Case Study: Analyzing Business Cycles at Paradise Industries

VerifiedAdded on 2023/01/11

|15

|3158

|78

Case Study

AI Summary

This case study provides a comprehensive analysis of Paradise Industries, focusing on its expenditure and conversion cycles. It begins with system flowcharts illustrating these cycles, detailing the processes involved in purchasing and converting resources into cash. The analysis identifies weaknesses in internal controls, particularly in the expenditure cycle, highlighting structural and documentation issues. The study examines risks within the conversion cycle, such as payment delays, decline in liquidity, and various operational challenges like void invoices and inventory deficiencies. Recommendations are provided to mitigate these risks, including establishing cognitive management activity for better financial control, adjusting procedures for excesses, and establishing regulatory systems. The study emphasizes the importance of internal controls and suggests improvements aligned with the COSO internal control module to enhance overall business process efficiency and reduce potential financial risks. The analysis underscores the significance of a well-managed cash conversion cycle for the financial health and sustainability of the company.

CASE STUDY-

PARADISE

INDUSTRIES

PARADISE

INDUSTRIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1. System flow chart of expenditure cycle...................................................................................4

1.1 Analysis of physical internal control weaknesses in the expenditure cycle......................5

2. System flow chart of conversion cycle....................................................................................9

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to reduce the

risks........................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

1. System flow chart of expenditure cycle...................................................................................4

1.1 Analysis of physical internal control weaknesses in the expenditure cycle......................5

2. System flow chart of conversion cycle....................................................................................9

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to reduce the

risks........................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

This action report is based on two working ideas; an expense cycle and a money exchange cycle.

The cycle flow chart will show the use of how and when to set up a purchase request and how

many duplicates must be sent to initiate a purchase request and will also talk about managing the

status of the work in progress. Discussion on the deficiency of the conventional construction

process model was discussed and a viable proposal is also proposed. The other consideration is a

cycle that changes money; he talked about the time and risks associated with the transformation

of finished products into money and also clarified the entire cycle method.

This action report is based on two working ideas; an expense cycle and a money exchange cycle.

The cycle flow chart will show the use of how and when to set up a purchase request and how

many duplicates must be sent to initiate a purchase request and will also talk about managing the

status of the work in progress. Discussion on the deficiency of the conventional construction

process model was discussed and a viable proposal is also proposed. The other consideration is a

cycle that changes money; he talked about the time and risks associated with the transformation

of finished products into money and also clarified the entire cycle method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

