BHP vs. Rio Tinto: A Detailed Comparison of Fair Value Accounting

VerifiedAdded on 2023/06/05

|8

|580

|78

Report

AI Summary

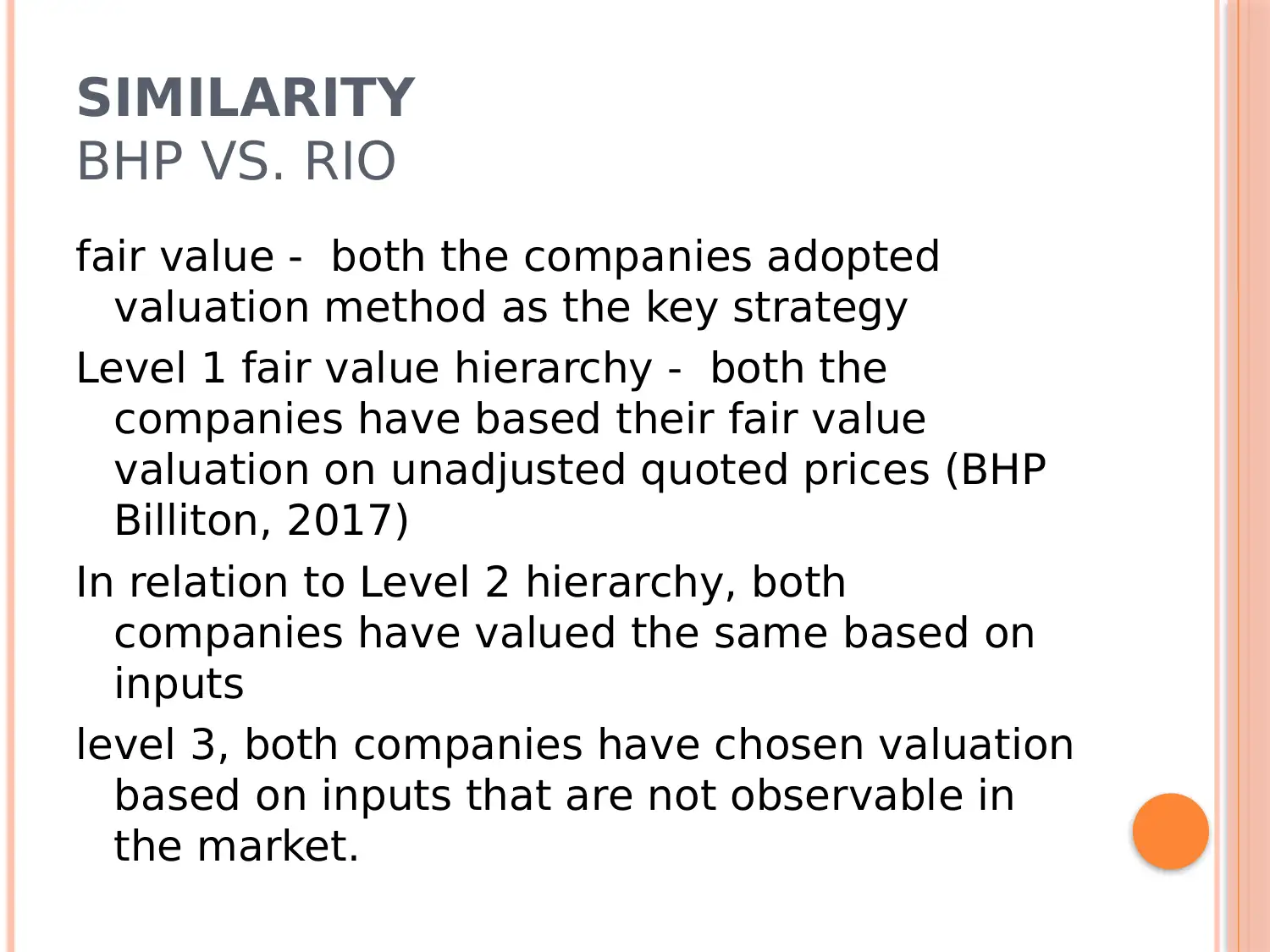

This report provides a comparative analysis of fair value accounting practices adopted by BHP Billiton and Rio Tinto, focusing on their approaches to fair value determination and asset valuation. It highlights the debate surrounding fair value accounting, particularly in relation to market efficiency and the impact of new accounting standards. The report identifies similarities in their valuation methods, such as the use of the fair value hierarchy and depreciation practices, while also contrasting differences in asset grouping and the valuation of financial instruments versus financial assets and liabilities. The analysis references the annual reports of both companies and academic literature to support its findings, offering insights into how these two major corporations apply fair value accounting principles in their financial reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.