Management Accounting Report: Eymen Ltd Financial Analysis

VerifiedAdded on 2021/02/21

|16

|4062

|96

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Eymen Ltd. It begins with an introduction to management accounting, highlighting its importance in providing financial information for managerial decision-making. The report explores various management accounting systems, including inventory management, cost accounting, price optimization, and job costing. It then examines different methods of management accounting reporting, such as budget reports, accounts receivable aging reports, job cost reports, and inventory reports, and their benefits. The analysis extends to evaluating how management accounting systems integrate within Eymen Ltd's processes. Furthermore, the report discusses planning tools used in management accounting, specifically benchmarking and cash flow budgeting, along with their respective advantages and disadvantages. The report includes completed calculations and analysis of company financial statements using variable costing, as well as a portfolio of completed calculations and analysis on company financial statements and income statements using variable costings. The report concludes with a discussion of the benefits of management accounting systems and their application within an organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

PART 1...................................................................................................................................3

A) Management accounting and requirements of different types of management accounting

systems...................................................................................................................................3

B) Methods used for management accounting reporting.......................................................4

C) Benefits of management accounting systems and its application within an organisation.5

D) Evaluation of the way management accounting systems and management accounting

reporting integrate within Eymen Ltd. processes...................................................................6

PART 2...................................................................................................................................7

Planning tools that are used in management accounting and its advantages and disadvantages 7

TASK 2............................................................................................................................................9

PART 1...................................................................................................................................9

Produce a portfolio of completed calculations and analysis on company financial statements

and income statements using variable costings......................................................................9

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

PART 1...................................................................................................................................3

A) Management accounting and requirements of different types of management accounting

systems...................................................................................................................................3

B) Methods used for management accounting reporting.......................................................4

C) Benefits of management accounting systems and its application within an organisation.5

D) Evaluation of the way management accounting systems and management accounting

reporting integrate within Eymen Ltd. processes...................................................................6

PART 2...................................................................................................................................7

Planning tools that are used in management accounting and its advantages and disadvantages 7

TASK 2............................................................................................................................................9

PART 1...................................................................................................................................9

Produce a portfolio of completed calculations and analysis on company financial statements

and income statements using variable costings......................................................................9

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is the procedure that helps the organisations to provide financial

information and resources to the manager so that manager can make a right use of the

information by analysing the same and making the right decision. (Bromwich and Scapens,

2016). This process basically includes collection, analyses and reporting information about the

different operation that are been conducted in the business. Present study will include the basic

needs of various types of management accounting systems and in the report various methods are

explained for the management accounting reporting. This report is based on the Eymen Ltd

company. Further, report calculates cost with the help of different techniques of cost analysis in

order to prepare an income statement with the use of marginal and absorption costs. Report will

also include advantages and disadvantages of planning tools that are used in budgetary control.

TASK 1

PART 1

A) Management accounting and requirements of different types of management accounting

systems

Management accounting is defined as a process in which financial information and

resources are provided to the manager so that manager can make a right decision. Generally

management accounting is used by the internal team of the organization, and this is the only

thing which makes it different from financial accounting. management accounting helps

financial information and resources are provided to the manager of the company so that these

information can be used by the managers for effective decision making process. This process

usually includes collection, analyses and reporting information with respect to the different

operation that are been conducted in the business.

Management accounting systems:-

Management accounting system is the internal systems which helps the company in

measuring and evaluating different processes that can help in managing business financially. In

these systems, financial information of the business are collected by the managers and then

report is been prepared for internal use of the managers in order to come up with appropriate

decisions in order to run the business smoothly.

The different types of management accounting systems are as follows:

Management accounting is the procedure that helps the organisations to provide financial

information and resources to the manager so that manager can make a right use of the

information by analysing the same and making the right decision. (Bromwich and Scapens,

2016). This process basically includes collection, analyses and reporting information about the

different operation that are been conducted in the business. Present study will include the basic

needs of various types of management accounting systems and in the report various methods are

explained for the management accounting reporting. This report is based on the Eymen Ltd

company. Further, report calculates cost with the help of different techniques of cost analysis in

order to prepare an income statement with the use of marginal and absorption costs. Report will

also include advantages and disadvantages of planning tools that are used in budgetary control.

TASK 1

PART 1

A) Management accounting and requirements of different types of management accounting

systems

Management accounting is defined as a process in which financial information and

resources are provided to the manager so that manager can make a right decision. Generally

management accounting is used by the internal team of the organization, and this is the only

thing which makes it different from financial accounting. management accounting helps

financial information and resources are provided to the manager of the company so that these

information can be used by the managers for effective decision making process. This process

usually includes collection, analyses and reporting information with respect to the different

operation that are been conducted in the business.

