Factors Influencing Customer Adoption of Internet Banking in Sri Lanka

VerifiedAdded on 2022/02/14

|20

|7563

|20

Report

AI Summary

This research paper investigates the factors influencing the adoption of internet banking in Sri Lanka, focusing on customer behavior and the challenges banks face in promoting online services. The study, based on an extension of the decomposed theory of planned behavior, examines the impact of attitudes (including innovation characteristics like relative advantage, compatibility, complexity, trialability, and risk), subjective norms, and perceived behavioral control on internet banking adoption. Conducted through an online questionnaire survey in the Colombo and Gampaha districts, the research reveals that attitudinal and perceived behavioral control factors are more significant than social influence in driving adoption. Specifically, relative advantage, compatibility with values, internet skills, trialability, risk perception, self-efficacy, and technology support were found to influence adoption. The study concludes with implications for banks, suggesting the need for pull strategies to encourage internet banking adoption among Sri Lankan customers, where resistance to adopting technology remains a significant issue. The paper also provides a detailed literature review on internet banking, its benefits, and its current status in Sri Lanka, highlighting the gap between awareness and actual usage of online banking services.

68

FACTORS AFFECTING TO CUSTOMER ADOPTION OF

INTERNET BANKING

H.A.H HETTIARACHCHI

Department of Commerce and Financial Management

University of Kelaniya, Sri Lanka

harshaka@kln.ac.lk

Abstract

This paper reports the findings of a study concerning the adoption of internet banking by

investigating consumer adoption within the context of Sri Lankan banking services. The

research framework was based on the extension to decomposed theory of planned behavior

which mainly includes attitude (including innovation characteristics such as relative

advantage, compatibility, complexity, trialability and risk), subjective norms, and perceived

behavioral control to assess internet banking adoption behavior. Online questionnaire survey

was conducted to gather the data and 108 complete responses were gathered from random

banking customers who were internet users from Colombo and Gampaha district. Descriptive

analysis was done to provide strength to the research study which showed that even though

considerable people were aware about internet banking, most of them were resistance to

adopt internet banking. Spearman’s rank correlation was used to examine relationship of

eleven hypotheses with actual internet banking usage. Results revealed that attitudinal and

perceived behavioral control factors rather than social influence (subjective norms) plays a

significant role in influencing adoption of internet banking. In particular relative advantage,

compatibility with values, internet skills, trialability, risk, confidence of using such services

(self-efficacy), and technology support found to influence the adoption of internet banking.

Conclusion of the research study implied that banks have to majorly influence the internet

banking adoption through ‘pull strategies’.

Keywords: Internet Banking, Sri Lanka, Resistance, Adoption, Behavior, Innovation

Introduction

Banking industry in Sri Lanka plays a vital role in managing financial assets. Conventionally

all the banking activities were carried out manually and always customers had to went to the

branch. This has consumed lot of time as well as the cost to both customer as well as bank.

Internet banking is now capturing the banking industry at a rapid phase by eliminating and

FACTORS AFFECTING TO CUSTOMER ADOPTION OF

INTERNET BANKING

H.A.H HETTIARACHCHI

Department of Commerce and Financial Management

University of Kelaniya, Sri Lanka

harshaka@kln.ac.lk

Abstract

This paper reports the findings of a study concerning the adoption of internet banking by

investigating consumer adoption within the context of Sri Lankan banking services. The

research framework was based on the extension to decomposed theory of planned behavior

which mainly includes attitude (including innovation characteristics such as relative

advantage, compatibility, complexity, trialability and risk), subjective norms, and perceived

behavioral control to assess internet banking adoption behavior. Online questionnaire survey

was conducted to gather the data and 108 complete responses were gathered from random

banking customers who were internet users from Colombo and Gampaha district. Descriptive

analysis was done to provide strength to the research study which showed that even though

considerable people were aware about internet banking, most of them were resistance to

adopt internet banking. Spearman’s rank correlation was used to examine relationship of

eleven hypotheses with actual internet banking usage. Results revealed that attitudinal and

perceived behavioral control factors rather than social influence (subjective norms) plays a

significant role in influencing adoption of internet banking. In particular relative advantage,

compatibility with values, internet skills, trialability, risk, confidence of using such services

(self-efficacy), and technology support found to influence the adoption of internet banking.

Conclusion of the research study implied that banks have to majorly influence the internet

banking adoption through ‘pull strategies’.

Keywords: Internet Banking, Sri Lanka, Resistance, Adoption, Behavior, Innovation

Introduction

Banking industry in Sri Lanka plays a vital role in managing financial assets. Conventionally

all the banking activities were carried out manually and always customers had to went to the

branch. This has consumed lot of time as well as the cost to both customer as well as bank.

Internet banking is now capturing the banking industry at a rapid phase by eliminating and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

69

transforming the conventional banking activities to a web based online system. Even though

this enhancement of new technology, recent finding in Sri Lanka illustrates that customers

were more resistance toward adopting such technology even it has more sufficient relative

advantages. It was found that only less than 1% of bank customers, in general, use online

banking, mobile banking, telephone banking and internet payment gateway and although

ATM services are extensively used, the usage of other IT driven services such as online

banking, mobile banking, internet payment gateway and telephone banking is almost

insignificant (Suraweera et al, 2011).

So with this prevailing situation this research study will drive on to identify the significance

of why most Sri Lankans are resistant to adopt internet banking hence these findings are

useful to professionals in the banking sector, especially for developers of such information

systems and the strategy makers, towards taking the banking services to a level commonly

applicable in the developed world today. This study will be looking at in-depth regarding

actual customer perspective on adoption or non-adoption of internet banking thus objective is

to identify factors affecting to adoption of internet banking.

Literature Review

Internet Banking

Internet banking has many names such as online banking, electronic banking, e banking,

virtual banking etc. In general it is a feature introduce by the bank to its customers to log into

their individual registered domain account (through the given username and password) on

bank website (through internet) and do almost every transaction they do by visiting the bank.

Registered internet banking users can perform common banking transactions such as writing

checks, paying bills, transferring funds, printing statements, and inquiring about account

balances etc. Today many banks are internet only banks where no brick and mortar bank

branches. Internet banking services are crucial for long term survival of the banks in the

world of electronic commerce (Burnham, 1996).

Importance of Internet Banking

The main benefits of internet banking to banks are cost saving, reaching new segments of the

population, efficiency, enhancement of the bank’s reputation and better customer service and

satisfaction (Brogdon, 1999; Jayawardhena et al, 2000).Traditional banks operating cost

account for between 50% and 60% of revenues, running costs of internet banking is estimated

at between 15% and 20% of revenues (Booz-Allen & Hamilton, 1997).The cost of an

transforming the conventional banking activities to a web based online system. Even though

this enhancement of new technology, recent finding in Sri Lanka illustrates that customers

were more resistance toward adopting such technology even it has more sufficient relative

advantages. It was found that only less than 1% of bank customers, in general, use online

banking, mobile banking, telephone banking and internet payment gateway and although

ATM services are extensively used, the usage of other IT driven services such as online

banking, mobile banking, internet payment gateway and telephone banking is almost

insignificant (Suraweera et al, 2011).

So with this prevailing situation this research study will drive on to identify the significance

of why most Sri Lankans are resistant to adopt internet banking hence these findings are

useful to professionals in the banking sector, especially for developers of such information

systems and the strategy makers, towards taking the banking services to a level commonly

applicable in the developed world today. This study will be looking at in-depth regarding

actual customer perspective on adoption or non-adoption of internet banking thus objective is

to identify factors affecting to adoption of internet banking.

