Financial Management and Control Report: ExxonMobil Analysis

VerifiedAdded on 2023/04/23

|22

|5909

|209

Report

AI Summary

This report provides a comprehensive financial analysis of ExxonMobil's performance, focusing on the years 2016 and 2017. Part A involves conducting a DuPont analysis and calculating various financial ratios, including Return on Owners' Equity (ROOE), margin ratios, turnover ratios, and gearing ratios, to assess the company's profitability, asset turnover, and leverage. The analysis reveals improvements in ROOE and financial stability. Part B critically evaluates the statement that debt is always cheaper than equity, examining the advantages and disadvantages of debt financing. Part C delves into project evaluation, including relevant cash flows and investment appraisal techniques, followed by an evaluation of the project's impact on the company's success. The report highlights the importance of financial analysis for informed decision-making and strategic planning.

Running head: FINANCIAL MANAGEMENT AND CONTROL

Financial Management and Control

Name of the Student:

Name of the University:

Authors Note:

Financial Management and Control

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT AND CONTROL

1

Table of Contents

Part A:........................................................................................................................................2

i) Conducting DuPont Analysis and Financial ratios for deriving the performance of the

organisation:...............................................................................................................................2

ii) Providing a report for the changes in profitability, asset turnover and leverage ratios:........4

Part B: Critically evaluating whether debt is always cheaper than equity so companies must

go for maximum debt to minimize their cost of capital.............................................................9

Part C:.......................................................................................................................................12

i) Providing relevant cash flows for the proposed project:......................................................12

ii) Calculating the investment appraisal techniques:................................................................13

iii) Critically evaluating the project evaluation decisions make or break of company:...........17

References and Bibliography:..................................................................................................19

1

Table of Contents

Part A:........................................................................................................................................2

i) Conducting DuPont Analysis and Financial ratios for deriving the performance of the

organisation:...............................................................................................................................2

ii) Providing a report for the changes in profitability, asset turnover and leverage ratios:........4

Part B: Critically evaluating whether debt is always cheaper than equity so companies must

go for maximum debt to minimize their cost of capital.............................................................9

Part C:.......................................................................................................................................12

i) Providing relevant cash flows for the proposed project:......................................................12

ii) Calculating the investment appraisal techniques:................................................................13

iii) Critically evaluating the project evaluation decisions make or break of company:...........17

References and Bibliography:..................................................................................................19

