Costing System Analysis: Fantori Limited's Decision-Making Process

VerifiedAdded on 2023/04/23

|6

|2518

|285

Case Study

AI Summary

This case study examines Fantori Limited, a sewing machine manufacturer, and its decision to evaluate its costing system. The company currently uses traditional absorption costing but is considering implementing activity-based costing (ABC). The analysis compares the two methods, calculating overhead allocation, cost per unit for both basic and advanced models, and overall profitability. The traditional method allocates overhead based on machine hours, while ABC uses multiple cost drivers based on activities like inspection, assembly, and scheduling. The study reveals that ABC provides a more accurate cost picture, impacting the profitability analysis and explaining the foreign buyer's preference for advanced models. The case highlights the importance of accurate costing for optimal pricing, decision-making, and business growth, demonstrating how traditional costing can distort profit margins and lead to incorrect business decisions. Finally, the assignment explores the impact of markup on pricing and the ultimate profit realized under each costing system, emphasizing the benefits of ABC in this scenario.

Case Analysis of Fantori Limited

Introduction

Fantori Limited is a well reputed company engaged in the business of manufacturing sewing

machines. The company manufactures two models of sewing machine at present and sells them to

external parties. The two models of sewing machines are basic model and advanced model (with

some additional features). In year 2017, the company made handsome profits and the business was

running quite well. The company has just entered into an unchartered territory whereby they have

procured order from a foreign buyer who wishes to procure only Advance grade sewing machine of

the company. This has put the company under a doubt why there has been no order for basic grade

and needs to revisit its costing system. Under the present circumstance, the company use traditional

method of costing i.e. absorption costing and uses Machine hours as the basis of allocation of fixed

overheads to the product. However, the company is considering to implement Activity Based Costing

and find the rationale for demand of only Advance sewing machines. In this regard , company ha

sought a detailed analysis of Traditional Costing Method vis-a vis Modern costing system and the

impact on the profits under both the methods.

Traditional Costing System V/s Modern Costing System

Traditional Costing system is an old concept and usually used for small enterprises. Under the said

method, the indirect cost of production is allocated on the basis of a fixed rate derived on the basis

of direct labour hours, machine hours etc. It does not map the correct allocation of cost to products.

To overcome this shortfall, a new method of costing was devised which was intended to generate

and map the indirect cost on various parameters known as pools. Thus, under the said method

correct or true cost of production is derived.

Further, the importance of accurate costing has been enumerated here-in-below:

(a) It helps businesses in making optimal decisions;

(b) It enables correct mark up on products;

(c) Wrong cost estimates may lead to business losses. Thus, correct costing enables guided decision

on product profitability;

(d) It helps in making decisions regarding which product shall be promoted by the company to

maximise its profits;

(e) It helps business to stay on schedule and track

(f) Healthy growth of business;

(g) Cost controlling.

Case Analysis

Costing under Traditional Method of Costing

In the present case, the company manufactures two grade of sewing machine namely Basic Grade

and Advanced Grade. Under the Basic Grade model, the Company incurs a direct material cost of $

350 and the direct labour cost of $ 175. Further, the machine hours involved in manufacturing of the

said product is 4700 Hours. In addition, the total number of units manufactured by the company is

1700 units.

Under the Advanced Grade model, the Company incurs a direct material cost of $ 580 and the direct

labour cost of $ 280. Further, the machine hours involved in manufacturing of the said product is

3500 Hours. In addition, the total number of units manufactured by the company is 1600 units.

Introduction

Fantori Limited is a well reputed company engaged in the business of manufacturing sewing

machines. The company manufactures two models of sewing machine at present and sells them to

external parties. The two models of sewing machines are basic model and advanced model (with

some additional features). In year 2017, the company made handsome profits and the business was

running quite well. The company has just entered into an unchartered territory whereby they have

procured order from a foreign buyer who wishes to procure only Advance grade sewing machine of

the company. This has put the company under a doubt why there has been no order for basic grade

and needs to revisit its costing system. Under the present circumstance, the company use traditional

method of costing i.e. absorption costing and uses Machine hours as the basis of allocation of fixed

overheads to the product. However, the company is considering to implement Activity Based Costing

and find the rationale for demand of only Advance sewing machines. In this regard , company ha

sought a detailed analysis of Traditional Costing Method vis-a vis Modern costing system and the

impact on the profits under both the methods.

Traditional Costing System V/s Modern Costing System

Traditional Costing system is an old concept and usually used for small enterprises. Under the said

method, the indirect cost of production is allocated on the basis of a fixed rate derived on the basis

of direct labour hours, machine hours etc. It does not map the correct allocation of cost to products.