Literature Review

Internet Banking

Internet banking has many names such as online banking, electronic banking, e banking,

virtual banking etc. In general it is a feature introduce by the bank to its customers to log into

their individual registered domain account (through the given username and password) on

bank website (through internet) and do almost every transaction they do by visiting the bank.

Registered internet banking users can perform common banking transactions such as writing

checks, paying bills, transferring funds, printing statements, and inquiring about account

balances etc. Today many banks are internet only banks where no brick and mortar bank

branches. Internet banking services are crucial for long term survival of the banks in the

world of electronic commerce (Burnham, 1996).

Importance of Internet Banking

The main benefits of internet banking to banks are cost saving, reaching new segments of the

population, efficiency, enhancement of the bank’s reputation and better customer service and

satisfaction (Brogdon, 1999; Jayawardhena et al, 2000).Traditional banks operating cost

account for between 50% and 60% of revenues, running costs of internet banking is estimated

at between 15% and 20% of revenues (Booz-Allen & Hamilton, 1997).The cost of an

70

electronic transaction is dramatically less when done online compare to at a branch

(Robinson, 2000). The single most important driving force behind the implementation of full

service internet banking by banks is the need to create powerful barriers to customer exiting

(Sheshnoff, 2000). He argues that once a customer moves to full service internet banking, the

likelihood of that customer moving to another financial institution is significantly diminished.

A survey in Denmark argued that internet banking might be useful for strengthening cross-

selling and price differentiation (Mols, 1998). Online banking is very useful and powerful

means which leads banking industry towards development, growth. It helps to enhance the

competitiveness of institutions (Kamel, 2005).

From the consumer’s perspective, internet banking provides a very convenient and effective

approach to manage one’s finances as it is easily accessible 24 hours a day, and seven days a

week. Besides, the information is current. With the help of the internet, banking is no longer

bound to time or geography. It has also been argued that electronic banks are more likely to

change in response to customers demand (Brogdon, 1999).Customers can manage their

banking affairs when they want, and they can enjoy more privacy while interacting with their

bank. It has been claimed that internet banking offers the customer more benefits at lower

costs (Mols, 1998).For users, convenience was the key benefit of internet banking

(Dassanayake, 2003). Internet banking is extremely beneficial to customers because of the

saving in costs, time and space it offers, its quick response to complaints, and its delivery of

improved services, all of which benefits make easier banking (Turban, 2000).

Status of Internet Banking in Sri Lanka

As per records in central bank of Sri Lanka currently (2012) there are 24 listed commercial

banks in Sri Lanka from that 12 are local banks who already have the internet banking facility

except Amana bank.

But the dark side of the internet banking in Sri Lanka is, even though majority of the

customers in the country were aware about e-banking facilities, most of them had not been

tried those facilities by themselves. They still pay their bills, withdraw money, check

balances, and deposit cheques at their bank counters much as the traditional way (Jayasiri &

Weerathunga, 2008). Although the banking professionals interviewed by the researchers

themselves are not pleased with this situation, they appear to be contented with the status quo

(Suraweera et al, 2011).Since now internet banking expanding its position from desktop PC

to mobile phone but Sri Lankans still resistance to adopt internet banking is becoming a huge

electronic transaction is dramatically less when done online compare to at a branch

(Robinson, 2000). The single most important driving force behind the implementation of full

service internet banking by banks is the need to create powerful barriers to customer exiting

(Sheshnoff, 2000). He argues that once a customer moves to full service internet banking, the

likelihood of that customer moving to another financial institution is significantly diminished.

A survey in Denmark argued that internet banking might be useful for strengthening cross-

selling and price differentiation (Mols, 1998). Online banking is very useful and powerful

means which leads banking industry towards development, growth. It helps to enhance the

competitiveness of institutions (Kamel, 2005).

From the consumer’s perspective, internet banking provides a very convenient and effective

approach to manage one’s finances as it is easily accessible 24 hours a day, and seven days a

week. Besides, the information is current. With the help of the internet, banking is no longer

bound to time or geography. It has also been argued that electronic banks are more likely to

change in response to customers demand (Brogdon, 1999).Customers can manage their

banking affairs when they want, and they can enjoy more privacy while interacting with their

bank. It has been claimed that internet banking offers the customer more benefits at lower

costs (Mols, 1998).For users, convenience was the key benefit of internet banking

(Dassanayake, 2003). Internet banking is extremely beneficial to customers because of the

saving in costs, time and space it offers, its quick response to complaints, and its delivery of

improved services, all of which benefits make easier banking (Turban, 2000).

Status of Internet Banking in Sri Lanka

As per records in central bank of Sri Lanka currently (2012) there are 24 listed commercial

banks in Sri Lanka from that 12 are local banks who already have the internet banking facility

except Amana bank.

But the dark side of the internet banking in Sri Lanka is, even though majority of the

customers in the country were aware about e-banking facilities, most of them had not been

tried those facilities by themselves. They still pay their bills, withdraw money, check

balances, and deposit cheques at their bank counters much as the traditional way (Jayasiri &

Weerathunga, 2008). Although the banking professionals interviewed by the researchers

themselves are not pleased with this situation, they appear to be contented with the status quo

(Suraweera et al, 2011).Since now internet banking expanding its position from desktop PC

to mobile phone but Sri Lankans still resistance to adopt internet banking is becoming a huge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

71

problem. Due to majority of Sri Lankans are not technology savvy, the banks tend to adopt a

wait and see attitude (Suraweera et al, 2011).

Theoretical Framework

This research study is mainly focus on identifying the factors influencing to adoption of

internet banking in Sri Lanka. The research framework for this study is based on the

extension to decomposed theory of planned behavior (Tan & Teo, 2000).

Extension to Decomposed Theory of Planned Behavior

The theory of planned behavior (TPB) is widely studied model from social psychology which

was extended from the theory of reasoned action (TRA). TPB hypothesized by individual’s

behavioral intension (BI) to perform a behavior is jointly determined by the individual’s

attitude toward performing the behavior (ATB), subjective norm (SN) and perceived

behavioral control (PBC). Taylor and Todd (1995) extended theory of planned behavior by

decomposing the attitude component (as relative advantage, compatibility, complexity, which

were mentioned in diffusion of innovation theory by Rogers, 1983) and perceived behavioral

control component (as self-efficacy and facilitating conditions). Based on the above

decomposed theory of planned behavior, Tan & Teo (2000) extended it to identify the factors

influencing internet banking adoption behavior on Singapore. So this research study is mainly

based on this extended theory of planned behavior and it is composed with;

1) Attitude

Attitude is defined as an individual’s positive and negative feelings (evaluative effect) about

performing target behavior (Fishbein & Ajzen, 1975). The different dimensions of attitudinal

belief toward an innovation can be measured using the five perceived attributes (relative

advantage, compatibility, complexity, trialability and observability) specifically first three

attributes of an innovation (Taylor & Todd, 1995). These attributes were originally proposed

in the diffusion of innovations theory (Rogers, 1983), were applied in this framework with

the exception of observability, which is defined as the degree to which the results of an

innovation are visible to others (Rogers, 1983). Observability was considered irrelevant in

this study because an important characteristic of doing banking is ‘privacy’. Therefore,

observing others using internet banking services may prove difficult unless one makes a

conscious effort to do so (Tan & Teo, 2000).

problem. Due to majority of Sri Lankans are not technology savvy, the banks tend to adopt a

wait and see attitude (Suraweera et al, 2011).

