SPSS Analysis of Factors Influencing Tax Compliance in the UAE

VerifiedAdded on 2023/06/14

|47

|7502

|248

Report

AI Summary

This report presents an analysis of factors affecting tax compliance intention in the UAE, based on a survey of 152 respondents. The demographic profile reveals a majority of female respondents, with most aged between 30-40 and holding bachelor's or master's degrees. Reliability tests, including Cronbach's alpha, confirm the internal consistency of the questionnaire. Factor analysis identifies key factors influencing tax compliance, and multiple regression analysis reveals the impact of tax-complying attitude, normative expectation, and perceived tax compliance control on tax compliance intention. The moderator variable also shows a statistically significant and positive impact. The report concludes by interpreting the regression coefficients and discussing the implications of the findings. The analysis was conducted using SPSS software, and the results are presented in tables and figures. Desklib offers similar solved assignments and past papers for students.

Results and Discussion

Demographic Profile of the respondents

Results shows that majority of the respondents are female and the proportion of male

comparatively less. Usually in the tax payer database male dominate female taxpayers. Similarly

the results from age distribution shows that 44 % of the respondents are in the age group of 30 -

40, followed by 32 % in 20 -30 age group. In terms of education level 51 5 have bachelor degree

followed by 47 % with master degree. Very less respondents have Phd degree and also the

respondents with only high school degree is also less. Around 58 % of the respondents are

studying accounts which means that people are trying to get the knowledge about the tax

compliance.

In terms of position in the most of the respondents are in the middle management followed by

high management and executive level. This shows that the respondents in the study are most

likely to be in the tax paying bracket. When asked about the TRN number 86 % of the

respondents said that they have TRN number which indicates most of the them pay their

tax, .Results from the tax registration type shows that most of them comes under company VAT

registration followed by legal person VAT registration. Results from turn over shows that

majority of the firms have turnover between 375000 and 1.5 million followed by 27 % having

turnover between 187000 and 375000. The detailed table and graph of the demographic profile

has been shown in the appendix 1.

2) Reliability test

For the current research the reliability test has been conducted to examine the internal

consistency of the questions included in the study. The reliability has been examined using the

Cronbach’s alpha. Since the questionnaire included the liker scale questions, it is considered to

be the most appropriate measure of reliability. In the current research the liker scale was set as

following:

1-Strongly Disagree/ Strongly Unlikely

5- Strongly Agree/Very Likely

Demographic Profile of the respondents

Results shows that majority of the respondents are female and the proportion of male

comparatively less. Usually in the tax payer database male dominate female taxpayers. Similarly

the results from age distribution shows that 44 % of the respondents are in the age group of 30 -

40, followed by 32 % in 20 -30 age group. In terms of education level 51 5 have bachelor degree

followed by 47 % with master degree. Very less respondents have Phd degree and also the

respondents with only high school degree is also less. Around 58 % of the respondents are

studying accounts which means that people are trying to get the knowledge about the tax

compliance.

In terms of position in the most of the respondents are in the middle management followed by

high management and executive level. This shows that the respondents in the study are most

likely to be in the tax paying bracket. When asked about the TRN number 86 % of the

respondents said that they have TRN number which indicates most of the them pay their

tax, .Results from the tax registration type shows that most of them comes under company VAT

registration followed by legal person VAT registration. Results from turn over shows that

majority of the firms have turnover between 375000 and 1.5 million followed by 27 % having

turnover between 187000 and 375000. The detailed table and graph of the demographic profile

has been shown in the appendix 1.

2) Reliability test

For the current research the reliability test has been conducted to examine the internal

consistency of the questions included in the study. The reliability has been examined using the

Cronbach’s alpha. Since the questionnaire included the liker scale questions, it is considered to

be the most appropriate measure of reliability. In the current research the liker scale was set as

following:

1-Strongly Disagree/ Strongly Unlikely

5- Strongly Agree/Very Likely

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

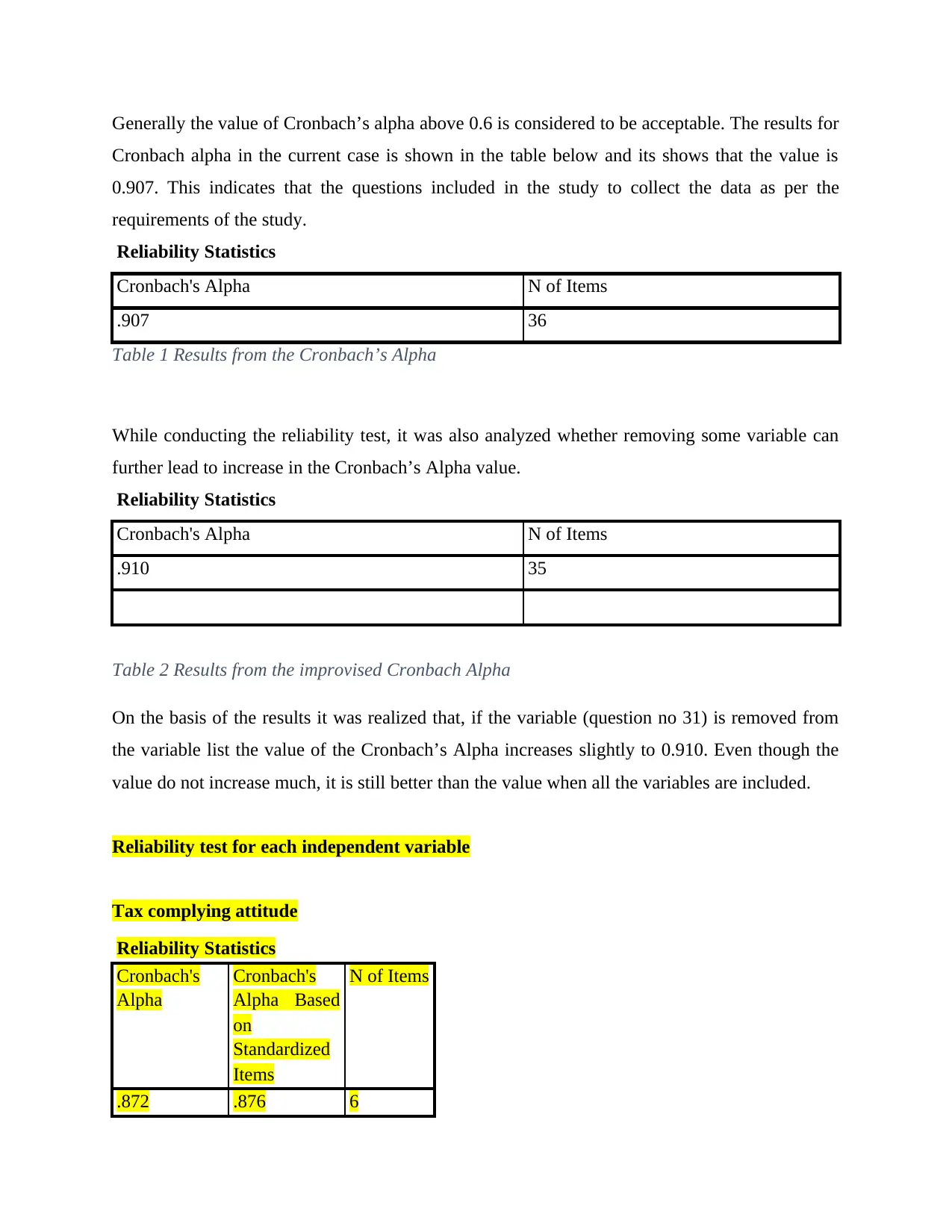

Generally the value of Cronbach’s alpha above 0.6 is considered to be acceptable. The results for