To overcome this shortfall, a new method of costing was devised which was intended to generate

and map the indirect cost on various parameters known as pools. Thus, under the said method

correct or true cost of production is derived.

Further, the importance of accurate costing has been enumerated here-in-below:

(a) It helps businesses in making optimal decisions;

(b) It enables correct mark up on products;

(c) Wrong cost estimates may lead to business losses. Thus, correct costing enables guided decision

on product profitability;

(d) It helps in making decisions regarding which product shall be promoted by the company to

maximise its profits;

(e) It helps business to stay on schedule and track

(f) Healthy growth of business;

(g) Cost controlling.

Case Analysis

Costing under Traditional Method of Costing

In the present case, the company manufactures two grade of sewing machine namely Basic Grade

and Advanced Grade. Under the Basic Grade model, the Company incurs a direct material cost of $

350 and the direct labour cost of $ 175. Further, the machine hours involved in manufacturing of the

said product is 4700 Hours. In addition, the total number of units manufactured by the company is

1700 units.

Under the Advanced Grade model, the Company incurs a direct material cost of $ 580 and the direct

labour cost of $ 280. Further, the machine hours involved in manufacturing of the said product is

3500 Hours. In addition, the total number of units manufactured by the company is 1600 units.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

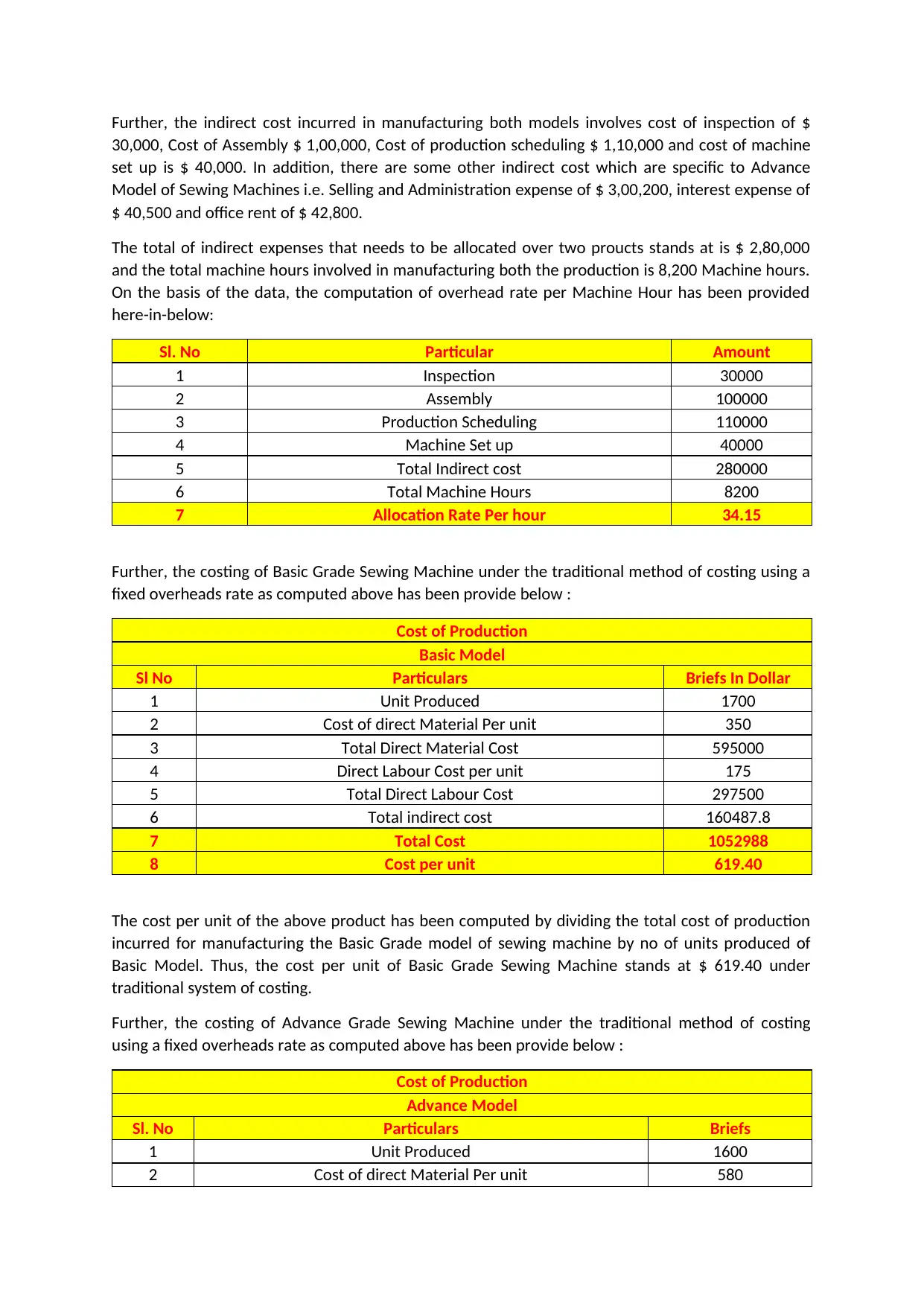

Further, the indirect cost incurred in manufacturing both models involves cost of inspection of $

