Fair Value Measurement of Assets: IFRS 13 and Wesfarmers

VerifiedAdded on 2020/03/02

|10

|2828

|205

Report

AI Summary

This report provides an executive summary on the significance of fair value measurement under IFRS 13, focusing on its application in business entities. It delves into the definition of fair value as per IASB, emphasizing the valuation techniques employed to determine the fair value of assets and liabilities, with a particular focus on non-current assets. The report highlights the challenges businesses encounter when implementing fair value measurement, particularly in the context of assets not actively traded. It uses Wesfarmers Limited as a case study, examining the types of non-current assets held by the company, and the problems faced in assessing their fair value. Furthermore, the report critically analyzes the practicality of the IASB's approach to fair value measurement for companies holding non-current assets that lack broad and deep markets, offering insights into the complexities and implications of IFRS 13.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report addresses the usefulness of the IFRS 13 standard adopted by the IASB in

relation to the fair value measurement in statement of financial position of business entities. The

report, as such, present an evaluation of the concept of fair value measurement concept and the

type of valuation techniques adopted by business entities for estimating the far value of its assets

and liabilities. Also, the report discusses the problems faced by the business entities for

implementing the use of fair value measurement concept. At last, the report presents a critical

analysis of the usefulness of IASB approach to fair value measurement for companies with non-

current assets that are not actively traded on broad and deep markets.

This report addresses the usefulness of the IFRS 13 standard adopted by the IASB in

relation to the fair value measurement in statement of financial position of business entities. The

report, as such, present an evaluation of the concept of fair value measurement concept and the

type of valuation techniques adopted by business entities for estimating the far value of its assets

and liabilities. Also, the report discusses the problems faced by the business entities for

implementing the use of fair value measurement concept. At last, the report presents a critical

analysis of the usefulness of IASB approach to fair value measurement for companies with non-

current assets that are not actively traded on broad and deep markets.

Introduction

The present report demonstrates the importance of fair value and measurement in the

statement of financial positions of business organizations. The term ‘fair value’ as per the IASB

is the price realized by selling an asset or paid through transfer of a liability in a transaction

occurring between the market participants on the date of measurement (IFRS 13 Fair Value

Measurement, 2010). For the purpose, the report presents an analysis of the company having

equity share capital listed on a stock exchange. The company selected for the purpose is

Wesfarmers Limited operating in the retail sector of Australia. The report, in this context,

identifies the major type of fixed assets of a selected company and discusses the problems faced

by it for assessing the fair value of these identified assets. In addition to this, the report carries

out a critical analysis of whether the IASB approach to fair value measurement is practical for

businesses having non-current assets that are not actively traded on broad markets.

IFRS 13 Fair Value Measurement

The IASB has developed and adopted the approach to measure fair value in its

International Financial Reporting Standard of IFRS 13. The IFRS 13 has defined the ‘fair value’

as a price that is received for selling an asset or is paid for transferring a liability. The IFRS 13

provides a standard framework to business entities regarding the measurement of fair value. The

standard is based on measuring fair value on the basis of market rather than using entity-specific

measurement (Abdalrahim and Hammad, 2015). The main objective behind the development of

IFRS 13 by IASB is to enhance the consistency and comparability in measurement of fair value.

The business entities for assessing the fair value should appropriately determine the respective

assets or liabilities whose fair values are to be assessed. However, in the case of measuring the

fair value of a fixed asset, the entities should select the valuation premise that is appropriate for

its measurement. The business entities under IFRS 13 should also determine the major market

for the asset or liability by taking into consideration the availability of data within the market that

would be used by the participants at the time of pricing an asset or liability (IFRS 13 — Fair

Value Measurement, 2017).

The IFRS 13 standard also incorporates specific guidelines for providing guidance to

business entities in relation to the measurement of fair value. The business entities are required to

The present report demonstrates the importance of fair value and measurement in the

statement of financial positions of business organizations. The term ‘fair value’ as per the IASB

is the price realized by selling an asset or paid through transfer of a liability in a transaction

occurring between the market participants on the date of measurement (IFRS 13 Fair Value

Measurement, 2010). For the purpose, the report presents an analysis of the company having

equity share capital listed on a stock exchange. The company selected for the purpose is

Wesfarmers Limited operating in the retail sector of Australia. The report, in this context,

identifies the major type of fixed assets of a selected company and discusses the problems faced

by it for assessing the fair value of these identified assets. In addition to this, the report carries

out a critical analysis of whether the IASB approach to fair value measurement is practical for

businesses having non-current assets that are not actively traded on broad markets.