Cronbach alpha in the current case is shown in the table below and its shows that the value is

0.907. This indicates that the questions included in the study to collect the data as per the

requirements of the study.

Reliability Statistics

Cronbach's Alpha N of Items

.907 36

Table 1 Results from the Cronbach’s Alpha

While conducting the reliability test, it was also analyzed whether removing some variable can

further lead to increase in the Cronbach’s Alpha value.

Reliability Statistics

Cronbach's Alpha N of Items

.910 35

Table 2 Results from the improvised Cronbach Alpha

On the basis of the results it was realized that, if the variable (question no 31) is removed from

the variable list the value of the Cronbach’s Alpha increases slightly to 0.910. Even though the

value do not increase much, it is still better than the value when all the variables are included.

Reliability test for each independent variable

Tax complying attitude

Reliability Statistics

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.872 .876 6

Cronbach alpha in the current case is shown in the table below and its shows that the value is

0.907. This indicates that the questions included in the study to collect the data as per the

requirements of the study.

Reliability Statistics

Cronbach's Alpha N of Items

.907 36

Table 1 Results from the Cronbach’s Alpha

While conducting the reliability test, it was also analyzed whether removing some variable can

further lead to increase in the Cronbach’s Alpha value.

Reliability Statistics

Cronbach's Alpha N of Items

.910 35

Table 2 Results from the improvised Cronbach Alpha

On the basis of the results it was realized that, if the variable (question no 31) is removed from

the variable list the value of the Cronbach’s Alpha increases slightly to 0.910. Even though the

value do not increase much, it is still better than the value when all the variables are included.

Reliability test for each independent variable

Tax complying attitude

Reliability Statistics

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.872 .876 6

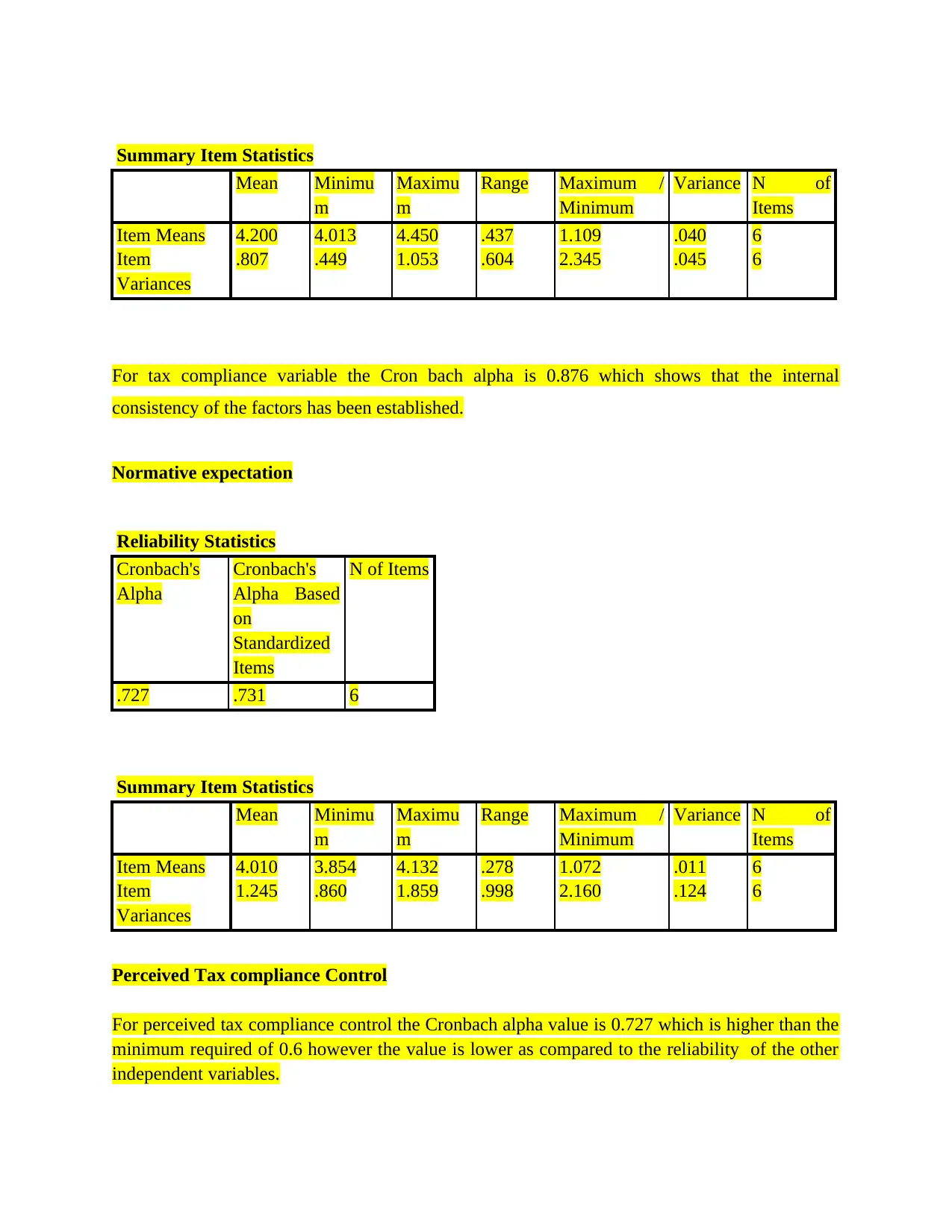

Summary Item Statistics

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 4.200 4.013 4.450 .437 1.109 .040 6

Item

Variances

.807 .449 1.053 .604 2.345 .045 6

For tax compliance variable the Cron bach alpha is 0.876 which shows that the internal

consistency of the factors has been established.

