Corporate Accounting Assignment (BO1COAC318): Fair Value & Impairment

VerifiedAdded on 2022/11/17

|12

|2858

|74

Report

AI Summary

This report presents a comprehensive analysis of corporate accounting, addressing fair value measurement and impairment calculations. Part A delves into the concept of fair value measurement, discussing its definition, the relevant accounting standard (AASB 13), its necessity, and practical implementation, including aspects like valuation techniques and disclosure requirements. Part B focuses on impairment calculations, specifically for Gali Limited, including journal entries recorded for loss on impairment as of June 30, 2015. The report provides detailed calculations and explanations, offering insights into the application of accounting standards in real-world scenarios. It serves as a valuable resource for students studying corporate accounting, offering a practical understanding of key concepts and their application.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 16 May 2019.

1 | P a g e

By student name

Professor

University

Date: 16 May 2019.

1 | P a g e

2

Executive Summary

A report has been prepared on the topic of corporate accounting. It has 2 sections. In the first section,

the fair value measurement concept has been discussed w.r.t. accounting standard and why the same is

necessary and how it can be implemented. The various aspects of fair value accounting and its uses, the

asset and liabilities on which the same can be implemented have all been discussed in the report. IN the

second section, the calculation of impairment has been done for the company Gali Limited, post which

the journal entry recorded for loss on impairment as on 30th June 2015 has also been shown.

2 | P a g e

Executive Summary

A report has been prepared on the topic of corporate accounting. It has 2 sections. In the first section,

the fair value measurement concept has been discussed w.r.t. accounting standard and why the same is

necessary and how it can be implemented. The various aspects of fair value accounting and its uses, the

asset and liabilities on which the same can be implemented have all been discussed in the report. IN the

second section, the calculation of impairment has been done for the company Gali Limited, post which

the journal entry recorded for loss on impairment as on 30th June 2015 has also been shown.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Table of Contents

Part A: Fair Value Measurement.................................................................................................................4

Introduction.............................................................................................................................................4

Discussion and Analysis...........................................................................................................................4

Disclosure................................................................................................................................................6

Conclusion...............................................................................................................................................7

Part B: Calculation for Impairment..............................................................................................................7

References.................................................................................................................................................10

3 | P a g e

Table of Contents

Part A: Fair Value Measurement.................................................................................................................4

Introduction.............................................................................................................................................4

Discussion and Analysis...........................................................................................................................4

Disclosure................................................................................................................................................6

Conclusion...............................................................................................................................................7

Part B: Calculation for Impairment..............................................................................................................7

References.................................................................................................................................................10

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Part A: Fair Value Measurement

Introduction

Australian Accounting Standards Board has specified one of the accounting standards for fair value

measurement which is AASB 13. It also finds a mention in section 334 of the Corporations Act, 2001.

AASB 13 covers the following areas:

1.) Fair value definition

2.) Single framework for measurement as per fair valuation rules

3.) fair value measurement disclosure

Discussion and Analysis

Definition: As per the definition given in AASB 13, fair value may be defined as the money receivable on

selling asset or amount that would be payable in order to settle or transfer any liability in any

transaction which is taking place in between 2 given participants of market on the given date

(Alexander, 2016).

There exists a Single standard framework for measurement of the fair value but the same is not

specific to any company rather it is based on market. It may be a possibility that the information on the

market values is available in case of few of the assets and liabilities. But for many of such assets or

liabilities, the market information may not be available. The main purpose of measuring fair value in

both the above situation remains the same i.e.identifying the value at which the given asset or the

liability may be sold or settled respectively to the given market participant at the time of measurement

of value (Belton, 2017).

In case the market value of the any given assets or liability is not available or identifiable, than company

measures by the help of technique of valuation, which inceases the use observable inputs, and reduce

using unobservable inputs. Since the values are based out of market, the same is measured based on the

assumptions from the particiapants and that helps in deciding the price of asset or liability. So

company’s intention for transferring the liability or retain the asset is irrelevant in this case.

Australian accounting standard 13 is applied when any other standard requires measurement of fair

value or any related disclosure.

On the following transactions,disclosure requirement of AASB13 is not applied:

1.) Transactions which are related to share based as per AASB2

2.) Transactions relating to leasing within scope of AASB 117 (Dichev, 2017)

3.) There might be some measurements which are like fair value but in actual they are not like

NRV in AASB 102 or value in use.

