Accounting Theory: Fair Value Accounting, US GAAP, and Audit Impact

VerifiedAdded on 2023/03/20

|11

|2390

|70

Essay

AI Summary

This essay delves into the complexities of fair value accounting and its implications under US GAAP, addressing the fundamental problems associated with historical cost measurement. It emphasizes the irrelevance of historical cost in reflecting the current economic reality of companies, where market values often significantly exceed asset values. The essay further discusses the importance of accounts reflecting economic reality, the challenges in achieving this, and methods for measuring economic reality in financial data. It also examines the concept of reliability in accounting, focusing on verifiability, representation faithfulness, and neutrality. Finally, the essay analyzes the impact of fair value accounting on the roles of auditors and the audit function, highlighting the need for enhanced training for accounting students to adapt to the evolving landscape of financial reporting. Desklib provides a platform to access this assignment and many other solved papers for students.

0

ACCOUNTING THEORY

Student’s Name

Accounting Theory

Course Studied

Course Code

City

State

Date

ACCOUNTING THEORY

Student’s Name

Accounting Theory

Course Studied

Course Code

City

State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Accounting Theory

The Fundamental Problem with Financial Statements Based Upon the Historic Cost

Measurement Principle Used Under US GAAP.

It is vital to anticipate the application of the historical cost accounting method for a

proper understanding of the correlated fundamental problem. According to the generally

accepted accounting principle (GAAP) in the US, the accounting books of the company are

documented as per the purchasing price of the assets. In other words, the assets on the balance

sheet of the firm are recorded following their purchasing expenditures. The historical cost

accounting technique is therefore conservative and based on the ancient transactions of the

company. Even though the historical cost accounting method has been said to be easy to

calculate and reliable, its fundamental problem circumnavigates its irrelevance at a later point in

time.

According to the case study, the market value of most companies is five times their asset

value. With this statement, it is clear that the asset value of the company is irrelevant today. The

historical cost of firm resources is irrelevant at a future point in time. For instance, a building

which is procured by a company some decades ago is likely to have a higher market value today

compared to the asset value recorded within the balance sheet of the company. A typical example

to illustrate this concept is the cost of multiple properties in New York one hundred years ago

($50,000) (Nicholas, 2019). Currently, the market value of the properties is $50 million

(Nicholas, 2019). However, when accountants prepare financial statements using the historical

cost accounting technique, the value of the asset ($50,000) is displayed on the balance sheet of

the firm. This aspect provided a misleading outlook of the actual financial level of the business.

Accounting Theory

The Fundamental Problem with Financial Statements Based Upon the Historic Cost

Measurement Principle Used Under US GAAP.

It is vital to anticipate the application of the historical cost accounting method for a

proper understanding of the correlated fundamental problem. According to the generally

accepted accounting principle (GAAP) in the US, the accounting books of the company are

documented as per the purchasing price of the assets. In other words, the assets on the balance

sheet of the firm are recorded following their purchasing expenditures. The historical cost

accounting technique is therefore conservative and based on the ancient transactions of the

company. Even though the historical cost accounting method has been said to be easy to

calculate and reliable, its fundamental problem circumnavigates its irrelevance at a later point in

time.

According to the case study, the market value of most companies is five times their asset

value. With this statement, it is clear that the asset value of the company is irrelevant today. The

historical cost of firm resources is irrelevant at a future point in time. For instance, a building

which is procured by a company some decades ago is likely to have a higher market value today

compared to the asset value recorded within the balance sheet of the company. A typical example

to illustrate this concept is the cost of multiple properties in New York one hundred years ago

($50,000) (Nicholas, 2019). Currently, the market value of the properties is $50 million

(Nicholas, 2019). However, when accountants prepare financial statements using the historical

cost accounting technique, the value of the asset ($50,000) is displayed on the balance sheet of

the firm. This aspect provided a misleading outlook of the actual financial level of the business.

2

The enormous dissimilarity between the firm’s market value and the asset value may mislead

decision making in the company.

Personalities Regarding the Principle of Measurement in Accounting (Accounts

Must Reflect Economic Reality)

In order to promote investors’ satisfaction in the economist, it is fundamental to initiate a

principle-based program that promotes faithful representation of the effects of the transactions,

the economic faithfulness of the balances intended to be displayed and the finances of the entire

enterprise. Therefore, the phrase “accounts must reflect economic reality” encompasses four

significant components which are assumed to have a common meaning. These components

include, faithful representation, reflection of the economic substance, provision of fair and true

representation and present fairly.

