Economics for Business: Analysis of UK Housing Market - SBLC4004

VerifiedAdded on 2023/06/13

|23

|4228

|136

Essay

AI Summary

This essay provides an analysis of the factors affecting housing prices in the United Kingdom, primarily focusing on demand and supply dynamics. It examines short-run influences such as affordability, consumer confidence, population demographics, real wages, interest rates, renting costs, and mortgage availability. On the supply side, the essay discusses the impact of production costs and taxation. The long-run perspective is also considered, along with an evaluation of government schemes like Help to Buy and Shared Ownership aimed at assisting first-time buyers. The essay identifies key drivers of price fluctuations in the UK housing market, offering a comprehensive overview of the economic forces at play.

Running head: FACTORS AFFECTING HOUSING PRICES IN UK

Factors Affecting Housing Prices in UK

Name of the Student:

Name of the University:

Author Note:

Factors Affecting Housing Prices in UK

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FACTORS AFFECTING HOUSING PRICES IN UK

Executive summary:

Demand and supply being the most important components of any economic analysis have been

used in this assignment to analyze the housing market of United Kingdom. The factors affecting

both demand and supply have been discussed and the short run and long run scenarios have

discussed subsequently. The impact of new governmental schemes like Help to Buy and Shared

Ownership which are aimed at providing help to first time buyers have also been discussed and

its impacts have been analyzed. Only the factors and their effects are discussed but the quantities

or magnitudes of the same have not been analyzed.

Executive summary:

Demand and supply being the most important components of any economic analysis have been

used in this assignment to analyze the housing market of United Kingdom. The factors affecting

both demand and supply have been discussed and the short run and long run scenarios have

discussed subsequently. The impact of new governmental schemes like Help to Buy and Shared

Ownership which are aimed at providing help to first time buyers have also been discussed and

its impacts have been analyzed. Only the factors and their effects are discussed but the quantities

or magnitudes of the same have not been analyzed.

2FACTORS AFFECTING HOUSING PRICES IN UK

Table of Contents

Introduction:....................................................................................................................................2

Demand Side Factors (Short Run):..................................................................................................2

Supply Side Factors (Short Run)...................................................................................................10

The Long Run Curve:....................................................................................................................15

Effects of Government Schemes:..................................................................................................15

Conclusion:....................................................................................................................................17

References:....................................................................................................................................18

Table of Contents

Introduction:....................................................................................................................................2

Demand Side Factors (Short Run):..................................................................................................2

Supply Side Factors (Short Run)...................................................................................................10

The Long Run Curve:....................................................................................................................15

Effects of Government Schemes:..................................................................................................15

Conclusion:....................................................................................................................................17

References:....................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FACTORS AFFECTING HOUSING PRICES IN UK

Introduction:

Demand and supply form the very basis of economic analysis in case of any market or

sector. It draws the relationship between factors that lead to the pricing of a product both in the

short run and the long run. The real estate and housing market in the United Kingdom is one of

those sectors which are most talked about and where demand and supply keep changing

drastically on an annual basis (Wilcox and Perry 2014). Studies suggest that this sector has been

gravely affected due to Brexit and even without that scenario prices keep fluctuating due to the

changing needs and choices of people. Research suggests that the house owning demographics in

UK has also altered over the years. It has shifted from young to the old. It us easier for the old

crowd of UK to own houses faster than the younger population who have to wait for years before

they get hold of good property (Booth and Choudhary 2013). To top it all, the construction rates

of property in UK have also gone down which causes increased shortage and higher prices. It has

also been observed that despite this huge demand for houses in the UK, most of the population is

still resorting to rent. There are various other reasons why this is happening. If a keen look is

taken at the House Price Index (HPI) for UK from 2006 to 2016, it can be observed that every

year there has been a increased growth in the prices apart from one or two years. In this essay,

the various aspects that drive the change of demand and supply are discussed and dealt with. In

addition, to the same both the short run and long run scenario are mentioned. The factors

affecting demand and supply of houses in UK are discussed in detail in the following section.