Theoretical Framework

This research study is mainly focus on identifying the factors influencing to adoption of

internet banking in Sri Lanka. The research framework for this study is based on the

extension to decomposed theory of planned behavior (Tan & Teo, 2000).

Extension to Decomposed Theory of Planned Behavior

The theory of planned behavior (TPB) is widely studied model from social psychology which

was extended from the theory of reasoned action (TRA). TPB hypothesized by individual’s

behavioral intension (BI) to perform a behavior is jointly determined by the individual’s

attitude toward performing the behavior (ATB), subjective norm (SN) and perceived

behavioral control (PBC). Taylor and Todd (1995) extended theory of planned behavior by

decomposing the attitude component (as relative advantage, compatibility, complexity, which

were mentioned in diffusion of innovation theory by Rogers, 1983) and perceived behavioral

control component (as self-efficacy and facilitating conditions). Based on the above

decomposed theory of planned behavior, Tan & Teo (2000) extended it to identify the factors

influencing internet banking adoption behavior on Singapore. So this research study is mainly

based on this extended theory of planned behavior and it is composed with;

1) Attitude

Attitude is defined as an individual’s positive and negative feelings (evaluative effect) about

performing target behavior (Fishbein & Ajzen, 1975). The different dimensions of attitudinal

belief toward an innovation can be measured using the five perceived attributes (relative

advantage, compatibility, complexity, trialability and observability) specifically first three

attributes of an innovation (Taylor & Todd, 1995). These attributes were originally proposed

in the diffusion of innovations theory (Rogers, 1983), were applied in this framework with

the exception of observability, which is defined as the degree to which the results of an

innovation are visible to others (Rogers, 1983). Observability was considered irrelevant in

this study because an important characteristic of doing banking is ‘privacy’. Therefore,

observing others using internet banking services may prove difficult unless one makes a

conscious effort to do so (Tan & Teo, 2000).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

72

a) Relative Advantage

Relative advantage is the degree to which an innovation provides benefits which supersede

those of its precursor and may incorporate factors such as economic benefits, images,

enhancement, convenience and satisfaction (Rogers, 1983) . In general relative advantage of

an innovation is positively related to its rate of adoption (Rogers, 1983). Likewise, as internet

banking allows customers to access their banking accounts from any location, at any time of

the day, it provides tremendous advantage and convenience to users. It also gives customers

greater control over managing their finances, as they are able check their accounts easily. In

view of the advantage that internet banking services offer, it would thus be expected that

individuals who perceive internet banking as advantageous would also be likely to adopt the

service (Tan & Teo, 2000). This leads to the hypothesis: 01 (H1A).

b) Compatibility

Compatibility is the degree to which the innovation fits with the potential adopter’s existing

values, previous experience and current needs (Rogers, 1983). An innovation is more likely

to be adopted when it is compatible with individual’s job responsibilities and value system

(Tornatzky & Klein, 1982). Internet banking has been viewed as a delivery channel that is

compatible with the profile of the modern day banking customer, who is likely to be

computer-literate and familiar with the internet. Therefore, it is expected that the more the

individual uses the internet, and the more he or she perceives the internet as compatible with

his or her life style, the more likely that the individual will adopt internet banking (Tan &

Teo, 2000). Thus, the hypotheses are: 02 (H1B), 03 (H1C).

In terms of compatibility with needs of the potential adopters, internet banking can be seen as

an expeditious tool that allows customers to better manage their multiple accounts. As there

are more financial products and services, it is expected that individuals who may have many

financial accounts and who subscribe to many banking services will be more inclined to

adopt internet banking (Tan & Teo, 2000). This leads to the following hypothesis: 04 (H1D).

c) Complexity

Compatibility is the degree to which an innovation is perceived to be difficult to understand,

learn or operate (Rogers, 1983). An innovation with substantial complexity requires more

technical skills and needs greater implementation and operational efforts to increase its

chances of adoption. As the internet is very user friendly with its “point and click” interface,

it is likely that potential customers may feel that internet banking services are less complex to

a) Relative Advantage

Relative advantage is the degree to which an innovation provides benefits which supersede

those of its precursor and may incorporate factors such as economic benefits, images,

enhancement, convenience and satisfaction (Rogers, 1983) . In general relative advantage of

an innovation is positively related to its rate of adoption (Rogers, 1983). Likewise, as internet

banking allows customers to access their banking accounts from any location, at any time of

the day, it provides tremendous advantage and convenience to users. It also gives customers

greater control over managing their finances, as they are able check their accounts easily. In

view of the advantage that internet banking services offer, it would thus be expected that

individuals who perceive internet banking as advantageous would also be likely to adopt the

service (Tan & Teo, 2000). This leads to the hypothesis: 01 (H1A).

b) Compatibility

Compatibility is the degree to which the innovation fits with the potential adopter’s existing

values, previous experience and current needs (Rogers, 1983). An innovation is more likely

to be adopted when it is compatible with individual’s job responsibilities and value system

(Tornatzky & Klein, 1982). Internet banking has been viewed as a delivery channel that is

compatible with the profile of the modern day banking customer, who is likely to be

computer-literate and familiar with the internet. Therefore, it is expected that the more the

individual uses the internet, and the more he or she perceives the internet as compatible with

his or her life style, the more likely that the individual will adopt internet banking (Tan &

Teo, 2000). Thus, the hypotheses are: 02 (H1B), 03 (H1C).

In terms of compatibility with needs of the potential adopters, internet banking can be seen as

an expeditious tool that allows customers to better manage their multiple accounts. As there

are more financial products and services, it is expected that individuals who may have many

financial accounts and who subscribe to many banking services will be more inclined to

adopt internet banking (Tan & Teo, 2000). This leads to the following hypothesis: 04 (H1D).

c) Complexity

Compatibility is the degree to which an innovation is perceived to be difficult to understand,

learn or operate (Rogers, 1983). An innovation with substantial complexity requires more

technical skills and needs greater implementation and operational efforts to increase its

chances of adoption. As the internet is very user friendly with its “point and click” interface,

it is likely that potential customers may feel that internet banking services are less complex to

73

use, and hence would be likely to use such services (Tan & Teo, 2000). This leads to the

hypothesis: 05 (H1E).

d) Trialability

Trialability is the degree to which an innovation may be experimented with on a limited basis

(Rogers, 1983).Potential adopters who are allowed to experiment with an innovation will feel

more comfortable with the innovation and are more likely to adopt it (Rogers, 1983). Thus, if

customers are given the opportunity to try the innovation, certain fears of the unknown may

be minimized. This is especially true when customers find that mistakes could be rectified,

thus providing a predictable situation (Tan & Teo, 2000). This leads to the hypothesis: 06

(H1F).

e) Risk

A common and widely recognized obstacle to electronic commerce adoption has been the

lack of security and privacy over internet. Its demonstrate risk as an additional dimension in

diffusion and adoption. This has led many to view internet commerce as a risky undertaking.

Thus, it is expected that only individuals who perceive using internet banking as a low risk

undertaking would be inclined to adopt it (Tan & Teo, 2000). This leads to the hypothesis: 07

(H1G).