FINANCIAL MANAGEMENT AND CONTROL

2

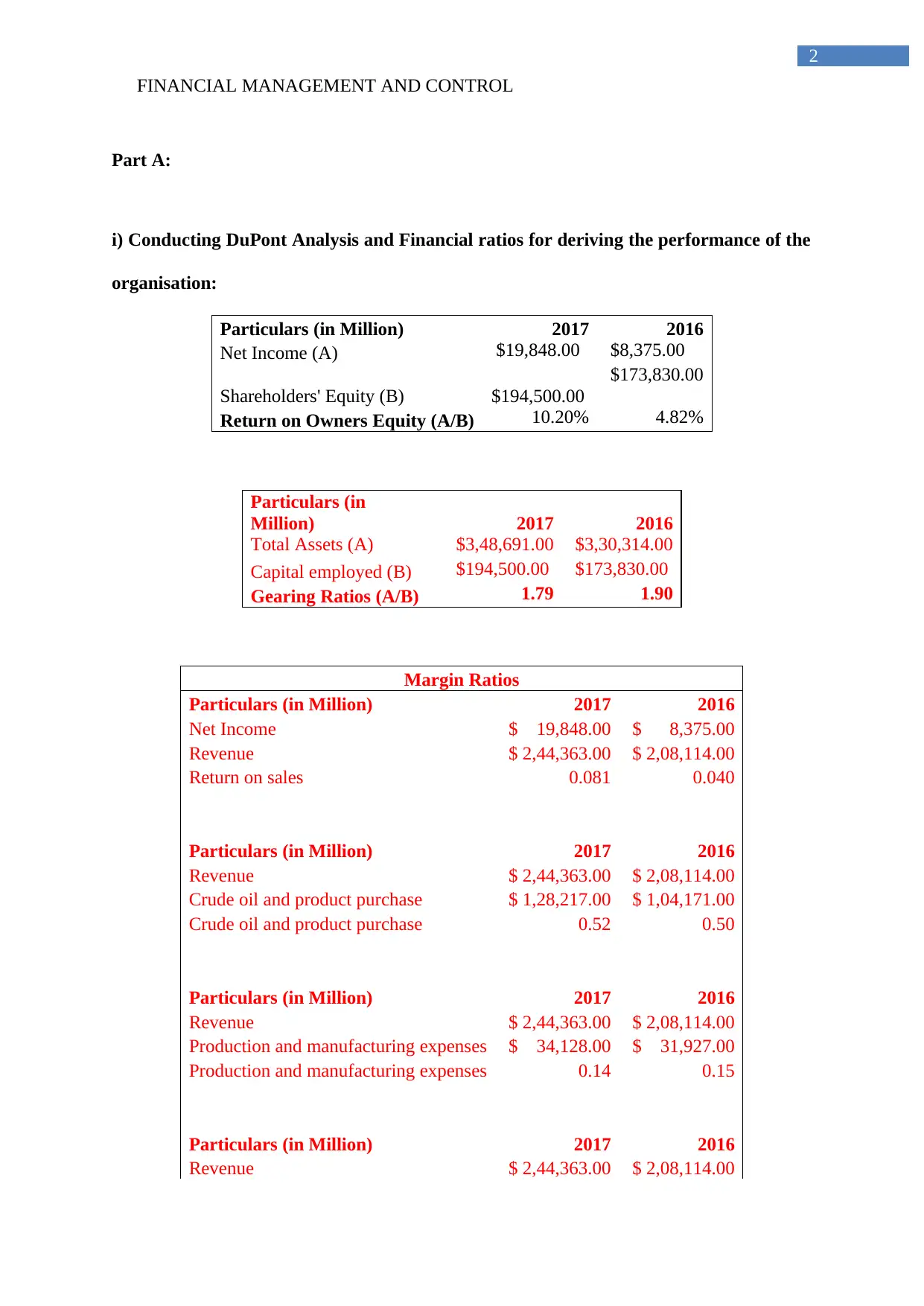

Part A:

i) Conducting DuPont Analysis and Financial ratios for deriving the performance of the

organisation:

Particulars (in Million) 2017 2016

Net Income (A) $19,848.00 $8,375.00

Shareholders' Equity (B) $194,500.00

$173,830.00

Return on Owners Equity (A/B) 10.20% 4.82%

Particulars (in

Million) 2017 2016

Total Assets (A) $3,48,691.00 $3,30,314.00

Capital employed (B) $194,500.00 $173,830.00

Gearing Ratios (A/B) 1.79 1.90

Margin Ratios

Particulars (in Million) 2017 2016

Net Income $ 19,848.00 $ 8,375.00

Revenue $ 2,44,363.00 $ 2,08,114.00

Return on sales 0.081 0.040

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Crude oil and product purchase $ 1,28,217.00 $ 1,04,171.00

Crude oil and product purchase 0.52 0.50

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Production and manufacturing expenses $ 34,128.00 $ 31,927.00

Production and manufacturing expenses 0.14 0.15

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

2

Part A:

i) Conducting DuPont Analysis and Financial ratios for deriving the performance of the

organisation:

Particulars (in Million) 2017 2016

Net Income (A) $19,848.00 $8,375.00

Shareholders' Equity (B) $194,500.00

$173,830.00

Return on Owners Equity (A/B) 10.20% 4.82%

Particulars (in

Million) 2017 2016

Total Assets (A) $3,48,691.00 $3,30,314.00

Capital employed (B) $194,500.00 $173,830.00

Gearing Ratios (A/B) 1.79 1.90

Margin Ratios

Particulars (in Million) 2017 2016

Net Income $ 19,848.00 $ 8,375.00

Revenue $ 2,44,363.00 $ 2,08,114.00

Return on sales 0.081 0.040

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Crude oil and product purchase $ 1,28,217.00 $ 1,04,171.00

Crude oil and product purchase 0.52 0.50

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Production and manufacturing expenses $ 34,128.00 $ 31,927.00

Production and manufacturing expenses 0.14 0.15

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT AND CONTROL

3

Depreciation and depletion 19893 22308

Depreciation and depletion 0.08 0.11

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Total expenses $ 2,25,689.00 $ 2,00,145.00

Total expenses 1.08 1.04

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Other taxes and duties $ 30,104.00 $ 29,020.00

Other taxes and duties 0.12 0.14

Turnover Ratios

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Total Assets (B) $ 348,691.00 $ 330,314.00

Asset turnover ratio (A/B) 0.70 0.63

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Non-current assets (B) $ 301,557.00 $ 288,898.00

Revenue to NCA (A/B) 0.81 0.72

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

PPE (B) $ 252,630.00 $ 244,224.00

Revenue to PPE (A/B) 0.97 0.85

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Investment (B) $ 39,160.00 $ 35,102.00

