Report: Costing Analysis of Fantori Ltd (ACC200, Term 3 2018)

VerifiedAdded on 2023/04/24

|15

|2322

|142

Report

AI Summary

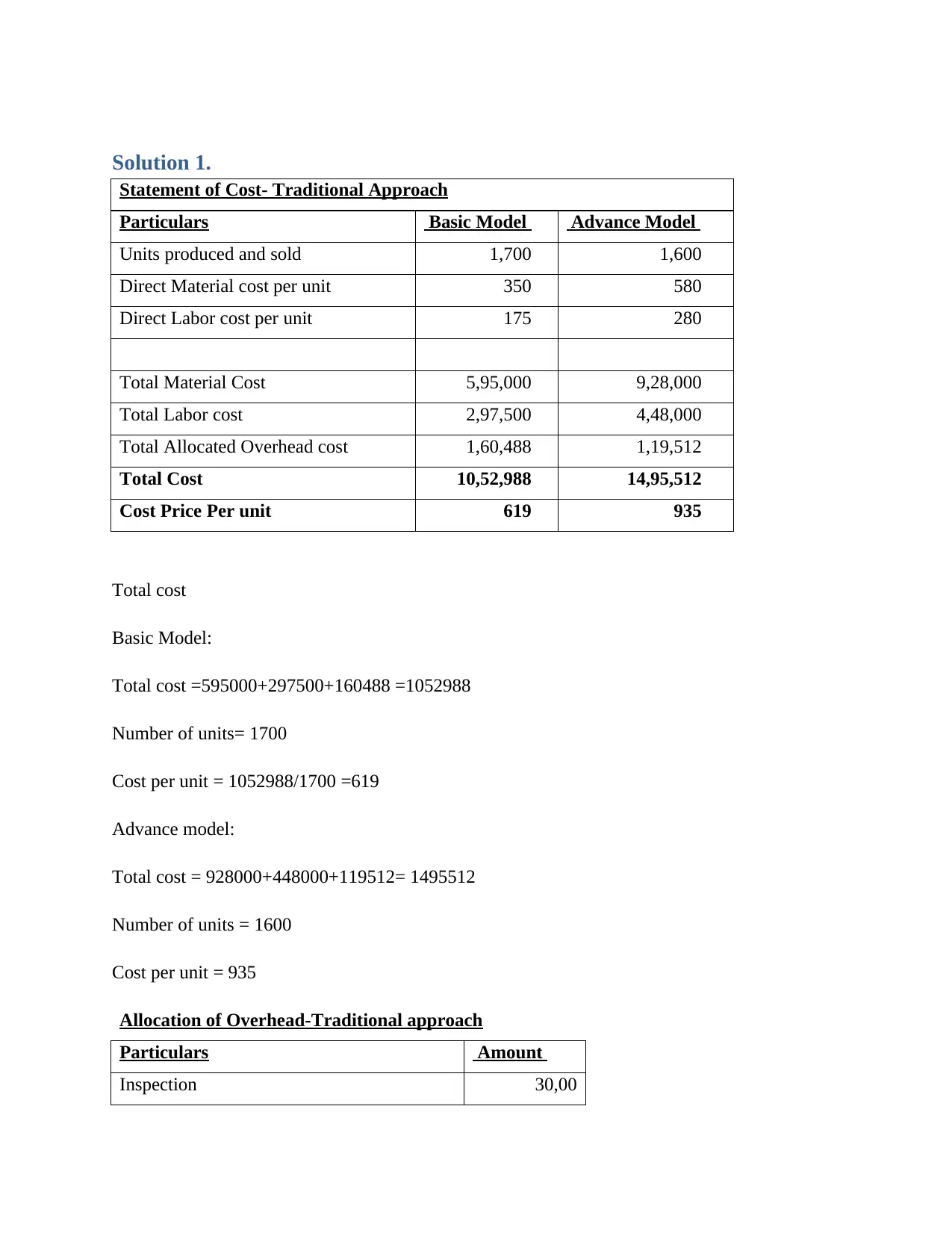

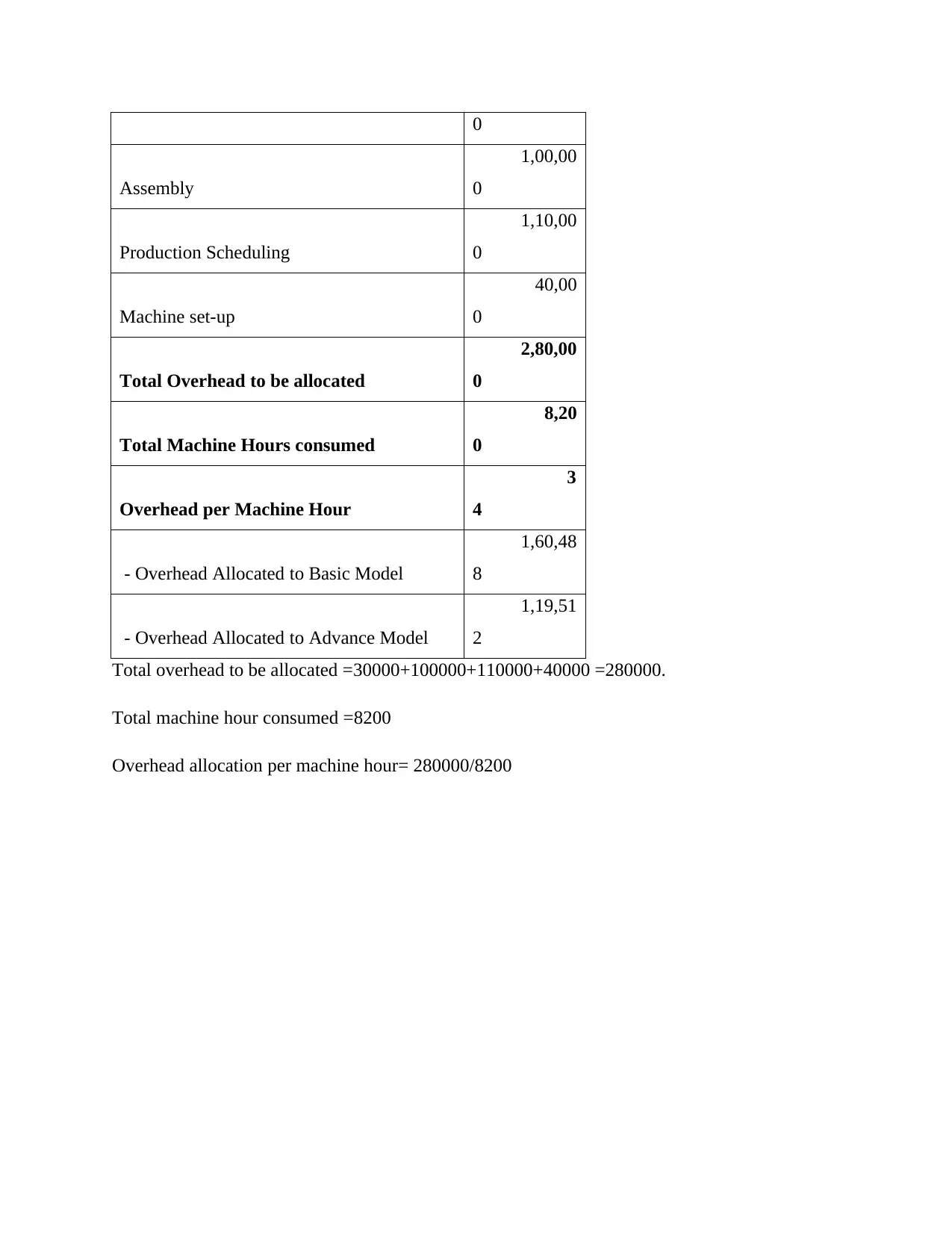

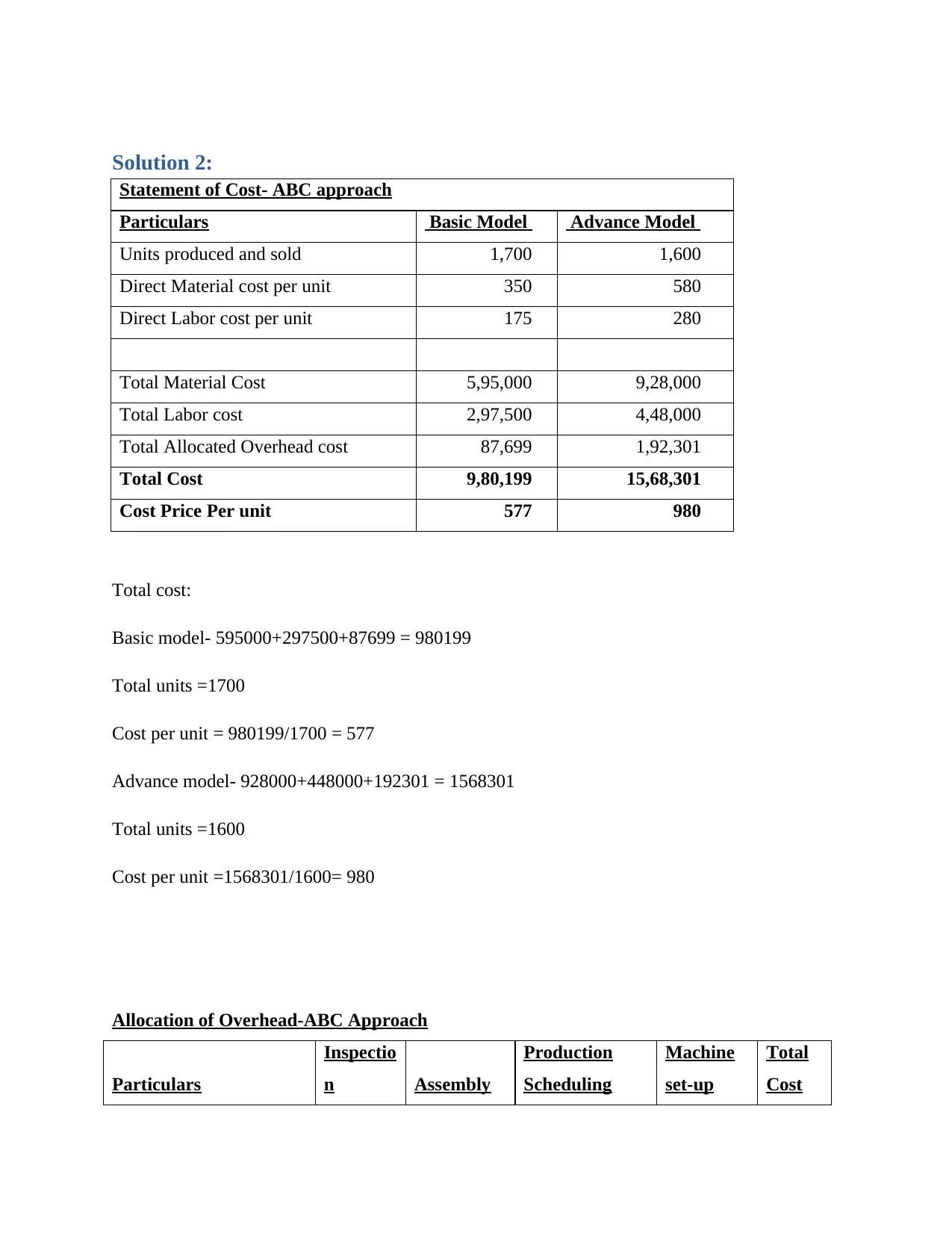

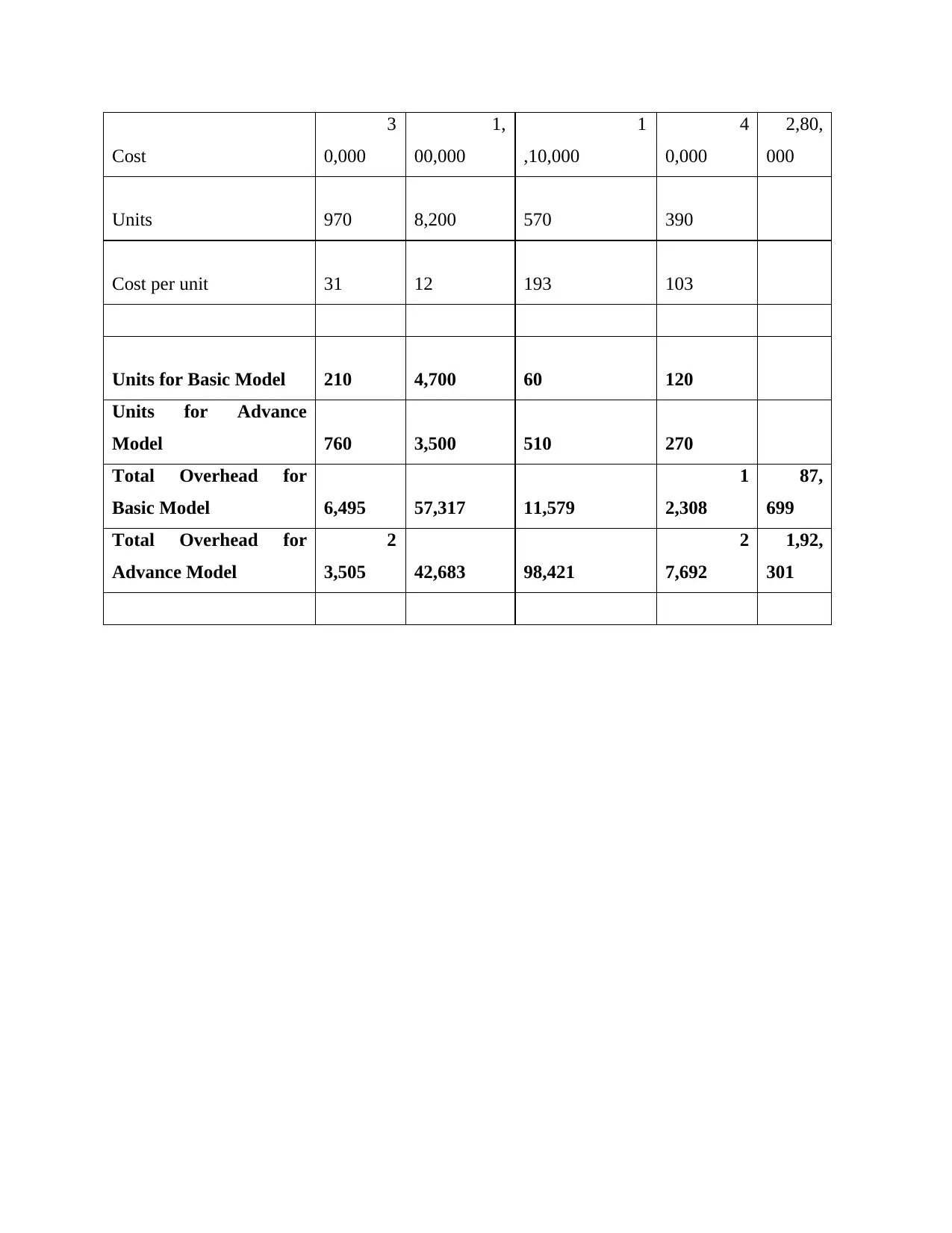

