Managerial Accounting Report: Tabcorp Executive Performance Review

VerifiedAdded on 2021/06/16

|19

|6076

|26

Report

AI Summary

This managerial accounting report presents a literature review evaluating executive performance and remuneration in Australian public companies, with a specific focus on Tabcorp Holdings Limited. The report examines the effectiveness of current control systems, identifies approaches to management performance and reward systems, and analyzes the company's methods for encouraging high performance among its executive team. The study explores the impact of various remuneration components, including fixed and variable compensation, short-term and long-term incentives, and shareholding policies. The report also includes a company review, a summary of findings, an analysis of remuneration methods, and recommendations for enhancing performance measures and reporting procedures. The key findings highlight the relationship between company performance, executive remuneration, and share price, ultimately aiming to provide insights into best practices for executive compensation and corporate governance within the Australian context.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of Student:

Name of University:

Author’s Note:

Managerial Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary

The main intention of the study is developing a literature review that could be able to evaluate

the executive performance along with remuneration for public listed companies across Australia.

In order to establish a well-defined review of the objectives, “Tabcorp Holdings Limited” has

been chosen for reporting purposes. The main aspects of the report will encompass the

effectiveness of the present control system for the selected company and identify the approach

for management performance along with the reward systems. The discourse of the study has

elaborated on company’s approach in terms of encouraging high performance objectives by its

executive team thereby analyzing whether it has been able to uplift itself in terms of

performance. The main recommendations of the report have also provided with enhancing

performance measures and reporting improvement as per remuneration reporting procedures.

The main findings of the remuneration procedures have been depicted with Target Reward Mix,

Fixed Remuneration, “Short-Term Incentives (Variable), Long-Term Incentives (Variable)”,

Appointment or Retention Incentives (Variable), Policy Prohibiting Hedging (Variable) and

Executives Shareholding Policy (Variable). It has further depicted that despite a significant

increase in company performance and remuneration, the share price has considerably reduced.

Executive Summary

The main intention of the study is developing a literature review that could be able to evaluate

the executive performance along with remuneration for public listed companies across Australia.

In order to establish a well-defined review of the objectives, “Tabcorp Holdings Limited” has

been chosen for reporting purposes. The main aspects of the report will encompass the

effectiveness of the present control system for the selected company and identify the approach

for management performance along with the reward systems. The discourse of the study has

elaborated on company’s approach in terms of encouraging high performance objectives by its

executive team thereby analyzing whether it has been able to uplift itself in terms of

performance. The main recommendations of the report have also provided with enhancing

performance measures and reporting improvement as per remuneration reporting procedures.

The main findings of the remuneration procedures have been depicted with Target Reward Mix,

Fixed Remuneration, “Short-Term Incentives (Variable), Long-Term Incentives (Variable)”,

Appointment or Retention Incentives (Variable), Policy Prohibiting Hedging (Variable) and

Executives Shareholding Policy (Variable). It has further depicted that despite a significant

increase in company performance and remuneration, the share price has considerably reduced.

2MANAGERIAL ACCOUNTING

Table of Contents

1. Introduction..................................................................................................................................3

2. Topic and Literature Review.......................................................................................................3

2.1 Executive Performance Evaluation and Remuneration in Public Companies.......................4

2.2 Effectiveness of Control Systems Within the Companies.....................................................5

2.3 Executive Performance and Reward Systems.......................................................................5

2.4 Motivation (Overview)..........................................................................................................6

3. Company Review.........................................................................................................................6

4. Findings Summary.....................................................................................................................12

5. Analysis of Remuneration Methods Used.................................................................................13

6. Recommendations......................................................................................................................14

7. Conclusion.................................................................................................................................14

References and Bibliography.........................................................................................................16

Table of Contents

1. Introduction..................................................................................................................................3

2. Topic and Literature Review.......................................................................................................3

2.1 Executive Performance Evaluation and Remuneration in Public Companies.......................4

2.2 Effectiveness of Control Systems Within the Companies.....................................................5

2.3 Executive Performance and Reward Systems.......................................................................5

2.4 Motivation (Overview)..........................................................................................................6

3. Company Review.........................................................................................................................6

4. Findings Summary.....................................................................................................................12

5. Analysis of Remuneration Methods Used.................................................................................13

6. Recommendations......................................................................................................................14

7. Conclusion.................................................................................................................................14

References and Bibliography.........................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

1. Introduction

Remuneration includes various types of payments received for services on employment

including compensation which constitutes the bonuses, basic salary and economic benefits which

are provided to the business executives and staffs at the time of their employment. The executive

compensation mainly comprises of the financial compensation along with other non-financial

rewards. The typical mixture comprises of call options on the stock of the company and

perquisites which are ideally configured for taking into consideration government regulations

and tax law. The different types of analysis associated to remuneration is recognized with diverse

range of practices associated to remuneration and the policies which explains the various ways in

which employees are compensated as per the reference market. The main intention of the study is

developing a literature review that could be able to evaluate the executive performance along

with remuneration for public listed companies across Australia. In order to establish a well-

defined review of the objectives, “Tabcorp Holdings Limited” has been chosen for reporting

purposes. The main aspects of the report will encompass the effectiveness of the present control

system for the selected company and identify the approach for management performance along

with the reward systems. The discourse of the study will be also elaborate on company’s

approach in terms of encouraging high performance objectives by its executive team thereby

analyzing whether it has been able to uplift itself in terms of performance. The main

recommendations of the report will be also provided with enhancing performance measures and

reporting improvement as per remuneration reporting procedures (Guillen et al. 2015).

