Impact of ISO 9000 Factors on Company Performance: A Detailed Study

VerifiedAdded on 2021/05/31

|25

|5081

|347

Report

AI Summary

This report investigates the impact of ISO 9000 certification on company performance, focusing on 25 key factors. The study examines the determinants of ISO 9000 adoption, comparing certified and non-certified Chinese firms across various metrics, including revenue, profit, and employee education levels. The research employs statistical methods, such as t-tests and ANOVA, to analyze the data from a Chinese database, revealing significant differences in performance between ISO-certified and non-certified companies. The findings highlight the importance of ISO 9000 certification for quality improvement, cost reduction, and business growth, offering insights for policy makers and academics alike. The report also explores the concept of ISO 9000 disguise and its influence on organizational behavior.

1

Factors of ISO 9000 and its Impact on

Company Performance

Factors of ISO 9000 and its Impact on

Company Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The motivation behind this paper was to build up the operational meaning of the idea of

disguise of ISO 9000, a hypothetical develop which scrutinize the merits in examine on

quality administration. An arrangement of particular elements and sub factors went for an

operation of the ISO 9000 disguise develop were proposed. The idea of not implementing the

compliance and enjoying the facilities of the norms instead was an unmistakably important

point, as in past works found in the writing in different nations, the conclusion was drawn

that associations don't embrace ISO 9000 homogeneously. The conclusions might be of

intrigue both for scholarly and proficient circles of movement. For administrators, the key

parts of a substantive selection of ISO 9000 were featured. For scholastics, certain particular

order components were proposed for a significant build so that these might be utilized as a

part of resulting works. ISO certification has turned into an inescapable instrument received

by firms to enhance their operational execution. In this paper, we look at the operational and

authoritative variables that improve the probability of receiving ISO certification and the

effect that ISO certification and proprietorship structure have upon firm execution. In any

case, our outcomes show that the positive effect of ISO certification on execution lessens in

firms where possession was much thought. Unique review information on Chinese firms was

examined, whether there was a distinction in the determinants of International Organization

for Standardization 9000 affirmation between the important factors for growth and

administration segments. Utilizing an experimental approach, discoveries uncover out that the

factors of ISO 9000 confirmation fundamentally vary amongst employee and administration

factors of the firms, particularly for quality change, cost diminishment and development of

these organizations. The consequences of this investigation could empower strategy

producers to better detail and adequately apply controls influencing the business

accomplishment of firms in both the assembling and administration segments.

Executive Summary

The motivation behind this paper was to build up the operational meaning of the idea of

disguise of ISO 9000, a hypothetical develop which scrutinize the merits in examine on

quality administration. An arrangement of particular elements and sub factors went for an

operation of the ISO 9000 disguise develop were proposed. The idea of not implementing the

compliance and enjoying the facilities of the norms instead was an unmistakably important

point, as in past works found in the writing in different nations, the conclusion was drawn

that associations don't embrace ISO 9000 homogeneously. The conclusions might be of

intrigue both for scholarly and proficient circles of movement. For administrators, the key

parts of a substantive selection of ISO 9000 were featured. For scholastics, certain particular

order components were proposed for a significant build so that these might be utilized as a

part of resulting works. ISO certification has turned into an inescapable instrument received

by firms to enhance their operational execution. In this paper, we look at the operational and

authoritative variables that improve the probability of receiving ISO certification and the

effect that ISO certification and proprietorship structure have upon firm execution. In any

case, our outcomes show that the positive effect of ISO certification on execution lessens in

firms where possession was much thought. Unique review information on Chinese firms was

examined, whether there was a distinction in the determinants of International Organization

for Standardization 9000 affirmation between the important factors for growth and

administration segments. Utilizing an experimental approach, discoveries uncover out that the

factors of ISO 9000 confirmation fundamentally vary amongst employee and administration

factors of the firms, particularly for quality change, cost diminishment and development of

these organizations. The consequences of this investigation could empower strategy

producers to better detail and adequately apply controls influencing the business

accomplishment of firms in both the assembling and administration segments.

3

Table of Contents

Executive Summary........................................................................................................................................ 2

Introduction....................................................................................................................................................... 4

Literature Review............................................................................................................................................ 5

Methodology...................................................................................................................................................... 6

Data Analysis..................................................................................................................................................... 7

Descriptive Analysis................................................................................................................................... 7

Inferential Analysis.................................................................................................................................. 11

Discussion and Recommendations........................................................................................................ 15

Limitation and Future scope..................................................................................................................... 16

References........................................................................................................................................................ 17

Appendix A....................................................................................................................................................... 20

Appendix B....................................................................................................................................................... 21

Appendix C: Regression Model................................................................................................................ 25

Table of Contents

Executive Summary........................................................................................................................................ 2

Introduction....................................................................................................................................................... 4

Literature Review............................................................................................................................................ 5

Methodology...................................................................................................................................................... 6

Data Analysis..................................................................................................................................................... 7

Descriptive Analysis................................................................................................................................... 7

Inferential Analysis.................................................................................................................................. 11

Discussion and Recommendations........................................................................................................ 15

Limitation and Future scope..................................................................................................................... 16

References........................................................................................................................................................ 17

Appendix A....................................................................................................................................................... 20

Appendix B....................................................................................................................................................... 21

Appendix C: Regression Model................................................................................................................ 25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

Firms don't act autonomously in light of the fact that they rely upon the authenticity forced by

institutional situations. In this manner, they were compelled to consolidate basic components,

practices, methods, and systems that were considered as an objective intends to acknowledge

hierarchical objectives. A portion of these prerequisites could be accomplished by the

reception of monetary frameworks, the significance of which has become enormously

important in the most recent decade. The across the board acknowledgment of monetary

frameworks has been ascribed in extraordinary part to the limit of those frameworks to

promote the existence of the establishment of a predominantly focused situation for them.

