Report: Adam & Co Expenditure Cycle, Systems, and Risks Analysis

VerifiedAdded on 2022/10/19

|18

|3199

|2

Report

AI Summary

This report offers a detailed analysis of Adam & Co's expenditure cycle, which is managed through a centralized accounting system with multiple networking terminals. The report examines the expenditure cycle based on three key systems: purchase, payroll, and cash disbursement, which are integral to the overall process. The analysis is supported by data flow diagrams (DFDs) and flowchart diagrams to illustrate the operational processes within Adam & Co. Moreover, the report critically assesses the potential risks and weaknesses inherent in each of the three systems. The purchase system is examined in detail, including procedures for placing orders, receiving inventory, and recognizing inventory needs. The cash disbursement system and payroll system are also thoroughly analyzed, highlighting their respective processes and data flows. The flowchart diagrams provide a visual representation of each system, enabling a clearer understanding of the processes involved. Furthermore, the report identifies and evaluates internal control weaknesses and potential risks within the purchase, payroll, and cash disbursement systems. The report concludes with a summary of the key findings and recommendations for improving the efficiency and security of the expenditure cycle.

Adam & Co Company 1

Adam & Co Company

Name

Professor

College

Course

Date

Adam & Co Company

Name

Professor

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adam & Co Company 2

Executive Summary

The discussion in this report seeks to understand the expenditure cycle of Adam & Co

which has a centralized system of accounting with manifold networking terminal in diverse

destinations. Thus a deeper examination of this cycle process is undertaken based on three

system including purchase, payroll and cash disbursement which make up expenditure cycle.

This discussion is supported by data flow diagram, and flowchart diagram to help understand

the systems in Adam & Co. This discussion also involves the examination of the potential

risks and weakness of all the three systems.

Executive Summary

The discussion in this report seeks to understand the expenditure cycle of Adam & Co

which has a centralized system of accounting with manifold networking terminal in diverse

destinations. Thus a deeper examination of this cycle process is undertaken based on three

system including purchase, payroll and cash disbursement which make up expenditure cycle.

This discussion is supported by data flow diagram, and flowchart diagram to help understand

the systems in Adam & Co. This discussion also involves the examination of the potential

risks and weakness of all the three systems.

Adam & Co Company 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

DFD Cash Disbursements (CDS) & Purchases Systems (PS)...................................................5

Purchase System.....................................................................................................................5

Fig1: DFD Purchase System..............................................................................................5

CDS........................................................................................................................................9

Fig 2: DFD Cash Disbursements Systems.........................................................................9

Payroll System DFD............................................................................................................10

Fig3: Payroll System DFD...............................................................................................10

Purchases System Flowchart................................................................................................11

CDS System Flowchart........................................................................................................13

Payroll System: System Flowchart......................................................................................14

System Internal Control Weaknesses and Risks......................................................................15

Payroll Systems....................................................................................................................15

Purchases System.................................................................................................................15

CDS......................................................................................................................................15

Conclusion................................................................................................................................16

Bibliography.............................................................................................................................17

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

DFD Cash Disbursements (CDS) & Purchases Systems (PS)...................................................5

Purchase System.....................................................................................................................5

Fig1: DFD Purchase System..............................................................................................5

CDS........................................................................................................................................9

Fig 2: DFD Cash Disbursements Systems.........................................................................9

Payroll System DFD............................................................................................................10

Fig3: Payroll System DFD...............................................................................................10

Purchases System Flowchart................................................................................................11

CDS System Flowchart........................................................................................................13

Payroll System: System Flowchart......................................................................................14

System Internal Control Weaknesses and Risks......................................................................15

Payroll Systems....................................................................................................................15

Purchases System.................................................................................................................15

CDS......................................................................................................................................15

Conclusion................................................................................................................................16

Bibliography.............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Adam & Co Company 4

Introduction

The main aim of this report is to examine the expenditure cycle of Adam & Co which

uses a centralized system of accounting with multiple networking terminal in diverse

locations. Therefore a comprehensive investigation into this expenditure cycle process is

carried out premised on three system which include purchase, payroll and cash disbursement

which make up expenditure cycle. The analysis is backed by data flow diagram, and

flowchart diagram to assist in understanding the systems in Adam & Co. This examination

further encompasses the probe of the weakness and potential risks in all the three systems.