However, arriving at accounts that represent economic reality is one of the most

challenging aspects. Several people argue that the economics of transactions are always in the

eyes of the beholder (Schneider, 2015). Nevertheless, this ideology should not oblige as an

justification against the efforts in preparing reports that provide a reasonable representation of

economic reality.

Accounts which reflect economic reality are likely to bring about volatility in earnings

(van, et, al., 2016). However, the fact remains that economic volatility represents of real market.

Therefore, accounts should aim at ensuring investors are better served by accessing data about

real volatility rather than using arcane rules that obscure this volatility. The volatility that will

appear in the financial documents of the companies will have a worrying consequence on the

market. Handling such a crisis will require investors to be taught about this volatility. On the

The enormous dissimilarity between the firm’s market value and the asset value may mislead

decision making in the company.

Personalities Regarding the Principle of Measurement in Accounting (Accounts

Must Reflect Economic Reality)

In order to promote investors’ satisfaction in the economist, it is fundamental to initiate a

principle-based program that promotes faithful representation of the effects of the transactions,

the economic faithfulness of the balances intended to be displayed and the finances of the entire

enterprise. Therefore, the phrase “accounts must reflect economic reality” encompasses four

significant components which are assumed to have a common meaning. These components

include, faithful representation, reflection of the economic substance, provision of fair and true

representation and present fairly.

However, arriving at accounts that represent economic reality is one of the most

challenging aspects. Several people argue that the economics of transactions are always in the

eyes of the beholder (Schneider, 2015). Nevertheless, this ideology should not oblige as an

justification against the efforts in preparing reports that provide a reasonable representation of

economic reality.

Accounts which reflect economic reality are likely to bring about volatility in earnings

(van, et, al., 2016). However, the fact remains that economic volatility represents of real market.

Therefore, accounts should aim at ensuring investors are better served by accessing data about

real volatility rather than using arcane rules that obscure this volatility. The volatility that will

appear in the financial documents of the companies will have a worrying consequence on the

market. Handling such a crisis will require investors to be taught about this volatility. On the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

long term, markets are likely to adopt new well-explained volatility, which actually exists unlike

the artificial accounting volatility, which fails to report economic reality. As investors

acknowledge volatility as natural, a shift will be realized in companies to concentrate on the

fundamentals of the business rather than focusing on short-term earning measures. Therefore,

accounts which represent economic reality aim at eliminating the artificial sense of the true

picture of the monetary level of a company.

Measurement of Economic Reality

Since economic reality is a representation of the accuracy in the recording of financial

data at the time of operations, then the measure of economic reality is equivalent to the measure

of the accuracy in the recording of such financial data. Therefore, the approach used in

measuring accuracy can be utilized measuring the degree of economic reality in accounting. In

measuring economic reality, it is fundamental to research the actual values and the documented

values as per the books of account of the firm. After having the documented values in the

financial statements and the actual values, the difference is calculated by subtracting the

documented values from the actual value. In order to get the percentage error in the

representation of the data, the difference is divided by the actual value and multiplied by a

hundred. For instance, suppose a business bought a sum of goods for $50,000 and instead

recorded $45,000 as the buying price. Economic reality will be measured by calculating the

percentage error in representation as followed

Percentage error

Difference in representation = Actual value – Documented value

= $50,000-45,000

long term, markets are likely to adopt new well-explained volatility, which actually exists unlike

the artificial accounting volatility, which fails to report economic reality. As investors

acknowledge volatility as natural, a shift will be realized in companies to concentrate on the

fundamentals of the business rather than focusing on short-term earning measures. Therefore,

accounts which represent economic reality aim at eliminating the artificial sense of the true

picture of the monetary level of a company.

Measurement of Economic Reality

Since economic reality is a representation of the accuracy in the recording of financial

data at the time of operations, then the measure of economic reality is equivalent to the measure

of the accuracy in the recording of such financial data. Therefore, the approach used in

measuring accuracy can be utilized measuring the degree of economic reality in accounting. In

measuring economic reality, it is fundamental to research the actual values and the documented

values as per the books of account of the firm. After having the documented values in the

financial statements and the actual values, the difference is calculated by subtracting the

documented values from the actual value. In order to get the percentage error in the

representation of the data, the difference is divided by the actual value and multiplied by a

hundred. For instance, suppose a business bought a sum of goods for $50,000 and instead

recorded $45,000 as the buying price. Economic reality will be measured by calculating the

percentage error in representation as followed

Percentage error

Difference in representation = Actual value – Documented value

= $50,000-45,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

= $5,000

% error shall be given by:

The difference in representation divided by Actual value and multiplied by 100%

=

Retrieved from: (Blackwell, Honaker, and King, 2017)

= (5000/50000) *100%

% error =10%

However, the percentage error does not represent the actual degree of economic reality.