4.) Transaction relating to plan assets which are based on fair value as per AASB119

5.) Where recoverable amount = fair value – disposal cost as per AASB136

4 | P a g e

Part A: Fair Value Measurement

Introduction

Australian Accounting Standards Board has specified one of the accounting standards for fair value

measurement which is AASB 13. It also finds a mention in section 334 of the Corporations Act, 2001.

AASB 13 covers the following areas:

1.) Fair value definition

2.) Single framework for measurement as per fair valuation rules

3.) fair value measurement disclosure

Discussion and Analysis

Definition: As per the definition given in AASB 13, fair value may be defined as the money receivable on

selling asset or amount that would be payable in order to settle or transfer any liability in any

transaction which is taking place in between 2 given participants of market on the given date

(Alexander, 2016).

There exists a Single standard framework for measurement of the fair value but the same is not

specific to any company rather it is based on market. It may be a possibility that the information on the

market values is available in case of few of the assets and liabilities. But for many of such assets or

liabilities, the market information may not be available. The main purpose of measuring fair value in

both the above situation remains the same i.e.identifying the value at which the given asset or the

liability may be sold or settled respectively to the given market participant at the time of measurement

of value (Belton, 2017).

In case the market value of the any given assets or liability is not available or identifiable, than company

measures by the help of technique of valuation, which inceases the use observable inputs, and reduce

using unobservable inputs. Since the values are based out of market, the same is measured based on the

assumptions from the particiapants and that helps in deciding the price of asset or liability. So

company’s intention for transferring the liability or retain the asset is irrelevant in this case.

Australian accounting standard 13 is applied when any other standard requires measurement of fair

value or any related disclosure.

On the following transactions,disclosure requirement of AASB13 is not applied:

1.) Transactions which are related to share based as per AASB2

2.) Transactions relating to leasing within scope of AASB 117 (Dichev, 2017)

3.) There might be some measurements which are like fair value but in actual they are not like

NRV in AASB 102 or value in use.

4.) Transaction relating to plan assets which are based on fair value as per AASB119

5.) Where recoverable amount = fair value – disposal cost as per AASB136

4 | P a g e

5

Description of fair value measurement framework in AASB13

It is used for measurement at initial and subsequent period if it is allowed by standards. Fair value

measurement for assets or liability could be for:

a.) Single liability or asset such as financial instrument

b.) Group of liabilities or assets or group of assets and liabilities like CGU (Trieu, 2017).

Single asset or liability, a batch of assets, a batch of liabilities or a batch of assets and liabilities for the

purpose of recognition depends on its unit. Account’s unit for the asset or liability must be find in line

with the Standard that needs or allows measurement, other than covered in this Standard (Arnott, et al.,

2017).

Initial Recognition of Fair Value: In exchange related transaction when any asset is purchased or liability

is taken up, the value, which is being incurred to acquire that asset or any value which is received on

account of taking up the liability, that price is called transaction price. It is also known as an entry price.

In contrary to that when any asset is sold or liability is transferred, the value, which will be received is

called the fair value of asset or the liability. It is also known as an exit price. Many times it may happen

to be transaction price equivalent to the fair value in some of the cases (Choy, 2018).

At the time of determining whether transaction price is equal to fair value at the time of initial

recognition, company should consider various things, which are specifically applicable to that given

transaction. If any other accounting standard specifically requires or allows that an asset and liability

should be measured at fair value initially and transaction price is different from the fair value in such

case company should record the balancing figure in the p & l unless that standard give specification

(Lavassani & Movahedi, 2017).

Techniques of Valuation: Company should use those techniques of valuation, which are correct and

accurate in the situations and about which certain facts, which are present for measurement by using

more observable inputs and less of those inputs which are not observable. The primay objective of

valuation is to estimating the value at which the asset will be disposed or liability will be given on the

given measurement date.

There are mainly three types of techniques :

1.) Approach based on Cost

2.) Approach based on Market

3.) Approach based on Income

Cost based Approach: The amount required by the company now to change its capacity of asset. This

cost is called the current replacement cost (Raiborn, et al., 2016).

Income based Approach: This approach changes future estimated cash flows or steams of income and

expenses into a discounted amount. Current market expectations is reflected by fair value

measurement.

5 | P a g e

Description of fair value measurement framework in AASB13

It is used for measurement at initial and subsequent period if it is allowed by standards. Fair value

measurement for assets or liability could be for:

a.) Single liability or asset such as financial instrument

b.) Group of liabilities or assets or group of assets and liabilities like CGU (Trieu, 2017).

