External Reporting 1 Solutions: Accounting and Financial Analysis

VerifiedAdded on 2023/06/09

|13

|1917

|452

Homework Assignment

AI Summary

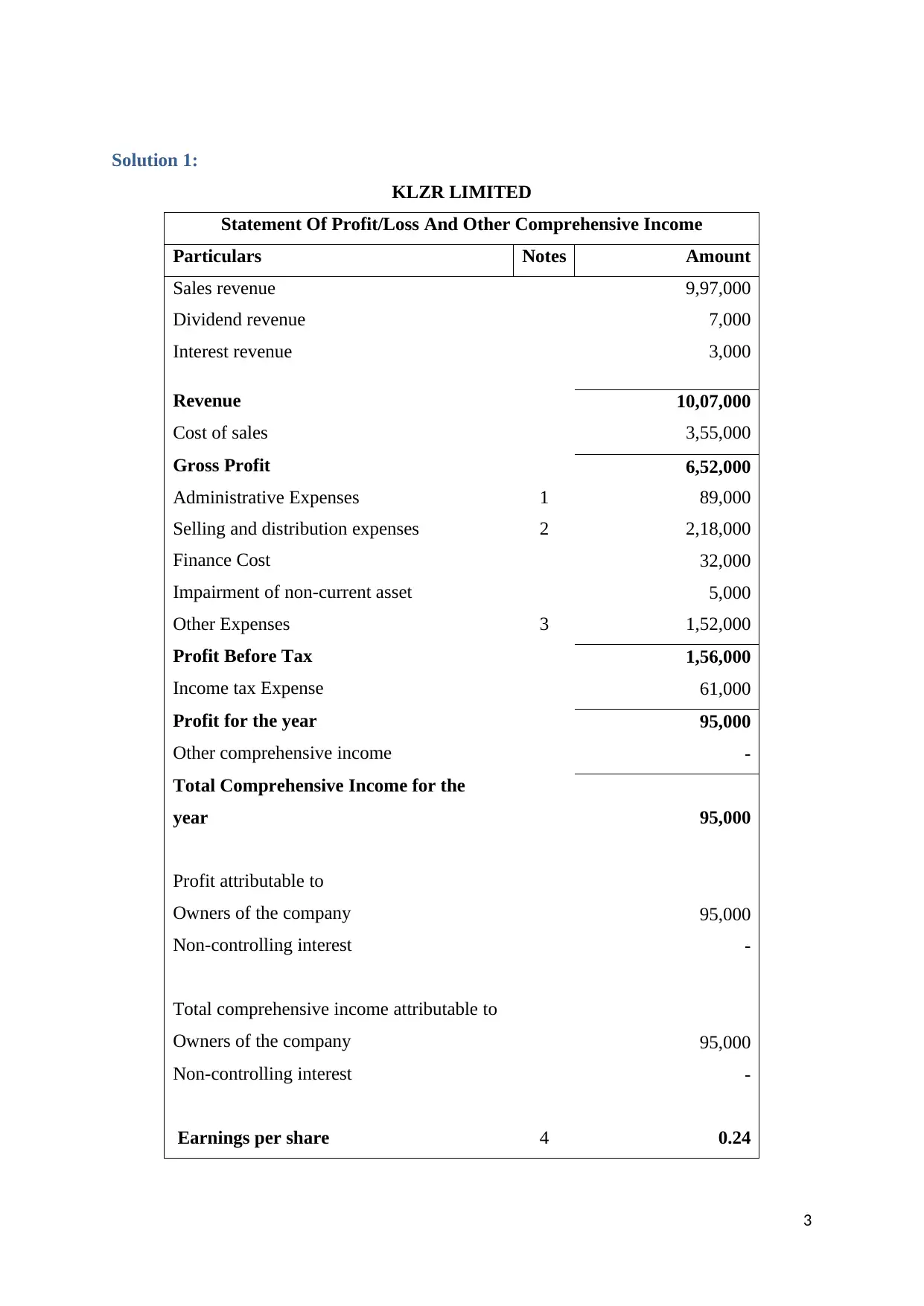

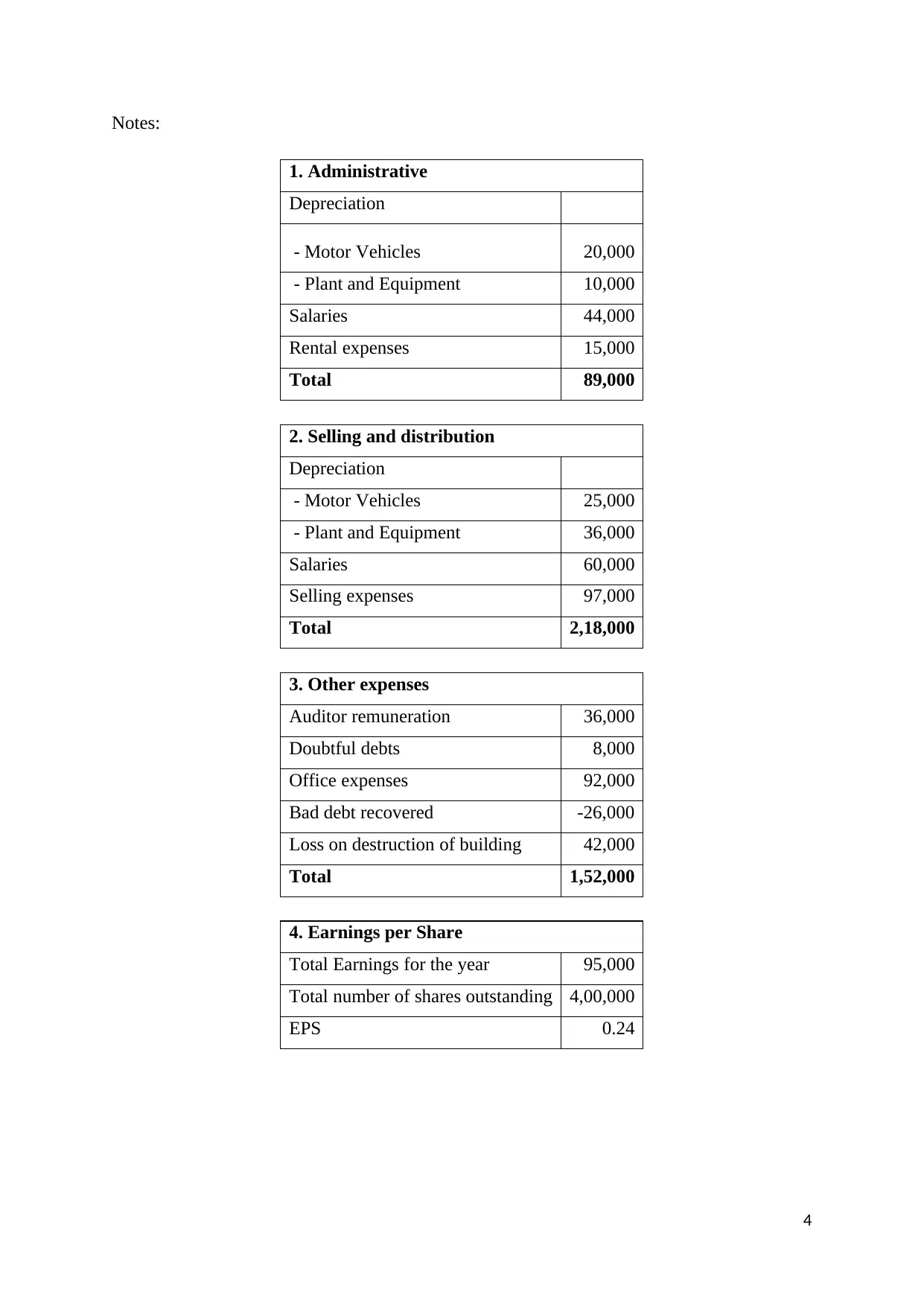

