The Role of External Auditing in Promoting Corporate Accountability

VerifiedAdded on 2023/04/08

|9

|1905

|385

Essay

AI Summary

This essay critically discusses the role of external auditors in promoting corporate accountability within business organizations. It highlights the responsibilities of auditors in preventing, detecting, and reporting financial fraud, errors, and illegal acts, emphasizing their role in confirming the accountability and stewardship of management. The discussion covers various aspects such as protecting the interests of shareholders by maintaining audit independence, reporting on the financial standing of companies, ensuring compliance with accounting principles, assessing organizational risks, developing crisis management plans, and maintaining relations with regulators. The essay concludes that external auditors promote corporate accountability by safeguarding stakeholder interests, preventing financial manipulations, and ensuring transparency in financial reporting, thereby fostering trust and confidence in the financial information provided by companies.

Running head: CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN

PROMOTING CORPORATE ACCOUNTABILITY

Critically Discuss the Role of External Auditing in Promoting Corporate Accountability

Name of the Student

Name of the University

Author’s Note

PROMOTING CORPORATE ACCOUNTABILITY

Critically Discuss the Role of External Auditing in Promoting Corporate Accountability

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Board of Directors

Investing Public

External Auditors Regulators

Internal

ShareholdersAudit Committee

Introduction

The responsibilities of the auditors are the prevention, detection and reporting

of financial fraud, errors and illegal acts. The auditors are responsible for confirming

the accountability and stewardship of the clients’ management (Chandler, Edwards

and Anderson 1993). The purpose of this is the reduction of the possibility that

managements’ statements of stewardship include mistakes as a result of measured

misstatements and innocent errors. The former may take the form of either

manipulation of financial statements’ information or falsification of accounting records

(Chandler, Edwards and Anderson 1993). In the presence of all of these aspects, it

is needed for the companies’ auditors to ensure the presence of corporate

accountability in the clients’ business operations. The main aim of this essay is to

conduct a critical discussion on the role of external auditors in the promotion of

corporate accountability within the business organizations.

Discussion

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Board of Directors

Investing Public

External Auditors Regulators

Internal

ShareholdersAudit Committee

Introduction

The responsibilities of the auditors are the prevention, detection and reporting

of financial fraud, errors and illegal acts. The auditors are responsible for confirming

the accountability and stewardship of the clients’ management (Chandler, Edwards

and Anderson 1993). The purpose of this is the reduction of the possibility that

managements’ statements of stewardship include mistakes as a result of measured

misstatements and innocent errors. The former may take the form of either

manipulation of financial statements’ information or falsification of accounting records

(Chandler, Edwards and Anderson 1993). In the presence of all of these aspects, it

is needed for the companies’ auditors to ensure the presence of corporate

accountability in the clients’ business operations. The main aim of this essay is to

conduct a critical discussion on the role of external auditors in the promotion of

corporate accountability within the business organizations.

