Managerial Accounting Report: Executive Remuneration Comparison

VerifiedAdded on 2023/06/07

|28

|6167

|289

Report

AI Summary

This report provides a comprehensive analysis of the remuneration structures of Woodside Petroleum and Santos, focusing on the fiscal year 2017. It examines the role of remuneration reports in public companies, the effectiveness of control systems, and the allocation of executive compensation, including fixed remuneration, short-term incentives (STI), and long-term incentives (LTI). The report compares the two companies' performance measures, such as earnings per share, and evaluates the relationship between executive pay and company performance, considering shareholder returns in the context of each company's financial health. Furthermore, it reviews the details of the remuneration committee and membership. The findings highlight the differences in remuneration practices and their impact on shareholder value, concluding with a comparative analysis of the remuneration methods used by both companies, assessing their effectiveness in the short and long term.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report is concerned with evaluating the remuneration structure of Woodside

Petroleum and its competitor, Santos in the Australian market. It has been evaluated that the

presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. it is

inherent that Woodside Petroleum has maintained an effective remuneration structure in line

with its overall financial performance. However, deficiencies could be observed in the executive

remuneration structure of Santos because of the poor financial health in the Australian market.

The net income of Woodside has increased coupled with fall in outstanding shares for

Woodside and the situation is just the opposite for Santos due to negative net income. Hence, the

returns of the shareholders are maximised for Woodside Petroleum. It needs to be also seen that

there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million.

Executive Summary:

The current report is concerned with evaluating the remuneration structure of Woodside

Petroleum and its competitor, Santos in the Australian market. It has been evaluated that the

presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. it is

inherent that Woodside Petroleum has maintained an effective remuneration structure in line

with its overall financial performance. However, deficiencies could be observed in the executive

remuneration structure of Santos because of the poor financial health in the Australian market.

The net income of Woodside has increased coupled with fall in outstanding shares for

Woodside and the situation is just the opposite for Santos due to negative net income. Hence, the

returns of the shareholders are maximised for Woodside Petroleum. It needs to be also seen that

there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million.

2MANAGERIAL ACCOUNTING

Table of Contents

1. Introduction:................................................................................................................................3

2. Review of topic and review of literature:....................................................................................3

2.1 Executive performance and remuneration in public companies:...........................................3

2.2 Effectiveness of control systems within companies:.............................................................5

3. Company reviews:.......................................................................................................................6

3.1 Details of remuneration committee and membership:...........................................................6

3.2 Allocation of executive remuneration:..................................................................................8

3.3 Mix of performance measures used:....................................................................................11

3.4 Company performance versus executive pay:.....................................................................17

4. Summary of findings:................................................................................................................19

5. Analysis and comparison of remuneration methods used:........................................................20

5.1 Best result in terms of shareholder returns:.........................................................................20

5.2 Best result in short-term:.....................................................................................................21

5.3 Best result in long-term:......................................................................................................22

6. Conclusion:................................................................................................................................23

References:....................................................................................................................................24

Table of Contents

1. Introduction:................................................................................................................................3

2. Review of topic and review of literature:....................................................................................3

2.1 Executive performance and remuneration in public companies:...........................................3

2.2 Effectiveness of control systems within companies:.............................................................5

3. Company reviews:.......................................................................................................................6

3.1 Details of remuneration committee and membership:...........................................................6

3.2 Allocation of executive remuneration:..................................................................................8

3.3 Mix of performance measures used:....................................................................................11

3.4 Company performance versus executive pay:.....................................................................17

4. Summary of findings:................................................................................................................19

5. Analysis and comparison of remuneration methods used:........................................................20

5.1 Best result in terms of shareholder returns:.........................................................................20

5.2 Best result in short-term:.....................................................................................................21

5.3 Best result in long-term:......................................................................................................22

6. Conclusion:................................................................................................................................23

References:....................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

1. Introduction:

The report aims in identifying the role of remuneration, which is depicted in the annual

report of an organisation. Remuneration report is mainly depicted in the annual report as per the

rulings of Companies Act, where the organisation needs to detect all the remuneration that has

been provided to the directors of the company. Remuneration report also allows the investors to

understand the level of income, which is generated by the directors of the company during

declining profit and improving earnings. The report mainly exists to evaluate the remuneration

report of Woodside Petroleum for the fiscal year of 2017. Further evaluation on the company is

conducted in the overall assessment where its remuneration report is analysed, while other

financial performance measures are also taken into consideration. With the summary of findings

and the comparison of the remuneration report, the assessment portrays the company’s

performance over the fiscal years.