2) Subjective Norms

Subjective norms refer to the person’s perception that most people who are important to

him/her think he/she should or should not perform the behavior in question (Fishbein &

Ajzen, 1975). It is related to behavior because people often act based on their perception of

what others think they should do. Subjective norms have been found to be more important

prior to, or in the early stages of innovation implementation when users have limited direct

experience from which to develop attitudes (Taylor & Todd, 1995). Most of the consumer-

oriented services, the consumer-relevant groups around the individual may influence the

individual’ adoption. Adopter’s friends, family, and colleagues/peers are groups that will

potentially influence the adoption (Tan & Teo, 2000). Although there is no basis on which to

predict how each of these groups will affect adoption of internet banking, it is nonetheless

expected that the influence of these groups as a whole will be significantly related to the

individual’s adoption internet banking (Tan & Teo, 2000). Therefore, hypothesis: 08 (H2)

warrants investigation.

use, and hence would be likely to use such services (Tan & Teo, 2000). This leads to the

hypothesis: 05 (H1E).

d) Trialability

Trialability is the degree to which an innovation may be experimented with on a limited basis

(Rogers, 1983).Potential adopters who are allowed to experiment with an innovation will feel

more comfortable with the innovation and are more likely to adopt it (Rogers, 1983). Thus, if

customers are given the opportunity to try the innovation, certain fears of the unknown may

be minimized. This is especially true when customers find that mistakes could be rectified,

thus providing a predictable situation (Tan & Teo, 2000). This leads to the hypothesis: 06

(H1F).

e) Risk

A common and widely recognized obstacle to electronic commerce adoption has been the

lack of security and privacy over internet. Its demonstrate risk as an additional dimension in

diffusion and adoption. This has led many to view internet commerce as a risky undertaking.

Thus, it is expected that only individuals who perceive using internet banking as a low risk

undertaking would be inclined to adopt it (Tan & Teo, 2000). This leads to the hypothesis: 07

(H1G).

2) Subjective Norms

Subjective norms refer to the person’s perception that most people who are important to

him/her think he/she should or should not perform the behavior in question (Fishbein &

Ajzen, 1975). It is related to behavior because people often act based on their perception of

what others think they should do. Subjective norms have been found to be more important

prior to, or in the early stages of innovation implementation when users have limited direct

experience from which to develop attitudes (Taylor & Todd, 1995). Most of the consumer-

oriented services, the consumer-relevant groups around the individual may influence the

individual’ adoption. Adopter’s friends, family, and colleagues/peers are groups that will

potentially influence the adoption (Tan & Teo, 2000). Although there is no basis on which to

predict how each of these groups will affect adoption of internet banking, it is nonetheless

expected that the influence of these groups as a whole will be significantly related to the

individual’s adoption internet banking (Tan & Teo, 2000). Therefore, hypothesis: 08 (H2)

warrants investigation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

74

3) Perceived Behavioral Control

Perceived behavioral control refers to the factors that may impede the performance of the

behavior. This definition encompasses two components.

The first component is “self-efficacy” and is defined as an individual’s self-confidence in

his or her ability to perform a behavior.

The second component is “facilitating conditions” and it reflects the availability of

resources needed to engage in the behavior.

Self-efficacy predicts intentions to use a wide range of technologically advanced products.

Thus, an individual confident in having the skills in using the computer and the internet is

more inclined to adopt internet banking. This is because the individual is comfortable in

using the innovation (Tan & Teo, 2000). This leads to the hypothesis: 09 (H3A).

The second component, facilitating conditions refers to the easy access of technological

resources and infrastructure. The government can play an intervention and leadership role in

the diffusion of innovation. Potential users, in turn would view new applications such as

internet banking services more favorably and hence be more likely to use them (Tan & Teo,

2000). The above arguments lead to the hypotheses: 10 (H3B).

As supporting technological infrastructures become easily and readily available, internet

commerce applications such as banking services will also become more feasible. As a result,

internet users would be expected to be more inclined to adopt internet banking. This leads to

hypotheses: 11 (H3C).

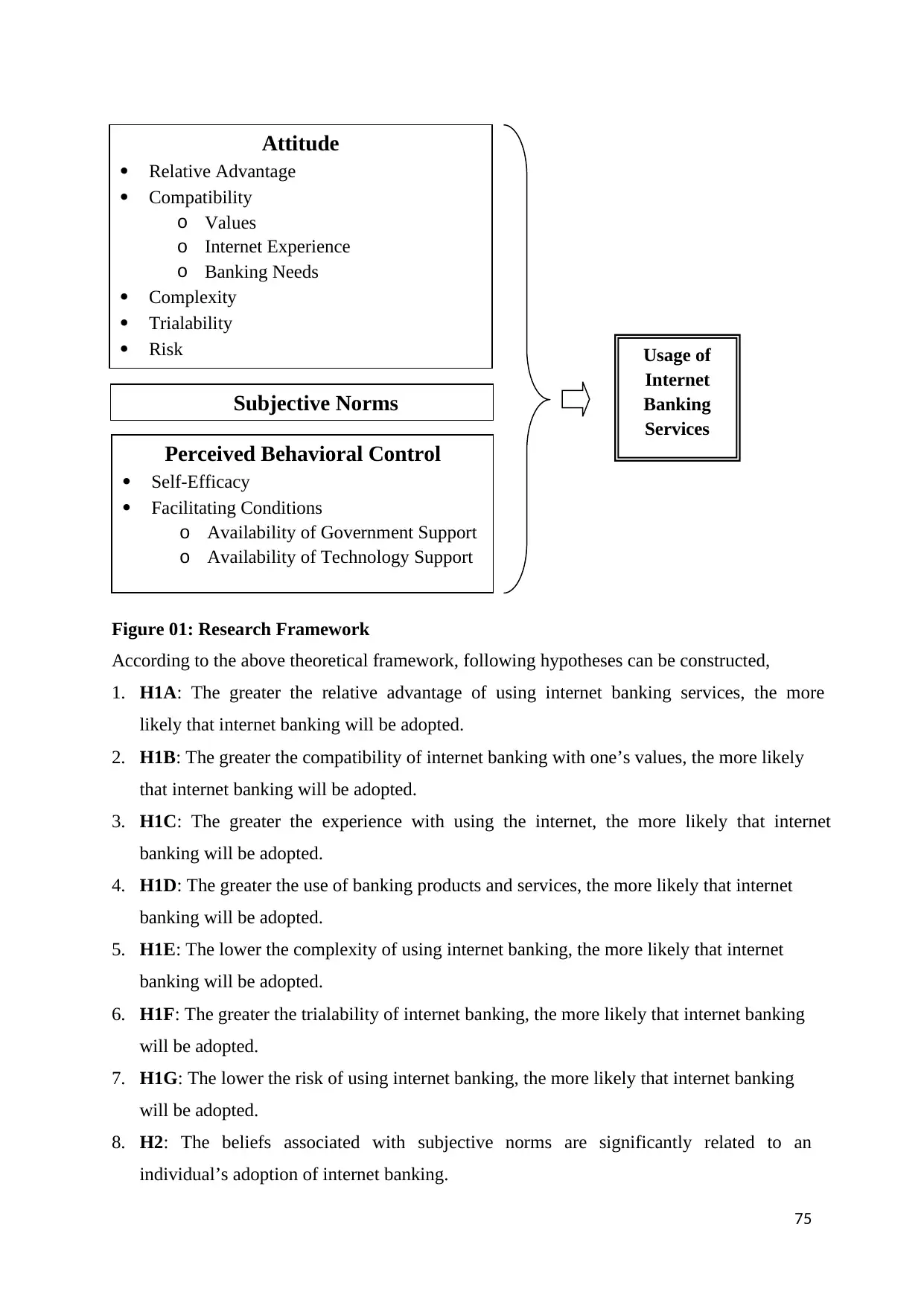

Research Framework

The research framework for this study is based on an extension to decomposed TPB which