Normative expectation

Reliability Statistics

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.727 .731 6

Summary Item Statistics

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 4.010 3.854 4.132 .278 1.072 .011 6

Item

Variances

1.245 .860 1.859 .998 2.160 .124 6

Perceived Tax compliance Control

For perceived tax compliance control the Cronbach alpha value is 0.727 which is higher than the

minimum required of 0.6 however the value is lower as compared to the reliability of the other

independent variables.

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 4.200 4.013 4.450 .437 1.109 .040 6

Item

Variances

.807 .449 1.053 .604 2.345 .045 6

For tax compliance variable the Cron bach alpha is 0.876 which shows that the internal

consistency of the factors has been established.

Normative expectation

Reliability Statistics

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.727 .731 6

Summary Item Statistics

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 4.010 3.854 4.132 .278 1.072 .011 6

Item

Variances

1.245 .860 1.859 .998 2.160 .124 6

Perceived Tax compliance Control

For perceived tax compliance control the Cronbach alpha value is 0.727 which is higher than the

minimum required of 0.6 however the value is lower as compared to the reliability of the other

independent variables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reliability Statistics

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.896 .893 14

Summary Item Statistics

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 3.876 3.649 4.199 .550 1.151 .029 14

Item

Variances

1.126 .778 1.525 .747 1.960 .063 14

For the last independent variable also the Cronbach alpha is 0.896 which suggests that the

internal consistency of the independent variable have also been established.

Factor analysis

In this section the results from the factor analysis has been discussed. Factor analysis shows

whether the questionnaire used to collect the data has been as per the requirement of the research

or not.

Firstly the results from the KMO and the Bartlett Test has been shown in the table below.

KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling

Adequacy.

.347

Bartlett's Test of

Sphericity

Approx. Chi-Square 8552.717

df 630

Sig. .000

Table 3 Results from the KMO and Bartlett’s Test

Cronbach's

Alpha

Cronbach's

Alpha Based

on

Standardized

Items

N of Items

.896 .893 14

Summary Item Statistics

Mean Minimu

m

Maximu

m

Range Maximum /

Minimum

Variance N of

Items

Item Means 3.876 3.649 4.199 .550 1.151 .029 14

Item

Variances

1.126 .778 1.525 .747 1.960 .063 14

For the last independent variable also the Cronbach alpha is 0.896 which suggests that the

internal consistency of the independent variable have also been established.

Factor analysis

In this section the results from the factor analysis has been discussed. Factor analysis shows

whether the questionnaire used to collect the data has been as per the requirement of the research

or not.

Firstly the results from the KMO and the Bartlett Test has been shown in the table below.

KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling

Adequacy.

.347

Bartlett's Test of

Sphericity

Approx. Chi-Square 8552.717

df 630

Sig. .000

Table 3 Results from the KMO and Bartlett’s Test

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

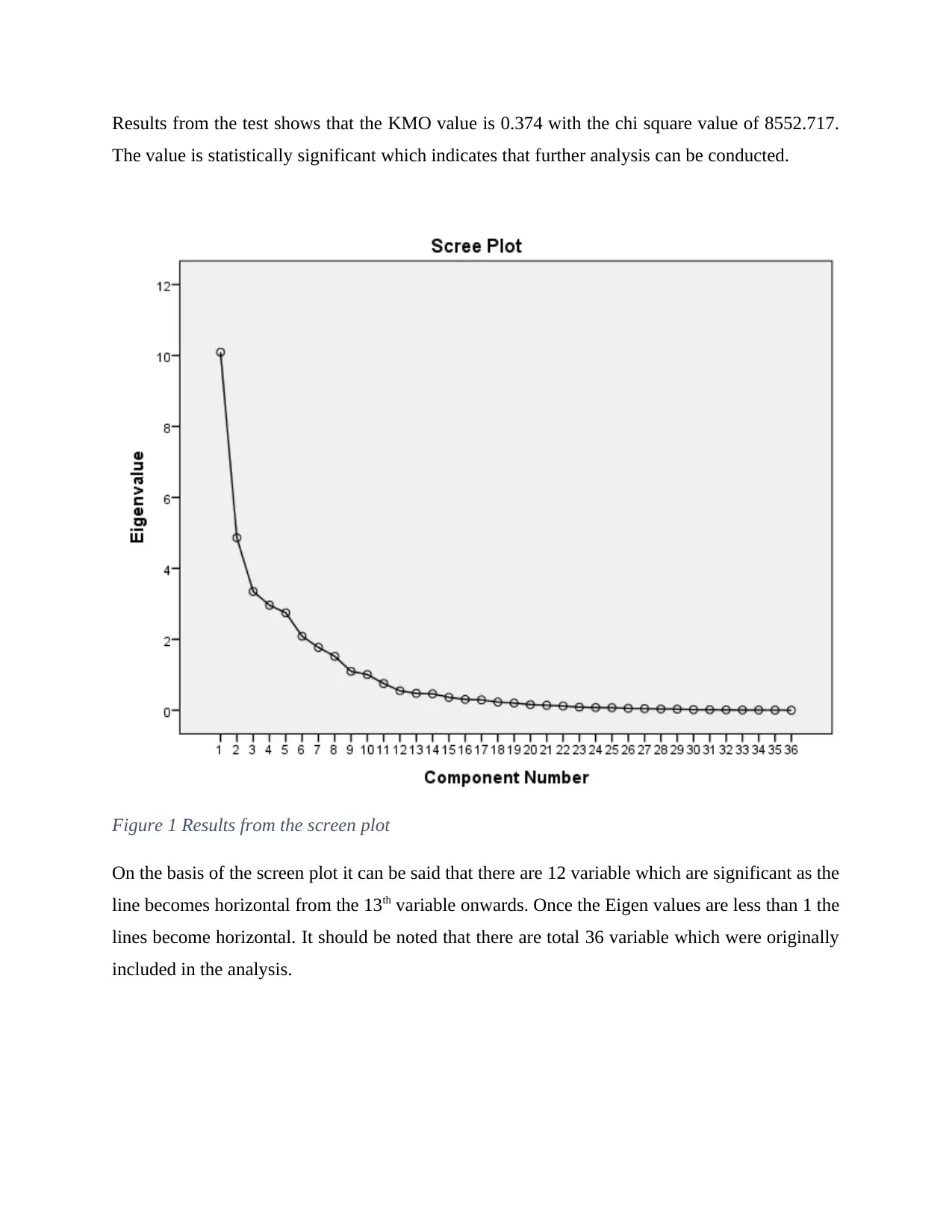

Results from the test shows that the KMO value is 0.374 with the chi square value of 8552.717.

The value is statistically significant which indicates that further analysis can be conducted.

Figure 1 Results from the screen plot

On the basis of the screen plot it can be said that there are 12 variable which are significant as the

line becomes horizontal from the 13th variable onwards. Once the Eigen values are less than 1 the

lines become horizontal. It should be noted that there are total 36 variable which were originally

included in the analysis.