Introduction:

Demand and supply form the very basis of economic analysis in case of any market or

sector. It draws the relationship between factors that lead to the pricing of a product both in the

short run and the long run. The real estate and housing market in the United Kingdom is one of

those sectors which are most talked about and where demand and supply keep changing

drastically on an annual basis (Wilcox and Perry 2014). Studies suggest that this sector has been

gravely affected due to Brexit and even without that scenario prices keep fluctuating due to the

changing needs and choices of people. Research suggests that the house owning demographics in

UK has also altered over the years. It has shifted from young to the old. It us easier for the old

crowd of UK to own houses faster than the younger population who have to wait for years before

they get hold of good property (Booth and Choudhary 2013). To top it all, the construction rates

of property in UK have also gone down which causes increased shortage and higher prices. It has

also been observed that despite this huge demand for houses in the UK, most of the population is

still resorting to rent. There are various other reasons why this is happening. If a keen look is

taken at the House Price Index (HPI) for UK from 2006 to 2016, it can be observed that every

year there has been a increased growth in the prices apart from one or two years. In this essay,

the various aspects that drive the change of demand and supply are discussed and dealt with. In

addition, to the same both the short run and long run scenario are mentioned. The factors

affecting demand and supply of houses in UK are discussed in detail in the following section.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FACTORS AFFECTING HOUSING PRICES IN UK