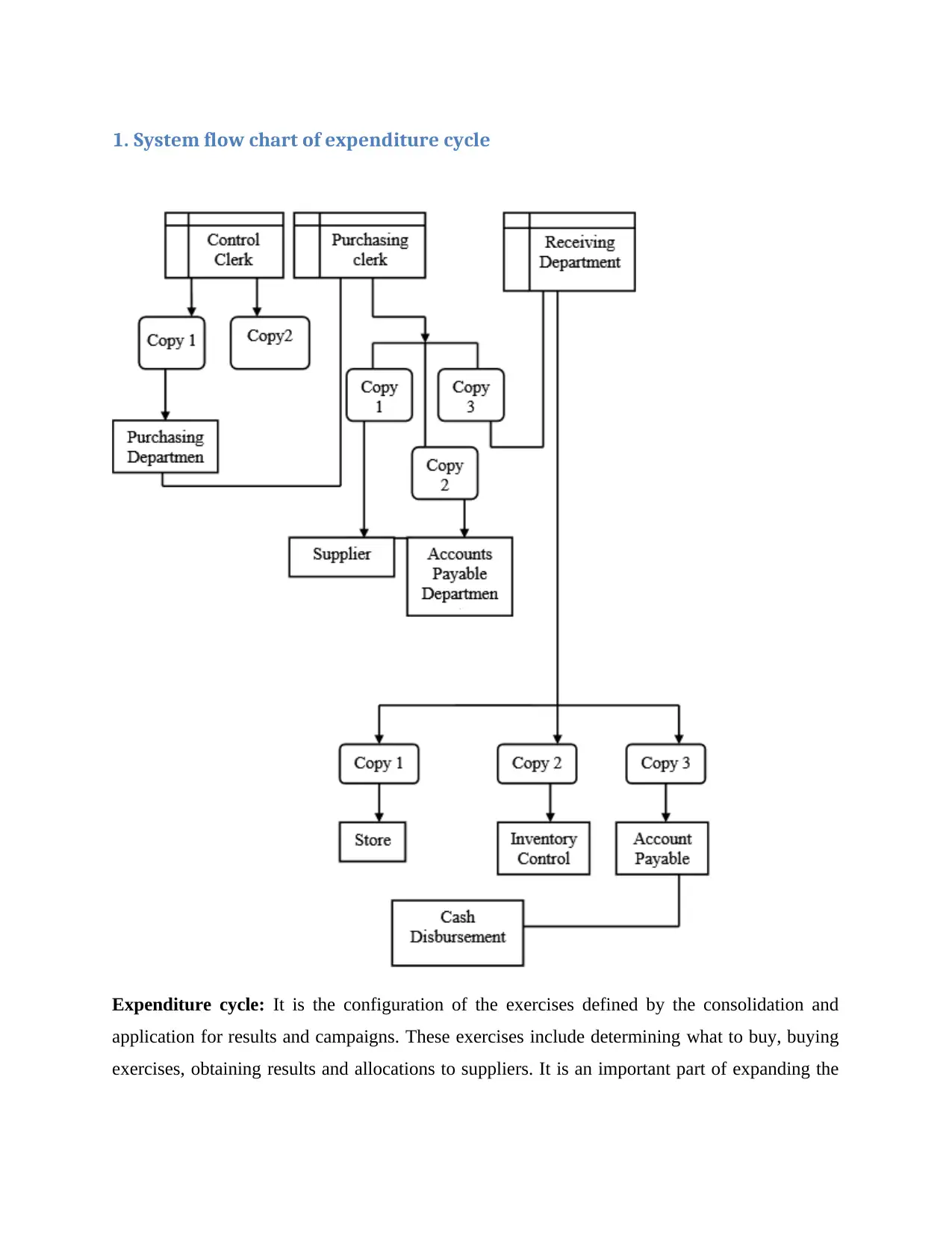

1. System flow chart of expenditure cycle

Expenditure cycle: It is the configuration of the exercises defined by the consolidation and

application for results and campaigns. These exercises include determining what to buy, buying

exercises, obtaining results and allocations to suppliers. It is an important part of expanding the

Expenditure cycle: It is the configuration of the exercises defined by the consolidation and

application for results and campaigns. These exercises include determining what to buy, buying

exercises, obtaining results and allocations to suppliers. It is an important part of expanding the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

use of routers, since the beginning of the ring business, where to purchase volume-based

prerequisites and a type of customer orders.

There are several distinct sections in the Expenditure cycle, including the demand for products

and campaigns, the choice of the supplier, the demand for goods and businesses, the receipt and

the resulting allowance.

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

• The income cycle system: the accountant (AC) performs most of the RC practices and incurs a

heavy burden on companies, especially RC, trades or methods. He is the beneficiary and

validates the customer's claim, preparing RC startup files, for example, slowing the orders / fine

pressing, but also maintains the stock general and the requests that the buyer buys. This is the

place where deceitful acts can occur. For models, the CA may have a sensitive position with the

customer and the President / Owner being deceived; it can also incur costs that are largely

reputable to the customer, but it records and reports on transactions using the standard. (Arens

and et.al., 2003).

• Expenditure cycle system: The Company combines authorization, registration and custody

functions in a single office; control of collection, purchases and stocks (R, P and IC). This is a

violation of the distribution of duties. R, P and IC staff carries out most of the community

practices and have a number of corporate responsibilities, in particular CE, operations or

procedures. Make requests, reconcile returns, split and post the stock and distribute the records

of paid information. This is the place where deceptive acts can occur. For models, R, P and IC

personnel may have controversial situations with the sender and the dismissal of the President /

Owner; he can also take unorganized soup (as well as hard food) and nobody will aim (Chan,

2006).

2. Weaknesses of documentation and commercial actions (methods)

The potential problems for (specialized) documents and businesses within a monstrous eggplant

consumption model are:

prerequisites and a type of customer orders.

There are several distinct sections in the Expenditure cycle, including the demand for products

and campaigns, the choice of the supplier, the demand for goods and businesses, the receipt and

the resulting allowance.