Discussion

2

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

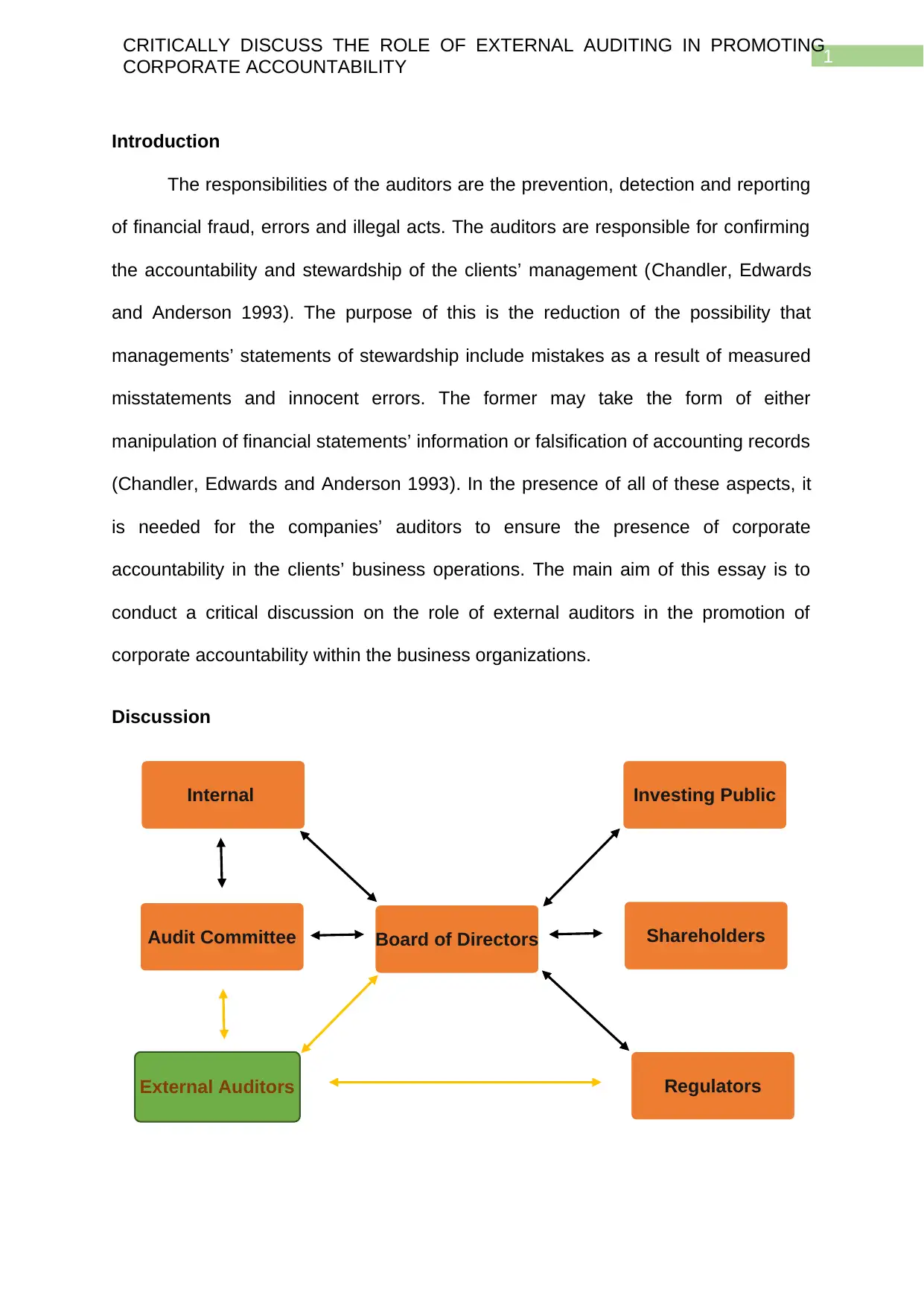

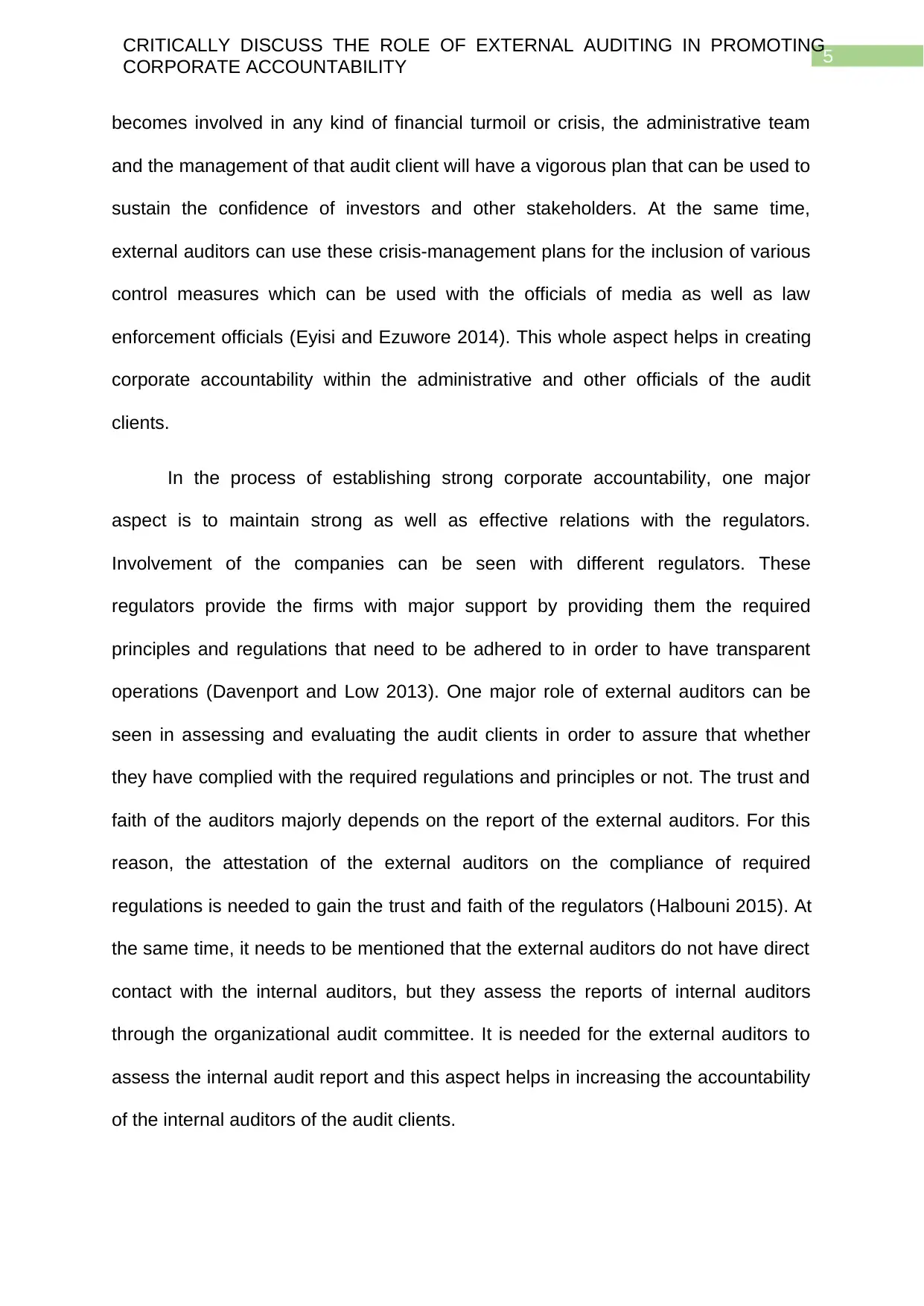

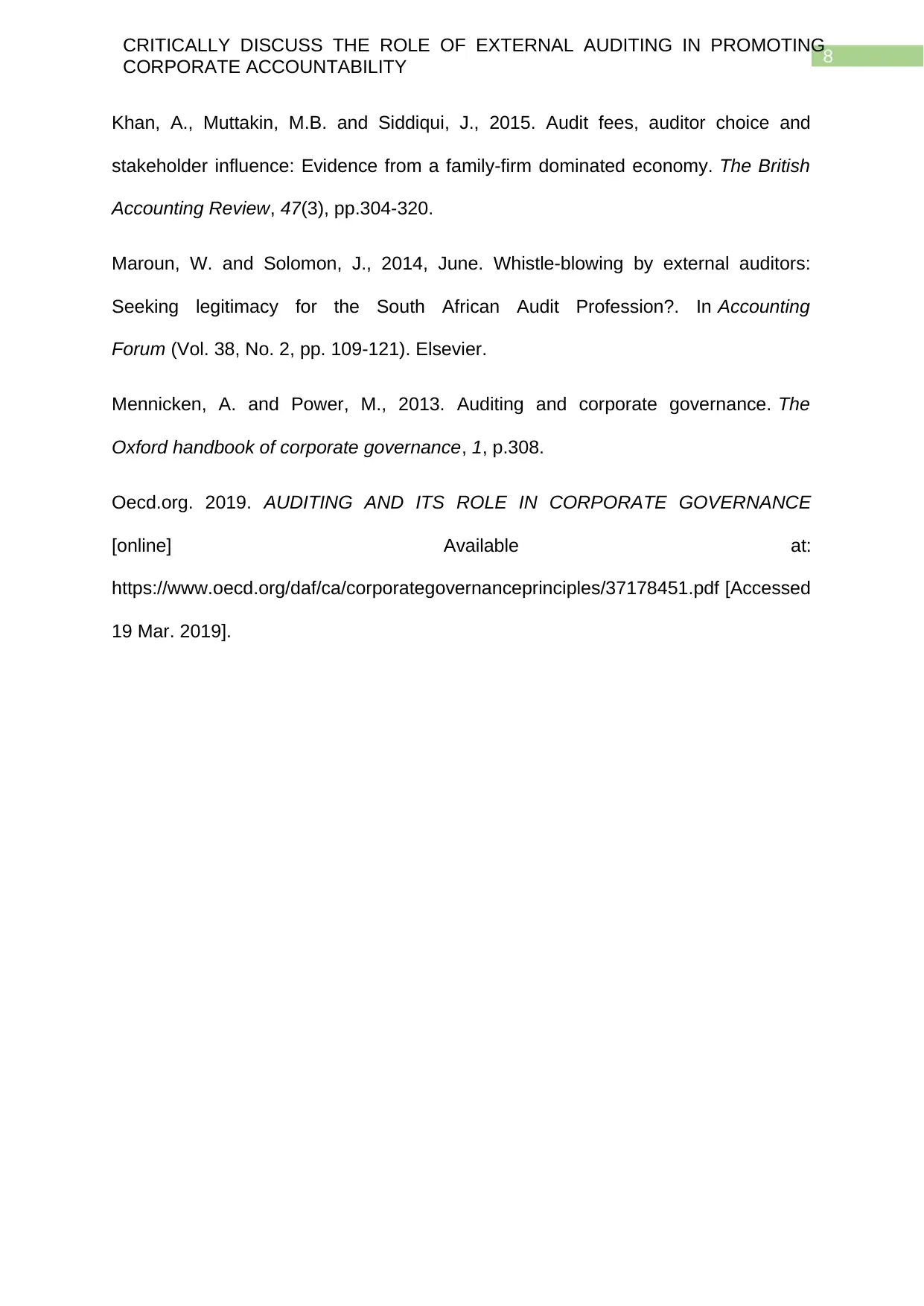

Figure: Place of the External Auditor in an Organization

(Source: oecd.org 2019)

The above figure shows the place of the external auditors in the

organizational structure. As per the above figure, external auditors have direct

contact with the directors, regulators and the audit committee and this aspect helps

the auditors in maintaining corporate accountability with the organizations. The

auditors are needed to ensure certain aspects with the aim to maintain corporate

accountability within the organizations (oecd.org 2019). The following discussion

sheds light on these aspects for the purpose of promoting corporate accountability.

It needs to be mentioned that the external auditors represents the interest of