2. Review of topic and review of literature:

2.1 Executive performance and remuneration in public companies:

Both executive performance evaluation and remuneration in public companies are

depicted in the annual report of the organisation. The remuneration report depicted in the

financial statement directly indicates the level of bonuses and monetary benefits that has been

provided to the directors and executives of the organisation. This identified remuneration system

is adequately evaluated by the auditors and regulator to identify whether the organisation is

correctly providing remunerations to its directors and executives. In this context, Riaz, et al.,

(2015) stated that organisation with the help of remuneration report is able to detect the level of

1. Introduction:

The report aims in identifying the role of remuneration, which is depicted in the annual

report of an organisation. Remuneration report is mainly depicted in the annual report as per the

rulings of Companies Act, where the organisation needs to detect all the remuneration that has

been provided to the directors of the company. Remuneration report also allows the investors to

understand the level of income, which is generated by the directors of the company during

declining profit and improving earnings. The report mainly exists to evaluate the remuneration

report of Woodside Petroleum for the fiscal year of 2017. Further evaluation on the company is

conducted in the overall assessment where its remuneration report is analysed, while other

financial performance measures are also taken into consideration. With the summary of findings

and the comparison of the remuneration report, the assessment portrays the company’s

performance over the fiscal years.

2. Review of topic and review of literature:

2.1 Executive performance and remuneration in public companies:

Both executive performance evaluation and remuneration in public companies are

depicted in the annual report of the organisation. The remuneration report depicted in the

financial statement directly indicates the level of bonuses and monetary benefits that has been

provided to the directors and executives of the organisation. This identified remuneration system

is adequately evaluated by the auditors and regulator to identify whether the organisation is

correctly providing remunerations to its directors and executives. In this context, Riaz, et al.,

(2015) stated that organisation with the help of remuneration report is able to detect the level of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

income that is distributed to directors and executives of the organisation. The level of

remuneration that is provided to the directors is considered to be as bonuses for the efforts

delivered by the Managing Directors. On the other hand, Hooghiemstra, Kuang and Qin (2017)

argued that investors are able to evaluate the loopholes in the current accounting system of

organisations, when they are able to identify that high remunerations are provided to director

while the organisation is making losses.

The remuneration report directly involved different types of methods that are used by the

organisation in paying the directives and executives. There are two different levels of payment

such as share-based payments and monetary payments. The organisation mainly provide share

based payment to the director and executive for long duration, while restricting the level of trees

that could be conducted for a particular period. This eventually helps in supporting the overall

share value of the organisation if the directors and executive think of selling their portion of

shares. Furthermore, the monetary benefit that is provided by the organisation is mainly for the

services that were conducted during the fiscal year. The bonuses are based on future share based

payments, which are provided to the executive for their services during the fiscal year.

According to Faghani, Monem and Ng (2015), the remuneration provided by the company to the

executive is based on the performance evaluation, which is conducted on annual basis to identify

the most efficient executive of the company. Moreover, Riaz, et al., (2015) indicated that

motivating the executive with monetary benefits for an effort during the fiscal year eventually

helps in improving the motivation level of employees. Therefore, with the remuneration report,

the organisation is able to detect the level of expenses that is conducted on executives and

directors for their initiatives. This eventually allows the investors to detect the level of expenses

income that is distributed to directors and executives of the organisation. The level of

remuneration that is provided to the directors is considered to be as bonuses for the efforts

delivered by the Managing Directors. On the other hand, Hooghiemstra, Kuang and Qin (2017)

argued that investors are able to evaluate the loopholes in the current accounting system of

organisations, when they are able to identify that high remunerations are provided to director

while the organisation is making losses.

The remuneration report directly involved different types of methods that are used by the

organisation in paying the directives and executives. There are two different levels of payment

such as share-based payments and monetary payments. The organisation mainly provide share

based payment to the director and executive for long duration, while restricting the level of trees

that could be conducted for a particular period. This eventually helps in supporting the overall

share value of the organisation if the directors and executive think of selling their portion of

shares. Furthermore, the monetary benefit that is provided by the organisation is mainly for the

services that were conducted during the fiscal year. The bonuses are based on future share based

payments, which are provided to the executive for their services during the fiscal year.

According to Faghani, Monem and Ng (2015), the remuneration provided by the company to the

executive is based on the performance evaluation, which is conducted on annual basis to identify

the most efficient executive of the company. Moreover, Riaz, et al., (2015) indicated that

motivating the executive with monetary benefits for an effort during the fiscal year eventually

helps in improving the motivation level of employees. Therefore, with the remuneration report,

the organisation is able to detect the level of expenses that is conducted on executives and

directors for their initiatives. This eventually allows the investors to detect the level of expenses

5MANAGERIAL ACCOUNTING

and determine whether the remuneration amount is feasible and viable for the directors or

executives.