The International Organization for Standardization prepared the ISO 9000 accreditation that

determines necessities for a quality administration framework to show that a firm consents to

the client and administrative prerequisites. ISO Survey of Certifications 2013 confirms

around 1,129,000 firms which have been confirmed worldwide to ISO 9000 benchmarks in

189 countries. Thusly, the fundamental issue of enthusiasm for the institutional financial

writing has been the authenticity and effectiveness picks upcoming about because of the

usage of institutional quality-arranged procedures, for example, ISO 9000 confirmation. In

any case, a predetermined number of observational examinations have come across to figure

out the factors of the ISO 9000 certification (Lo et al., 2013). Surveys of such degree were

obligatory and imperative in light of the fact that theoretically stranded observational

exploration focus into the factors of ISO 9000. Affirmation can contribute noteworthy bits of

knowledge into firms' authoritative conduct by clarifying why certain kinds of firms look for

ISO 9000 affirmation while others don't. Firms were adopting for ISO 9000 accreditation

even with less number of customers. Though there was not enough significance for every

industry section, still ISO 9000 affirmation facilitates to grow the business from many angles.

Introduction

Firms don't act autonomously in light of the fact that they rely upon the authenticity forced by

institutional situations. In this manner, they were compelled to consolidate basic components,

practices, methods, and systems that were considered as an objective intends to acknowledge

hierarchical objectives. A portion of these prerequisites could be accomplished by the

reception of monetary frameworks, the significance of which has become enormously

important in the most recent decade. The across the board acknowledgment of monetary

frameworks has been ascribed in extraordinary part to the limit of those frameworks to

promote the existence of the establishment of a predominantly focused situation for them.

The International Organization for Standardization prepared the ISO 9000 accreditation that

determines necessities for a quality administration framework to show that a firm consents to

the client and administrative prerequisites. ISO Survey of Certifications 2013 confirms

around 1,129,000 firms which have been confirmed worldwide to ISO 9000 benchmarks in

189 countries. Thusly, the fundamental issue of enthusiasm for the institutional financial

writing has been the authenticity and effectiveness picks upcoming about because of the

usage of institutional quality-arranged procedures, for example, ISO 9000 confirmation. In

any case, a predetermined number of observational examinations have come across to figure

out the factors of the ISO 9000 certification (Lo et al., 2013). Surveys of such degree were

obligatory and imperative in light of the fact that theoretically stranded observational

exploration focus into the factors of ISO 9000. Affirmation can contribute noteworthy bits of

knowledge into firms' authoritative conduct by clarifying why certain kinds of firms look for

ISO 9000 affirmation while others don't. Firms were adopting for ISO 9000 accreditation

even with less number of customers. Though there was not enough significance for every

industry section, still ISO 9000 affirmation facilitates to grow the business from many angles.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Literature Review

Hypothetical structure, writing audit, and research question call attention to that disguise of

the ISO 9000 standard involves a dynamic utilization of hidden practices to adjust conduct

and basic leadership (Abe, Bassett & Dempsey, 2012). These creators construct their work in

light of learning creation; one of the hypothetical structures that have been advanced in this

writing is to examine the interrelationships between ISO 9000 and information of the

administration. They maintain that administration frameworks. Those concealed the QM

frameworks (QMS) of ISO 9000 guidelines; contain unequivocal and verifiable types of

implanted information (Martínez-Costa et al., 2009). Data progresses toward becoming

learning when it was deciphered by people, given a specific circumstance, and moored into

the convictions and duties of people (Beitsch, Yeager & Moran, 2015). Express information

was a goal and balanced learning that was without setting; it speaks to the systematized

rendition of the data that can be put away and transmitted (Rafiquzzaman et al., 2017). Then

again, unsaid learning was subjective and encounters based information that can't be caught

in words and put away what's more, transmitted, frequently in light of the fact that it was

setting particular; this likewise incorporates intellectual abilities, for example, convictions

and instinct and also specialized aptitudes (Du, Yin & Zhang, 2016). As worried by disguise

was especially important to the examination of ISO 9000 benchmarks as it speaks to the way

toward retaining both implicit and unequivocal data into the association and making an

interpretation of it into information (Dahlgaard, Khanji & Kristensen, 2008). As underlined,

QMS proposed by ISO 9000 can be viewed as one sort of encoded information and can

encourage learning to stockpile, information exchange lastly, learning application (Ahmed,

2017). Moreover, as underlined, ISO 9000 empowers data sharing as a key to defeat the

correspondence obstructions existing in associations (Lin & Jang, 2008). Among these works,

specify ought to be made of a paper that was taken as a kind of perspective in our work which

adds to hypothesis and practice by propelling comprehension of the elaboration of ISO 9000

norms, in view of broadly referenced past works (Helena, Monteiro, & Lee 2008). Moreover,

there likewise exist different works that may likewise be of intrigue, despite the fact that they

might be founded on somewhat extraordinary systems and ideas (Foley et al, 2008). The

African perspective of the internal policies for ISO compliance was studied and a positive

correlation with ISO certification was observed (Fikru, 2016). In Ethiopian scenario same

sort of results were evident, positive effect of ISO 9001, 14001 and employee size of the

Literature Review

Hypothetical structure, writing audit, and research question call attention to that disguise of

the ISO 9000 standard involves a dynamic utilization of hidden practices to adjust conduct

and basic leadership (Abe, Bassett & Dempsey, 2012). These creators construct their work in

light of learning creation; one of the hypothetical structures that have been advanced in this

writing is to examine the interrelationships between ISO 9000 and information of the

administration. They maintain that administration frameworks. Those concealed the QM

frameworks (QMS) of ISO 9000 guidelines; contain unequivocal and verifiable types of

implanted information (Martínez-Costa et al., 2009). Data progresses toward becoming

learning when it was deciphered by people, given a specific circumstance, and moored into

the convictions and duties of people (Beitsch, Yeager & Moran, 2015). Express information

was a goal and balanced learning that was without setting; it speaks to the systematized

rendition of the data that can be put away and transmitted (Rafiquzzaman et al., 2017). Then

again, unsaid learning was subjective and encounters based information that can't be caught

in words and put away what's more, transmitted, frequently in light of the fact that it was

setting particular; this likewise incorporates intellectual abilities, for example, convictions

and instinct and also specialized aptitudes (Du, Yin & Zhang, 2016). As worried by disguise

was especially important to the examination of ISO 9000 benchmarks as it speaks to the way

toward retaining both implicit and unequivocal data into the association and making an

interpretation of it into information (Dahlgaard, Khanji & Kristensen, 2008). As underlined,