2. Topic and Literature Review

In general, the remuneration reports depict that the performance evaluation of “Chief

Executive Officers” is done on a yearly basis as per their overall performance and pay. As

discussed by Li (2017), the most identified concern for the managers and CEOs show that the

payment settings in several ways our mismatching in nature and the remuneration of CEO is

higher than expectations. A benchmark for recording the remuneration of the CEO has shown

that the top management of different companies listed in ASX have not considered evaluating the

performance of CEO. This is seen to be having a detrimental effect on the company thereby

creating a parity among the pay of the executive and manager. These differences are also

1. Introduction

Remuneration includes various types of payments received for services on employment

including compensation which constitutes the bonuses, basic salary and economic benefits which

are provided to the business executives and staffs at the time of their employment. The executive

compensation mainly comprises of the financial compensation along with other non-financial

rewards. The typical mixture comprises of call options on the stock of the company and

perquisites which are ideally configured for taking into consideration government regulations

and tax law. The different types of analysis associated to remuneration is recognized with diverse

range of practices associated to remuneration and the policies which explains the various ways in

which employees are compensated as per the reference market. The main intention of the study is

developing a literature review that could be able to evaluate the executive performance along

with remuneration for public listed companies across Australia. In order to establish a well-

defined review of the objectives, “Tabcorp Holdings Limited” has been chosen for reporting

purposes. The main aspects of the report will encompass the effectiveness of the present control

system for the selected company and identify the approach for management performance along

with the reward systems. The discourse of the study will be also elaborate on company’s

approach in terms of encouraging high performance objectives by its executive team thereby

analyzing whether it has been able to uplift itself in terms of performance. The main

recommendations of the report will be also provided with enhancing performance measures and

reporting improvement as per remuneration reporting procedures (Guillen et al. 2015).

2. Topic and Literature Review

In general, the remuneration reports depict that the performance evaluation of “Chief

Executive Officers” is done on a yearly basis as per their overall performance and pay. As

discussed by Li (2017), the most identified concern for the managers and CEOs show that the

payment settings in several ways our mismatching in nature and the remuneration of CEO is

higher than expectations. A benchmark for recording the remuneration of the CEO has shown

that the top management of different companies listed in ASX have not considered evaluating the

performance of CEO. This is seen to be having a detrimental effect on the company thereby

creating a parity among the pay of the executive and manager. These differences are also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

evaluated with the performance of the individuals rather than reward as per their own interest. It

got gathered from more than 500 public listed companies are seen with inequality of pay without

any performance measurement for the governance of the companies (Herring et al. 2014).

It has been further identified that there is a growing study which is relates to the

executive compensation and corporate governance. These discourse states that most of it is

included in the structure of ownership and characteristics of the board. Theoretically, the

members of the board needs to be independent which is designed to be positive for pay

performance and shareholder satisfaction. It is also noteworthy that AASB released several

executive disclosures pertaining to executive remuneration . The main amendments for the

Corporations Act has been considered as per CLERP9 which has been further able to disclose

various requirements for disclosing executive compensation and executive in addition to the

shareholders through compensation report which is voted by shareholders for the public listed

companies (Fernández Méndez et al. 2017).

As stated by Van Dijk et al. (2014), the performance process evaluation is considered to

be particularly complex in nature as it needs to consider that achievements of CEO along with

the targets and goals set for company which benefits the shareholders both in the long run and

short-run. It needs to be further understood that the board committee is responsible for evaluating

the short-run depictions as per previous performance of financial targets and behavioural aspects.

In addition to this, the evaluation remuneration is based on three perspectives, where the CEO is

accountable for evaluating the financial performance. The operative level is further seen to be

held accountable for the customer satisfaction, improving the company portfolio, research and

development activities (Afrifa and Adesina 2017). In the end they evaluations are able to depict

the various decisions along with strategies formulated for long-term and also settlement of the

same. It has been further understood that overtime the peer groups has been able to attain a

significant benchmark in compared to all firms which is stable for long time and able to act as an

escalator for executives which is used by the firms to bypass the performance measure that

supports executive pay in terms of the peer groups (Ekdahl 2014).

2.1 Executive Performance Evaluation and Remuneration in Public Companies

It needs to be understood that performance evaluation at executive level is not easy. The

several considerations which goes into the performance analysis is mainly considered annually in

evaluated with the performance of the individuals rather than reward as per their own interest. It

got gathered from more than 500 public listed companies are seen with inequality of pay without

any performance measurement for the governance of the companies (Herring et al. 2014).

It has been further identified that there is a growing study which is relates to the

executive compensation and corporate governance. These discourse states that most of it is

included in the structure of ownership and characteristics of the board. Theoretically, the

members of the board needs to be independent which is designed to be positive for pay

performance and shareholder satisfaction. It is also noteworthy that AASB released several

executive disclosures pertaining to executive remuneration . The main amendments for the

Corporations Act has been considered as per CLERP9 which has been further able to disclose

various requirements for disclosing executive compensation and executive in addition to the

shareholders through compensation report which is voted by shareholders for the public listed

companies (Fernández Méndez et al. 2017).