Instead, the percentage is inversely proportional to economic reality. In other words, the larger

the percentage error, the smaller the representation of economic reality within the financial

information. On the other hand, the smaller the percentage error, the higher the representation of

economic reality in the financial data presented.

Following the fact that financial data is presented using different sets of data, economic

reality can also be measured by combining such data and calculating the level of precision of the

data. The precision of a group of dimensions can be obtained by calculating the standard

deviation of such a group of measurements where n-1 is the degree of freedom.

Retrieved from: (Jurado, Ludvigson, and Ng, 2015)

= $5,000

% error shall be given by:

The difference in representation divided by Actual value and multiplied by 100%

=

Retrieved from: (Blackwell, Honaker, and King, 2017)

= (5000/50000) *100%

% error =10%

However, the percentage error does not represent the actual degree of economic reality.

Instead, the percentage is inversely proportional to economic reality. In other words, the larger

the percentage error, the smaller the representation of economic reality within the financial

information. On the other hand, the smaller the percentage error, the higher the representation of

economic reality in the financial data presented.

Following the fact that financial data is presented using different sets of data, economic

reality can also be measured by combining such data and calculating the level of precision of the

data. The precision of a group of dimensions can be obtained by calculating the standard

deviation of such a group of measurements where n-1 is the degree of freedom.

Retrieved from: (Jurado, Ludvigson, and Ng, 2015)