Revenue to investment (A/B) 6.24 5.93

Particulars (in Million) 2017 2016

Revenue $2,44,363.00 $2,08,114.00

3

Depreciation and depletion 19893 22308

Depreciation and depletion 0.08 0.11

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Total expenses $ 2,25,689.00 $ 2,00,145.00

Total expenses 1.08 1.04

Particulars (in Million) 2017 2016

Revenue $ 2,44,363.00 $ 2,08,114.00

Other taxes and duties $ 30,104.00 $ 29,020.00

Other taxes and duties 0.12 0.14

Turnover Ratios

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Total Assets (B) $ 348,691.00 $ 330,314.00

Asset turnover ratio (A/B) 0.70 0.63

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Non-current assets (B) $ 301,557.00 $ 288,898.00

Revenue to NCA (A/B) 0.81 0.72

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

PPE (B) $ 252,630.00 $ 244,224.00

Revenue to PPE (A/B) 0.97 0.85

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Investment (B) $ 39,160.00 $ 35,102.00

Revenue to investment (A/B) 6.24 5.93

Particulars (in Million) 2017 2016

Revenue $2,44,363.00 $2,08,114.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT AND CONTROL

4

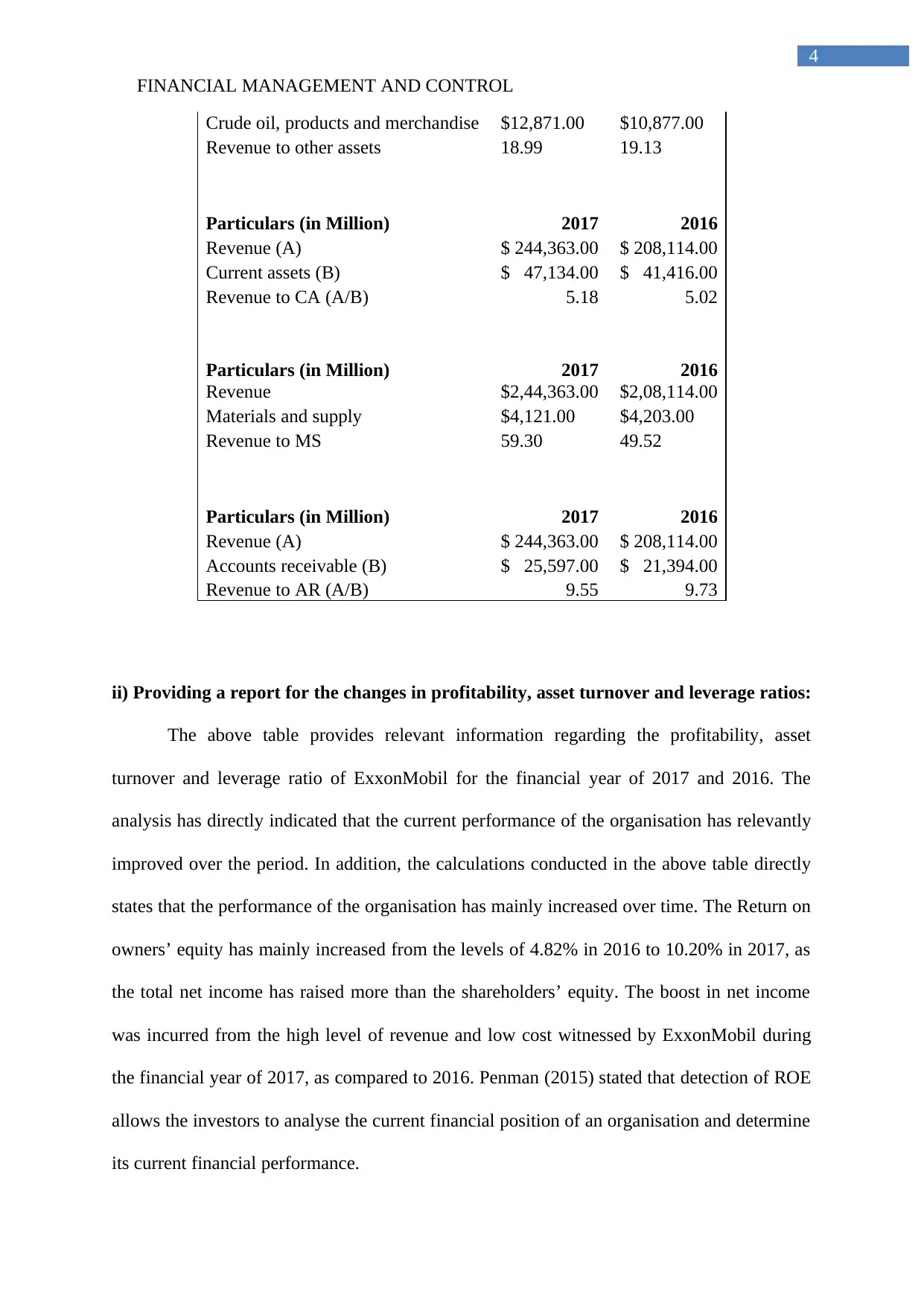

Crude oil, products and merchandise $12,871.00 $10,877.00

Revenue to other assets 18.99 19.13

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Current assets (B) $ 47,134.00 $ 41,416.00