Introduction

The main aim of this report is to examine the expenditure cycle of Adam & Co which

uses a centralized system of accounting with multiple networking terminal in diverse

locations. Therefore a comprehensive investigation into this expenditure cycle process is

carried out premised on three system which include purchase, payroll and cash disbursement

which make up expenditure cycle. The analysis is backed by data flow diagram, and

flowchart diagram to assist in understanding the systems in Adam & Co. This examination

further encompasses the probe of the weakness and potential risks in all the three systems.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adam & Co Company 5

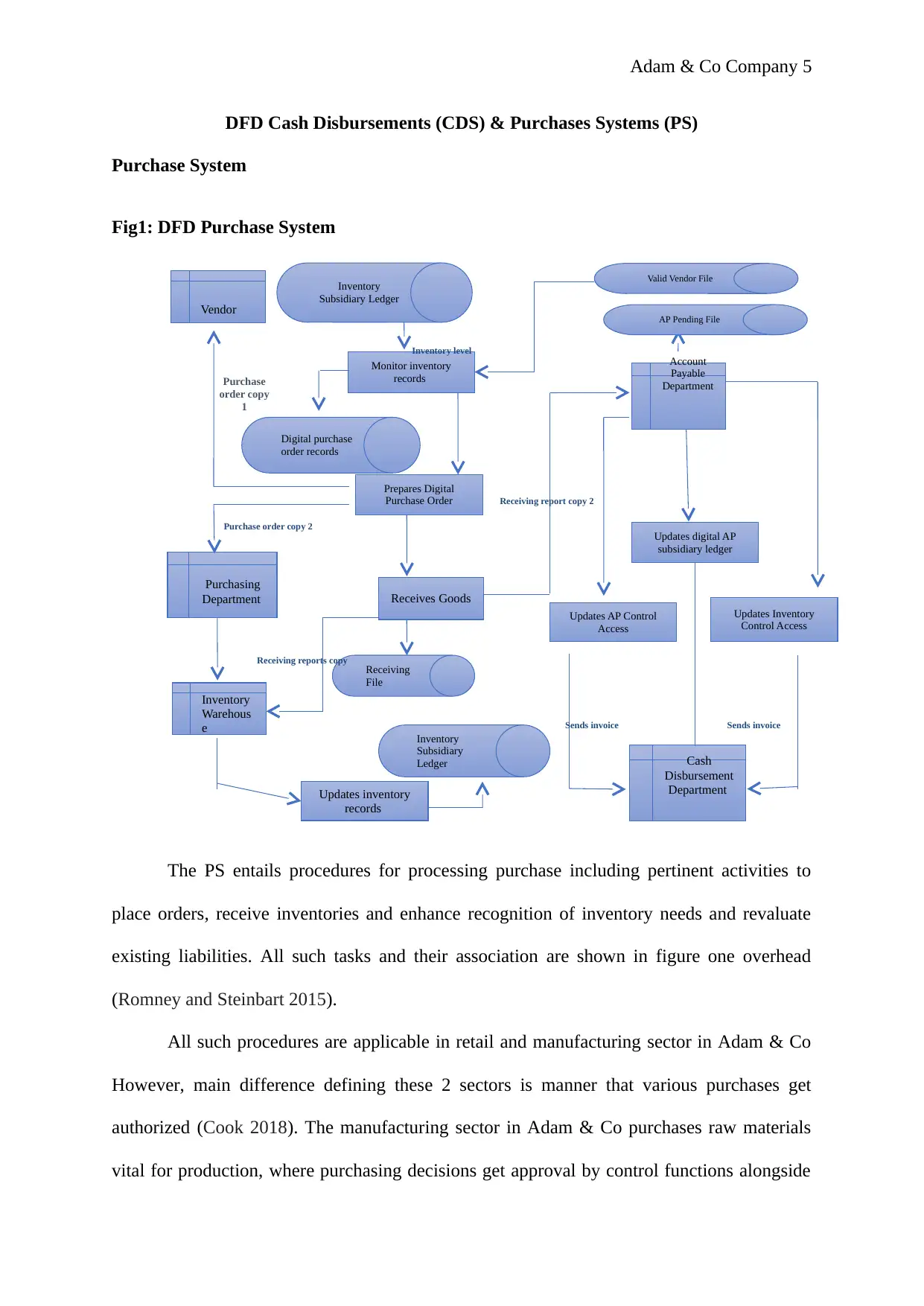

DFD Cash Disbursements (CDS) & Purchases Systems (PS)

Purchase System

Fig1: DFD Purchase System

The PS entails procedures for processing purchase including pertinent activities to

place orders, receive inventories and enhance recognition of inventory needs and revaluate

existing liabilities. All such tasks and their association are shown in figure one overhead

(Romney and Steinbart 2015).