2.2 Effectiveness of control systems within companies:

Presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. Scott

(2015) mentioned that without the presence of adequate control system within the organisation

the management is not able to exercise decisions, which could improve productivity and

efficiency of the company. Without the presence of an adequate control system businesses are

not able to develop and execute strategic plans, which helps in generating higher revenue in the

end. Therefore, it could be understood that organisations using the control system are able to

fulfil their objectives and obtain sustainable growth by adequately utilising the available

resources. The organisation also needs to have an adequate internal control system to support the

legal and regulatory standards that has been imposed by the adequate authorities. Hence, it could

be understood that without the presence of effective control system organisations are not able to

operate their 100%, which directly affects their capability to reach higher levels of revenue and

income (Argyris, 2017).

There are different benefits of an effective control system, which can be used by the

organisation to improve the timing of their decision making process. Furthermore, an effective

control system would increase the quality of information that can be received by different

departments of the organisation (Kerzner and Kerzner, 2017). This eventually helps in

minimising the lead-time that is taken for transferring data from one department to other. This

and determine whether the remuneration amount is feasible and viable for the directors or

executives.

2.2 Effectiveness of control systems within companies:

Presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. Scott

(2015) mentioned that without the presence of adequate control system within the organisation

the management is not able to exercise decisions, which could improve productivity and

efficiency of the company. Without the presence of an adequate control system businesses are

not able to develop and execute strategic plans, which helps in generating higher revenue in the

end. Therefore, it could be understood that organisations using the control system are able to

fulfil their objectives and obtain sustainable growth by adequately utilising the available

resources. The organisation also needs to have an adequate internal control system to support the

legal and regulatory standards that has been imposed by the adequate authorities. Hence, it could

be understood that without the presence of effective control system organisations are not able to

operate their 100%, which directly affects their capability to reach higher levels of revenue and

income (Argyris, 2017).

There are different benefits of an effective control system, which can be used by the

organisation to improve the timing of their decision making process. Furthermore, an effective

control system would increase the quality of information that can be received by different

departments of the organisation (Kerzner and Kerzner, 2017). This eventually helps in

minimising the lead-time that is taken for transferring data from one department to other. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

adequate effectiveness would eventually help in reducing the time taken for the decision making

process, which increases their operating conditions This improvement in the control system

would eventually allow the organisation to successfully complete the financial report on time

without delay. Furthermore, organisations with the help of the control system are able to design

and maintain adequate executive performance and reward system, which could be used for

motivating employees. This kind of systems is eventually helpful to motivate the workforce and

minimise the employee turnover ratio of an organisation. Sayles (2017) stated that with the use

of adequate reward system organisations are able to maximize the output of a workforce present

within the company. Therefore, it can be understood that within an effective control systems the

organisation is set on right track, where the operations and efficiency would eventually improve.