30,000, Cost of Assembly $ 1,00,000, Cost of production scheduling $ 1,10,000 and cost of machine

set up is $ 40,000. In addition, there are some other indirect cost which are specific to Advance

Model of Sewing Machines i.e. Selling and Administration expense of $ 3,00,200, interest expense of

$ 40,500 and office rent of $ 42,800.

The total of indirect expenses that needs to be allocated over two proucts stands at is $ 2,80,000

and the total machine hours involved in manufacturing both the production is 8,200 Machine hours.

On the basis of the data, the computation of overhead rate per Machine Hour has been provided

here-in-below:

Sl. No Particular Amount

1 Inspection 30000

2 Assembly 100000

3 Production Scheduling 110000

4 Machine Set up 40000

5 Total Indirect cost 280000

6 Total Machine Hours 8200

7 Allocation Rate Per hour 34.15

Further, the costing of Basic Grade Sewing Machine under the traditional method of costing using a

fixed overheads rate as computed above has been provide below :

Cost of Production

Basic Model

Sl No Particulars Briefs In Dollar

1 Unit Produced 1700

2 Cost of direct Material Per unit 350

3 Total Direct Material Cost 595000

4 Direct Labour Cost per unit 175

5 Total Direct Labour Cost 297500

6 Total indirect cost 160487.8

7 Total Cost 1052988

8 Cost per unit 619.40

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Basic Grade model of sewing machine by no of units produced of

Basic Model. Thus, the cost per unit of Basic Grade Sewing Machine stands at $ 619.40 under

traditional system of costing.

Further, the costing of Advance Grade Sewing Machine under the traditional method of costing

using a fixed overheads rate as computed above has been provide below :

Cost of Production

Advance Model

Sl. No Particulars Briefs

1 Unit Produced 1600

2 Cost of direct Material Per unit 580

30,000, Cost of Assembly $ 1,00,000, Cost of production scheduling $ 1,10,000 and cost of machine

set up is $ 40,000. In addition, there are some other indirect cost which are specific to Advance

Model of Sewing Machines i.e. Selling and Administration expense of $ 3,00,200, interest expense of

$ 40,500 and office rent of $ 42,800.

The total of indirect expenses that needs to be allocated over two proucts stands at is $ 2,80,000

and the total machine hours involved in manufacturing both the production is 8,200 Machine hours.

On the basis of the data, the computation of overhead rate per Machine Hour has been provided

here-in-below:

Sl. No Particular Amount

1 Inspection 30000

2 Assembly 100000

3 Production Scheduling 110000

4 Machine Set up 40000

5 Total Indirect cost 280000

6 Total Machine Hours 8200

7 Allocation Rate Per hour 34.15

Further, the costing of Basic Grade Sewing Machine under the traditional method of costing using a

fixed overheads rate as computed above has been provide below :

Cost of Production

Basic Model

Sl No Particulars Briefs In Dollar

1 Unit Produced 1700

2 Cost of direct Material Per unit 350

3 Total Direct Material Cost 595000

4 Direct Labour Cost per unit 175

5 Total Direct Labour Cost 297500

6 Total indirect cost 160487.8

7 Total Cost 1052988

8 Cost per unit 619.40

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Basic Grade model of sewing machine by no of units produced of

Basic Model. Thus, the cost per unit of Basic Grade Sewing Machine stands at $ 619.40 under

traditional system of costing.

Further, the costing of Advance Grade Sewing Machine under the traditional method of costing

using a fixed overheads rate as computed above has been provide below :