Revenue to CA (A/B) 5.18 5.02

Particulars (in Million) 2017 2016

Revenue $2,44,363.00 $2,08,114.00

Materials and supply $4,121.00 $4,203.00

Revenue to MS 59.30 49.52

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Accounts receivable (B) $ 25,597.00 $ 21,394.00

Revenue to AR (A/B) 9.55 9.73

ii) Providing a report for the changes in profitability, asset turnover and leverage ratios:

The above table provides relevant information regarding the profitability, asset

turnover and leverage ratio of ExxonMobil for the financial year of 2017 and 2016. The

analysis has directly indicated that the current performance of the organisation has relevantly

improved over the period. In addition, the calculations conducted in the above table directly

states that the performance of the organisation has mainly increased over time. The Return on

owners’ equity has mainly increased from the levels of 4.82% in 2016 to 10.20% in 2017, as

the total net income has raised more than the shareholders’ equity. The boost in net income

was incurred from the high level of revenue and low cost witnessed by ExxonMobil during

the financial year of 2017, as compared to 2016. Penman (2015) stated that detection of ROE

allows the investors to analyse the current financial position of an organisation and determine

its current financial performance.

4

Crude oil, products and merchandise $12,871.00 $10,877.00

Revenue to other assets 18.99 19.13

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Current assets (B) $ 47,134.00 $ 41,416.00

Revenue to CA (A/B) 5.18 5.02

Particulars (in Million) 2017 2016

Revenue $2,44,363.00 $2,08,114.00

Materials and supply $4,121.00 $4,203.00

Revenue to MS 59.30 49.52

Particulars (in Million) 2017 2016

Revenue (A) $ 244,363.00 $ 208,114.00

Accounts receivable (B) $ 25,597.00 $ 21,394.00

Revenue to AR (A/B) 9.55 9.73

ii) Providing a report for the changes in profitability, asset turnover and leverage ratios:

The above table provides relevant information regarding the profitability, asset

turnover and leverage ratio of ExxonMobil for the financial year of 2017 and 2016. The

analysis has directly indicated that the current performance of the organisation has relevantly

improved over the period. In addition, the calculations conducted in the above table directly

states that the performance of the organisation has mainly increased over time. The Return on

owners’ equity has mainly increased from the levels of 4.82% in 2016 to 10.20% in 2017, as

the total net income has raised more than the shareholders’ equity. The boost in net income

was incurred from the high level of revenue and low cost witnessed by ExxonMobil during

the financial year of 2017, as compared to 2016. Penman (2015) stated that detection of ROE

allows the investors to analyse the current financial position of an organisation and determine

its current financial performance.

FINANCIAL MANAGEMENT AND CONTROL

5

The financial health of ExxonMobil can be detected the gearing ratio, which has

declined from the levels of 1.90% in 2016 to 1.79% in 2017. The decline in gearing ratios can

eventually help in detecting the level of financial stability, which has been witnessed by

ExxonMobil during the financial year of 2017. The decline in gearing ratio is due to the

reduction in long term debt and increment in the capital employed by the organisation.

Kanapickiene and Grundiene (2015) mentioned that reduction in debt accumulation directly

helps the organisation to minimise the occurrence of excessive interest payments, which

directly erodes the profits of an organisation. However, the current level of long-term debt is

adequate, where the organisation can accumulate more for supporting its long-term

objectives.

ROOE Return on Owner’s Equity is a profitability ratio, which helps to measure the

capability of the firm to generate surplus from its capital generated from

shareholder’s investment. The Return on Owner’s Equity of Exxon Mobil

have shown a very dramatic and drastic increase in the year 2017. The

ROOE of the company for the year 2016 was 4.82% and the same for the

year 2017 is 10.20%, which is an increase of more than 50% in a single

year. The increase in the ROOE of the company shows that the company

utilising the shareholder’s investment very efficiently and effectively to

generate income. The boom in the ROOE is mainly due the increased net

income, but at the same time a huge increase in shareholder equity has also

been noticed, which also helped the company to increase its quality of

operations. The company had access to invest in other and different due to

increased fund from shareholder and the extra investment helped the

company to generate more income.