the stakeholders and it is considered as one of the major responsibilities of the

external auditors for promoting corporate accountability is to protect the interest of

the shareholders (Harrison and van der Laan Smith 2015). It is possible for the

external auditors to protect the interest of the shareholders in the presence of the

fact that the external auditors prepare the audit report while maintaining the required

audit independence from the influence of clients’ managements (Harrison and van

der Laan Smith 2015). It is considered as one of the major responsibilities of the

external auditors to report on the state of the financial standing of the companies

along with attesting the validity of their financial reports released for the shareholders

to inform them about the true financial performance and position. At the same time,

the external auditors ensure on the fact that the boards of directors of the clients

receive reliable as well as accurate financial information for the purpose of decision-

making. It needs to be mentioned that the boards of the clients can question external

auditors about the view and assessment of the appropriateness of the used

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Figure: Place of the External Auditor in an Organization

(Source: oecd.org 2019)

The above figure shows the place of the external auditors in the

organizational structure. As per the above figure, external auditors have direct

contact with the directors, regulators and the audit committee and this aspect helps

the auditors in maintaining corporate accountability with the organizations. The

auditors are needed to ensure certain aspects with the aim to maintain corporate

accountability within the organizations (oecd.org 2019). The following discussion

sheds light on these aspects for the purpose of promoting corporate accountability.

