Analyzing Accounting Standards: Fair Value, Impairment, and IFRS 13

VerifiedAdded on 2020/10/05

|8

|2257

|152

Report

AI Summary

This report provides a comprehensive overview of accounting standards, with a specific focus on fair value measurement as per IFRS 13 and impairment loss. The report begins with an introduction to accounting standards and their importance in financial reporting, followed by a detailed explanation of fair value measurement, including its objectives, definitions, and valuation techniques such as the cost approach, market approach, and income approach. The report also explores the concept of impairment loss, explaining its definition, calculation process, and journal entries. A case study involving Gali Ltd. demonstrates the application of impairment loss accounting. The conclusion summarizes the key findings and emphasizes the practical application of these accounting standards in financial decision-making. The report includes references to relevant literature and online resources.

Use of Accounting

Standards

Standards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Accounting standard on fair value measurement........................................................................1

PART B............................................................................................................................................4

Impairment loss...........................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Accounting standard on fair value measurement........................................................................1

PART B............................................................................................................................................4

Impairment loss...........................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

INTRODUCTION

Accounting standards suggests the core methods and techniques that are useful for

solving any accounting problem. All organisations should use accounting standards to maintain

their records and keep it appropriately so that their financial statements show the accurate image

of company (Barker and Schulte, 2017). This report covers the fair value management

accounting standards that are produced by International Financial Reporting Standards.

Furthermore, it includes the impairment loss with solving critical financial issue.

PART A

Accounting standard on fair value measurement

Accounting standards refer to the written documents that are issued by several accounting

bodies which are expert in accounts and provide the best treatment, presentation and proper

disclosure of all types of transactions. It includes all kinds of rules and regulations that are used

to maintain control or govern an organisational accounting process (Cenciarelli, De Santis and

Greco, 2018). These are the general set for determining core principles and procedures that are

used in making financial statements. According to fair value management, such accounting

standards are the basic guidelines that direct or supervise main accounting practices. In this

context, IFRS 13 demonstrates fair values that are set out for a framework and measure its fair

value as well as needs disclosure about this management. An organisation must measure all its

assets and liabilities with its location, condition and restriction for sale. Such standards must

provide the best hierarchy of methods that arrive at core fair value of all things (IFRS 13 Fair

Value Measurement, 2013). Fair value measurement is an alternative technique that measures the

value of all types of assets and liabilities.

There are Generally Accepted Accounting Principles that are used at high level among all

private as well as public organisations to accomplish their objectives. IFRS 13 never specify the

unit of an account that should be used for measuring the core value. It means that it is left to the

individual standard to demonstrate account for fair value measurement (DeFond and et.al.,

2018). This standard refers to the fair value that is based on exit price notion and it uses main

hierarchy for such value results of which are based on market. It developed in September 2005

by IFRS and issued in May 2011. It has also several amendments that are derived by Annual

Improvements to IFRSs Cycle in December 2013.

1

Accounting standards suggests the core methods and techniques that are useful for

solving any accounting problem. All organisations should use accounting standards to maintain

their records and keep it appropriately so that their financial statements show the accurate image

of company (Barker and Schulte, 2017). This report covers the fair value management

accounting standards that are produced by International Financial Reporting Standards.

Furthermore, it includes the impairment loss with solving critical financial issue.

PART A

Accounting standard on fair value measurement

Accounting standards refer to the written documents that are issued by several accounting

bodies which are expert in accounts and provide the best treatment, presentation and proper

disclosure of all types of transactions. It includes all kinds of rules and regulations that are used

to maintain control or govern an organisational accounting process (Cenciarelli, De Santis and

Greco, 2018). These are the general set for determining core principles and procedures that are

used in making financial statements. According to fair value management, such accounting

standards are the basic guidelines that direct or supervise main accounting practices. In this

context, IFRS 13 demonstrates fair values that are set out for a framework and measure its fair

value as well as needs disclosure about this management. An organisation must measure all its

assets and liabilities with its location, condition and restriction for sale. Such standards must

provide the best hierarchy of methods that arrive at core fair value of all things (IFRS 13 Fair

Value Measurement, 2013). Fair value measurement is an alternative technique that measures the

value of all types of assets and liabilities.

