Foundations in Accounting: Fair Value Accounting Debate Report

VerifiedAdded on 2021/04/24

|11

|2524

|70

Report

AI Summary

This report delves into the debate between Fair Value Accounting (FVA) and Historical Cost Accounting (HCA), particularly within the context of International Financial Reporting Standards (IFRS). It examines the advantages and disadvantages of FVA, its impact on balance sheets, and whether it should permanently replace HCA for valuing non-current assets. The report uses the 2017 Annual Report of Wesfarmers as a case study, analyzing how the company applies FVA to various non-current assets such as investments, deferred tax assets, property, plant and equipment, goodwill, intangible assets, and derivatives. It highlights the benefits of FVA, including accurate asset valuation and reduced manipulation, while also acknowledging limitations like market fluctuations and investor perceptions. The analysis concludes that FVA provides a more realistic reflection of a company's financial position, advocating for its continued use over HCA to provide investors with reliable financial information. The report emphasizes the importance of choosing the appropriate accounting method for organizational success.

Running head: FOUNDATIONS IN ACCOUNTING

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FOUNDATIONS IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

IFRS Statement of Fair Value Accounting......................................................................................2

Fair Value vs. Historical Cost Accounting......................................................................................3

Benefits and Issues of Fair Value Accounting................................................................................3

Effects on Balance Sheet.................................................................................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

IFRS Statement of Fair Value Accounting......................................................................................2

Fair Value vs. Historical Cost Accounting......................................................................................3

Benefits and Issues of Fair Value Accounting................................................................................3

Effects on Balance Sheet.................................................................................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................9

2FOUNDATIONS IN ACCOUNTING

Introduction

Increasing number of accounting standards all over the world are allowing the standards

of Fair Value Accounting (FVA) for the purpose of financial reporting. The International

Financial Reporting Standard (IFRS) can be considered as one of them allowing FVA for the

accounting treatment of non-current assets of the companies (Graham, Carmichael &

Carmichael, 2012). It needs to be mentioned that IFRS have agreed on the application of FVA

for ascertaining the value of their non-current assets without involving the market value of them

over Historical Cost Accounting (HCA). While the main aim of the development of financial

statements is to reflect the reality of financial situation, variation in the accounting opinion can

be seen under the process of FVA and HCA. The main aim of this report is to ascertain whether

FVA should permanently replace HCA for the valuation of non-current assets. For the purpose of

this report, the 2017 Annual Report of Wesfarners is taken into consideration.

IFRS Statement of Fair Value Accounting

All the details related with the implementation of fair value measurement can be seen in

the IFRS Framework 13 Fair Value Measurement. According to this standard, all the business

entities under Australian Securities Exchange (ASX) need to use fair value measurement for the

measurement of the fair value of all of their assets including non-current assets. According to this

standard, the definition of faire value can be provided based on an ‘exit price’ notion and used

the hierarchy of fair value that results in market based measurement rather than any entity

specific measurement (iasplus.com, 2018). In this aspect, IFRS 5 Non-current Assets Held for

Sale and Discontinued Operation states the process of accounting treatment of non-current

assets. According to this standard, assets held for sales are not depreciable and they are required

Introduction

Increasing number of accounting standards all over the world are allowing the standards

of Fair Value Accounting (FVA) for the purpose of financial reporting. The International

Financial Reporting Standard (IFRS) can be considered as one of them allowing FVA for the

accounting treatment of non-current assets of the companies (Graham, Carmichael &

Carmichael, 2012). It needs to be mentioned that IFRS have agreed on the application of FVA

for ascertaining the value of their non-current assets without involving the market value of them

over Historical Cost Accounting (HCA). While the main aim of the development of financial

statements is to reflect the reality of financial situation, variation in the accounting opinion can

be seen under the process of FVA and HCA. The main aim of this report is to ascertain whether

FVA should permanently replace HCA for the valuation of non-current assets. For the purpose of

this report, the 2017 Annual Report of Wesfarners is taken into consideration.