All such procedures are applicable in retail and manufacturing sector in Adam & Co

However, main difference defining these 2 sectors is manner that various purchases get

authorized (Cook 2018). The manufacturing sector in Adam & Co purchases raw materials

vital for production, where purchasing decisions get approval by control functions alongside

Purchasing

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory

Subsidiary

Ledger

Receiving

File

Digital purchase

order records

Purchase

order copy

1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice Sends invoice

Inventory level

Inventory

Subsidiary Ledger

DFD Cash Disbursements (CDS) & Purchases Systems (PS)

Purchase System

Fig1: DFD Purchase System

The PS entails procedures for processing purchase including pertinent activities to

place orders, receive inventories and enhance recognition of inventory needs and revaluate

existing liabilities. All such tasks and their association are shown in figure one overhead

(Romney and Steinbart 2015).

All such procedures are applicable in retail and manufacturing sector in Adam & Co

However, main difference defining these 2 sectors is manner that various purchases get

authorized (Cook 2018). The manufacturing sector in Adam & Co purchases raw materials

vital for production, where purchasing decisions get approval by control functions alongside

Purchasing

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory

Subsidiary

Ledger

Receiving

File

Digital purchase

order records

Purchase

order copy

1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice Sends invoice

Inventory level

Inventory

Subsidiary Ledger

Adam & Co Company 6

production planning. The retailing sector in Adam & Co purchases finished goods for

reselling and function for inventories control provides purchasing approval (Thite and

Sandhu 2014).

The process of inventories records monitoring is facilitated whenever Adam & Co

exhausts is stock by transferring materials in production stage. Such procedure is conversion

cycle while reselling finished goods to consumers is called revenue cycle. The inventory

controls monitors and records the finished products alongside its inventory levels. With a

plunge in the stock levels and predetermining point for reordering, a need ensues for the

purchasing clerk to prepare function for purchase order that shall initiate purchasing process.

Afterwards, purchase requisition is fundable and varies in different organizations.

Typically, the company will facilitate and prepare a discrete purchase requisition for various

inventory items where need be (Fauzi and Setyawan, 2018). Resultantly, multiple purchasing

requisitions may be evidently for an available vendor and these requisitions need to be

combined into one purchasing order then sent to a vendor. Such a system type allows every

PO to get linked to many purchase requisitions.

The preparation of the purchase order function obtains the purchasing requisitions,

organized by the vendor whenever needed. Afterwards, the Purchase Order (PO) copy is

designed for the respective vendors as indicated in the Data Flow Diagram (DFD) in Fig 1.

Additionally, another copy is transferred to the purchasing department for a set-up of the

Account Payable (AP) functions meant for temporary filing of the AP pending files.

Consequently a blind copies of a file is sent by clerk to Receiving Goods functions

(Yuliyanto 2018).

Many companies experience a time lag between receiving goods and placing an order.

During this stage, various PO copies will be included in the temporary files in the account

payable department, and no economic aspect is executed. At this juncture, the Adam & Co

production planning. The retailing sector in Adam & Co purchases finished goods for

reselling and function for inventories control provides purchasing approval (Thite and

Sandhu 2014).

The process of inventories records monitoring is facilitated whenever Adam & Co

exhausts is stock by transferring materials in production stage. Such procedure is conversion

cycle while reselling finished goods to consumers is called revenue cycle. The inventory

controls monitors and records the finished products alongside its inventory levels. With a

plunge in the stock levels and predetermining point for reordering, a need ensues for the

purchasing clerk to prepare function for purchase order that shall initiate purchasing process.

Afterwards, purchase requisition is fundable and varies in different organizations.

Typically, the company will facilitate and prepare a discrete purchase requisition for various

inventory items where need be (Fauzi and Setyawan, 2018). Resultantly, multiple purchasing

requisitions may be evidently for an available vendor and these requisitions need to be

combined into one purchasing order then sent to a vendor. Such a system type allows every

PO to get linked to many purchase requisitions.

The preparation of the purchase order function obtains the purchasing requisitions,

organized by the vendor whenever needed. Afterwards, the Purchase Order (PO) copy is

designed for the respective vendors as indicated in the Data Flow Diagram (DFD) in Fig 1.

Additionally, another copy is transferred to the purchasing department for a set-up of the

Account Payable (AP) functions meant for temporary filing of the AP pending files.

Consequently a blind copies of a file is sent by clerk to Receiving Goods functions

(Yuliyanto 2018).

Many companies experience a time lag between receiving goods and placing an order.

During this stage, various PO copies will be included in the temporary files in the account

payable department, and no economic aspect is executed. At this juncture, the Adam & Co

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Adam & Co Company 7

organization has never received stock or incurred financial obligations. Thus, there is no need

of facilitating the making of formal entries in the accounting records (Fedaghi, 2014).

Nonetheless, the company may decide the make a memo entry while referring to the pendant

stock-related receipts besides obligation (Jarrah 2018).