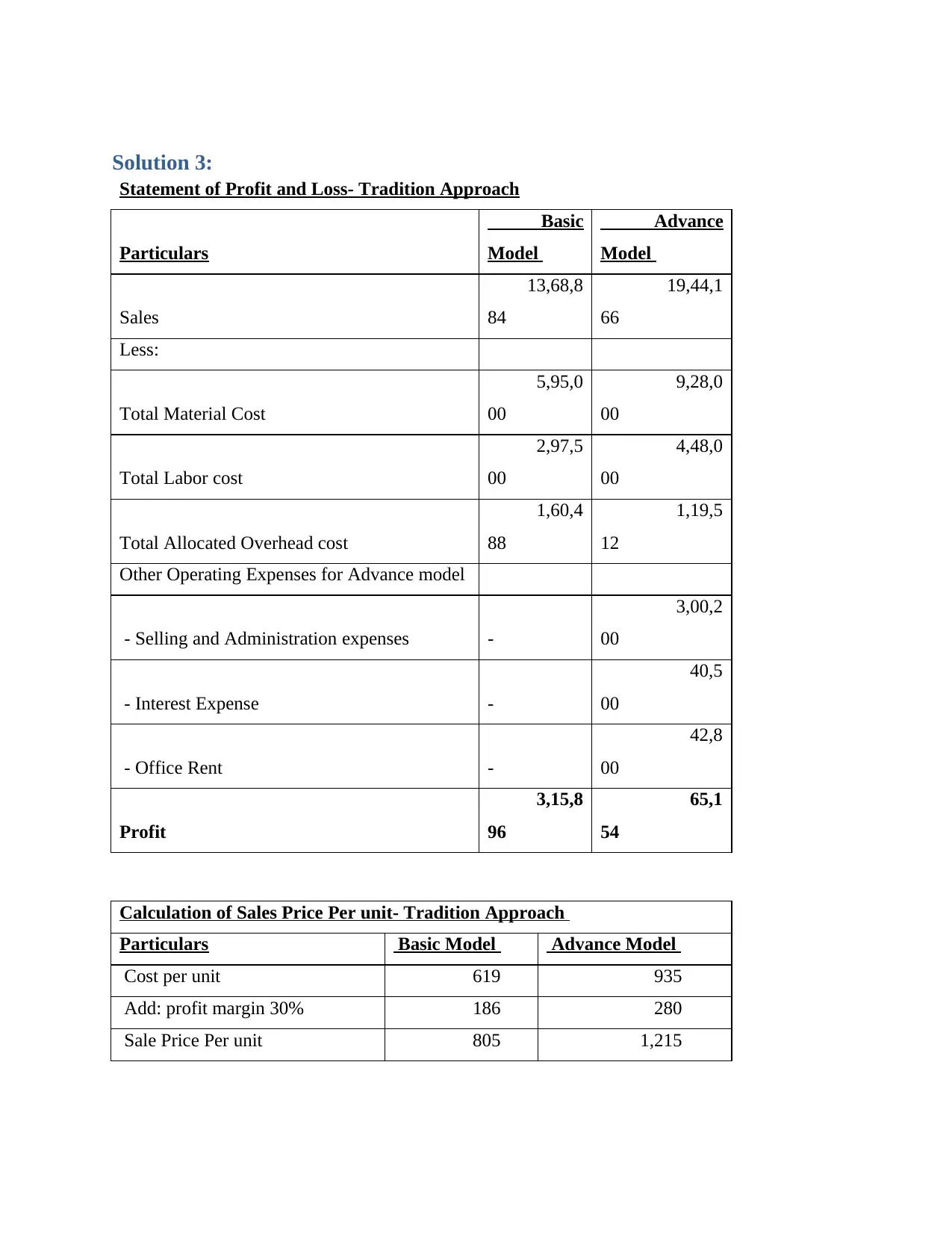

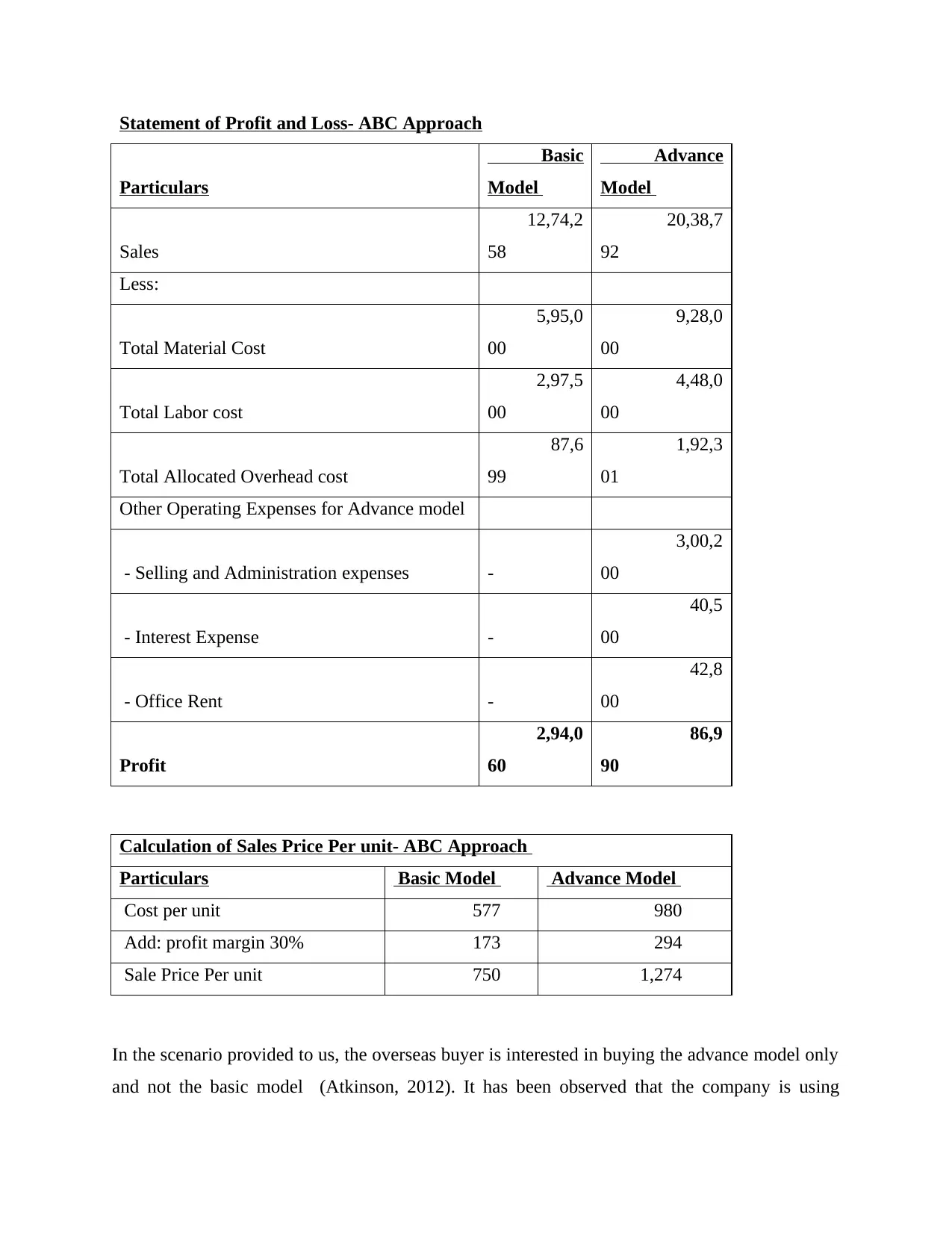

This report analyzes Fantori Ltd, a sewing machine manufacturer, focusing on its costing methods and the behavior of an overseas buyer. The company currently uses traditional costing, allocating overhead based on machine hours. The report compares this approach to activity-based costing (ABC), demonstrating how different costing methods impact product pricing and profitability. It explores the reasons why the overseas buyer is only interested in the advanced model and not the basic model, suggesting that the traditional costing method may be distorting the perceived costs of the products. The report includes calculations of costs using both traditional and ABC methods, analyzes the impact of under-applied overhead, and provides insights into how Fantori Ltd can improve its costing practices to make informed business decisions, especially regarding pricing and sales strategies. The report also includes statements of profit and loss under both costing methods, calculation of sales prices per unit, and an explanation of overhead expenses and their allocation, along with treatments for under-applied overhead. Finally, the report concludes with a practical example of under-absorption and the various methods to treat it.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.