As stated by Van Dijk et al. (2014), the performance process evaluation is considered to

be particularly complex in nature as it needs to consider that achievements of CEO along with

the targets and goals set for company which benefits the shareholders both in the long run and

short-run. It needs to be further understood that the board committee is responsible for evaluating

the short-run depictions as per previous performance of financial targets and behavioural aspects.

In addition to this, the evaluation remuneration is based on three perspectives, where the CEO is

accountable for evaluating the financial performance. The operative level is further seen to be

held accountable for the customer satisfaction, improving the company portfolio, research and

development activities (Afrifa and Adesina 2017). In the end they evaluations are able to depict

the various decisions along with strategies formulated for long-term and also settlement of the

same. It has been further understood that overtime the peer groups has been able to attain a

significant benchmark in compared to all firms which is stable for long time and able to act as an

escalator for executives which is used by the firms to bypass the performance measure that

supports executive pay in terms of the peer groups (Ekdahl 2014).

2.1 Executive Performance Evaluation and Remuneration in Public Companies

It needs to be understood that performance evaluation at executive level is not easy. The

several considerations which goes into the performance analysis is mainly considered annually in

5MANAGERIAL ACCOUNTING

most of the public listed companies. They evaluation of performance which may be better

described as a way to evaluate previous performance is necessary for the board to set future

targets which is conducive in taking decisions associated to the remuneration of the executives.

In this consideration the effectiveness of the performance analysis is depicted with previous

performance which is considered with the future targets and this will assist the remuneration

committee in undertaking decisions pertaining to future compensation, employment and strategic

goals. The goal setting factor has revealed that executive performance analysis may rely on

continuing leadership development of the board which offers feedbacks concerning the areas in

which the executives are assessed with innovative skills and performing better jobs. In the recent

times, a massive remuneration growth has been depicted in terms of executives (Albertsen and

Lueg 2014).

2.2 Effectiveness of Control Systems Within the Companies

The control systems significance for the business organization is considered with

developing the strategic plans so that the business objectives can be accomplished as desired.

Moreover, with the assistance of control systems a company is able to accomplish the various

types of needs which require adherence to the legal regulatory standards and internal standards

requirement. One of the main significant factor for effectiveness in the control system is depicted

with quality of the information received. However, there needs to be updated information and

accuracy incorporated within the control systems. Moreover, with the assistance of internal

controls information can be procured in a more timely manner. However, the processing of these

financial information needs to be done in such a way that they are not delayed by any means.

Therefore, the significance of the control system is necessary for maintaining executive

performance along with reward systems (Chang, Yu and Hung 2015).

2.3 Executive Performance and Reward Systems

As discussed by Jaafar and James (2014), the reward system for the executive comprises

of several types of integrated policies and procedures which are brought into practice in order to

reward its executive in alignment to the skin, competence, contribution as per the market worth.

It needs to be understood that such a reward system is considered to maintain suitable level of

benefits and being along with various types of reward system (Goh and Gupta 2016). The

recognition of financial rewards is considered with fixed and variable pay along with benefits to

most of the public listed companies. They evaluation of performance which may be better

described as a way to evaluate previous performance is necessary for the board to set future

targets which is conducive in taking decisions associated to the remuneration of the executives.

In this consideration the effectiveness of the performance analysis is depicted with previous

performance which is considered with the future targets and this will assist the remuneration

committee in undertaking decisions pertaining to future compensation, employment and strategic

goals. The goal setting factor has revealed that executive performance analysis may rely on

continuing leadership development of the board which offers feedbacks concerning the areas in

which the executives are assessed with innovative skills and performing better jobs. In the recent

times, a massive remuneration growth has been depicted in terms of executives (Albertsen and

Lueg 2014).

2.2 Effectiveness of Control Systems Within the Companies

The control systems significance for the business organization is considered with

developing the strategic plans so that the business objectives can be accomplished as desired.

Moreover, with the assistance of control systems a company is able to accomplish the various

types of needs which require adherence to the legal regulatory standards and internal standards

requirement. One of the main significant factor for effectiveness in the control system is depicted

with quality of the information received. However, there needs to be updated information and

accuracy incorporated within the control systems. Moreover, with the assistance of internal

controls information can be procured in a more timely manner. However, the processing of these

financial information needs to be done in such a way that they are not delayed by any means.

Therefore, the significance of the control system is necessary for maintaining executive

performance along with reward systems (Chang, Yu and Hung 2015).

2.3 Executive Performance and Reward Systems

As discussed by Jaafar and James (2014), the reward system for the executive comprises

of several types of integrated policies and procedures which are brought into practice in order to

reward its executive in alignment to the skin, competence, contribution as per the market worth.

It needs to be understood that such a reward system is considered to maintain suitable level of

benefits and being along with various types of reward system (Goh and Gupta 2016). The

recognition of financial rewards is considered with fixed and variable pay along with benefits to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

employee pertaining to overall remuneration. The various elements of the executive

remuneration are also identified with non-financial rewards which is discerned with recognition,

responsibility, achievements and praise. These are considered with individual growth and

management systems performance. There are major ways in which the system of reward

comprises of procedures for measuring the personal contribution and job values within the jobs

along with a range of benefits provided to the employee. Such benefits include market-rate and

job analyses based on performance management. Some of the other empirical research has stated

that there are certain performance rewards which motivates the employees to work to their best

of their ability and retain as the best employee with identifying the rewarding system as part of

their contribution. Some of the major issues faced by the managers during the reward

management and performance evaluation is recognized with getting out the performance

management which is more logical to both implied and employees along with attainment of

organizational goals (Dawid, Harting and Van Der Hoog 2018).