The value is statistically significant which indicates that further analysis can be conducted.

Figure 1 Results from the screen plot

On the basis of the screen plot it can be said that there are 12 variable which are significant as the

line becomes horizontal from the 13th variable onwards. Once the Eigen values are less than 1 the

lines become horizontal. It should be noted that there are total 36 variable which were originally

included in the analysis.

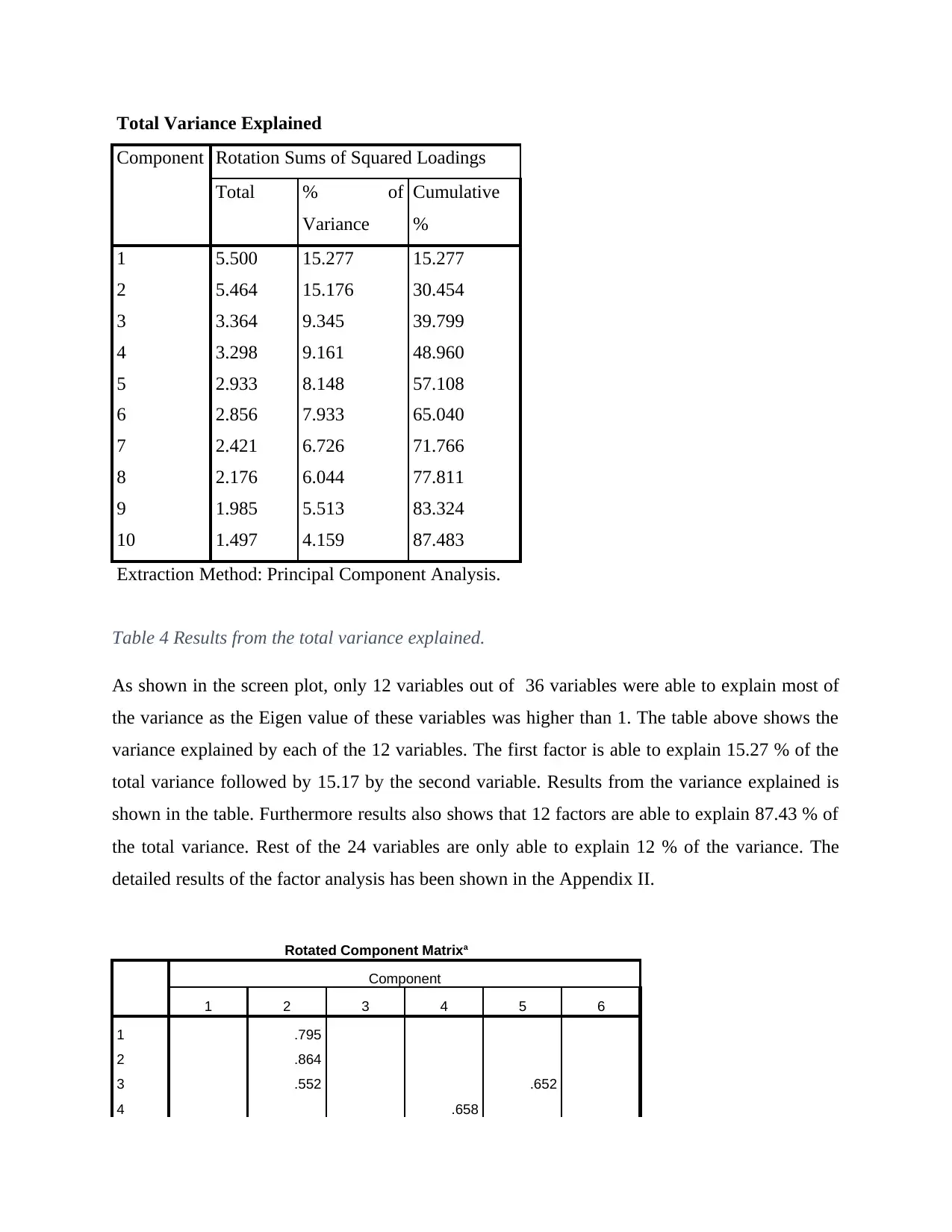

Total Variance Explained

Component Rotation Sums of Squared Loadings

Total % of

Variance

Cumulative

%

1 5.500 15.277 15.277

2 5.464 15.176 30.454

3 3.364 9.345 39.799

4 3.298 9.161 48.960

5 2.933 8.148 57.108

6 2.856 7.933 65.040

7 2.421 6.726 71.766

8 2.176 6.044 77.811

9 1.985 5.513 83.324

10 1.497 4.159 87.483

Extraction Method: Principal Component Analysis.

Table 4 Results from the total variance explained.

As shown in the screen plot, only 12 variables out of 36 variables were able to explain most of

the variance as the Eigen value of these variables was higher than 1. The table above shows the

variance explained by each of the 12 variables. The first factor is able to explain 15.27 % of the

total variance followed by 15.17 by the second variable. Results from the variance explained is

shown in the table. Furthermore results also shows that 12 factors are able to explain 87.43 % of

the total variance. Rest of the 24 variables are only able to explain 12 % of the variance. The

detailed results of the factor analysis has been shown in the Appendix II.

