Analyzing External Auditor Reliance on Internal Auditing Factors

VerifiedAdded on 2020/05/16

|49

|11052

|80

Report

AI Summary

This report examines the critical relationship between external and internal auditing, focusing on the reliance of external auditors on internal audit functions within Jordan. The study investigates the influence of three key factors: performance, competency, and objectivity, using descriptive statistics, correlation analysis, reliability analysis, and regression/ANOVA tables to analyze the data. The findings reveal strong positive correlations between internal auditor performance and external auditor factors such as nature, timing, and extent of work, suggesting a significant level of reliance. Specifically, the objectivity of internal auditors plays a crucial role in shaping the nature, timing, and scope of external audits. The report concludes with implications for practice and recommendations for enhancing the effectiveness of audit processes. This report provides a comprehensive analysis of the interplay between internal and external auditing in Jordan, highlighting the importance of internal audit functions in supporting and influencing the work of external auditors, and providing a valuable resource for students and professionals in the field of finance.

Running head: RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Name of the Student

Name of the University

Author Note

RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Table of Contents

CHAPTER FOUR: RESULTS........................................................................................................2

Purpose of the study.....................................................................................................................2

Interpretation of the Descriptive Statistics Table........................................................................2

Interpretation of the Correlations Tables.....................................................................................4

Interpretation of the Reliability Analysis Tables.........................................................................5

Interpretation of the Regression and ANOVA Table..................................................................8

Summary....................................................................................................................................12

CHAPTER FIVE: DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS................13

Discussion..................................................................................................................................13

Conclusion.................................................................................................................................15

Implications for practice............................................................................................................17

Recommendations......................................................................................................................17

References......................................................................................................................................18

Appendices....................................................................................................................................23

Table of Contents

CHAPTER FOUR: RESULTS........................................................................................................2

Purpose of the study.....................................................................................................................2

Interpretation of the Descriptive Statistics Table........................................................................2

Interpretation of the Correlations Tables.....................................................................................4

Interpretation of the Reliability Analysis Tables.........................................................................5

Interpretation of the Regression and ANOVA Table..................................................................8

Summary....................................................................................................................................12

CHAPTER FIVE: DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS................13

Discussion..................................................................................................................................13

Conclusion.................................................................................................................................15

Implications for practice............................................................................................................17

Recommendations......................................................................................................................17

References......................................................................................................................................18

Appendices....................................................................................................................................23

2RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

CHAPTER FOUR: RESULTS

Purpose of the study

Purpose of the study was to explore and comprehend the influence of reliance by external

auditors on internal audits in Jordan. Three major factors were considered while conducting the

research, viz. Performance, Competency and Objectivity (Mekler et al. 2017). In-depth analysis

regarding the connection between the external and internal audit sectors within Jordan.

Hypotheses were constructed in relevance to determining the effect of the aforementioned three

factors. Reliability analysis has also been carried out to find the internal consistency between the

responses.

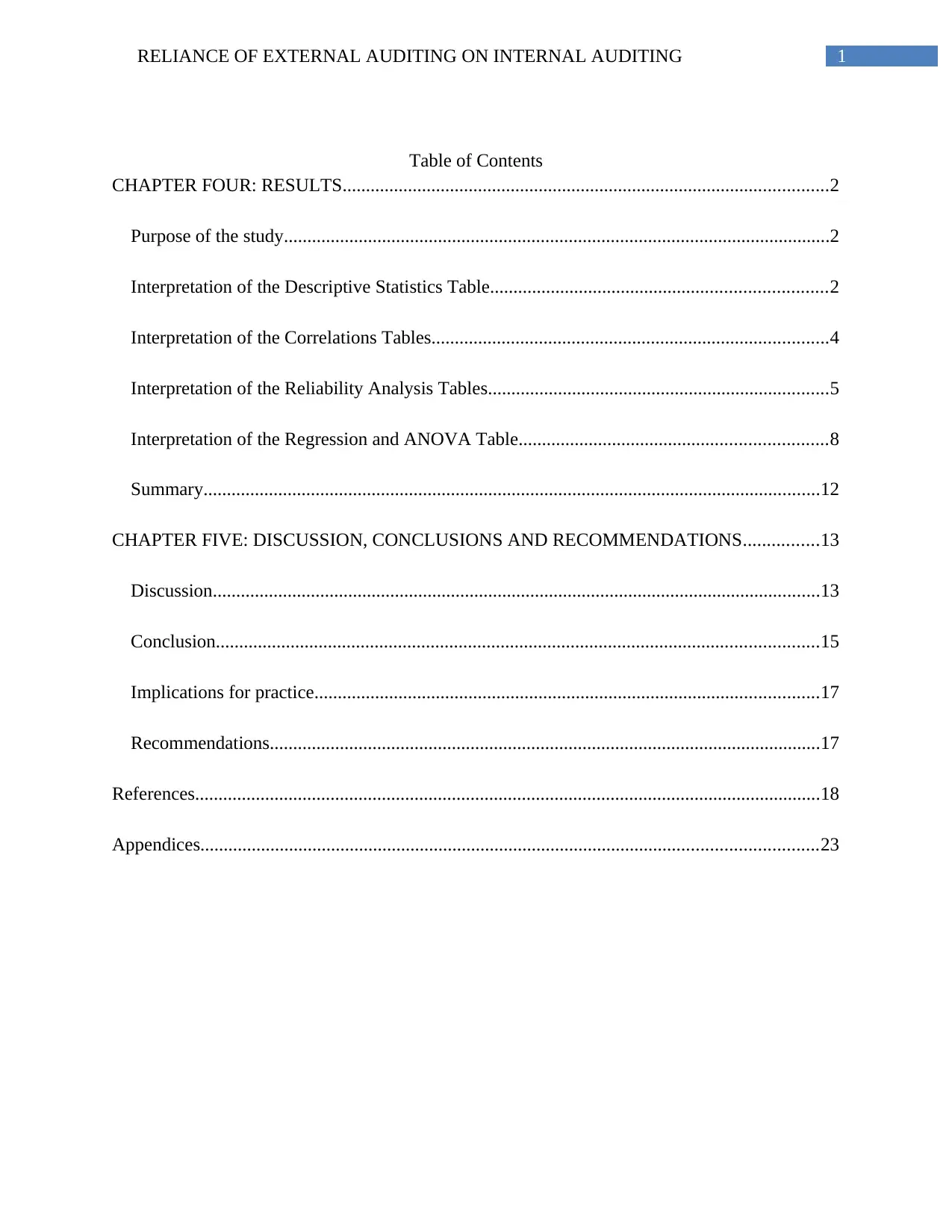

Interpretation of the Descriptive Statistics Table

The descriptive table is presented below, that provides the Minimum, Maximum,

Arithmetic mean and the Standard Deviation (Revelle 2017).

N Minimum Maximum Mean Std. Deviation

a1 200 1 5 3.60 1.129

a2 200 1 5 3.74 .978

a3 200 1 5 3.74 1.103

a4 200 1 5 3.83 1.096

a5 200 1 5 3.93 1.015

a6 200 1 5 3.73 1.016

a7 200 1 5 3.70 1.048

a8 200 1 5 3.80 .935

a9 200 1 5 3.82 .966

a10 200 1 5 3.82 .998

a11 200 1 5 3.76 1.014

a12 200 1 5 3.83 .829

a13 200 1 5 3.79 .950

a14 200 1 5 3.86 .895

a15 200 1 5 3.79 .894

a16 200 1 5 3.76 .936

a17 200 1 5 3.79 .931

a18 200 1 5 3.78 .925

CHAPTER FOUR: RESULTS

Purpose of the study

Purpose of the study was to explore and comprehend the influence of reliance by external

auditors on internal audits in Jordan. Three major factors were considered while conducting the

research, viz. Performance, Competency and Objectivity (Mekler et al. 2017). In-depth analysis

regarding the connection between the external and internal audit sectors within Jordan.

Hypotheses were constructed in relevance to determining the effect of the aforementioned three

factors. Reliability analysis has also been carried out to find the internal consistency between the

responses.

Interpretation of the Descriptive Statistics Table

The descriptive table is presented below, that provides the Minimum, Maximum,

Arithmetic mean and the Standard Deviation (Revelle 2017).