QMS proposed by ISO 9000 can be viewed as one sort of encoded information and can

encourage learning to stockpile, information exchange lastly, learning application (Ahmed,

2017). Moreover, as underlined, ISO 9000 empowers data sharing as a key to defeat the

correspondence obstructions existing in associations (Lin & Jang, 2008). Among these works,

specify ought to be made of a paper that was taken as a kind of perspective in our work which

adds to hypothesis and practice by propelling comprehension of the elaboration of ISO 9000

norms, in view of broadly referenced past works (Helena, Monteiro, & Lee 2008). Moreover,

there likewise exist different works that may likewise be of intrigue, despite the fact that they

might be founded on somewhat extraordinary systems and ideas (Foley et al, 2008). The

African perspective of the internal policies for ISO compliance was studied and a positive

correlation with ISO certification was observed (Fikru, 2016). In Ethiopian scenario same

sort of results were evident, positive effect of ISO 9001, 14001 and employee size of the

6

firms were constructively correlated with growth of the firms (Fikru, 2014a). In late 20th

century Japanese firms realised the positive aspect of ISO compliance and started to adapt the

norms for their firms (Nakamura, Takahashi & Vertinsky, 2001). Notwithstanding, as we

should endeavour to content underneath, from the audit of observational writing influenced it

to can be determined that subjective experimental research was required keeping in mind the

end goal to build up the operational meaning of the idea of ISO 9000 disguise, which in this

manner legitimizes our work being completed.

Methodology

The current paper was created in four overlays. An observational method has been utilized to

narrow the gap in the writing by exploring the probability of firms embracing ISO 9000

affirmation. Furthermore, this paper gives vital bits of knowledge into how the assembling

and administration divisions see and draw in with ISO 9000 authentication Thirdly, we take

contention, proposing that it was vital to investigate the elements that clarify the selection of

a worldwide standard at its beginning times since they may vary from the components that

clarify its later reception. Subsequently, inspections were done for to differentiate between

the adopters and defaulters (Cao & Prakash, 2011). A unique Chinese database from National

Bureau of Statistics has allowed exploring the extent of the factors of ISO 9000 confirmation.

In the following segment, a hypothetical reason to the ISO 9000 confirmation and detail

theories has been depicted. Three hypotheses were tested in the inferential analysis.

Firstly, it was hypothesized that,

H10: sales and profit of companies were independent of ISO 9000 complaint factor.

Secondly,

H20: Return on assets and return on sales were hypothesized to be indifferent to ISO certified

and a non-certified case, this study was separately done based on FDI status.

In the third hypothesis,

H30: Capital from state and overseas for both ISO statuses was compared considering them

to be same.

firms were constructively correlated with growth of the firms (Fikru, 2014a). In late 20th

century Japanese firms realised the positive aspect of ISO compliance and started to adapt the

norms for their firms (Nakamura, Takahashi & Vertinsky, 2001). Notwithstanding, as we

should endeavour to content underneath, from the audit of observational writing influenced it

to can be determined that subjective experimental research was required keeping in mind the

end goal to build up the operational meaning of the idea of ISO 9000 disguise, which in this

manner legitimizes our work being completed.

Methodology

The current paper was created in four overlays. An observational method has been utilized to

narrow the gap in the writing by exploring the probability of firms embracing ISO 9000

affirmation. Furthermore, this paper gives vital bits of knowledge into how the assembling

and administration divisions see and draw in with ISO 9000 authentication Thirdly, we take

contention, proposing that it was vital to investigate the elements that clarify the selection of

a worldwide standard at its beginning times since they may vary from the components that

clarify its later reception. Subsequently, inspections were done for to differentiate between

the adopters and defaulters (Cao & Prakash, 2011). A unique Chinese database from National

Bureau of Statistics has allowed exploring the extent of the factors of ISO 9000 confirmation.

In the following segment, a hypothetical reason to the ISO 9000 confirmation and detail

theories has been depicted. Three hypotheses were tested in the inferential analysis.

Firstly, it was hypothesized that,

H10: sales and profit of companies were independent of ISO 9000 complaint factor.

Secondly,

H20: Return on assets and return on sales were hypothesized to be indifferent to ISO certified

and a non-certified case, this study was separately done based on FDI status.

In the third hypothesis,

H30: Capital from state and overseas for both ISO statuses was compared considering them