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

• The income cycle system: the accountant (AC) performs most of the RC practices and incurs a

heavy burden on companies, especially RC, trades or methods. He is the beneficiary and

validates the customer's claim, preparing RC startup files, for example, slowing the orders / fine

pressing, but also maintains the stock general and the requests that the buyer buys. This is the

place where deceitful acts can occur. For models, the CA may have a sensitive position with the

customer and the President / Owner being deceived; it can also incur costs that are largely

reputable to the customer, but it records and reports on transactions using the standard. (Arens

and et.al., 2003).

• Expenditure cycle system: The Company combines authorization, registration and custody

functions in a single office; control of collection, purchases and stocks (R, P and IC). This is a

violation of the distribution of duties. R, P and IC staff carries out most of the community

practices and have a number of corporate responsibilities, in particular CE, operations or

procedures. Make requests, reconcile returns, split and post the stock and distribute the records

of paid information. This is the place where deceptive acts can occur. For models, R, P and IC

personnel may have controversial situations with the sender and the dismissal of the President /

Owner; he can also take unorganized soup (as well as hard food) and nobody will aim (Chan,

2006).

2. Weaknesses of documentation and commercial actions (methods)

The potential problems for (specialized) documents and businesses within a monstrous eggplant

consumption model are:

• Good numbers in EC records, for example, do not negate the number of entries. Creating and

separating performance / report will be problematic, especially when the association begins to

run another accounting structure.

• During the scope of the approval application field, the accountant confirms the claim directly

without checking the customer's credit records (customer check record or customer accounting

information source). Apparently the client has not yet given much commitment to the society

(Gay and Simnett, 2012).

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Protection of representative books; There are several elements that must be distinguished,

for example, from expenditure, trading records, profitability of stocks, and board data.

This can create empathy between the AC and the customer. Likewise, business side

reports will not be reviewed by the President / Owner. (Australia, 2007).

Documentation checks

The RC documents are not complete:

Multiple copies of Request records for values (CO) are needed for one is not enough. At

an unlikely time when the accountant basically educates the CO emissions information

over the phone, it appears that an operations manager is making up the basic information,

which can lead to misunderstandings.

With respect to the telephone application, there is no specific CO cited by the customer

and a Registered Identification Order (OA), in this sense the trade has no substantive

power and no evidence..

Resource responsibility checks

The employee is asked to order (do) the goods from the construction of traffic center /

place when the CA or the president / owner submit an oral complaint at any informal

separating performance / report will be problematic, especially when the association begins to

run another accounting structure.

• During the scope of the approval application field, the accountant confirms the claim directly

without checking the customer's credit records (customer check record or customer accounting

information source). Apparently the client has not yet given much commitment to the society

(Gay and Simnett, 2012).

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Protection of representative books; There are several elements that must be distinguished,

for example, from expenditure, trading records, profitability of stocks, and board data.

This can create empathy between the AC and the customer. Likewise, business side

reports will not be reviewed by the President / Owner. (Australia, 2007).

Documentation checks

The RC documents are not complete:

Multiple copies of Request records for values (CO) are needed for one is not enough. At

an unlikely time when the accountant basically educates the CO emissions information

over the phone, it appears that an operations manager is making up the basic information,

which can lead to misunderstandings.

With respect to the telephone application, there is no specific CO cited by the customer

and a Registered Identification Order (OA), in this sense the trade has no substantive

power and no evidence..

Resource responsibility checks

The employee is asked to order (do) the goods from the construction of traffic center /

place when the CA or the president / owner submit an oral complaint at any informal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

level, to ensure that the exchange issuer is recognized (reported). This is risky because it

will likely yield results but there is no evidence (Ebert and Griffin, 2005).

Executives exercise controls

There were no regulatory approaches compared to the RC, for example credit approval, account

benefits, endorsements and assessment strategies; this can cause disruption as the rally continues

to form and begin to use more people to manage the RC. With the non-development of clustering

techniques, RC strategies can be rendered in states of vulnerability and irregularity. Also, if the

accountant leaves, the association will have difficulty in establishing the new employee to

replace him.

The possible shortcomings of the general control of the body's EC framework are:

Organizational Controls

Personnel have a number of responsibilities relating to the acquisition, purchase and

inspection of the register, which should vary, for example, from inventory checks, credit

liabilities and customer data. Action. Most of the CE modules are completed by R, P and

IC personnel. This can cause a moving situation.

Document checks

CE documents are not complete as there are no adequate documents of:

Buy the application, which shows that it is not allowed in the application design.

Buy a bid, which shows that there is no officer to trade.