It needs to be mentioned that the external auditors represents the interest of

the stakeholders and it is considered as one of the major responsibilities of the

external auditors for promoting corporate accountability is to protect the interest of

the shareholders (Harrison and van der Laan Smith 2015). It is possible for the

external auditors to protect the interest of the shareholders in the presence of the

fact that the external auditors prepare the audit report while maintaining the required

audit independence from the influence of clients’ managements (Harrison and van

der Laan Smith 2015). It is considered as one of the major responsibilities of the

external auditors to report on the state of the financial standing of the companies

along with attesting the validity of their financial reports released for the shareholders

to inform them about the true financial performance and position. At the same time,

the external auditors ensure on the fact that the boards of directors of the clients

receive reliable as well as accurate financial information for the purpose of decision-

making. It needs to be mentioned that the boards of the clients can question external

auditors about the view and assessment of the appropriateness of the used

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

accounting principles. Then, the auditors are needed to provide the required audit

evidence on the fact that the company has complied with the correct accounting

principles (Khan, A., Muttakin and Siddiqui 2015). This whole aspect helps in

maintain the corporate accountability.

The external auditors of the companies have a major role to play in the

promotion of accountability that leads to the promotion of overall corporate

accountability. The external auditors have the right of introducing appropriate

measures as well as policies designed in compelling accountability within the

workplace. Accountability can be considered as an assurance that the evaluation of

an individual or organization will be done on the basis of their performance or

behaviour related to some aspects for which they are accountable (Aggarwal 2013).

In this context, it needs to be mentioned that the senior management of the company

is accountable for the preparation as well as presentation of the financial statements

while complying with the required accounting principles and regulations. For

example, external auditors have the right for imposing appropriate penalties for

certain officers of senior management for manipulating the financial statements by

inflating accounting figures or cooking the accounting values (Kassem and Higson

2016). In the presence of all these reasons, the external auditors can promote

corporate accountability by imposing certain penalties such as removing the

personnel from his position, reduction in the compensation of the involved personnel

like reduction in the annual bonuses, elimination or reduction in pension and others

(Kassem and Higson 2016). All these aspects together play crucial part in the

promotion of corporate accountability within the organizations.

Another major role of the auditors can be seen in the assessment of

organizational risks along with the development of proper plans for mitigating those

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

accounting principles. Then, the auditors are needed to provide the required audit

evidence on the fact that the company has complied with the correct accounting

principles (Khan, A., Muttakin and Siddiqui 2015). This whole aspect helps in

maintain the corporate accountability.

The external auditors of the companies have a major role to play in the

promotion of accountability that leads to the promotion of overall corporate

accountability. The external auditors have the right of introducing appropriate

measures as well as policies designed in compelling accountability within the

workplace. Accountability can be considered as an assurance that the evaluation of

an individual or organization will be done on the basis of their performance or

behaviour related to some aspects for which they are accountable (Aggarwal 2013).

In this context, it needs to be mentioned that the senior management of the company

is accountable for the preparation as well as presentation of the financial statements

while complying with the required accounting principles and regulations. For

example, external auditors have the right for imposing appropriate penalties for

certain officers of senior management for manipulating the financial statements by

inflating accounting figures or cooking the accounting values (Kassem and Higson

2016). In the presence of all these reasons, the external auditors can promote

corporate accountability by imposing certain penalties such as removing the

personnel from his position, reduction in the compensation of the involved personnel

like reduction in the annual bonuses, elimination or reduction in pension and others

(Kassem and Higson 2016). All these aspects together play crucial part in the

promotion of corporate accountability within the organizations.