Management accounting systems:-

Management accounting system is the internal systems which helps the company in

measuring and evaluating different processes that can help in managing business financially. In

these systems, financial information of the business are collected by the managers and then

report is been prepared for internal use of the managers in order to come up with appropriate

decisions in order to run the business smoothly.

The different types of management accounting systems are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system:- As the name suggests it is an management accounting

system that specify placement of stocked good and processes in Eymen Ltd. (Ismail, Isa

and Mia, 2018). It involves processes that maintains stocked products that are assets of

company, raw material and finished products. These generally are placed at different

locations as part of supply network so that regular and planned course of production can

be there Cost Accounting system:- It is a management accounting system which helps the Eymen

Ltd in ascertaining the cost involved in a product or process to evaluate organisation’s

profitability. This management accounting tool is used to estimate the cost related to

products so that they can analyse profitability of the business and also inventory

valuation. It is basically used by manufactures of the business in order to record the

different production activities by using inventory system. Price Optimization System:- It is mathematical analysis that Eymen Ltd uses in order to

determine customers respond at different prices for its offerings with the use of different

channels. This system is used in an organisation to ensure that their products are sell

quickly by satisfying the customers with respect to prices of product.

Job Costing System:- Job costing system is used by the managers in Eymen Ltd to assign

and accumulate the cost related to manufacturing of individual unit of output. It is

basically used in the situation where items produced generally differs and have a

significant cost (Bromwich and Scapens, 2016).

B) Methods used for management accounting reporting

Management accounting reporting is generally used by the managers in order to monitor

the performance of the Eymen Ltd. These reports are required quarterly, monthly, weekly and

even for daily purposes. Different methods that are used for management accounting reports are

as follows:- Budget report:- Budget report is the tool in which the actual result is a comparison of the

actual result with the actually setup budget of the company. This report is used by t

Eymen Ltd to analyse company's performance. The estimated budget is based on the

actual expenses from the previous years and if the company had over budget than future

years may required to have increased budget. Mangers of the firm use some of the funds

system that specify placement of stocked good and processes in Eymen Ltd. (Ismail, Isa

and Mia, 2018). It involves processes that maintains stocked products that are assets of

company, raw material and finished products. These generally are placed at different

locations as part of supply network so that regular and planned course of production can

be there Cost Accounting system:- It is a management accounting system which helps the Eymen

Ltd in ascertaining the cost involved in a product or process to evaluate organisation’s

profitability. This management accounting tool is used to estimate the cost related to

products so that they can analyse profitability of the business and also inventory

valuation. It is basically used by manufactures of the business in order to record the

different production activities by using inventory system. Price Optimization System:- It is mathematical analysis that Eymen Ltd uses in order to

determine customers respond at different prices for its offerings with the use of different

channels. This system is used in an organisation to ensure that their products are sell

quickly by satisfying the customers with respect to prices of product.

Job Costing System:- Job costing system is used by the managers in Eymen Ltd to assign

and accumulate the cost related to manufacturing of individual unit of output. It is

basically used in the situation where items produced generally differs and have a

significant cost (Bromwich and Scapens, 2016).

B) Methods used for management accounting reporting

Management accounting reporting is generally used by the managers in order to monitor

the performance of the Eymen Ltd. These reports are required quarterly, monthly, weekly and

even for daily purposes. Different methods that are used for management accounting reports are

as follows:- Budget report:- Budget report is the tool in which the actual result is a comparison of the

actual result with the actually setup budget of the company. This report is used by t

Eymen Ltd to analyse company's performance. The estimated budget is based on the

actual expenses from the previous years and if the company had over budget than future

years may required to have increased budget. Mangers of the firm use some of the funds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from budget to give employees bonus in order to motivate them for some financial goals

of the business (Maas, Schaltegger and Crutzen, 2016). Accounts Receivable aging reports:- This tool is used for managing cash flow for the

Eymen Ltd for extending the credit of their potential customers. Managers basically uses

this report in order to analyse the problems that company usually face related to

collection process. There are some cases when customers do not pay their balances, in

such situations company tighten its credit policies in order to overcome these issues. The

analyse the accounts receivable aging at the end of financial year. Job Cost reports:- Job cost report are the process of coding and allocating project

expenses to track financial efficiency and profitability These reports are used by the

managers of Eymen ltd. to analyse the expenses related to specific project. In order to

evaluate profitability of the business, this report is matched with the estimated revenue as

this helps in identifying higher earning areas for the firm and firm can put its efforts for

high profit margins.