Report Received. This is essential for the stock exchange and further investigation.

Internal controls suggested

For the RC framework:

There should be courses of cognitive management activity for BC, for example, credit

understanding, account privileges and trading and trading components.

Adjustments must be made in accordance with the procedures and strategies indicated by

excesses and receipts (which appear to have been raised).

will likely yield results but there is no evidence (Ebert and Griffin, 2005).

Executives exercise controls

There were no regulatory approaches compared to the RC, for example credit approval, account

benefits, endorsements and assessment strategies; this can cause disruption as the rally continues

to form and begin to use more people to manage the RC. With the non-development of clustering

techniques, RC strategies can be rendered in states of vulnerability and irregularity. Also, if the

accountant leaves, the association will have difficulty in establishing the new employee to

replace him.

The possible shortcomings of the general control of the body's EC framework are:

Organizational Controls

Personnel have a number of responsibilities relating to the acquisition, purchase and

inspection of the register, which should vary, for example, from inventory checks, credit

liabilities and customer data. Action. Most of the CE modules are completed by R, P and

IC personnel. This can cause a moving situation.

Document checks

CE documents are not complete as there are no adequate documents of:

Buy the application, which shows that it is not allowed in the application design.

Buy a bid, which shows that there is no officer to trade.

Report Received. This is essential for the stock exchange and further investigation.

Internal controls suggested

For the RC framework:

There should be courses of cognitive management activity for BC, for example, credit

understanding, account privileges and trading and trading components.

Adjustments must be made in accordance with the procedures and strategies indicated by

excesses and receipts (which appear to have been raised).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traders, for example, need to have the cash receipt diary and recall records periodically

positioned to provide a revised and revised format route

CE Framework:

The regulatory systems should be set up as closely as possible, buying products and the

strategy for buying and distributing money.

Methods and understanding of cash allowances and allowances (only if organized) should be

investigated.

Directors periodically review the screen, checking for breakdowns and portable inventory

reports.

For example, stock burgers need to be looked at to provide stock burgers and forest staff.

Recommendations of these injection controls are in accordance with the control elements and

reviews of the COSO internal control module.

positioned to provide a revised and revised format route

CE Framework:

The regulatory systems should be set up as closely as possible, buying products and the

strategy for buying and distributing money.

Methods and understanding of cash allowances and allowances (only if organized) should be

investigated.

Directors periodically review the screen, checking for breakdowns and portable inventory

reports.

For example, stock burgers need to be looked at to provide stock burgers and forest staff.

Recommendations of these injection controls are in accordance with the control elements and

reviews of the COSO internal control module.