The next step comprise the receipt stock where goods arrive as the receiving report

gets prepared. These goods are then reconciled with the packing slip and DPO. Copies of the

document include the data on quantity and prices of the items received. The foremost aim of

these documents is to permit receiving clerk to inspect and count inventories before drafting

the receiving report. Mostly, the receiving department is busy and their staff as subjected to

pressure of unloading the delivery vehicles or signing lading bills (Gautam, 2010). In such

cases, the receiving clerk will only be provided with the relevant data on item quantity and

accept a delivery of products in reference to the provided data.

In the cycle, the next stage in the provision of update regarding the inventory record.

Relative to the inventories valuation technique, the inventories controls technique varies in

different organizations. A company that utilizes a standardized cost framework may execute

their inventory at a predetermined standardized figure irrespective of the charges being paid

to a given vendor (Bhoite, 2012). Presenting a standardized inventories ledger necessitates

the relevant data regarding the quantity attained. Since the receiving reports contain the item

quantity data, this file serves this purpose. Thus, updating the main cost inventory ledger

necessitates more financial data from the inventory warehouse. During the process of this

transaction, accounts payable needs a set-up. The AP function receives this setting the

temporary files of the receiving report and PO is filed. The Adam & Co organization has

received these stock from respective vendors and realized respective obligation for received

goods’ payment.

organization has never received stock or incurred financial obligations. Thus, there is no need

of facilitating the making of formal entries in the accounting records (Fedaghi, 2014).

Nonetheless, the company may decide the make a memo entry while referring to the pendant

stock-related receipts besides obligation (Jarrah 2018).

The next step comprise the receipt stock where goods arrive as the receiving report

gets prepared. These goods are then reconciled with the packing slip and DPO. Copies of the

document include the data on quantity and prices of the items received. The foremost aim of

these documents is to permit receiving clerk to inspect and count inventories before drafting

the receiving report. Mostly, the receiving department is busy and their staff as subjected to

pressure of unloading the delivery vehicles or signing lading bills (Gautam, 2010). In such

cases, the receiving clerk will only be provided with the relevant data on item quantity and

accept a delivery of products in reference to the provided data.

In the cycle, the next stage in the provision of update regarding the inventory record.

Relative to the inventories valuation technique, the inventories controls technique varies in

different organizations. A company that utilizes a standardized cost framework may execute

their inventory at a predetermined standardized figure irrespective of the charges being paid

to a given vendor (Bhoite, 2012). Presenting a standardized inventories ledger necessitates

the relevant data regarding the quantity attained. Since the receiving reports contain the item

quantity data, this file serves this purpose. Thus, updating the main cost inventory ledger

necessitates more financial data from the inventory warehouse. During the process of this

transaction, accounts payable needs a set-up. The AP function receives this setting the

temporary files of the receiving report and PO is filed. The Adam & Co organization has

received these stock from respective vendors and realized respective obligation for received

goods’ payment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adam & Co Company 8

In completing this process, the AP clerk must evaluate the exact obligation valuation

till the point the invoice gets received. Whenever an estimate is materially improper, an

adjustment of the entry needs to be undertaken to rectify the mistakes. Because received

invoice receipt activates AP techniques alongside processes, clerks must evaluate unrecorded

liabilities when closing. Upon the arrival of the inventories, the AP clerks reconcile the

relevant financial data with purchasing order and receiving report in available awaiting file.

Such is called trio-way matching which verifies quantity obtained and respective prices.

During this moment, the clerk progressively updates the DPO subsidiary ledger, AP controls

account alongside stock controls account in GL. Lastly, an invoice, PO and receiving report

are then transferred (Hall 2015).

In completing this process, the AP clerk must evaluate the exact obligation valuation

till the point the invoice gets received. Whenever an estimate is materially improper, an

adjustment of the entry needs to be undertaken to rectify the mistakes. Because received

invoice receipt activates AP techniques alongside processes, clerks must evaluate unrecorded

liabilities when closing. Upon the arrival of the inventories, the AP clerks reconcile the

relevant financial data with purchasing order and receiving report in available awaiting file.

Such is called trio-way matching which verifies quantity obtained and respective prices.

During this moment, the clerk progressively updates the DPO subsidiary ledger, AP controls

account alongside stock controls account in GL. Lastly, an invoice, PO and receiving report

are then transferred (Hall 2015).