There are Generally Accepted Accounting Principles that are used at high level among all

private as well as public organisations to accomplish their objectives. IFRS 13 never specify the

unit of an account that should be used for measuring the core value. It means that it is left to the

individual standard to demonstrate account for fair value measurement (DeFond and et.al.,

2018). This standard refers to the fair value that is based on exit price notion and it uses main

hierarchy for such value results of which are based on market. It developed in September 2005

by IFRS and issued in May 2011. It has also several amendments that are derived by Annual

Improvements to IFRSs Cycle in December 2013.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Objective of Fair Value Measurement – This accounting standard is based on the actual or fair

value of an asset or liabilities that are used in every business to achieve growth and development

(Dvořák, 2017). So, for this reason, there are some important objectives of this standard that are

described as below:

It demonstrates the fair value.

It describes the disclosure about fair value measurements.

Its main objective is set out in a single IFRS; a framework for measuring fair value.

In this context, there are some definitions that are useful for describing its core value and

help in all types of businesses. These are as follows:

Active Market – It is a special market that manages all types of transactions for the liabilities

and assets that take place with full frequency. It is also provided with volume for pricing

information on an ongoing basis.

Fair Value – It refers to a particular price that would be received to sell an equipment or it is a

price for payment to reduce the liability in specific order (Farrugia, 2014). This value is a

transaction that commences in between several market participants on the date.

Best and Highest Use – It means that the use of a non-financial asset by different marketers

would increase value of a particular asset or specific group of liabilities and assets within it can

be used.

Exit Price – It is known as the special price that would be paid to transfer a liability and receive

to sell an asset.

Main Advantageous Market – It describes a market segment that maximises the amount that is

received through selling particular equipment and also shows minimised amount to be paid to

transfer the liability (Filip and et.al., 2017). All these are taken into consideration after all

transactional and transport expenses.

Principle Market – It holds complete level of activities and greatest volume for all liabilities

and assets and so, known as the principle market.

Guidance on measurement – According to the International Financial Reporting Standards,

core guidelines are issued for more understanding about Fair Value Measurement. These are

given as below:

It operates on a theory that is assumed on an orderly transaction in between different

participants in the target market (MARTÍN and Osma, 2018). It is commenced on a special date

2

value of an asset or liabilities that are used in every business to achieve growth and development

(Dvořák, 2017). So, for this reason, there are some important objectives of this standard that are

described as below:

It demonstrates the fair value.

It describes the disclosure about fair value measurements.

Its main objective is set out in a single IFRS; a framework for measuring fair value.

In this context, there are some definitions that are useful for describing its core value and

help in all types of businesses. These are as follows:

Active Market – It is a special market that manages all types of transactions for the liabilities

and assets that take place with full frequency. It is also provided with volume for pricing

information on an ongoing basis.

Fair Value – It refers to a particular price that would be received to sell an equipment or it is a

price for payment to reduce the liability in specific order (Farrugia, 2014). This value is a

transaction that commences in between several market participants on the date.

Best and Highest Use – It means that the use of a non-financial asset by different marketers

would increase value of a particular asset or specific group of liabilities and assets within it can

be used.

Exit Price – It is known as the special price that would be paid to transfer a liability and receive

to sell an asset.

Main Advantageous Market – It describes a market segment that maximises the amount that is

received through selling particular equipment and also shows minimised amount to be paid to

transfer the liability (Filip and et.al., 2017). All these are taken into consideration after all

transactional and transport expenses.

Principle Market – It holds complete level of activities and greatest volume for all liabilities

and assets and so, known as the principle market.

Guidance on measurement – According to the International Financial Reporting Standards,

core guidelines are issued for more understanding about Fair Value Measurement. These are

given as below:

It operates on a theory that is assumed on an orderly transaction in between different

participants in the target market (MARTÍN and Osma, 2018). It is commenced on a special date

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

under different market conditions. If a company holds non-financial asset then this accounting

standard describes the best and highest use for it. An organisation takes into account the special

characteristics of liability or asset that are being measured by market participants. There is an

optional exception applied for several financial liabilities as well as assets that are providing the

positions according to market condition, risk and penetration.