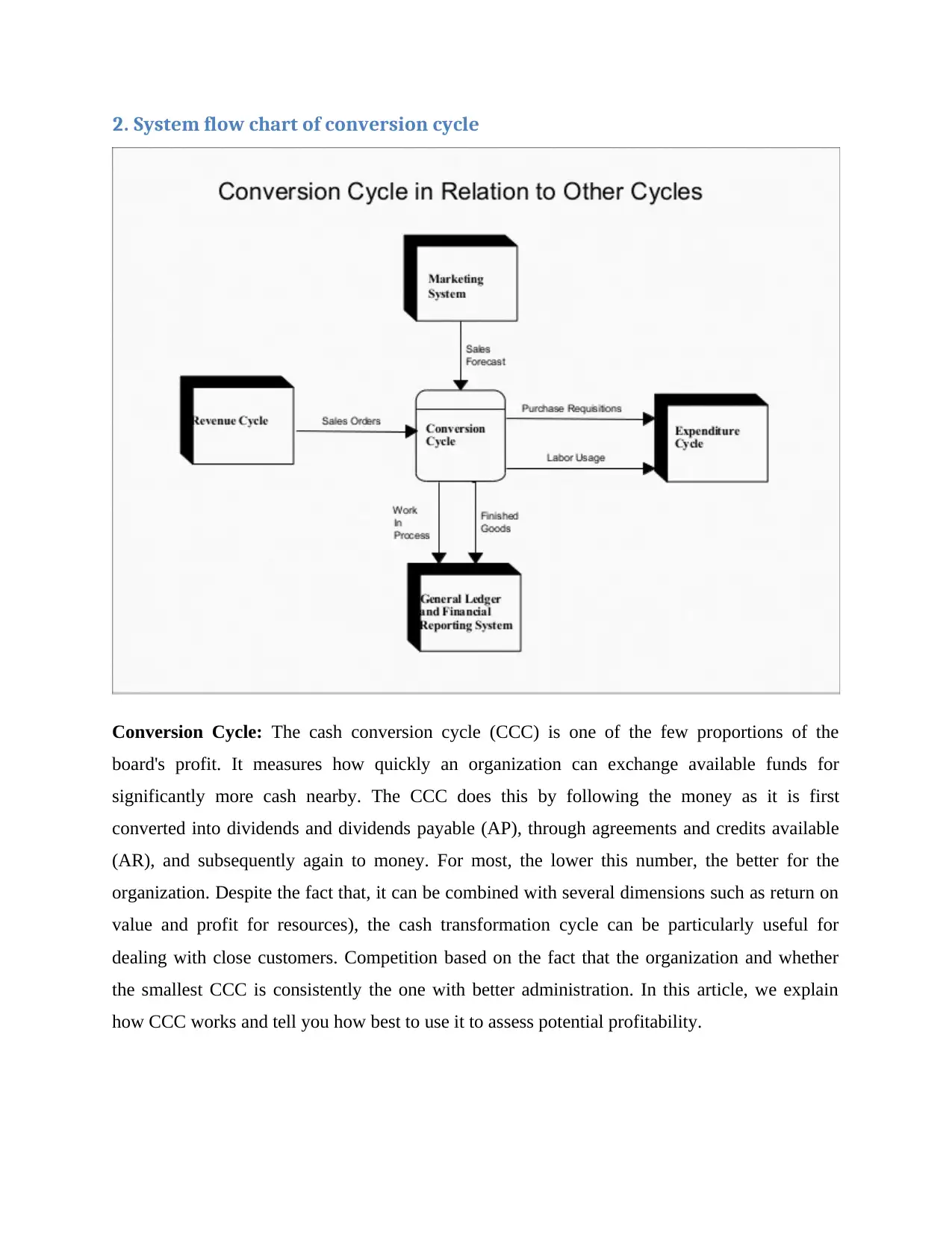

2. System flow chart of conversion cycle

Conversion Cycle: The cash conversion cycle (CCC) is one of the few proportions of the

board's profit. It measures how quickly an organization can exchange available funds for

significantly more cash nearby. The CCC does this by following the money as it is first

converted into dividends and dividends payable (AP), through agreements and credits available

(AR), and subsequently again to money. For most, the lower this number, the better for the

organization. Despite the fact that, it can be combined with several dimensions such as return on

value and profit for resources), the cash transformation cycle can be particularly useful for

dealing with close customers. Competition based on the fact that the organization and whether

the smallest CCC is consistently the one with better administration. In this article, we explain

how CCC works and tell you how best to use it to assess potential profitability.

Conversion Cycle: The cash conversion cycle (CCC) is one of the few proportions of the

board's profit. It measures how quickly an organization can exchange available funds for

significantly more cash nearby. The CCC does this by following the money as it is first

converted into dividends and dividends payable (AP), through agreements and credits available

(AR), and subsequently again to money. For most, the lower this number, the better for the

organization. Despite the fact that, it can be combined with several dimensions such as return on

value and profit for resources), the cash transformation cycle can be particularly useful for

dealing with close customers. Competition based on the fact that the organization and whether

the smallest CCC is consistently the one with better administration. In this article, we explain

how CCC works and tell you how best to use it to assess potential profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to

reduce the risks

An association freed from the threat of dissolution in the coming months is seen as a constant

concern. This standard attempts to squeeze the work into a company's ability to obtain credit

because banks understand that an association must continue its activities to obtain funds to pay

for its commitments. In this way, if a company is associated with remaining in business, the risk

of the association going into credit appreciation increases. It also creates the impression that it is

difficult for society to obtain major credit or credit. This risk is evident as part of the journey

through the global liquidity transformation cycle (Hoggett and et.al., 2006).

Types of risks involved in cash conversion cycle:

1. Delay in Payment: The real problem starts when longer customers pay and YOU increase

dramatically. Perhaps the most obvious formula in this situation is that the society is financing

the gap by getting from the banks. This is dangerous, given that the new task is not a piece of the

exercises or campaigns, but a consideration for the residents. Talking to office residents and

raising the AP DO may be a smart idea to manage the expansion in the DO DO. Unfortunately,

this show moves problems down the line. The result is a progression of cash-strapped societies

and working solely to pay their residents (Head and Herman, 2002).