Single asset or liability, a batch of assets, a batch of liabilities or a batch of assets and liabilities for the

purpose of recognition depends on its unit. Account’s unit for the asset or liability must be find in line

with the Standard that needs or allows measurement, other than covered in this Standard (Arnott, et al.,

2017).

Initial Recognition of Fair Value: In exchange related transaction when any asset is purchased or liability

is taken up, the value, which is being incurred to acquire that asset or any value which is received on

account of taking up the liability, that price is called transaction price. It is also known as an entry price.

In contrary to that when any asset is sold or liability is transferred, the value, which will be received is

called the fair value of asset or the liability. It is also known as an exit price. Many times it may happen

to be transaction price equivalent to the fair value in some of the cases (Choy, 2018).

At the time of determining whether transaction price is equal to fair value at the time of initial

recognition, company should consider various things, which are specifically applicable to that given

transaction. If any other accounting standard specifically requires or allows that an asset and liability

should be measured at fair value initially and transaction price is different from the fair value in such

case company should record the balancing figure in the p & l unless that standard give specification

(Lavassani & Movahedi, 2017).

Techniques of Valuation: Company should use those techniques of valuation, which are correct and

accurate in the situations and about which certain facts, which are present for measurement by using

more observable inputs and less of those inputs which are not observable. The primay objective of

valuation is to estimating the value at which the asset will be disposed or liability will be given on the

given measurement date.

There are mainly three types of techniques :

1.) Approach based on Cost

2.) Approach based on Market

3.) Approach based on Income

Cost based Approach: The amount required by the company now to change its capacity of asset. This

cost is called the current replacement cost (Raiborn, et al., 2016).

Income based Approach: This approach changes future estimated cash flows or steams of income and

expenses into a discounted amount. Current market expectations is reflected by fair value

measurement.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Examples: present value technique, Black Scholes model, option-pricing models, binomial model that

shows both time value of option and intrinsic value . Multi period excess earnings technique from which

the fair value of some non tangible assets is measured (ICAEW, 2011).

Present value technique: It describes use of present value for the measurement. There are various sub

techniques under present value techniques such as discount rate adjustment technique, expected

present value technique. This also considers risk and uncertainty involved (Sithole, et al., 2017).

Measurement components based on the concept of Present value:

a.) Measurement of upcoming cash flows estimation

b.) Possible differences in value and the timing

c.) Time value

d.) Risk premium

e.) Other relevant factors

f.) Non-performance risk relating to liability

Risk and uncertainty: Measurement of fair value under this technique is made based on conditions,

which are uncertain such as cash flows, which are used for discounting, are just estimates they are not

actual or known values.

Fair value hierarchy: Hierarchy is made for the purpose of increasing the regularity in the measurement

of fair value and disclosures. This is categorized into three parts. Three levels are as follows:

Level one inputs are used when the active markets do exist for the similar assets or liabilities, which is

assessible by the company at the given date of measurement. (Goldmann, 2016).

Level two inputs are in addition to what are covered in Level 1 and additionally which are observable for

the given set of assets or liabilities either directly or indirectly.

Level three inputs are basically those which are unobservable .

Disclosure

Company should make certain important disclosures which will ultimately help a lot to various users to

analyse its financial stetement:

a.) Fair value relating to asset and liabilities in financial statement , the techniques of valuation

being used and inputs being used for the purpose of measurement.

b.) For repeatedly applying measurement via Level 3 inputs, the effect of the measurement on p &

l or OCI for the period (Meroño-Cerdán, et al., 2017).

Entity should appropriately make disclosure showing and giving explanation regarding the hierarchy for

recurrant and non-recurrant measurements.Entity shall make proper disclosure and should consistently

follow policy for transfers between different levels of hierarchy (Johan, 2018). Recognition of into level

transfers or transfers out of levels must be same. Following should be included:

6 | P a g e

Examples: present value technique, Black Scholes model, option-pricing models, binomial model that

shows both time value of option and intrinsic value . Multi period excess earnings technique from which

the fair value of some non tangible assets is measured (ICAEW, 2011).

Present value technique: It describes use of present value for the measurement. There are various sub

techniques under present value techniques such as discount rate adjustment technique, expected

present value technique. This also considers risk and uncertainty involved (Sithole, et al., 2017).