3. Company reviews:

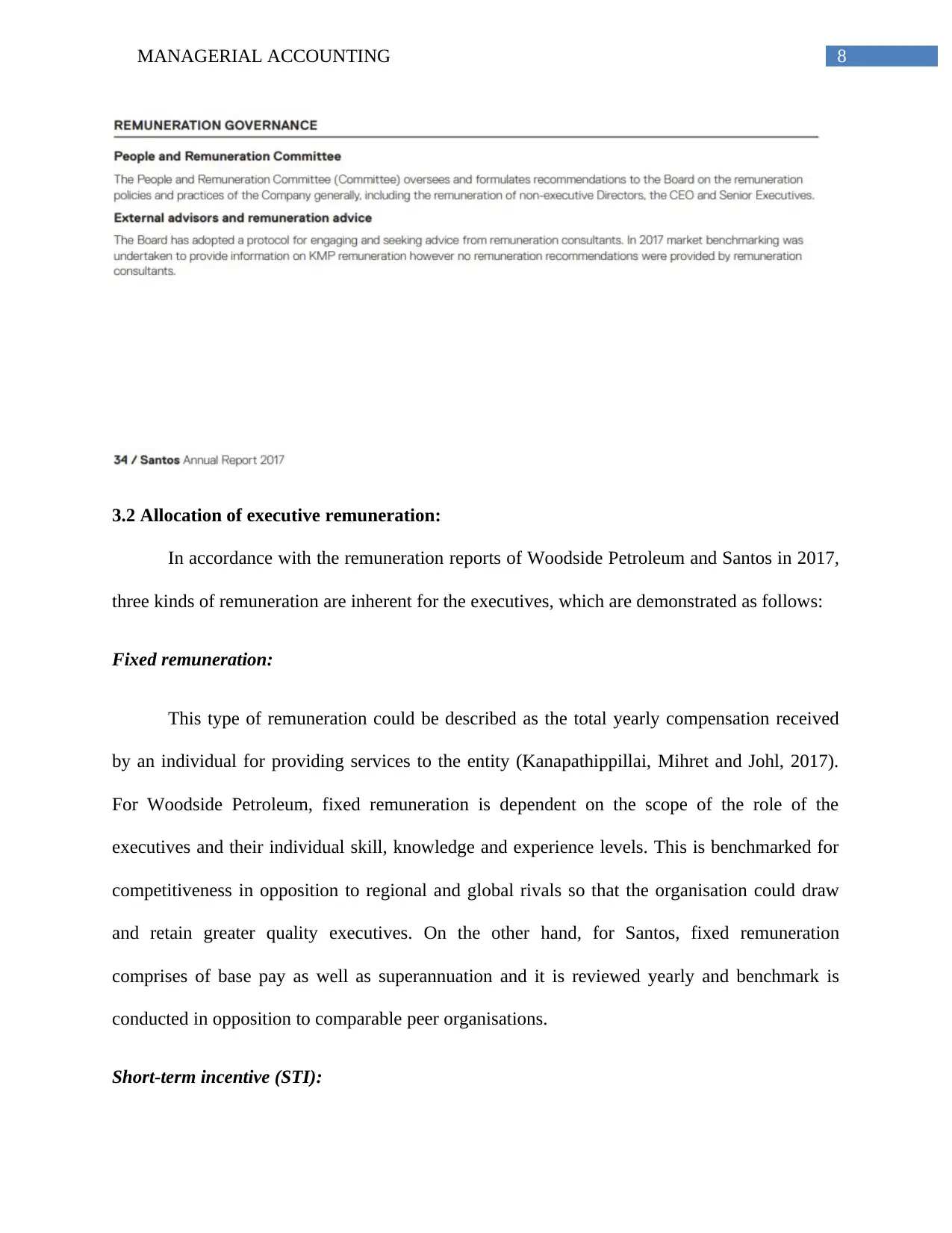

3.1 Details of remuneration committee and membership:

After critical evaluation of the annual report of Woodside Petroleum in 2017, no

disclosures have been made regarding the number of members present in the remuneration

committee, while for Santos, three members are present in the remuneration committee of the

organisation. The remuneration committee is accountable for reviewing as well as

recommending the board regarding the remuneration policy of the organisation while assessing

its efficiency and compliance with the relevant standards (Beaumont, Clarkson and Tutticci,

2018). Moreover, another responsibility of these committees is to review and recommend the

individual levels of remuneration related to the key personnel of the two organisations. The

memberships of the committees and their chairpersons would be determined based on the

business situations by the respective boards (Scott, 2015).

adequate effectiveness would eventually help in reducing the time taken for the decision making

process, which increases their operating conditions This improvement in the control system

would eventually allow the organisation to successfully complete the financial report on time

without delay. Furthermore, organisations with the help of the control system are able to design

and maintain adequate executive performance and reward system, which could be used for

motivating employees. This kind of systems is eventually helpful to motivate the workforce and

minimise the employee turnover ratio of an organisation. Sayles (2017) stated that with the use

of adequate reward system organisations are able to maximize the output of a workforce present

within the company. Therefore, it can be understood that within an effective control systems the

organisation is set on right track, where the operations and efficiency would eventually improve.

3. Company reviews:

3.1 Details of remuneration committee and membership:

After critical evaluation of the annual report of Woodside Petroleum in 2017, no

disclosures have been made regarding the number of members present in the remuneration

committee, while for Santos, three members are present in the remuneration committee of the

organisation. The remuneration committee is accountable for reviewing as well as

recommending the board regarding the remuneration policy of the organisation while assessing

its efficiency and compliance with the relevant standards (Beaumont, Clarkson and Tutticci,

2018). Moreover, another responsibility of these committees is to review and recommend the

individual levels of remuneration related to the key personnel of the two organisations. The

memberships of the committees and their chairpersons would be determined based on the

business situations by the respective boards (Scott, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

The remuneration committees of both the organisations hold time to time meetings in a

specific financial period depending on both external and internal situations. Moreover, both the

organisations use independent consultants in order to gather professional advice related to

executive remuneration as well as other matters associated remuneration and there is direct

relationship between these services and the remuneration committees (Goh and Gupta, 2016).

The chairpersons of the committee are engaged in evaluating the associations and costs to be

incurred for the management consultants. Finally, it has been identified that the remuneration

committees of both organisations obtain recommendations from their consultants to adhere to the

“Corporations Act 2001”.

The remuneration committees of both the organisations hold time to time meetings in a

specific financial period depending on both external and internal situations. Moreover, both the

organisations use independent consultants in order to gather professional advice related to

executive remuneration as well as other matters associated remuneration and there is direct

relationship between these services and the remuneration committees (Goh and Gupta, 2016).

The chairpersons of the committee are engaged in evaluating the associations and costs to be

incurred for the management consultants. Finally, it has been identified that the remuneration

committees of both organisations obtain recommendations from their consultants to adhere to the

“Corporations Act 2001”.