Gearing Gearing ratio of a company is calculated to determine the net percentage

5

The financial health of ExxonMobil can be detected the gearing ratio, which has

declined from the levels of 1.90% in 2016 to 1.79% in 2017. The decline in gearing ratios can

eventually help in detecting the level of financial stability, which has been witnessed by

ExxonMobil during the financial year of 2017. The decline in gearing ratio is due to the

reduction in long term debt and increment in the capital employed by the organisation.

Kanapickiene and Grundiene (2015) mentioned that reduction in debt accumulation directly

helps the organisation to minimise the occurrence of excessive interest payments, which

directly erodes the profits of an organisation. However, the current level of long-term debt is

adequate, where the organisation can accumulate more for supporting its long-term

objectives.

ROOE Return on Owner’s Equity is a profitability ratio, which helps to measure the

capability of the firm to generate surplus from its capital generated from

shareholder’s investment. The Return on Owner’s Equity of Exxon Mobil

have shown a very dramatic and drastic increase in the year 2017. The

ROOE of the company for the year 2016 was 4.82% and the same for the

year 2017 is 10.20%, which is an increase of more than 50% in a single

year. The increase in the ROOE of the company shows that the company

utilising the shareholder’s investment very efficiently and effectively to

generate income. The boom in the ROOE is mainly due the increased net

income, but at the same time a huge increase in shareholder equity has also

been noticed, which also helped the company to increase its quality of

operations. The company had access to invest in other and different due to

increased fund from shareholder and the extra investment helped the

company to generate more income.

Gearing Gearing ratio of a company is calculated to determine the net percentage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT AND CONTROL

6

Ratios that reflects the amount of existing equity, which will be required by the

company to pay off company’s outstanding debts. The company’s gearing

ratio is calculated for two years, 2016 and 2017, and calculated by its long-

term liabilities of the particular year by the capital employed of that year.

The gearing ratio for 2016 is 1.90 and the same for 2017 is 1.79, which

shows that the gearing ratio has decreased. The main reason behind the

decrease is because the company have lessened debt financing, but increase

equity financing and as a result the company’s long-term liability decreased

and it also means that the company has more than sufficient equity capital to

pay out its outstanding debts.

Margin ratios Margin ratios are profitability ratios which are calculated to determine the

margins or requirement of revenue and other elements. In this case the

margin ratios that are used are return on sales, cost of single dollar of

revenue in general and cost of a single dollar of revenue (from research and

development, marketing, administration and general expenses).

Overall

The Return on sales of the company or the net income to revenue ratio have

hugely increased to more than 50% of that of last year, because the company

net income has an increase of $11,473 million, and the revenue also have

increased to approximately $36,249 million i.e. the sales have immensely

increased and thus return on sales increased. The company’s ability to

generate profit from sales is improved and very good.

Details

Revenue

The revenue of the company has immensely increased to approximately

6

Ratios that reflects the amount of existing equity, which will be required by the

company to pay off company’s outstanding debts. The company’s gearing

ratio is calculated for two years, 2016 and 2017, and calculated by its long-

term liabilities of the particular year by the capital employed of that year.

The gearing ratio for 2016 is 1.90 and the same for 2017 is 1.79, which

shows that the gearing ratio has decreased. The main reason behind the

decrease is because the company have lessened debt financing, but increase

equity financing and as a result the company’s long-term liability decreased

and it also means that the company has more than sufficient equity capital to

pay out its outstanding debts.

Margin ratios Margin ratios are profitability ratios which are calculated to determine the

margins or requirement of revenue and other elements. In this case the

margin ratios that are used are return on sales, cost of single dollar of

revenue in general and cost of a single dollar of revenue (from research and

development, marketing, administration and general expenses).

Overall

The Return on sales of the company or the net income to revenue ratio have

hugely increased to more than 50% of that of last year, because the company

net income has an increase of $11,473 million, and the revenue also have

increased to approximately $36,249 million i.e. the sales have immensely

increased and thus return on sales increased. The company’s ability to

generate profit from sales is improved and very good.

Details

Revenue

The revenue of the company has immensely increased to approximately

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT AND CONTROL

7

$36,249 million and due to this change the net income of the company have

also increased. The revenue of the company has a huge boom due to its

increase in sales, despite of increase in costs and expenses.

Expenses

Crude oil and product purchase:

The Crude oil and product purchase of revenue of the company have

increased, as in 2016, it was 0.50 and in 2017, it is 0.50. The slight

increment in the Crude oil and product purchase of revenue is due to

increase in oil prices.