IFRS 13 Fair Value Measurement

The IASB has developed and adopted the approach to measure fair value in its

International Financial Reporting Standard of IFRS 13. The IFRS 13 has defined the ‘fair value’

as a price that is received for selling an asset or is paid for transferring a liability. The IFRS 13

provides a standard framework to business entities regarding the measurement of fair value. The

standard is based on measuring fair value on the basis of market rather than using entity-specific

measurement (Abdalrahim and Hammad, 2015). The main objective behind the development of

IFRS 13 by IASB is to enhance the consistency and comparability in measurement of fair value.

The business entities for assessing the fair value should appropriately determine the respective

assets or liabilities whose fair values are to be assessed. However, in the case of measuring the

fair value of a fixed asset, the entities should select the valuation premise that is appropriate for

its measurement. The business entities under IFRS 13 should also determine the major market

for the asset or liability by taking into consideration the availability of data within the market that

would be used by the participants at the time of pricing an asset or liability (IFRS 13 — Fair

Value Measurement, 2017).

The IFRS 13 standard also incorporates specific guidelines for providing guidance to

business entities in relation to the measurement of fair value. The business entities are required to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consider the asset condition and the location and any type of limitations imposed on the sale and

asset use. Also, the measurement of fair value requires an orderly transaction to take place

between the participants within the market on the date of measuring the assets or liabilities. The

fair value of a liability states the non-performance risk that takes into account the credit risk of a

business entity. The business enterprises should also use appropriate valuation techniques for

measuring the fair value of an asset or liability (Christensen and Nicolaev, 2011). The main

purpose the valuation technique is to predict the actual price at which an organized business

contract for selling an asset or transferring a liability ocuurs. The main valuation techniques used

for measuring the fair value of an asset are market approach, cost approach and income

approach. The market approach incorporates the use of price and other information available in

the market for carrying out orderly transactions. On the other hand, the cost approach uses the

current replacement cost that would be required for replacing the serving ability of an asset.

However, the income approach depicts the recent fluctuations in the market by transferring the

future amount of cash flows unto a single amount (IFRS 13 Fair Value Measurement, 2010).