Valuation techniques – For measuring the fair value by an organisation, there may be use of

appropriate valuation techniques in several circumstances. There is sufficient data and

information available to measure fair value. It also increases the use of observable inputs and

reduce use of unobservable inputs (Ogundana and et.al., 2018). Main objective to use these

valuation techniques is to estimate price at which a transaction is made to sell a special type of

asset and transfer the liability. In this context, there are majorly three widely used methods for

fair valuation which are as follows:

Cost Approach – It is a specific method that arrives to appraisal value of an asset in

which accrued depreciation is less from the asset's replacement cost at actual price.

Market Approach – It refers to the valuation method that is utilised in demonstrating the

appraisal value of an organisation and intangible asset. Market approach is used for the

estimation of core value of company.

Income Approach – In this method, the accountant should convert future amounts such

as income and expenses as well as cash flows to a single amount (Sellhorn and Stier,

2017). It also reflects the current market expectations about those of future amount.

These accounting standards come at IFRS 13 and it is applicable for annual reporting

periods that starts from 1st January 2013. So, for this reason, all companies should apply it from

this time and may use for an earlier accounting period.

PART B

Impairment loss

Impairment loss refers to net carrying value of reduction in an asset or equipment that

exceeds the future undisclosed cash flow. Net carrying value is the cost value of an asset minus

its depreciation. In this context, impairment occurs when an organisation abandon or sell its

assets because it may no longer be beneficial for company (Sundgren, Mäki and Somoza-López,

2018). Such asset is also recognised as a loss for the organisation and accountant should show it

3

standard describes the best and highest use for it. An organisation takes into account the special

characteristics of liability or asset that are being measured by market participants. There is an

optional exception applied for several financial liabilities as well as assets that are providing the

positions according to market condition, risk and penetration.

Valuation techniques – For measuring the fair value by an organisation, there may be use of

appropriate valuation techniques in several circumstances. There is sufficient data and

information available to measure fair value. It also increases the use of observable inputs and

reduce use of unobservable inputs (Ogundana and et.al., 2018). Main objective to use these

valuation techniques is to estimate price at which a transaction is made to sell a special type of

asset and transfer the liability. In this context, there are majorly three widely used methods for

fair valuation which are as follows:

Cost Approach – It is a specific method that arrives to appraisal value of an asset in

which accrued depreciation is less from the asset's replacement cost at actual price.

Market Approach – It refers to the valuation method that is utilised in demonstrating the

appraisal value of an organisation and intangible asset. Market approach is used for the

estimation of core value of company.

Income Approach – In this method, the accountant should convert future amounts such

as income and expenses as well as cash flows to a single amount (Sellhorn and Stier,

2017). It also reflects the current market expectations about those of future amount.

These accounting standards come at IFRS 13 and it is applicable for annual reporting

periods that starts from 1st January 2013. So, for this reason, all companies should apply it from

this time and may use for an earlier accounting period.

PART B

Impairment loss

Impairment loss refers to net carrying value of reduction in an asset or equipment that

exceeds the future undisclosed cash flow. Net carrying value is the cost value of an asset minus

its depreciation. In this context, impairment occurs when an organisation abandon or sell its

assets because it may no longer be beneficial for company (Sundgren, Mäki and Somoza-López,

2018). Such asset is also recognised as a loss for the organisation and accountant should show it

3

in income and expense statements. For calculating the impairment loss, every company should

follow a special process that is as follows:

Firstly, accountant must identify the factors in which this particular asset is impairment.

For this purpose, it contains new legislation, overall turnover, different market conditions

and many more. It will also depend on the organisational structure.

Second step is identification of fair market value of the asset and making comparison

with other organisation with carrying core value of the asset if it is sold in the target

market.

Third step is to make comparison of fair market value of an asset with its carrying value

that is showing in the organisational financial statements.