IFRS Statement of Fair Value Accounting

All the details related with the implementation of fair value measurement can be seen in

the IFRS Framework 13 Fair Value Measurement. According to this standard, all the business

entities under Australian Securities Exchange (ASX) need to use fair value measurement for the

measurement of the fair value of all of their assets including non-current assets. According to this

standard, the definition of faire value can be provided based on an ‘exit price’ notion and used

the hierarchy of fair value that results in market based measurement rather than any entity

specific measurement (iasplus.com, 2018). In this aspect, IFRS 5 Non-current Assets Held for

Sale and Discontinued Operation states the process of accounting treatment of non-current

assets. According to this standard, assets held for sales are not depreciable and they are required

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FOUNDATIONS IN ACCOUNTING

to be valued on the basis of fair value less costs to sell. Moreover, they are required to be

presented separately in the financial statements. In addition, there is a need for separate

disclosure for all these non-current assets (iasplus.com, 2018).

Fair Value vs. Historical Cost Accounting

There are major differences between FVA and HCA. It can be seen that FVA is regarded

as the improvement of HCA as the concept of FVA has been developed to overcome the

drawbacks of HCA (Chircop & Novotny-Farkas, 2016). Under the process of HCA, the initial

price paid at the time of purchasing any asset or liability only matters. The prices of the assets

and the liabilities in the balance sheet cannot include any fluctuations of price. However,

difference can be seen in case of FVA. FVA takes into account all the changes in the value of

assets and liabilities from time to time basis. Thus, it needs to be mentioned that the value of the

assets and liabilities reflect the correct market value under the process of FVA (Ayres, Huang &

Myring, 2017). From the above, it can be seen that the process of FVA takes into account the

volatility in the price of assets and liabilities where HCA does not consider this volatile in price.

This volatility make FVA superior to HCA as it provides the financial results of the companies

that are not based on possible subjective valuation or any other method (Ellul et al., 2015).

Benefits and Issues of Fair Value Accounting

It needs to be mentioned that the process of FVA has some major advantages. At the

same time, there are also some major limitations of FVA. They are discussed below:

Benefits

to be valued on the basis of fair value less costs to sell. Moreover, they are required to be

presented separately in the financial statements. In addition, there is a need for separate

disclosure for all these non-current assets (iasplus.com, 2018).

Fair Value vs. Historical Cost Accounting

There are major differences between FVA and HCA. It can be seen that FVA is regarded

as the improvement of HCA as the concept of FVA has been developed to overcome the

drawbacks of HCA (Chircop & Novotny-Farkas, 2016). Under the process of HCA, the initial

price paid at the time of purchasing any asset or liability only matters. The prices of the assets

and the liabilities in the balance sheet cannot include any fluctuations of price. However,

difference can be seen in case of FVA. FVA takes into account all the changes in the value of

assets and liabilities from time to time basis. Thus, it needs to be mentioned that the value of the

assets and liabilities reflect the correct market value under the process of FVA (Ayres, Huang &

Myring, 2017). From the above, it can be seen that the process of FVA takes into account the

volatility in the price of assets and liabilities where HCA does not consider this volatile in price.

This volatility make FVA superior to HCA as it provides the financial results of the companies

that are not based on possible subjective valuation or any other method (Ellul et al., 2015).

Benefits and Issues of Fair Value Accounting

It needs to be mentioned that the process of FVA has some major advantages. At the

same time, there are also some major limitations of FVA. They are discussed below:

Benefits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FOUNDATIONS IN ACCOUNTING

The use of FVA helps in providing the accurate valuation of the assets and liabilities of

the business organizations. FVA takes into account the increases and decreases in the

value of assets and liabilities. It helps in providing the correct financial position of the

company (Laux, 2016).

Under the process of FVA, there is less possibility of doing manipulation with the

accounting data. Under FVA, the tracking of sales price is done based on the actual or

estimated value that helps in providing the measurement of true income (Zack, 2012).

FVA helps in tracking the value of all types of assets where the valuation of assets and

liabilities is not always correct in case of HCA. For this reason, accountants all over the

world prefer the application of FVA (Wang & Zhang, 2017).