Adam & Co Company 9

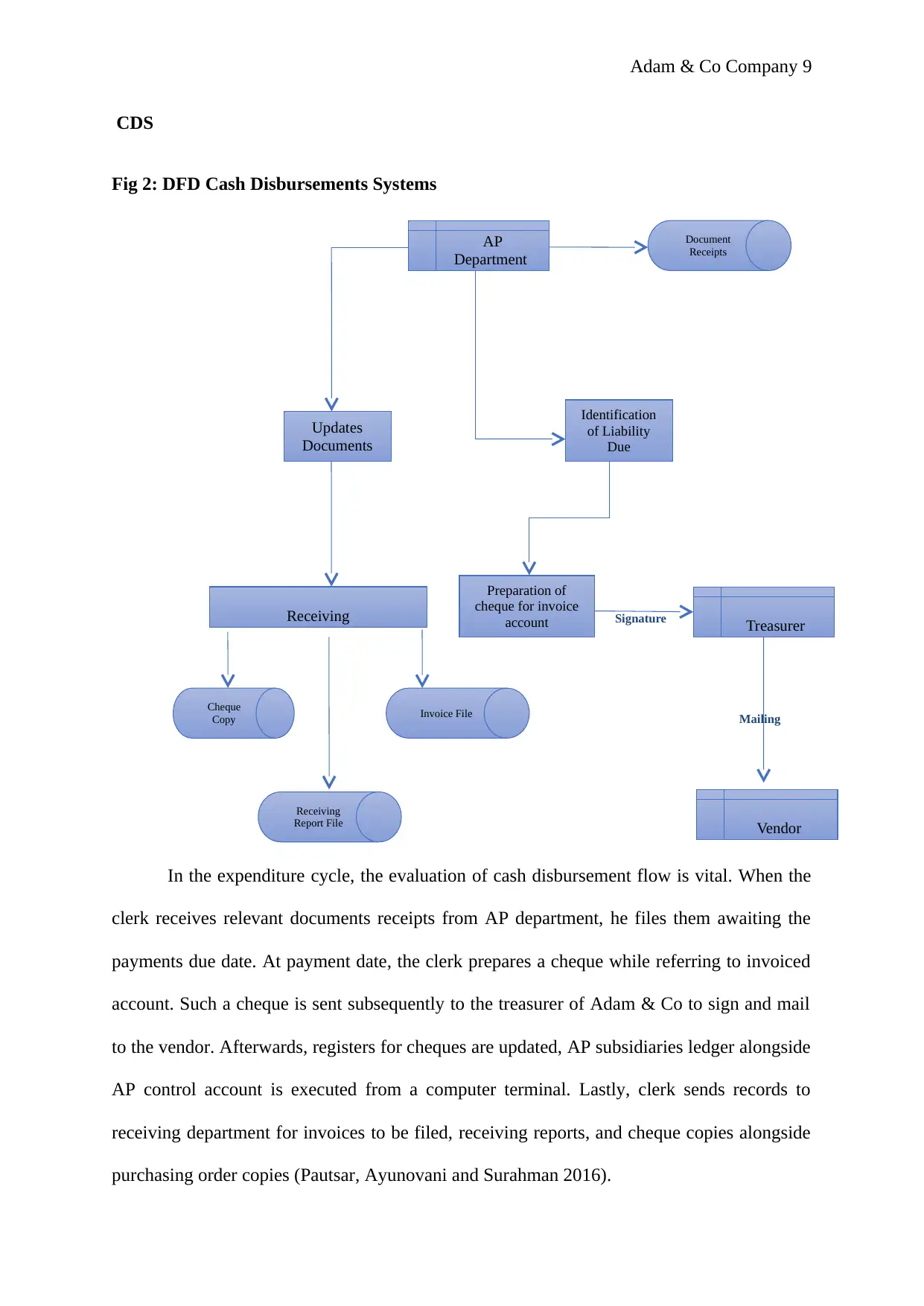

CDS

Fig 2: DFD Cash Disbursements Systems

In the expenditure cycle, the evaluation of cash disbursement flow is vital. When the

clerk receives relevant documents receipts from AP department, he files them awaiting the

payments due date. At payment date, the clerk prepares a cheque while referring to invoiced

account. Such a cheque is sent subsequently to the treasurer of Adam & Co to sign and mail

to the vendor. Afterwards, registers for cheques are updated, AP subsidiaries ledger alongside

AP control account is executed from a computer terminal. Lastly, clerk sends records to

receiving department for invoices to be filed, receiving reports, and cheque copies alongside

purchasing order copies (Pautsar, Ayunovani and Surahman 2016).

AP

Department

Updates

Documents

Document

Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving

Report File

Invoice File

Cheque

Copy

CDS

Fig 2: DFD Cash Disbursements Systems

In the expenditure cycle, the evaluation of cash disbursement flow is vital. When the

clerk receives relevant documents receipts from AP department, he files them awaiting the

payments due date. At payment date, the clerk prepares a cheque while referring to invoiced

account. Such a cheque is sent subsequently to the treasurer of Adam & Co to sign and mail

to the vendor. Afterwards, registers for cheques are updated, AP subsidiaries ledger alongside

AP control account is executed from a computer terminal. Lastly, clerk sends records to

receiving department for invoices to be filed, receiving reports, and cheque copies alongside

purchasing order copies (Pautsar, Ayunovani and Surahman 2016).