to be same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Data Analysis

Descriptive Analysis

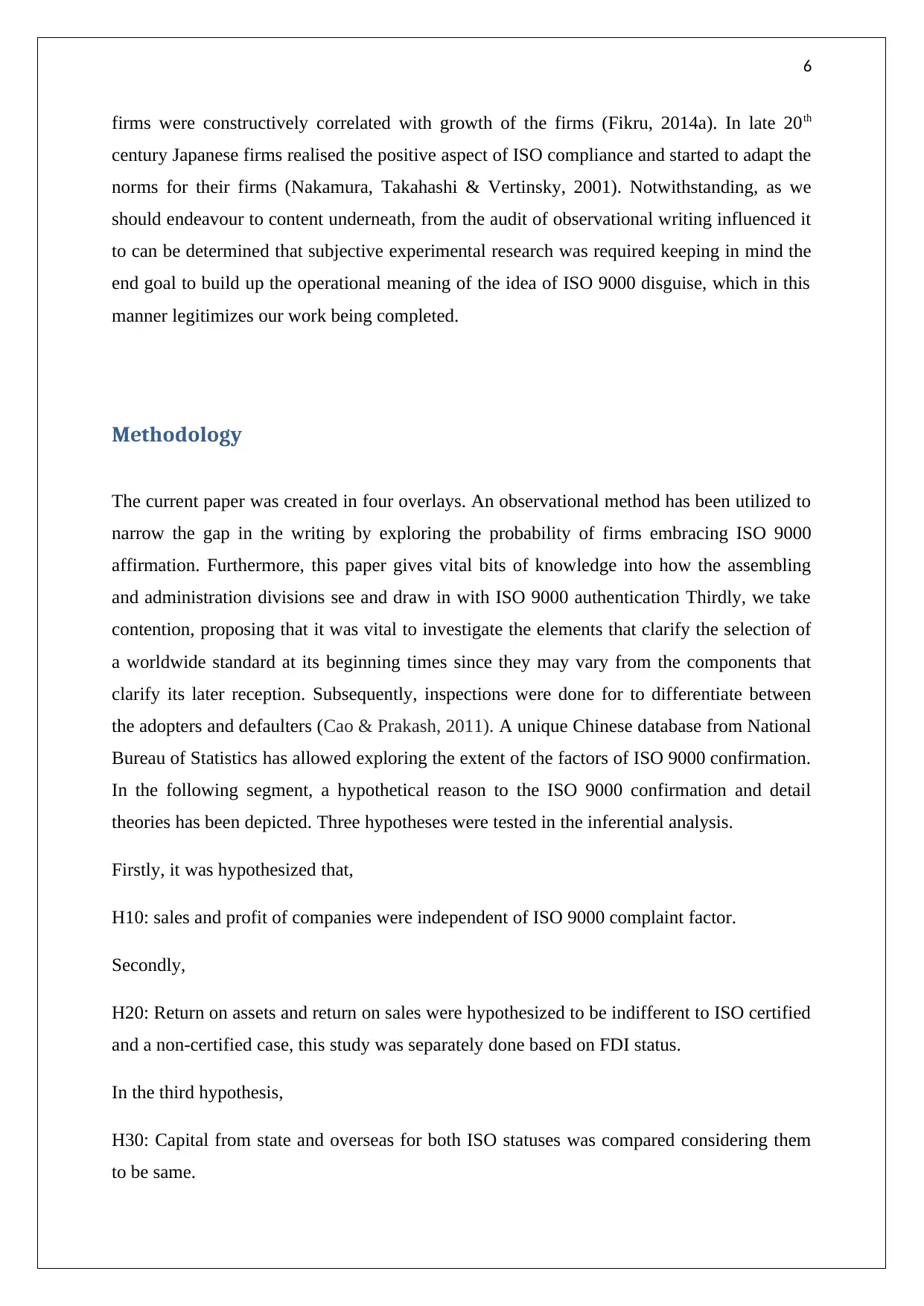

Research data were collected from the database of National Bureau of Statistics of China.

The data were collected in an economic survey in 2008 and the description of the variables

has been provided in the appendix section. The database was considered reliable due to its

source. Total 5717 company data were available, where 460 companies were ISO 9000

registered and rest of 5257 companies were non-ISO 9000 complaint companies. The average

and standard deviation of all the variables (scale variable) has been provided in table 1 and

table 2, based on ISO 9000 complaint and non-complaint companies. Revenue and sales of

the firms were taken as dependent variables in the research work.

Table 1: Variables and Descriptive Statistics for Non-ISO Certified Companies

Descriptive for Not ISO 9000 certified

Companies (5257)

Variable Mean Std.

Deviation

master and doctor 1.10 4.71

bachelor 9.49 23.27

diploma 11.34 20.95

high school 11.63 28.71

other 6.54 25.92

sales 10132.88 29617.09

profit 1865.26 6911.27

asset 14981.12 53574.92

equity 6899.36 30642.06

capital paid 4371.79 16971.71

capital from state 1138.29 11427.34

capital from overseas 329.61 4650.86

capital from other 2903.90 11278.13

return on sales 0.19 0.12

return on asset 0.23 0.21

percentage of FDI 0.02 0.15

FDI dummy 0.03 0.17

age of company in years 7.39 6.82

Data Analysis

Descriptive Analysis

Research data were collected from the database of National Bureau of Statistics of China.

The data were collected in an economic survey in 2008 and the description of the variables

has been provided in the appendix section. The database was considered reliable due to its

source. Total 5717 company data were available, where 460 companies were ISO 9000

registered and rest of 5257 companies were non-ISO 9000 complaint companies. The average

and standard deviation of all the variables (scale variable) has been provided in table 1 and

table 2, based on ISO 9000 complaint and non-complaint companies. Revenue and sales of

the firms were taken as dependent variables in the research work.

Table 1: Variables and Descriptive Statistics for Non-ISO Certified Companies

Descriptive for Not ISO 9000 certified

Companies (5257)

Variable Mean Std.

Deviation

master and doctor 1.10 4.71

bachelor 9.49 23.27

diploma 11.34 20.95

high school 11.63 28.71

other 6.54 25.92

sales 10132.88 29617.09

profit 1865.26 6911.27

asset 14981.12 53574.92

equity 6899.36 30642.06

capital paid 4371.79 16971.71

capital from state 1138.29 11427.34

capital from overseas 329.61 4650.86

capital from other 2903.90 11278.13

return on sales 0.19 0.12

return on asset 0.23 0.21

percentage of FDI 0.02 0.15

FDI dummy 0.03 0.17

age of company in years 7.39 6.82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