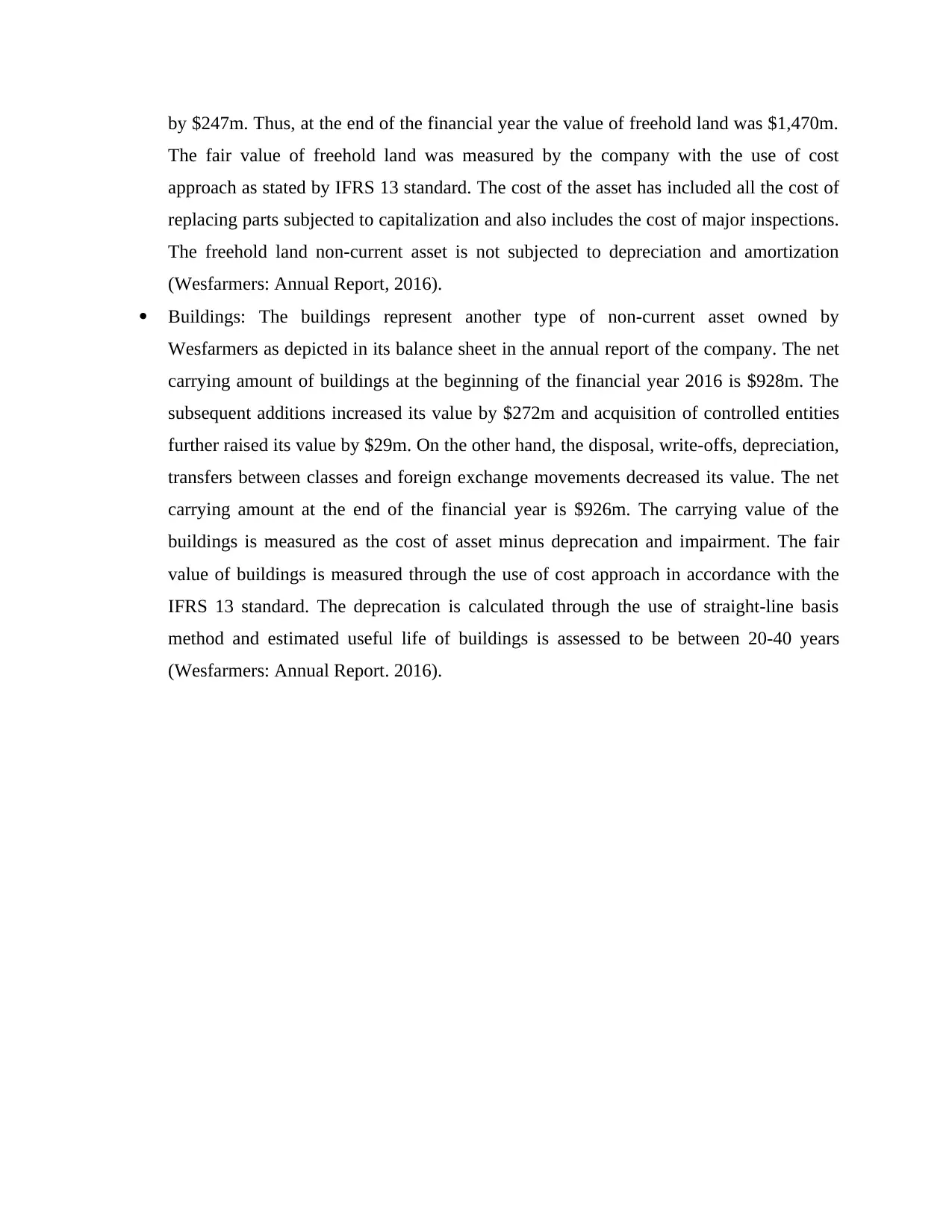

Major types of Non-current (fixed) asset owned by Wesfarmers Limited

The non-current assets of a business entity refer to the long-term investments made by it

such as in property, plant and equipment. The term ‘non-current asset’ is used mainly to depict

the assets that cannot be easily liquidated, that is they cannot be easily converted into cash. On

the other hand, the current assets refer to the assets that can be easily liquidated such as cash or

bank accounts (IFRS 13 Fair Value Measurement, 2010). The non-current assets of Wesfarmers

Limited are described in the present section of the report. Wesfarmers, a recognized retail

company of Australia has described its type of non-current assets in the notes to financial

statements section of its annual report. The major types of non-current assets recognized by the

company are as follows:

Freehold Land: The freehold land is categorized by the company under non-current asset

of property. As depicted form the balance sheet of the company, the initial value of

freehold land at the beginning of the financial year was $1,547m. The subsequent

addition to its value of $118 m was made during the year. The acquisition of its

controlled entities increased its value to $49m and foreign exchange movements also

raised its value by $3m. On the other hand, disposals and write-offs decreased its value

asset use. Also, the measurement of fair value requires an orderly transaction to take place

between the participants within the market on the date of measuring the assets or liabilities. The

fair value of a liability states the non-performance risk that takes into account the credit risk of a

business entity. The business enterprises should also use appropriate valuation techniques for

measuring the fair value of an asset or liability (Christensen and Nicolaev, 2011). The main

purpose the valuation technique is to predict the actual price at which an organized business

contract for selling an asset or transferring a liability ocuurs. The main valuation techniques used

for measuring the fair value of an asset are market approach, cost approach and income

approach. The market approach incorporates the use of price and other information available in

the market for carrying out orderly transactions. On the other hand, the cost approach uses the

current replacement cost that would be required for replacing the serving ability of an asset.

However, the income approach depicts the recent fluctuations in the market by transferring the

future amount of cash flows unto a single amount (IFRS 13 Fair Value Measurement, 2010).

