Financial Analysis and Performance Comparison: Farsons vs. Heiniken

VerifiedAdded on 2023/01/18

|20

|4806

|32

Report

AI Summary

This report presents a detailed financial analysis comparing Farsons and Heiniken, two companies in the beer manufacturing industry. The analysis includes a comprehensive examination of profitability ratios, such as operating profit margin, net profit margin, return on assets (ROA), and return on equity (ROE), to assess their financial performance. Leverage ratios like the debt-equity ratio and debt-assets ratio are evaluated to understand their financial risk and capital structure. Liquidity ratios, including the current ratio and quick ratio, are assessed to determine their ability to meet short-term obligations. Efficiency ratios, such as receivable turnover, payable turnover, asset turnover, and inventory days, are analyzed to gauge their operational efficiency. The report also includes an analysis of working capital and annual cash flow for both companies, along with vertical and horizontal analysis for both companies to provide a more comprehensive financial overview. The findings highlight the strengths and weaknesses of each company, offering insights into their financial health and performance trends.

Financial Analysis Management &

Enterprise - FAME

Enterprise - FAME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Presentation of the detailed analysis in the financial performance between the two

companies....................................................................................................................................3

2. Importance of analysing working capital -..............................................................................8

3. Analysis of annual cash flow of both the companies...............................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIXE.................................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Presentation of the detailed analysis in the financial performance between the two

companies....................................................................................................................................3

2. Importance of analysing working capital -..............................................................................8

3. Analysis of annual cash flow of both the companies...............................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIXE.................................................................................................................................13

INTRODUCTION

Financial analysis helps the company to have the major impacts in masking the effective

decision-making in the organization. There are various level of ways which will help in proper

analysing the business situation of company in more effective way for particular level of

development. For the comparison two firm which have been chosen to have the proper analysis.

The companies are Farsons and Heiniken as both are beer manufacture company as the level of

competitor firm. Farsons is a Maltese food and beverage conglomerate. The businesses of the

Farsons Group include brewing, production, sale and distribution of beers. On the other hand is

a pale lager beer with 5% alcohol by volume produced by the Dutch brewing company Heiniken

International. Heiniken beer is sold in a green bottle with a red star.

MAIN BODY

1. Presentation of the detailed analysis in the financial performance between the two companies.

Profitability ratio

Operating profit margin- the operating profit ratio have the clear indication regarding

the profits which is earned by company after meeting all the level of cost such as raw material

and wages of labour etc. the company has been type of profitably ratio which have the depiction

of efficiency as per firm in keeping control in the cost and expenses which have been attached in

business operation development. The higher level of margining in operation profit have the

reselection of the better level of performance in an enterprise in the systematic accounting

period. The ratio analysis of company Heiniken has seen that operating margin is having the

steep level of declining as comparative to the competitor firm arson in the level of increasing

trend. This has the clear indication that the latter company have the more level of efficiency in

order to meet in operation expenses as the former one. The companies are considered to be more

effective which is somewhere having the major level of contribution in development of company

in more appropriate manner.

Net profit margin- The profitability ratio have the proper level of indication which are in

level of sales proportion of the systematic sales revenue which can be converted into the net

profit. The ratio has been analysed as the measure of key performance in the profitability of firm.

The increase higher level of profit margin makes the company more effective along with

efficiency in range of conversing the sales into net profit. As per the result of the analysed that

Financial analysis helps the company to have the major impacts in masking the effective

decision-making in the organization. There are various level of ways which will help in proper

analysing the business situation of company in more effective way for particular level of

development. For the comparison two firm which have been chosen to have the proper analysis.

The companies are Farsons and Heiniken as both are beer manufacture company as the level of

competitor firm. Farsons is a Maltese food and beverage conglomerate. The businesses of the

Farsons Group include brewing, production, sale and distribution of beers. On the other hand is

a pale lager beer with 5% alcohol by volume produced by the Dutch brewing company Heiniken

International. Heiniken beer is sold in a green bottle with a red star.