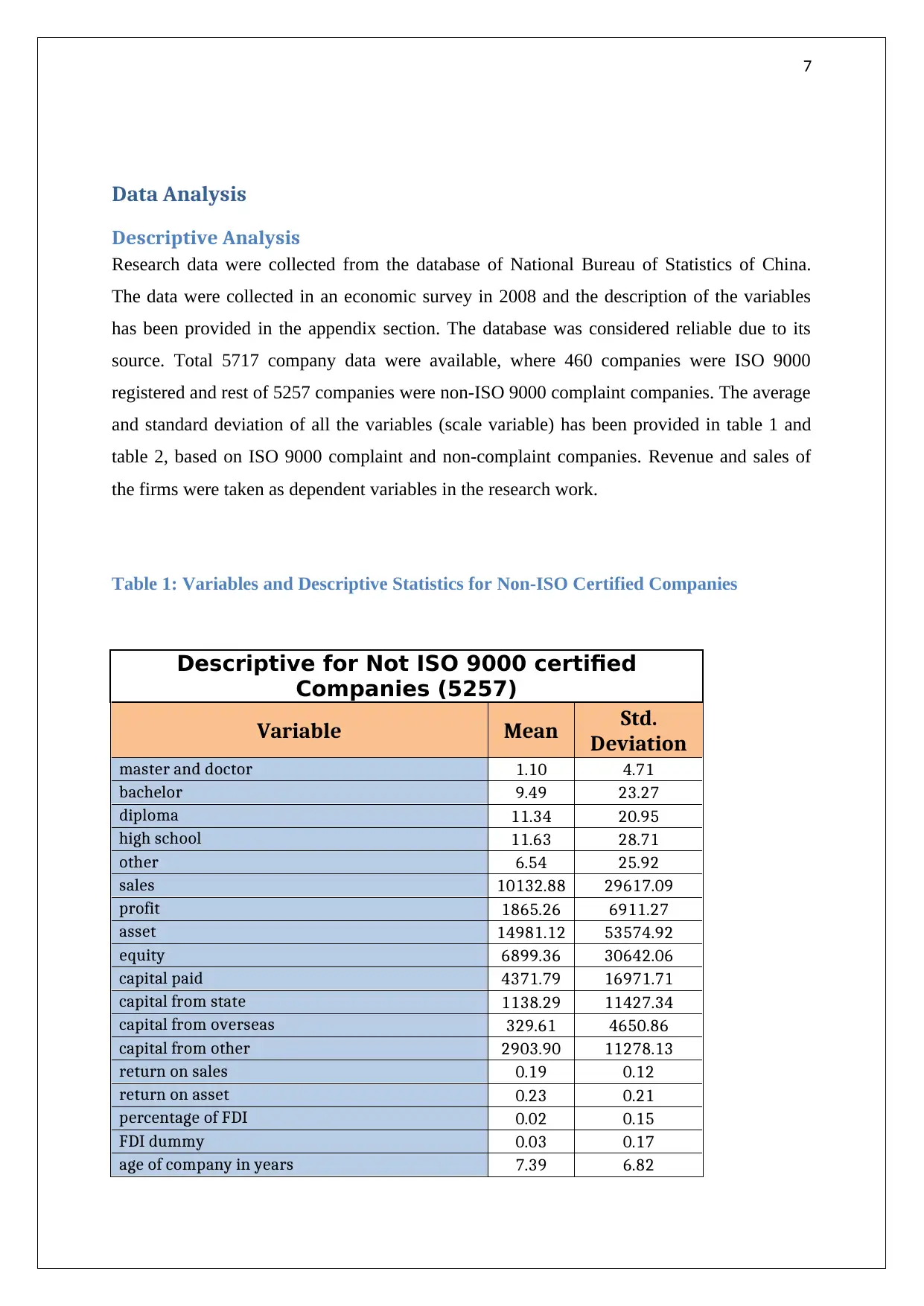

Comparative observation of employee status revealed that for ISO compliant companies’

average number of employees with higher education was significantly greater than non-ISO

9000 complaint companies. Though there was a remarkable difference in standard deviation,

it only signified the variability in the educational background of the employees. Other two

important fields were sales and amount of capital invested in the companies. ISO complaint

companies had a higher average in these two aspects as well. This was although explained by

the average age of the companies. The mean age of ISO 9000 authenticated companies

revealed that established companies had mainly enrolled for the ISO authentication compared

to new fold companies in China.

Figure 1: Change of Revenue with year of certification

Comparative observation of employee status revealed that for ISO compliant companies’

average number of employees with higher education was significantly greater than non-ISO

9000 complaint companies. Though there was a remarkable difference in standard deviation,

it only signified the variability in the educational background of the employees. Other two

important fields were sales and amount of capital invested in the companies. ISO complaint

companies had a higher average in these two aspects as well. This was although explained by

the average age of the companies. The mean age of ISO 9000 authenticated companies

revealed that established companies had mainly enrolled for the ISO authentication compared

to new fold companies in China.