Another major role of the auditors can be seen in the assessment of

organizational risks along with the development of proper plans for mitigating those

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

risks. External auditors have a crucial role to play in the promotion of corporate

accountability by conducting risk assessment on periodic basis. In this aspect, the

external auditors are responsible for reviewing the security measures of their audit

clients against the corporate frauds and corruption (Mennicken and Power 2013). At

the same time, in order to assess the potential organizational risks, the external

auditors have to ensure the analysis of the overall risk tolerance of the clients there;

they are also needed to asses and analyse the efforts that the audit clients have put

towards the mitigation of those risks. For instance, in case a business organisation

has a whistleblowing system that has been underperforming for long, the external

auditors are needed to ensure that there is enough effort made for improving the

system (Maroun and Solomon 2014). This aspect helps in the reduction in errors as

well as deliberate manipulation within the financial statements so that the

stakeholders can obtain the true and fair financial statements. These steps and

measures of the external auditors are needed for establishing as well as promoting

corporate accountability within the client organizations (Maroun and Solomon 2014).

Crisis management is considered as one crucial function of the business

organizations in the presence of the fact that the presence of effective crisis

management mechanism assists the companies in dealing with sudden emergency

situations and external auditors have a major role to play in the crisis management

mechanism of the companies. External auditors of the companies can play a crucial

role in ensuring effective corporate accountability with the development of efficient

crisis-management plans that can be used in the events like corruption or financial

frauds (Alleyne, Hudaib and Pike 2013). In this particular role, it is required for the

external auditors to assess the role and responsibilities of different administrative

officials within the organizations. In this particular manner, in case the audit client

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

risks. External auditors have a crucial role to play in the promotion of corporate

accountability by conducting risk assessment on periodic basis. In this aspect, the

external auditors are responsible for reviewing the security measures of their audit

clients against the corporate frauds and corruption (Mennicken and Power 2013). At

the same time, in order to assess the potential organizational risks, the external

auditors have to ensure the analysis of the overall risk tolerance of the clients there;

they are also needed to asses and analyse the efforts that the audit clients have put

towards the mitigation of those risks. For instance, in case a business organisation

has a whistleblowing system that has been underperforming for long, the external

auditors are needed to ensure that there is enough effort made for improving the

system (Maroun and Solomon 2014). This aspect helps in the reduction in errors as

well as deliberate manipulation within the financial statements so that the

stakeholders can obtain the true and fair financial statements. These steps and

measures of the external auditors are needed for establishing as well as promoting

corporate accountability within the client organizations (Maroun and Solomon 2014).

Crisis management is considered as one crucial function of the business

organizations in the presence of the fact that the presence of effective crisis

management mechanism assists the companies in dealing with sudden emergency

situations and external auditors have a major role to play in the crisis management

mechanism of the companies. External auditors of the companies can play a crucial

role in ensuring effective corporate accountability with the development of efficient

crisis-management plans that can be used in the events like corruption or financial

frauds (Alleyne, Hudaib and Pike 2013). In this particular role, it is required for the

external auditors to assess the role and responsibilities of different administrative

officials within the organizations. In this particular manner, in case the audit client

5

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

becomes involved in any kind of financial turmoil or crisis, the administrative team

and the management of that audit client will have a vigorous plan that can be used to

sustain the confidence of investors and other stakeholders. At the same time,

external auditors can use these crisis-management plans for the inclusion of various

control measures which can be used with the officials of media as well as law

enforcement officials (Eyisi and Ezuwore 2014). This whole aspect helps in creating

corporate accountability within the administrative and other officials of the audit

clients.

In the process of establishing strong corporate accountability, one major

aspect is to maintain strong as well as effective relations with the regulators.