N Minimum Maximum Mean Std. Deviation

a1 200 1 5 3.60 1.129

a2 200 1 5 3.74 .978

a3 200 1 5 3.74 1.103

a4 200 1 5 3.83 1.096

a5 200 1 5 3.93 1.015

a6 200 1 5 3.73 1.016

a7 200 1 5 3.70 1.048

a8 200 1 5 3.80 .935

a9 200 1 5 3.82 .966

a10 200 1 5 3.82 .998

a11 200 1 5 3.76 1.014

a12 200 1 5 3.83 .829

a13 200 1 5 3.79 .950

a14 200 1 5 3.86 .895

a15 200 1 5 3.79 .894

a16 200 1 5 3.76 .936

a17 200 1 5 3.79 .931

a18 200 1 5 3.78 .925

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

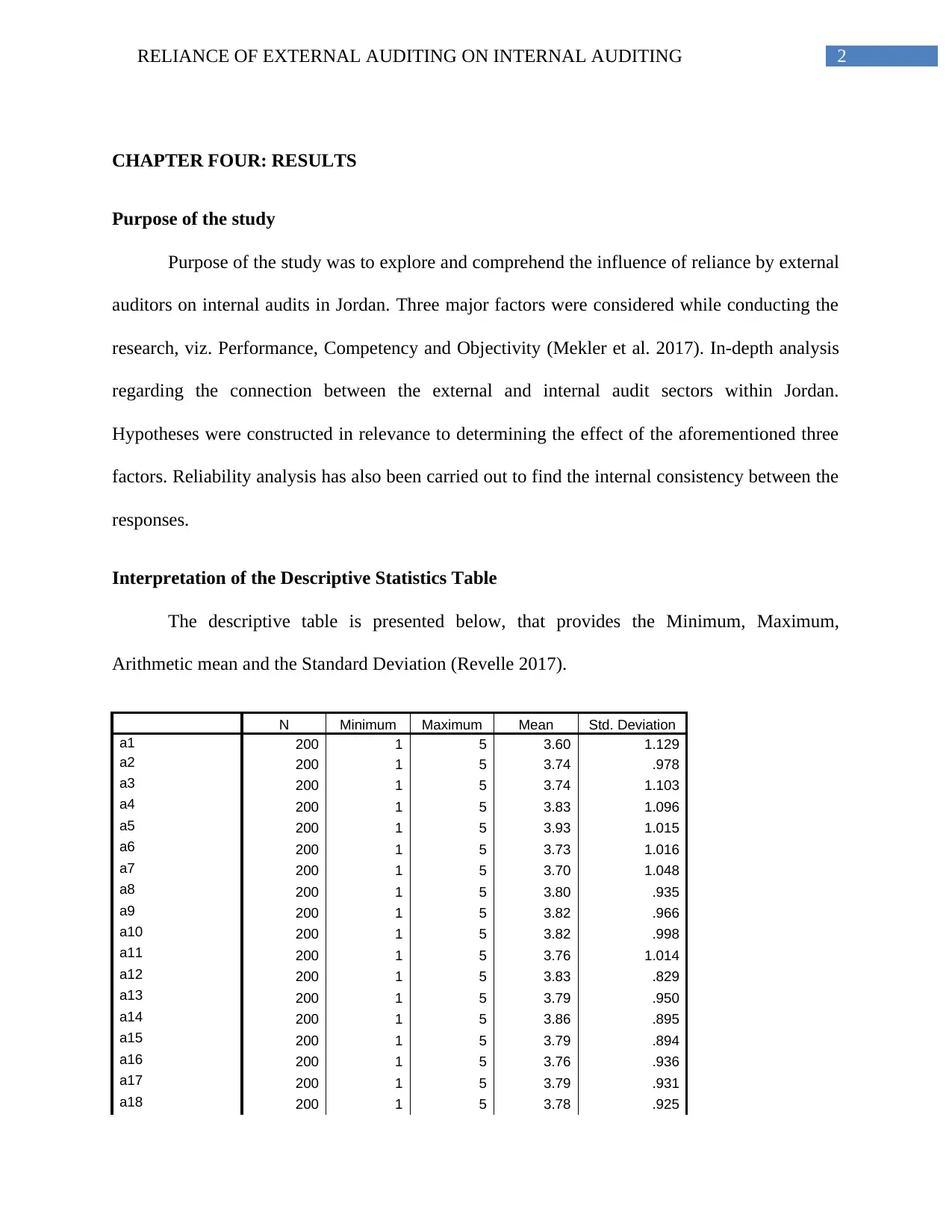

a19 200 1 5 3.72 .989

a20 200 1 5 3.74 .968

a21 200 1 5 3.97 1.104

a22 200 1 5 4.05 1.041

a23 200 1 5 3.90 1.027

a24 200 1 5 3.80 1.152

a25 200 1 5 3.96 1.093

a26 200 1 5 3.96 1.160

a27 200 1 5 4.06 .941

a28 200 1 5 4.01 1.010

a29 200 1 5 4.08 1.007

a30 200 1 5 3.97 1.044

b1 200 1 5 3.94 1.040

b2 200 1 5 3.90 1.094

b3 200 1 5 3.86 1.047

b4 200 1 5 3.84 1.096

b5 200 1 5 3.82 1.042

b6 200 1 5 3.69 1.019

b7 200 1 5 3.60 1.103

b8 200 1 5 3.52 1.130

b9 200 1 5 3.55 1.102

b10 200 1 5 3.55 1.133

b11 200 1 5 4.10 .953

b12 200 1 5 4.10 1.037

b13 200 1 5 3.98 1.063

b14 200 1 5 3.88 1.128

b15 200 1 5 3.89 1.115

Performance: 200 1 5 3.77 .585

Competence 200 1 5 3.78 .545

Objectivity 200 1 5 3.97 .606

internal auditor

performance 200 1 5 3.84 .530

Nature 200 1 5 3.87 .727

Timing 200 1 5 3.58 .721

Extent 200 1 5 3.99 .706

external auditor 200 1 5 3.81 .650

Valid N (listwise) 200

Standard Deviation of the factors a1 to a30 and b1 to b15 are all around 1.00. The average values

of the three external auditors’ along with external auditor’s characteristics differ from 3.77 to

3.99.

a19 200 1 5 3.72 .989

a20 200 1 5 3.74 .968

a21 200 1 5 3.97 1.104

a22 200 1 5 4.05 1.041

a23 200 1 5 3.90 1.027

a24 200 1 5 3.80 1.152

a25 200 1 5 3.96 1.093

a26 200 1 5 3.96 1.160

a27 200 1 5 4.06 .941

a28 200 1 5 4.01 1.010

a29 200 1 5 4.08 1.007

a30 200 1 5 3.97 1.044

b1 200 1 5 3.94 1.040

b2 200 1 5 3.90 1.094

b3 200 1 5 3.86 1.047

b4 200 1 5 3.84 1.096

b5 200 1 5 3.82 1.042

b6 200 1 5 3.69 1.019

b7 200 1 5 3.60 1.103

b8 200 1 5 3.52 1.130

b9 200 1 5 3.55 1.102

b10 200 1 5 3.55 1.133

b11 200 1 5 4.10 .953

b12 200 1 5 4.10 1.037

b13 200 1 5 3.98 1.063

b14 200 1 5 3.88 1.128

b15 200 1 5 3.89 1.115

Performance: 200 1 5 3.77 .585

Competence 200 1 5 3.78 .545

Objectivity 200 1 5 3.97 .606

internal auditor

performance 200 1 5 3.84 .530

Nature 200 1 5 3.87 .727

Timing 200 1 5 3.58 .721

Extent 200 1 5 3.99 .706

external auditor 200 1 5 3.81 .650

Valid N (listwise) 200

Standard Deviation of the factors a1 to a30 and b1 to b15 are all around 1.00. The average values

of the three external auditors’ along with external auditor’s characteristics differ from 3.77 to

3.99.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Interpretation of the Correlations Tables

From the correlations table, that showed the Pearsonian measure of Correlation, the

correlation values of Performance with Nature, Timing and Extent were found out to

be .746, .611 and .685 respectively (Wang and Zhang 2016). It is to be noted that Performance

is the independent variable under consideration and Nature, Timing and Extent are dependent

variables. Correlation between the external auditor and performance is 0.752. Thus, it can be

inferred that all of the variables have a positive relation with Performance (Zhou et al. 2016).