Figure 1: Change of Revenue with year of certification

9

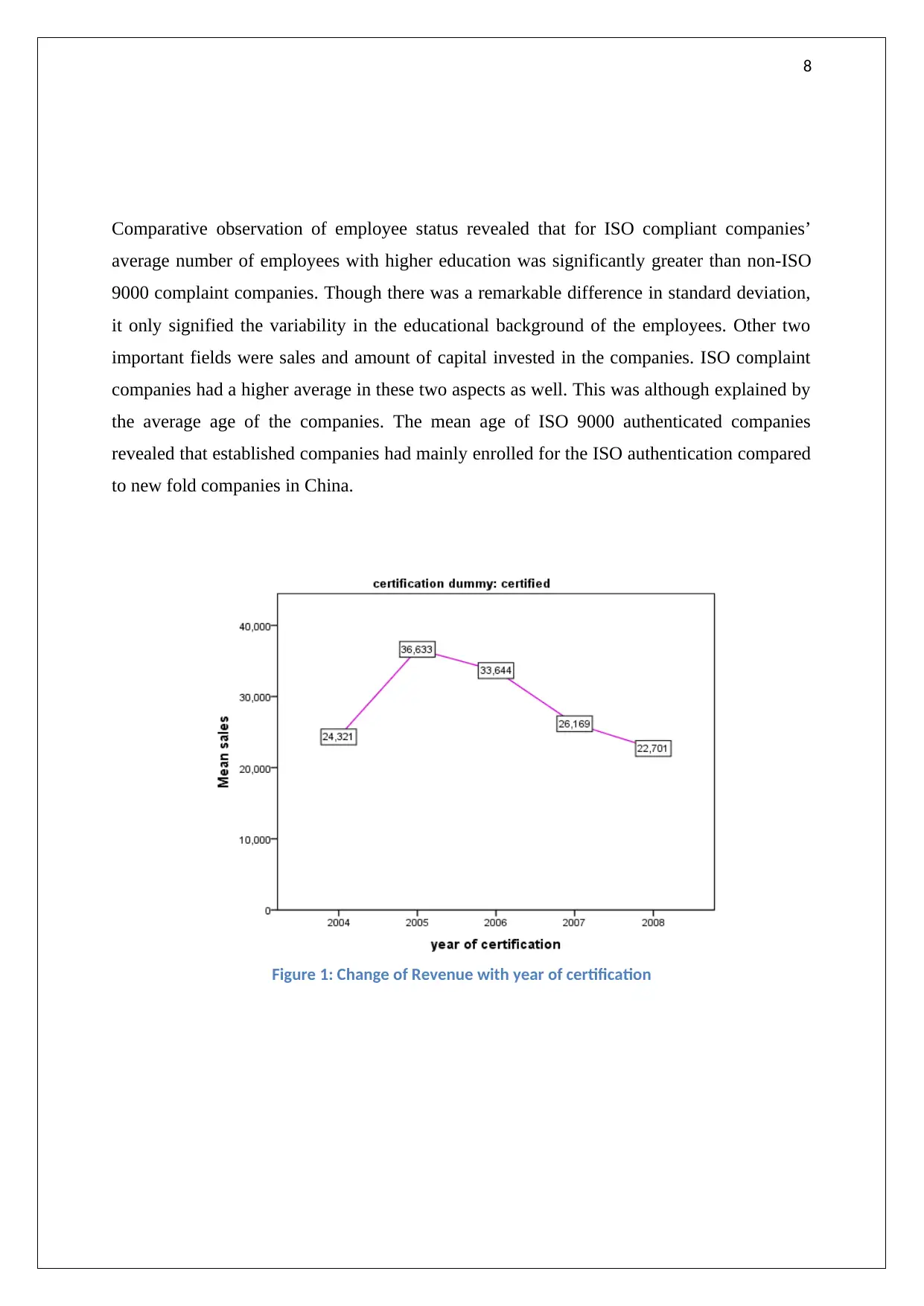

Table 2: Variables and Descriptive Statistics for ISO Certified Companies

Descriptive for ISO 9000 certified Companies

(460)

Variable Mean Std.

Deviation

master and doctor 4.54 11.73

bachelor 38.83 55.59

diploma 31.00 44.44

high school 19.52 51.92

other 6.64 26.65

sales 29591.67 55356.92

profit 4384.67 9237.04

asset 33524.54 63491.07

equity 16772.57 33693.40

capital paid 9267.01 18155.24

capital from state 1919.22 9187.62

capital from overseas 569.00 3953.45

capital from other 6778.79 15922.06

return on sales 0.15 0.12

return on asset 0.17 0.17

percentage of FDI 0.03 0.15

FDI dummy 0.03 0.18

age of company in years 10.28 9.14

Table 2: Variables and Descriptive Statistics for ISO Certified Companies

Descriptive for ISO 9000 certified Companies

(460)

Variable Mean Std.

Deviation

master and doctor 4.54 11.73

bachelor 38.83 55.59

diploma 31.00 44.44

high school 19.52 51.92

other 6.64 26.65

sales 29591.67 55356.92

profit 4384.67 9237.04

asset 33524.54 63491.07

equity 16772.57 33693.40

capital paid 9267.01 18155.24

capital from state 1919.22 9187.62

capital from overseas 569.00 3953.45

capital from other 6778.79 15922.06

return on sales 0.15 0.12

return on asset 0.17 0.17

percentage of FDI 0.03 0.15

FDI dummy 0.03 0.18

age of company in years 10.28 9.14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