AP

Department

Updates

Documents

Document

Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving

Report File

Invoice File

Cheque

Copy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Adam & Co Company 10

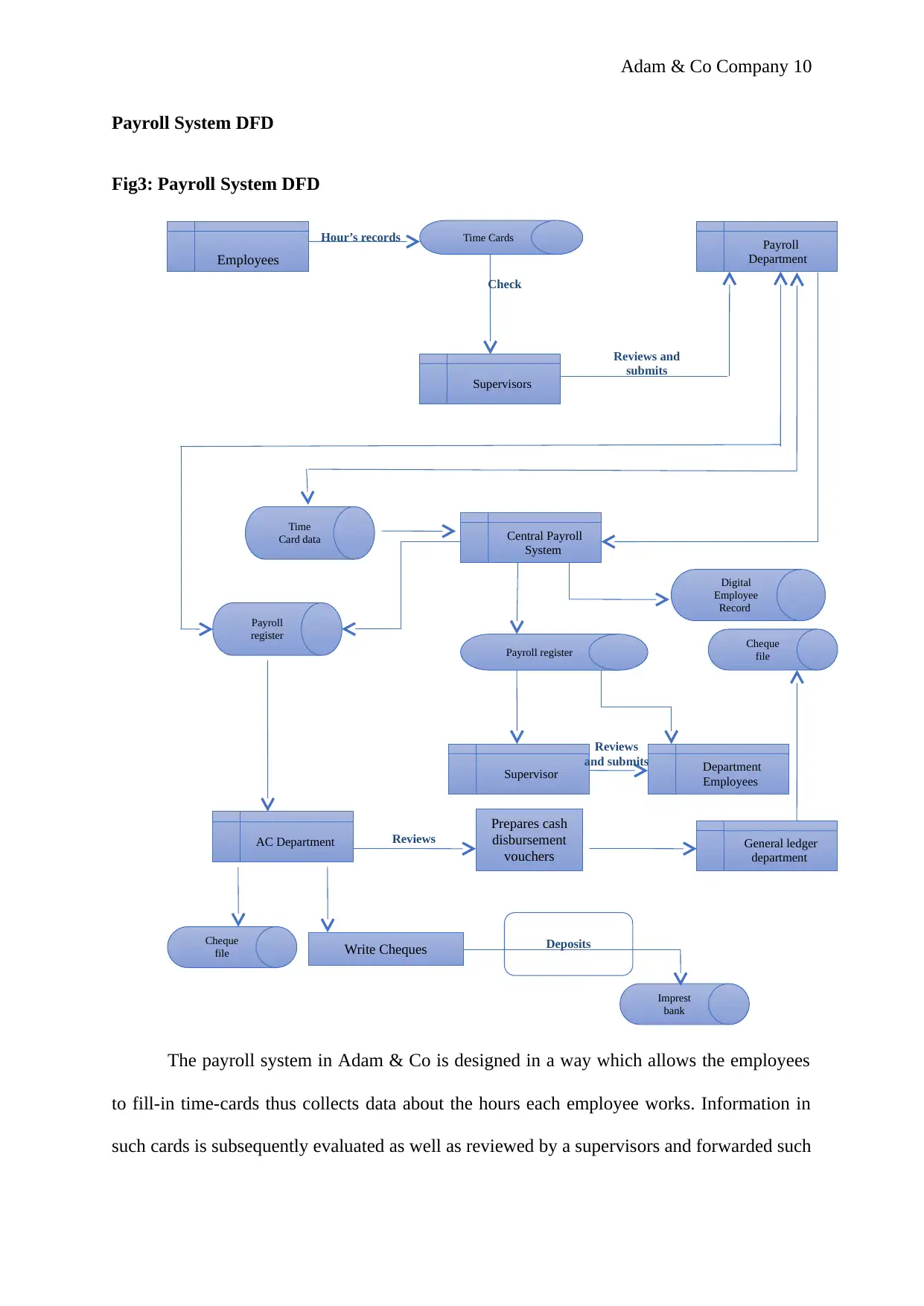

Payroll System DFD

Fig3: Payroll System DFD

The payroll system in Adam & Co is designed in a way which allows the employees

to fill-in time-cards thus collects data about the hours each employee works. Information in

such cards is subsequently evaluated as well as reviewed by a supervisors and forwarded such

