Financial Accounting Report and Budget Recommendations for 2018

VerifiedAdded on 2020/05/16

|23

|1479

|354

Report

AI Summary

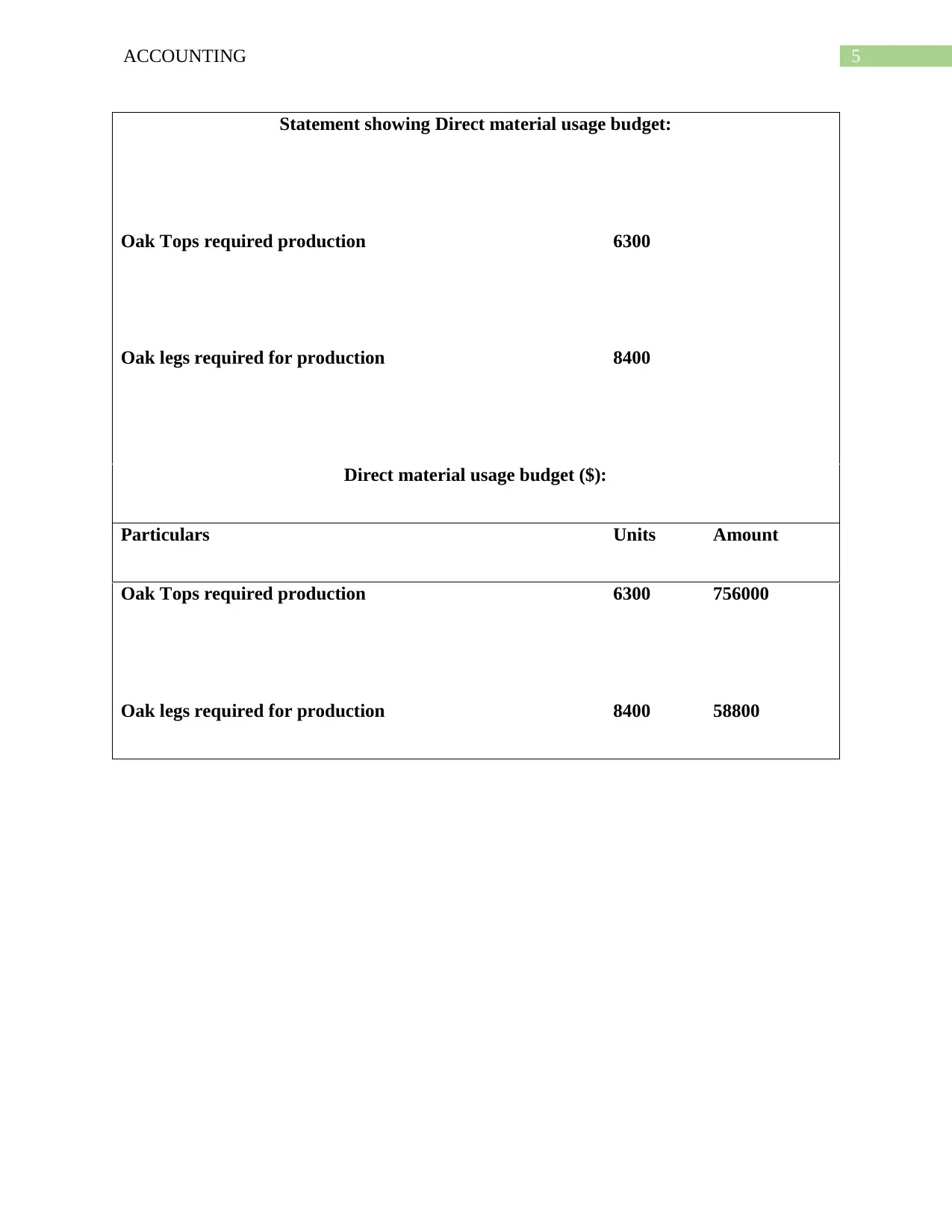

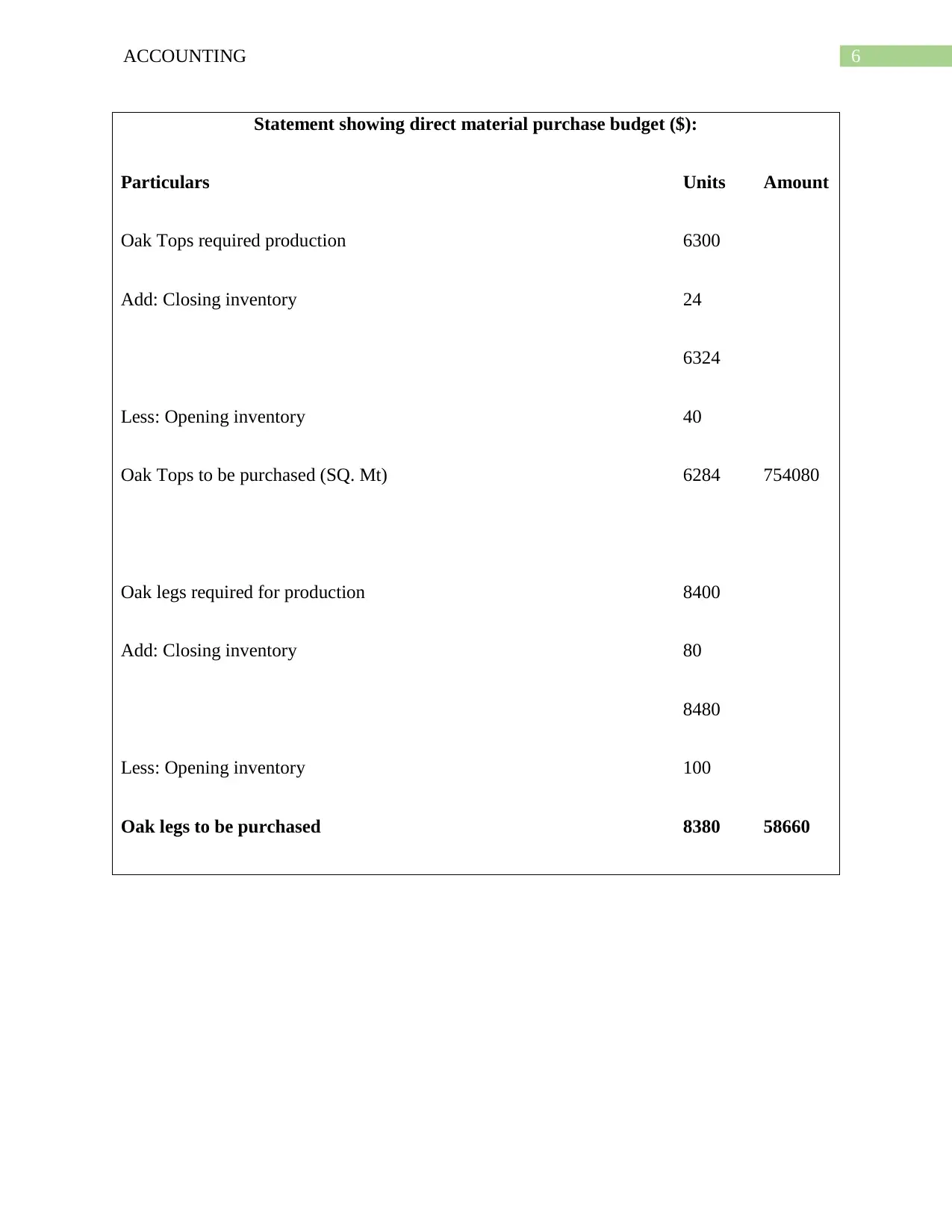

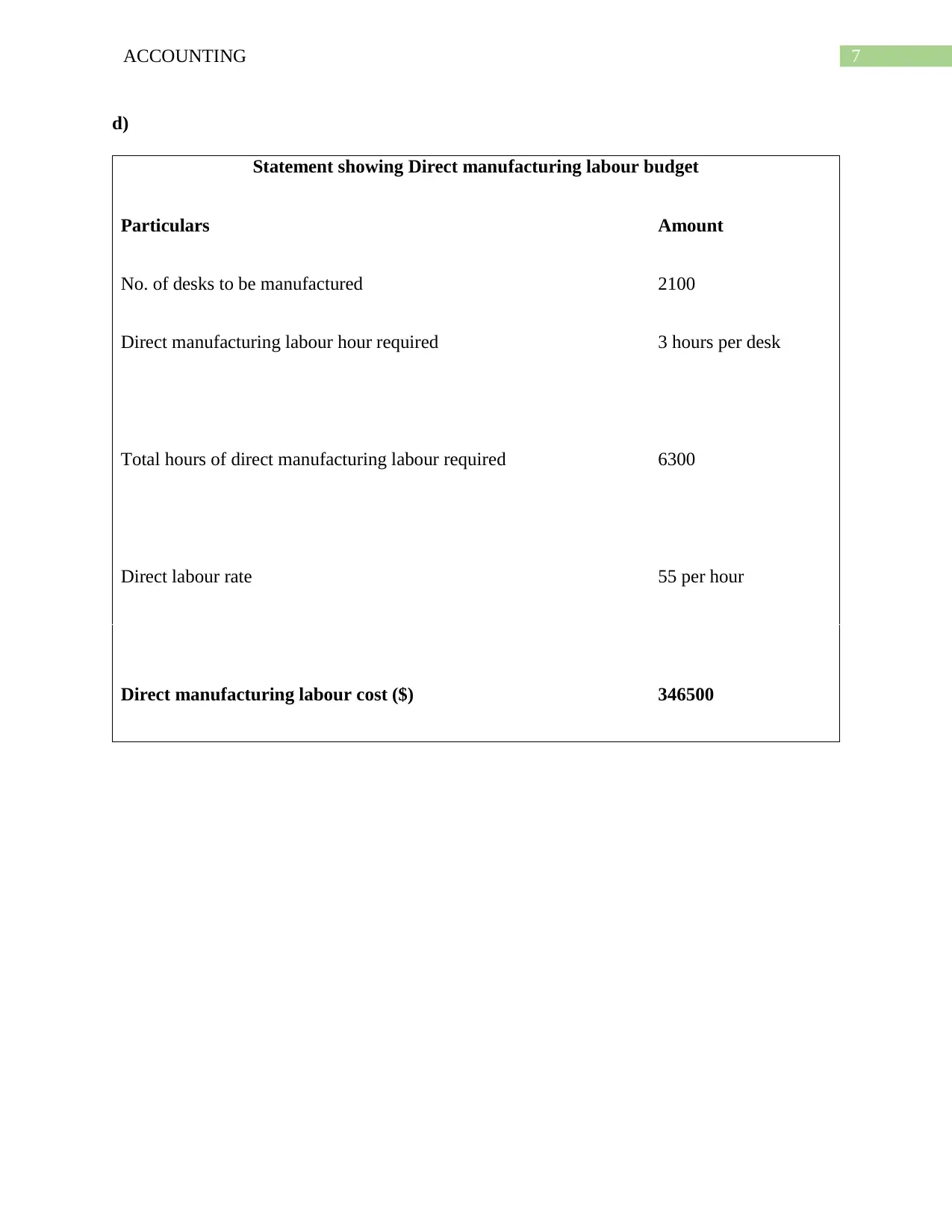

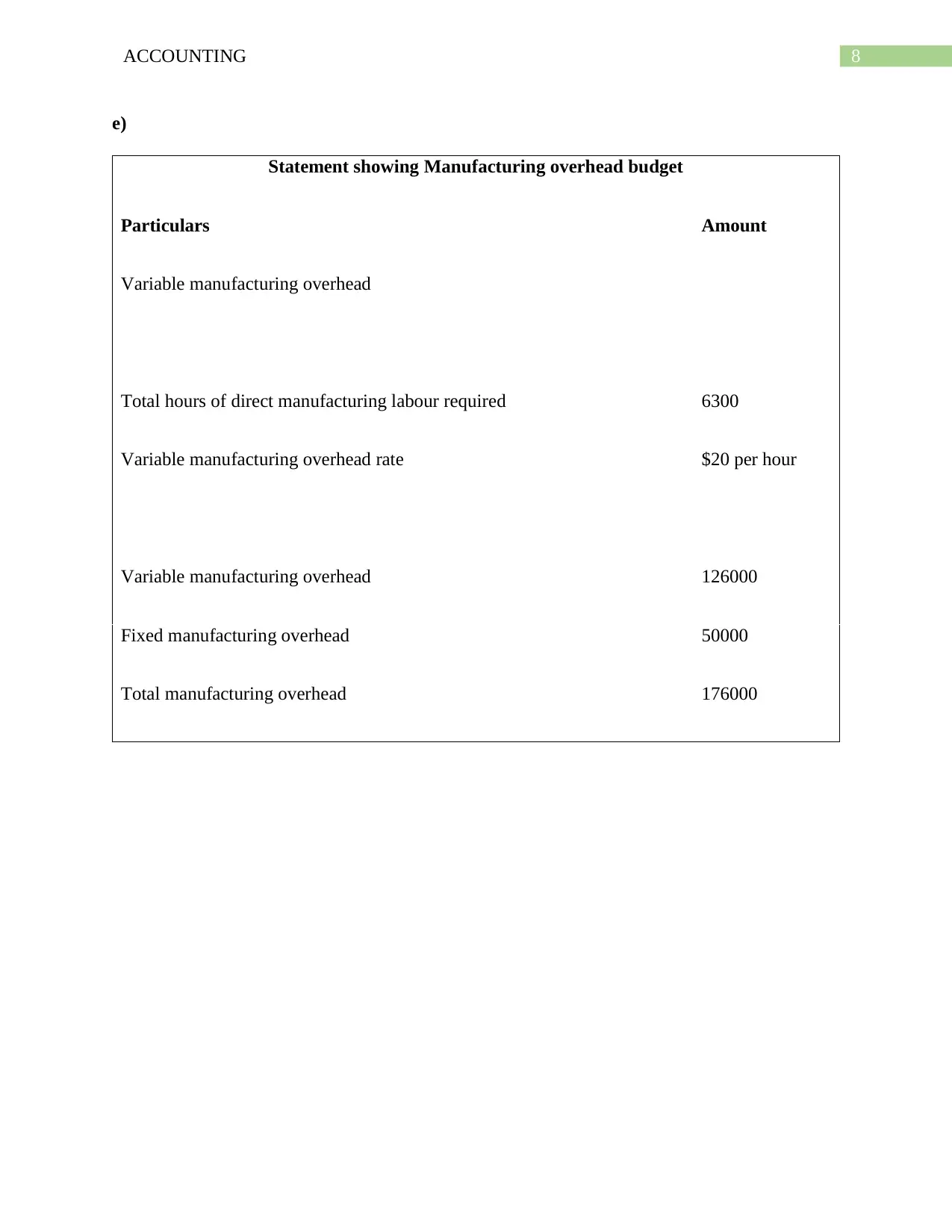

This accounting report analyzes the financial performance of Exhibition Furniture, focusing on budget recommendations for 2018. It examines revenue projections, cost of goods sold, and inventory management, particularly the impact of increasing prices for raw materials like oak tops and legs. The report highlights the company's use of the FIFO method and identifies key issues such as rising material costs and the need for efficient resource utilization. Recommendations include inviting quotations for raw materials, optimizing resource use, implementing an effective appraisal method for overhead costs, and adopting modern equipment to enhance production efficiency and customer satisfaction. The report aims to improve the company's financial performance and operational efficiency through strategic budgeting and cost control measures, as detailed in the memorandum to the CEO.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.