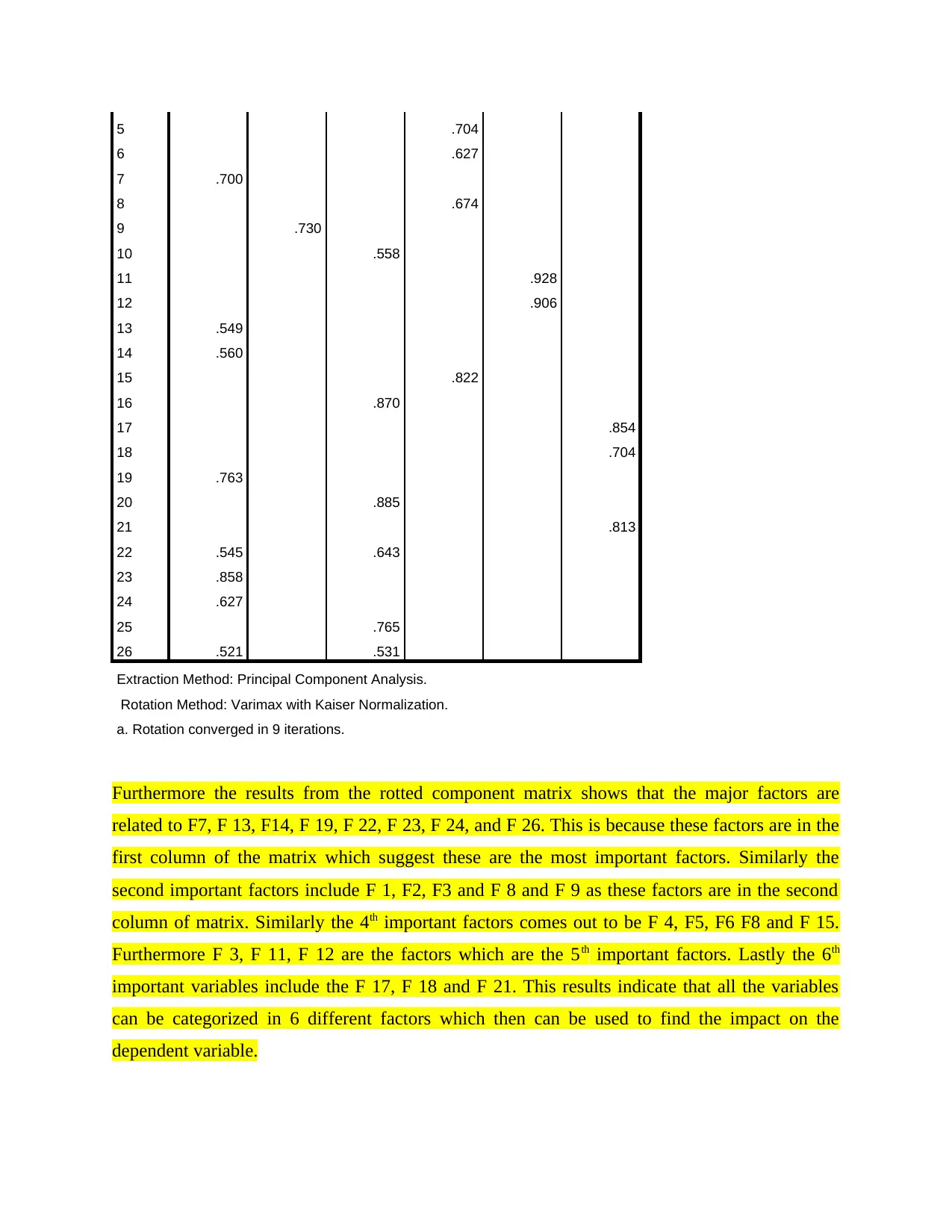

Rotated Component Matrixa

Component

1 2 3 4 5 6

1 .795

2 .864

3 .552 .652

4 .658

Component Rotation Sums of Squared Loadings

Total % of

Variance

Cumulative

%

1 5.500 15.277 15.277

2 5.464 15.176 30.454

3 3.364 9.345 39.799

4 3.298 9.161 48.960

5 2.933 8.148 57.108

6 2.856 7.933 65.040

7 2.421 6.726 71.766

8 2.176 6.044 77.811

9 1.985 5.513 83.324

10 1.497 4.159 87.483

Extraction Method: Principal Component Analysis.

Table 4 Results from the total variance explained.

As shown in the screen plot, only 12 variables out of 36 variables were able to explain most of

the variance as the Eigen value of these variables was higher than 1. The table above shows the

variance explained by each of the 12 variables. The first factor is able to explain 15.27 % of the

total variance followed by 15.17 by the second variable. Results from the variance explained is

shown in the table. Furthermore results also shows that 12 factors are able to explain 87.43 % of

the total variance. Rest of the 24 variables are only able to explain 12 % of the variance. The

detailed results of the factor analysis has been shown in the Appendix II.

Rotated Component Matrixa

Component

1 2 3 4 5 6

1 .795

2 .864

3 .552 .652

4 .658

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 .704

6 .627

7 .700

8 .674

9 .730

10 .558

11 .928

12 .906

13 .549

14 .560

15 .822

16 .870

17 .854

18 .704

19 .763

20 .885

21 .813

22 .545 .643

23 .858

24 .627

25 .765

26 .521 .531

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

a. Rotation converged in 9 iterations.

Furthermore the results from the rotted component matrix shows that the major factors are

related to F7, F 13, F14, F 19, F 22, F 23, F 24, and F 26. This is because these factors are in the

first column of the matrix which suggest these are the most important factors. Similarly the

second important factors include F 1, F2, F3 and F 8 and F 9 as these factors are in the second

column of matrix. Similarly the 4th important factors comes out to be F 4, F5, F6 F8 and F 15.

Furthermore F 3, F 11, F 12 are the factors which are the 5th important factors. Lastly the 6th

important variables include the F 17, F 18 and F 21. This results indicate that all the variables

can be categorized in 6 different factors which then can be used to find the impact on the

dependent variable.

6 .627

7 .700

8 .674

9 .730

10 .558

11 .928

12 .906

13 .549

14 .560

15 .822

16 .870

17 .854

18 .704

19 .763

20 .885

21 .813

22 .545 .643

23 .858

24 .627

25 .765

26 .521 .531

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

a. Rotation converged in 9 iterations.

Furthermore the results from the rotted component matrix shows that the major factors are

related to F7, F 13, F14, F 19, F 22, F 23, F 24, and F 26. This is because these factors are in the

first column of the matrix which suggest these are the most important factors. Similarly the

second important factors include F 1, F2, F3 and F 8 and F 9 as these factors are in the second

column of matrix. Similarly the 4th important factors comes out to be F 4, F5, F6 F8 and F 15.

Furthermore F 3, F 11, F 12 are the factors which are the 5th important factors. Lastly the 6th

important variables include the F 17, F 18 and F 21. This results indicate that all the variables

can be categorized in 6 different factors which then can be used to find the impact on the

dependent variable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Multiple regression analysis

The regression analysis is has been performed to find the impact of the independent variables on

the dependent variable. The impact is decided on the basis of the regression coefficient of the

independent. If the coefficient is positive then the independent variable have positive and if the

regression coefficient is negative then the impact is also negative. For the current research the

dependent and the independent variables are as follows:

Dependent variable:

Tax compliance intention

Independent variable:

Tax complying attitude

Normative expectation

Perceived Tax compliance Control

Moderator variable:

Perceived Tax compliance Control * tax compliance intention

The regression analysis is has been performed to find the impact of the independent variables on

the dependent variable. The impact is decided on the basis of the regression coefficient of the

independent. If the coefficient is positive then the independent variable have positive and if the

regression coefficient is negative then the impact is also negative. For the current research the

dependent and the independent variables are as follows:

Dependent variable:

Tax compliance intention

Independent variable:

Tax complying attitude

Normative expectation

Perceived Tax compliance Control

Moderator variable:

Perceived Tax compliance Control * tax compliance intention

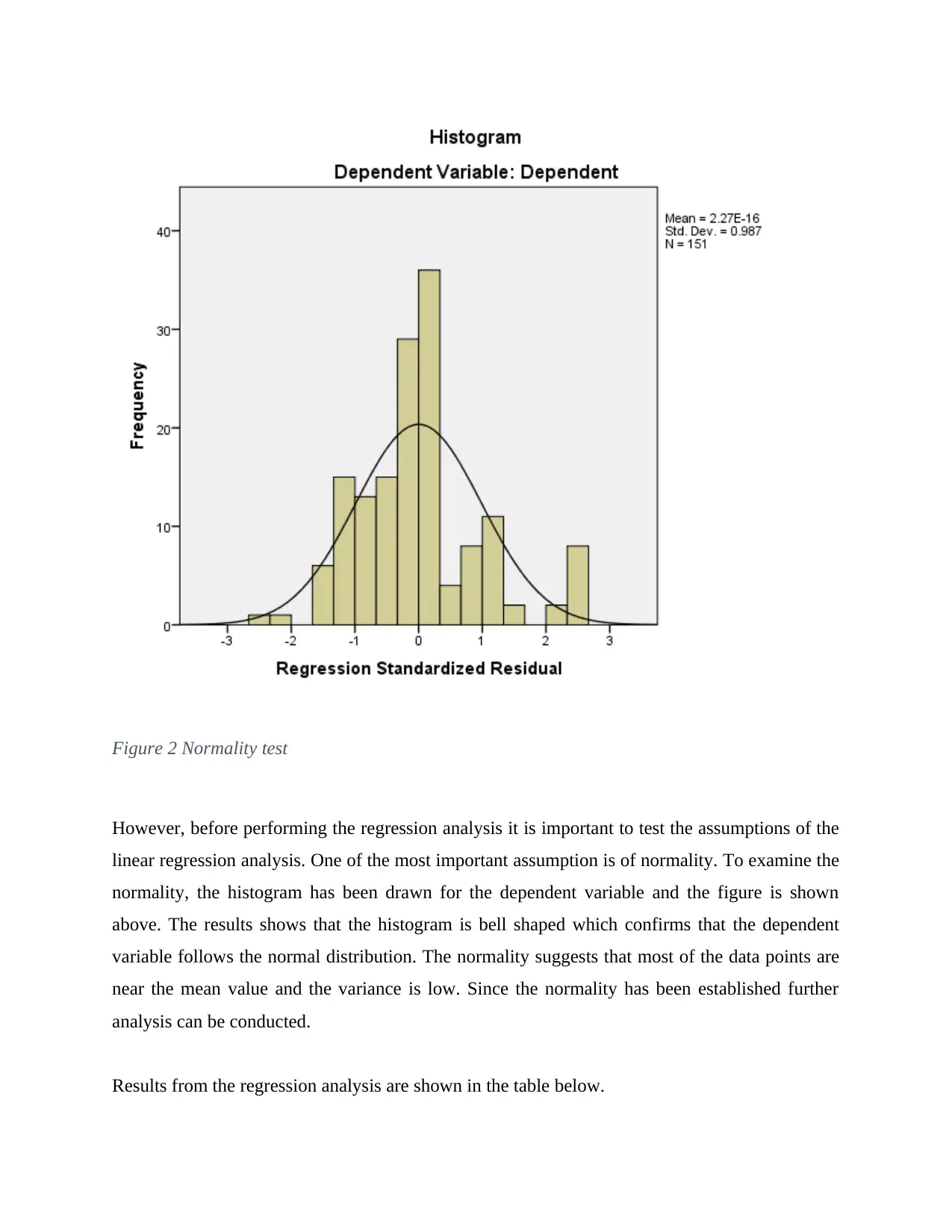

Figure 2 Normality test

However, before performing the regression analysis it is important to test the assumptions of the

linear regression analysis. One of the most important assumption is of normality. To examine the

normality, the histogram has been drawn for the dependent variable and the figure is shown

above. The results shows that the histogram is bell shaped which confirms that the dependent

variable follows the normal distribution. The normality suggests that most of the data points are

near the mean value and the variance is low. Since the normality has been established further

analysis can be conducted.

Results from the regression analysis are shown in the table below.

However, before performing the regression analysis it is important to test the assumptions of the

linear regression analysis. One of the most important assumption is of normality. To examine the

normality, the histogram has been drawn for the dependent variable and the figure is shown

above. The results shows that the histogram is bell shaped which confirms that the dependent

variable follows the normal distribution. The normality suggests that most of the data points are

near the mean value and the variance is low. Since the normality has been established further

analysis can be conducted.

Results from the regression analysis are shown in the table below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