Prepares cash

disbursement

vouchers

Payroll

DepartmentEmployees

Time Cards

Supervisors

Central Payroll

System

Time

Card data

Payroll

register

Payroll register

Supervisor

AC Department

Write Cheques

Cheque

file

Imprest

bank

General ledger

department

Cheque

file

Department

Employees

Reviews and

submits

Hour’s records

Digital

Employee

Record

Reviews

and submits

Deposits

Reviews

Check

Payroll System DFD

Fig3: Payroll System DFD

The payroll system in Adam & Co is designed in a way which allows the employees

to fill-in time-cards thus collects data about the hours each employee works. Information in

such cards is subsequently evaluated as well as reviewed by a supervisors and forwarded such

Prepares cash

disbursement

vouchers

Payroll

DepartmentEmployees

Time Cards

Supervisors

Central Payroll

System

Time

Card data

Payroll

register

Payroll register

Supervisor

AC Department

Write Cheques

Cheque

file

Imprest

bank

General ledger

department

Cheque

file

Department

Employees

Reviews and

submits

Hour’s records

Digital

Employee

Record

Reviews

and submits

Deposits

Reviews

Check

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adam & Co Company 11

data to payroll department (Janvrin and Watson 2017). Payroll system gets referenced from

Adam & Co central PS which is located in data processes department whereby a clerk inputs

data as well as print paycheque copies, payroll registers copies and copies of records of

digital employees. The clerk, from the payroll department, possibly files time-cards and

transfer the employees’ payment cheques to a supervisor to distribute as well as review.

Afterwards, the clerk sends a payroll register copy to AP department while another copy

containing time-cards is sent to department for payroll (Lopez et al. 2017).

AP clerks then appraises register then makes the CD voucher manually. Afterwards, a

clerk then passes on a payroll register alongside voucher to the GL department and AP clerk

draws a cheque for payroll to be deposited in the bank’s imprest account.