FVA helps the companies by allowing the process of asset reduction within the market.

This particular aspect helps the companies in surviving in difficult economy (Bick,

Orlova & Sun, 2017).

Limitations

Under the process of FVA, large fluctuations in the value of assets can be seen many

time in the year and this changes are required to be recorded in the financial statements.

This particular aspect affects the financial position of the companies (lorian Marcel

Nuţă, 2015).

There are investors for the companies who do not notice that the company is using

FVA. This particular aspects create major dissatisfaction among the investors as they

can only seen the reduction in the net income. It can be considered as another limitation

of FVA (Liao et al., 2013).

The use of FVA helps in providing the accurate valuation of the assets and liabilities of

the business organizations. FVA takes into account the increases and decreases in the

value of assets and liabilities. It helps in providing the correct financial position of the

company (Laux, 2016).

Under the process of FVA, there is less possibility of doing manipulation with the

accounting data. Under FVA, the tracking of sales price is done based on the actual or

estimated value that helps in providing the measurement of true income (Zack, 2012).

FVA helps in tracking the value of all types of assets where the valuation of assets and

liabilities is not always correct in case of HCA. For this reason, accountants all over the

world prefer the application of FVA (Wang & Zhang, 2017).

FVA helps the companies by allowing the process of asset reduction within the market.

This particular aspect helps the companies in surviving in difficult economy (Bick,

Orlova & Sun, 2017).

Limitations

Under the process of FVA, large fluctuations in the value of assets can be seen many

time in the year and this changes are required to be recorded in the financial statements.

This particular aspect affects the financial position of the companies (lorian Marcel

Nuţă, 2015).

There are investors for the companies who do not notice that the company is using

FVA. This particular aspects create major dissatisfaction among the investors as they

can only seen the reduction in the net income. It can be considered as another limitation

of FVA (Liao et al., 2013).

5FOUNDATIONS IN ACCOUNTING

Although it is crucial to consider the present value of the assets and liabilities, it is

necessary to have the historical record for measuring the accuracy. The loss of

historical aspect under FVA can be considered as a major limitation of FVA (Zyla,

2013).

Thus, from the above discussion, it can be seen that FVA has both benefits and limitations

and the accountants are required to consider all of these aspects while using FVA.