8MANAGERIAL ACCOUNTING

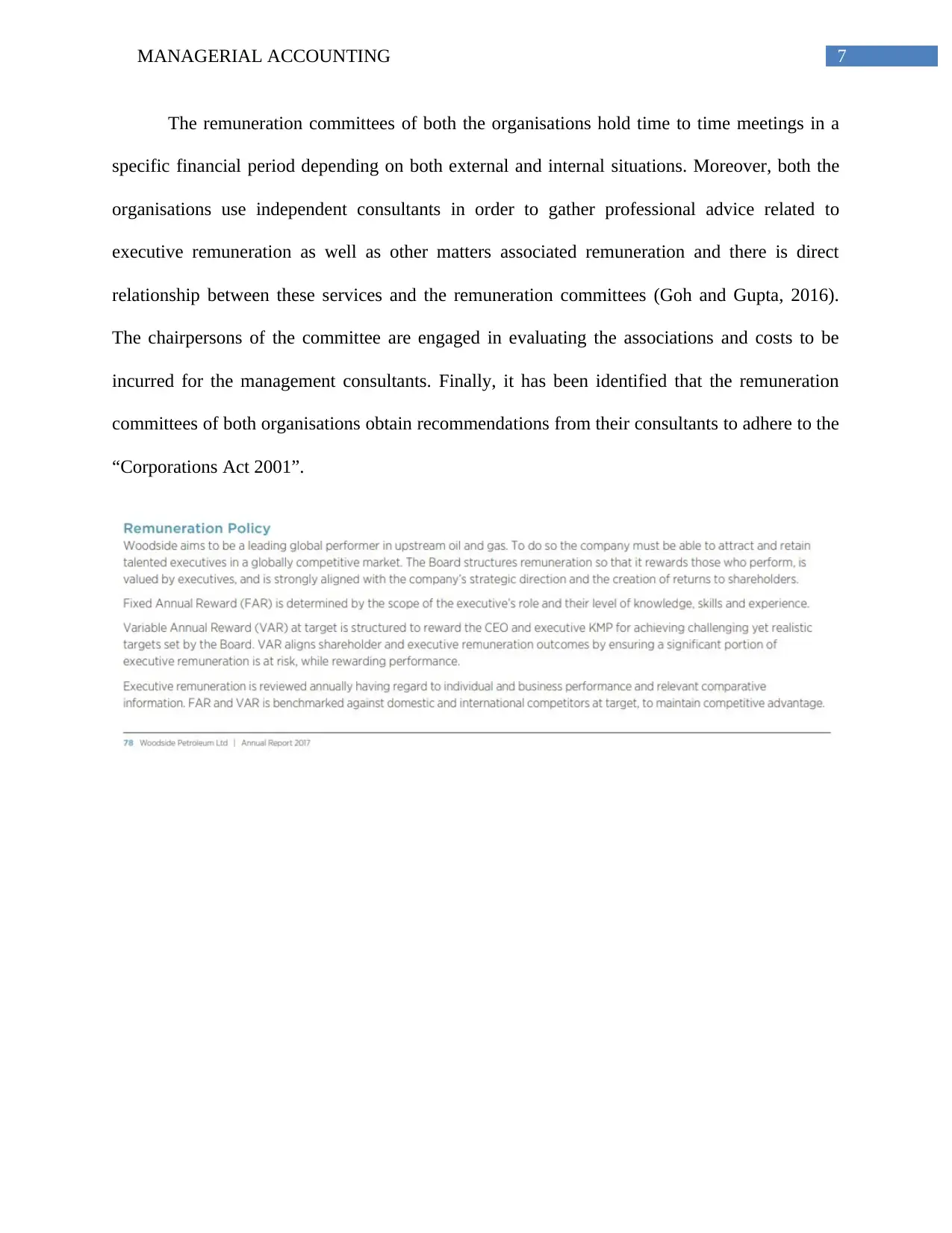

3.2 Allocation of executive remuneration:

In accordance with the remuneration reports of Woodside Petroleum and Santos in 2017,

three kinds of remuneration are inherent for the executives, which are demonstrated as follows:

Fixed remuneration:

This type of remuneration could be described as the total yearly compensation received

by an individual for providing services to the entity (Kanapathippillai, Mihret and Johl, 2017).

For Woodside Petroleum, fixed remuneration is dependent on the scope of the role of the

executives and their individual skill, knowledge and experience levels. This is benchmarked for

competitiveness in opposition to regional and global rivals so that the organisation could draw

and retain greater quality executives. On the other hand, for Santos, fixed remuneration

comprises of base pay as well as superannuation and it is reviewed yearly and benchmark is

conducted in opposition to comparable peer organisations.

Short-term incentive (STI):

3.2 Allocation of executive remuneration:

In accordance with the remuneration reports of Woodside Petroleum and Santos in 2017,

three kinds of remuneration are inherent for the executives, which are demonstrated as follows:

Fixed remuneration:

This type of remuneration could be described as the total yearly compensation received

by an individual for providing services to the entity (Kanapathippillai, Mihret and Johl, 2017).