Major types of Non-current (fixed) asset owned by Wesfarmers Limited

The non-current assets of a business entity refer to the long-term investments made by it

such as in property, plant and equipment. The term ‘non-current asset’ is used mainly to depict

the assets that cannot be easily liquidated, that is they cannot be easily converted into cash. On

the other hand, the current assets refer to the assets that can be easily liquidated such as cash or

bank accounts (IFRS 13 Fair Value Measurement, 2010). The non-current assets of Wesfarmers

Limited are described in the present section of the report. Wesfarmers, a recognized retail

company of Australia has described its type of non-current assets in the notes to financial

statements section of its annual report. The major types of non-current assets recognized by the

company are as follows:

Freehold Land: The freehold land is categorized by the company under non-current asset

of property. As depicted form the balance sheet of the company, the initial value of

freehold land at the beginning of the financial year was $1,547m. The subsequent

addition to its value of $118 m was made during the year. The acquisition of its

controlled entities increased its value to $49m and foreign exchange movements also

raised its value by $3m. On the other hand, disposals and write-offs decreased its value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

by $247m. Thus, at the end of the financial year the value of freehold land was $1,470m.

The fair value of freehold land was measured by the company with the use of cost

approach as stated by IFRS 13 standard. The cost of the asset has included all the cost of

replacing parts subjected to capitalization and also includes the cost of major inspections.

The freehold land non-current asset is not subjected to depreciation and amortization

(Wesfarmers: Annual Report, 2016).

Buildings: The buildings represent another type of non-current asset owned by

Wesfarmers as depicted in its balance sheet in the annual report of the company. The net

carrying amount of buildings at the beginning of the financial year 2016 is $928m. The

subsequent additions increased its value by $272m and acquisition of controlled entities

further raised its value by $29m. On the other hand, the disposal, write-offs, depreciation,

transfers between classes and foreign exchange movements decreased its value. The net

carrying amount at the end of the financial year is $926m. The carrying value of the

buildings is measured as the cost of asset minus deprecation and impairment. The fair

value of buildings is measured through the use of cost approach in accordance with the

IFRS 13 standard. The deprecation is calculated through the use of straight-line basis

method and estimated useful life of buildings is assessed to be between 20-40 years

(Wesfarmers: Annual Report. 2016).

The fair value of freehold land was measured by the company with the use of cost

approach as stated by IFRS 13 standard. The cost of the asset has included all the cost of

replacing parts subjected to capitalization and also includes the cost of major inspections.

The freehold land non-current asset is not subjected to depreciation and amortization

(Wesfarmers: Annual Report, 2016).

Buildings: The buildings represent another type of non-current asset owned by

Wesfarmers as depicted in its balance sheet in the annual report of the company. The net

carrying amount of buildings at the beginning of the financial year 2016 is $928m. The

subsequent additions increased its value by $272m and acquisition of controlled entities

further raised its value by $29m. On the other hand, the disposal, write-offs, depreciation,

transfers between classes and foreign exchange movements decreased its value. The net

carrying amount at the end of the financial year is $926m. The carrying value of the

buildings is measured as the cost of asset minus deprecation and impairment. The fair

value of buildings is measured through the use of cost approach in accordance with the

IFRS 13 standard. The deprecation is calculated through the use of straight-line basis

method and estimated useful life of buildings is assessed to be between 20-40 years

(Wesfarmers: Annual Report. 2016).