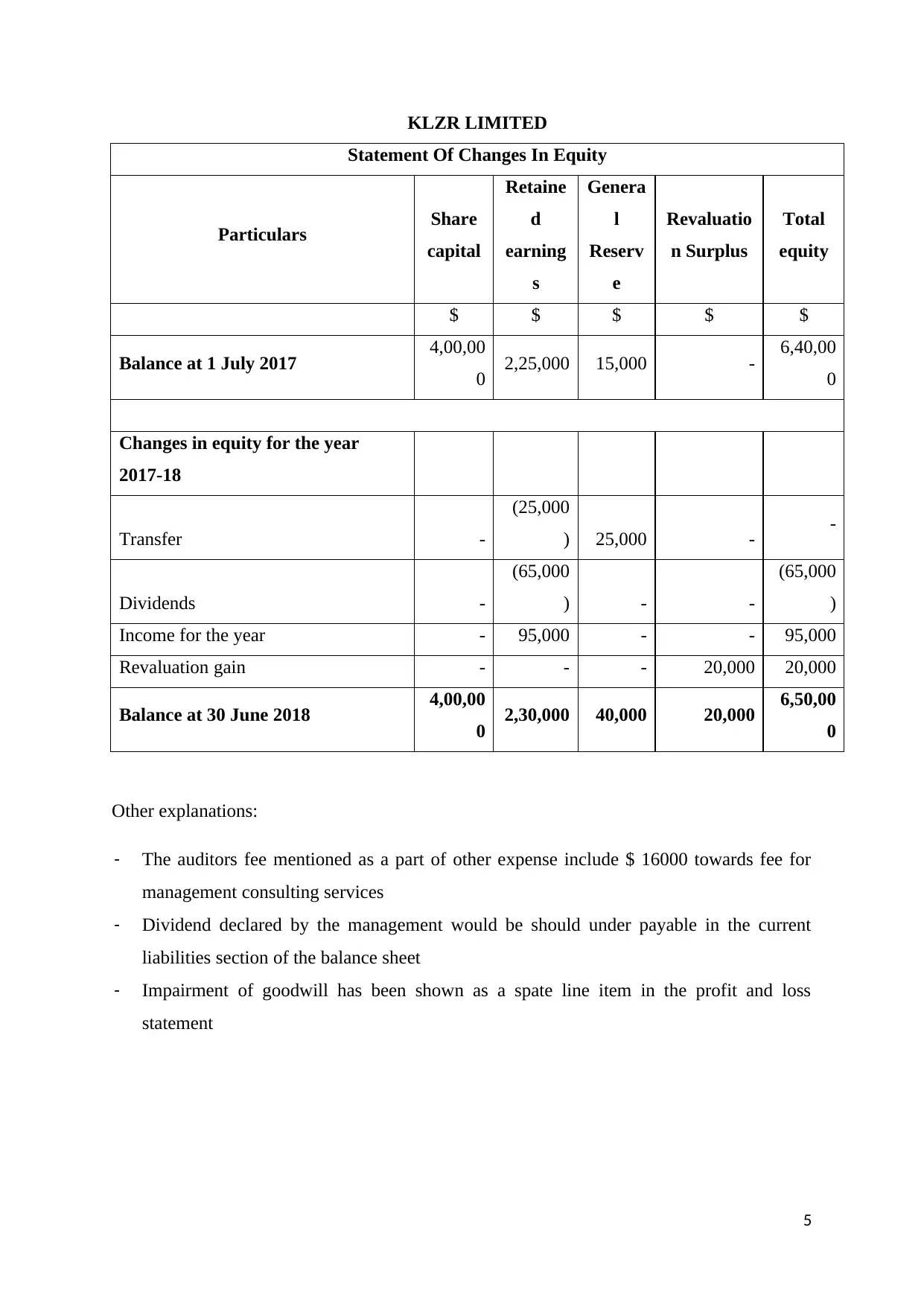

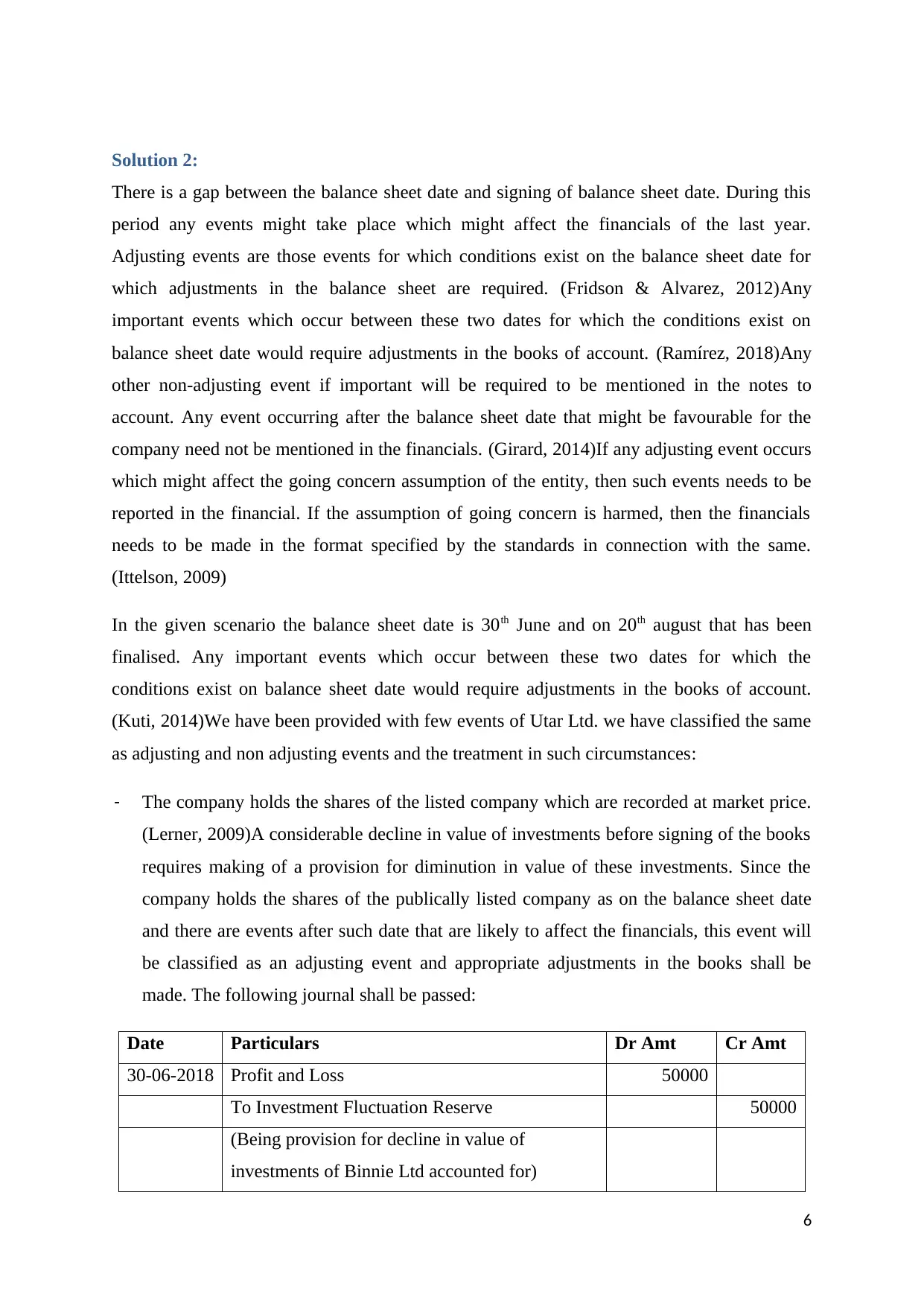

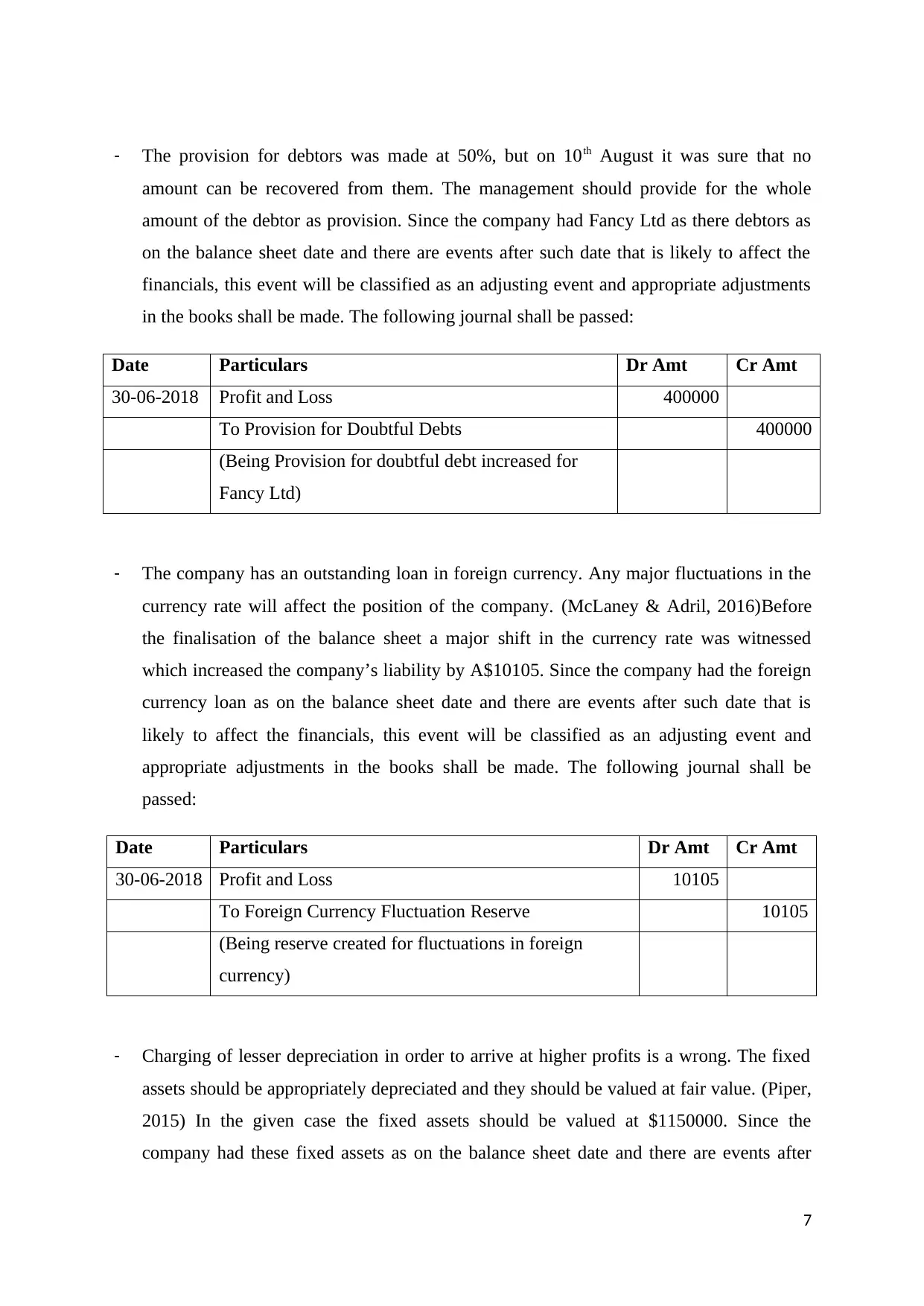

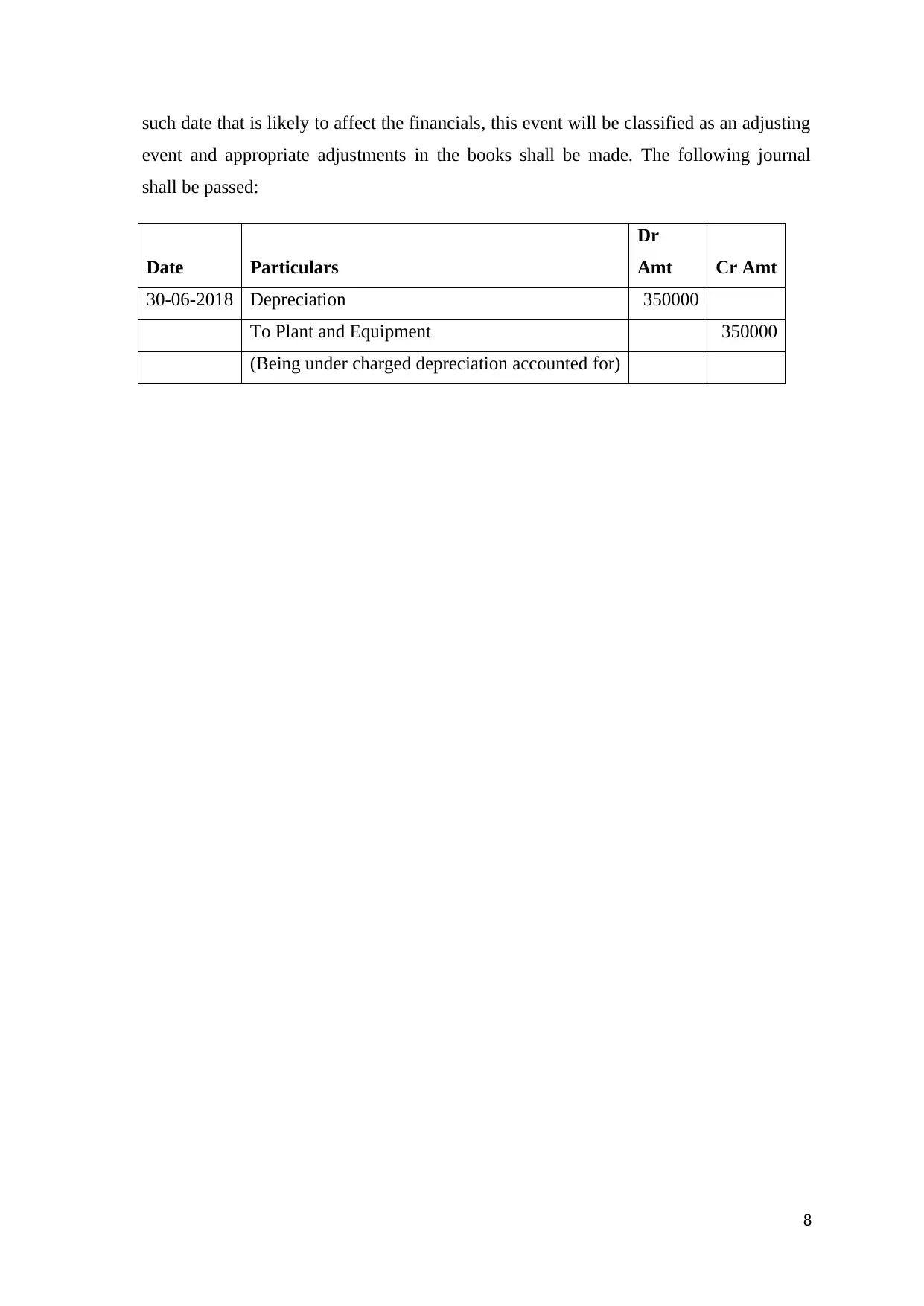

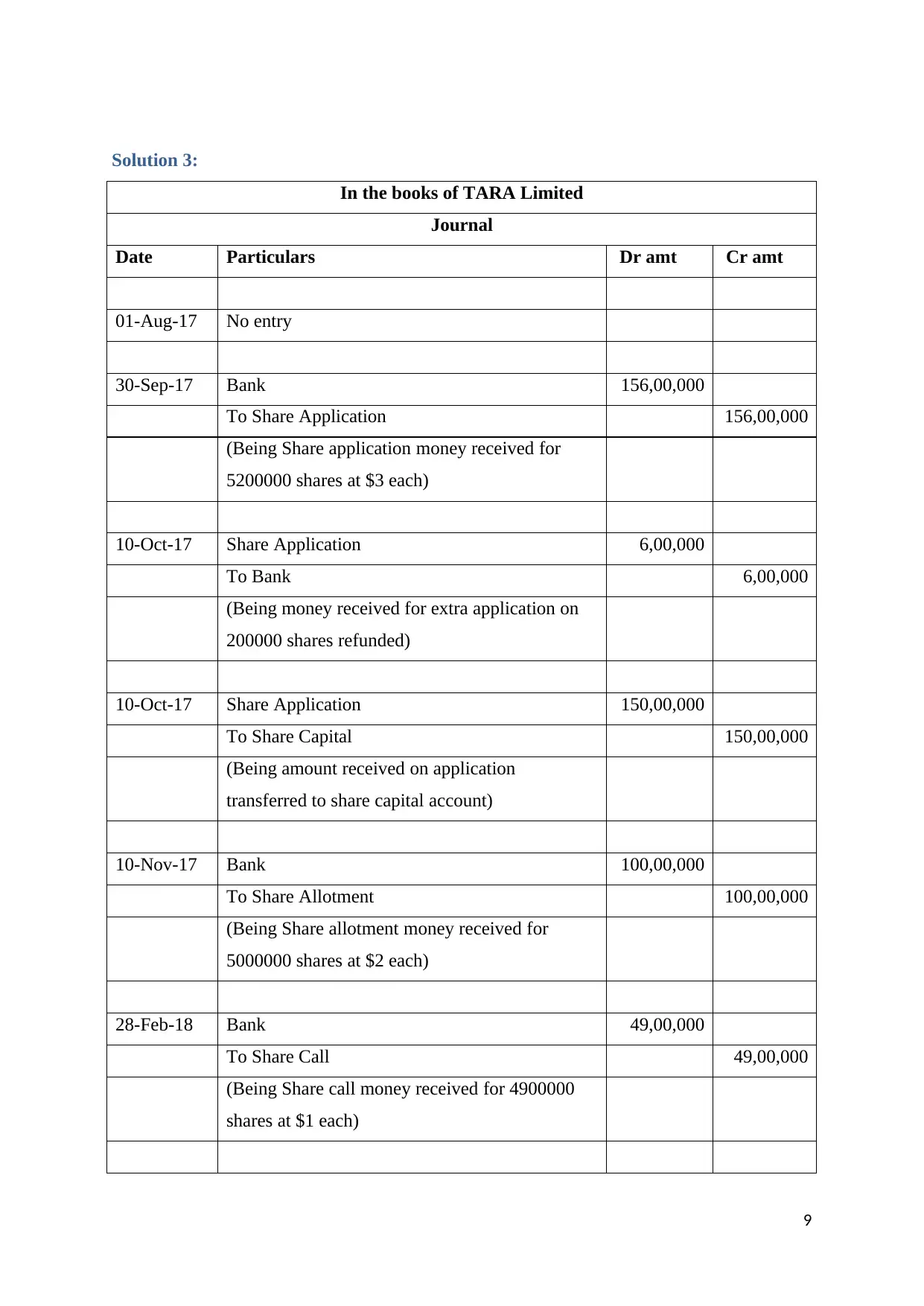