For Woodside Petroleum, fixed remuneration is dependent on the scope of the role of the

executives and their individual skill, knowledge and experience levels. This is benchmarked for

competitiveness in opposition to regional and global rivals so that the organisation could draw

and retain greater quality executives. On the other hand, for Santos, fixed remuneration

comprises of base pay as well as superannuation and it is reviewed yearly and benchmark is

conducted in opposition to comparable peer organisations.

Short-term incentive (STI):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

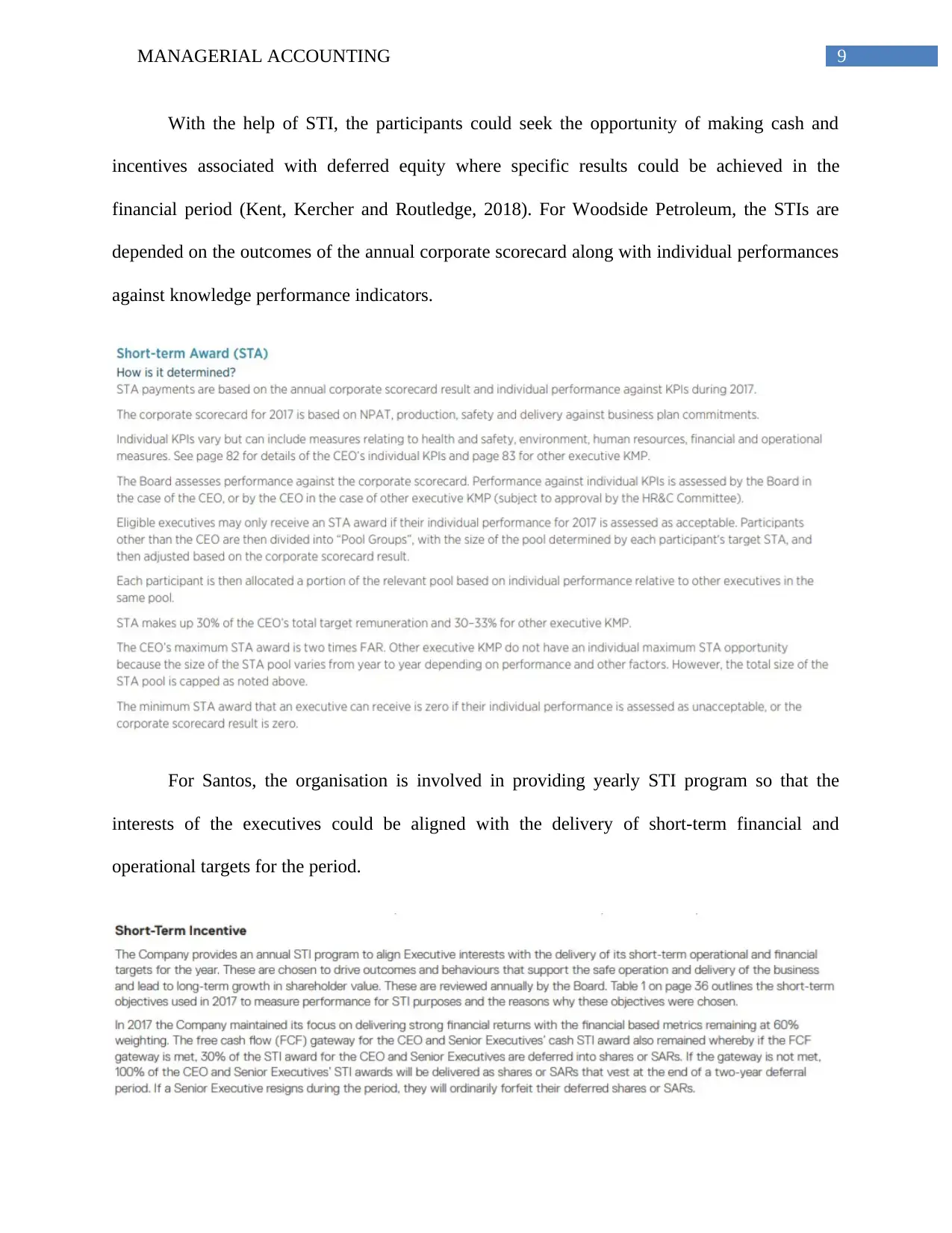

With the help of STI, the participants could seek the opportunity of making cash and

incentives associated with deferred equity where specific results could be achieved in the

financial period (Kent, Kercher and Routledge, 2018). For Woodside Petroleum, the STIs are

depended on the outcomes of the annual corporate scorecard along with individual performances

against knowledge performance indicators.

For Santos, the organisation is involved in providing yearly STI program so that the

interests of the executives could be aligned with the delivery of short-term financial and

operational targets for the period.

With the help of STI, the participants could seek the opportunity of making cash and

incentives associated with deferred equity where specific results could be achieved in the

financial period (Kent, Kercher and Routledge, 2018). For Woodside Petroleum, the STIs are

depended on the outcomes of the annual corporate scorecard along with individual performances

against knowledge performance indicators.