Especially, dependency of Nature and External Audits are of greater order. There exists a

moderately strong relation between these. That implies the increase of one would do the same for

the other dependent variables. Similarly if one decreases, same occurs for the others (Salleh

2015). Form the table the sig. (2-tailed) value is found to be 0.00 which is less than the level of

significance established 0.05. Thus we conclude there is a relation between performance and the

other aspects of external auditors and the null hypothesis, H01 is rejected (Bonett and Wright

2015). Implying, there is significant relation between internal auditor's performance and external

auditor's natures. Observing the table below, the correlations values are high for all the

independent factors along with the overall inter auditor performance with the external auditor

(Javanmard and Montanari 2014). This shows a positive correlation

Correlations

Nature Timing Extent

external

auditor

Performance: Pearson

Correlation .746(**) .611(**) .685(**) .752(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

Competence Pearson

Correlation .697(**) .584(**) .694(**) .727(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

Objectivity Pearson

Correlation

.759(**) .661(**) .731(**) .792(**)

Interpretation of the Correlations Tables

From the correlations table, that showed the Pearsonian measure of Correlation, the

correlation values of Performance with Nature, Timing and Extent were found out to

be .746, .611 and .685 respectively (Wang and Zhang 2016). It is to be noted that Performance

is the independent variable under consideration and Nature, Timing and Extent are dependent

variables. Correlation between the external auditor and performance is 0.752. Thus, it can be

inferred that all of the variables have a positive relation with Performance (Zhou et al. 2016).

Especially, dependency of Nature and External Audits are of greater order. There exists a

moderately strong relation between these. That implies the increase of one would do the same for

the other dependent variables. Similarly if one decreases, same occurs for the others (Salleh

2015). Form the table the sig. (2-tailed) value is found to be 0.00 which is less than the level of

significance established 0.05. Thus we conclude there is a relation between performance and the

other aspects of external auditors and the null hypothesis, H01 is rejected (Bonett and Wright

2015). Implying, there is significant relation between internal auditor's performance and external

auditor's natures. Observing the table below, the correlations values are high for all the

independent factors along with the overall inter auditor performance with the external auditor

(Javanmard and Montanari 2014). This shows a positive correlation

Correlations

Nature Timing Extent

external

auditor

Performance: Pearson

Correlation .746(**) .611(**) .685(**) .752(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

Competence Pearson

Correlation .697(**) .584(**) .694(**) .727(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

Objectivity Pearson

Correlation

.759(**) .661(**) .731(**) .792(**)