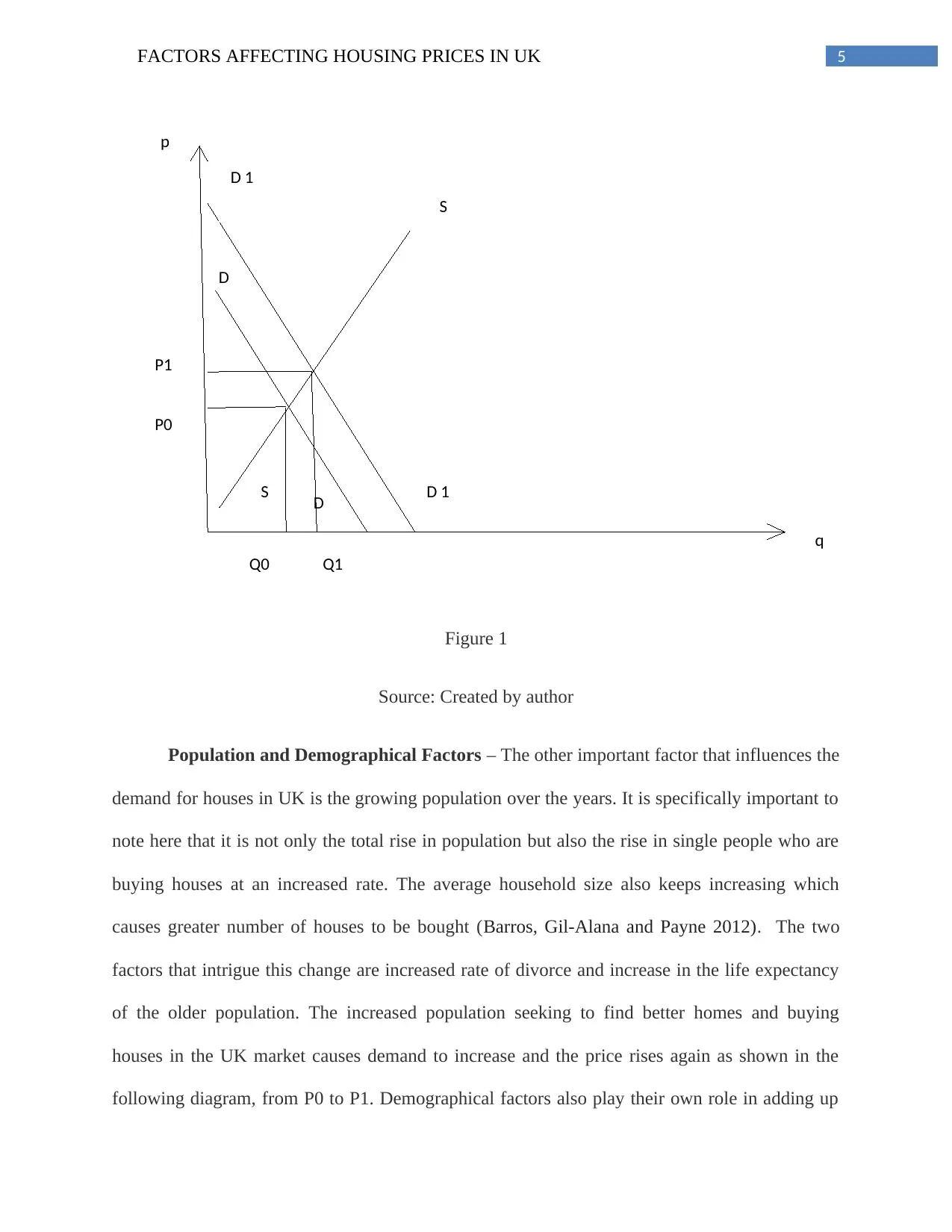

Demand Side Factors (Short Run):

Affordability and Consumer Confidence - With increase in the amount of gross

disposable income that the households own, the demand for houses have inevitably increased. It

should also be noted here that as house is considered to a luxurious good, with some increase in

income, the demand increases even more. This causes the price to rise even higher. This

increased effect on prices is primarily felt in the short run.

With the rising prices, consumer confidence also varies as their income also increases.

When the economy is in a situation where it is facing a boom, the demand for houses rises faster

than the increase in income of the population residing in UK (Mulliner, Smallbone and Maliene

2013). The following diagram shows that with increase in affordability as demand rises, the

demand curve shifts from DD to D1D1 while supply remaining constant, causing the equilibrium

price (from P0 to P1) as well as the quantity to rise (from Q0 to Q1).

Demand Side Factors (Short Run):

Affordability and Consumer Confidence - With increase in the amount of gross

disposable income that the households own, the demand for houses have inevitably increased. It

should also be noted here that as house is considered to a luxurious good, with some increase in

income, the demand increases even more. This causes the price to rise even higher. This

increased effect on prices is primarily felt in the short run.

With the rising prices, consumer confidence also varies as their income also increases.

When the economy is in a situation where it is facing a boom, the demand for houses rises faster

than the increase in income of the population residing in UK (Mulliner, Smallbone and Maliene

2013). The following diagram shows that with increase in affordability as demand rises, the

demand curve shifts from DD to D1D1 while supply remaining constant, causing the equilibrium

price (from P0 to P1) as well as the quantity to rise (from Q0 to Q1).

5FACTORS AFFECTING HOUSING PRICES IN UK

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 1

Source: Created by author

Population and Demographical Factors – The other important factor that influences the

demand for houses in UK is the growing population over the years. It is specifically important to

note here that it is not only the total rise in population but also the rise in single people who are

buying houses at an increased rate. The average household size also keeps increasing which

causes greater number of houses to be bought (Barros, Gil-Alana and Payne 2012). The two

factors that intrigue this change are increased rate of divorce and increase in the life expectancy

of the older population. The increased population seeking to find better homes and buying

houses in the UK market causes demand to increase and the price rises again as shown in the

following diagram, from P0 to P1. Demographical factors also play their own role in adding up

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 1

Source: Created by author

Population and Demographical Factors – The other important factor that influences the

demand for houses in UK is the growing population over the years. It is specifically important to

note here that it is not only the total rise in population but also the rise in single people who are

buying houses at an increased rate. The average household size also keeps increasing which

causes greater number of houses to be bought (Barros, Gil-Alana and Payne 2012). The two

factors that intrigue this change are increased rate of divorce and increase in the life expectancy

of the older population. The increased population seeking to find better homes and buying

houses in the UK market causes demand to increase and the price rises again as shown in the

following diagram, from P0 to P1. Demographical factors also play their own role in adding up

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FACTORS AFFECTING HOUSING PRICES IN UK

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

to the already existing demand for houses in UK. It has been noted that since 2006, the age group

that is looking out to buy new houses and is being successful in doing so are the people who are

of the age group 65-74 years (Wilcox and Perry 2014). This is so because for them buying is

easy because of the money saved over the years which for the youngsters is not possible and

hence they have to wait longer to save enough (Clapham et al. 2014). This wait is causing a

continued existence of demand for houses.