Cost of Production

Advance Model

Sl. No Particulars Briefs

1 Unit Produced 1600

2 Cost of direct Material Per unit 580

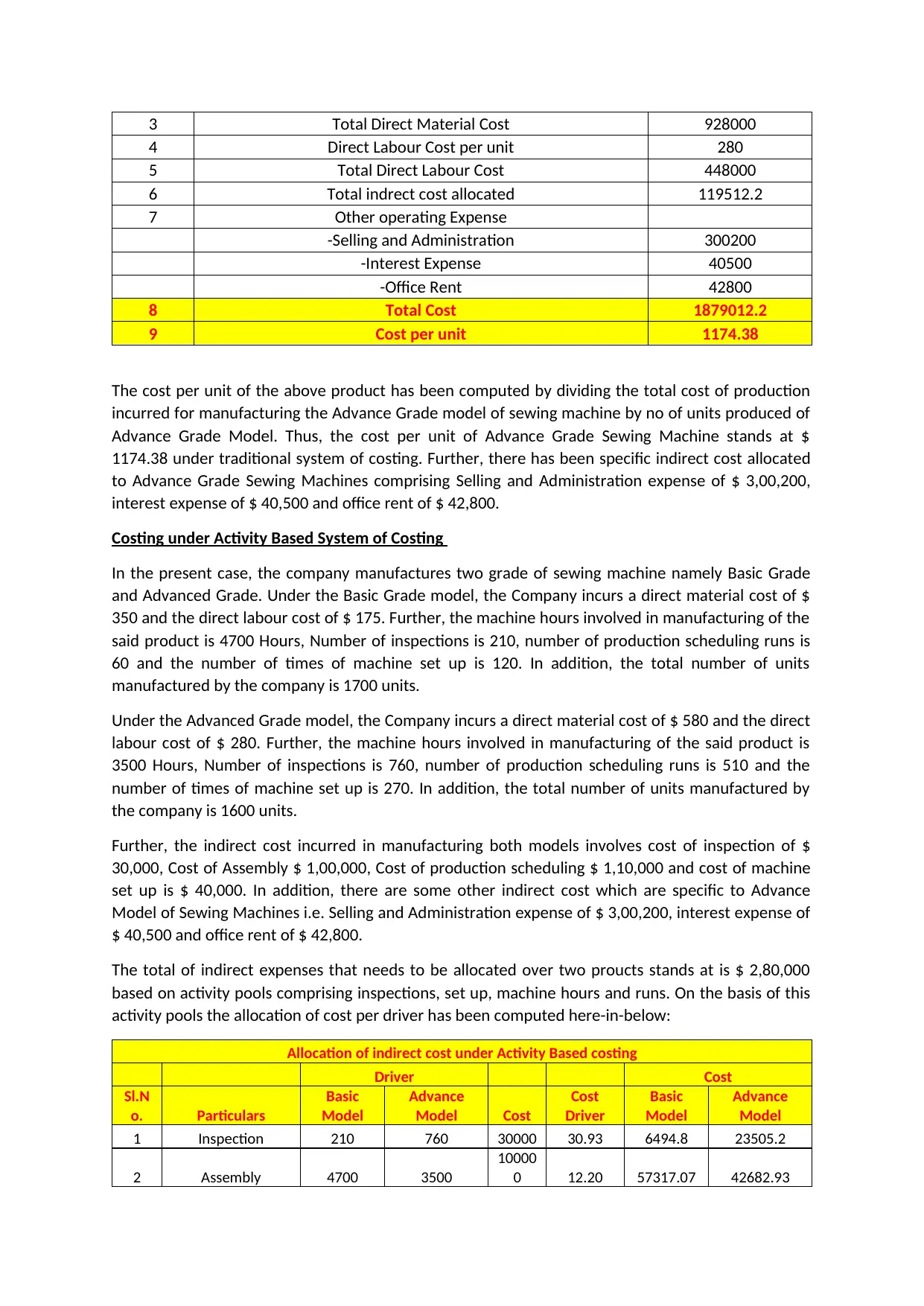

3 Total Direct Material Cost 928000

4 Direct Labour Cost per unit 280

5 Total Direct Labour Cost 448000

6 Total indrect cost allocated 119512.2

7 Other operating Expense

-Selling and Administration 300200

-Interest Expense 40500

-Office Rent 42800

8 Total Cost 1879012.2

9 Cost per unit 1174.38

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Advance Grade model of sewing machine by no of units produced of

Advance Grade Model. Thus, the cost per unit of Advance Grade Sewing Machine stands at $

1174.38 under traditional system of costing. Further, there has been specific indirect cost allocated

to Advance Grade Sewing Machines comprising Selling and Administration expense of $ 3,00,200,

interest expense of $ 40,500 and office rent of $ 42,800.

Costing under Activity Based System of Costing

In the present case, the company manufactures two grade of sewing machine namely Basic Grade

and Advanced Grade. Under the Basic Grade model, the Company incurs a direct material cost of $

350 and the direct labour cost of $ 175. Further, the machine hours involved in manufacturing of the

said product is 4700 Hours, Number of inspections is 210, number of production scheduling runs is

60 and the number of times of machine set up is 120. In addition, the total number of units

manufactured by the company is 1700 units.