5

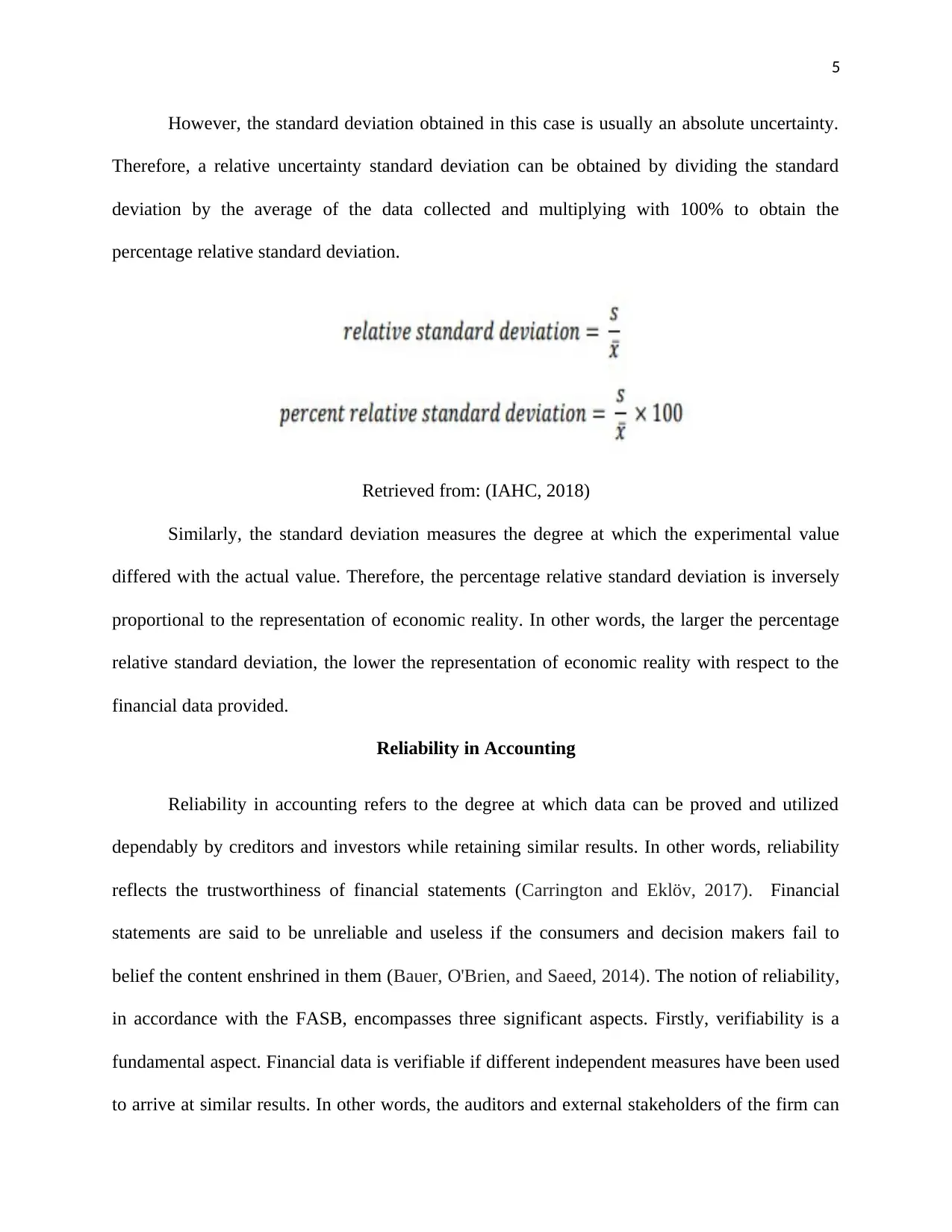

However, the standard deviation obtained in this case is usually an absolute uncertainty.

Therefore, a relative uncertainty standard deviation can be obtained by dividing the standard

deviation by the average of the data collected and multiplying with 100% to obtain the

percentage relative standard deviation.

Retrieved from: (IAHC, 2018)

Similarly, the standard deviation measures the degree at which the experimental value

differed with the actual value. Therefore, the percentage relative standard deviation is inversely

proportional to the representation of economic reality. In other words, the larger the percentage

relative standard deviation, the lower the representation of economic reality with respect to the

financial data provided.

Reliability in Accounting

Reliability in accounting refers to the degree at which data can be proved and utilized

dependably by creditors and investors while retaining similar results. In other words, reliability

reflects the trustworthiness of financial statements (Carrington and Eklöv, 2017). Financial

statements are said to be unreliable and useless if the consumers and decision makers fail to

belief the content enshrined in them (Bauer, O'Brien, and Saeed, 2014). The notion of reliability,

in accordance with the FASB, encompasses three significant aspects. Firstly, verifiability is a

fundamental aspect. Financial data is verifiable if different independent measures have been used

to arrive at similar results. In other words, the auditors and external stakeholders of the firm can

However, the standard deviation obtained in this case is usually an absolute uncertainty.

Therefore, a relative uncertainty standard deviation can be obtained by dividing the standard

deviation by the average of the data collected and multiplying with 100% to obtain the

percentage relative standard deviation.

Retrieved from: (IAHC, 2018)

Similarly, the standard deviation measures the degree at which the experimental value

differed with the actual value. Therefore, the percentage relative standard deviation is inversely

proportional to the representation of economic reality. In other words, the larger the percentage

relative standard deviation, the lower the representation of economic reality with respect to the

financial data provided.

Reliability in Accounting

Reliability in accounting refers to the degree at which data can be proved and utilized

dependably by creditors and investors while retaining similar results. In other words, reliability

reflects the trustworthiness of financial statements (Carrington and Eklöv, 2017). Financial

statements are said to be unreliable and useless if the consumers and decision makers fail to

belief the content enshrined in them (Bauer, O'Brien, and Saeed, 2014). The notion of reliability,

in accordance with the FASB, encompasses three significant aspects. Firstly, verifiability is a

fundamental aspect. Financial data is verifiable if different independent measures have been used

to arrive at similar results. In other words, the auditors and external stakeholders of the firm can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

quantify and evaluate the financial statements of the company and present similar outcomes.

Auditors cannot offer an unqualified opinion if they can’t verify the financial data.

Secondly, representation faithfulness is essential (Kythreotis, 2014). Representation

faithfulness simply refers to the aspect whereby the financial statements represent the reality of

all transactions that occurred during the year. For instance, a company that reflects "$100,000" as

the cost of goods when the real cost was $159,000 does not reflect the reality. Therefore, such

financial information is said to be unreliable.

Finally, neutrality serves a significant role while anticipating the aspect of reliability.