Figure 2

Source: Created by author

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

to the already existing demand for houses in UK. It has been noted that since 2006, the age group

that is looking out to buy new houses and is being successful in doing so are the people who are

of the age group 65-74 years (Wilcox and Perry 2014). This is so because for them buying is

easy because of the money saved over the years which for the youngsters is not possible and

hence they have to wait longer to save enough (Clapham et al. 2014). This wait is causing a

continued existence of demand for houses.

Figure 2

Source: Created by author

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FACTORS AFFECTING HOUSING PRICES IN UK

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Real Wages and Incomes – It is also reported that for the years 2006 to 2016, the

demand for houses and real estate has increased due to the increase in the amount of money

earned and the real wages received by the population residing in the UK (Aron et al. 2012). As

housing involves a product that is highly income elastic, it results in the demand rising with rise

in incomes. This is also a factor that causes a direct impact on the affordability. Studies have

shown that the richest 5% of households have undergone the highest increase in income, while

the poorest 5% have undergone lower rises in income. With respect to this it can be asserted that

demand for housing is increasing due to the population moving from low income to high income

levels. This increase in demand is again explained graphically with the help of the following

diagram, where as demand rises, the demand curve shifts to the right and the prices rise in turn as

in the above cases, from P0 to P1.

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Real Wages and Incomes – It is also reported that for the years 2006 to 2016, the

demand for houses and real estate has increased due to the increase in the amount of money

earned and the real wages received by the population residing in the UK (Aron et al. 2012). As

housing involves a product that is highly income elastic, it results in the demand rising with rise

in incomes. This is also a factor that causes a direct impact on the affordability. Studies have

shown that the richest 5% of households have undergone the highest increase in income, while

the poorest 5% have undergone lower rises in income. With respect to this it can be asserted that

demand for housing is increasing due to the population moving from low income to high income

levels. This increase in demand is again explained graphically with the help of the following

diagram, where as demand rises, the demand curve shifts to the right and the prices rise in turn as

in the above cases, from P0 to P1.

8FACTORS AFFECTING HOUSING PRICES IN UK

Figure 3

Source: Created by author

Interest Rates- The most important factor that influences the price of houses in the UK

is the level of interest rates as the general level of interest rates in UK has its own impact on the

mortgage interest rate payments. In UK unlike the rest of the continent, the mortgage interest

payments are variable unlike elsewhere in the continent, where the rates are fixed more or less.

Variable mortgage payments cause the amount of affordability to change which has its own

impact on the demand for houses as mentioned above (Anundsen and Jansen 2013). The rates

being variable fluctuate when the Bank of England announces a change in the base rates of the

mortgage payments. This in turn causes a change in demand as mortgage payments take up a

large portion of the income of an individual’s personal disposable income. The variable

mortgage rate has reduced from 6.50% to 2.05% causing an increase in demand as portrayed in

the following diagram, causing the demand curve to shift to the right from DD to D1D1 and

causing the price to rise from P0 to P1.

Figure 3

Source: Created by author

Interest Rates- The most important factor that influences the price of houses in the UK

is the level of interest rates as the general level of interest rates in UK has its own impact on the

mortgage interest rate payments. In UK unlike the rest of the continent, the mortgage interest

payments are variable unlike elsewhere in the continent, where the rates are fixed more or less.