Inventory and manufacturing- Eymen ltd basically uses these reports to make the

manufacturing process of the business more efficient. Report includes inventory waste,

hourly labour costs and overhead cost and these helps the company to make comparison

between different assembly lines in order to improve them. This also helps in analysing

the best performing departments so that they can be offered bonuses in order to motivate

them to keep their performance high.

C) Benefits of management accounting systems and its application within an organisation

Management accounting is having following benefits within organisation context:- Formulation of financial strategies:- Financial strategies will help Eymen ltd in

formulating with the different management accounting systems by the managers and they

can use sales forecasts and budgets and also job costing techniques for the organisation.

Financial statements will help the Eymen ltd in incorporating different data of the

company so that different strategies can be developed in order to enhance net profit and

gross income of the firm. Accounts managers can use these methods for implementing

financial strategies in planning for operating cost reduction. This helps the company to

reach out its goals in an effective manner (Aduda and Ndaita, 2017).

of the business (Maas, Schaltegger and Crutzen, 2016). Accounts Receivable aging reports:- This tool is used for managing cash flow for the

Eymen Ltd for extending the credit of their potential customers. Managers basically uses

this report in order to analyse the problems that company usually face related to

collection process. There are some cases when customers do not pay their balances, in

such situations company tighten its credit policies in order to overcome these issues. The

analyse the accounts receivable aging at the end of financial year. Job Cost reports:- Job cost report are the process of coding and allocating project

expenses to track financial efficiency and profitability These reports are used by the

managers of Eymen ltd. to analyse the expenses related to specific project. In order to

evaluate profitability of the business, this report is matched with the estimated revenue as

this helps in identifying higher earning areas for the firm and firm can put its efforts for

high profit margins.

Inventory and manufacturing- Eymen ltd basically uses these reports to make the

manufacturing process of the business more efficient. Report includes inventory waste,

hourly labour costs and overhead cost and these helps the company to make comparison

between different assembly lines in order to improve them. This also helps in analysing

the best performing departments so that they can be offered bonuses in order to motivate

them to keep their performance high.

C) Benefits of management accounting systems and its application within an organisation

Management accounting is having following benefits within organisation context:- Formulation of financial strategies:- Financial strategies will help Eymen ltd in

formulating with the different management accounting systems by the managers and they

can use sales forecasts and budgets and also job costing techniques for the organisation.

Financial statements will help the Eymen ltd in incorporating different data of the

company so that different strategies can be developed in order to enhance net profit and

gross income of the firm. Accounts managers can use these methods for implementing

financial strategies in planning for operating cost reduction. This helps the company to

reach out its goals in an effective manner (Aduda and Ndaita, 2017).

Financial outcomes of decisions are explained with the use of accounting systems:-

Managers of Eymen ltd uses these management accounting systems to understand the

respective debt and equity related to firm and they analyse the different consequences of

adding debt and equity. These systems play an important role in understanding and

deriving the impacts of different decisions they are making over budgets and financial

statements of Eymen Ltd. Profits and losses of the company depends on the management

accounting systems used by Eymen Ltd. for decision making. It helps in Monitoring Expenses:- The major role of this system is to create budgets for

the firm that is flexible for the business. For the same managers of Eymen ltd can

prepares reports on daily bases, monthly and also yearly as it will helps them to

understand what are the requirements and they are able to monitor the expenses that

business operations will be in need.

Maintains the profitability of the business:- Management accounting system use different

tools in order to keep organisation's profitability high and for the same as they uses break

even analysis. It is used by the management accountant of a Eymen ltd as it is helpful for

categorising production costs between variable and fixed. It also determines production

level of the company and also sales as they affect profitability of the business (Malmi,

2016). They also analyse direct and indirect cost related to manufacturing in the business.

D) Evaluation of the way management accounting systems and management accounting

reporting integrate within Eymen Ltd. processes

The integration between organisational processes and budgeting report makes a path for

organisation activities so that they reach targets in better way. Activities of the company directs

towards the cost achievement as it makes the pricing strategies easier and integration between the

report and companies activities helps the managers to plan for future production (Maas,

Schaltegger and Crutzen, 2016).

Integration of these systems with the organisation process is important. Back office

system and Inventory integration have to be flexible enough and also transparent. The reason is

that business processes may require adjustments to the integration for continuous changes.

Management accounting system usually contributes in continuous improvement in an

organisation with integration of cost accounting system. In these ways management accounting

systems and management accounting reporting integrate within organisational processes.