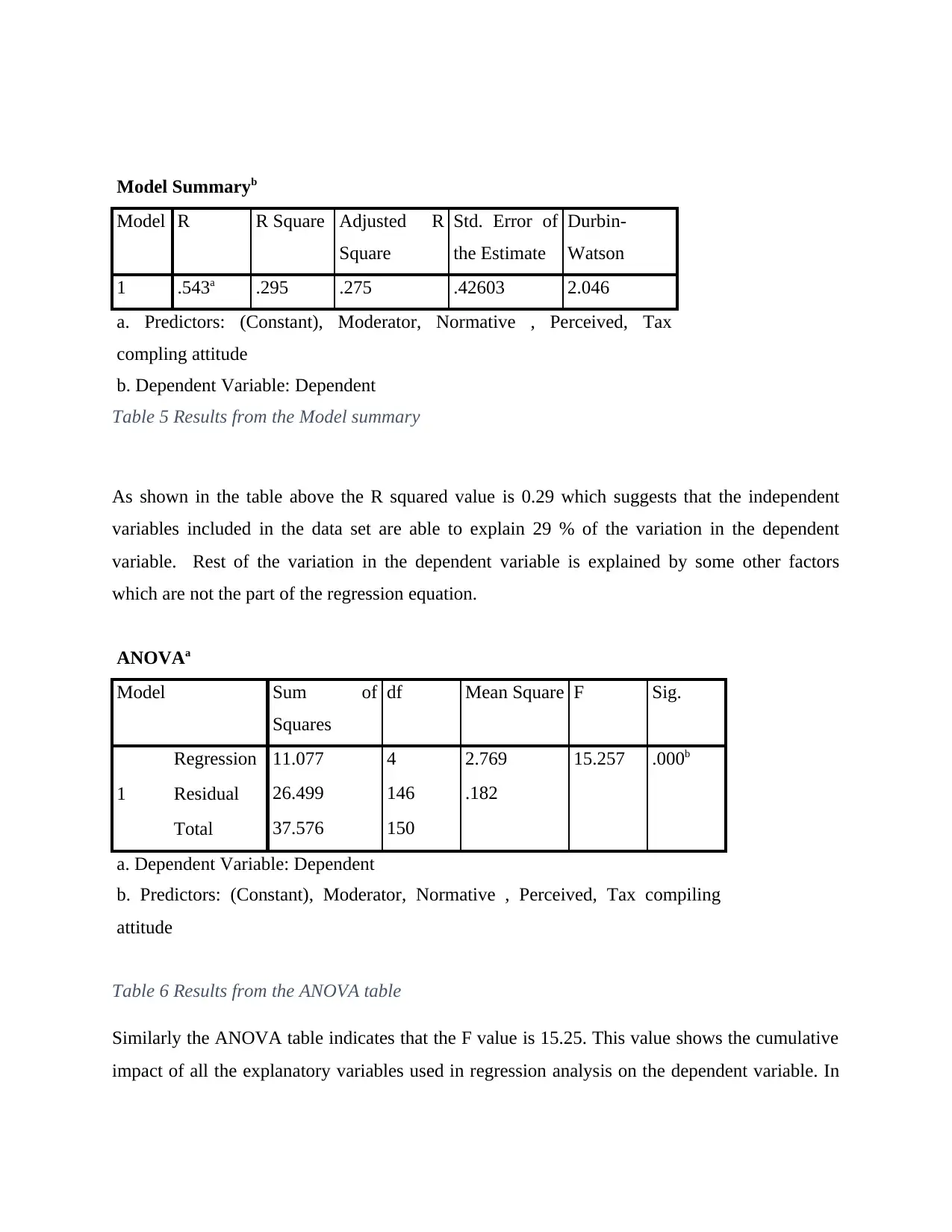

Model Summaryb

Model R R Square Adjusted R

Square

Std. Error of

the Estimate

Durbin-

Watson

1 .543a .295 .275 .42603 2.046

a. Predictors: (Constant), Moderator, Normative , Perceived, Tax

compling attitude

b. Dependent Variable: Dependent

Table 5 Results from the Model summary

As shown in the table above the R squared value is 0.29 which suggests that the independent

variables included in the data set are able to explain 29 % of the variation in the dependent

variable. Rest of the variation in the dependent variable is explained by some other factors

which are not the part of the regression equation.

ANOVAa

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 11.077 4 2.769 15.257 .000b

Residual 26.499 146 .182

Total 37.576 150

a. Dependent Variable: Dependent

b. Predictors: (Constant), Moderator, Normative , Perceived, Tax compiling

attitude

Table 6 Results from the ANOVA table

Similarly the ANOVA table indicates that the F value is 15.25. This value shows the cumulative

impact of all the explanatory variables used in regression analysis on the dependent variable. In

Model R R Square Adjusted R

Square

Std. Error of

the Estimate

Durbin-

Watson

1 .543a .295 .275 .42603 2.046

a. Predictors: (Constant), Moderator, Normative , Perceived, Tax

compling attitude

b. Dependent Variable: Dependent

Table 5 Results from the Model summary

As shown in the table above the R squared value is 0.29 which suggests that the independent

variables included in the data set are able to explain 29 % of the variation in the dependent

variable. Rest of the variation in the dependent variable is explained by some other factors

which are not the part of the regression equation.

ANOVAa

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 11.077 4 2.769 15.257 .000b

Residual 26.499 146 .182

Total 37.576 150

a. Dependent Variable: Dependent

b. Predictors: (Constant), Moderator, Normative , Perceived, Tax compiling

attitude

Table 6 Results from the ANOVA table

Similarly the ANOVA table indicates that the F value is 15.25. This value shows the cumulative

impact of all the explanatory variables used in regression analysis on the dependent variable. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the current case the F value is statistically significant as the p value is less than 0.05. So the

cumulative impact is significant.

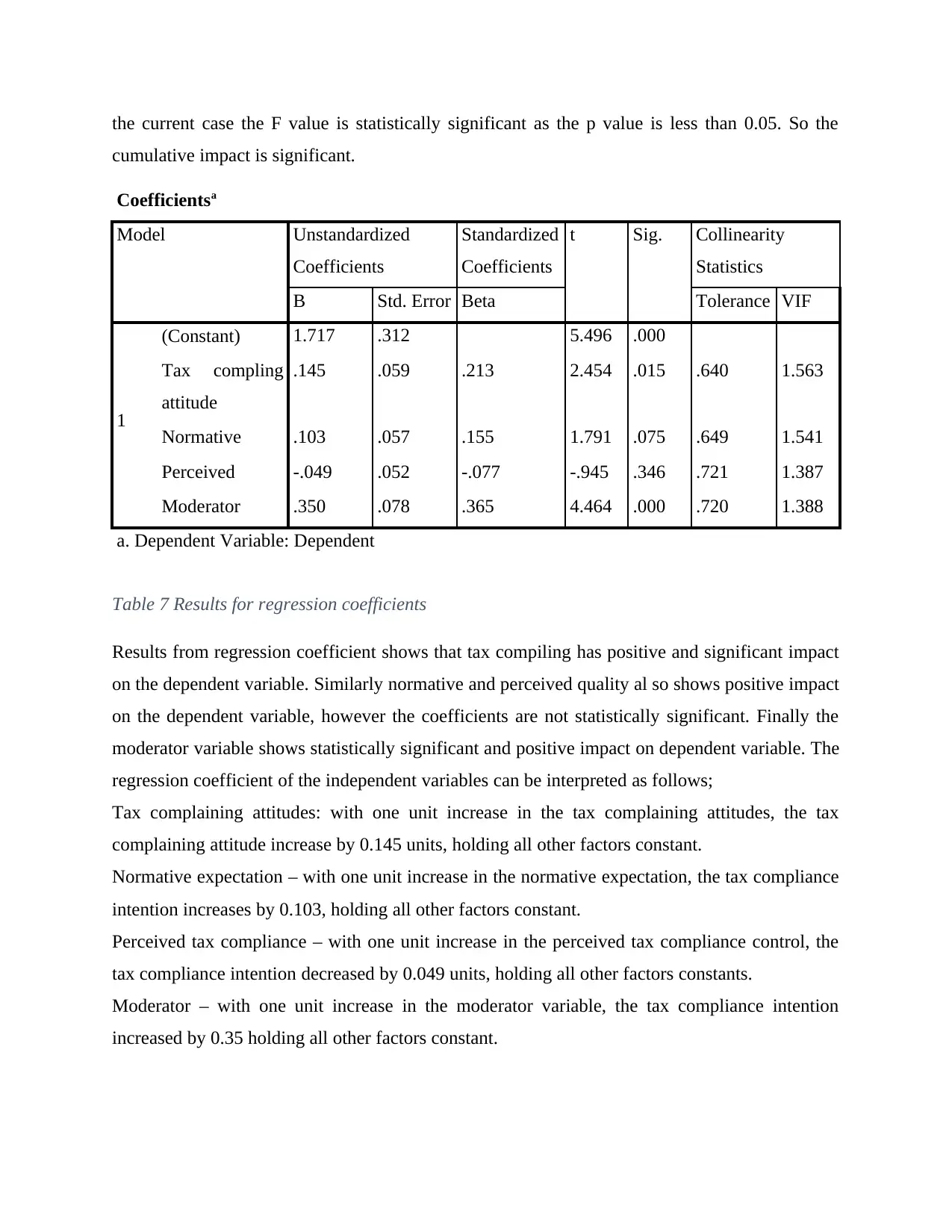

Coefficientsa

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig. Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) 1.717 .312 5.496 .000