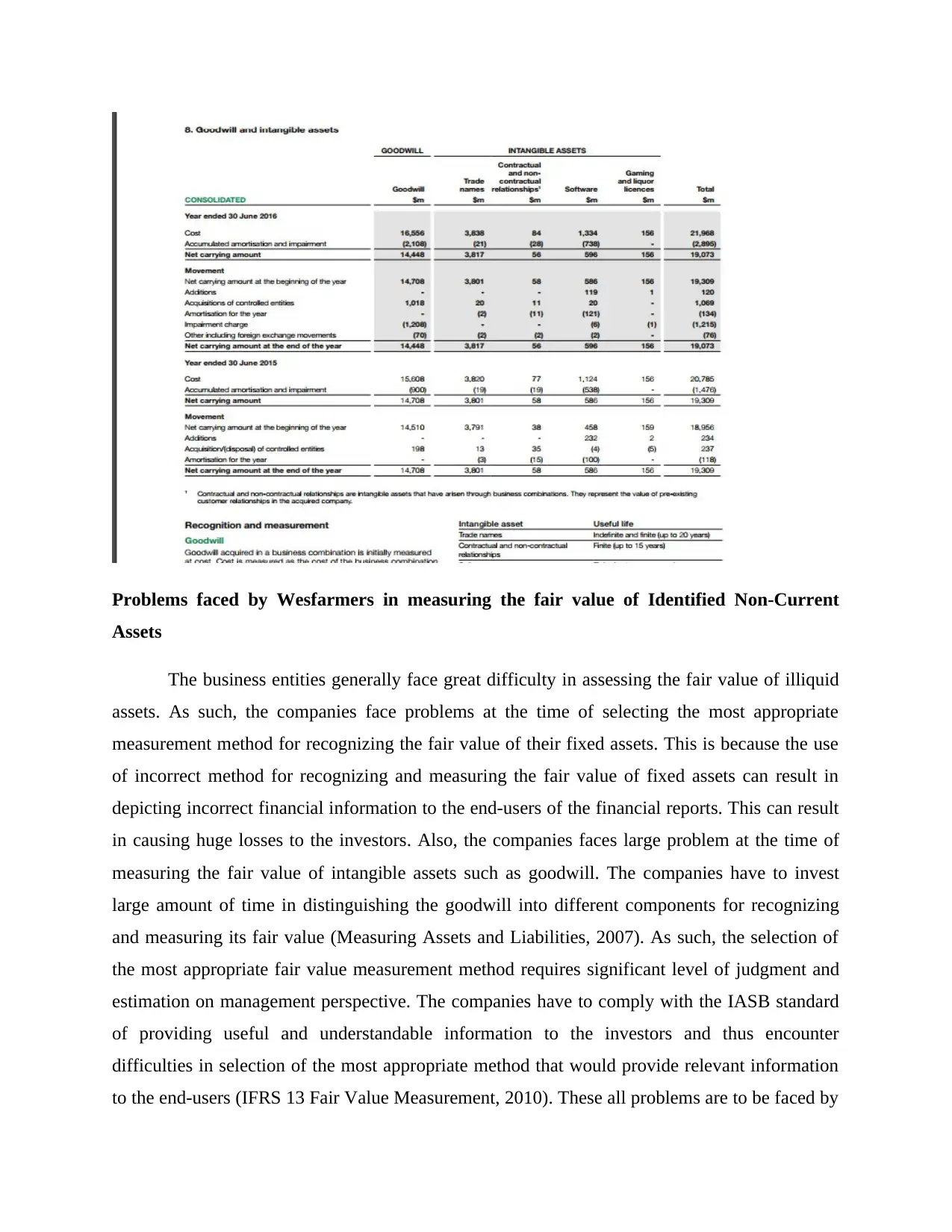

Goodwill: The goodwill is depicted as intangible non-current asset in the balance sheet of

Wesfarmers Limited. The net carrying amount of the goodwill as depicted in the balance

sheet of the company is $14,708m. The acquisition of controlled entities has increased

the value of goodwill. On the other hand, the impairment charge and foreign exchange

movements have decreased the value of goodwill. Thus, the net carrying amount of the

goodwill at the end of the financial year is $14,448m. The fair value of goodwill is

measured by the use of cost approach. The cost is measured as the cost of business

combined by deducting the net fair value of acquired and identifiable assets, liabilities

and contingent liabilities. The accumulated impairment losses are deducted from the cost

of goodwill measured (Wesfarmers: Annual Report. 2016).