By accomplishing this process, accountant must find out its impairment loss value if the

holding cost of all asset exceeds its fair market value and that particular asset is called as

impaired (Barker and Schulte, 2017).

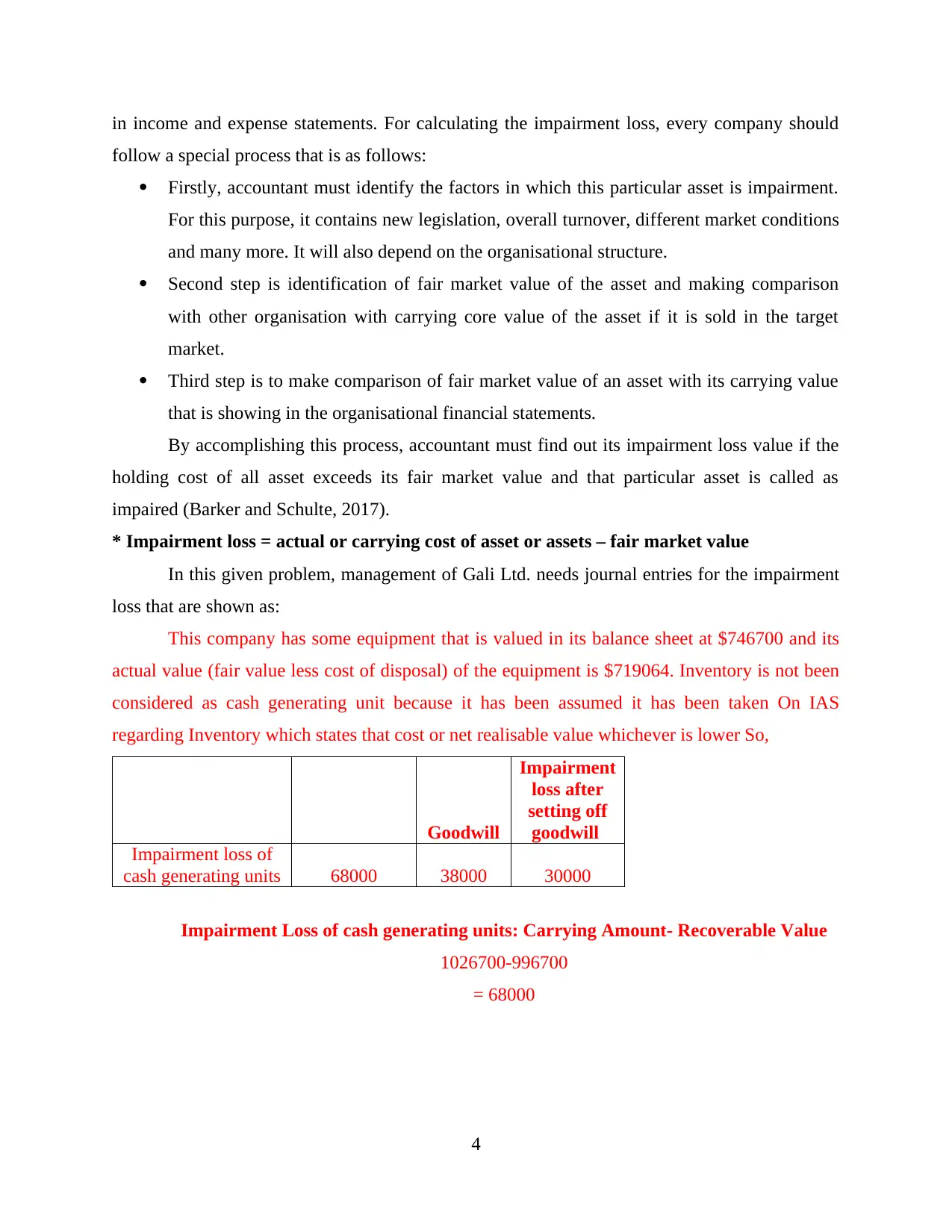

* Impairment loss = actual or carrying cost of asset or assets – fair market value