Effects on Balance Sheet

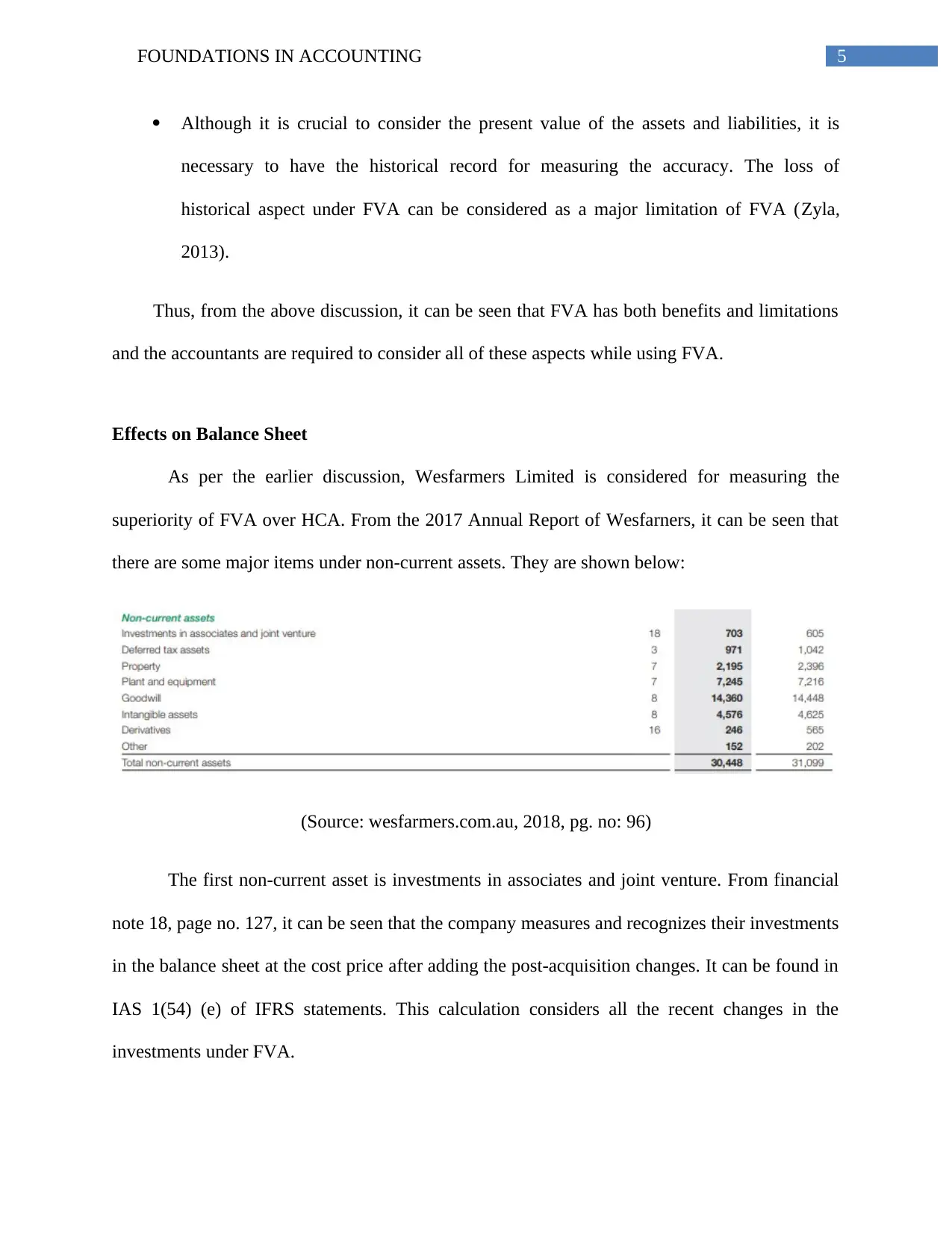

As per the earlier discussion, Wesfarmers Limited is considered for measuring the

superiority of FVA over HCA. From the 2017 Annual Report of Wesfarners, it can be seen that

there are some major items under non-current assets. They are shown below:

(Source: wesfarmers.com.au, 2018, pg. no: 96)

The first non-current asset is investments in associates and joint venture. From financial

note 18, page no. 127, it can be seen that the company measures and recognizes their investments

in the balance sheet at the cost price after adding the post-acquisition changes. It can be found in

IAS 1(54) (e) of IFRS statements. This calculation considers all the recent changes in the

investments under FVA.

Although it is crucial to consider the present value of the assets and liabilities, it is

necessary to have the historical record for measuring the accuracy. The loss of

historical aspect under FVA can be considered as a major limitation of FVA (Zyla,

2013).

Thus, from the above discussion, it can be seen that FVA has both benefits and limitations

and the accountants are required to consider all of these aspects while using FVA.

Effects on Balance Sheet

As per the earlier discussion, Wesfarmers Limited is considered for measuring the

superiority of FVA over HCA. From the 2017 Annual Report of Wesfarners, it can be seen that

there are some major items under non-current assets. They are shown below:

(Source: wesfarmers.com.au, 2018, pg. no: 96)

The first non-current asset is investments in associates and joint venture. From financial

note 18, page no. 127, it can be seen that the company measures and recognizes their investments

in the balance sheet at the cost price after adding the post-acquisition changes. It can be found in

IAS 1(54) (e) of IFRS statements. This calculation considers all the recent changes in the

investments under FVA.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FOUNDATIONS IN ACCOUNTING

The next non-current assets are Deferred Assets. In the calculation of deferred tax assets,

the company follow the IFRS standard of IAS 1 (54) (o), (56). According to this standard, the

recognition of this asset is done in the date of balance sheet. It implies that the company consider

all the changes in the value of deferred tax assets while it would not be possible in case of HCA

(wesfarmers.com.au, pg no: 106).