Wesfarmers Limited. The net carrying amount of the goodwill as depicted in the balance

sheet of the company is $14,708m. The acquisition of controlled entities has increased

the value of goodwill. On the other hand, the impairment charge and foreign exchange

movements have decreased the value of goodwill. Thus, the net carrying amount of the

goodwill at the end of the financial year is $14,448m. The fair value of goodwill is

measured by the use of cost approach. The cost is measured as the cost of business

combined by deducting the net fair value of acquired and identifiable assets, liabilities

and contingent liabilities. The accumulated impairment losses are deducted from the cost

of goodwill measured (Wesfarmers: Annual Report. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Problems faced by Wesfarmers in measuring the fair value of Identified Non-Current

Assets

The business entities generally face great difficulty in assessing the fair value of illiquid

assets. As such, the companies face problems at the time of selecting the most appropriate

measurement method for recognizing the fair value of their fixed assets. This is because the use

of incorrect method for recognizing and measuring the fair value of fixed assets can result in

depicting incorrect financial information to the end-users of the financial reports. This can result

in causing huge losses to the investors. Also, the companies faces large problem at the time of

measuring the fair value of intangible assets such as goodwill. The companies have to invest

large amount of time in distinguishing the goodwill into different components for recognizing

and measuring its fair value (Measuring Assets and Liabilities, 2007). As such, the selection of

the most appropriate fair value measurement method requires significant level of judgment and

estimation on management perspective. The companies have to comply with the IASB standard

of providing useful and understandable information to the investors and thus encounter

difficulties in selection of the most appropriate method that would provide relevant information

to the end-users (IFRS 13 Fair Value Measurement, 2010). These all problems are to be faced by

Assets

The business entities generally face great difficulty in assessing the fair value of illiquid

assets. As such, the companies face problems at the time of selecting the most appropriate

measurement method for recognizing the fair value of their fixed assets. This is because the use

of incorrect method for recognizing and measuring the fair value of fixed assets can result in

depicting incorrect financial information to the end-users of the financial reports. This can result

in causing huge losses to the investors. Also, the companies faces large problem at the time of

measuring the fair value of intangible assets such as goodwill. The companies have to invest

large amount of time in distinguishing the goodwill into different components for recognizing

and measuring its fair value (Measuring Assets and Liabilities, 2007). As such, the selection of

the most appropriate fair value measurement method requires significant level of judgment and

estimation on management perspective. The companies have to comply with the IASB standard

of providing useful and understandable information to the investors and thus encounter

difficulties in selection of the most appropriate method that would provide relevant information

to the end-users (IFRS 13 Fair Value Measurement, 2010). These all problems are to be faced by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers also in measuring the fair value of its fixed assets as identified above (Wesfarmers:

Annual Report. 2016).

The Wesfarmers have adopted the use of cost approach in measuring the fair value of its

non-current assets. The cost approach method as stated in the IFRS 13 standard is used for

measuring the fair value of an asset or liability by estimating the current replacement cost that

would be required for replacing the service capacity of an asset. The cost approach used for

estimating the fair value of land is not depreciated while the value of building is depreciated

through the use of straight-line basis method. On the other hand, the fair value of goodwill

measured at cost by deducting the accumulated impairment losses. The measurement method

used by the company is reviewed annually by the management for determining the real value of

its fixed assets and thus protecting the investors’ confidence. The company as such also face

problem in reviewing the measurement method adopted whenever there us change in the

economic circumstances such as change in store performance or changes in the long-term coal

price forecasts (Wesfarmers: Annual Report. 2016).

Critical analysis for determining the practical basis of IASB’s approach to fair value

measurement for companies with fixed assets not actively traded

The international and national accounting standard-setting bodies have mandated the

business companies to integrate the use of fair value measurement concept. The use of fair value

accounting technique is mandated by the IASB for securing the interests of investors by

providing them relevant information for decision-making. However, there has been continuous

debate on the usefulness of IASB approach to fair value measurement for companies with fixed

assets (Herrmann, Saudagaran and Thomas, 2006). The fair value measurement concept was

criticized as it estimates the value of some assets at zero that resulted in the downfall of many

business entities. The use of fair value measurement concept makes it rather difficult to identify

the managerial fraud and the estimation is more difficult if the company has non-current asset.

The fair value amendments are also rather difficult to be understood by the auditors and therefore

its application becomes very complicated by the business entities (Alaryan, Haiji and Alrabei,

2014).

Annual Report. 2016).