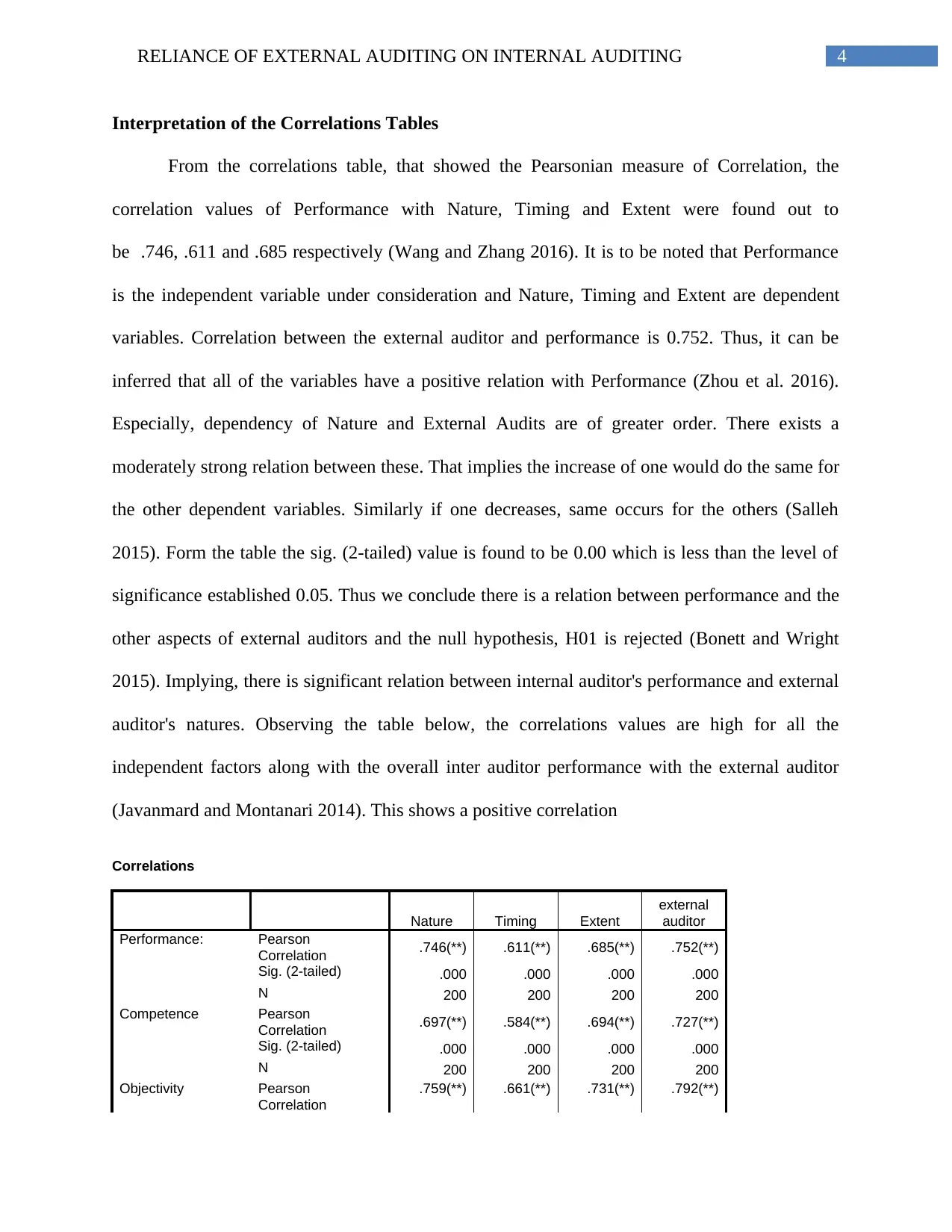

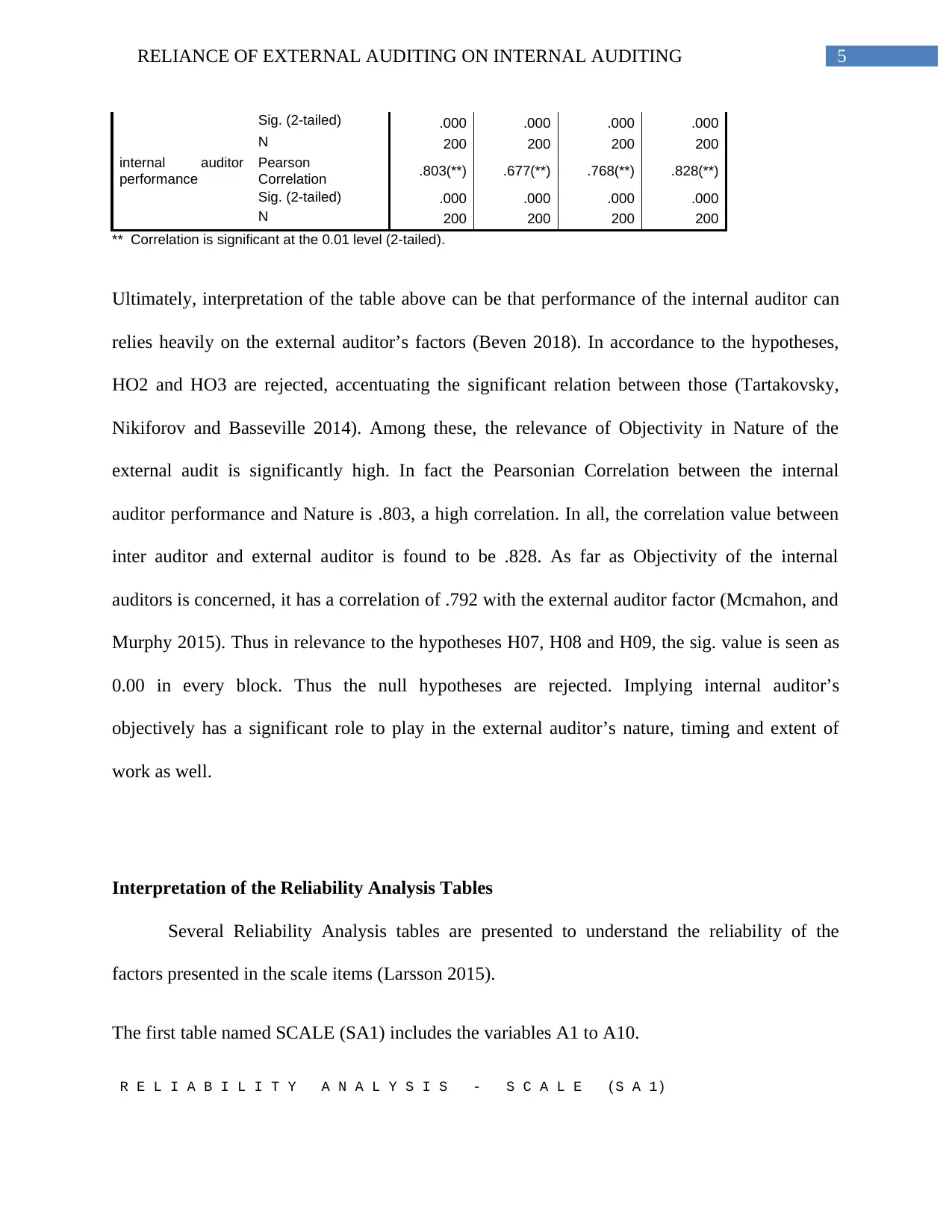

5RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

internal auditor

performance

Pearson

Correlation .803(**) .677(**) .768(**) .828(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

** Correlation is significant at the 0.01 level (2-tailed).

Ultimately, interpretation of the table above can be that performance of the internal auditor can

relies heavily on the external auditor’s factors (Beven 2018). In accordance to the hypotheses,

HO2 and HO3 are rejected, accentuating the significant relation between those (Tartakovsky,

Nikiforov and Basseville 2014). Among these, the relevance of Objectivity in Nature of the

external audit is significantly high. In fact the Pearsonian Correlation between the internal

auditor performance and Nature is .803, a high correlation. In all, the correlation value between

inter auditor and external auditor is found to be .828. As far as Objectivity of the internal

auditors is concerned, it has a correlation of .792 with the external auditor factor (Mcmahon, and

Murphy 2015). Thus in relevance to the hypotheses H07, H08 and H09, the sig. value is seen as

0.00 in every block. Thus the null hypotheses are rejected. Implying internal auditor’s

objectively has a significant role to play in the external auditor’s nature, timing and extent of

work as well.

Interpretation of the Reliability Analysis Tables

Several Reliability Analysis tables are presented to understand the reliability of the

factors presented in the scale items (Larsson 2015).

The first table named SCALE (SA1) includes the variables A1 to A10.

R E L I A B I L I T Y A N A L Y S I S - S C A L E (S A 1)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

internal auditor

performance

Pearson

Correlation .803(**) .677(**) .768(**) .828(**)

Sig. (2-tailed) .000 .000 .000 .000

N 200 200 200 200

** Correlation is significant at the 0.01 level (2-tailed).

Ultimately, interpretation of the table above can be that performance of the internal auditor can

relies heavily on the external auditor’s factors (Beven 2018). In accordance to the hypotheses,

HO2 and HO3 are rejected, accentuating the significant relation between those (Tartakovsky,

Nikiforov and Basseville 2014). Among these, the relevance of Objectivity in Nature of the

external audit is significantly high. In fact the Pearsonian Correlation between the internal

auditor performance and Nature is .803, a high correlation. In all, the correlation value between

inter auditor and external auditor is found to be .828. As far as Objectivity of the internal

auditors is concerned, it has a correlation of .792 with the external auditor factor (Mcmahon, and

Murphy 2015). Thus in relevance to the hypotheses H07, H08 and H09, the sig. value is seen as

0.00 in every block. Thus the null hypotheses are rejected. Implying internal auditor’s

objectively has a significant role to play in the external auditor’s nature, timing and extent of

work as well.

Interpretation of the Reliability Analysis Tables

Several Reliability Analysis tables are presented to understand the reliability of the

factors presented in the scale items (Larsson 2015).

The first table named SCALE (SA1) includes the variables A1 to A10.

R E L I A B I L I T Y A N A L Y S I S - S C A L E (S A 1)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

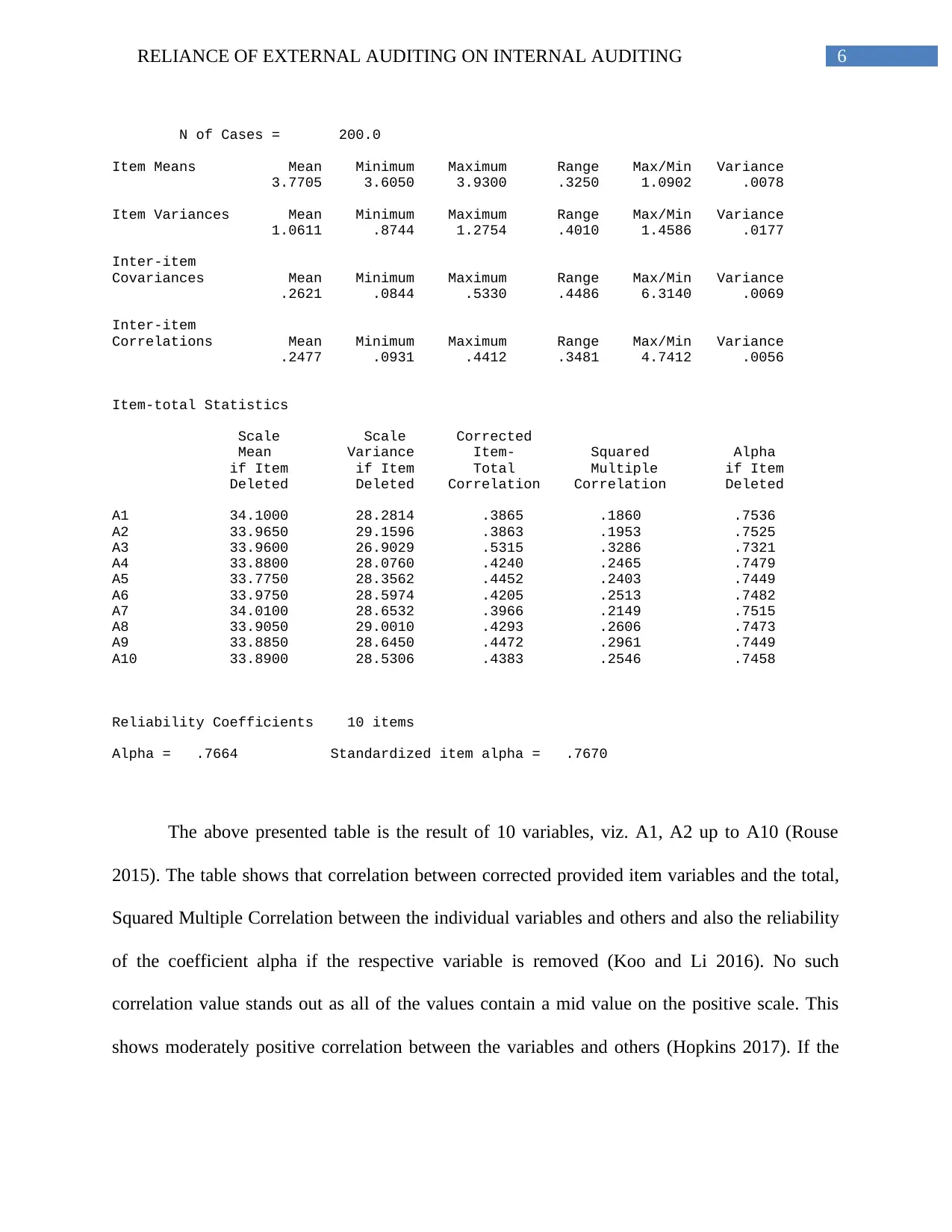

6RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

N of Cases = 200.0

Item Means Mean Minimum Maximum Range Max/Min Variance

3.7705 3.6050 3.9300 .3250 1.0902 .0078

Item Variances Mean Minimum Maximum Range Max/Min Variance

1.0611 .8744 1.2754 .4010 1.4586 .0177

Inter-item

Covariances Mean Minimum Maximum Range Max/Min Variance

.2621 .0844 .5330 .4486 6.3140 .0069

Inter-item

Correlations Mean Minimum Maximum Range Max/Min Variance

.2477 .0931 .4412 .3481 4.7412 .0056

Item-total Statistics

Scale Scale Corrected

Mean Variance Item- Squared Alpha

if Item if Item Total Multiple if Item

Deleted Deleted Correlation Correlation Deleted

A1 34.1000 28.2814 .3865 .1860 .7536

A2 33.9650 29.1596 .3863 .1953 .7525

A3 33.9600 26.9029 .5315 .3286 .7321

A4 33.8800 28.0760 .4240 .2465 .7479

A5 33.7750 28.3562 .4452 .2403 .7449

A6 33.9750 28.5974 .4205 .2513 .7482

A7 34.0100 28.6532 .3966 .2149 .7515

A8 33.9050 29.0010 .4293 .2606 .7473

A9 33.8850 28.6450 .4472 .2961 .7449

A10 33.8900 28.5306 .4383 .2546 .7458

Reliability Coefficients 10 items

Alpha = .7664 Standardized item alpha = .7670

The above presented table is the result of 10 variables, viz. A1, A2 up to A10 (Rouse

