglected area of HRM

research. Human Resource Management Review, 24(1), pp.1-4.

Hollenbeck, J.R. and Jamieson, B.B., 2015. Human capital, social capital, and social network

analysis: Implications for strategic human resource management. The Academy of

Management Perspectives, 29(3), pp.370-385.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.