Measurement components based on the concept of Present value:

a.) Measurement of upcoming cash flows estimation

b.) Possible differences in value and the timing

c.) Time value

d.) Risk premium

e.) Other relevant factors

f.) Non-performance risk relating to liability

Risk and uncertainty: Measurement of fair value under this technique is made based on conditions,

which are uncertain such as cash flows, which are used for discounting, are just estimates they are not

actual or known values.

Fair value hierarchy: Hierarchy is made for the purpose of increasing the regularity in the measurement

of fair value and disclosures. This is categorized into three parts. Three levels are as follows:

Level one inputs are used when the active markets do exist for the similar assets or liabilities, which is

assessible by the company at the given date of measurement. (Goldmann, 2016).

Level two inputs are in addition to what are covered in Level 1 and additionally which are observable for

the given set of assets or liabilities either directly or indirectly.

Level three inputs are basically those which are unobservable .

Disclosure

Company should make certain important disclosures which will ultimately help a lot to various users to

analyse its financial stetement:

a.) Fair value relating to asset and liabilities in financial statement , the techniques of valuation

being used and inputs being used for the purpose of measurement.

b.) For repeatedly applying measurement via Level 3 inputs, the effect of the measurement on p &

l or OCI for the period (Meroño-Cerdán, et al., 2017).

Entity should appropriately make disclosure showing and giving explanation regarding the hierarchy for

recurrant and non-recurrant measurements.Entity shall make proper disclosure and should consistently

follow policy for transfers between different levels of hierarchy (Johan, 2018). Recognition of into level

transfers or transfers out of levels must be same. Following should be included:

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

1.) Date of affair or any variation in conditions

2.) Starting of reporting period

3.) At the last of the reporting period

Company shall disclose the required information for every assets and liabilities which are not measured

in the books but for which the fair value is shown. Company is not required to show disclosures

regarding the important unobservable inputs, which are considered in measurement of fair value

categorization under Level 3 of hierarchy (Hepp, 2018). Company shall show the quantitative values in a

table format except any other format is suitable.

Conclusion

Disclosure of fair value in the financial statement of any company is one of the most important

disclosure as it shows or reflects the true value to various users of financial statement. It helps users to

make decisions relating to the desired expectations of users of financial statement. Conceptual

framework of fair value measurement tells us how to use fair value account especially in financial

instruments to make appropriate decision. Keeping in mind above facts it can be concluded that fair

value measurement is one of the most important recognition and measurement for any company as it

reflects the true picture of the company.