developed to assess internet banking adoption in Singapore by Tan & Teo (2000). According

to Taylor and Todd, intension to adopt certain technology in return is expected to affect

actual adoption of such technology. Like that, intention to adopt internet banking services, in

return, is expected to affect the actual adoption of internet banking (Tan & Teo, 2000).So in

this research study ‘intention to adopt’ is exempted from this Tan & Teo’s (2000) framework

since intention obviously lead to actual behavior. Also in this research study it is mainly

focused on observing the actual internet banking usage behavior rather than intention to

perform actual behavior thus then it is possible to assess factors affecting to actual adoption

or non-adoption of internet banking. Figure 01 show the relevant research framework use for

this study which was designed based on extension to decomposed TPB.

3) Perceived Behavioral Control

Perceived behavioral control refers to the factors that may impede the performance of the

behavior. This definition encompasses two components.

The first component is “self-efficacy” and is defined as an individual’s self-confidence in

his or her ability to perform a behavior.

The second component is “facilitating conditions” and it reflects the availability of

resources needed to engage in the behavior.

Self-efficacy predicts intentions to use a wide range of technologically advanced products.

Thus, an individual confident in having the skills in using the computer and the internet is

more inclined to adopt internet banking. This is because the individual is comfortable in

using the innovation (Tan & Teo, 2000). This leads to the hypothesis: 09 (H3A).

The second component, facilitating conditions refers to the easy access of technological

resources and infrastructure. The government can play an intervention and leadership role in

the diffusion of innovation. Potential users, in turn would view new applications such as

internet banking services more favorably and hence be more likely to use them (Tan & Teo,

2000). The above arguments lead to the hypotheses: 10 (H3B).

As supporting technological infrastructures become easily and readily available, internet

commerce applications such as banking services will also become more feasible. As a result,

internet users would be expected to be more inclined to adopt internet banking. This leads to

hypotheses: 11 (H3C).

Research Framework

The research framework for this study is based on an extension to decomposed TPB which

developed to assess internet banking adoption in Singapore by Tan & Teo (2000). According

to Taylor and Todd, intension to adopt certain technology in return is expected to affect

actual adoption of such technology. Like that, intention to adopt internet banking services, in

return, is expected to affect the actual adoption of internet banking (Tan & Teo, 2000).So in

this research study ‘intention to adopt’ is exempted from this Tan & Teo’s (2000) framework

since intention obviously lead to actual behavior. Also in this research study it is mainly

focused on observing the actual internet banking usage behavior rather than intention to

perform actual behavior thus then it is possible to assess factors affecting to actual adoption

or non-adoption of internet banking. Figure 01 show the relevant research framework use for

this study which was designed based on extension to decomposed TPB.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

75

Figure

Figure 01: Research Framework

According to the above theoretical framework, following hypotheses can be constructed,

1. H1A: The greater the relative advantage of using internet banking services, the more

likely that internet banking will be adopted.

2. H1B: The greater the compatibility of internet banking with one’s values, the more likely

that internet banking will be adopted.

3. H1C: The greater the experience with using the internet, the more likely that internet

banking will be adopted.

4. H1D: The greater the use of banking products and services, the more likely that internet

banking will be adopted.

5. H1E: The lower the complexity of using internet banking, the more likely that internet

banking will be adopted.

6. H1F: The greater the trialability of internet banking, the more likely that internet banking

will be adopted.

7. H1G: The lower the risk of using internet banking, the more likely that internet banking

will be adopted.

8. H2: The beliefs associated with subjective norms are significantly related to an

individual’s adoption of internet banking.

Attitude

Relative Advantage

Compatibility

o Values

o Internet Experience

o Banking Needs

Complexity

Trialability

Risk Usage of

Internet

Banking

Services

Subjective Norms

Perceived Behavioral Control

Self-Efficacy

Facilitating Conditions

o Availability of Government Support

o Availability of Technology Support

Figure

Figure 01: Research Framework

According to the above theoretical framework, following hypotheses can be constructed,

1. H1A: The greater the relative advantage of using internet banking services, the more

likely that internet banking will be adopted.

2. H1B: The greater the compatibility of internet banking with one’s values, the more likely

that internet banking will be adopted.

3. H1C: The greater the experience with using the internet, the more likely that internet

banking will be adopted.

4. H1D: The greater the use of banking products and services, the more likely that internet

banking will be adopted.

5. H1E: The lower the complexity of using internet banking, the more likely that internet

banking will be adopted.

6. H1F: The greater the trialability of internet banking, the more likely that internet banking

will be adopted.

7. H1G: The lower the risk of using internet banking, the more likely that internet banking

will be adopted.

8. H2: The beliefs associated with subjective norms are significantly related to an

individual’s adoption of internet banking.

Attitude

Relative Advantage

Compatibility

o Values

o Internet Experience

o Banking Needs

Complexity

Trialability

Risk Usage of

Internet

Banking

Services

Subjective Norms

Perceived Behavioral Control

Self-Efficacy

Facilitating Conditions

o Availability of Government Support

o Availability of Technology Support

76

9. H3A: The greater the self-efficacy toward using internet banking, the more likely that

internet banking will be adopted.

10. H3B: The greater the extent of government support for internet banking, the more likely

that internet banking will be adopted.

11. H3C: The greater the extent of technological support for internet banking, the more likely

that internet banking will be adopted.

Research Methodology

The main goal of this study is to identify the factors influencing adoption of internet banking

from customer’s point of view thus the most appropriate strategy is quantitative survey. The

online questionnaire method is used because the internet is the most suitable medium through

which to reach the desired sample of internet users hence the findings can only apply to

internet users rather than general population (Tan & Teo, 2000). So in this study it was

justifiable to get data from internet users in order to apply Sri Lanka as a whole. Also internet

users were considered because it was assumed that in order to be familiar with internet

banking, respondents have at least familiar with internet and on the other hand emails users

were assumed to be internet users where this research gathered data through emails. Among

the provinces the highest computer awareness of 51% is reported by the western province and

highest email use of 18.5% is reported from western province thus the pattern of using the

internet among provinces is similar to the pattern of email use and it is important to note that

the higher the use of internet higher the use of email (Media Center for National

Development of Sri Lanka, 2010). Based on above statistics sample population of this study

was limited to Colombo and Gampaha district banking customers, who were internet users or

rather email users since most of the computer and internet savvy people live in these districts.

Also in order to use internet banking, respondents should be bank customers obviously since

non-banking customer doesn’t have any intention of using internet banking. In order to get

responses online and the link of this questionnaire was attached to email message and send it

to desired individuals thus simple random sampling technique was used. 15 days were

allocated to get the responses. From the 180 personalized emails sent 108 responses were

collected which were complete with no missing data. So the sample size was 108 and the

response rate was 60%.