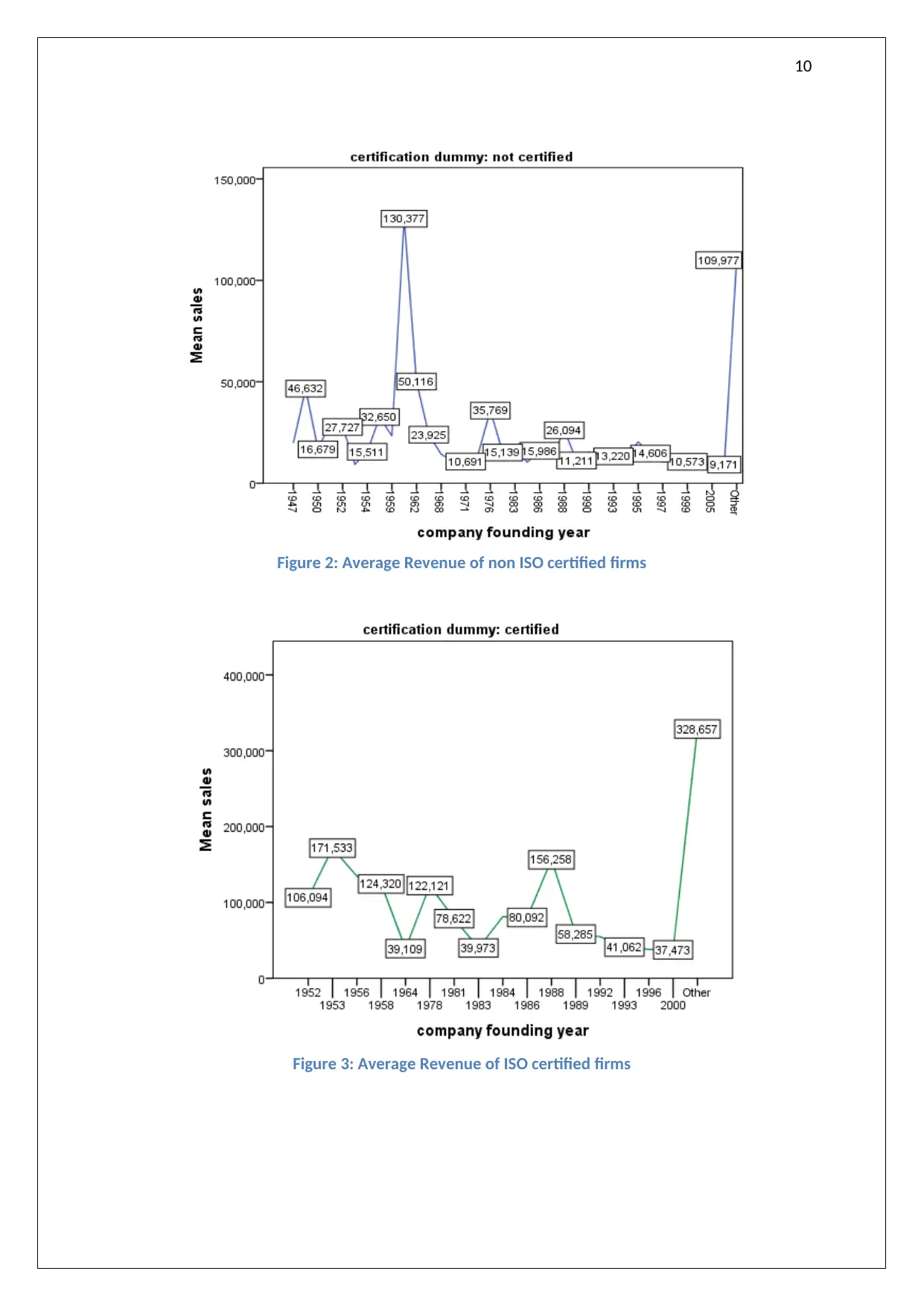

Figure 2: Average Revenue of non ISO certified firms

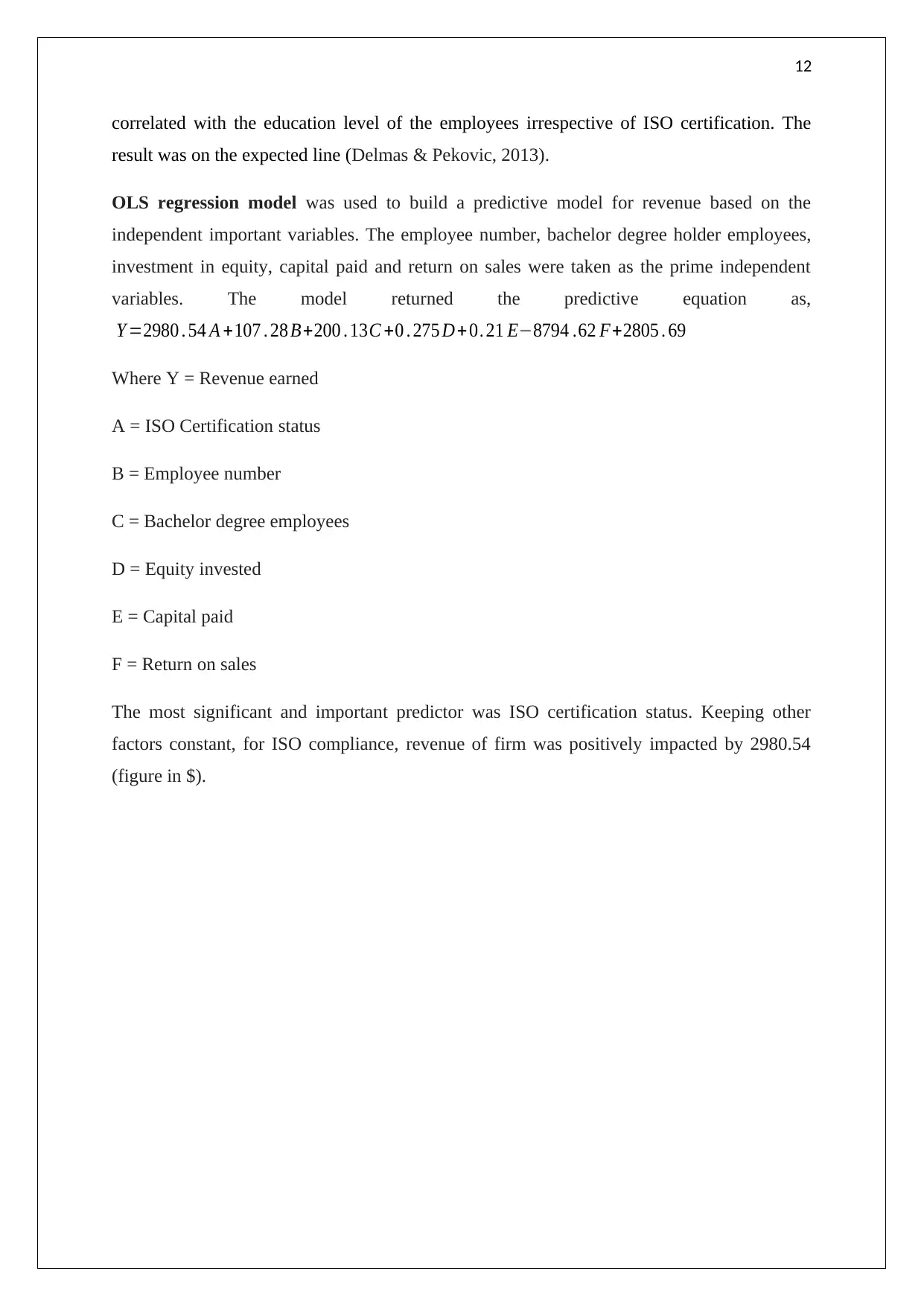

Figure 3: Average Revenue of ISO certified firms

Figure 2: Average Revenue of non ISO certified firms

Figure 3: Average Revenue of ISO certified firms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Inferential Analysis

The inferential analysis was done using the SPSS statistical software package. The entire data

set (scale variables) was checked for reliability, the Cronbach’s Alpha (α = 0.74) for chosen

variables described that there was enough significant collection for inferential analysis.