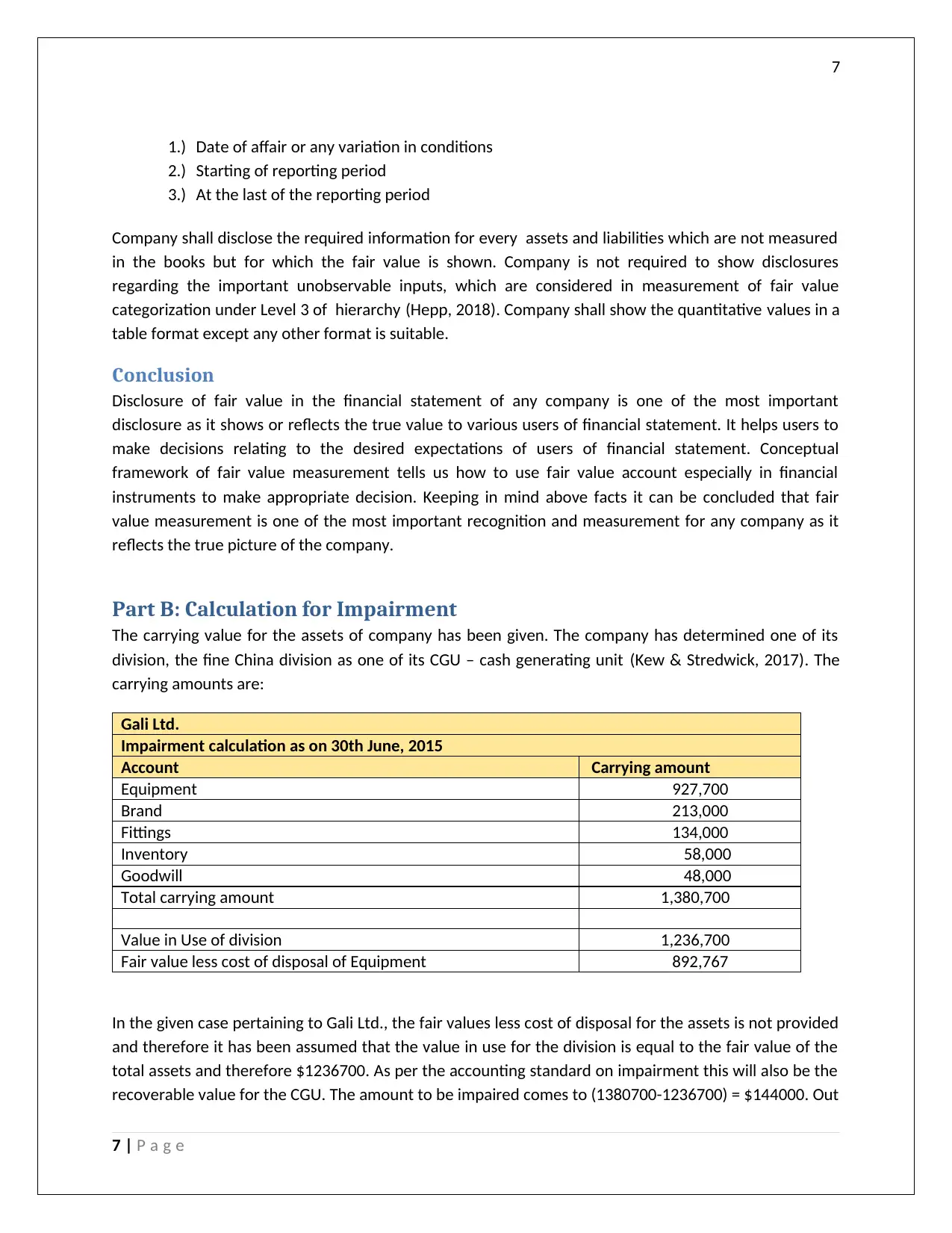

Part B: Calculation for Impairment

The carrying value for the assets of company has been given. The company has determined one of its

division, the fine China division as one of its CGU – cash generating unit (Kew & Stredwick, 2017). The

carrying amounts are:

Gali Ltd.

Impairment calculation as on 30th June, 2015

Account Carrying amount

Equipment 927,700

Brand 213,000

Fittings 134,000

Inventory 58,000

Goodwill 48,000

Total carrying amount 1,380,700

Value in Use of division 1,236,700

Fair value less cost of disposal of Equipment 892,767

In the given case pertaining to Gali Ltd., the fair values less cost of disposal for the assets is not provided

and therefore it has been assumed that the value in use for the division is equal to the fair value of the

total assets and therefore $1236700. As per the accounting standard on impairment this will also be the

recoverable value for the CGU. The amount to be impaired comes to (1380700-1236700) = $144000. Out

7 | P a g e

1.) Date of affair or any variation in conditions

2.) Starting of reporting period

3.) At the last of the reporting period

Company shall disclose the required information for every assets and liabilities which are not measured

in the books but for which the fair value is shown. Company is not required to show disclosures

regarding the important unobservable inputs, which are considered in measurement of fair value

categorization under Level 3 of hierarchy (Hepp, 2018). Company shall show the quantitative values in a

table format except any other format is suitable.

Conclusion

Disclosure of fair value in the financial statement of any company is one of the most important

disclosure as it shows or reflects the true value to various users of financial statement. It helps users to

make decisions relating to the desired expectations of users of financial statement. Conceptual

framework of fair value measurement tells us how to use fair value account especially in financial

instruments to make appropriate decision. Keeping in mind above facts it can be concluded that fair

value measurement is one of the most important recognition and measurement for any company as it

reflects the true picture of the company.

Part B: Calculation for Impairment

The carrying value for the assets of company has been given. The company has determined one of its

division, the fine China division as one of its CGU – cash generating unit (Kew & Stredwick, 2017). The

carrying amounts are:

Gali Ltd.