Reliability

Cronbach’s coefficient alpha was computed to test for reliability extracting the first 20

respondents’ data (table 01).As a standard mechanism it is suggested to have minimum 0.6

9. H3A: The greater the self-efficacy toward using internet banking, the more likely that

internet banking will be adopted.

10. H3B: The greater the extent of government support for internet banking, the more likely

that internet banking will be adopted.

11. H3C: The greater the extent of technological support for internet banking, the more likely

that internet banking will be adopted.

Research Methodology

The main goal of this study is to identify the factors influencing adoption of internet banking

from customer’s point of view thus the most appropriate strategy is quantitative survey. The

online questionnaire method is used because the internet is the most suitable medium through

which to reach the desired sample of internet users hence the findings can only apply to

internet users rather than general population (Tan & Teo, 2000). So in this study it was

justifiable to get data from internet users in order to apply Sri Lanka as a whole. Also internet

users were considered because it was assumed that in order to be familiar with internet

banking, respondents have at least familiar with internet and on the other hand emails users

were assumed to be internet users where this research gathered data through emails. Among

the provinces the highest computer awareness of 51% is reported by the western province and

highest email use of 18.5% is reported from western province thus the pattern of using the

internet among provinces is similar to the pattern of email use and it is important to note that

the higher the use of internet higher the use of email (Media Center for National

Development of Sri Lanka, 2010). Based on above statistics sample population of this study

was limited to Colombo and Gampaha district banking customers, who were internet users or

rather email users since most of the computer and internet savvy people live in these districts.

Also in order to use internet banking, respondents should be bank customers obviously since

non-banking customer doesn’t have any intention of using internet banking. In order to get

responses online and the link of this questionnaire was attached to email message and send it

to desired individuals thus simple random sampling technique was used. 15 days were

allocated to get the responses. From the 180 personalized emails sent 108 responses were

collected which were complete with no missing data. So the sample size was 108 and the

response rate was 60%.

Reliability

Cronbach’s coefficient alpha was computed to test for reliability extracting the first 20

respondents’ data (table 01).As a standard mechanism it is suggested to have minimum 0.6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

77

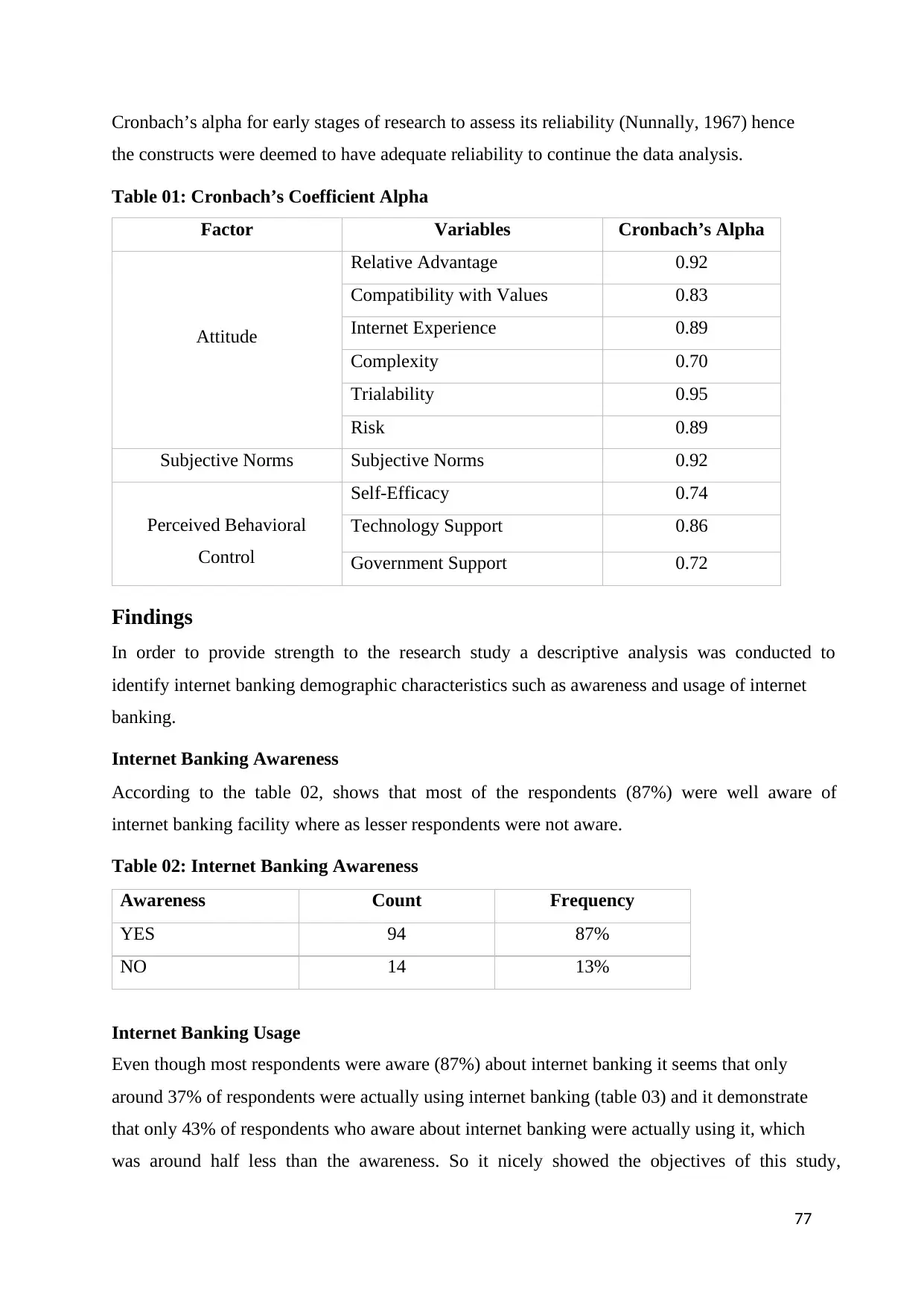

Cronbach’s alpha for early stages of research to assess its reliability (Nunnally, 1967) hence

the constructs were deemed to have adequate reliability to continue the data analysis.

Table 01: Cronbach’s Coefficient Alpha

Factor Variables Cronbach’s Alpha

Attitude

Relative Advantage 0.92

Compatibility with Values 0.83

Internet Experience 0.89

Complexity 0.70

Trialability 0.95

Risk 0.89

Subjective Norms Subjective Norms 0.92

Perceived Behavioral

Control

Self-Efficacy 0.74

Technology Support 0.86

Government Support 0.72

Findings

In order to provide strength to the research study a descriptive analysis was conducted to

identify internet banking demographic characteristics such as awareness and usage of internet

banking.