2015). The table shows that correlation between corrected provided item variables and the total,

Squared Multiple Correlation between the individual variables and others and also the reliability

of the coefficient alpha if the respective variable is removed (Koo and Li 2016). No such

correlation value stands out as all of the values contain a mid value on the positive scale. This

shows moderately positive correlation between the variables and others (Hopkins 2017). If the

N of Cases = 200.0

Item Means Mean Minimum Maximum Range Max/Min Variance

3.7705 3.6050 3.9300 .3250 1.0902 .0078

Item Variances Mean Minimum Maximum Range Max/Min Variance

1.0611 .8744 1.2754 .4010 1.4586 .0177

Inter-item

Covariances Mean Minimum Maximum Range Max/Min Variance

.2621 .0844 .5330 .4486 6.3140 .0069

Inter-item

Correlations Mean Minimum Maximum Range Max/Min Variance

.2477 .0931 .4412 .3481 4.7412 .0056

Item-total Statistics

Scale Scale Corrected

Mean Variance Item- Squared Alpha

if Item if Item Total Multiple if Item

Deleted Deleted Correlation Correlation Deleted

A1 34.1000 28.2814 .3865 .1860 .7536

A2 33.9650 29.1596 .3863 .1953 .7525

A3 33.9600 26.9029 .5315 .3286 .7321

A4 33.8800 28.0760 .4240 .2465 .7479

A5 33.7750 28.3562 .4452 .2403 .7449

A6 33.9750 28.5974 .4205 .2513 .7482

A7 34.0100 28.6532 .3966 .2149 .7515

A8 33.9050 29.0010 .4293 .2606 .7473

A9 33.8850 28.6450 .4472 .2961 .7449

A10 33.8900 28.5306 .4383 .2546 .7458

Reliability Coefficients 10 items

Alpha = .7664 Standardized item alpha = .7670

The above presented table is the result of 10 variables, viz. A1, A2 up to A10 (Rouse

2015). The table shows that correlation between corrected provided item variables and the total,

Squared Multiple Correlation between the individual variables and others and also the reliability

of the coefficient alpha if the respective variable is removed (Koo and Li 2016). No such

correlation value stands out as all of the values contain a mid value on the positive scale. This

shows moderately positive correlation between the variables and others (Hopkins 2017). If the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

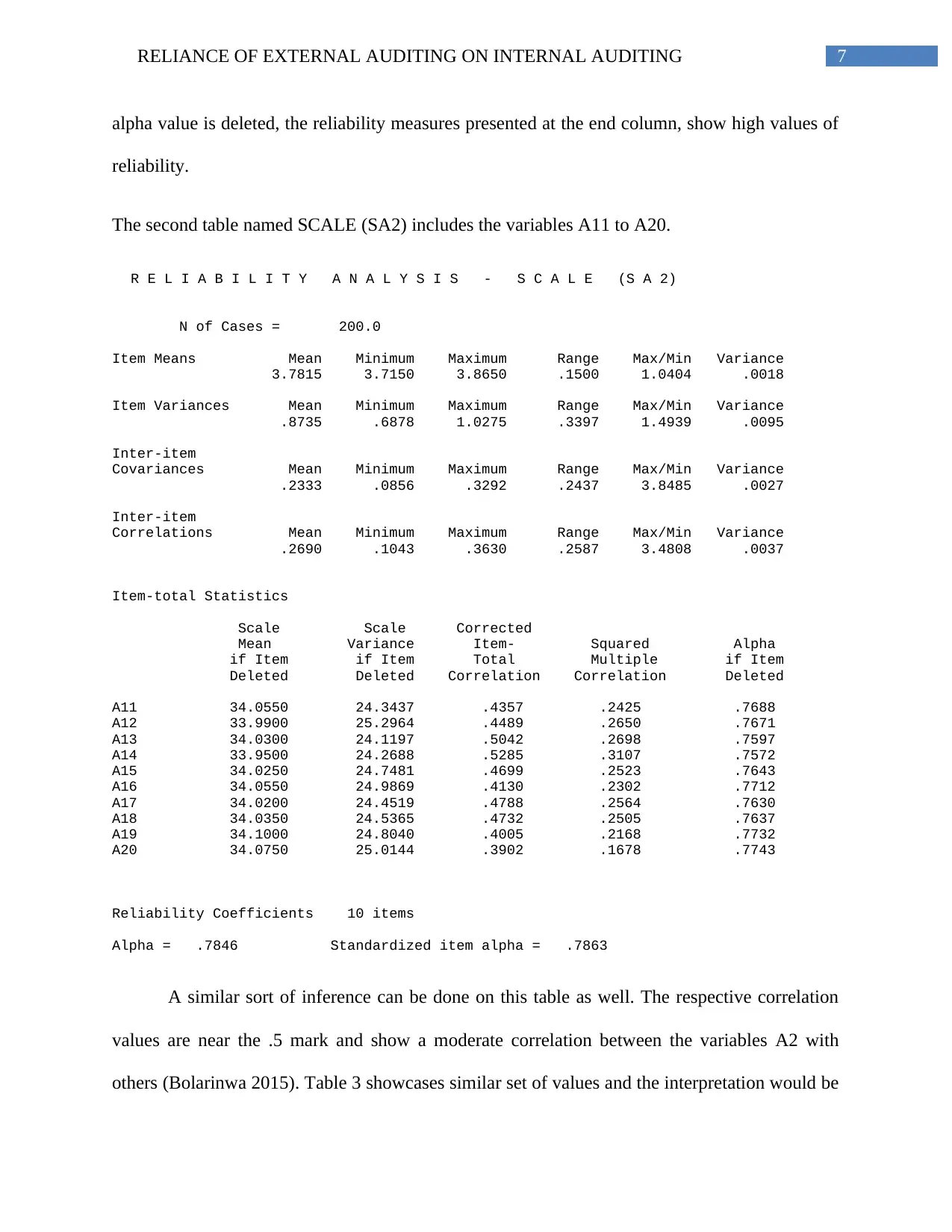

7RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

alpha value is deleted, the reliability measures presented at the end column, show high values of

reliability.

The second table named SCALE (SA2) includes the variables A11 to A20.

R E L I A B I L I T Y A N A L Y S I S - S C A L E (S A 2)

N of Cases = 200.0

Item Means Mean Minimum Maximum Range Max/Min Variance

3.7815 3.7150 3.8650 .1500 1.0404 .0018

Item Variances Mean Minimum Maximum Range Max/Min Variance

.8735 .6878 1.0275 .3397 1.4939 .0095

Inter-item

Covariances Mean Minimum Maximum Range Max/Min Variance

.2333 .0856 .3292 .2437 3.8485 .0027

Inter-item

Correlations Mean Minimum Maximum Range Max/Min Variance

.2690 .1043 .3630 .2587 3.4808 .0037

Item-total Statistics

Scale Scale Corrected

Mean Variance Item- Squared Alpha

if Item if Item Total Multiple if Item

Deleted Deleted Correlation Correlation Deleted

A11 34.0550 24.3437 .4357 .2425 .7688

A12 33.9900 25.2964 .4489 .2650 .7671

A13 34.0300 24.1197 .5042 .2698 .7597

A14 33.9500 24.2688 .5285 .3107 .7572

A15 34.0250 24.7481 .4699 .2523 .7643

A16 34.0550 24.9869 .4130 .2302 .7712

A17 34.0200 24.4519 .4788 .2564 .7630

A18 34.0350 24.5365 .4732 .2505 .7637

A19 34.1000 24.8040 .4005 .2168 .7732

A20 34.0750 25.0144 .3902 .1678 .7743

Reliability Coefficients 10 items

Alpha = .7846 Standardized item alpha = .7863

A similar sort of inference can be done on this table as well. The respective correlation

values are near the .5 mark and show a moderate correlation between the variables A2 with

others (Bolarinwa 2015). Table 3 showcases similar set of values and the interpretation would be

alpha value is deleted, the reliability measures presented at the end column, show high values of

reliability.