Under the Advanced Grade model, the Company incurs a direct material cost of $ 580 and the direct

labour cost of $ 280. Further, the machine hours involved in manufacturing of the said product is

3500 Hours, Number of inspections is 760, number of production scheduling runs is 510 and the

number of times of machine set up is 270. In addition, the total number of units manufactured by

the company is 1600 units.

Further, the indirect cost incurred in manufacturing both models involves cost of inspection of $

30,000, Cost of Assembly $ 1,00,000, Cost of production scheduling $ 1,10,000 and cost of machine

set up is $ 40,000. In addition, there are some other indirect cost which are specific to Advance

Model of Sewing Machines i.e. Selling and Administration expense of $ 3,00,200, interest expense of

$ 40,500 and office rent of $ 42,800.

The total of indirect expenses that needs to be allocated over two proucts stands at is $ 2,80,000

based on activity pools comprising inspections, set up, machine hours and runs. On the basis of this

activity pools the allocation of cost per driver has been computed here-in-below:

Allocation of indirect cost under Activity Based costing

Driver Cost

Sl.N

o. Particulars

Basic

Model

Advance

Model Cost

Cost

Driver

Basic

Model

Advance

Model

1 Inspection 210 760 30000 30.93 6494.8 23505.2

2 Assembly 4700 3500

10000

0 12.20 57317.07 42682.93

4 Direct Labour Cost per unit 280

5 Total Direct Labour Cost 448000

6 Total indrect cost allocated 119512.2

7 Other operating Expense

-Selling and Administration 300200

-Interest Expense 40500

-Office Rent 42800

8 Total Cost 1879012.2

9 Cost per unit 1174.38

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Advance Grade model of sewing machine by no of units produced of

Advance Grade Model. Thus, the cost per unit of Advance Grade Sewing Machine stands at $

1174.38 under traditional system of costing. Further, there has been specific indirect cost allocated

to Advance Grade Sewing Machines comprising Selling and Administration expense of $ 3,00,200,

interest expense of $ 40,500 and office rent of $ 42,800.

Costing under Activity Based System of Costing

In the present case, the company manufactures two grade of sewing machine namely Basic Grade

and Advanced Grade. Under the Basic Grade model, the Company incurs a direct material cost of $

350 and the direct labour cost of $ 175. Further, the machine hours involved in manufacturing of the

said product is 4700 Hours, Number of inspections is 210, number of production scheduling runs is

60 and the number of times of machine set up is 120. In addition, the total number of units

manufactured by the company is 1700 units.

Under the Advanced Grade model, the Company incurs a direct material cost of $ 580 and the direct

labour cost of $ 280. Further, the machine hours involved in manufacturing of the said product is

3500 Hours, Number of inspections is 760, number of production scheduling runs is 510 and the

number of times of machine set up is 270. In addition, the total number of units manufactured by

the company is 1600 units.

Further, the indirect cost incurred in manufacturing both models involves cost of inspection of $

30,000, Cost of Assembly $ 1,00,000, Cost of production scheduling $ 1,10,000 and cost of machine

set up is $ 40,000. In addition, there are some other indirect cost which are specific to Advance

Model of Sewing Machines i.e. Selling and Administration expense of $ 3,00,200, interest expense of

$ 40,500 and office rent of $ 42,800.

The total of indirect expenses that needs to be allocated over two proucts stands at is $ 2,80,000

based on activity pools comprising inspections, set up, machine hours and runs. On the basis of this

activity pools the allocation of cost per driver has been computed here-in-below:

Allocation of indirect cost under Activity Based costing

Driver Cost

Sl.N

o. Particulars

Basic

Model

Advance

Model Cost

Cost

Driver

Basic

Model

Advance

Model

1 Inspection 210 760 30000 30.93 6494.8 23505.2

2 Assembly 4700 3500

10000

0 12.20 57317.07 42682.93

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Production

Scheduling 60 510

11000

0 192.98 11578.9 98421.1

4 Machine Set up 120 270 40000 102.56 12307.69 27692.31

Total Indirect Cost allocation 87698.56 192301.44

Under the above table, the inspection cost has been allocated on the basis of number of inspections

carried out for both the grade which is 210 for Basic Grade Sewing Machine and 760 for advanced

grade sewing machines.

The cost of Assembly has been allocated on the basis of Machine Hours involved for manufacturing

of both the grade which is 4700 hours for Basic Model Grade and 3700 Hours for Advance Model

Grade.

The cost of production scheduling has been allocated on the basis of runs involved for

manufacturing of both the grade which is 60 runs for Basic Model Grade and 510 runs for Advanced

Model Grade.