Production and manufacturing expenses of the company have decreased up

to $2,201 m from that of 2016, and thus the cost of per dollar of revenue

with the Production and manufacturing expenses is also decreased from 0.15

to 0.14. The reason of the decrease of the ratio is majorly due to the

reduction in production expense.

The overall expenses in Depreciation, depletion, other taxes and duties have

mainly declined due to improvements in expenditure conditions of the

organisation.

Total expenses have inclined from 1.04 to 1.08 in 2017. This needs review

by management to examine why the total expenses have increased slightly

in 2017 over 2016.

Turnover ratio Overall

Per dollar of investment in total assets, revenue has declined / weakened

from 59 cents to 34 cents.

Details – Revenue to NCA

The decline in revenue to total NCA is $2.15 to $1.33. This is indicative of

7

$36,249 million and due to this change the net income of the company have

also increased. The revenue of the company has a huge boom due to its

increase in sales, despite of increase in costs and expenses.

Expenses

Crude oil and product purchase:

The Crude oil and product purchase of revenue of the company have

increased, as in 2016, it was 0.50 and in 2017, it is 0.50. The slight

increment in the Crude oil and product purchase of revenue is due to

increase in oil prices.

Production and manufacturing expenses of the company have decreased up

to $2,201 m from that of 2016, and thus the cost of per dollar of revenue

with the Production and manufacturing expenses is also decreased from 0.15

to 0.14. The reason of the decrease of the ratio is majorly due to the

reduction in production expense.

The overall expenses in Depreciation, depletion, other taxes and duties have

mainly declined due to improvements in expenditure conditions of the

organisation.

Total expenses have inclined from 1.04 to 1.08 in 2017. This needs review

by management to examine why the total expenses have increased slightly

in 2017 over 2016.

Turnover ratio Overall

Per dollar of investment in total assets, revenue has declined / weakened

from 59 cents to 34 cents.

Details – Revenue to NCA

The decline in revenue to total NCA is $2.15 to $1.33. This is indicative of

FINANCIAL MANAGEMENT AND CONTROL

8

underutilisation of NCA.

Even within the NCAs the decline is sharpest for revenue to goodwill and

intangible assets indicative of new acquisitions to provide immediate

synergy to existing business.

Details – Revenue to CA

Revenue earned per dollar of cash and marketable securities has declined

due to sharp increase in yearend balance of cash and marketable securities

for a cash rich company.

Increase in revenue to AR balance is indicative of a well-oiled collection

machinery which is on top of collection despite expansion.

Gearing Ratio Overall

Debt to equity ratio has declined marginally as asset expansion of $8772m

has been financed by a long-term debt of $1500m and fresh Equity of

$7410m.

Conclusion Decline in ROOE in 2017 is mainly due to poorer margin and lower

turnover in 2017 as compared to 2016.

Immediate management attention and intervention is required to boost

profitability and increase asset utilisation to improve its financial

performance and position.

Part B: Critically evaluating whether debt is always cheaper than equity so companies

must go for maximum debt to minimize their cost of capital

“Debt is always cheaper than equity so companies must go for maximum debt to

minimize their cost of capital”.

8

underutilisation of NCA.

Even within the NCAs the decline is sharpest for revenue to goodwill and

intangible assets indicative of new acquisitions to provide immediate

synergy to existing business.

Details – Revenue to CA

Revenue earned per dollar of cash and marketable securities has declined

due to sharp increase in yearend balance of cash and marketable securities

for a cash rich company.

Increase in revenue to AR balance is indicative of a well-oiled collection

machinery which is on top of collection despite expansion.

Gearing Ratio Overall

Debt to equity ratio has declined marginally as asset expansion of $8772m

has been financed by a long-term debt of $1500m and fresh Equity of

$7410m.

Conclusion Decline in ROOE in 2017 is mainly due to poorer margin and lower

turnover in 2017 as compared to 2016.

Immediate management attention and intervention is required to boost

profitability and increase asset utilisation to improve its financial

performance and position.

Part B: Critically evaluating whether debt is always cheaper than equity so companies

must go for maximum debt to minimize their cost of capital

“Debt is always cheaper than equity so companies must go for maximum debt to

minimize their cost of capital”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT AND CONTROL

9

The above statement states that for a company, debt financing is much cheaper and

beneficiary than issuing equity, in terms of reducing the cost of capital of the company. Debt

is a form of generating cash through borrowing amount from different parties, and borrowed

amount is known as debt (Pianeselli and Zaghini 2014). There are various types of debt

instruments used by companies to generate capital, out of which the main instruments are

corporate loans, bonds and debentures. On the other hand, Equity can be defined as the share

of capital that are issued for the public, which the public can purchase, in order to earn profit,

through dividend. In general, equity can be also defined as the difference between the value

of the liability and asset of something owned (Nguyen and Rugman 2015).