The second table named SCALE (SA2) includes the variables A11 to A20.

R E L I A B I L I T Y A N A L Y S I S - S C A L E (S A 2)

N of Cases = 200.0

Item Means Mean Minimum Maximum Range Max/Min Variance

3.7815 3.7150 3.8650 .1500 1.0404 .0018

Item Variances Mean Minimum Maximum Range Max/Min Variance

.8735 .6878 1.0275 .3397 1.4939 .0095

Inter-item

Covariances Mean Minimum Maximum Range Max/Min Variance

.2333 .0856 .3292 .2437 3.8485 .0027

Inter-item

Correlations Mean Minimum Maximum Range Max/Min Variance

.2690 .1043 .3630 .2587 3.4808 .0037

Item-total Statistics

Scale Scale Corrected

Mean Variance Item- Squared Alpha

if Item if Item Total Multiple if Item

Deleted Deleted Correlation Correlation Deleted

A11 34.0550 24.3437 .4357 .2425 .7688

A12 33.9900 25.2964 .4489 .2650 .7671

A13 34.0300 24.1197 .5042 .2698 .7597

A14 33.9500 24.2688 .5285 .3107 .7572

A15 34.0250 24.7481 .4699 .2523 .7643

A16 34.0550 24.9869 .4130 .2302 .7712

A17 34.0200 24.4519 .4788 .2564 .7630

A18 34.0350 24.5365 .4732 .2505 .7637

A19 34.1000 24.8040 .4005 .2168 .7732

A20 34.0750 25.0144 .3902 .1678 .7743

Reliability Coefficients 10 items

Alpha = .7846 Standardized item alpha = .7863

A similar sort of inference can be done on this table as well. The respective correlation

values are near the .5 mark and show a moderate correlation between the variables A2 with

others (Bolarinwa 2015). Table 3 showcases similar set of values and the interpretation would be

8RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

the same. Fourth table includes all the variables A1 to A30 and provides a scale for overall

relation between all the variables (Yu and Richardson 2015). The Squared Multiple Correlation

values can be observed with the value centered on a bit more than .3. This implies although there

is not a strong relation between them, however, there exists positive relation (Koo. and Li 2016).

The reliability of the scales if any one of the respective variables were deleted in the fourth table

is high and majority is greater than 0.9. This means that it is also to be noted the item means and

variances along with the inter-item co variances and correlations are also provided in the

respective tables (Kim, Lee and Lim 2017). In all, it can be concluded that required level of

internal consistency is existent in the scale items.

Interpretation of the Regression and ANOVA Table

From the first Regression table, R-squared value is found to be .650. This implies that

that nature explains 65% of the internal auditor’s characters (Bennell and Canter 2017). The

first ANOVA Table provided considers Nature as the dependent variable and Objectivity,

Competence and Performance are the constants. ANOVA tables are constructed to test whether a

significant difference between the two distinct group means exists (Austin and Steyerberg 2015).

The significance value is calculated as 0.00 which is less than the fixed level of significance

value, 0.05 (Binabaj 2014). Thus the reliance of internal auditor’s mentioned aspects on the

nature of the external auditors is high.

The two following tables to the first one are concerned with the relation between Timing

and Extent with the three factors of internal auditors (Moon 2016). Further tables are also

provided to illustrate the relation between the variables (Park 2015). The mean of the Inter-item

correlations of the respective tables are given below.

the same. Fourth table includes all the variables A1 to A30 and provides a scale for overall

relation between all the variables (Yu and Richardson 2015). The Squared Multiple Correlation

values can be observed with the value centered on a bit more than .3. This implies although there

is not a strong relation between them, however, there exists positive relation (Koo. and Li 2016).

The reliability of the scales if any one of the respective variables were deleted in the fourth table

is high and majority is greater than 0.9. This means that it is also to be noted the item means and

variances along with the inter-item co variances and correlations are also provided in the

respective tables (Kim, Lee and Lim 2017). In all, it can be concluded that required level of

internal consistency is existent in the scale items.

Interpretation of the Regression and ANOVA Table

From the first Regression table, R-squared value is found to be .650. This implies that

that nature explains 65% of the internal auditor’s characters (Bennell and Canter 2017). The

first ANOVA Table provided considers Nature as the dependent variable and Objectivity,

Competence and Performance are the constants. ANOVA tables are constructed to test whether a

significant difference between the two distinct group means exists (Austin and Steyerberg 2015).

The significance value is calculated as 0.00 which is less than the fixed level of significance

value, 0.05 (Binabaj 2014). Thus the reliance of internal auditor’s mentioned aspects on the

nature of the external auditors is high.

The two following tables to the first one are concerned with the relation between Timing

and Extent with the three factors of internal auditors (Moon 2016). Further tables are also

provided to illustrate the relation between the variables (Park 2015). The mean of the Inter-item

correlations of the respective tables are given below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