The cost of Machine Set up has been allocated on the basis of set up involved for manufacturing of

both the grade which is 120 Machine set ups for Basic Model Grade and 270 Machine set ups for

Advanced Model Grade.

Further, the costing of Basic Grade Sewing Machine under the Modern costing system method of

costing using a pool of cost drivers as computed above has been provide below :

Cost of Production

Basic Model

Sl No Particulars Briefs

1 Unit Produced 1700

2 Cost of direct Material Per unit 350

3 Total Direct Material Cost 595000

4 Direct Labour Cost per unit 175

5 Total Direct Labour Cost 297500

6 Total indirect cost 87698.6

7 Total Cost 980198.6

8 Cost per unit 576.59

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Basic Grade model of sewing machine by no of units produced of

Basic Model. Thus, the cost per unit of Basic Grade Sewing Machine stands at $ 576.59 under Activity

Based system of costing. The cost has decreased by $ 42.82 per unit of Basic Grade Sewing Machine.

Further, the costing of Advanced Grade Sewing Machine under the Modern costing system method

of costing using a pool of cost drivers as computed above has been provide below :

Cost of Production

Advance Model

Sl No Particulars Briefs

1 Unit Produced 1600

2 Cost of direct Material Per unit 580

Production

Scheduling 60 510

11000

0 192.98 11578.9 98421.1

4 Machine Set up 120 270 40000 102.56 12307.69 27692.31

Total Indirect Cost allocation 87698.56 192301.44

Under the above table, the inspection cost has been allocated on the basis of number of inspections

carried out for both the grade which is 210 for Basic Grade Sewing Machine and 760 for advanced

grade sewing machines.

The cost of Assembly has been allocated on the basis of Machine Hours involved for manufacturing

of both the grade which is 4700 hours for Basic Model Grade and 3700 Hours for Advance Model

Grade.

The cost of production scheduling has been allocated on the basis of runs involved for

manufacturing of both the grade which is 60 runs for Basic Model Grade and 510 runs for Advanced

Model Grade.

The cost of Machine Set up has been allocated on the basis of set up involved for manufacturing of

both the grade which is 120 Machine set ups for Basic Model Grade and 270 Machine set ups for

Advanced Model Grade.

Further, the costing of Basic Grade Sewing Machine under the Modern costing system method of

costing using a pool of cost drivers as computed above has been provide below :

Cost of Production

Basic Model

Sl No Particulars Briefs

1 Unit Produced 1700

2 Cost of direct Material Per unit 350

3 Total Direct Material Cost 595000

4 Direct Labour Cost per unit 175

5 Total Direct Labour Cost 297500

6 Total indirect cost 87698.6

7 Total Cost 980198.6

8 Cost per unit 576.59

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Basic Grade model of sewing machine by no of units produced of

Basic Model. Thus, the cost per unit of Basic Grade Sewing Machine stands at $ 576.59 under Activity

Based system of costing. The cost has decreased by $ 42.82 per unit of Basic Grade Sewing Machine.

Further, the costing of Advanced Grade Sewing Machine under the Modern costing system method

of costing using a pool of cost drivers as computed above has been provide below :

Cost of Production

Advance Model

Sl No Particulars Briefs

1 Unit Produced 1600

2 Cost of direct Material Per unit 580

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 Total Direct Material Cost 928000

4 Direct Labour Cost per unit 280

5 Total Direct Labour Cost 448000

6 Total indirect cost allocated 192301.4

7 Other operating Expense

-Selling and Administration 300200

-Interest Expense 40500

-Office Rent 42800

8 Total Cost 1951801.4

9 Cost per unit 1219.88

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Advanced Grade model of sewing machine by no of units produced

of Advance Model. Thus, the cost per unit of Advance Grade Sewing Machine stands at $ 1219.88

under Activity Based system of costing. The cost has decreased by $ 45.19 per unit of Advance Grade

Sewing Machine.

Profitability under Traditional System of Costing Vis-a Vis- Modern System of Costing

Under the present case, it has been established that the sales price of the Advance Grade Sewing

Machine has been quoted at 30 % markup of cost under the traditional method of costing. Based on

the same the profitability of two methods of costing has been computed here-in-below:

Statement showing Profitability under Traditional Method and Activity Based Costing

SL No Particulars Traditional Method Activity Based Costing

1 Cost of Production 1879012.2 1951801.4

2 Mark Up 563703.7

3 Selling Price 2442715.9 2442715.9

4 Profit (3-1) 563703.7 490914.4

5 No of Units 1600 1600

6 Profit per Unit 352.31 306.82

On perusal of the above table, it can be inferred that profit is decreased under the Activity Based

costing system, thus the foreign companies have placed order for this grade of sewing machine as

the cost captured by traditional method is incorrect and company has loaded a markup of 30% on

under cost computed under traditional system of costing .Further, the basis of computation of cost

has been detailed above.