For Santos, the organisation is involved in providing yearly STI program so that the

interests of the executives could be aligned with the delivery of short-term financial and

operational targets for the period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

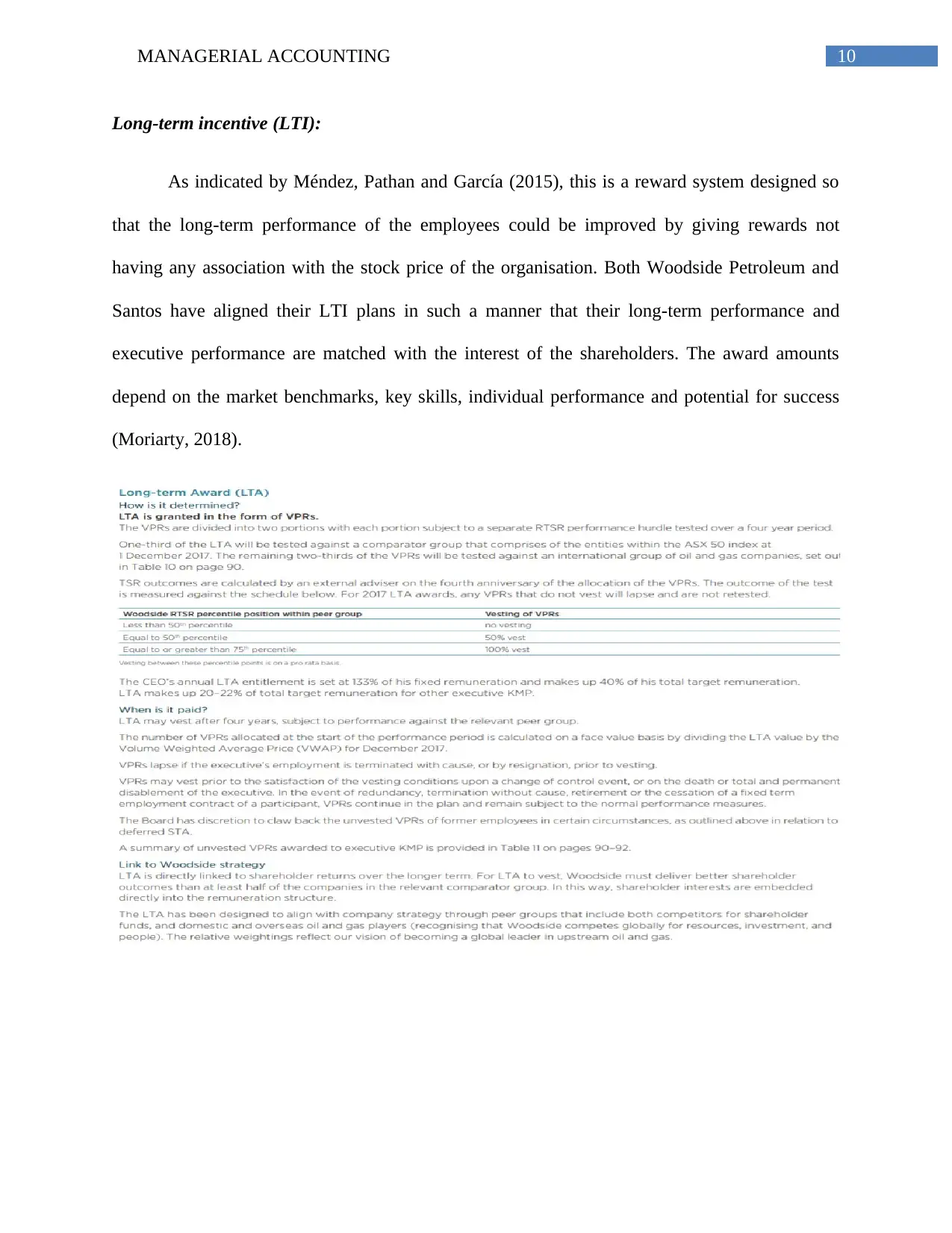

Long-term incentive (LTI):

As indicated by Méndez, Pathan and García (2015), this is a reward system designed so

that the long-term performance of the employees could be improved by giving rewards not

having any association with the stock price of the organisation. Both Woodside Petroleum and

Santos have aligned their LTI plans in such a manner that their long-term performance and

executive performance are matched with the interest of the shareholders. The award amounts

depend on the market benchmarks, key skills, individual performance and potential for success

(Moriarty, 2018).

Long-term incentive (LTI):

As indicated by Méndez, Pathan and García (2015), this is a reward system designed so

that the long-term performance of the employees could be improved by giving rewards not

having any association with the stock price of the organisation. Both Woodside Petroleum and

Santos have aligned their LTI plans in such a manner that their long-term performance and

executive performance are matched with the interest of the shareholders. The award amounts

depend on the market benchmarks, key skills, individual performance and potential for success

(Moriarty, 2018).