The next non-current asset is property. According to IFRS IAS 1 (54) (a), while

measuring the cost of plant, Wesfarmers considers all the necessary changes in the value like

depreciation, impairment, cost of replacing parts and others. It implies the adoption of FVA by

the company (wesfarmers.com.au, pg no: 109).

The next non-current asset is Plant and equipment. Same like property, Wesfarmers use

IFRS standard IAS 1 (54) (a) for the valuation of their plant and equipment. In this process, the

company considers all the necessary changes in the value of this asset while reporting them in

the balance sheet. It indicates the adoption of FVA by the company (wesfarmers.com.au, pg no:

109).

The next non-current asset of Wesfarmers is Goodwill. In the financial note no. 8, it is

clearly stated that the company uses FVA for the measurement and reporting of their goodwill.

In this context, the company follows the IFRS principle of IAS 1 (54) (c). It implies that the

company takes into consideration all the current changes in goodwill (wesfarmers.com.au, pg no:

110). The next items are Intangible assets other than Goodwill. It needs to be mentioned that the

company uses the same standard for these assets (wesfarmers.com.au, pg no: 110).

The next non-current asset of the company is Derivatives. As per the financial note no.

16, it can be seen that the company uses fair value method for valuation of their derivatives on

The next non-current assets are Deferred Assets. In the calculation of deferred tax assets,

the company follow the IFRS standard of IAS 1 (54) (o), (56). According to this standard, the

recognition of this asset is done in the date of balance sheet. It implies that the company consider

all the changes in the value of deferred tax assets while it would not be possible in case of HCA

(wesfarmers.com.au, pg no: 106).

The next non-current asset is property. According to IFRS IAS 1 (54) (a), while

measuring the cost of plant, Wesfarmers considers all the necessary changes in the value like

depreciation, impairment, cost of replacing parts and others. It implies the adoption of FVA by

the company (wesfarmers.com.au, pg no: 109).

The next non-current asset is Plant and equipment. Same like property, Wesfarmers use

IFRS standard IAS 1 (54) (a) for the valuation of their plant and equipment. In this process, the

company considers all the necessary changes in the value of this asset while reporting them in

the balance sheet. It indicates the adoption of FVA by the company (wesfarmers.com.au, pg no:

109).

The next non-current asset of Wesfarmers is Goodwill. In the financial note no. 8, it is

clearly stated that the company uses FVA for the measurement and reporting of their goodwill.

In this context, the company follows the IFRS principle of IAS 1 (54) (c). It implies that the

company takes into consideration all the current changes in goodwill (wesfarmers.com.au, pg no:

110). The next items are Intangible assets other than Goodwill. It needs to be mentioned that the

company uses the same standard for these assets (wesfarmers.com.au, pg no: 110).

The next non-current asset of the company is Derivatives. As per the financial note no.

16, it can be seen that the company uses fair value method for valuation of their derivatives on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FOUNDATIONS IN ACCOUNTING

the date of their contracts and the company re-measures them on the basis of fair value. For this

reason, the company follows the standards of IAS 1 (54) (d) and IFRS7 (8) (a). It needs to be

mentioned that the company also use FVA in case of the measurement and valuation of hedging

instruments.

It needs to be mentioned that the values in the amounts of balance sheet have major

impact on the financial position of the business organizations as the investor largely reply on the

figures of balance sheet for determining the credit worthiness of the company (Graham,

Carmichael & Carmichael, 2012). For this reason, the financial statements including balance

sheet need to reflect the actual financial position of the companies. The same aspect is also

applicable for the financial statements of Wesfarmers. The above discussion denotes that the

company has complied with the regulations of IFRS in order to follow the principles of FVA.

However, in case Wesfarmers used HCA, there would be significant difference in the values of

non-current assets. Due to not taking into consideration the recent changes in the values of assets

under HCA, the value of the assets did not express the actual financial position of the company

and it would mislead the investors in the investment decision-making process.