2.4 Motivation (Overview)

The remuneration philosophy of Tabcorp Holdings has revealed that it aims to extract,

motivate and retain individuals with high-calibre throughout the organization by following a

competitive and consistent business objective which are normally accepted as a good market

practice. The key principles under the remuneration has revealed generating “long-term

shareholder value”, “driving performance, ensuring market competitiveness and driving the right

behaviour”. In reference to “creating long-term shareholder value” the company aims to reward

the executives by taking the individual’s performance which are aligned with the business

objectives (Doran et al. 2014).

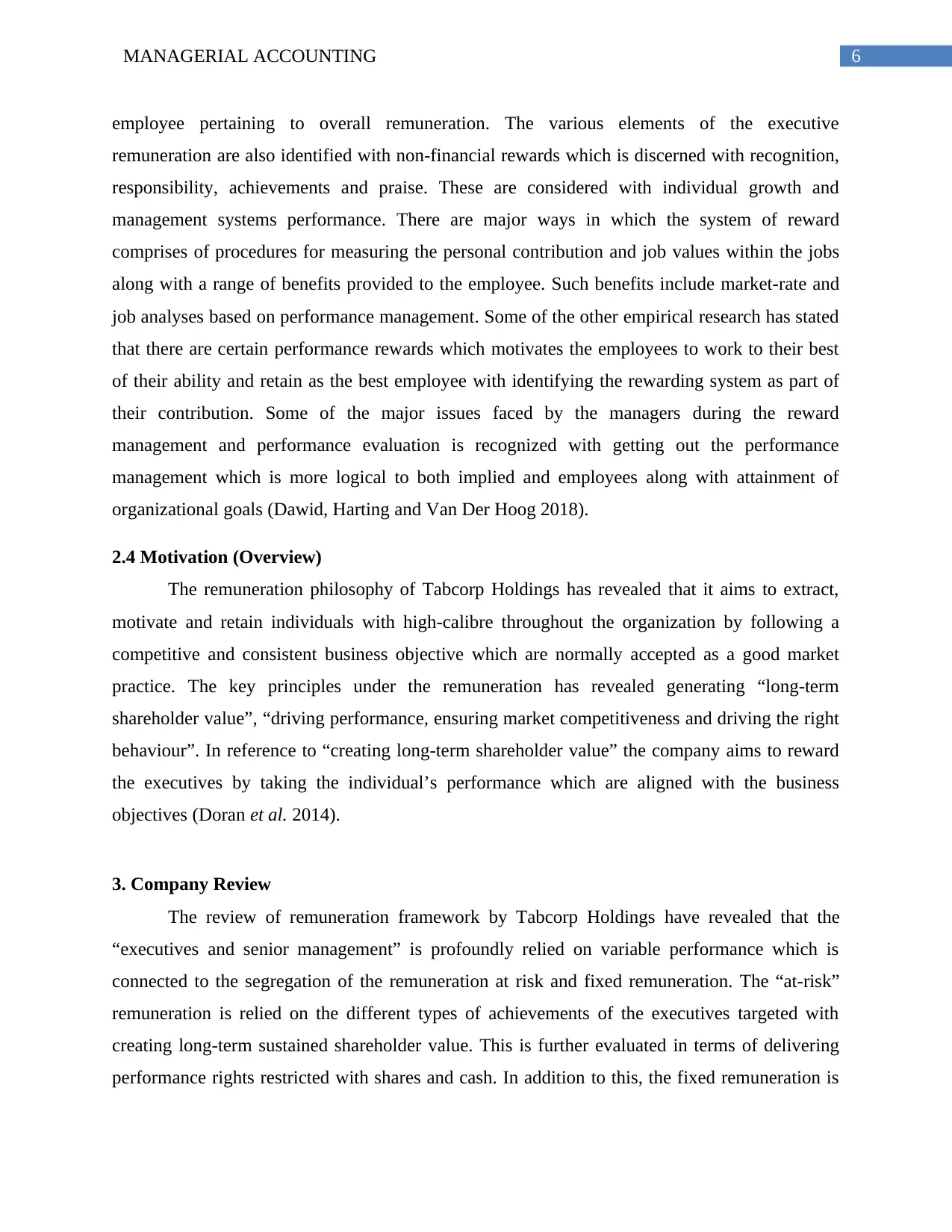

3. Company Review

The review of remuneration framework by Tabcorp Holdings have revealed that the

“executives and senior management” is profoundly relied on variable performance which is

connected to the segregation of the remuneration at risk and fixed remuneration. The “at-risk”

remuneration is relied on the different types of achievements of the executives targeted with

creating long-term sustained shareholder value. This is further evaluated in terms of delivering

performance rights restricted with shares and cash. In addition to this, the fixed remuneration is

employee pertaining to overall remuneration. The various elements of the executive

remuneration are also identified with non-financial rewards which is discerned with recognition,

responsibility, achievements and praise. These are considered with individual growth and

management systems performance. There are major ways in which the system of reward

comprises of procedures for measuring the personal contribution and job values within the jobs

along with a range of benefits provided to the employee. Such benefits include market-rate and

job analyses based on performance management. Some of the other empirical research has stated

that there are certain performance rewards which motivates the employees to work to their best

of their ability and retain as the best employee with identifying the rewarding system as part of

their contribution. Some of the major issues faced by the managers during the reward

management and performance evaluation is recognized with getting out the performance

management which is more logical to both implied and employees along with attainment of

organizational goals (Dawid, Harting and Van Der Hoog 2018).