Tax compling

attitude

.145 .059 .213 2.454 .015 .640 1.563

Normative .103 .057 .155 1.791 .075 .649 1.541

Perceived -.049 .052 -.077 -.945 .346 .721 1.387

Moderator .350 .078 .365 4.464 .000 .720 1.388

a. Dependent Variable: Dependent

Table 7 Results for regression coefficients

Results from regression coefficient shows that tax compiling has positive and significant impact

on the dependent variable. Similarly normative and perceived quality al so shows positive impact

on the dependent variable, however the coefficients are not statistically significant. Finally the

moderator variable shows statistically significant and positive impact on dependent variable. The

regression coefficient of the independent variables can be interpreted as follows;

Tax complaining attitudes: with one unit increase in the tax complaining attitudes, the tax

complaining attitude increase by 0.145 units, holding all other factors constant.

Normative expectation – with one unit increase in the normative expectation, the tax compliance

intention increases by 0.103, holding all other factors constant.

Perceived tax compliance – with one unit increase in the perceived tax compliance control, the

tax compliance intention decreased by 0.049 units, holding all other factors constants.

Moderator – with one unit increase in the moderator variable, the tax compliance intention

increased by 0.35 holding all other factors constant.

cumulative impact is significant.

Coefficientsa

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig. Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) 1.717 .312 5.496 .000

Tax compling

attitude

.145 .059 .213 2.454 .015 .640 1.563

Normative .103 .057 .155 1.791 .075 .649 1.541

Perceived -.049 .052 -.077 -.945 .346 .721 1.387

Moderator .350 .078 .365 4.464 .000 .720 1.388

a. Dependent Variable: Dependent

Table 7 Results for regression coefficients

Results from regression coefficient shows that tax compiling has positive and significant impact

on the dependent variable. Similarly normative and perceived quality al so shows positive impact

on the dependent variable, however the coefficients are not statistically significant. Finally the

moderator variable shows statistically significant and positive impact on dependent variable. The

regression coefficient of the independent variables can be interpreted as follows;

Tax complaining attitudes: with one unit increase in the tax complaining attitudes, the tax

complaining attitude increase by 0.145 units, holding all other factors constant.

Normative expectation – with one unit increase in the normative expectation, the tax compliance

intention increases by 0.103, holding all other factors constant.

Perceived tax compliance – with one unit increase in the perceived tax compliance control, the

tax compliance intention decreased by 0.049 units, holding all other factors constants.

Moderator – with one unit increase in the moderator variable, the tax compliance intention

increased by 0.35 holding all other factors constant.

To examine the existence of the multicollinarity, the VIF test has been performed and the results

from the collinearity statistics shows that the VIF values are between 1 and 10 which indicates

that there is no problem of multicollinarity in the regression equation(Armstrong, 2012; Iaci and

Singh, 2012).

Many previous scholars have also studied the factors affecting the tax compliance intention and

different scholars have identified various factors. A study by (MACHOGU, 2011) have shown

that the factors such as public governance quality, ethinicity and the attitudes affect the tax

compliance. Another study by (Engida and Abera, 2014) identified different factors such as the

economic factors ( benefit and cost of tax evasion, rate of tax, audits), institutional factors ( tax

authority, role of government) , social factors (positive perception, government policies) and

individual factors ( individual finance, awareness, attitude, knowledge). On the other hand

(Remali et al., 2015) analyzed the factors affecting the non-compliance of taxpayers. On the

basis of the results from the primary data authors concluded that the tax morale and the personal

morale are significantly related to the attitude of tax non-compliance. Furthermore the study by

(Marandu, Mbekomize and Ifezue, 2015) review and analyze the factors affecting the taxpayers

compliance. Secondary data was collected for the time period 1985-2012, Results from the study

suggests that the normative, attitudinal and subjective variables are the major factors affecting

the tax compliance. Results from this study are similar to the findings of the current study. This

shows that the current research is in line with the previous researches and can help to fill the gap

in the existing literature.

Furthermore the results from the data analysis also shows that the tax compliance intention is

positively and significantly correlated with tax compliance attitude. Also the relationship

between the normative expectation and the tax compliance intention are also positively and

significantly correlated. This indicates that people with positive normative expectation about the

tax compliance are expected to pay tax. This is may be because the people have positive

expectation, that the paid tax will be used for the betterment of the society which will improve

the overall wellbeing of all the people. Paying tax is also social responsibility so, people with

from the collinearity statistics shows that the VIF values are between 1 and 10 which indicates

that there is no problem of multicollinarity in the regression equation(Armstrong, 2012; Iaci and

Singh, 2012).

Many previous scholars have also studied the factors affecting the tax compliance intention and

different scholars have identified various factors. A study by (MACHOGU, 2011) have shown

that the factors such as public governance quality, ethinicity and the attitudes affect the tax

compliance. Another study by (Engida and Abera, 2014) identified different factors such as the

economic factors ( benefit and cost of tax evasion, rate of tax, audits), institutional factors ( tax

authority, role of government) , social factors (positive perception, government policies) and

individual factors ( individual finance, awareness, attitude, knowledge). On the other hand

(Remali et al., 2015) analyzed the factors affecting the non-compliance of taxpayers. On the

basis of the results from the primary data authors concluded that the tax morale and the personal

morale are significantly related to the attitude of tax non-compliance. Furthermore the study by

(Marandu, Mbekomize and Ifezue, 2015) review and analyze the factors affecting the taxpayers

compliance. Secondary data was collected for the time period 1985-2012, Results from the study

suggests that the normative, attitudinal and subjective variables are the major factors affecting

the tax compliance. Results from this study are similar to the findings of the current study. This

shows that the current research is in line with the previous researches and can help to fill the gap

in the existing literature.

Furthermore the results from the data analysis also shows that the tax compliance intention is

positively and significantly correlated with tax compliance attitude. Also the relationship

between the normative expectation and the tax compliance intention are also positively and

significantly correlated. This indicates that people with positive normative expectation about the

tax compliance are expected to pay tax. This is may be because the people have positive

expectation, that the paid tax will be used for the betterment of the society which will improve

the overall wellbeing of all the people. Paying tax is also social responsibility so, people with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 47

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.