MAIN BODY

1. Presentation of the detailed analysis in the financial performance between the two companies.

Profitability ratio

Operating profit margin- the operating profit ratio have the clear indication regarding

the profits which is earned by company after meeting all the level of cost such as raw material

and wages of labour etc. the company has been type of profitably ratio which have the depiction

of efficiency as per firm in keeping control in the cost and expenses which have been attached in

business operation development. The higher level of margining in operation profit have the

reselection of the better level of performance in an enterprise in the systematic accounting

period. The ratio analysis of company Heiniken has seen that operating margin is having the

steep level of declining as comparative to the competitor firm arson in the level of increasing

trend. This has the clear indication that the latter company have the more level of efficiency in

order to meet in operation expenses as the former one. The companies are considered to be more

effective which is somewhere having the major level of contribution in development of company

in more appropriate manner.

Net profit margin- The profitability ratio have the proper level of indication which are in

level of sales proportion of the systematic sales revenue which can be converted into the net

profit. The ratio has been analysed as the measure of key performance in the profitability of firm.

The increase higher level of profit margin makes the company more effective along with

efficiency in range of conversing the sales into net profit. As per the result of the analysed that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the Heiniken is having the four years decline as there i8s systematic decrease in operating profit.

This has the clear indication that the company is not able to have the well level of performance is

the aspects of sales along with generating the level of operating profit. On the other hand the

NPM of the latter company is having the level of increase as compare to former one through

having proper level of profit generation. This is helping in reflecting better performance of

company as compare to is competitors in gaining the level of competitive advantage in

understanding the marketing environment in more proper level.

Return on assets () – it has been refereed as ratio which have measurement of effectiveness in

companies in the respects to have proper level of earning as per the investment done

systematically on assets. This also helps in having the clear level of reflection about the company

level of conversion of money in purchasing the assets into the net profit. The positive level of

result in of the ratio have the proper level of insinuation in company ability to generate a high

level of profit generation with having the systematic level of investment of assets. As per

properly analysis the both companies return on assets it has been clearly identified as the

Heinlein ROA is 5 and Farsons is resulted as 7 which turned out to have the managing of the

latter company is able to have more focus in generation of more efficient use of its assets as

compared to Heiniken.

Return On Equity (ROE) – as consideration of the profitability ratio is term as the ability in

having the generation of the specific profits which is earned by company in having systematize

investment on shareholder in inside the company. In accordance to have the level of proper

analysis it has been identified that Heiniken is having the downfall trend as comparative to its

competitor firm. The later one is having the level of increase in the company that is from 8 to 12

in the between of four years. The company able to have the proper generation of amount of

annual profit along with having proper level of investment which is being made by the

shareholders as compare to the specific competitors Heiniken. In existence of positive

relationship has increase the level of ability of company to have the increase level of generation

of profit without adding much to the capital of the firm.

Leverage ratio -

Debt-equity ratio- this ratio has the indication of values in percentage in regard to

financing of company along with proper attainment from their respective investors and

shareholders. The higher level of debt equity ratio have the major level of reflection in more of

This has the clear indication that the company is not able to have the well level of performance is

the aspects of sales along with generating the level of operating profit. On the other hand the

NPM of the latter company is having the level of increase as compare to former one through

having proper level of profit generation. This is helping in reflecting better performance of

company as compare to is competitors in gaining the level of competitive advantage in

understanding the marketing environment in more proper level.

Return on assets () – it has been refereed as ratio which have measurement of effectiveness in

companies in the respects to have proper level of earning as per the investment done

systematically on assets. This also helps in having the clear level of reflection about the company

level of conversion of money in purchasing the assets into the net profit. The positive level of

result in of the ratio have the proper level of insinuation in company ability to generate a high

level of profit generation with having the systematic level of investment of assets. As per

properly analysis the both companies return on assets it has been clearly identified as the

Heinlein ROA is 5 and Farsons is resulted as 7 which turned out to have the managing of the

latter company is able to have more focus in generation of more efficient use of its assets as

compared to Heiniken.