2.4 Motivation (Overview)

The remuneration philosophy of Tabcorp Holdings has revealed that it aims to extract,

motivate and retain individuals with high-calibre throughout the organization by following a

competitive and consistent business objective which are normally accepted as a good market

practice. The key principles under the remuneration has revealed generating “long-term

shareholder value”, “driving performance, ensuring market competitiveness and driving the right

behaviour”. In reference to “creating long-term shareholder value” the company aims to reward

the executives by taking the individual’s performance which are aligned with the business

objectives (Doran et al. 2014).

3. Company Review

The review of remuneration framework by Tabcorp Holdings have revealed that the

“executives and senior management” is profoundly relied on variable performance which is

connected to the segregation of the remuneration at risk and fixed remuneration. The “at-risk”

remuneration is relied on the different types of achievements of the executives targeted with

creating long-term sustained shareholder value. This is further evaluated in terms of delivering

performance rights restricted with shares and cash. In addition to this, the fixed remuneration is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

set with the market “competitive and commensurate with the incumbent’s skills, experience and

job responsibilities”. The review of group’s remuneration framework has been able to

recommend to the board for suitable arrangements pertaining remuneration made for the KMP

including MD and CEO (Kanapathippillai, Johl and Wines 2016).

Figure: Proportion of remuneration at risk

(Source: Tabcorp.com.au. 2018)

The detailed explanation of the different types of remuneration offered by the company is

depicted below as follows:

Intrinsic Rewards

The remuneration philosophy adopted by the company ensures that it is self-administered

by those employees who are motivated from inside rather than expecting any reward such as

bonus our gifts. This is evident with some of the non-financial intrinsic remuneration rewards

such as, recognition of employee achievements with the growth of the organization. The

important discourse on such a reward system is included with the procedures for measuring

personal contributions, job values along with “level of employee benefits” which includes the job

analysis and “market-rate evaluation” and “performance management” (Khalid and Rehman

2014).

Extrinsic Rewards

These are depicted to be externally administered and takes into consideration the

financial aspects of remuneration. The different types of reward systems include financial

set with the market “competitive and commensurate with the incumbent’s skills, experience and

job responsibilities”. The review of group’s remuneration framework has been able to

recommend to the board for suitable arrangements pertaining remuneration made for the KMP

including MD and CEO (Kanapathippillai, Johl and Wines 2016).

Figure: Proportion of remuneration at risk

(Source: Tabcorp.com.au. 2018)

The detailed explanation of the different types of remuneration offered by the company is

depicted below as follows:

Intrinsic Rewards

The remuneration philosophy adopted by the company ensures that it is self-administered

by those employees who are motivated from inside rather than expecting any reward such as

bonus our gifts. This is evident with some of the non-financial intrinsic remuneration rewards

such as, recognition of employee achievements with the growth of the organization. The

important discourse on such a reward system is included with the procedures for measuring

personal contributions, job values along with “level of employee benefits” which includes the job

analysis and “market-rate evaluation” and “performance management” (Khalid and Rehman

2014).

Extrinsic Rewards

These are depicted to be externally administered and takes into consideration the

financial aspects of remuneration. The different types of reward systems include financial

8MANAGERIAL ACCOUNTING

rewards such as fixed and variable pay which to gather comprises of the overall remuneration.

Tabcorb considers recognizing the efforts of a hard-working employee and promotes extrinsic

rewards with various types of long-term incentive plan, cash compensation, grant for options and

retirement packages (Kirsten and Du Toit 2018). The different types of process of remuneration

present in Tabcorb’s remuneration report comprises of:

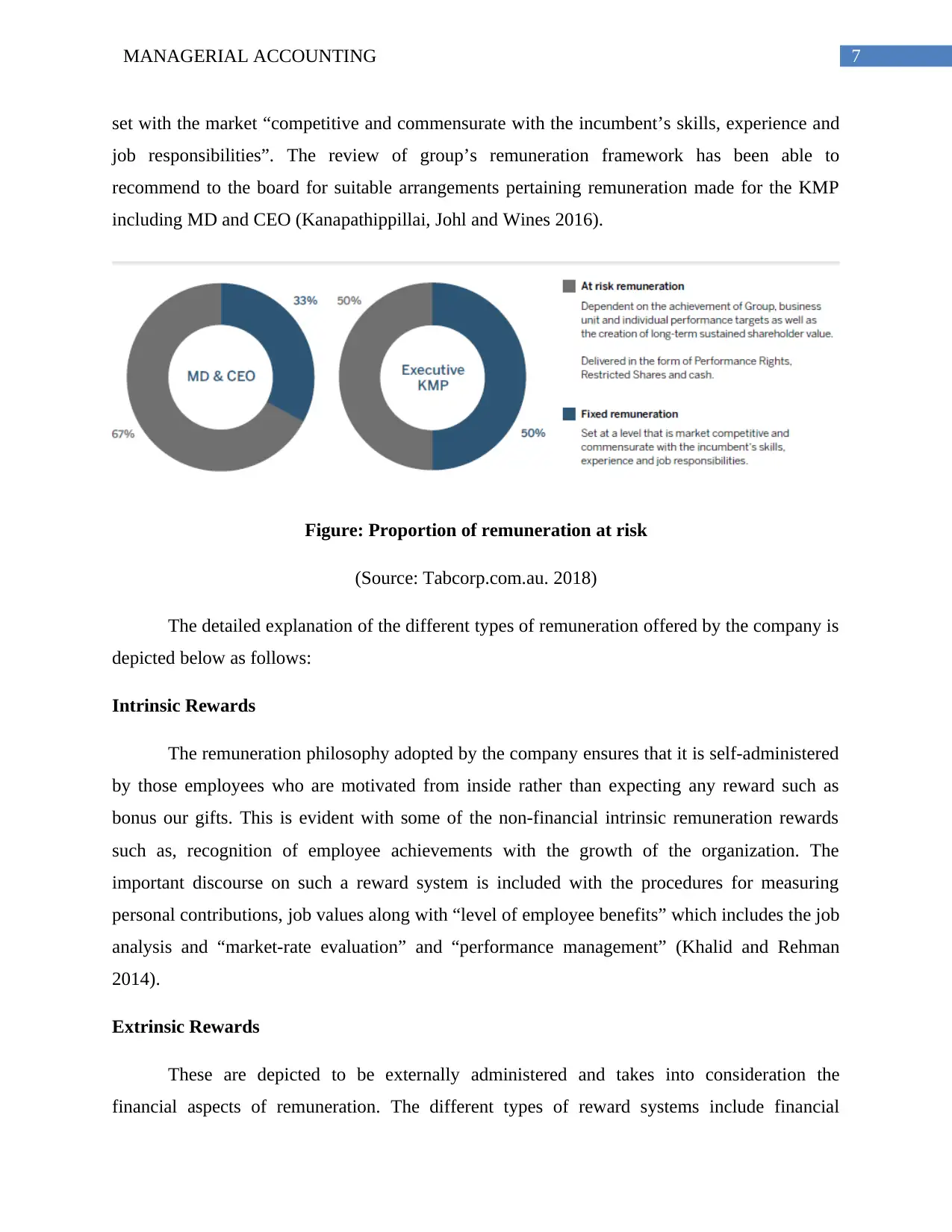

Target Reward Mix

Tabcorp ensures that the total remuneration, which is a sum of “fixed and variable

remuneration” is “competitive, reasonable, fair” and comprises of “extensive market

benchmarking” regularly undertaken against “wide range of relevant organizations”. It needs to

be understood that the target reward mix is comprised of a split between on target variable

remuneration and fixed remuneration. It needs to be for the discerned that the target reward mix

for the CEO & MD is stated with a total of 67% of at-risk performance and 50% equity based

(Lee and Isa 2015).

Figure: “Executive KMP target reward mix for the year ended 30 June 2017”

(Source: Tabcorp.com.au. 2018)

Fixed Remuneration

rewards such as fixed and variable pay which to gather comprises of the overall remuneration.

Tabcorb considers recognizing the efforts of a hard-working employee and promotes extrinsic

rewards with various types of long-term incentive plan, cash compensation, grant for options and

retirement packages (Kirsten and Du Toit 2018). The different types of process of remuneration

present in Tabcorb’s remuneration report comprises of:

Target Reward Mix

Tabcorp ensures that the total remuneration, which is a sum of “fixed and variable

remuneration” is “competitive, reasonable, fair” and comprises of “extensive market

benchmarking” regularly undertaken against “wide range of relevant organizations”. It needs to

be understood that the target reward mix is comprised of a split between on target variable

remuneration and fixed remuneration. It needs to be for the discerned that the target reward mix

for the CEO & MD is stated with a total of 67% of at-risk performance and 50% equity based

(Lee and Isa 2015).

Figure: “Executive KMP target reward mix for the year ended 30 June 2017”

(Source: Tabcorp.com.au. 2018)

Fixed Remuneration

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

The fixed remuneration for the executive KMP comprises of statutory superannuation

contributions, cash salary and several types of other benefits which they may be elected to

receive on sacrificing salary such as extra aids made to superannuation pertaining motor vehicle

novated leases. In addition to this, the executive KMP remuneration takes into account the skills,

information and involvement which is required to perform a magnitude of responsibilities in an

efficient manner. The comprehensive benchmarking exercise is seen to be undertaken by various

types of the “Executive KMP (including the MD & CEO) remuneration structures” which are

compared to be incumbent with the roles of other organizations for ensuring that the group is

viable in attracting, retaining and rewarding crucial talent. On 30 June 2017, the company was

placed between “70th and 80th largest organisations listed on the ASX” as per market

capitalization. The benchmarking remuneration levels to the organization has been ranked

between 50 to 100 on the ASX in terms of market capitalization. The main strategy of fixed

remuneration at the market median is applicable to those “executive KMP who are performing”

appropriate as per their roles. A higher or lower “fixed remuneration level” may be provided

contingent on the complexity of incumbent’s skills and experience, performance levels and

various types of requirements of groups retention policies (Leong et al. 2015).