11MANAGERIAL ACCOUNTING

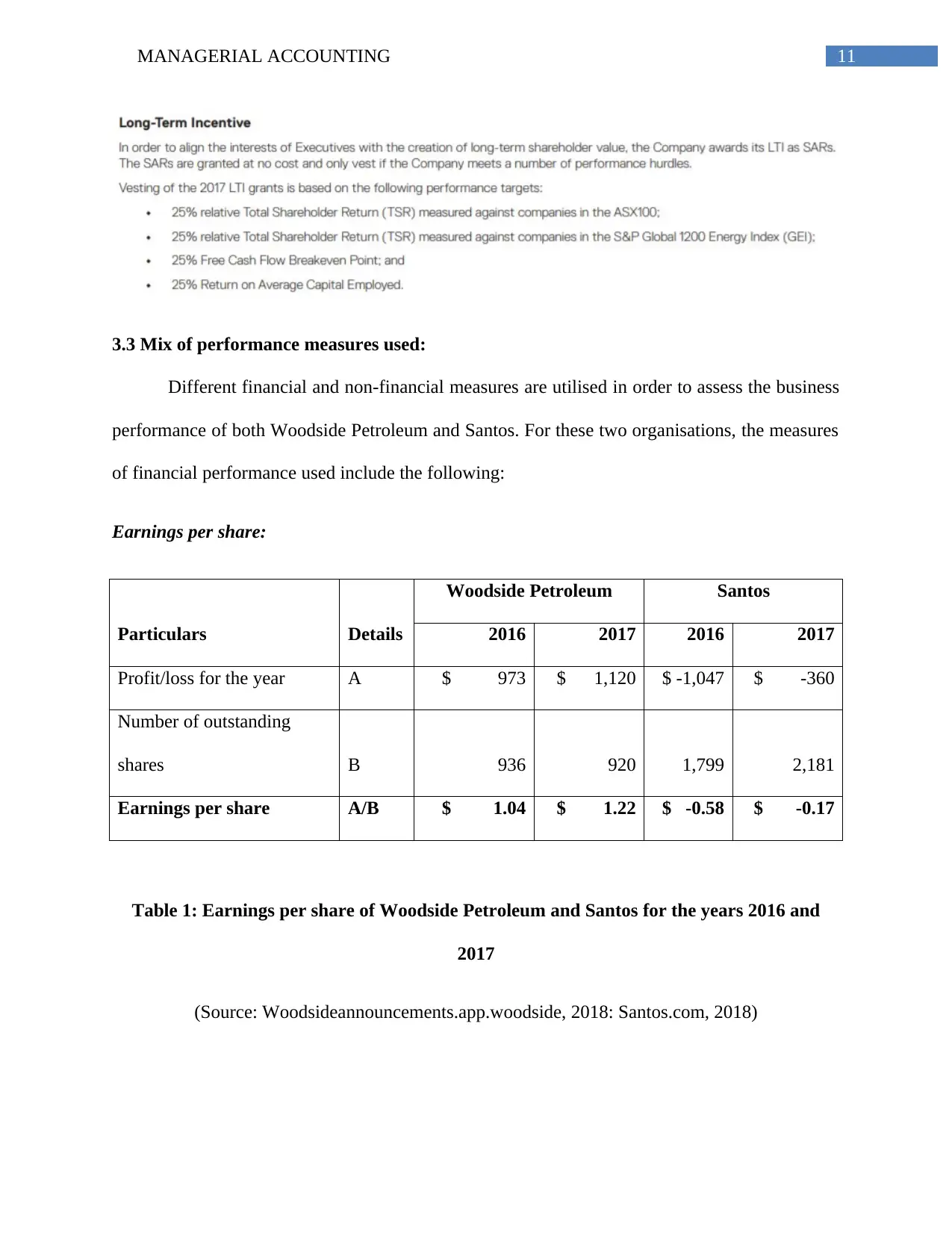

3.3 Mix of performance measures used:

Different financial and non-financial measures are utilised in order to assess the business

performance of both Woodside Petroleum and Santos. For these two organisations, the measures

of financial performance used include the following:

Earnings per share:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Profit/loss for the year A $ 973 $ 1,120 $ -1,047 $ -360

Number of outstanding

shares B 936 920 1,799 2,181

Earnings per share A/B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Table 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

3.3 Mix of performance measures used:

Different financial and non-financial measures are utilised in order to assess the business

performance of both Woodside Petroleum and Santos. For these two organisations, the measures

of financial performance used include the following:

Earnings per share:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Profit/loss for the year A $ 973 $ 1,120 $ -1,047 $ -360

Number of outstanding

shares B 936 920 1,799 2,181

Earnings per share A/B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Table 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.