Managers of Eymen ltd uses these management accounting systems to understand the

respective debt and equity related to firm and they analyse the different consequences of

adding debt and equity. These systems play an important role in understanding and

deriving the impacts of different decisions they are making over budgets and financial

statements of Eymen Ltd. Profits and losses of the company depends on the management

accounting systems used by Eymen Ltd. for decision making. It helps in Monitoring Expenses:- The major role of this system is to create budgets for

the firm that is flexible for the business. For the same managers of Eymen ltd can

prepares reports on daily bases, monthly and also yearly as it will helps them to

understand what are the requirements and they are able to monitor the expenses that

business operations will be in need.

Maintains the profitability of the business:- Management accounting system use different

tools in order to keep organisation's profitability high and for the same as they uses break

even analysis. It is used by the management accountant of a Eymen ltd as it is helpful for

categorising production costs between variable and fixed. It also determines production

level of the company and also sales as they affect profitability of the business (Malmi,

2016). They also analyse direct and indirect cost related to manufacturing in the business.

D) Evaluation of the way management accounting systems and management accounting

reporting integrate within Eymen Ltd. processes

The integration between organisational processes and budgeting report makes a path for

organisation activities so that they reach targets in better way. Activities of the company directs

towards the cost achievement as it makes the pricing strategies easier and integration between the

report and companies activities helps the managers to plan for future production (Maas,

Schaltegger and Crutzen, 2016).

Integration of these systems with the organisation process is important. Back office

system and Inventory integration have to be flexible enough and also transparent. The reason is

that business processes may require adjustments to the integration for continuous changes.

Management accounting system usually contributes in continuous improvement in an

organisation with integration of cost accounting system. In these ways management accounting

systems and management accounting reporting integrate within organisational processes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2

Planning tools that are used in management accounting and its advantages and disadvantages

The different planning tools are as follows:-

Benchmarking:

It is one of the common internal system which is used by the Eymen ltd as it includes

comparing the policies, procedure, product or process of the company on the basis of the already

set standard of the measurement. Benchmarking system of management generally starts with

setting up of a standard which need to be achieved by the organization and comparing the actual

performance of the company with already set measurement (Parmenter, 2015). Outcome of the

benchmarking system helps the organization in the reviewing the actual performance of the

management and also in identifying the opportunities for improvement. There are generally two

type of the benchmarking i.e. internal benchmarking in which the standard are set up on the basis

of the company past performance and other one is the external benchmarking in which

companies used to compare the actual performance with the performance of other companies in

the industry. This technique is generally used to overcome the problem of the competitiveness in

the market and also to improve the productivity of an organization. This planning tool basically

helps in increasing the competitive nature of different companies that are working in the same

field (Larkin and et.al., 2015).

Advantages:-

It helps in implementing creative ideas for the overall development of the organisation.

Increased competition helps company to maintain their position for running a successful

business.

It helps the company to get aware about the activities that are essential for improving the

profits of the organisation.

Disadvantages:-

Instead of incorporating other company's ideas, it can check its feasibility in their own

company.

Here, company usually have to keep an eye on their competition instead of their own

growth (Benchmarking, 2019).

Planning tools that are used in management accounting and its advantages and disadvantages

The different planning tools are as follows:-

Benchmarking:

It is one of the common internal system which is used by the Eymen ltd as it includes

comparing the policies, procedure, product or process of the company on the basis of the already

set standard of the measurement. Benchmarking system of management generally starts with

setting up of a standard which need to be achieved by the organization and comparing the actual

performance of the company with already set measurement (Parmenter, 2015). Outcome of the

benchmarking system helps the organization in the reviewing the actual performance of the

management and also in identifying the opportunities for improvement. There are generally two

type of the benchmarking i.e. internal benchmarking in which the standard are set up on the basis

of the company past performance and other one is the external benchmarking in which

companies used to compare the actual performance with the performance of other companies in

the industry. This technique is generally used to overcome the problem of the competitiveness in

the market and also to improve the productivity of an organization. This planning tool basically

helps in increasing the competitive nature of different companies that are working in the same

field (Larkin and et.al., 2015).

Advantages:-

It helps in implementing creative ideas for the overall development of the organisation.

Increased competition helps company to maintain their position for running a successful

business.

It helps the company to get aware about the activities that are essential for improving the

profits of the organisation.

Disadvantages:-

Instead of incorporating other company's ideas, it can check its feasibility in their own

company.

Here, company usually have to keep an eye on their competition instead of their own

growth (Benchmarking, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increased in dependency is seen and instead of depending on other company have built

their own networks in order to make them independent for better future.

