Fairfax Media Ltd: Provisions, Contingencies, Leases & Asset Valuation

VerifiedAdded on 2023/06/12

|10

|2010

|446

Essay

AI Summary

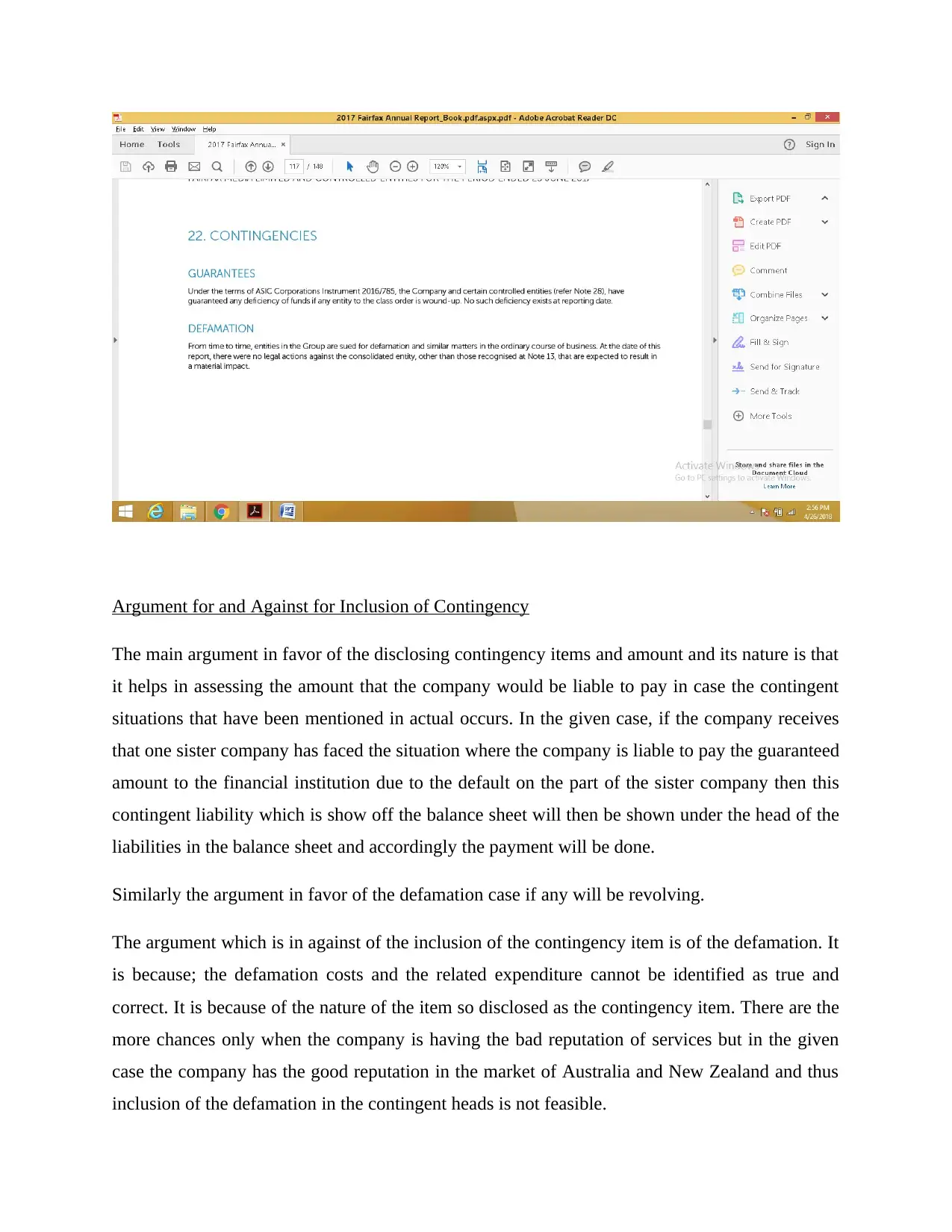

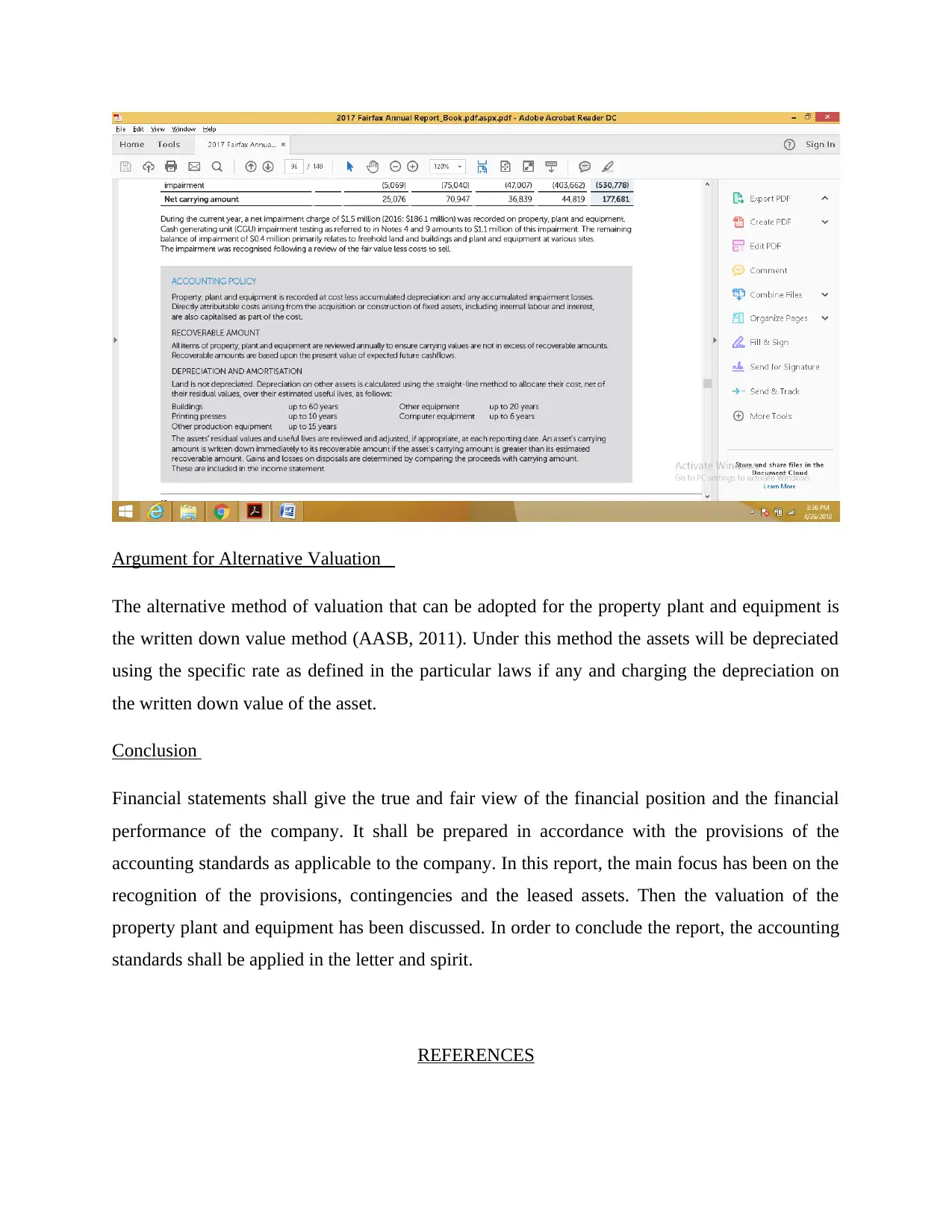

This essay provides a detailed analysis of Fairfax Media Limited's financial reporting practices, focusing on provisions, contingencies, leased items, and the valuation of non-current assets, based on their 2017 annual report. It examines the recognition criteria and measurement issues associated with provisions and contingencies, specifically discussing employee benefits, restructuring, property-related provisions, and potential defamation claims. The essay also argues for and against the inclusion of contingency items in financial reports. Furthermore, it explores the classification and presentation of leased items, considering potential reclassifications under new accounting standards. Finally, the report evaluates the valuation method used for property, plant, and equipment, suggesting an alternative approach and concluding with the importance of adhering to accounting standards for accurate financial representation. Desklib offers this and other solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.