Independent t-test was used as a statistical tool to draw an inferential conclusion on the first

hypothesis. Average sales for certified ($ 29591.67) and non-ISO complaint ($10132.88)

companies were compared, and statistically significant difference (t (5715) = -12.33, p <

0.05) was discovered in sales between ISO certified and non-certified companies.

Average profit for certified ($ 4384.67) and non-ISO complaint ($ 1865.26) companies were

compared, and statistically significant difference (t (5715) = -7.44, p < 0.05) was discovered

in sales between ISO certified and non-certified companies.

For the second hypothesis, ANOVA was used as a tool for analysis. Levene's homogeneity (L

= 36.38, p < 0.05) test assured the validity of analysis of variance. The investigation was

done in two phases; for no FDI status, a statistically significant difference in return on asset

(F = 35.64, p < 0.05) was observed. Similar result was observed for return on sales (F =

47.59, p < 0.05). The comparison was done between ISO certified and a non-certified group

of companies. The null hypothesis was rejected based on the results. For companies with FDI

inputs the results were different, there was no significant difference in return on assets (F =

1.73, p = 0.19) and return on sales (F = 0.7, p = 0.8) between ISO 9000 certified and non

certified firms.

The third hypothetical assumption was crosschecked based on ISO 9000 enrolment status of

the Chinese companies using ANOVA. Capital from state (F = 2.03, p = 0.15) and overseas

(F = 1.15, p = 0.28), were found to be non-significantly dissimilar between two groups. Here,

it was observed that ISO certification did not have an effect on capital from state and

overseas.

Additionally, association among the employee education level and decisive factors were

checked. In table 3 and table 4, Pearson’s correlation coefficients were provided. Return on

asset was the only variable which was uncorrelated with diploma and high school level of

education for non-ISO compliant companies. Capital from states was also insignificantly

Inferential Analysis

The inferential analysis was done using the SPSS statistical software package. The entire data

set (scale variables) was checked for reliability, the Cronbach’s Alpha (α = 0.74) for chosen

variables described that there was enough significant collection for inferential analysis.

Independent t-test was used as a statistical tool to draw an inferential conclusion on the first

hypothesis. Average sales for certified ($ 29591.67) and non-ISO complaint ($10132.88)

companies were compared, and statistically significant difference (t (5715) = -12.33, p <

0.05) was discovered in sales between ISO certified and non-certified companies.

Average profit for certified ($ 4384.67) and non-ISO complaint ($ 1865.26) companies were

compared, and statistically significant difference (t (5715) = -7.44, p < 0.05) was discovered

in sales between ISO certified and non-certified companies.

For the second hypothesis, ANOVA was used as a tool for analysis. Levene's homogeneity (L

= 36.38, p < 0.05) test assured the validity of analysis of variance. The investigation was

done in two phases; for no FDI status, a statistically significant difference in return on asset

(F = 35.64, p < 0.05) was observed. Similar result was observed for return on sales (F =

47.59, p < 0.05). The comparison was done between ISO certified and a non-certified group

of companies. The null hypothesis was rejected based on the results. For companies with FDI

inputs the results were different, there was no significant difference in return on assets (F =

1.73, p = 0.19) and return on sales (F = 0.7, p = 0.8) between ISO 9000 certified and non

certified firms.

The third hypothetical assumption was crosschecked based on ISO 9000 enrolment status of

the Chinese companies using ANOVA. Capital from state (F = 2.03, p = 0.15) and overseas

(F = 1.15, p = 0.28), were found to be non-significantly dissimilar between two groups. Here,

it was observed that ISO certification did not have an effect on capital from state and

overseas.

Additionally, association among the employee education level and decisive factors were

checked. In table 3 and table 4, Pearson’s correlation coefficients were provided. Return on

asset was the only variable which was uncorrelated with diploma and high school level of

education for non-ISO compliant companies. Capital from states was also insignificantly

12

correlated with the education level of the employees irrespective of ISO certification. The

result was on the expected line (Delmas & Pekovic, 2013).

OLS regression model was used to build a predictive model for revenue based on the

independent important variables. The employee number, bachelor degree holder employees,

investment in equity, capital paid and return on sales were taken as the prime independent

variables. The model returned the predictive equation as,

Y =2980 . 54 A +107 . 28 B+200 . 13C +0 . 275 D+0. 21 E−8794 .62 F+2805 . 69

Where Y = Revenue earned

A = ISO Certification status

B = Employee number

C = Bachelor degree employees

D = Equity invested

E = Capital paid

F = Return on sales

The most significant and important predictor was ISO certification status. Keeping other

factors constant, for ISO compliance, revenue of firm was positively impacted by 2980.54

(figure in $).

correlated with the education level of the employees irrespective of ISO certification. The

result was on the expected line (Delmas & Pekovic, 2013).

OLS regression model was used to build a predictive model for revenue based on the

independent important variables. The employee number, bachelor degree holder employees,

investment in equity, capital paid and return on sales were taken as the prime independent

variables. The model returned the predictive equation as,

Y =2980 . 54 A +107 . 28 B+200 . 13C +0 . 275 D+0. 21 E−8794 .62 F+2805 . 69

Where Y = Revenue earned

A = ISO Certification status

B = Employee number

C = Bachelor degree employees

D = Equity invested

E = Capital paid

F = Return on sales

The most significant and important predictor was ISO certification status. Keeping other

factors constant, for ISO compliance, revenue of firm was positively impacted by 2980.54

(figure in $).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.