Most financial statements of the company are usually biased as the managers strive to see the

company improving. Therefore, most of the companies tend to record increased performance

while neglecting unfavourable events. The aspect of neutrality requires the accountants and

financial managers to prepare financial statements that are completely unbiased. For example, a

firm with data regarding a probable lawsuit should report such information under the notes of the

financial statement. Withholding such data renders the financial statements unreliable to external

creditors and investors.

Impact of Using Fair Values on the Roles of Auditors and the Audit Function

The current focus on execution of fair value accounting will enormous complications

among the auditors. Firstly, if the fair value accounting is elected and/or the fair value

framework disseminated by the FASB is not appropriately interpreted, there will be an

impairment on the internal and external auditors’ ability to evaluate the cogency of the

management’s proclaimed estimations thus raising the audit risk (Glover, Taylor and Wu, 2016).

Additionally, the current fair value accounting will create complexities for the auditors with

quantify and evaluate the financial statements of the company and present similar outcomes.

Auditors cannot offer an unqualified opinion if they can’t verify the financial data.

Secondly, representation faithfulness is essential (Kythreotis, 2014). Representation

faithfulness simply refers to the aspect whereby the financial statements represent the reality of

all transactions that occurred during the year. For instance, a company that reflects "$100,000" as

the cost of goods when the real cost was $159,000 does not reflect the reality. Therefore, such

financial information is said to be unreliable.

Finally, neutrality serves a significant role while anticipating the aspect of reliability.

Most financial statements of the company are usually biased as the managers strive to see the

company improving. Therefore, most of the companies tend to record increased performance

while neglecting unfavourable events. The aspect of neutrality requires the accountants and

financial managers to prepare financial statements that are completely unbiased. For example, a

firm with data regarding a probable lawsuit should report such information under the notes of the

financial statement. Withholding such data renders the financial statements unreliable to external

creditors and investors.

Impact of Using Fair Values on the Roles of Auditors and the Audit Function

The current focus on execution of fair value accounting will enormous complications

among the auditors. Firstly, if the fair value accounting is elected and/or the fair value

framework disseminated by the FASB is not appropriately interpreted, there will be an

impairment on the internal and external auditors’ ability to evaluate the cogency of the

management’s proclaimed estimations thus raising the audit risk (Glover, Taylor and Wu, 2016).

Additionally, the current fair value accounting will create complexities for the auditors with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

respect to ascertaining that the proclaimed prices reflect economic reality, especially for financial

liabilities and assets that lack an active market.

Fair value accounting strategy will affect the training of accounting students (Brusca,

Caperchione, Cohen and Rossi, 2015). It is fundamental to realize the difference between the

historical cost accounting and the current fair value accounting in order to realize the changes

imposed on the education program. Unlike in the ancient program where assets were recorded at

their purchase price, the current strategy promotes recording assets at their market value and

taking note of the differences in the financial statements ones the recording has been made

(Chea, 2011). It is therefore to vital to train the students to be conversant with the market trends

of each and every item in the company. The students have to be empowered on research

strategies that will enable them to be updated with the market value of the company assets.

Additionally, the normal structure of the balance sheet and income statement has to change in

order to provide more columns for documenting the value changes over a given period.

Therefore, it is clear that fair value accounting shall have a significant impact on the training of

accounting students.

respect to ascertaining that the proclaimed prices reflect economic reality, especially for financial

liabilities and assets that lack an active market.

Fair value accounting strategy will affect the training of accounting students (Brusca,

Caperchione, Cohen and Rossi, 2015). It is fundamental to realize the difference between the

historical cost accounting and the current fair value accounting in order to realize the changes

imposed on the education program. Unlike in the ancient program where assets were recorded at

their purchase price, the current strategy promotes recording assets at their market value and

taking note of the differences in the financial statements ones the recording has been made

(Chea, 2011). It is therefore to vital to train the students to be conversant with the market trends

of each and every item in the company. The students have to be empowered on research

strategies that will enable them to be updated with the market value of the company assets.

Additionally, the normal structure of the balance sheet and income statement has to change in

order to provide more columns for documenting the value changes over a given period.

Therefore, it is clear that fair value accounting shall have a significant impact on the training of

accounting students.

8

References

Bauer, A.M., O'Brien, P.C. and Saeed, U., 2014. Reliability makes accounting relevant: a

comment on the IASB Conceptual Framework project. Accounting in Europe, 11(2), pp.211-217.