Involvement of the companies can be seen with different regulators. These

regulators provide the firms with major support by providing them the required

principles and regulations that need to be adhered to in order to have transparent

operations (Davenport and Low 2013). One major role of external auditors can be

seen in assessing and evaluating the audit clients in order to assure that whether

they have complied with the required regulations and principles or not. The trust and

faith of the auditors majorly depends on the report of the external auditors. For this

reason, the attestation of the external auditors on the compliance of required

regulations is needed to gain the trust and faith of the regulators (Halbouni 2015). At

the same time, it needs to be mentioned that the external auditors do not have direct

contact with the internal auditors, but they assess the reports of internal auditors

through the organizational audit committee. It is needed for the external auditors to

assess the internal audit report and this aspect helps in increasing the accountability

of the internal auditors of the audit clients.

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

becomes involved in any kind of financial turmoil or crisis, the administrative team

and the management of that audit client will have a vigorous plan that can be used to

sustain the confidence of investors and other stakeholders. At the same time,

external auditors can use these crisis-management plans for the inclusion of various

control measures which can be used with the officials of media as well as law

enforcement officials (Eyisi and Ezuwore 2014). This whole aspect helps in creating

corporate accountability within the administrative and other officials of the audit

clients.

In the process of establishing strong corporate accountability, one major

aspect is to maintain strong as well as effective relations with the regulators.

Involvement of the companies can be seen with different regulators. These

regulators provide the firms with major support by providing them the required

principles and regulations that need to be adhered to in order to have transparent

operations (Davenport and Low 2013). One major role of external auditors can be

seen in assessing and evaluating the audit clients in order to assure that whether

they have complied with the required regulations and principles or not. The trust and

faith of the auditors majorly depends on the report of the external auditors. For this

reason, the attestation of the external auditors on the compliance of required

regulations is needed to gain the trust and faith of the regulators (Halbouni 2015). At

the same time, it needs to be mentioned that the external auditors do not have direct

contact with the internal auditors, but they assess the reports of internal auditors

through the organizational audit committee. It is needed for the external auditors to

assess the internal audit report and this aspect helps in increasing the accountability

of the internal auditors of the audit clients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Conclusion

It can be seen from the above discussion that the external auditors can

promote corporate accountability by maintaining the interest of the stakeholders

where they report the credibility of the management in preparation of financial

statements. For this reason, the external auditors take different corrective measures

for the prevention of financial frauds and manipulations in the financial statements.

At the same time, the external auditors of the companies play crucial roles in

assessing organizational risks along with developing crisis management mechanism.

All these aspects together make the senior managements and board of directors of

the companies accountable towards their works related to the preparation as well as

presentation of the financial statements. Increased accountability leads to the

reduction in errors, frauds and manipulation in accounting and financial works; and

helps the investors and other stakeholders in gaining correct information about the

financial position and performance of the companies.

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Conclusion

It can be seen from the above discussion that the external auditors can

promote corporate accountability by maintaining the interest of the stakeholders

where they report the credibility of the management in preparation of financial

statements. For this reason, the external auditors take different corrective measures

for the prevention of financial frauds and manipulations in the financial statements.

At the same time, the external auditors of the companies play crucial roles in

assessing organizational risks along with developing crisis management mechanism.

All these aspects together make the senior managements and board of directors of

the companies accountable towards their works related to the preparation as well as

presentation of the financial statements. Increased accountability leads to the

reduction in errors, frauds and manipulation in accounting and financial works; and

helps the investors and other stakeholders in gaining correct information about the

financial position and performance of the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

References

Aggarwal, P., 2013. Impact of corporate governance on corporate financial

performance. IOSR Journal of Business and Management, 13(3), pp.1-5.

Alleyne, P., Hudaib, M. and Pike, R., 2013. Towards a conceptual model of whistle-

blowing intentions among external auditors. The British Accounting Review, 45(1),

pp.10-23.

Chandler, R.A., Edwards, J.R. and Anderson, M., 1993. Changing perceptions of the

role of the company auditor, 1840–1940. Accounting and Business

Research, 23(92), pp.443-459.

Davenport, E. and Low, W., 2013. From trust to compliance: accountability in the fair

trade movement. Social Enterprise Journal, 9(1), pp.88-101.