Further, the importance of accurate costing has been enumerated here-in-below:

(h) It helps businesses in making optimal decisions;

(i) It enables correct mark up on products;

(j) Wrong cost estimates may lead to business losses. Thus, correct costing enables guided decision

on product profitability;

(k) It helps in making decisions regarding which product shall be promoted by the company to

maximise its profits;

(l) It helps business to stay on schedule and track

4 Direct Labour Cost per unit 280

5 Total Direct Labour Cost 448000

6 Total indirect cost allocated 192301.4

7 Other operating Expense

-Selling and Administration 300200

-Interest Expense 40500

-Office Rent 42800

8 Total Cost 1951801.4

9 Cost per unit 1219.88

The cost per unit of the above product has been computed by dividing the total cost of production

incurred for manufacturing the Advanced Grade model of sewing machine by no of units produced

of Advance Model. Thus, the cost per unit of Advance Grade Sewing Machine stands at $ 1219.88

under Activity Based system of costing. The cost has decreased by $ 45.19 per unit of Advance Grade

Sewing Machine.

Profitability under Traditional System of Costing Vis-a Vis- Modern System of Costing

Under the present case, it has been established that the sales price of the Advance Grade Sewing

Machine has been quoted at 30 % markup of cost under the traditional method of costing. Based on

the same the profitability of two methods of costing has been computed here-in-below:

Statement showing Profitability under Traditional Method and Activity Based Costing

SL No Particulars Traditional Method Activity Based Costing

1 Cost of Production 1879012.2 1951801.4

2 Mark Up 563703.7

3 Selling Price 2442715.9 2442715.9

4 Profit (3-1) 563703.7 490914.4

5 No of Units 1600 1600

6 Profit per Unit 352.31 306.82

On perusal of the above table, it can be inferred that profit is decreased under the Activity Based

costing system, thus the foreign companies have placed order for this grade of sewing machine as

the cost captured by traditional method is incorrect and company has loaded a markup of 30% on

under cost computed under traditional system of costing .Further, the basis of computation of cost

has been detailed above.

Further, the importance of accurate costing has been enumerated here-in-below:

(h) It helps businesses in making optimal decisions;

(i) It enables correct mark up on products;

(j) Wrong cost estimates may lead to business losses. Thus, correct costing enables guided decision

on product profitability;

(k) It helps in making decisions regarding which product shall be promoted by the company to

maximise its profits;