There are many merits and demerits of debt financing, evaluating which, the

preference of using debt over equity can be determined. The main advantages of debt

financing are- (i) in debt financing, it is not required to give up stake or share of the company,

but in some circumstances, it is only required to use a collateral for loan, where only the

ownership of the collateral may have to be give up, (ii) debt financing helps in retain control

on business, which means that the lender or lending institution, that lends the money have no

right to say how the money could be used in the business (Overesch and Wamser 2014), (iii)

in debt financing, the amount needed to pay back along the interest can be determined in

advance, which makes easier in preparing future business plans and also in preparing budget,

(iv) in debt financing, the interest payments are tax deductible i.e. the interest payments are

permitted as expense deductions against revenues to arrive at taxable income (Molly et al.

2018). Hence, it helps in lowering a company’s taxes, (v) using debt financing, additional

money is provided in the capital of the company, the additional profit earned by providing

additional capital is been shared among the shareholders or the company can keep the profit

and use it for other purpose (Jung, Herbohn and Clarkson 2018). There are also certain risks

involved in debt financing, which are as follows- (i) since, the company has to pay a fixed

9

The above statement states that for a company, debt financing is much cheaper and

beneficiary than issuing equity, in terms of reducing the cost of capital of the company. Debt

is a form of generating cash through borrowing amount from different parties, and borrowed

amount is known as debt (Pianeselli and Zaghini 2014). There are various types of debt

instruments used by companies to generate capital, out of which the main instruments are

corporate loans, bonds and debentures. On the other hand, Equity can be defined as the share

of capital that are issued for the public, which the public can purchase, in order to earn profit,

through dividend. In general, equity can be also defined as the difference between the value

of the liability and asset of something owned (Nguyen and Rugman 2015).

There are many merits and demerits of debt financing, evaluating which, the

preference of using debt over equity can be determined. The main advantages of debt

financing are- (i) in debt financing, it is not required to give up stake or share of the company,

but in some circumstances, it is only required to use a collateral for loan, where only the

ownership of the collateral may have to be give up, (ii) debt financing helps in retain control

on business, which means that the lender or lending institution, that lends the money have no

right to say how the money could be used in the business (Overesch and Wamser 2014), (iii)

in debt financing, the amount needed to pay back along the interest can be determined in

advance, which makes easier in preparing future business plans and also in preparing budget,

(iv) in debt financing, the interest payments are tax deductible i.e. the interest payments are

permitted as expense deductions against revenues to arrive at taxable income (Molly et al.

2018). Hence, it helps in lowering a company’s taxes, (v) using debt financing, additional

money is provided in the capital of the company, the additional profit earned by providing

additional capital is been shared among the shareholders or the company can keep the profit

and use it for other purpose (Jung, Herbohn and Clarkson 2018). There are also certain risks

involved in debt financing, which are as follows- (i) since, the company has to pay a fixed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT AND CONTROL

10

rate of interest on the fixed principle, within a fixed period of time, hence the firm feel

tremendous pressure of returning the borrowed amount, when the company generate

insufficient profit or losses, (ii) debt financing also develops financial risks, because the

company have to pay the interest and the principle amount at time, irrespective of whether the

company have generated profit or loss, which can also lead to bankruptcy of the

company(Yazdanfar and Ohman 2015).

Equity financing also has many advantages and disadvantages, considering which

company decides to use equity financing for capital generation. Most of the company uses

financing as the main source of generating capital, i.e. a company’s maximum capital is from

the shareholder’s equity, rather than from debt (Nguyen and Rugman 2015). Some of the

main advantages of equity is- (i) compared to debt financing or other financing, equity

financing has less burden of repayment of loan or interest, which helps the company in using

the earnings in growing the business, (ii) in equity financing, equity holders are the partners

of the business, which means the growth of the business is the growth of the shareholders,

hence some of the shareholders, who are more knowledgeable or well connected, provides

feedback and necessary suggestions to grow the business and by considering the suggestion

and feedback, the business can learn grow as well, (iii) the other main merit of the equity

financing is that, there is no issue in lacking of creditworthiness, because poor credit history

does not affect equity financing, rather increases the chance of equity financing got more

preferred than debt financing (Cimini et al. 2015). There are also some disadvantages of

equity financing, out of which the main disadvantage is that the company loses its optimum

control on the business, because the shareholders interfere in operations as owners of the

equity shares of the company. The other major disadvantage is that, due to sharing

ownership, there is a chance of conflicts, in case of any distinction between the vision of the

owner and vision of the management, and management style of running business. The equity

10

rate of interest on the fixed principle, within a fixed period of time, hence the firm feel

tremendous pressure of returning the borrowed amount, when the company generate

insufficient profit or losses, (ii) debt financing also develops financial risks, because the

company have to pay the interest and the principle amount at time, irrespective of whether the

company have generated profit or loss, which can also lead to bankruptcy of the

company(Yazdanfar and Ohman 2015).