The Wesfarmers have adopted the use of cost approach in measuring the fair value of its

non-current assets. The cost approach method as stated in the IFRS 13 standard is used for

measuring the fair value of an asset or liability by estimating the current replacement cost that

would be required for replacing the service capacity of an asset. The cost approach used for

estimating the fair value of land is not depreciated while the value of building is depreciated

through the use of straight-line basis method. On the other hand, the fair value of goodwill

measured at cost by deducting the accumulated impairment losses. The measurement method

used by the company is reviewed annually by the management for determining the real value of

its fixed assets and thus protecting the investors’ confidence. The company as such also face

problem in reviewing the measurement method adopted whenever there us change in the

economic circumstances such as change in store performance or changes in the long-term coal

price forecasts (Wesfarmers: Annual Report. 2016).

Critical analysis for determining the practical basis of IASB’s approach to fair value

measurement for companies with fixed assets not actively traded

The international and national accounting standard-setting bodies have mandated the

business companies to integrate the use of fair value measurement concept. The use of fair value

accounting technique is mandated by the IASB for securing the interests of investors by

providing them relevant information for decision-making. However, there has been continuous

debate on the usefulness of IASB approach to fair value measurement for companies with fixed

assets (Herrmann, Saudagaran and Thomas, 2006). The fair value measurement concept was

criticized as it estimates the value of some assets at zero that resulted in the downfall of many

business entities. The use of fair value measurement concept makes it rather difficult to identify

the managerial fraud and the estimation is more difficult if the company has non-current asset.

The fair value amendments are also rather difficult to be understood by the auditors and therefore

its application becomes very complicated by the business entities (Alaryan, Haiji and Alrabei,

2014).

The IFRS 13 standard adopted by the IASB regarding measuring the fair value of assets

and liabilities requires businesses to adopt appropriate valuation techniques to estimate the fair

value of its assets. As such, the business having non-current assets rather face difficulty in

effectively complying with this IFRS standard as it requires appropriate judgment of

management and annual review. Also, special training has to be provided to the auditors and

accountant for estimating the fair value of its non-current assets fairly and adequately. This

requires companies with non-current assets to develop and establish new procedures for

determining the appropriate measurement policies and procedures (Edwards and Walker, 2009).

Thus, the use of fair value measurement concept can provide misleading information for the

business having assets that fluctuate largely in value throughout the year. Also, the information

available from the market in relation to the non-current asset may not indicate its fundamental

value due to market inefficiencies. In addition to this, the manipulation in the price of an asset by

a business entity also poses a major risk in assessing the fair value of an asset. This happen

mainly in illiquid markets as trading by firms can impact its traded as well as its quoted prices.

Therefore, it can be stated from the overall discussion that IASB approach to fair value

measurement is not largely practical for companies that operates in illiquid financial market

(Scarlata, Sole and Novoa, 2009).

Conclusion

Thus, it can be stated from the overall discussion that IASB has adopted the IFRS 13

standard in relation to the fair value measurement for improving the quality of financial

reporting. However, the business entities having non-current assets also face difficulties in

recognizing and measuring the fair value of its fixed assets such as property, plant and

equipment. The appropriate use of fair value accounting requires correct judgment and selection

on the part of management otherwise it can result in incorrect valuation of the fixed assets of the

company. The measurement method also requires annual review on the part of the company in

order to ensure that the method adopted is in accordance to the external market conditions.

and liabilities requires businesses to adopt appropriate valuation techniques to estimate the fair

value of its assets. As such, the business having non-current assets rather face difficulty in

effectively complying with this IFRS standard as it requires appropriate judgment of

management and annual review. Also, special training has to be provided to the auditors and

accountant for estimating the fair value of its non-current assets fairly and adequately. This

requires companies with non-current assets to develop and establish new procedures for

determining the appropriate measurement policies and procedures (Edwards and Walker, 2009).

Thus, the use of fair value measurement concept can provide misleading information for the

business having assets that fluctuate largely in value throughout the year. Also, the information

available from the market in relation to the non-current asset may not indicate its fundamental

value due to market inefficiencies. In addition to this, the manipulation in the price of an asset by

a business entity also poses a major risk in assessing the fair value of an asset. This happen

mainly in illiquid markets as trading by firms can impact its traded as well as its quoted prices.

Therefore, it can be stated from the overall discussion that IASB approach to fair value

measurement is not largely practical for companies that operates in illiquid financial market

(Scarlata, Sole and Novoa, 2009).