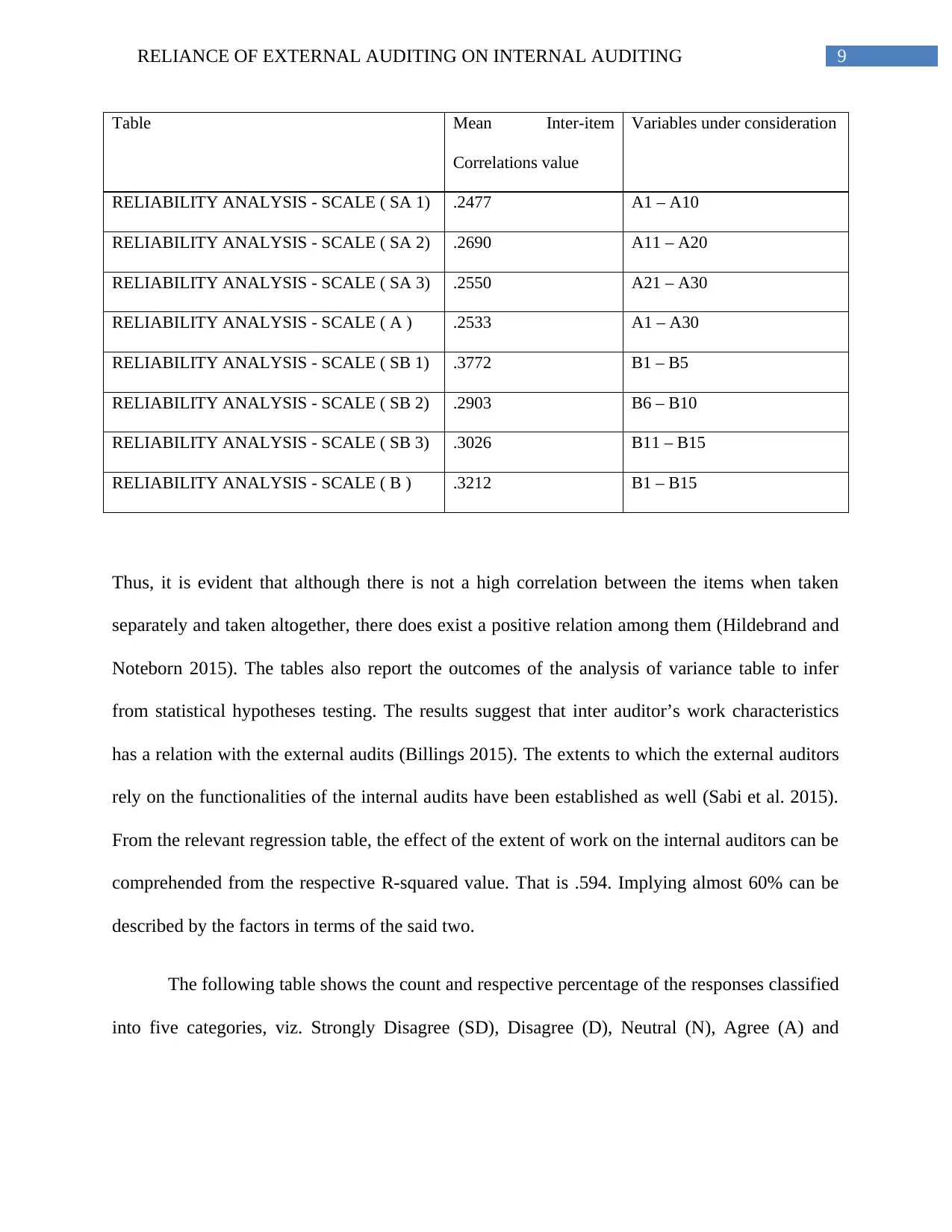

Table Mean Inter-item

Correlations value

Variables under consideration

RELIABILITY ANALYSIS - SCALE ( SA 1) .2477 A1 – A10

RELIABILITY ANALYSIS - SCALE ( SA 2) .2690 A11 – A20

RELIABILITY ANALYSIS - SCALE ( SA 3) .2550 A21 – A30

RELIABILITY ANALYSIS - SCALE ( A ) .2533 A1 – A30

RELIABILITY ANALYSIS - SCALE ( SB 1) .3772 B1 – B5

RELIABILITY ANALYSIS - SCALE ( SB 2) .2903 B6 – B10

RELIABILITY ANALYSIS - SCALE ( SB 3) .3026 B11 – B15

RELIABILITY ANALYSIS - SCALE ( B ) .3212 B1 – B15

Thus, it is evident that although there is not a high correlation between the items when taken

separately and taken altogether, there does exist a positive relation among them (Hildebrand and

Noteborn 2015). The tables also report the outcomes of the analysis of variance table to infer

from statistical hypotheses testing. The results suggest that inter auditor’s work characteristics

has a relation with the external audits (Billings 2015). The extents to which the external auditors

rely on the functionalities of the internal audits have been established as well (Sabi et al. 2015).

From the relevant regression table, the effect of the extent of work on the internal auditors can be

comprehended from the respective R-squared value. That is .594. Implying almost 60% can be

described by the factors in terms of the said two.

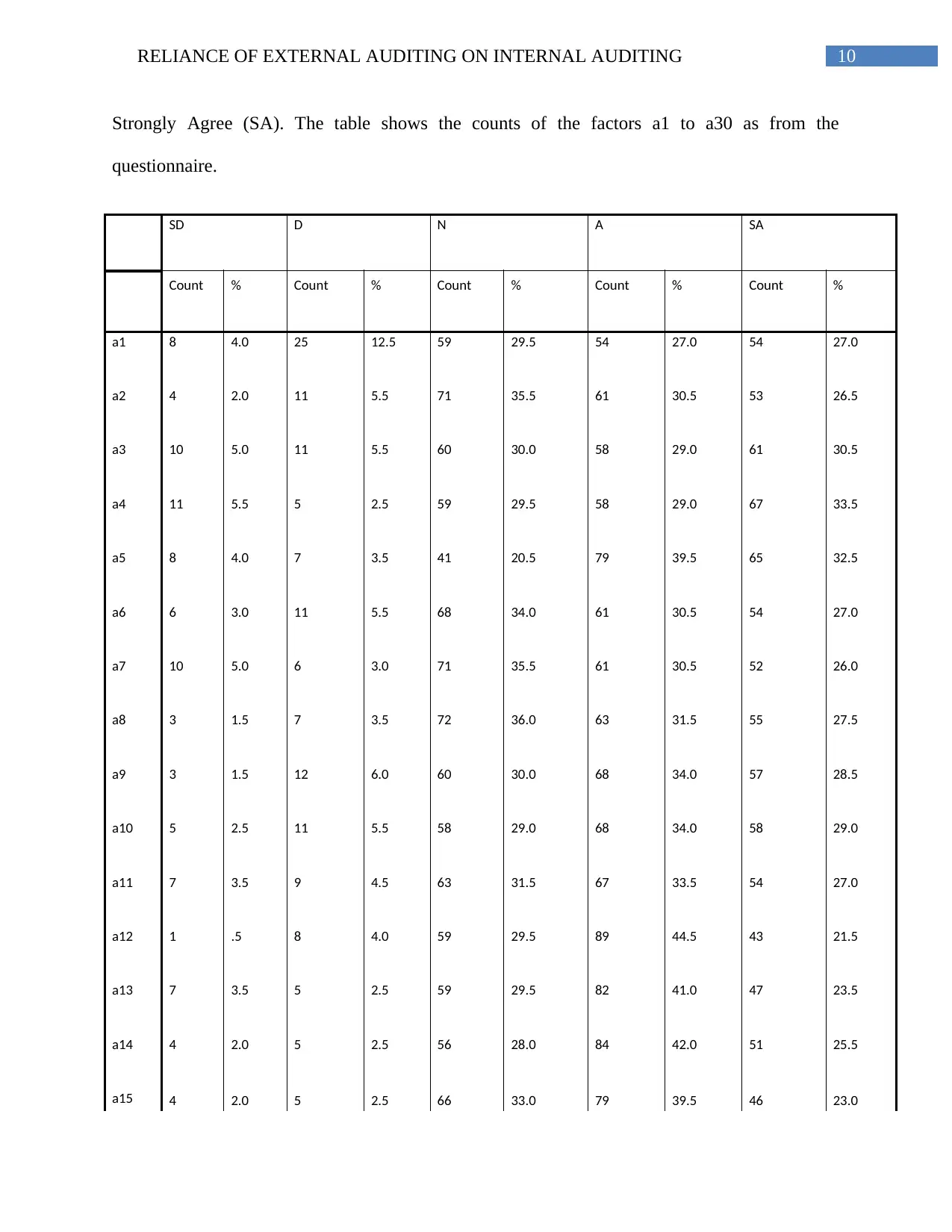

The following table shows the count and respective percentage of the responses classified

into five categories, viz. Strongly Disagree (SD), Disagree (D), Neutral (N), Agree (A) and

Table Mean Inter-item

Correlations value

Variables under consideration

RELIABILITY ANALYSIS - SCALE ( SA 1) .2477 A1 – A10

RELIABILITY ANALYSIS - SCALE ( SA 2) .2690 A11 – A20

RELIABILITY ANALYSIS - SCALE ( SA 3) .2550 A21 – A30

RELIABILITY ANALYSIS - SCALE ( A ) .2533 A1 – A30

RELIABILITY ANALYSIS - SCALE ( SB 1) .3772 B1 – B5

RELIABILITY ANALYSIS - SCALE ( SB 2) .2903 B6 – B10

RELIABILITY ANALYSIS - SCALE ( SB 3) .3026 B11 – B15

RELIABILITY ANALYSIS - SCALE ( B ) .3212 B1 – B15

Thus, it is evident that although there is not a high correlation between the items when taken

separately and taken altogether, there does exist a positive relation among them (Hildebrand and

Noteborn 2015). The tables also report the outcomes of the analysis of variance table to infer

from statistical hypotheses testing. The results suggest that inter auditor’s work characteristics

has a relation with the external audits (Billings 2015). The extents to which the external auditors

rely on the functionalities of the internal audits have been established as well (Sabi et al. 2015).

From the relevant regression table, the effect of the extent of work on the internal auditors can be

comprehended from the respective R-squared value. That is .594. Implying almost 60% can be

described by the factors in terms of the said two.

The following table shows the count and respective percentage of the responses classified

into five categories, viz. Strongly Disagree (SD), Disagree (D), Neutral (N), Agree (A) and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

Strongly Agree (SA). The table shows the counts of the factors a1 to a30 as from the

questionnaire.

SD D N A SA

Count % Count % Count % Count % Count %

a1 8 4.0 25 12.5 59 29.5 54 27.0 54 27.0

a2 4 2.0 11 5.5 71 35.5 61 30.5 53 26.5

a3 10 5.0 11 5.5 60 30.0 58 29.0 61 30.5

a4 11 5.5 5 2.5 59 29.5 58 29.0 67 33.5

a5 8 4.0 7 3.5 41 20.5 79 39.5 65 32.5

a6 6 3.0 11 5.5 68 34.0 61 30.5 54 27.0

a7 10 5.0 6 3.0 71 35.5 61 30.5 52 26.0

a8 3 1.5 7 3.5 72 36.0 63 31.5 55 27.5

a9 3 1.5 12 6.0 60 30.0 68 34.0 57 28.5

a10 5 2.5 11 5.5 58 29.0 68 34.0 58 29.0

a11 7 3.5 9 4.5 63 31.5 67 33.5 54 27.0

a12 1 .5 8 4.0 59 29.5 89 44.5 43 21.5

a13 7 3.5 5 2.5 59 29.5 82 41.0 47 23.5

a14 4 2.0 5 2.5 56 28.0 84 42.0 51 25.5

a15 4 2.0 5 2.5 66 33.0 79 39.5 46 23.0

Strongly Agree (SA). The table shows the counts of the factors a1 to a30 as from the

questionnaire.