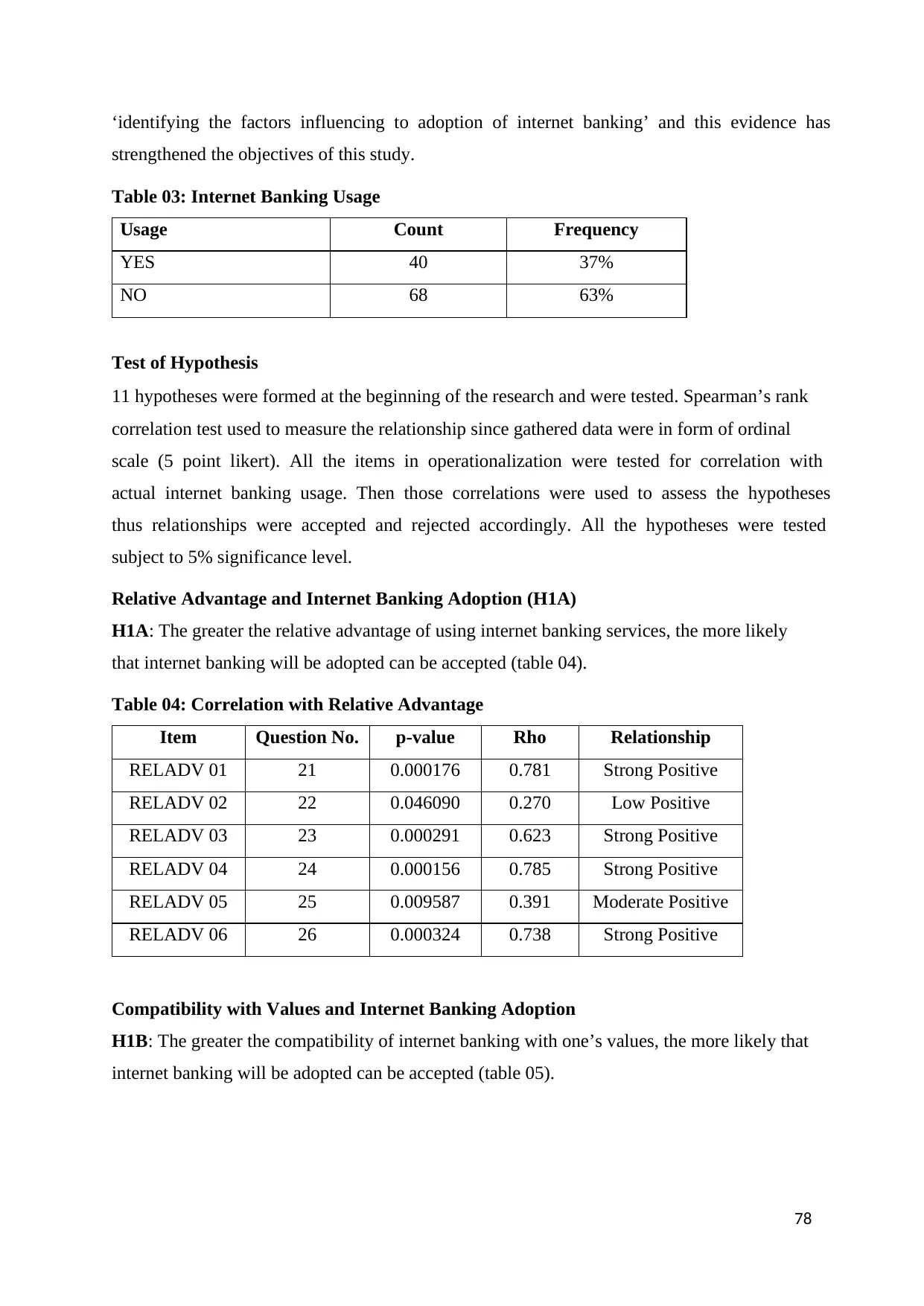

Internet Banking Awareness

According to the table 02, shows that most of the respondents (87%) were well aware of

internet banking facility where as lesser respondents were not aware.

Table 02: Internet Banking Awareness

Awareness Count Frequency

YES 94 87%

NO 14 13%

Internet Banking Usage

Even though most respondents were aware (87%) about internet banking it seems that only

around 37% of respondents were actually using internet banking (table 03) and it demonstrate

that only 43% of respondents who aware about internet banking were actually using it, which

was around half less than the awareness. So it nicely showed the objectives of this study,

Cronbach’s alpha for early stages of research to assess its reliability (Nunnally, 1967) hence

the constructs were deemed to have adequate reliability to continue the data analysis.

Table 01: Cronbach’s Coefficient Alpha

Factor Variables Cronbach’s Alpha

Attitude

Relative Advantage 0.92

Compatibility with Values 0.83

Internet Experience 0.89

Complexity 0.70

Trialability 0.95

Risk 0.89

Subjective Norms Subjective Norms 0.92

Perceived Behavioral

Control

Self-Efficacy 0.74

Technology Support 0.86

Government Support 0.72

Findings

In order to provide strength to the research study a descriptive analysis was conducted to

identify internet banking demographic characteristics such as awareness and usage of internet

banking.

Internet Banking Awareness

According to the table 02, shows that most of the respondents (87%) were well aware of

internet banking facility where as lesser respondents were not aware.

Table 02: Internet Banking Awareness

Awareness Count Frequency

YES 94 87%

NO 14 13%

Internet Banking Usage

Even though most respondents were aware (87%) about internet banking it seems that only

around 37% of respondents were actually using internet banking (table 03) and it demonstrate

that only 43% of respondents who aware about internet banking were actually using it, which

was around half less than the awareness. So it nicely showed the objectives of this study,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

78

‘identifying the factors influencing to adoption of internet banking’ and this evidence has

strengthened the objectives of this study.

Table 03: Internet Banking Usage

Usage Count Frequency

YES 40 37%

NO 68 63%

Test of Hypothesis

11 hypotheses were formed at the beginning of the research and were tested. Spearman’s rank

correlation test used to measure the relationship since gathered data were in form of ordinal

scale (5 point likert). All the items in operationalization were tested for correlation with

actual internet banking usage. Then those correlations were used to assess the hypotheses

thus relationships were accepted and rejected accordingly. All the hypotheses were tested

subject to 5% significance level.