Return On Equity (ROE) – as consideration of the profitability ratio is term as the ability in

having the generation of the specific profits which is earned by company in having systematize

investment on shareholder in inside the company. In accordance to have the level of proper

analysis it has been identified that Heiniken is having the downfall trend as comparative to its

competitor firm. The later one is having the level of increase in the company that is from 8 to 12

in the between of four years. The company able to have the proper generation of amount of

annual profit along with having proper level of investment which is being made by the

shareholders as compare to the specific competitors Heiniken. In existence of positive

relationship has increase the level of ability of company to have the increase level of generation

of profit without adding much to the capital of the firm.

Leverage ratio -

Debt-equity ratio- this ratio has the indication of values in percentage in regard to

financing of company along with proper attainment from their respective investors and

shareholders. The higher level of debt equity ratio have the major level of reflection in more of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

creditor turn financing as compare to investor financing. The evaluation of this respective ratio

have the proper evaluation of both company in have the proper level of increase in recent past

years. This is not stated as the good design for the companies as it has the level of representation

that company is not able to make the level of sufficient cash in order to have the satisfaction in

terms of obligation which is been related to debt. This also stated that company is having the

tendency of risk at higher level so respective companies have to take aggressive action in

financing of its growth in terms of debts. It can be significantly impacts of changes in long term

debts and assets as they tend to have larger accounts as compared to short term debts and assets.

Debt-assets ratio- the following leverage ratio have reflection about the liabilities amount

which is been owned by the firm. The ideal ratio is equating to 1 in which the company use to

own the similar level of assets and liabilities. Its also have the tendency of showing that is firm is

highly leverage. As per the ratio analysis of the respective firm it can be analysed that company

have the increase level of debt assets ratio but less than 1. This states that company is having the

more level of assets as compare to debt which means that company is able to meet up its

obligation by selling the assets if needed and concluded to have less risky company.

Liquidity ratio

Current ratio- This ratio has the indication is measure the actual liquidation position of

company with having proper level of assessment of current asset along with current liabilities in

firm. In the past years the former company have the level of increase in their current assets which

means the company is capable to make the efficient use of assets along with having the ability in

order to have the meet of the short term obligation. On the other side the latter company that is

Farsons have reach the ideal ratio of the specific one that is 2;1 which is grater as comparer to

the Heiniken. The layer company is having more level of better performance and stability in

maintaining the liquidity position of the marketing firm.

Quick ratio- this ratio has the indication of liquid position of firm along with having the

ability of the companies to have the proper level of paying off of the recent obligation with the

use of the assets at the immediate level. This ratio has been considered as the more level of

conservative in nature. It has been analysed that the company have the increase level of which

have the clear level of depicts which is maintaining the better relationship in maintaining the

liquidity position of the organization within the industry.

Efficiency ratio-

have the proper evaluation of both company in have the proper level of increase in recent past

years. This is not stated as the good design for the companies as it has the level of representation

that company is not able to make the level of sufficient cash in order to have the satisfaction in

terms of obligation which is been related to debt. This also stated that company is having the

tendency of risk at higher level so respective companies have to take aggressive action in

financing of its growth in terms of debts. It can be significantly impacts of changes in long term

debts and assets as they tend to have larger accounts as compared to short term debts and assets.

Debt-assets ratio- the following leverage ratio have reflection about the liabilities amount

which is been owned by the firm. The ideal ratio is equating to 1 in which the company use to

own the similar level of assets and liabilities. Its also have the tendency of showing that is firm is

highly leverage. As per the ratio analysis of the respective firm it can be analysed that company

have the increase level of debt assets ratio but less than 1. This states that company is having the

more level of assets as compare to debt which means that company is able to meet up its

obligation by selling the assets if needed and concluded to have less risky company.