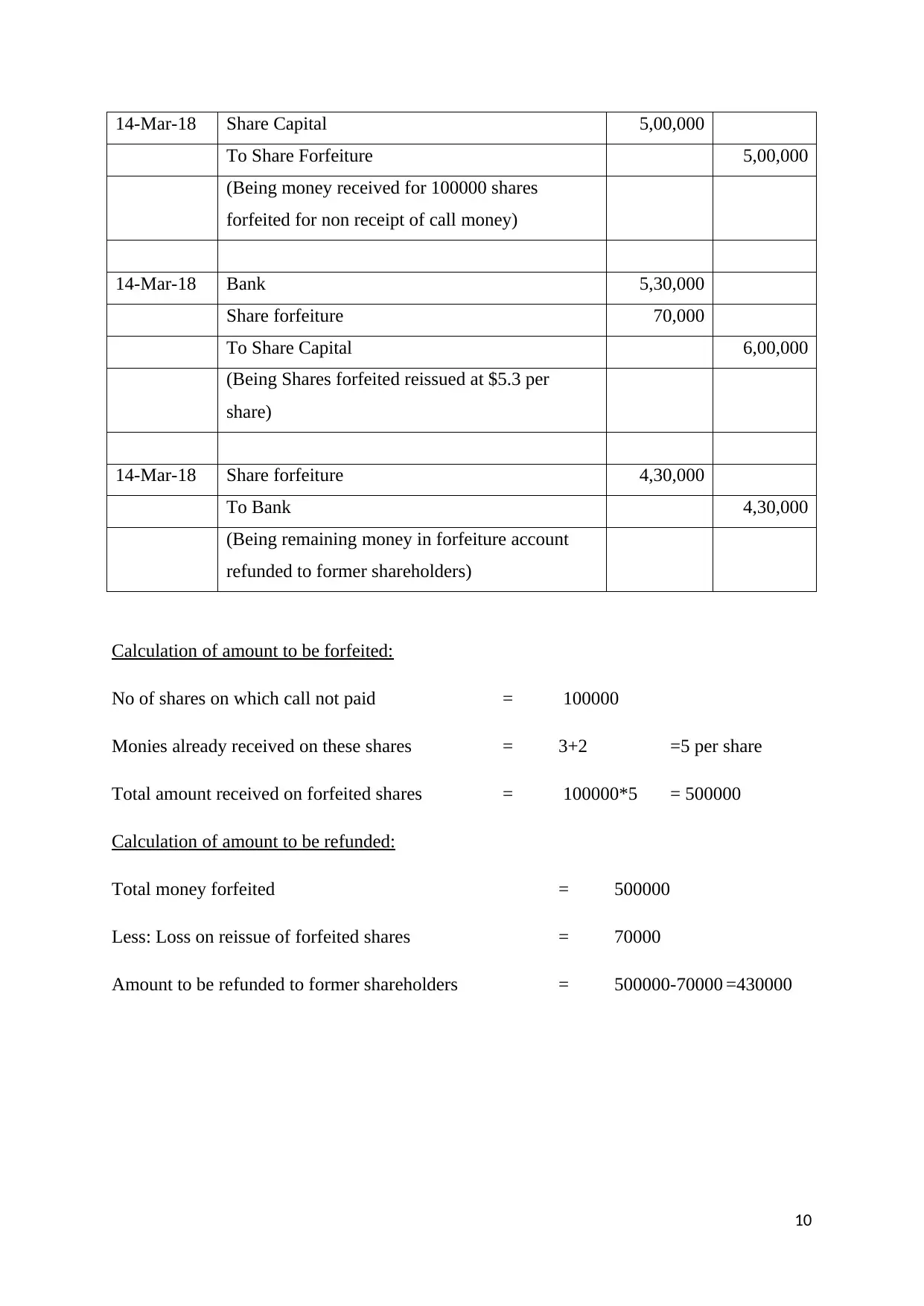

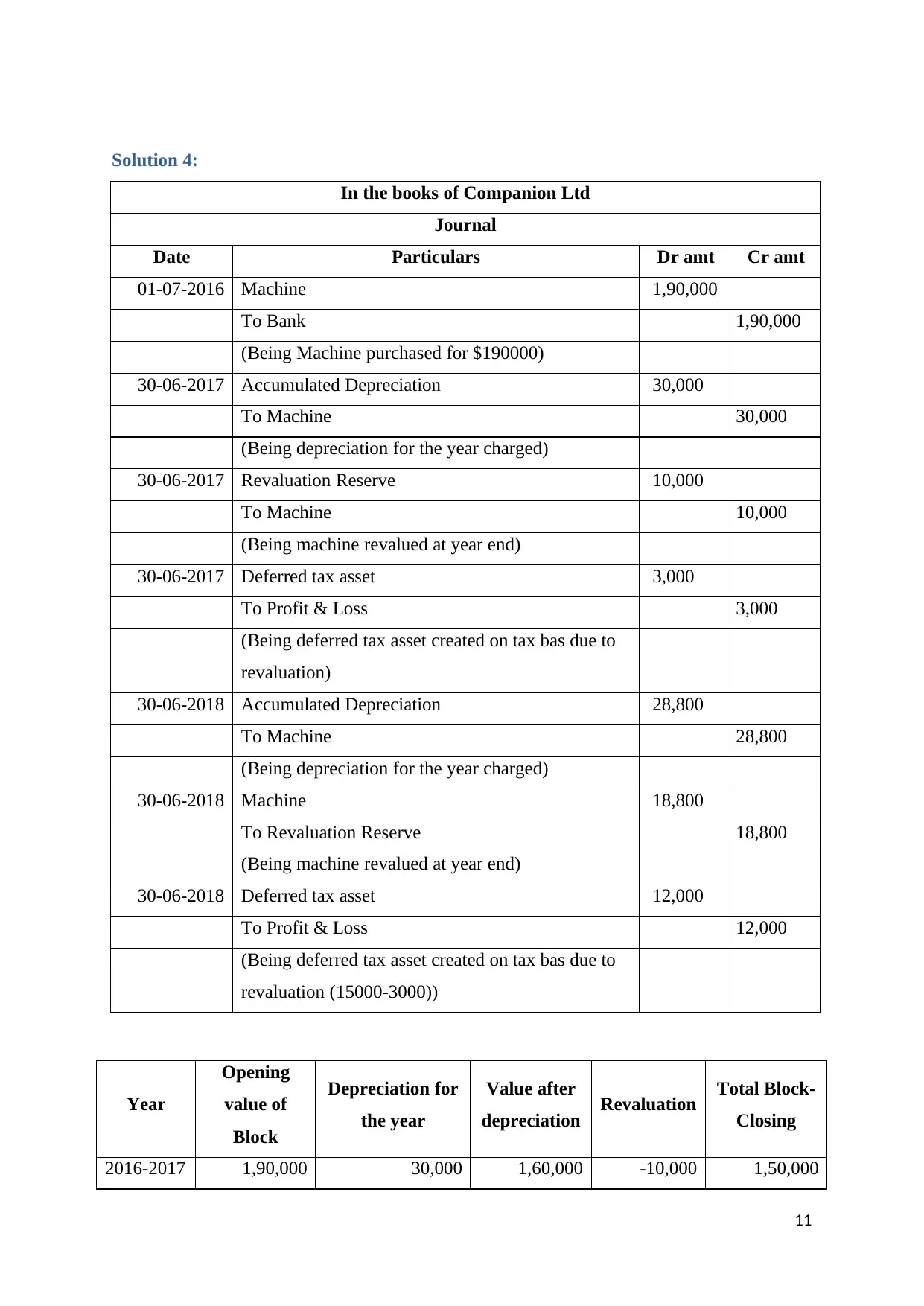

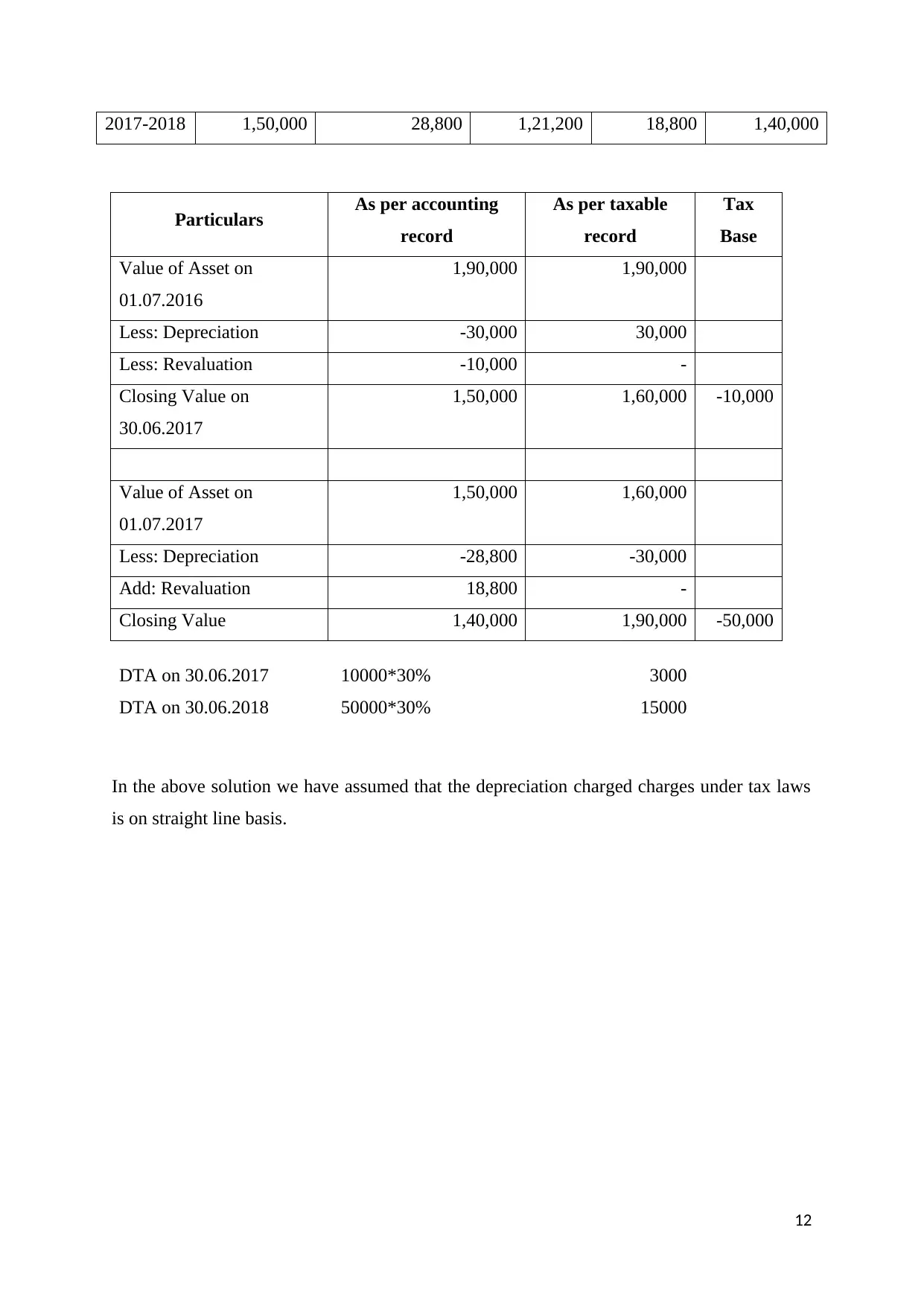

This document presents comprehensive solutions to an external reporting assignment. The solutions cover various aspects of financial reporting, starting with the preparation of a Statement of Profit or Loss and Other Comprehensive Income and a Statement of Changes in Equity for KLZR Limited, including detailed notes on administrative, selling, and other expenses, as well as earnings per share calculations. The assignment then addresses adjusting and non-adjusting events, providing a classification and treatment of events occurring between the balance sheet date and the signing date. Furthermore, the document includes journal entries for share capital transactions, such as share applications, allotments, and forfeitures, detailing the calculations involved. Finally, the assignment concludes with the preparation of journal entries and calculations related to machine revaluation, depreciation, and deferred tax assets, illustrating the accounting treatment of these items. This assignment provides a complete overview of external reporting principles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.