Short-Term Incentives (Variable)

The STI of the company is designated to reward the employees for achievement by the

group, individual performance and business unit over a period of 12 months which are seen to be

in alignment with the group’s long-term corporate planning thereby creating long-term

shareholder value. It is worth noting that the eligibility of participating in the STI plan is

depicted with mid-level managers, senior managers along with “Senior Executive Leadership

Team (including Executive KMP)”. It needs to be discerned that “reduced or no STI awards” are

applicable in case the group is not able to meeting financial targets. The pool of STI is seen to be

governed by groups funding multiplier which is responsible for setting the pool and “dependent

on the Group’s NPAT before non-recurring items performance”. The conduction of STI award is

identified as it three-step process which includes set the STI pool (considered with group funding

multiplier), setting the divisional of multipliers and setting of individual performance multipliers

(Maas and Rosendaal 2016).

The fixed remuneration for the executive KMP comprises of statutory superannuation

contributions, cash salary and several types of other benefits which they may be elected to

receive on sacrificing salary such as extra aids made to superannuation pertaining motor vehicle

novated leases. In addition to this, the executive KMP remuneration takes into account the skills,

information and involvement which is required to perform a magnitude of responsibilities in an

efficient manner. The comprehensive benchmarking exercise is seen to be undertaken by various

types of the “Executive KMP (including the MD & CEO) remuneration structures” which are

compared to be incumbent with the roles of other organizations for ensuring that the group is

viable in attracting, retaining and rewarding crucial talent. On 30 June 2017, the company was

placed between “70th and 80th largest organisations listed on the ASX” as per market

capitalization. The benchmarking remuneration levels to the organization has been ranked

between 50 to 100 on the ASX in terms of market capitalization. The main strategy of fixed

remuneration at the market median is applicable to those “executive KMP who are performing”

appropriate as per their roles. A higher or lower “fixed remuneration level” may be provided

contingent on the complexity of incumbent’s skills and experience, performance levels and

various types of requirements of groups retention policies (Leong et al. 2015).

Short-Term Incentives (Variable)

The STI of the company is designated to reward the employees for achievement by the

group, individual performance and business unit over a period of 12 months which are seen to be

in alignment with the group’s long-term corporate planning thereby creating long-term

shareholder value. It is worth noting that the eligibility of participating in the STI plan is

depicted with mid-level managers, senior managers along with “Senior Executive Leadership

Team (including Executive KMP)”. It needs to be discerned that “reduced or no STI awards” are

applicable in case the group is not able to meeting financial targets. The pool of STI is seen to be

governed by groups funding multiplier which is responsible for setting the pool and “dependent

on the Group’s NPAT before non-recurring items performance”. The conduction of STI award is

identified as it three-step process which includes set the STI pool (considered with group funding

multiplier), setting the divisional of multipliers and setting of individual performance multipliers