Liquidity ratio

Current ratio- This ratio has the indication is measure the actual liquidation position of

company with having proper level of assessment of current asset along with current liabilities in

firm. In the past years the former company have the level of increase in their current assets which

means the company is capable to make the efficient use of assets along with having the ability in

order to have the meet of the short term obligation. On the other side the latter company that is

Farsons have reach the ideal ratio of the specific one that is 2;1 which is grater as comparer to

the Heiniken. The layer company is having more level of better performance and stability in

maintaining the liquidity position of the marketing firm.

Quick ratio- this ratio has the indication of liquid position of firm along with having the

ability of the companies to have the proper level of paying off of the recent obligation with the

use of the assets at the immediate level. This ratio has been considered as the more level of

conservative in nature. It has been analysed that the company have the increase level of which

have the clear level of depicts which is maintaining the better relationship in maintaining the

liquidity position of the organization within the industry.

Efficiency ratio-

Receivable turnover- the ratio have the indication in collection process in company to

have assurance the large numbers of customer quality pay-off along with debt settlement in quick

basis. The high level of receivable turnover have clear indication which have reflection that t5he

company have the more basis in cash basis rather than having the credit basis. From the above

figure it can be clearly evaluated that the company Farsons is having the higher level of turnover

of receivable as compare to the Heiniken. This result that company is having the higher level of

efficiency. The company is able to have the high proportion of the quality customers who are

pausing the debt in quicker manner. This also have the indication that the company us bale to

have the clear level of operation's of the cash basis.

Payable turnover which have ratio which shows the creditors the level of liquidity along

with credit wordiness of the company. The huge level of reflection have the promptness that the

payment can be made in purchasing the level of supplier in credit. The companies are having the

level of stable ratio which shows that there are makes of the payment on correct times without

taking the long period.

Asset turnover- the ratio have the application in generating the level of assets which are

higher in nature. This situation has been considered as the favourable one which is due to more

and efficient level of use of assets. In the proper level of ration analysis it has been analysed that

both companies are non-performing well. This is also helped the company in order to have rise in

producing sales along with meeting up target.

Inventory days- this has the indication of the fast moving inventories which is resultant as

the high ratio along with slow moving will result as the obsolete level of inventory. In analysis, it

can be interpreted that the both companies are high which means that there is more level of stock

which is moving as there is no existence of extra inventory in company.

Shareholders ratio

Shareholders equity ratio-it is the financial ratio which have the indication in level of

proportional with is relative to equity which is considered as the major element on financing the

companies. The companies' shareholder ratio is stable over the years which means better

financial state of an entity.