Equity financing also has many advantages and disadvantages, considering which

company decides to use equity financing for capital generation. Most of the company uses

financing as the main source of generating capital, i.e. a company’s maximum capital is from

the shareholder’s equity, rather than from debt (Nguyen and Rugman 2015). Some of the

main advantages of equity is- (i) compared to debt financing or other financing, equity

financing has less burden of repayment of loan or interest, which helps the company in using

the earnings in growing the business, (ii) in equity financing, equity holders are the partners

of the business, which means the growth of the business is the growth of the shareholders,

hence some of the shareholders, who are more knowledgeable or well connected, provides

feedback and necessary suggestions to grow the business and by considering the suggestion

and feedback, the business can learn grow as well, (iii) the other main merit of the equity

financing is that, there is no issue in lacking of creditworthiness, because poor credit history

does not affect equity financing, rather increases the chance of equity financing got more

preferred than debt financing (Cimini et al. 2015). There are also some disadvantages of

equity financing, out of which the main disadvantage is that the company loses its optimum

control on the business, because the shareholders interfere in operations as owners of the

equity shares of the company. The other major disadvantage is that, due to sharing

ownership, there is a chance of conflicts, in case of any distinction between the vision of the

owner and vision of the management, and management style of running business. The equity

FINANCIAL MANAGEMENT AND CONTROL

11

financing is very costly, and very demanding and time consuming as compared to debt

financing, which may distract management focus from the core business activities (Cole and

Sokolyk 2018).

In the above discussions, it can be concluded that both the equity financing and debt

financing have its own strength and weaknesses, and due to the high risk in debt financing,

most of the business prefer equity financing over debt financing. If the risk was managed

properly, debt financing could be better option for capital generation than equity financing.

Debt financing is better than equity financing in reducing the cost of capital. Debt financing

is much cheaper than equity financing, because it helps in managing the cost of the business

by reducing cost (Pillai 2015). Debt financing helps in reduce cost, due to its following

features- (i) debt financing provides tax benefits to the firm, since the interest paid on debt

are tax deductible, unlike the dividends paid to the equity shareholders, (ii) in case of

bankruptcy of the company, the debt holders have the first right to claim the company’s

assets, before the shareholders and due to such limited risk, it is usually cheaper than equity

financing(Solomon 2016), (iii) since debt holders have a fixed rate of return, they cannot

claim or participate in the upside in earnings of the business, unlike shareholders. Debt

holders don’t charge extra interest or return, when company earns extra surplus (Chava

2014). Thus, it can be concluded that debt financing is cheaper than equity financing, and

hence it is also the better option in generating capital by reducing the cost of capital.

Part C:

i) Providing relevant cash flows for the proposed project:

The following table is the free cash flow statement of SENTO Corp prepared from the

data relevant to the proposed project:

11

financing is very costly, and very demanding and time consuming as compared to debt

financing, which may distract management focus from the core business activities (Cole and

Sokolyk 2018).

In the above discussions, it can be concluded that both the equity financing and debt

financing have its own strength and weaknesses, and due to the high risk in debt financing,

most of the business prefer equity financing over debt financing. If the risk was managed

properly, debt financing could be better option for capital generation than equity financing.

Debt financing is better than equity financing in reducing the cost of capital. Debt financing

is much cheaper than equity financing, because it helps in managing the cost of the business

by reducing cost (Pillai 2015). Debt financing helps in reduce cost, due to its following

features- (i) debt financing provides tax benefits to the firm, since the interest paid on debt

are tax deductible, unlike the dividends paid to the equity shareholders, (ii) in case of

bankruptcy of the company, the debt holders have the first right to claim the company’s

assets, before the shareholders and due to such limited risk, it is usually cheaper than equity

financing(Solomon 2016), (iii) since debt holders have a fixed rate of return, they cannot

claim or participate in the upside in earnings of the business, unlike shareholders. Debt

holders don’t charge extra interest or return, when company earns extra surplus (Chava

2014). Thus, it can be concluded that debt financing is cheaper than equity financing, and

hence it is also the better option in generating capital by reducing the cost of capital.

Part C:

i) Providing relevant cash flows for the proposed project:

The following table is the free cash flow statement of SENTO Corp prepared from the

data relevant to the proposed project:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.