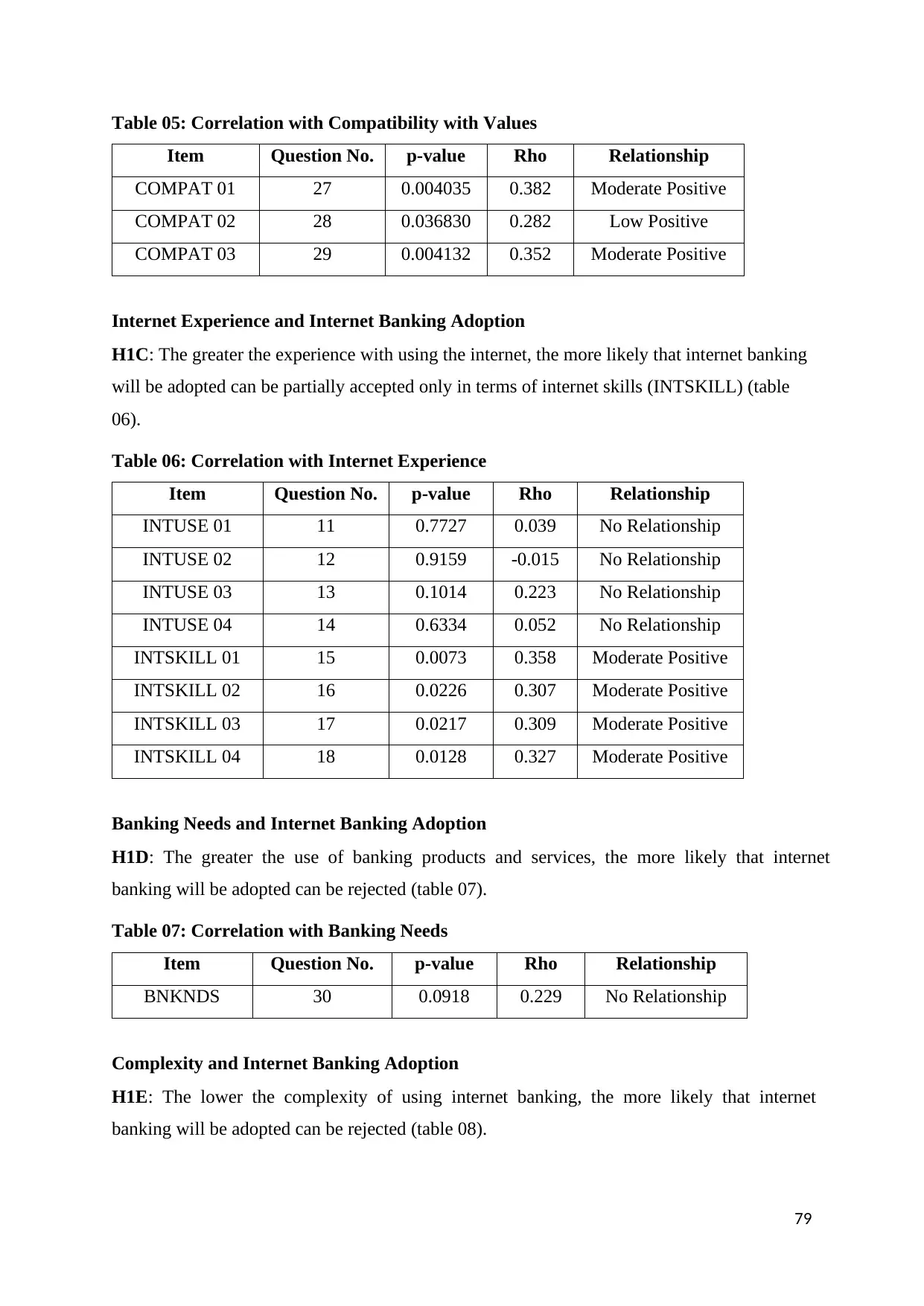

Relative Advantage and Internet Banking Adoption (H1A)

H1A: The greater the relative advantage of using internet banking services, the more likely

that internet banking will be adopted can be accepted (table 04).

Table 04: Correlation with Relative Advantage

Item Question No. p-value Rho Relationship

RELADV 01 21 0.000176 0.781 Strong Positive

RELADV 02 22 0.046090 0.270 Low Positive

RELADV 03 23 0.000291 0.623 Strong Positive

RELADV 04 24 0.000156 0.785 Strong Positive

RELADV 05 25 0.009587 0.391 Moderate Positive

RELADV 06 26 0.000324 0.738 Strong Positive

Compatibility with Values and Internet Banking Adoption

H1B: The greater the compatibility of internet banking with one’s values, the more likely that

internet banking will be adopted can be accepted (table 05).

‘identifying the factors influencing to adoption of internet banking’ and this evidence has

strengthened the objectives of this study.

Table 03: Internet Banking Usage

Usage Count Frequency

YES 40 37%

NO 68 63%

Test of Hypothesis

11 hypotheses were formed at the beginning of the research and were tested. Spearman’s rank

correlation test used to measure the relationship since gathered data were in form of ordinal

scale (5 point likert). All the items in operationalization were tested for correlation with

actual internet banking usage. Then those correlations were used to assess the hypotheses

thus relationships were accepted and rejected accordingly. All the hypotheses were tested

subject to 5% significance level.

Relative Advantage and Internet Banking Adoption (H1A)

H1A: The greater the relative advantage of using internet banking services, the more likely

that internet banking will be adopted can be accepted (table 04).

Table 04: Correlation with Relative Advantage

Item Question No. p-value Rho Relationship

RELADV 01 21 0.000176 0.781 Strong Positive

RELADV 02 22 0.046090 0.270 Low Positive

RELADV 03 23 0.000291 0.623 Strong Positive

RELADV 04 24 0.000156 0.785 Strong Positive

RELADV 05 25 0.009587 0.391 Moderate Positive

RELADV 06 26 0.000324 0.738 Strong Positive

Compatibility with Values and Internet Banking Adoption

H1B: The greater the compatibility of internet banking with one’s values, the more likely that

internet banking will be adopted can be accepted (table 05).

79

Table 05: Correlation with Compatibility with Values

Item Question No. p-value Rho Relationship

COMPAT 01 27 0.004035 0.382 Moderate Positive

COMPAT 02 28 0.036830 0.282 Low Positive

COMPAT 03 29 0.004132 0.352 Moderate Positive

Internet Experience and Internet Banking Adoption

H1C: The greater the experience with using the internet, the more likely that internet banking

will be adopted can be partially accepted only in terms of internet skills (INTSKILL) (table

06).

Table 06: Correlation with Internet Experience

Item Question No. p-value Rho Relationship

INTUSE 01 11 0.7727 0.039 No Relationship

INTUSE 02 12 0.9159 -0.015 No Relationship

INTUSE 03 13 0.1014 0.223 No Relationship

INTUSE 04 14 0.6334 0.052 No Relationship

INTSKILL 01 15 0.0073 0.358 Moderate Positive

INTSKILL 02 16 0.0226 0.307 Moderate Positive

INTSKILL 03 17 0.0217 0.309 Moderate Positive

INTSKILL 04 18 0.0128 0.327 Moderate Positive

Banking Needs and Internet Banking Adoption

H1D: The greater the use of banking products and services, the more likely that internet

banking will be adopted can be rejected (table 07).

Table 07: Correlation with Banking Needs

Item Question No. p-value Rho Relationship

BNKNDS 30 0.0918 0.229 No Relationship

Complexity and Internet Banking Adoption

H1E: The lower the complexity of using internet banking, the more likely that internet

banking will be adopted can be rejected (table 08).

Table 05: Correlation with Compatibility with Values

Item Question No. p-value Rho Relationship

COMPAT 01 27 0.004035 0.382 Moderate Positive

COMPAT 02 28 0.036830 0.282 Low Positive

COMPAT 03 29 0.004132 0.352 Moderate Positive

Internet Experience and Internet Banking Adoption

H1C: The greater the experience with using the internet, the more likely that internet banking

will be adopted can be partially accepted only in terms of internet skills (INTSKILL) (table

06).

Table 06: Correlation with Internet Experience

Item Question No. p-value Rho Relationship

INTUSE 01 11 0.7727 0.039 No Relationship

INTUSE 02 12 0.9159 -0.015 No Relationship

INTUSE 03 13 0.1014 0.223 No Relationship

INTUSE 04 14 0.6334 0.052 No Relationship

INTSKILL 01 15 0.0073 0.358 Moderate Positive

INTSKILL 02 16 0.0226 0.307 Moderate Positive

INTSKILL 03 17 0.0217 0.309 Moderate Positive

INTSKILL 04 18 0.0128 0.327 Moderate Positive

Banking Needs and Internet Banking Adoption

H1D: The greater the use of banking products and services, the more likely that internet

banking will be adopted can be rejected (table 07).

Table 07: Correlation with Banking Needs

Item Question No. p-value Rho Relationship

BNKNDS 30 0.0918 0.229 No Relationship

Complexity and Internet Banking Adoption

H1E: The lower the complexity of using internet banking, the more likely that internet

banking will be adopted can be rejected (table 08).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.