Blackwell, M., Honaker, J. and King, G., 2017. A unified approach to measurement error and

missing data: overview and applications. Sociological Methods & Research, 46(3), pp.303-341.

Brusca, I., Caperchione, E., Cohen, S. and Rossi, F.M., 2015. Comparing accounting systems in

Europe. In Public Sector Accounting and Auditing in Europe (pp. 235-251). Palgrave Macmillan,

London.

Carrington, T. and Eklöv Alander, G., 2017. Justifications of accounting reliability. In European

Accounting Association Congress, Valencia, Spain, 10-12 May 2017.

Chea, A.C., 2011. Fair value accounting: Its impacts on financial reporting and how it can be

enhanced to provide more clarity and reliability of information for users of financial

statements. International journal of business and social science, 2(20).

References

Bauer, A.M., O'Brien, P.C. and Saeed, U., 2014. Reliability makes accounting relevant: a

comment on the IASB Conceptual Framework project. Accounting in Europe, 11(2), pp.211-217.

Blackwell, M., Honaker, J. and King, G., 2017. A unified approach to measurement error and

missing data: overview and applications. Sociological Methods & Research, 46(3), pp.303-341.

Brusca, I., Caperchione, E., Cohen, S. and Rossi, F.M., 2015. Comparing accounting systems in

Europe. In Public Sector Accounting and Auditing in Europe (pp. 235-251). Palgrave Macmillan,

London.

Carrington, T. and Eklöv Alander, G., 2017. Justifications of accounting reliability. In European

Accounting Association Congress, Valencia, Spain, 10-12 May 2017.

Chea, A.C., 2011. Fair value accounting: Its impacts on financial reporting and how it can be

enhanced to provide more clarity and reliability of information for users of financial

statements. International journal of business and social science, 2(20).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing fair

value measurements and complex estimates: Implications for auditing standards and the

academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

IAHC (2018). Accuracy and Precision [online]. Retrieved from:

https://www.lahc.edu/classes/chemistry/arias/Exp%201%20-%20AccPreF11.pdf (Accessed on

19th May 2019).

Jurado, K., Ludvigson, S.C. and Ng, S., 2015. Measuring uncertainty. American Economic

Review, 105(3), pp.1177-1216.

Kythreotis, A., 2014. Measurement of financial reporting quality based on IFRS conceptual

framework’s fundamental qualitative characteristics. European Journal of Accounting, Finance

& Business, 2(3), pp.4-29.

Nicholas, S., (2019). How the market-to-market accounting and historical cost accounting differ

[online]. Retrieved from: https://www.investopedia.com/ask/answers/042315/how-market-

market-accounting-different-historical-cost-accounting.asp (Accessed on 19th May 2019).

Schneider, A., 2015. Reflexivity in sustainability accounting and management: Transcending the

economic focus of corporate sustainability. Journal of Business Ethics, 127(3), pp.525-536.

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing fair

value measurements and complex estimates: Implications for auditing standards and the

academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

IAHC (2018). Accuracy and Precision [online]. Retrieved from:

https://www.lahc.edu/classes/chemistry/arias/Exp%201%20-%20AccPreF11.pdf (Accessed on

19th May 2019).

Jurado, K., Ludvigson, S.C. and Ng, S., 2015. Measuring uncertainty. American Economic

Review, 105(3), pp.1177-1216.

Kythreotis, A., 2014. Measurement of financial reporting quality based on IFRS conceptual

framework’s fundamental qualitative characteristics. European Journal of Accounting, Finance

& Business, 2(3), pp.4-29.

Nicholas, S., (2019). How the market-to-market accounting and historical cost accounting differ

[online]. Retrieved from: https://www.investopedia.com/ask/answers/042315/how-market-

market-accounting-different-historical-cost-accounting.asp (Accessed on 19th May 2019).

Schneider, A., 2015. Reflexivity in sustainability accounting and management: Transcending the

economic focus of corporate sustainability. Journal of Business Ethics, 127(3), pp.525-536.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Van Mosseveld, C., Hernández-Peña, P., Arán, D., Cherilova, V. and Mataria, A., 2016. How to

ensure the quality of health accounts. Health Policy, 120(5), pp.544-551.

Van Mosseveld, C., Hernández-Peña, P., Arán, D., Cherilova, V. and Mataria, A., 2016. How to

ensure the quality of health accounts. Health Policy, 120(5), pp.544-551.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.