2. Decline in Liquidity: A sensible assessment of the accumulation of liquidity is important

because reduced liquidity encourages the expansion of liquidity risk. Budget experts and experts

focus on the ability to share in cash and that sufficient funds are available to deal with ordinary

matters and retailers who aim to decide if they can generally buy the money to pay for the goods

given to a gentleman. Equally necessary for external evaluators for the tasks, for example by

analyzing the issues in question..

3. Void Invoices: An organization is reached by someone who is professional in talking to a

specialist supplier / cooperative / bank. Contact can be made by phone, letter, fax or email. The

fraudulent person approaches the fact that the bank subtleties for the allowance (for example the

subtleties of the beneficiary of the financial balance) are adjusted for the following applications.

The proposed new record is restricted by the scammer.

reduce the risks

An association freed from the threat of dissolution in the coming months is seen as a constant

concern. This standard attempts to squeeze the work into a company's ability to obtain credit

because banks understand that an association must continue its activities to obtain funds to pay

for its commitments. In this way, if a company is associated with remaining in business, the risk

of the association going into credit appreciation increases. It also creates the impression that it is

difficult for society to obtain major credit or credit. This risk is evident as part of the journey

through the global liquidity transformation cycle (Hoggett and et.al., 2006).

Types of risks involved in cash conversion cycle:

1. Delay in Payment: The real problem starts when longer customers pay and YOU increase

dramatically. Perhaps the most obvious formula in this situation is that the society is financing

the gap by getting from the banks. This is dangerous, given that the new task is not a piece of the

exercises or campaigns, but a consideration for the residents. Talking to office residents and

raising the AP DO may be a smart idea to manage the expansion in the DO DO. Unfortunately,

this show moves problems down the line. The result is a progression of cash-strapped societies

and working solely to pay their residents (Head and Herman, 2002).

2. Decline in Liquidity: A sensible assessment of the accumulation of liquidity is important

because reduced liquidity encourages the expansion of liquidity risk. Budget experts and experts

focus on the ability to share in cash and that sufficient funds are available to deal with ordinary

matters and retailers who aim to decide if they can generally buy the money to pay for the goods

given to a gentleman. Equally necessary for external evaluators for the tasks, for example by

analyzing the issues in question..

3. Void Invoices: An organization is reached by someone who is professional in talking to a

specialist supplier / cooperative / bank. Contact can be made by phone, letter, fax or email. The

fraudulent person approaches the fact that the bank subtleties for the allowance (for example the

subtleties of the beneficiary of the financial balance) are adjusted for the following applications.

The proposed new record is restricted by the scammer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Lack of inputs: For example, failure to reveal sources of information for example of authentic

products and categories for construction strategies.

5. Deficiency inventory: The problems introduced can lead to depressive equities, poor trading

indicators and habitual barrier power available for the purchase of disenchanted shares. For

example, a Structure brand offers a shoe model in 3 sizes. One month after the start of the period,

the shadow is rarely sold and must be limited in order to cancel the following operation.

6. Acutely sharpened: An article is generating more enthusiasm than expected and is

immediately out of stock. If the offer window is limited, it may discuss loss of payment

opportunities. For example, a famous toy on Christmas may disintegrate in January.

7. A worthy loss: Sitting continuously on an article, part or rack is material that can be found

inexpensively. The price may drop rapidly due to other serious sources of information or non-

quantitative transportation costs.

8. Natural hazards: Look for deficiencies that lead to incorrect stock inspection. For example,

an organization finds that a large amount of dollar business ends when it audits its year-end.

9. Channel index: Stocks sent to relocate offices talk about a strange kind of stock risk.

Subscribers sometimes have the ability to return non-return offers, expanding profits when

nothing sells. Sections that are deficient in a channel can damage future agreements in the same

way as subscribers stop applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The dangerous thing about flexible chains is that your jurisdiction includes direct actions for

suppliers, your union, and your customers. This is what is restricted by your suppliers,

customers, and status at all times (Laudon and Laudon, 2004).

1. Simplify the inventory:

One of the most powerful organizations for starters in the adaptive chain is probably the stock

size change with the aim of quickly reacting and limiting the amount of cash attached to the

products and categories for construction strategies.