(Maas and Rosendaal 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

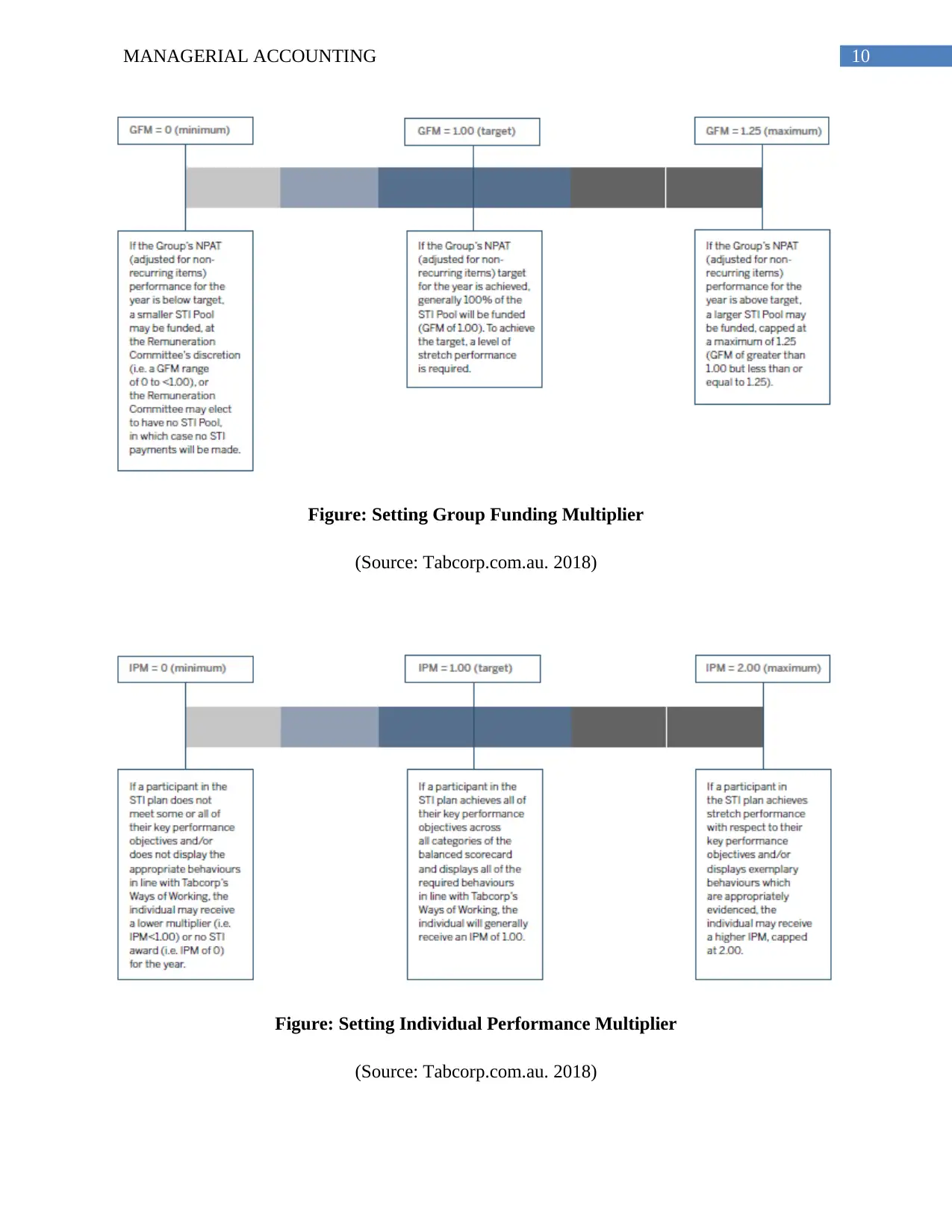

Figure: Setting Group Funding Multiplier

(Source: Tabcorp.com.au. 2018)

Figure: Setting Individual Performance Multiplier

(Source: Tabcorp.com.au. 2018)

Figure: Setting Group Funding Multiplier

(Source: Tabcorp.com.au. 2018)

Figure: Setting Individual Performance Multiplier

(Source: Tabcorp.com.au. 2018)

11MANAGERIAL ACCOUNTING

Long-Term Incentives (Variable)

It needs to be noted that the LTI of Tabcorp is intended to reward it “senior management

team” for contributing to create “long-term shareholder value” in retaining important talent

within the organization. The company reviews LTI annually and ensures that the business

objectives continue to reward shareholder value and is competitive in appealing and retaining

high-performing executives. The purpose of LTI plan is to drive long-term performance for the

business thereby creating shareholder value and aligning senior management and shareholder

interest to retain high-performing and skilled senior managers (Moosa 2017). It has been for the

discerned that “MD and CEO of the company has an on-target opportunity of LTI of 100%” of

the total fixed remuneration. In addition to this, the executive KMP is discerned to be having an

on target “LTI” opportunity of 50% fixed remuneration. It is also understood that both MD and

CEO have the opportunity to own up to two times on the “on-target opportunity for

outperformance”. However, the outperformance shall be realized only if Tabcorp achieves the

top quartile returns from the shareholder (Melis, Gaia and Carta 2015).

Appointment or Retention Incentives (Variable)

The restricted shares may be issued to the various types of senior managers as incentive

after that appointment. This includes new employee joining in Tabcorp, employee retention or

internal promotion. These are particularly considered as ordinary shares of the company which

acts as a retaining procedure and are subject to restriction of up to three years. In addition to this,

the “senior managers” may also issue the “Performance Rights upon appointment”. These are

considered as instruments which are issued as part of LTI and subject to hurdles and vesting

conditions (Parmenter 2015).

Policy Prohibiting Hedging (Variable)

It has been further depicted that the participants in the various types of incentive plans

including both “STI and LTI” are limited from hedging the unvested performance rights and total

value of restricted shares. Such parties are not allowed to enter derivative management with

respect to equity instruments granted as part of this plans. It is to be further noted that they could

Long-Term Incentives (Variable)

It needs to be noted that the LTI of Tabcorp is intended to reward it “senior management

team” for contributing to create “long-term shareholder value” in retaining important talent

within the organization. The company reviews LTI annually and ensures that the business

objectives continue to reward shareholder value and is competitive in appealing and retaining

high-performing executives. The purpose of LTI plan is to drive long-term performance for the

business thereby creating shareholder value and aligning senior management and shareholder

interest to retain high-performing and skilled senior managers (Moosa 2017). It has been for the

discerned that “MD and CEO of the company has an on-target opportunity of LTI of 100%” of

the total fixed remuneration. In addition to this, the executive KMP is discerned to be having an

on target “LTI” opportunity of 50% fixed remuneration. It is also understood that both MD and

CEO have the opportunity to own up to two times on the “on-target opportunity for

outperformance”. However, the outperformance shall be realized only if Tabcorp achieves the

top quartile returns from the shareholder (Melis, Gaia and Carta 2015).

Appointment or Retention Incentives (Variable)

The restricted shares may be issued to the various types of senior managers as incentive

after that appointment. This includes new employee joining in Tabcorp, employee retention or

internal promotion. These are particularly considered as ordinary shares of the company which

acts as a retaining procedure and are subject to restriction of up to three years. In addition to this,

the “senior managers” may also issue the “Performance Rights upon appointment”. These are

considered as instruments which are issued as part of LTI and subject to hurdles and vesting

conditions (Parmenter 2015).

Policy Prohibiting Hedging (Variable)

It has been further depicted that the participants in the various types of incentive plans

including both “STI and LTI” are limited from hedging the unvested performance rights and total

value of restricted shares. Such parties are not allowed to enter derivative management with

respect to equity instruments granted as part of this plans. It is to be further noted that they could

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.