Conclusion

This is one of the best technique as it helps the company in keeping eye on both internal and

external environment at a time as it sees the growth of the company and competitor growth both

together which can help company in getting competitive advantage.

Cash flow budgeting:-

A cash flow budget is an estimate of all cash receipts and all cash expenditures that are

expected to occur during a certain time period. In this budgeting Eye men ltd used to Estimates

monthly, bimonthly, or quarterly, and can include non farm income and expenditures as well as

farm items. It is an estimate of cash receipt and expenditures that are expected to occur at certain

period of time. These estimates can be made monthly, bimonthly or quarterly.

Advantages:-

It helps in avoiding debt as some amount of cash is set aside for the emergency situation.

Many a times company face emergency situation that can be overcome with its use.

It became easy for the company to identify cash deficits as it determines if the company

is having enough cash in order to meet the obligations (Reichard and Van Helden, 2016).

Company is able to communicate its financial position and it became easy for the

managers to determine the current and future issues that are needed to be addressed.

Disadvantages:-

It usually creates a situation of theft as cash is one of the easiest asset to steal and it is

tough to trace cash in an big organisation as flow of cash is high in them.

It may limit the amount of debt that company creates for its business.

It forces cost to become the primary factor in making decisions.

Conclusion

This technique is good but not that proficient as compare to the other as this technique includes

assumption before hand itself which can prove difficult for the manager to assumption the

expenditure before hand itself. Wrong assumption sometime creates the situation of the wrong

result for the organization.

Break-even analysis:-

their own networks in order to make them independent for better future.

Conclusion

This is one of the best technique as it helps the company in keeping eye on both internal and

external environment at a time as it sees the growth of the company and competitor growth both

together which can help company in getting competitive advantage.

Cash flow budgeting:-

A cash flow budget is an estimate of all cash receipts and all cash expenditures that are

expected to occur during a certain time period. In this budgeting Eye men ltd used to Estimates

monthly, bimonthly, or quarterly, and can include non farm income and expenditures as well as

farm items. It is an estimate of cash receipt and expenditures that are expected to occur at certain

period of time. These estimates can be made monthly, bimonthly or quarterly.

Advantages:-

It helps in avoiding debt as some amount of cash is set aside for the emergency situation.

Many a times company face emergency situation that can be overcome with its use.

It became easy for the company to identify cash deficits as it determines if the company

is having enough cash in order to meet the obligations (Reichard and Van Helden, 2016).

Company is able to communicate its financial position and it became easy for the

managers to determine the current and future issues that are needed to be addressed.

Disadvantages:-

It usually creates a situation of theft as cash is one of the easiest asset to steal and it is

tough to trace cash in an big organisation as flow of cash is high in them.

It may limit the amount of debt that company creates for its business.

It forces cost to become the primary factor in making decisions.

Conclusion

This technique is good but not that proficient as compare to the other as this technique includes

assumption before hand itself which can prove difficult for the manager to assumption the

expenditure before hand itself. Wrong assumption sometime creates the situation of the wrong

result for the organization.

Break-even analysis:-

Break-even analysis is a technique widely used by production management and

management accountants in the Eymen ltd. It is based on categorising production costs between

those which are "variable" (costs that change when the production output changes) and those that

are "fixed" (costs not directly related to the volume of production). It is the relationship between

the cost volume and profits that is represented for the different levels of the activity. It emphasis

is placed on the break even point where business neither receives profit nor a loss.

Advantages:-

It helps in measuring profit and losses with respect to production and sales of the

business.

It is easy to analyse effect of different changes in the sales prices of products (Morano

and Tajani, 2017).

It become easy to analyse relationship between variable and fixed cost.

Disadvantages:-

Its assumption is that there is constant sales price at all output level and that's not true at

all.

Another assumption is that production and sales do not differ.

Preparing the break even chart is time consuming(Reichard and Van Helden, 2016).

Conclusion

This technique is also a good technique in measurement but this technique also used to depend

on the assumption of the sales price but on the same end it is one of the best technique to

measure the production of the business.

TASK 2

PART 1

Produce a portfolio of completed calculations and analysis on company financial statements and

income statements using variable costings.

Marginal Costing Techniques: It is that technique in which variable cost of product is

charged to the unit cost and at the other side fixed cost for the period is completely written off

against the contribution. This term implies that the rate of change related to cost of Eymen ltd .

due to increase in its production level of the product by one unit.

management accountants in the Eymen ltd. It is based on categorising production costs between

those which are "variable" (costs that change when the production output changes) and those that

are "fixed" (costs not directly related to the volume of production). It is the relationship between

the cost volume and profits that is represented for the different levels of the activity. It emphasis

is placed on the break even point where business neither receives profit nor a loss.