In this given problem, management of Gali Ltd. needs journal entries for the impairment

loss that are shown as:

This company has some equipment that is valued in its balance sheet at $746700 and its

actual value (fair value less cost of disposal) of the equipment is $719064. Inventory is not been

considered as cash generating unit because it has been assumed it has been taken On IAS

regarding Inventory which states that cost or net realisable value whichever is lower So,

Goodwill

Impairment

loss after

setting off

goodwill

Impairment loss of

cash generating units 68000 38000 30000

Impairment Loss of cash generating units: Carrying Amount- Recoverable Value

1026700-996700

= 68000

4

follow a special process that is as follows:

Firstly, accountant must identify the factors in which this particular asset is impairment.

For this purpose, it contains new legislation, overall turnover, different market conditions

and many more. It will also depend on the organisational structure.

Second step is identification of fair market value of the asset and making comparison

with other organisation with carrying core value of the asset if it is sold in the target

market.

Third step is to make comparison of fair market value of an asset with its carrying value

that is showing in the organisational financial statements.

By accomplishing this process, accountant must find out its impairment loss value if the

holding cost of all asset exceeds its fair market value and that particular asset is called as

impaired (Barker and Schulte, 2017).

* Impairment loss = actual or carrying cost of asset or assets – fair market value

In this given problem, management of Gali Ltd. needs journal entries for the impairment

loss that are shown as:

This company has some equipment that is valued in its balance sheet at $746700 and its

actual value (fair value less cost of disposal) of the equipment is $719064. Inventory is not been

considered as cash generating unit because it has been assumed it has been taken On IAS

regarding Inventory which states that cost or net realisable value whichever is lower So,