(l) It helps business to stay on schedule and track

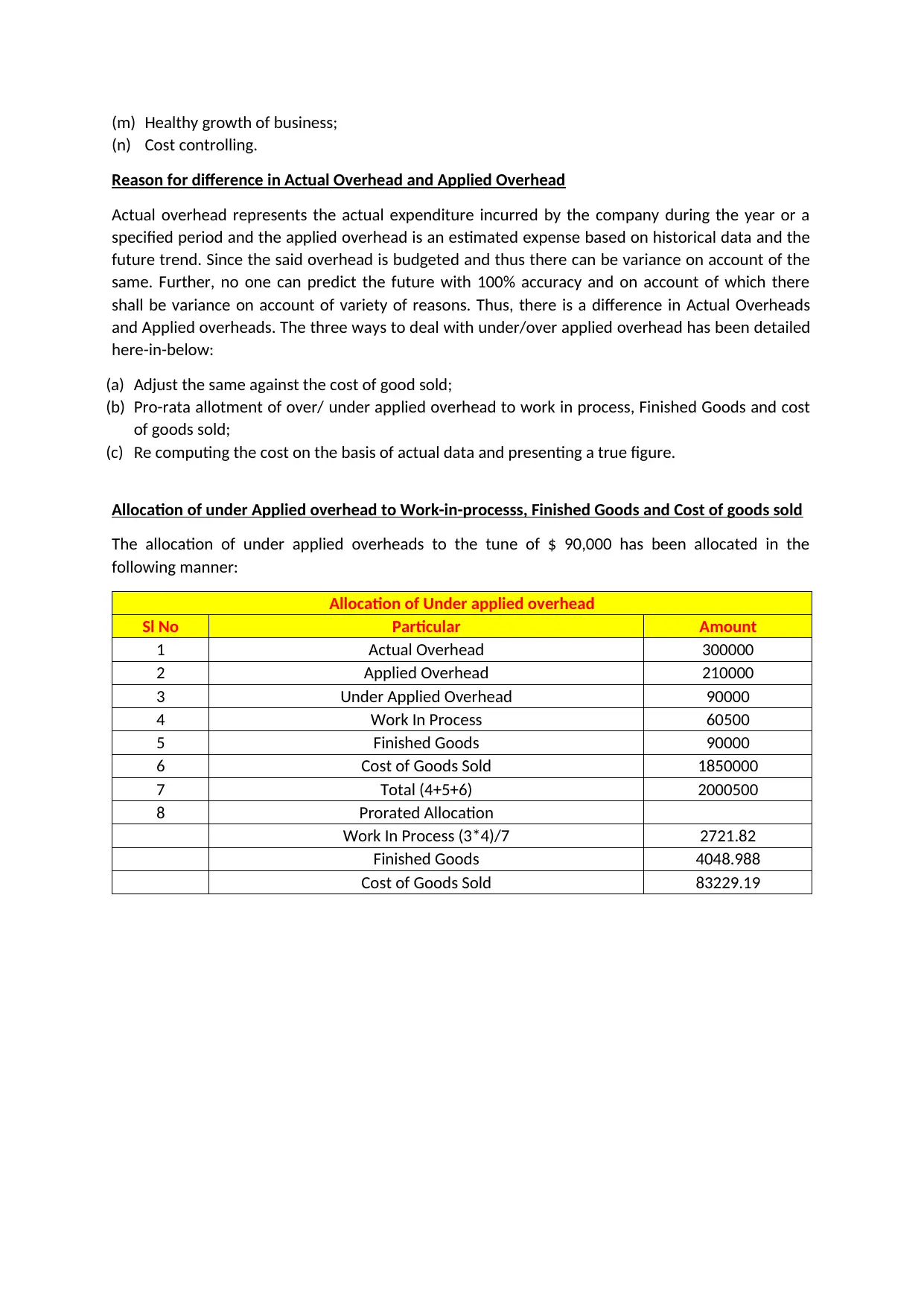

(m) Healthy growth of business;

(n) Cost controlling.

Reason for difference in Actual Overhead and Applied Overhead

Actual overhead represents the actual expenditure incurred by the company during the year or a

specified period and the applied overhead is an estimated expense based on historical data and the

future trend. Since the said overhead is budgeted and thus there can be variance on account of the

same. Further, no one can predict the future with 100% accuracy and on account of which there

shall be variance on account of variety of reasons. Thus, there is a difference in Actual Overheads

and Applied overheads. The three ways to deal with under/over applied overhead has been detailed

here-in-below:

(a) Adjust the same against the cost of good sold;

(b) Pro-rata allotment of over/ under applied overhead to work in process, Finished Goods and cost

of goods sold;

(c) Re computing the cost on the basis of actual data and presenting a true figure.

Allocation of under Applied overhead to Work-in-processs, Finished Goods and Cost of goods sold

The allocation of under applied overheads to the tune of $ 90,000 has been allocated in the

following manner:

Allocation of Under applied overhead

Sl No Particular Amount

1 Actual Overhead 300000

2 Applied Overhead 210000

3 Under Applied Overhead 90000

4 Work In Process 60500

5 Finished Goods 90000

6 Cost of Goods Sold 1850000

7 Total (4+5+6) 2000500

8 Prorated Allocation

Work In Process (3*4)/7 2721.82

Finished Goods 4048.988

Cost of Goods Sold 83229.19

(n) Cost controlling.

Reason for difference in Actual Overhead and Applied Overhead

Actual overhead represents the actual expenditure incurred by the company during the year or a

specified period and the applied overhead is an estimated expense based on historical data and the

future trend. Since the said overhead is budgeted and thus there can be variance on account of the

same. Further, no one can predict the future with 100% accuracy and on account of which there

shall be variance on account of variety of reasons. Thus, there is a difference in Actual Overheads

and Applied overheads. The three ways to deal with under/over applied overhead has been detailed

here-in-below:

(a) Adjust the same against the cost of good sold;

(b) Pro-rata allotment of over/ under applied overhead to work in process, Finished Goods and cost

of goods sold;

(c) Re computing the cost on the basis of actual data and presenting a true figure.

Allocation of under Applied overhead to Work-in-processs, Finished Goods and Cost of goods sold

The allocation of under applied overheads to the tune of $ 90,000 has been allocated in the

following manner:

Allocation of Under applied overhead

Sl No Particular Amount

1 Actual Overhead 300000

2 Applied Overhead 210000

3 Under Applied Overhead 90000

4 Work In Process 60500

5 Finished Goods 90000

6 Cost of Goods Sold 1850000

7 Total (4+5+6) 2000500

8 Prorated Allocation

Work In Process (3*4)/7 2721.82

Finished Goods 4048.988

Cost of Goods Sold 83229.19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.