Eyisi, A.S. and Ezuwore, C.N., 2014. The impact of forensic auditors in corporate

governance. Research Journal of Finance and Accounting, 5(8), pp.31-39.

Halbouni, S.S., 2015. The Role of Auditors in Preventing, Detecting, and Reporting

Fraud: The Case of the U nited A rab E mirates (UAE). International Journal of

Auditing, 19(2), pp.117-130.

Harrison, J.S. and van der Laan Smith, J., 2015. Responsible accounting for

stakeholders. Journal of Management Studies, 52(7), pp.935-960.

Kassem, R. and Higson, A.W., 2016. External auditors and corporate corruption:

Implications for external audit regulators. Current Issues in Auditing, 10(1), pp.P1-

P10.

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

References

Aggarwal, P., 2013. Impact of corporate governance on corporate financial

performance. IOSR Journal of Business and Management, 13(3), pp.1-5.

Alleyne, P., Hudaib, M. and Pike, R., 2013. Towards a conceptual model of whistle-

blowing intentions among external auditors. The British Accounting Review, 45(1),

pp.10-23.

Chandler, R.A., Edwards, J.R. and Anderson, M., 1993. Changing perceptions of the

role of the company auditor, 1840–1940. Accounting and Business

Research, 23(92), pp.443-459.

Davenport, E. and Low, W., 2013. From trust to compliance: accountability in the fair

trade movement. Social Enterprise Journal, 9(1), pp.88-101.

Eyisi, A.S. and Ezuwore, C.N., 2014. The impact of forensic auditors in corporate

governance. Research Journal of Finance and Accounting, 5(8), pp.31-39.

Halbouni, S.S., 2015. The Role of Auditors in Preventing, Detecting, and Reporting

Fraud: The Case of the U nited A rab E mirates (UAE). International Journal of

Auditing, 19(2), pp.117-130.

Harrison, J.S. and van der Laan Smith, J., 2015. Responsible accounting for

stakeholders. Journal of Management Studies, 52(7), pp.935-960.

Kassem, R. and Higson, A.W., 2016. External auditors and corporate corruption:

Implications for external audit regulators. Current Issues in Auditing, 10(1), pp.P1-

P10.

8

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Khan, A., Muttakin, M.B. and Siddiqui, J., 2015. Audit fees, auditor choice and

stakeholder influence: Evidence from a family-firm dominated economy. The British

Accounting Review, 47(3), pp.304-320.

Maroun, W. and Solomon, J., 2014, June. Whistle-blowing by external auditors:

Seeking legitimacy for the South African Audit Profession?. In Accounting

Forum (Vol. 38, No. 2, pp. 109-121). Elsevier.

Mennicken, A. and Power, M., 2013. Auditing and corporate governance. The

Oxford handbook of corporate governance, 1, p.308.

Oecd.org. 2019. AUDITING AND ITS ROLE IN CORPORATE GOVERNANCE

[online] Available at:

https://www.oecd.org/daf/ca/corporategovernanceprinciples/37178451.pdf [Accessed

19 Mar. 2019].

CRITICALLY DISCUSS THE ROLE OF EXTERNAL AUDITING IN PROMOTING

CORPORATE ACCOUNTABILITY

Khan, A., Muttakin, M.B. and Siddiqui, J., 2015. Audit fees, auditor choice and

stakeholder influence: Evidence from a family-firm dominated economy. The British

Accounting Review, 47(3), pp.304-320.

Maroun, W. and Solomon, J., 2014, June. Whistle-blowing by external auditors:

Seeking legitimacy for the South African Audit Profession?. In Accounting

Forum (Vol. 38, No. 2, pp. 109-121). Elsevier.

Mennicken, A. and Power, M., 2013. Auditing and corporate governance. The

Oxford handbook of corporate governance, 1, p.308.

Oecd.org. 2019. AUDITING AND ITS ROLE IN CORPORATE GOVERNANCE

[online] Available at:

https://www.oecd.org/daf/ca/corporategovernanceprinciples/37178451.pdf [Accessed

19 Mar. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.