Conclusion

The selection of appropriate accounting method is an important factor for the success of

the whole organization. In this process, business organizations are required to consider both the

advantages and disadvantages of the accounting methods. From the above discussion, it can be

seen that IFRS has provided all the details related to the use of FVA for the ASX listed

companies. According to the above discussion, it can be observed that the process of FVA has

both advantages and disadvantages, but the portion of advantages is more than the portion of

the date of their contracts and the company re-measures them on the basis of fair value. For this

reason, the company follows the standards of IAS 1 (54) (d) and IFRS7 (8) (a). It needs to be

mentioned that the company also use FVA in case of the measurement and valuation of hedging

instruments.

It needs to be mentioned that the values in the amounts of balance sheet have major

impact on the financial position of the business organizations as the investor largely reply on the

figures of balance sheet for determining the credit worthiness of the company (Graham,

Carmichael & Carmichael, 2012). For this reason, the financial statements including balance

sheet need to reflect the actual financial position of the companies. The same aspect is also

applicable for the financial statements of Wesfarmers. The above discussion denotes that the

company has complied with the regulations of IFRS in order to follow the principles of FVA.

However, in case Wesfarmers used HCA, there would be significant difference in the values of

non-current assets. Due to not taking into consideration the recent changes in the values of assets

under HCA, the value of the assets did not express the actual financial position of the company

and it would mislead the investors in the investment decision-making process.

Conclusion

The selection of appropriate accounting method is an important factor for the success of

the whole organization. In this process, business organizations are required to consider both the

advantages and disadvantages of the accounting methods. From the above discussion, it can be

seen that IFRS has provided all the details related to the use of FVA for the ASX listed

companies. According to the above discussion, it can be observed that the process of FVA has

both advantages and disadvantages, but the portion of advantages is more than the portion of

8FOUNDATIONS IN ACCOUNTING

disadvantages as compared to HCA. In case of Wesfarmers, the above discussion indicates that

the company uses FVA method for the valuation and presentation of their non-current assets in

the financial statements. The above discussion shows that in case of the adoption of HC instead

of FVA, there would be major differences in the values of non-current assets; and this would

lead to the miss-presentation of the financial position of Wesfarmers. This whole process would

mislead the investors in determining the actual financial position of the company. Thus, on the

basis of the whole discussion, it can be concluded that FVA should permanently replace FVA as

the accounting process of the companies.

disadvantages as compared to HCA. In case of Wesfarmers, the above discussion indicates that

the company uses FVA method for the valuation and presentation of their non-current assets in

the financial statements. The above discussion shows that in case of the adoption of HC instead

of FVA, there would be major differences in the values of non-current assets; and this would

lead to the miss-presentation of the financial position of Wesfarmers. This whole process would

mislead the investors in determining the actual financial position of the company. Thus, on the

basis of the whole discussion, it can be concluded that FVA should permanently replace FVA as

the accounting process of the companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FOUNDATIONS IN ACCOUNTING

References

2017 Annual Report. (2018). Wesfarmers.com.au. Retrieved 27 March 2018, from

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Ayres, Huang, & Myring. (2017). Fair value accounting and analyst forecast accuracy. Advances

in Accounting, 37, 58-70.

Bick, Orlova, & Sun. (2017). Fair value accounting and corporate cash holdings. Advances in

Accounting, Advances in Accounting.

Chircop, & Novotny-Farkas. (2016). The economic consequences of extending the use of fair

value accounting in regulatory capital calculations. Journal of Accounting and

Economics, 62(2-3), 183-203.

Ellul, A., Jotikasthira, C., Lundblad, C., & Wang, Y. (2015). Is Historical Cost Accounting a

Panacea? Market Stress, Incentive Distortions, and Gains Trading. Journal of

Finance, 70(6), 2489-2538.

Graham, Carmichael, & Carmichael, D. R. (2012). Financial accounting and general

topics (12th ed., Accountants' handbook ; v. 1). Hoboken, N.J.: John Wiley & Sons.