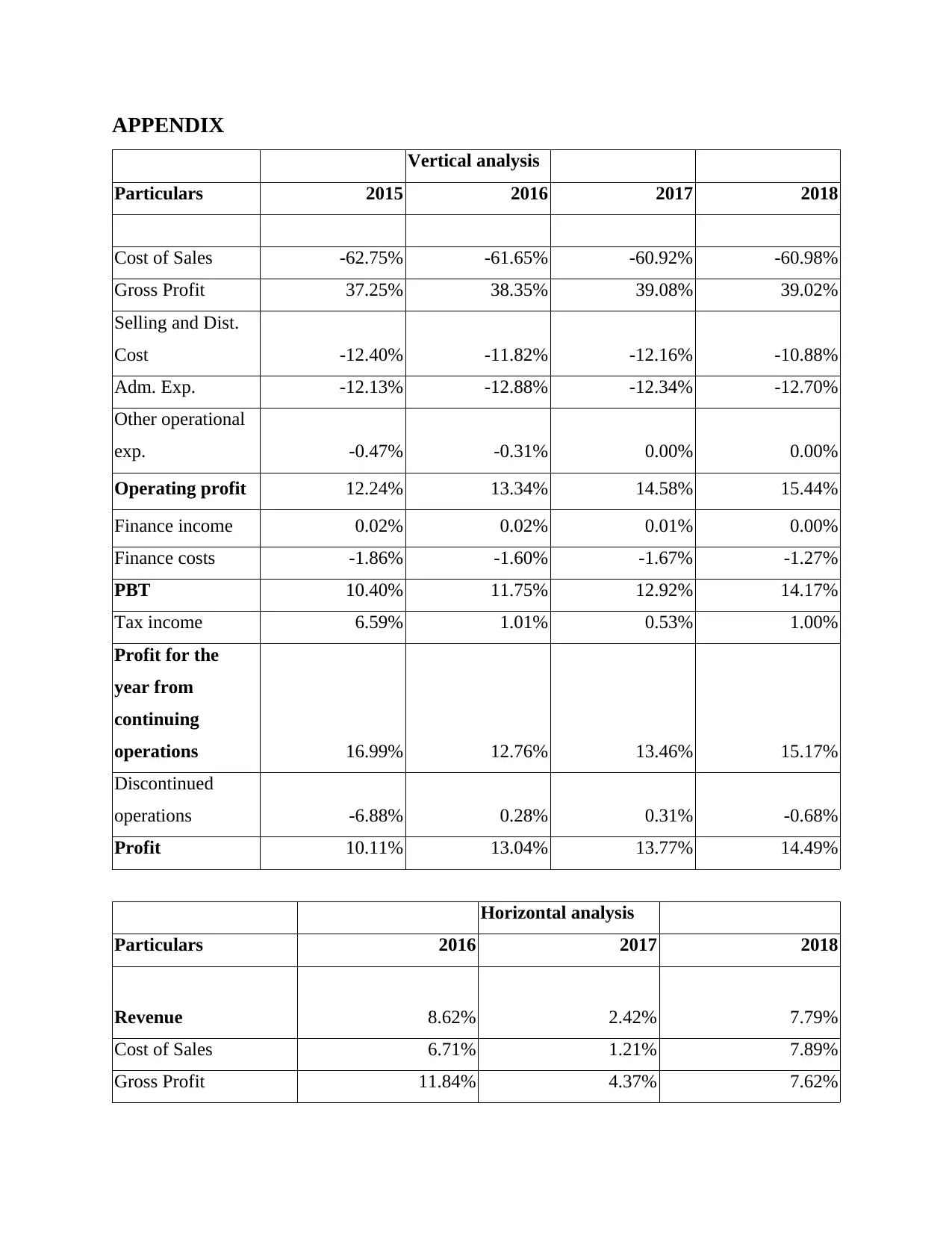

Vertical analysis of Farsons

have assurance the large numbers of customer quality pay-off along with debt settlement in quick

basis. The high level of receivable turnover have clear indication which have reflection that t5he

company have the more basis in cash basis rather than having the credit basis. From the above

figure it can be clearly evaluated that the company Farsons is having the higher level of turnover

of receivable as compare to the Heiniken. This result that company is having the higher level of

efficiency. The company is able to have the high proportion of the quality customers who are

pausing the debt in quicker manner. This also have the indication that the company us bale to

have the clear level of operation's of the cash basis.

Payable turnover which have ratio which shows the creditors the level of liquidity along

with credit wordiness of the company. The huge level of reflection have the promptness that the

payment can be made in purchasing the level of supplier in credit. The companies are having the

level of stable ratio which shows that there are makes of the payment on correct times without

taking the long period.

Asset turnover- the ratio have the application in generating the level of assets which are

higher in nature. This situation has been considered as the favourable one which is due to more

and efficient level of use of assets. In the proper level of ration analysis it has been analysed that

both companies are non-performing well. This is also helped the company in order to have rise in

producing sales along with meeting up target.

Inventory days- this has the indication of the fast moving inventories which is resultant as

the high ratio along with slow moving will result as the obsolete level of inventory. In analysis, it

can be interpreted that the both companies are high which means that there is more level of stock

which is moving as there is no existence of extra inventory in company.

Shareholders ratio

Shareholders equity ratio-it is the financial ratio which have the indication in level of

proportional with is relative to equity which is considered as the major element on financing the

companies. The companies' shareholder ratio is stable over the years which means better

financial state of an entity.