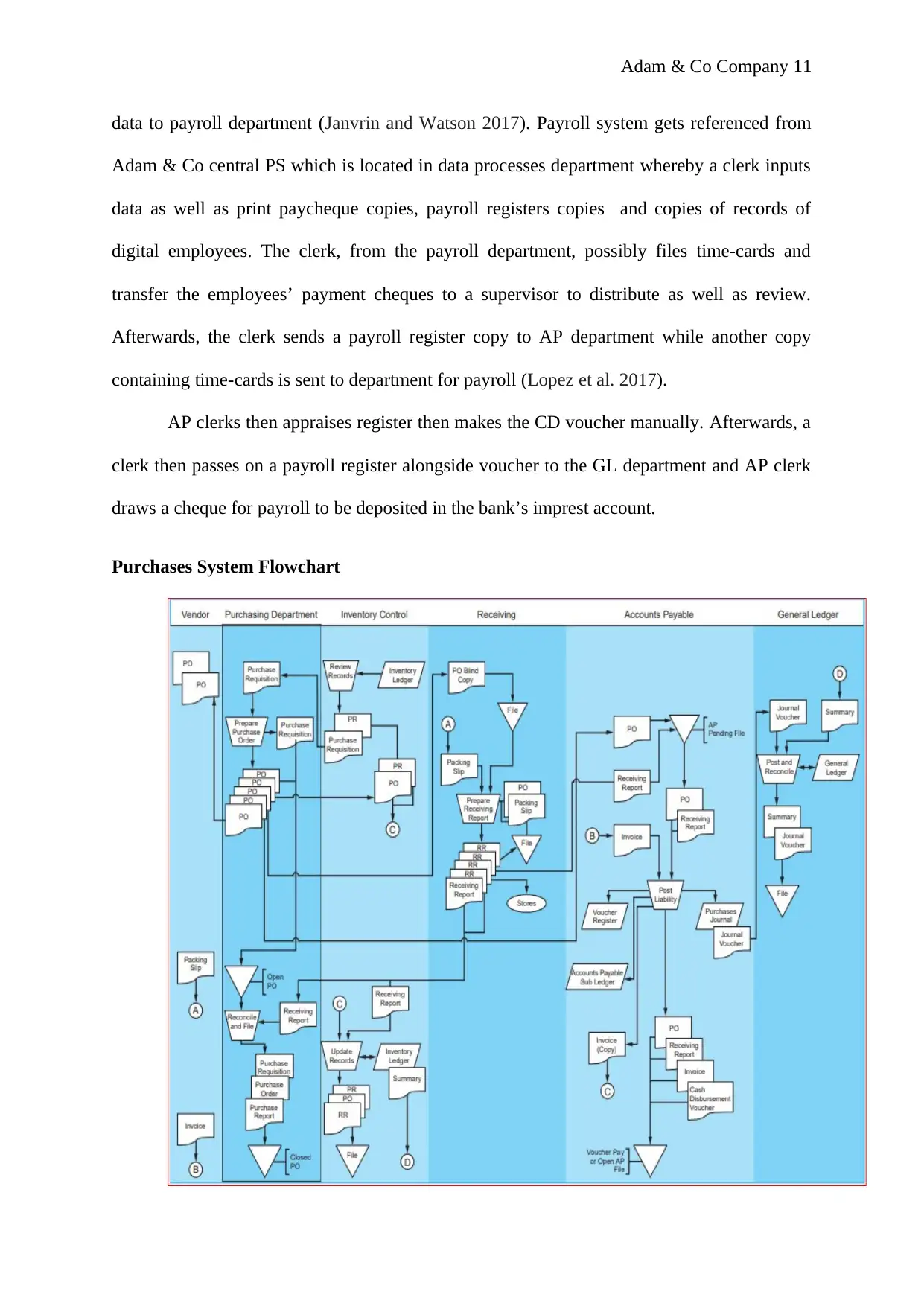

Purchases System Flowchart

data to payroll department (Janvrin and Watson 2017). Payroll system gets referenced from

Adam & Co central PS which is located in data processes department whereby a clerk inputs

data as well as print paycheque copies, payroll registers copies and copies of records of

digital employees. The clerk, from the payroll department, possibly files time-cards and

transfer the employees’ payment cheques to a supervisor to distribute as well as review.

Afterwards, the clerk sends a payroll register copy to AP department while another copy

containing time-cards is sent to department for payroll (Lopez et al. 2017).

AP clerks then appraises register then makes the CD voucher manually. Afterwards, a

clerk then passes on a payroll register alongside voucher to the GL department and AP clerk

draws a cheque for payroll to be deposited in the bank’s imprest account.

Purchases System Flowchart

Adam & Co Company 12

The flowchart of a system comprises inventory control where inventory level remains

monitored. During a plunge in predetermined point of reordering, a clerk will draft a

purchasing requisition where a copy gets transferred to department for purchase while

another to available purchase requisition file. It should be noted that the provision of the

authorization controls in stock controls department is separated from department for purchase

which executing transactions.

This process follows the purchase requisition, sorting by vendors and preparation of

the PO for every vendor in the purchasing department. Here, 2 copies of the PO are

transferred to vendor and PO copy is transferred to inventory control to be filed alongside

available purchasing requisition. The goods which originate from vendors are reconciled with

blind copies of PO. At the completion of physical counting alongside inspection procedure,

receiving clerk then prepares different reports which state status alongside quantity of stock.

A copy of the receiving reports is passed on to inventory department alongside physical

inventory. Remaining copy is transferred to department for purchases and a clerk can then

reconcile it with PO available.

In AP department, the clerk receives inward invoice where information is reconciled

with available awaiting doc file. Thereafter, relevant transactions record in journal purchases

is executed alongside points, along with AP subsidiary ledger being prepared. It follows a

liabilities records, where a clerk sends source documents, receiving reports alongside

available files for voucher payable. During this point, DAP subsidiaries ledgers update takes

place, and it include AP controls account alongside the stock control accounts in GL

department from computer terminal. Lastly, the clerk transfers the invoices, PO copies and

receiving reports to the cash disbursement department.

The flowchart of a system comprises inventory control where inventory level remains

monitored. During a plunge in predetermined point of reordering, a clerk will draft a

purchasing requisition where a copy gets transferred to department for purchase while

another to available purchase requisition file. It should be noted that the provision of the

authorization controls in stock controls department is separated from department for purchase

which executing transactions.

This process follows the purchase requisition, sorting by vendors and preparation of

the PO for every vendor in the purchasing department. Here, 2 copies of the PO are

transferred to vendor and PO copy is transferred to inventory control to be filed alongside

available purchasing requisition. The goods which originate from vendors are reconciled with

blind copies of PO. At the completion of physical counting alongside inspection procedure,

receiving clerk then prepares different reports which state status alongside quantity of stock.

A copy of the receiving reports is passed on to inventory department alongside physical

inventory. Remaining copy is transferred to department for purchases and a clerk can then

reconcile it with PO available.

In AP department, the clerk receives inward invoice where information is reconciled

with available awaiting doc file. Thereafter, relevant transactions record in journal purchases

is executed alongside points, along with AP subsidiary ledger being prepared. It follows a

liabilities records, where a clerk sends source documents, receiving reports alongside

available files for voucher payable. During this point, DAP subsidiaries ledgers update takes

place, and it include AP controls account alongside the stock control accounts in GL

department from computer terminal. Lastly, the clerk transfers the invoices, PO copies and

receiving reports to the cash disbursement department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.