Conclusion

Thus, it can be stated from the overall discussion that IASB has adopted the IFRS 13

standard in relation to the fair value measurement for improving the quality of financial

reporting. However, the business entities having non-current assets also face difficulties in

recognizing and measuring the fair value of its fixed assets such as property, plant and

equipment. The appropriate use of fair value accounting requires correct judgment and selection

on the part of management otherwise it can result in incorrect valuation of the fixed assets of the

company. The measurement method also requires annual review on the part of the company in

order to ensure that the method adopted is in accordance to the external market conditions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abdalrahim, A.A. and Hammad, S.M. 2015. The Impact of the Application of Fair Value

Accounting on the Quality of Accounting Information. An Empirical Study on a Group of

Companies Listed on the Khartoum Stock Exchange. International Journal of Academic

Research in Accounting, Finance and Management Sciences 5 (1), pp. 148–160.

Alaryan, L., Haija, A. and Alrabei, A. 2014. The Relationship between Fair Value Accounting

and Presence of Manipulation in Financial Statements. International Journal of Accounting and

Financial Reporting 4(1), pp. 221-237.

Christensen, H. B. and Nicolaev, V. V. 2011. Does fair value accounting for non-financial assets

pass the market test? Review of Accounting Studies 18 (3), pp. 734-775.

Edwards, J.R. and Walker, S. 2009. The Routledge Companion to Accounting History.

Routledge.

Herrmann, D., Saudagaran, S. M. and Thomas, W. B. 2006. The quality of fair value measures

for property, plant, and equipment. Accounting Forum 30 (1), pp. 43-59.

IFRS 13 — Fair Value Measurement. 2017. [Online]. Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs13 [Accessed on: 24 August 2017].

IFRS 13 Fair Value Measurement. 2010. Online]. Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

ifrs-factsheets/factsheet-ifrs13-fair-value-measurement.pdf?la=en [Accessed on: 24 August

2017].

Measuring Assets and Liabilities. 2007. [Online]. Available at: https://www.pwc.com/gx/en/ifrs-

reporting/pdf/measuringassetssurvey.pdf [Accessed on: 24 August 2017].

Scarlata, J., Sole, J. and Novoa, A. 2009. Procyclicality and Fair Value Accounting. International

Monetary Fund.

Wesfarmers: Annual Report. 2016. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4

[Accessed on: 24 August 2017].

Abdalrahim, A.A. and Hammad, S.M. 2015. The Impact of the Application of Fair Value

Accounting on the Quality of Accounting Information. An Empirical Study on a Group of

Companies Listed on the Khartoum Stock Exchange. International Journal of Academic

Research in Accounting, Finance and Management Sciences 5 (1), pp. 148–160.

Alaryan, L., Haija, A. and Alrabei, A. 2014. The Relationship between Fair Value Accounting

and Presence of Manipulation in Financial Statements. International Journal of Accounting and

Financial Reporting 4(1), pp. 221-237.

Christensen, H. B. and Nicolaev, V. V. 2011. Does fair value accounting for non-financial assets

pass the market test? Review of Accounting Studies 18 (3), pp. 734-775.

Edwards, J.R. and Walker, S. 2009. The Routledge Companion to Accounting History.

Routledge.

Herrmann, D., Saudagaran, S. M. and Thomas, W. B. 2006. The quality of fair value measures

for property, plant, and equipment. Accounting Forum 30 (1), pp. 43-59.

IFRS 13 — Fair Value Measurement. 2017. [Online]. Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs13 [Accessed on: 24 August 2017].

IFRS 13 Fair Value Measurement. 2010. Online]. Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

ifrs-factsheets/factsheet-ifrs13-fair-value-measurement.pdf?la=en [Accessed on: 24 August

2017].

Measuring Assets and Liabilities. 2007. [Online]. Available at: https://www.pwc.com/gx/en/ifrs-

reporting/pdf/measuringassetssurvey.pdf [Accessed on: 24 August 2017].

Scarlata, J., Sole, J. and Novoa, A. 2009. Procyclicality and Fair Value Accounting. International

Monetary Fund.

Wesfarmers: Annual Report. 2016. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4

[Accessed on: 24 August 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.