SD D N A SA

Count % Count % Count % Count % Count %

a1 8 4.0 25 12.5 59 29.5 54 27.0 54 27.0

a2 4 2.0 11 5.5 71 35.5 61 30.5 53 26.5

a3 10 5.0 11 5.5 60 30.0 58 29.0 61 30.5

a4 11 5.5 5 2.5 59 29.5 58 29.0 67 33.5

a5 8 4.0 7 3.5 41 20.5 79 39.5 65 32.5

a6 6 3.0 11 5.5 68 34.0 61 30.5 54 27.0

a7 10 5.0 6 3.0 71 35.5 61 30.5 52 26.0

a8 3 1.5 7 3.5 72 36.0 63 31.5 55 27.5

a9 3 1.5 12 6.0 60 30.0 68 34.0 57 28.5

a10 5 2.5 11 5.5 58 29.0 68 34.0 58 29.0

a11 7 3.5 9 4.5 63 31.5 67 33.5 54 27.0

a12 1 .5 8 4.0 59 29.5 89 44.5 43 21.5

a13 7 3.5 5 2.5 59 29.5 82 41.0 47 23.5

a14 4 2.0 5 2.5 56 28.0 84 42.0 51 25.5

a15 4 2.0 5 2.5 66 33.0 79 39.5 46 23.0

11RELIANCE OF EXTERNAL AUDITING ON INTERNAL AUDITING

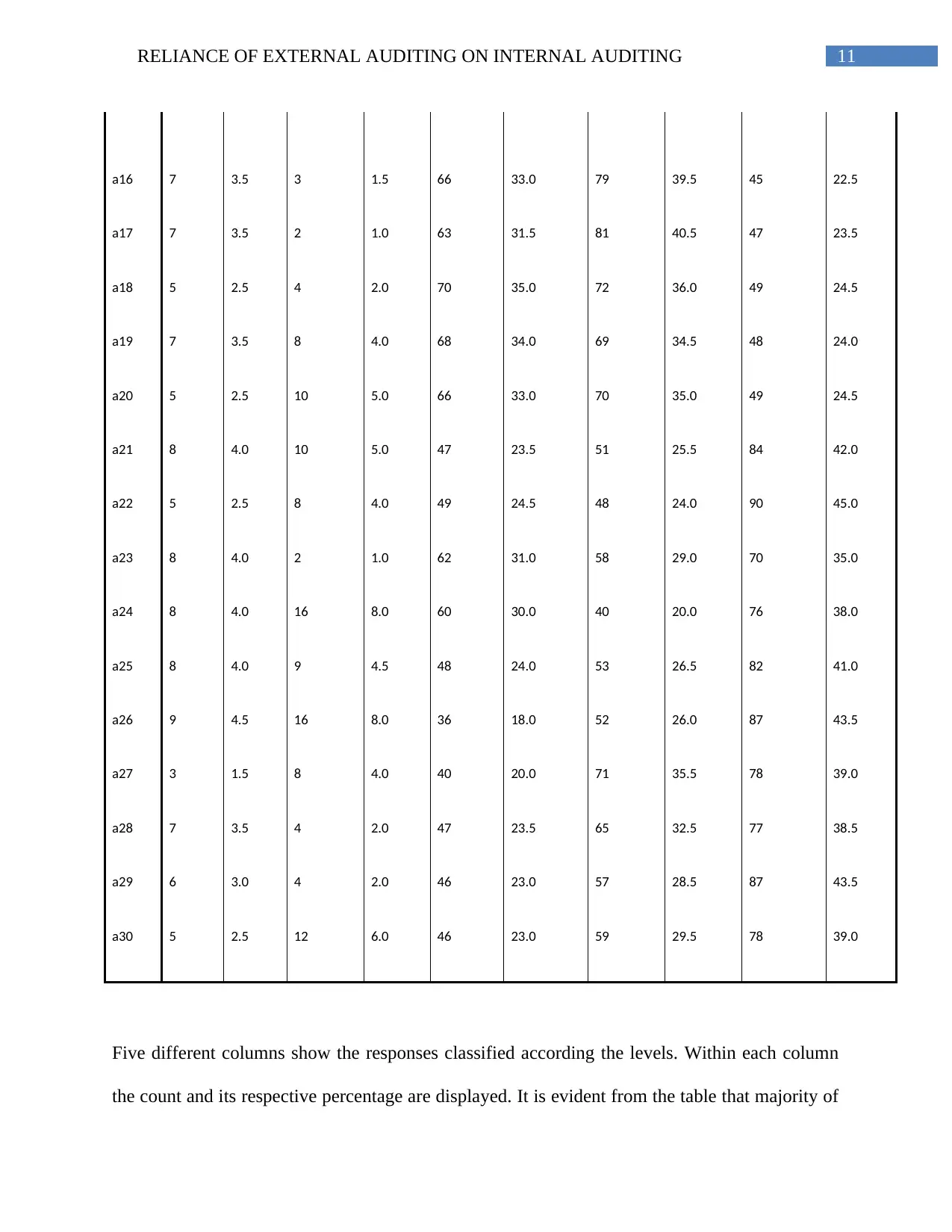

a16 7 3.5 3 1.5 66 33.0 79 39.5 45 22.5

a17 7 3.5 2 1.0 63 31.5 81 40.5 47 23.5

a18 5 2.5 4 2.0 70 35.0 72 36.0 49 24.5

a19 7 3.5 8 4.0 68 34.0 69 34.5 48 24.0

a20 5 2.5 10 5.0 66 33.0 70 35.0 49 24.5

a21 8 4.0 10 5.0 47 23.5 51 25.5 84 42.0

a22 5 2.5 8 4.0 49 24.5 48 24.0 90 45.0

a23 8 4.0 2 1.0 62 31.0 58 29.0 70 35.0

a24 8 4.0 16 8.0 60 30.0 40 20.0 76 38.0

a25 8 4.0 9 4.5 48 24.0 53 26.5 82 41.0

a26 9 4.5 16 8.0 36 18.0 52 26.0 87 43.5

a27 3 1.5 8 4.0 40 20.0 71 35.5 78 39.0

a28 7 3.5 4 2.0 47 23.5 65 32.5 77 38.5

a29 6 3.0 4 2.0 46 23.0 57 28.5 87 43.5

a30 5 2.5 12 6.0 46 23.0 59 29.5 78 39.0

Five different columns show the responses classified according the levels. Within each column

the count and its respective percentage are displayed. It is evident from the table that majority of

a16 7 3.5 3 1.5 66 33.0 79 39.5 45 22.5

a17 7 3.5 2 1.0 63 31.5 81 40.5 47 23.5

a18 5 2.5 4 2.0 70 35.0 72 36.0 49 24.5

a19 7 3.5 8 4.0 68 34.0 69 34.5 48 24.0

a20 5 2.5 10 5.0 66 33.0 70 35.0 49 24.5

a21 8 4.0 10 5.0 47 23.5 51 25.5 84 42.0

a22 5 2.5 8 4.0 49 24.5 48 24.0 90 45.0

a23 8 4.0 2 1.0 62 31.0 58 29.0 70 35.0

a24 8 4.0 16 8.0 60 30.0 40 20.0 76 38.0

a25 8 4.0 9 4.5 48 24.0 53 26.5 82 41.0

a26 9 4.5 16 8.0 36 18.0 52 26.0 87 43.5

a27 3 1.5 8 4.0 40 20.0 71 35.5 78 39.0

a28 7 3.5 4 2.0 47 23.5 65 32.5 77 38.5

a29 6 3.0 4 2.0 46 23.0 57 28.5 87 43.5

a30 5 2.5 12 6.0 46 23.0 59 29.5 78 39.0

Five different columns show the responses classified according the levels. Within each column

the count and its respective percentage are displayed. It is evident from the table that majority of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 49

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.