Advantages:-

It helps in measuring profit and losses with respect to production and sales of the

business.

It is easy to analyse effect of different changes in the sales prices of products (Morano

and Tajani, 2017).

It become easy to analyse relationship between variable and fixed cost.

Disadvantages:-

Its assumption is that there is constant sales price at all output level and that's not true at

all.

Another assumption is that production and sales do not differ.

Preparing the break even chart is time consuming(Reichard and Van Helden, 2016).

Conclusion

This technique is also a good technique in measurement but this technique also used to depend

on the assumption of the sales price but on the same end it is one of the best technique to

measure the production of the business.

TASK 2

PART 1

Produce a portfolio of completed calculations and analysis on company financial statements and

income statements using variable costings.

Marginal Costing Techniques: It is that technique in which variable cost of product is

charged to the unit cost and at the other side fixed cost for the period is completely written off

against the contribution. This term implies that the rate of change related to cost of Eymen ltd .

due to increase in its production level of the product by one unit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption Costing Techniques: Absorption Costing is a managerial accounting cost

method in which all the respective manufacturing cost associated with a production process are

accumulated together. This type of cost is generally used to create an inventory valuation. Key

component of Absorption cost are Direct Material, Direct Labour, Variable Manufacturing and

Fixed manufacturing.

Marginal costing

May

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 400000 10.5 4200000

Less: variable cost

Direct materials: 400000 1.375 550000

Direct labour 400000 1.88 750000

Total variable cost 1300000

Contribution 2900000

Less: fixed overheads 600000

Net profit 2300000

June

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 360000 10.5 3780000

Less: COGS

Opening stock 0 0 0

Purchases 400000 3.25 1300000

Closing stock 40000 3.25 130000

COGS 1170000

Contribution /GP 2610000

Less: fixed overheads 600000

method in which all the respective manufacturing cost associated with a production process are

accumulated together. This type of cost is generally used to create an inventory valuation. Key

component of Absorption cost are Direct Material, Direct Labour, Variable Manufacturing and

Fixed manufacturing.

Marginal costing

May

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 400000 10.5 4200000

Less: variable cost

Direct materials: 400000 1.375 550000

Direct labour 400000 1.88 750000

Total variable cost 1300000

Contribution 2900000

Less: fixed overheads 600000

Net profit 2300000

June

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 360000 10.5 3780000

Less: COGS

Opening stock 0 0 0

Purchases 400000 3.25 1300000

Closing stock 40000 3.25 130000

COGS 1170000

Contribution /GP 2610000

Less: fixed overheads 600000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