Goodwill

Impairment

loss after

setting off

goodwill

Impairment loss of

cash generating units 68000 38000 30000

Impairment Loss of cash generating units: Carrying Amount- Recoverable Value

1026700-996700

= 68000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

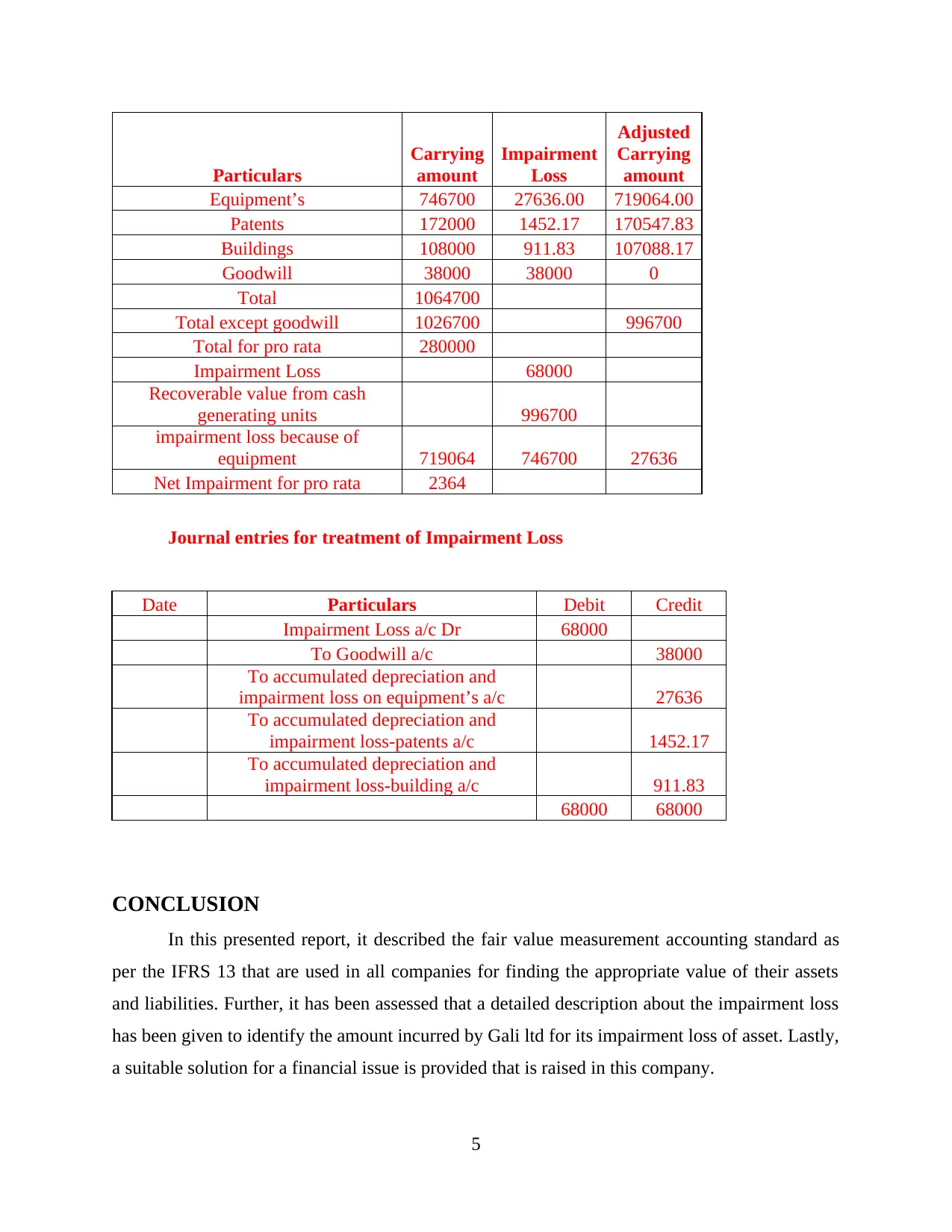

Particulars

Carrying

amount

Impairment

Loss

Adjusted

Carrying

amount

Equipment’s 746700 27636.00 719064.00

Patents 172000 1452.17 170547.83

Buildings 108000 911.83 107088.17

Goodwill 38000 38000 0

Total 1064700

Total except goodwill 1026700 996700

Total for pro rata 280000

Impairment Loss 68000

Recoverable value from cash

generating units 996700

impairment loss because of

equipment 719064 746700 27636

Net Impairment for pro rata 2364

Journal entries for treatment of Impairment Loss

Date Particulars Debit Credit

Impairment Loss a/c Dr 68000

To Goodwill a/c 38000

To accumulated depreciation and

impairment loss on equipment’s a/c 27636

To accumulated depreciation and

impairment loss-patents a/c 1452.17

To accumulated depreciation and

impairment loss-building a/c 911.83

68000 68000

CONCLUSION

In this presented report, it described the fair value measurement accounting standard as

per the IFRS 13 that are used in all companies for finding the appropriate value of their assets

and liabilities. Further, it has been assessed that a detailed description about the impairment loss

has been given to identify the amount incurred by Gali ltd for its impairment loss of asset. Lastly,

a suitable solution for a financial issue is provided that is raised in this company.

5

Carrying

amount

Impairment

Loss

Adjusted

Carrying

amount

Equipment’s 746700 27636.00 719064.00

Patents 172000 1452.17 170547.83

Buildings 108000 911.83 107088.17

Goodwill 38000 38000 0

Total 1064700

Total except goodwill 1026700 996700

Total for pro rata 280000

Impairment Loss 68000

Recoverable value from cash

generating units 996700

impairment loss because of

equipment 719064 746700 27636

Net Impairment for pro rata 2364

Journal entries for treatment of Impairment Loss

Date Particulars Debit Credit

Impairment Loss a/c Dr 68000

To Goodwill a/c 38000

To accumulated depreciation and

impairment loss on equipment’s a/c 27636

To accumulated depreciation and

impairment loss-patents a/c 1452.17

To accumulated depreciation and

impairment loss-building a/c 911.83

68000 68000

CONCLUSION

In this presented report, it described the fair value measurement accounting standard as

per the IFRS 13 that are used in all companies for finding the appropriate value of their assets

and liabilities. Further, it has been assessed that a detailed description about the impairment loss

has been given to identify the amount incurred by Gali ltd for its impairment loss of asset. Lastly,

a suitable solution for a financial issue is provided that is raised in this company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value measurement

for non-financial assets. Accounting, Organizations and Society, 56, pp.55-67.