IFRS 13 — Fair Value Measurement. (2018). Iasplus.com. Retrieved 27 March 2018, from

https://www.iasplus.com/en/standards/ifrs/if

IFRS 5 — Non-current Assets Held for Sale and Discontinued Operations. (2018). Iasplus.com.

Retrieved 27 March 2018, from https://www.iasplus.com/en/standards/ifrs/if

References

2017 Annual Report. (2018). Wesfarmers.com.au. Retrieved 27 March 2018, from

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Ayres, Huang, & Myring. (2017). Fair value accounting and analyst forecast accuracy. Advances

in Accounting, 37, 58-70.

Bick, Orlova, & Sun. (2017). Fair value accounting and corporate cash holdings. Advances in

Accounting, Advances in Accounting.

Chircop, & Novotny-Farkas. (2016). The economic consequences of extending the use of fair

value accounting in regulatory capital calculations. Journal of Accounting and

Economics, 62(2-3), 183-203.

Ellul, A., Jotikasthira, C., Lundblad, C., & Wang, Y. (2015). Is Historical Cost Accounting a

Panacea? Market Stress, Incentive Distortions, and Gains Trading. Journal of

Finance, 70(6), 2489-2538.

Graham, Carmichael, & Carmichael, D. R. (2012). Financial accounting and general

topics (12th ed., Accountants' handbook ; v. 1). Hoboken, N.J.: John Wiley & Sons.

IFRS 13 — Fair Value Measurement. (2018). Iasplus.com. Retrieved 27 March 2018, from

https://www.iasplus.com/en/standards/ifrs/if

IFRS 5 — Non-current Assets Held for Sale and Discontinued Operations. (2018). Iasplus.com.

Retrieved 27 March 2018, from https://www.iasplus.com/en/standards/ifrs/if

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FOUNDATIONS IN ACCOUNTING

Laux, C. (2016). The economic consequences of extending the use of fair value accounting in

regulatory capital calculations: A discussion. Journal of Accounting and

Economics, 62(2-3), 204-208.

Liao, Kang, Morris, & Tang. (2013). Information asymmetry of fair value accounting during the

financial crisis. Journal of Contemporary Accounting & Economics, 9(2), 221-23

lorian Marcel Nuţă. (2015). FAIR VALUE ACCOUNTING CRISIS DEBATE – A

REVIEW. Analele Universităţii Constantin Brâncuşi Din Târgu Jiu : Seria

Economie, 2(1), 136-139

Wang, & Zhang. (2017). Fair value accounting and corporate debt structure. Advances in

Accounting, 37, 46-57.

Zack, G. (2012). Fair Value Accounting. In Financial Statement Fraud (pp. 117-128). Hoboken,

NJ, USA: John Wiley & Sons.

Zyla, M. (2013). Fair value measurement practical guidance and implementation (2nd ed.,

Wiley Corporate F&A). Hoboken, N.J.: Wiley.

Laux, C. (2016). The economic consequences of extending the use of fair value accounting in

regulatory capital calculations: A discussion. Journal of Accounting and

Economics, 62(2-3), 204-208.

Liao, Kang, Morris, & Tang. (2013). Information asymmetry of fair value accounting during the

financial crisis. Journal of Contemporary Accounting & Economics, 9(2), 221-23

lorian Marcel Nuţă. (2015). FAIR VALUE ACCOUNTING CRISIS DEBATE – A

REVIEW. Analele Universităţii Constantin Brâncuşi Din Târgu Jiu : Seria

Economie, 2(1), 136-139

Wang, & Zhang. (2017). Fair value accounting and corporate debt structure. Advances in

Accounting, 37, 46-57.

Zack, G. (2012). Fair Value Accounting. In Financial Statement Fraud (pp. 117-128). Hoboken,

NJ, USA: John Wiley & Sons.

Zyla, M. (2013). Fair value measurement practical guidance and implementation (2nd ed.,

Wiley Corporate F&A). Hoboken, N.J.: Wiley.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.