Variable mortgage payments cause the amount of affordability to change which has its own

impact on the demand for houses as mentioned above (Anundsen and Jansen 2013). The rates

being variable fluctuate when the Bank of England announces a change in the base rates of the

mortgage payments. This in turn causes a change in demand as mortgage payments take up a

large portion of the income of an individual’s personal disposable income. The variable

mortgage rate has reduced from 6.50% to 2.05% causing an increase in demand as portrayed in

the following diagram, causing the demand curve to shift to the right from DD to D1D1 and

causing the price to rise from P0 to P1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FACTORS AFFECTING HOUSING PRICES IN UK

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 4

Source: Created by author

Renting Costs – The cost of renting also contributes significantly, to the demand for

housing and real estate in the UK. Studies suggest that the average cost of renting in UK has

increased by 22%, causing the demand for houses to even rise higher especially after 2011

(Oxley and Smith 2012). This is so because for the population residing, it is a better option to

invest in a house owned rather than paying such high rents. This in turn instigates the buyers to

increase their budget capacity for buying a house. This again causes the demand curve to shift to

the right (from DD to D1D1) and the price to rise from P0 to P1, which is shown in the following

diagram.

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 4

Source: Created by author

Renting Costs – The cost of renting also contributes significantly, to the demand for

housing and real estate in the UK. Studies suggest that the average cost of renting in UK has

increased by 22%, causing the demand for houses to even rise higher especially after 2011

(Oxley and Smith 2012). This is so because for the population residing, it is a better option to

invest in a house owned rather than paying such high rents. This in turn instigates the buyers to

increase their budget capacity for buying a house. This again causes the demand curve to shift to

the right (from DD to D1D1) and the price to rise from P0 to P1, which is shown in the following

diagram.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FACTORS AFFECTING HOUSING PRICES IN UK

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 5

Source: Created by author

Availability of Mortgage- The availability of mortgage also pays an important role in

shaping the demand for housing and real estate. As the number of mortgage instruments are

being reduced by the banks in the UK, the population in UK is finding it difficult to finance the

property. Studies suggest that the Credit Crisis of 2008 led to the fall in availability of finance for

mortgage (Becker, Osborn and Yildirim 2012). This can be explained better with the

understanding of the fact that mortgage lending depends on how strong the inter-bank lending is

in a country. Hence, as this criteria was hampered due to the Credit Crisis of 2008, the number of

mortgages lent and the number of mortgage instruments used fell invariably. This is the only

demand side factor that acts in a way which is different than the rest of the factors (illustrated in

q

p

S

S

D 1

D 1

D

D

P0

P1

Q0 Q1

Figure 5

Source: Created by author

Availability of Mortgage- The availability of mortgage also pays an important role in

shaping the demand for housing and real estate. As the number of mortgage instruments are

being reduced by the banks in the UK, the population in UK is finding it difficult to finance the

property. Studies suggest that the Credit Crisis of 2008 led to the fall in availability of finance for

mortgage (Becker, Osborn and Yildirim 2012). This can be explained better with the

understanding of the fact that mortgage lending depends on how strong the inter-bank lending is

in a country. Hence, as this criteria was hampered due to the Credit Crisis of 2008, the number of

mortgages lent and the number of mortgage instruments used fell invariably. This is the only

demand side factor that acts in a way which is different than the rest of the factors (illustrated in