Cenciarelli, V.G., De Santis, F. and Greco, G., 2018. External audit and fair value measurements.

DeFond and et.al., 2018. The Usefulness of Fair Value Accounting in Executive Compensation.

Dvořák, J., 2017. How Do Czech Companies Report Fair Value Measurement Under IFRS

13?. European Financial and Accounting Journal, 2017(3), pp.117-128.

Farrugia, C., 2014. An analysis of the impact of IFRS 13 fair value measurement on local listed

entities (Master's thesis, University of Malta).

Filip and et.al., 2017. Literature Review on the Effect of Implementation of IFRS 13 Fair Value

Measurement.

MARTÍN, F.M. and Osma, B.G., 2018. Does IFRS 9 Consider Financial Statement Users’

Preferences with Respect to IFRS 13 Fair Value Hierarchy? A Suggestion to Refine the

Definition of OCI. Estudios de Economía Aplicada, 36(2), pp.515-536.

Ogundana and et.al., 2018. FAIR VALUE MEASUREMENT (IFRS 13) AND INVESTING

DECISION: THE STANDPOINT OF ACCOUNTING ACADEMICS AND AUDITORS

IN LAGOS AND OGUN STATE, NIGERIA. Academy of Accounting and Financial

Studies Journal, 22(1), pp.1-12.

Sellhorn, T. and Stier, C., 2017. Fair value measurement for long-lived operating assets:

Research evidence.

Sundgren, S., Mäki, J. and Somoza-López, A., 2018. Analyst coverage, market liquidity and

disclosure quality: a study of fair-value disclosures by European real estate companies

under IAS 40 and IFRS 13. The International Journal of Accounting, 53(1), pp.54-75.

Online

IFRS 13 Fair Value Measurement. 2013. [Online]. Available through

<https://www.icaew.com/technical/financial-reporting/ifrs/ifrs-standards/ifrs-13-fair-

value-measurement>.

6

Books and Journals

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value measurement

for non-financial assets. Accounting, Organizations and Society, 56, pp.55-67.

Cenciarelli, V.G., De Santis, F. and Greco, G., 2018. External audit and fair value measurements.

DeFond and et.al., 2018. The Usefulness of Fair Value Accounting in Executive Compensation.

Dvořák, J., 2017. How Do Czech Companies Report Fair Value Measurement Under IFRS

13?. European Financial and Accounting Journal, 2017(3), pp.117-128.

Farrugia, C., 2014. An analysis of the impact of IFRS 13 fair value measurement on local listed

entities (Master's thesis, University of Malta).

Filip and et.al., 2017. Literature Review on the Effect of Implementation of IFRS 13 Fair Value

Measurement.

MARTÍN, F.M. and Osma, B.G., 2018. Does IFRS 9 Consider Financial Statement Users’

Preferences with Respect to IFRS 13 Fair Value Hierarchy? A Suggestion to Refine the

Definition of OCI. Estudios de Economía Aplicada, 36(2), pp.515-536.

Ogundana and et.al., 2018. FAIR VALUE MEASUREMENT (IFRS 13) AND INVESTING

DECISION: THE STANDPOINT OF ACCOUNTING ACADEMICS AND AUDITORS

IN LAGOS AND OGUN STATE, NIGERIA. Academy of Accounting and Financial

Studies Journal, 22(1), pp.1-12.

Sellhorn, T. and Stier, C., 2017. Fair value measurement for long-lived operating assets:

Research evidence.

Sundgren, S., Mäki, J. and Somoza-López, A., 2018. Analyst coverage, market liquidity and

disclosure quality: a study of fair-value disclosures by European real estate companies

under IAS 40 and IFRS 13. The International Journal of Accounting, 53(1), pp.54-75.

Online

IFRS 13 Fair Value Measurement. 2013. [Online]. Available through

<https://www.icaew.com/technical/financial-reporting/ifrs/ifrs-standards/ifrs-13-fair-

value-measurement>.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.