Impairment calculation as on 30th June, 2015

Account Carrying amount

Equipment 927,700

Brand 213,000

Fittings 134,000

Inventory 58,000

Goodwill 48,000

Total carrying amount 1,380,700

Value in Use of division 1,236,700

Fair value less cost of disposal of Equipment 892,767

In the given case pertaining to Gali Ltd., the fair values less cost of disposal for the assets is not provided

and therefore it has been assumed that the value in use for the division is equal to the fair value of the

total assets and therefore $1236700. As per the accounting standard on impairment this will also be the

recoverable value for the CGU. The amount to be impaired comes to (1380700-1236700) = $144000. Out

7 | P a g e

8

of the amount, the amount needs to be first allocated towards goodwill post which it can be allocated to

the other assets as per the accounting standard and therefore amount allocated towards impairment of

goodwill is $48000 (Heminway, 2017). Remaining amount of $(144000-48000) = $96000 can now be

allocated towards other assets. As per the accounting standard, the current assets, which are being held

for sale, do not qualify for impairment and therefore the inventory will not be impaired in the given

case. The working for impairment expense allocation to other assets has been shown below:

Account Carrying Amount Pro rata Impairment loss allocated Adjusted CA

Equipment 927,700 0.73 69,867 857,833

Brand 213,000 0.17 16,041 196,959

Fittings 134,000 0.11 10,092 123,908

Total CA 1274700 1.00 96,000 1178700

Furthermore, since the fair value less cost of disposal has been given for equipment therefore

impairment on the same is limited to the extent such that carrying value cannot go below $892767 and

therefore the maximum allocation of impairment to the value of the equipment, is $34933. The rest of

the amount which has been allocated to equipment (69867-34933) = $34934 should now be

apportioned to the other assets of the CGU (Jefferson, 2017).

The 2nd level of allocation and final summary of impairment has been shown below:

Account Adjusted

CA Pro rata Impairment loss

allocated

Total impairment loss

allocated

Equipmen

t 34,933

Brand 196,959

0.6

1 21,444 37,485

Fittings 123,908

0.3

9 13,490 23,582

Total CA 320,867

1.0

0 34,934 96,000

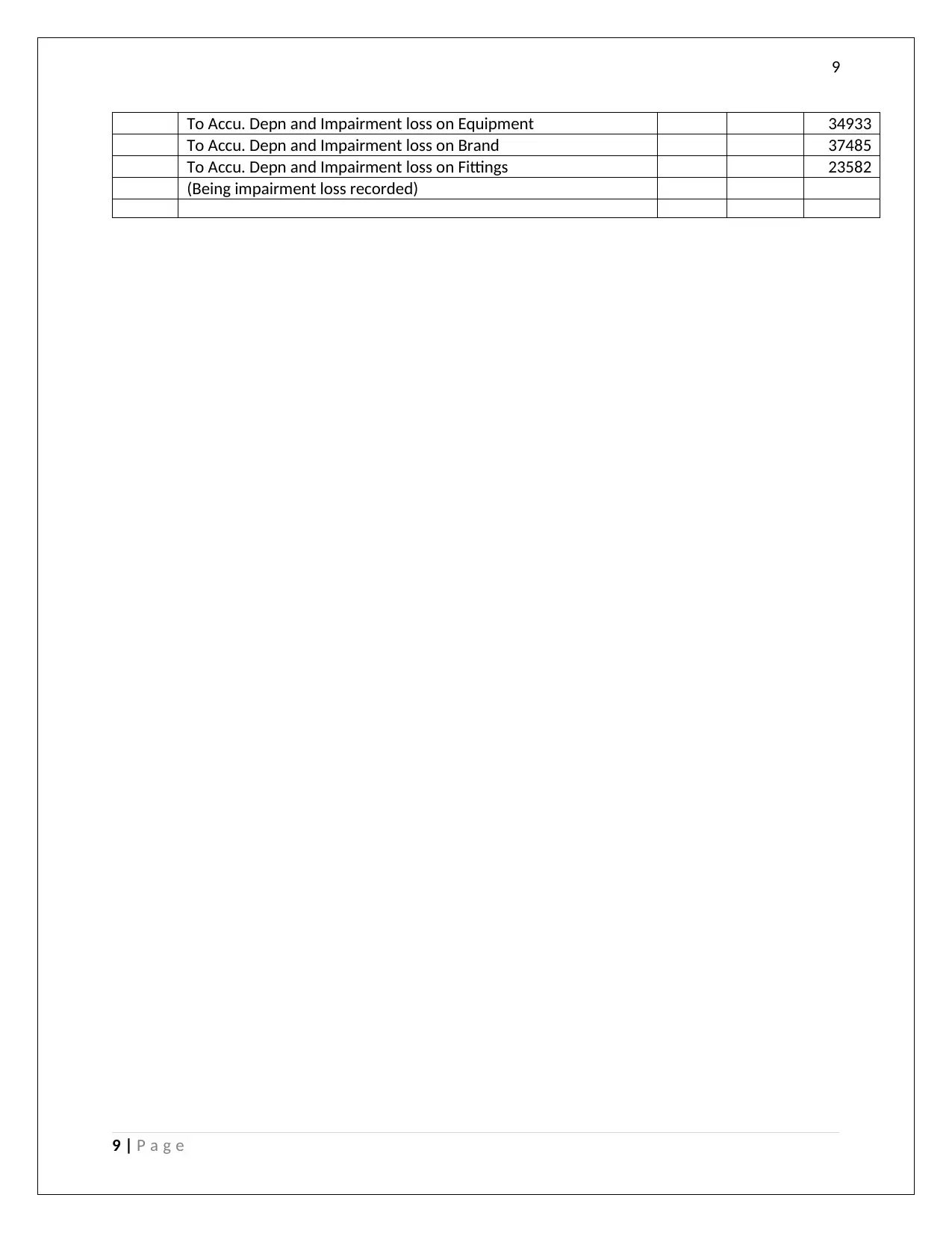

Therefore, the final allocation is as follows:

Goodwill: $48000; Equipment: $34933; Brand: $37485; Fittings: 23582

The journal entry to record the impairment loss in the books of accounts as on 30 th June 2015 has been

shown below:

Journal

Date Particulars Dr./Cr. Amt ($) Amt ($)

2015

30-Jun Impairment Loss Dr. 144000

To Goodwill 48000

8 | P a g e

of the amount, the amount needs to be first allocated towards goodwill post which it can be allocated to

the other assets as per the accounting standard and therefore amount allocated towards impairment of

goodwill is $48000 (Heminway, 2017). Remaining amount of $(144000-48000) = $96000 can now be

allocated towards other assets. As per the accounting standard, the current assets, which are being held

for sale, do not qualify for impairment and therefore the inventory will not be impaired in the given

case. The working for impairment expense allocation to other assets has been shown below:

Account Carrying Amount Pro rata Impairment loss allocated Adjusted CA

Equipment 927,700 0.73 69,867 857,833

Brand 213,000 0.17 16,041 196,959

Fittings 134,000 0.11 10,092 123,908

Total CA 1274700 1.00 96,000 1178700

Furthermore, since the fair value less cost of disposal has been given for equipment therefore

impairment on the same is limited to the extent such that carrying value cannot go below $892767 and

therefore the maximum allocation of impairment to the value of the equipment, is $34933. The rest of

the amount which has been allocated to equipment (69867-34933) = $34934 should now be

apportioned to the other assets of the CGU (Jefferson, 2017).

The 2nd level of allocation and final summary of impairment has been shown below:

Account Adjusted

CA Pro rata Impairment loss

allocated

Total impairment loss

allocated

Equipmen

t 34,933

Brand 196,959

0.6

1 21,444 37,485

Fittings 123,908

0.3

9 13,490 23,582

Total CA 320,867

1.0

0 34,934 96,000

Therefore, the final allocation is as follows:

Goodwill: $48000; Equipment: $34933; Brand: $37485; Fittings: 23582

The journal entry to record the impairment loss in the books of accounts as on 30 th June 2015 has been

shown below:

Journal

Date Particulars Dr./Cr. Amt ($) Amt ($)

2015

30-Jun Impairment Loss Dr. 144000

To Goodwill 48000

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

To Accu. Depn and Impairment loss on Equipment 34933

To Accu. Depn and Impairment loss on Brand 37485

To Accu. Depn and Impairment loss on Fittings 23582

(Being impairment loss recorded)

9 | P a g e

To Accu. Depn and Impairment loss on Equipment 34933

To Accu. Depn and Impairment loss on Brand 37485

To Accu. Depn and Impairment loss on Fittings 23582

(Being impairment loss recorded)

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Johan, S., 2018. The Relationship Between Economic Value Added, Market Value Added And Return On

Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan Kewirausahaan,

3(1), pp. 121-134.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

10 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Johan, S., 2018. The Relationship Between Economic Value Added, Market Value Added And Return On

Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan Kewirausahaan,

3(1), pp. 121-134.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

10 | P a g e

11

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

11 | P a g e

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.