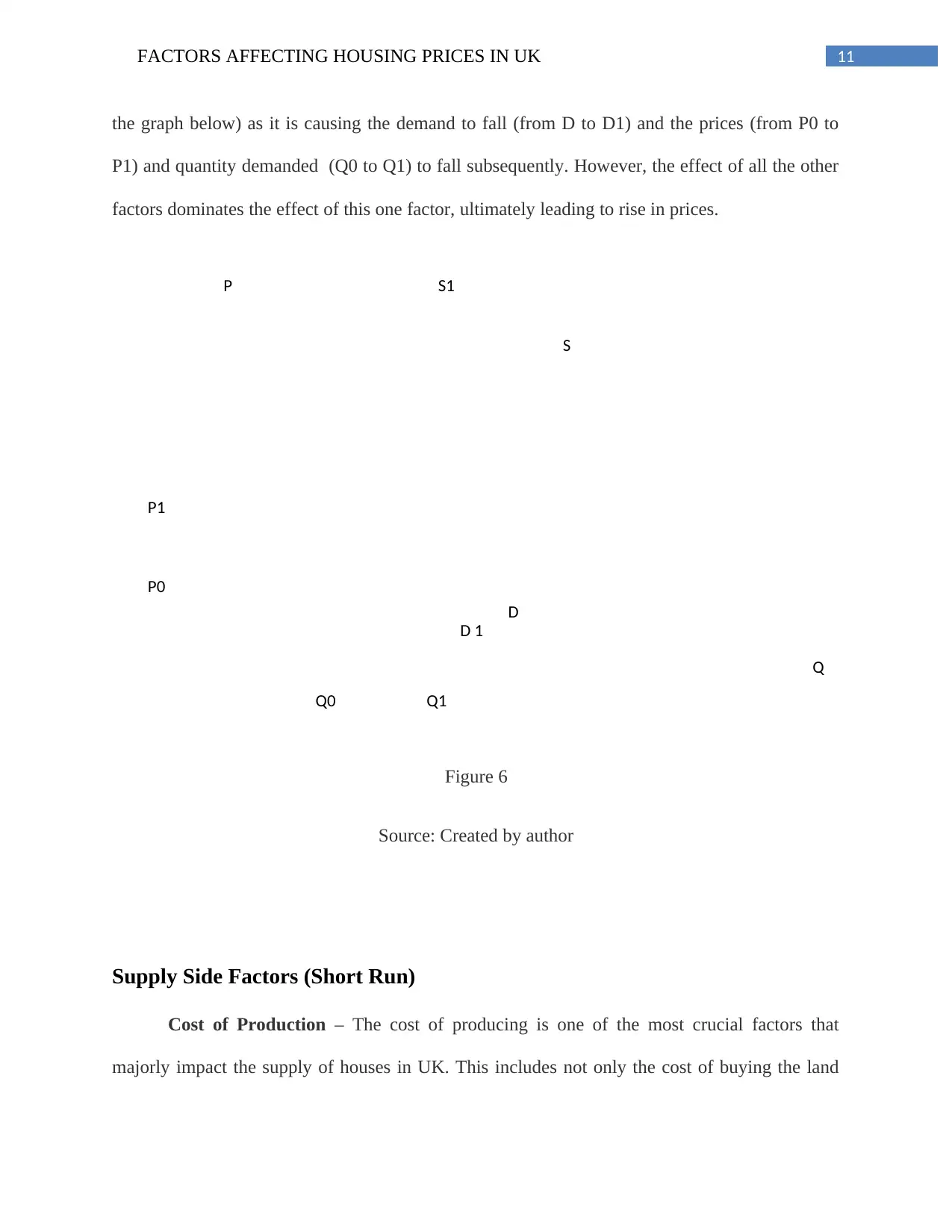

11FACTORS AFFECTING HOUSING PRICES IN UK

P

Q

P1

P0

Q0 Q1

S

S1

D 1

D

the graph below) as it is causing the demand to fall (from D to D1) and the prices (from P0 to

P1) and quantity demanded (Q0 to Q1) to fall subsequently. However, the effect of all the other

factors dominates the effect of this one factor, ultimately leading to rise in prices.

Figure 6

Source: Created by author

Supply Side Factors (Short Run)

Cost of Production – The cost of producing is one of the most crucial factors that

majorly impact the supply of houses in UK. This includes not only the cost of buying the land

P

Q

P1

P0

Q0 Q1

S

S1

D 1

D

the graph below) as it is causing the demand to fall (from D to D1) and the prices (from P0 to

P1) and quantity demanded (Q0 to Q1) to fall subsequently. However, the effect of all the other

factors dominates the effect of this one factor, ultimately leading to rise in prices.

Figure 6

Source: Created by author

Supply Side Factors (Short Run)

Cost of Production – The cost of producing is one of the most crucial factors that

majorly impact the supply of houses in UK. This includes not only the cost of buying the land

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.