5. Deficiency inventory: The problems introduced can lead to depressive equities, poor trading

indicators and habitual barrier power available for the purchase of disenchanted shares. For

example, a Structure brand offers a shoe model in 3 sizes. One month after the start of the period,

the shadow is rarely sold and must be limited in order to cancel the following operation.

6. Acutely sharpened: An article is generating more enthusiasm than expected and is

immediately out of stock. If the offer window is limited, it may discuss loss of payment

opportunities. For example, a famous toy on Christmas may disintegrate in January.

7. A worthy loss: Sitting continuously on an article, part or rack is material that can be found

inexpensively. The price may drop rapidly due to other serious sources of information or non-

quantitative transportation costs.

8. Natural hazards: Look for deficiencies that lead to incorrect stock inspection. For example,

an organization finds that a large amount of dollar business ends when it audits its year-end.

9. Channel index: Stocks sent to relocate offices talk about a strange kind of stock risk.

Subscribers sometimes have the ability to return non-return offers, expanding profits when

nothing sells. Sections that are deficient in a channel can damage future agreements in the same

way as subscribers stop applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The dangerous thing about flexible chains is that your jurisdiction includes direct actions for

suppliers, your union, and your customers. This is what is restricted by your suppliers,

customers, and status at all times (Laudon and Laudon, 2004).

1. Simplify the inventory:

One of the most powerful organizations for starters in the adaptive chain is probably the stock

size change with the aim of quickly reacting and limiting the amount of cash attached to the

fund. To stack from the warehouse and stock while accumulated enough to handle consumer

problems, start by experimenting with these methods from start to finish:

Multilateral idea reduced the article plan

Manage provider travel times

Selection of coordinate systems (eg JIT and VMI)

Remove people from the useless channel

Develop relaxed speculation and advocacy association.

2. Increase the buying cycle:

The appropriate (and certainly not) challenges facing the challenges can be major obstacles in the

time it takes for suppliers to pay. When trying to extend the opportunity to a large part of the

installments (to keep as much money as you would expect), the impact on the payment of the

compensation providers can be quite unexpected (McLeod and Schell, 2001).

However, the withdrawal, authoritative understanding and the more distant parts of the main

custodians can help you reorder the amount in your pocket. Determine the location in those areas

of the optical chain:

Screen lease dependencies to limit contributions faster than integrated terms

Distinction between reporting structures and receipts of the work process

Build a supplier base for real breakthroughs in bargaining

3. Advance Order to Money Circle:

The cost strategy is variable; it depends on time, reliability and accuracy. Finally, when the client

begins to prepare social treatment for leisure, many have begun the procedure to ensure proper

and precise treatment (Romney and Steinbart, 2006).

Restricting this pressure to the time of the assortment is difficult, while maintaining a high

degree of formation, rigid behavior over time and uninterrupted removal accuracy. Try to

separate your approach into these small categories to see where you might have the opportunity

to start shortening your time from asking for money:

Naturally add cost (speed and accuracy) resources.

problems, start by experimenting with these methods from start to finish:

Multilateral idea reduced the article plan

Manage provider travel times

Selection of coordinate systems (eg JIT and VMI)

Remove people from the useless channel

Develop relaxed speculation and advocacy association.

2. Increase the buying cycle:

The appropriate (and certainly not) challenges facing the challenges can be major obstacles in the

time it takes for suppliers to pay. When trying to extend the opportunity to a large part of the

installments (to keep as much money as you would expect), the impact on the payment of the

compensation providers can be quite unexpected (McLeod and Schell, 2001).

However, the withdrawal, authoritative understanding and the more distant parts of the main

custodians can help you reorder the amount in your pocket. Determine the location in those areas

of the optical chain:

Screen lease dependencies to limit contributions faster than integrated terms

Distinction between reporting structures and receipts of the work process

Build a supplier base for real breakthroughs in bargaining

3. Advance Order to Money Circle:

The cost strategy is variable; it depends on time, reliability and accuracy. Finally, when the client

begins to prepare social treatment for leisure, many have begun the procedure to ensure proper

and precise treatment (Romney and Steinbart, 2006).

Restricting this pressure to the time of the assortment is difficult, while maintaining a high

degree of formation, rigid behavior over time and uninterrupted removal accuracy. Try to

separate your approach into these small categories to see where you might have the opportunity

to start shortening your time from asking for money:

Naturally add cost (speed and accuracy) resources.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.