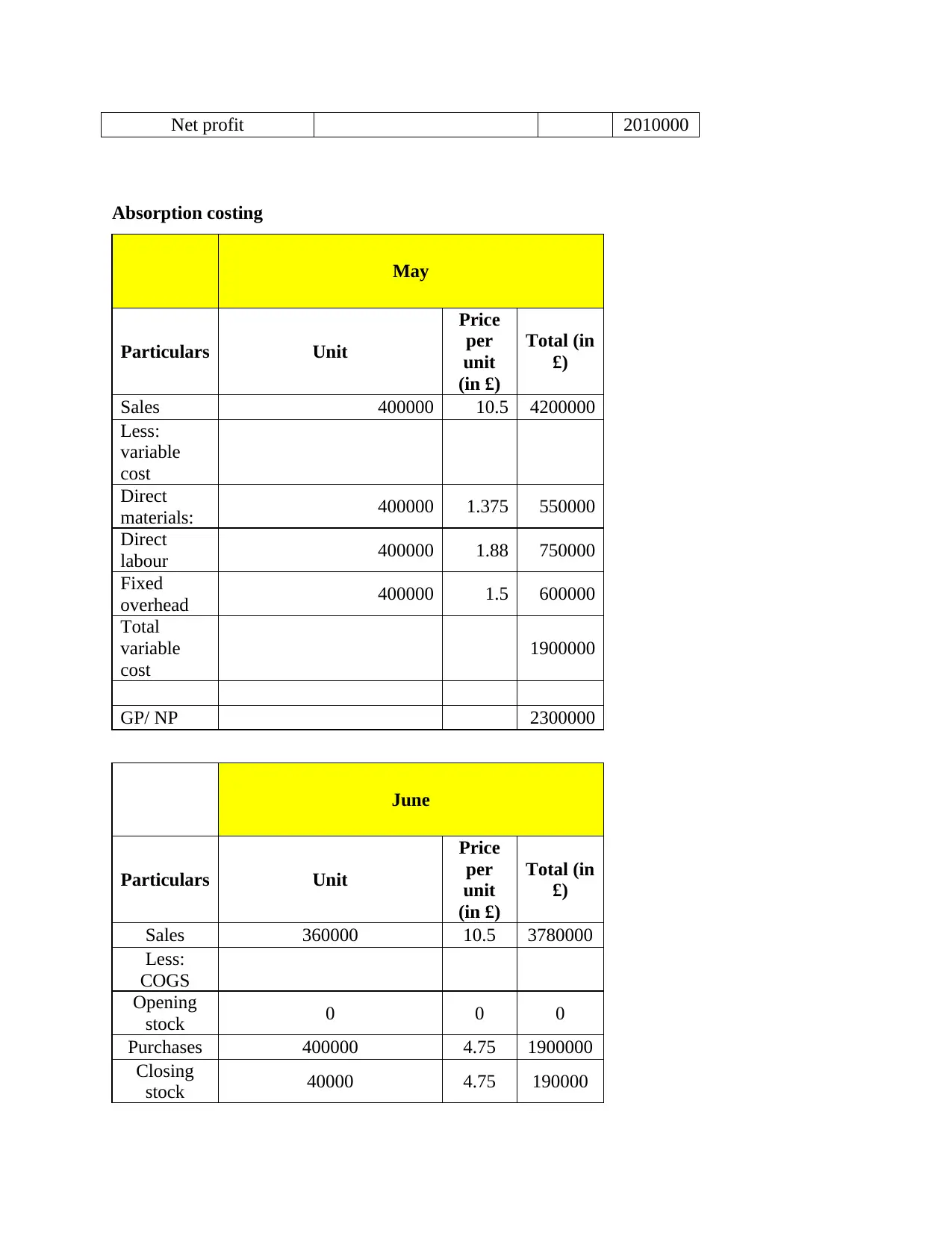

Net profit 2010000

Absorption costing

May

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 400000 10.5 4200000

Less:

variable

cost

Direct

materials: 400000 1.375 550000

Direct

labour 400000 1.88 750000

Fixed

overhead 400000 1.5 600000

Total

variable

cost

1900000

GP/ NP 2300000

June

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 360000 10.5 3780000

Less:

COGS

Opening

stock 0 0 0

Purchases 400000 4.75 1900000

Closing

stock 40000 4.75 190000

Absorption costing

May

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 400000 10.5 4200000

Less:

variable

cost

Direct

materials: 400000 1.375 550000

Direct

labour 400000 1.88 750000

Fixed

overhead 400000 1.5 600000

Total

variable

cost

1900000

GP/ NP 2300000

June

Particulars Unit

Price

per

unit

(in £)

Total (in

£)

Sales 360000 10.5 3780000

Less:

COGS

Opening

stock 0 0 0

Purchases 400000 4.75 1900000

Closing

stock 40000 4.75 190000

COGS 1710000

GP/ NP 2070000

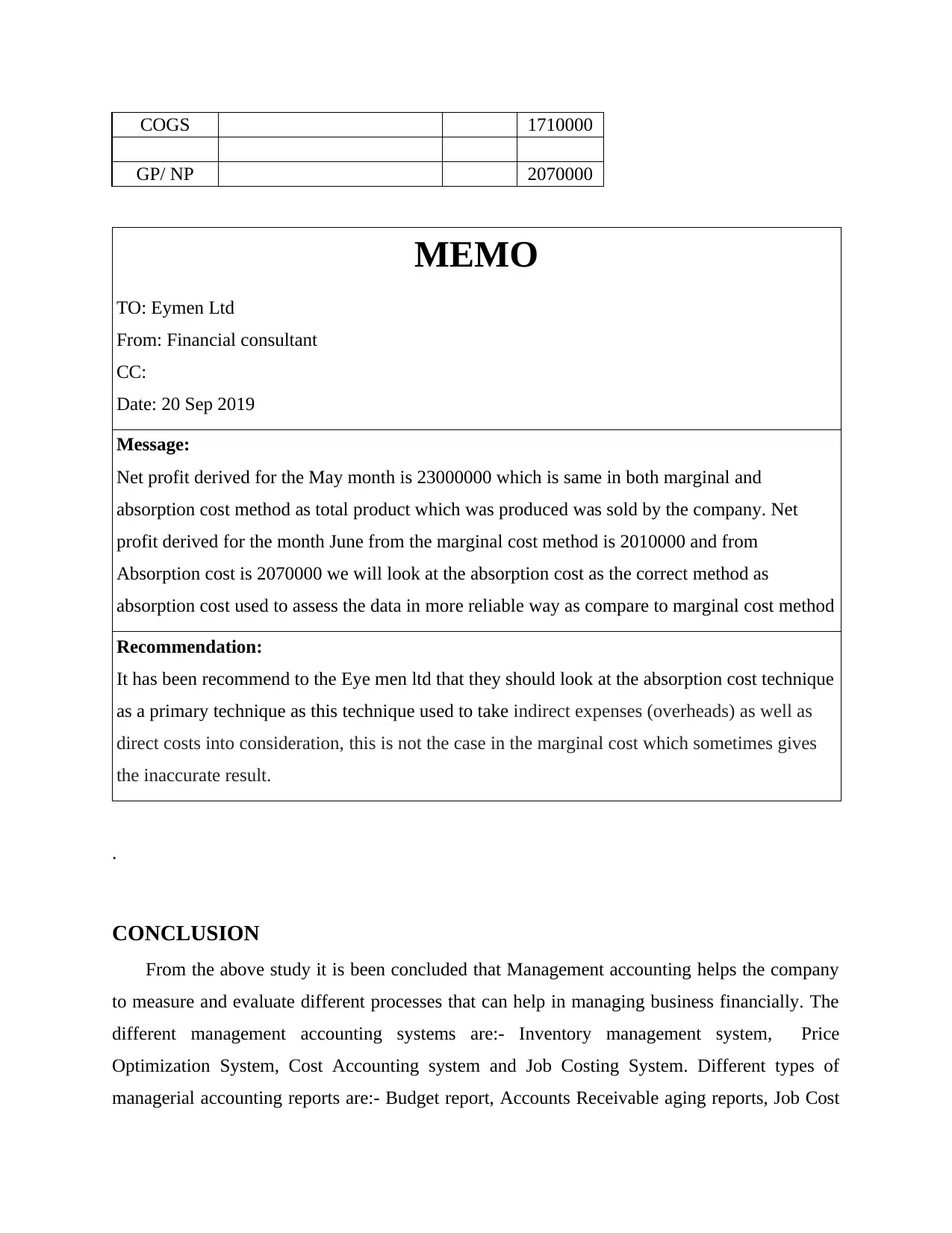

MEMO

TO: Eymen Ltd

From: Financial consultant

CC:

Date: 20 Sep 2019

Message:

Net profit derived for the May month is 23000000 which is same in both marginal and

absorption cost method as total product which was produced was sold by the company. Net

profit derived for the month June from the marginal cost method is 2010000 and from

Absorption cost is 2070000 we will look at the absorption cost as the correct method as

absorption cost used to assess the data in more reliable way as compare to marginal cost method

Recommendation:

It has been recommend to the Eye men ltd that they should look at the absorption cost technique

as a primary technique as this technique used to take indirect expenses (overheads) as well as

direct costs into consideration, this is not the case in the marginal cost which sometimes gives

the inaccurate result.

.

CONCLUSION

From the above study it is been concluded that Management accounting helps the company

to measure and evaluate different processes that can help in managing business financially. The

different management accounting systems are:- Inventory management system, Price

Optimization System, Cost Accounting system and Job Costing System. Different types of

managerial accounting reports are:- Budget report, Accounts Receivable aging reports, Job Cost

GP/ NP 2070000

MEMO

TO: Eymen Ltd

From: Financial consultant

CC:

Date: 20 Sep 2019

Message:

Net profit derived for the May month is 23000000 which is same in both marginal and

absorption cost method as total product which was produced was sold by the company. Net

profit derived for the month June from the marginal cost method is 2010000 and from

Absorption cost is 2070000 we will look at the absorption cost as the correct method as

absorption cost used to assess the data in more reliable way as compare to marginal cost method

Recommendation:

It has been recommend to the Eye men ltd that they should look at the absorption cost technique

as a primary technique as this technique used to take indirect expenses (overheads) as well as

direct costs into consideration, this is not the case in the marginal cost which sometimes gives

the inaccurate result.

.

CONCLUSION

From the above study it is been concluded that Management accounting helps the company

to measure and evaluate different processes that can help in managing business financially. The

different management accounting systems are:- Inventory management system, Price

Optimization System, Cost Accounting system and Job Costing System. Different types of

managerial accounting reports are:- Budget report, Accounts Receivable aging reports, Job Cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.