Vertical analysis of Farsons

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For the vertical analysis it can be concluded that the company is not able to have the there is the

increased level of profit from the year 2015 to years 2018. That is the company have almost 5%

increase in level of profit as compare to is the previous years.

Horizontal analysis of Farsons.

In the horizontal analysis it has been concluded that the company has reduced to the level in

making the profit in the last years . The company has almost below less than 50% as compared to

the base years in make the level of profit.

Horizontal analysis of Heiniken

On the basis of the horizontals' analysis it can be analysed the as competitive to the base year

2015 the company have maximum reduction in years 2016 and the years 2018.

Vertical analysis of Heiniken

The vertical analysis of the company states that the profitability of company doesn't have the

belongingness to any ODF the specific trends. But is has been evaluated all around the 10% in

last four years. But in last year 2018 it has been reduced as the steep level.

2. Importance of analysing working capital -

Working capital :

The working capital has been considered as the calculation of variance between the

current assess the company and the current liabilities. The current assets re such as the s accounts

receivable, cash and current outstanding expenses, accounts payable etc. the company have the

consideration of the different types of working capital which are considered as the temporary and

permanent, gross and net working capital etc . For instance, it can be considered as company has

the portion which is debt within the time period of one year. The working capital have the

consideration of resultants of various level of activities such as the debt management, payment to

creditors etc. on the further level the analysis of working capital as can be defined as the analysis

which is helping in having proper level of determination in sufficiency and liquidity as compared

current assets to current liabilities.

Farsons

The analysis of the both the companies is considered as important part before taking any

level of decision. There should be proper evaluation of the working capital by Farsons before

taking any level of particular decision as it helps in examiner the timeline of the current

liabilities. The information helps in gaining the level of capitals which helps the company to

increased level of profit from the year 2015 to years 2018. That is the company have almost 5%

increase in level of profit as compare to is the previous years.

Horizontal analysis of Farsons.

In the horizontal analysis it has been concluded that the company has reduced to the level in

making the profit in the last years . The company has almost below less than 50% as compared to

the base years in make the level of profit.

Horizontal analysis of Heiniken

On the basis of the horizontals' analysis it can be analysed the as competitive to the base year

2015 the company have maximum reduction in years 2016 and the years 2018.

Vertical analysis of Heiniken

The vertical analysis of the company states that the profitability of company doesn't have the

belongingness to any ODF the specific trends. But is has been evaluated all around the 10% in

last four years. But in last year 2018 it has been reduced as the steep level.

2. Importance of analysing working capital -

Working capital :

The working capital has been considered as the calculation of variance between the

current assess the company and the current liabilities. The current assets re such as the s accounts

receivable, cash and current outstanding expenses, accounts payable etc. the company have the

consideration of the different types of working capital which are considered as the temporary and

permanent, gross and net working capital etc . For instance, it can be considered as company has

the portion which is debt within the time period of one year. The working capital have the

consideration of resultants of various level of activities such as the debt management, payment to

creditors etc. on the further level the analysis of working capital as can be defined as the analysis

which is helping in having proper level of determination in sufficiency and liquidity as compared

current assets to current liabilities.

Farsons

The analysis of the both the companies is considered as important part before taking any

level of decision. There should be proper evaluation of the working capital by Farsons before

taking any level of particular decision as it helps in examiner the timeline of the current

liabilities. The information helps in gaining the level of capitals which helps the company to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have the proper level of determination with in the level of currents availabilities which will have

the acquirement of the funds on term basis which is performed in aversion types of the

organization. The company will be able to make the plan to shift additional cash into long term

investment vehicles. This will help the company in longer term in taking the decision and

consideration ODF all aspects which will have the maximization operation. This will have the

lead to the maintenance of the level of operation which are smooth in nature a support the

company in order to have the level of improbability and crabbing as well. The company will be

ensured by effectiveness in managing proper level if accounts payables and management of

stock.

Heiniken

The company can have the use of the account payable repost to have the proper division of

the variant accounts payable into the next 30 days bucket in having the proper level of evaluation

of the liquidity available with company. On the other hand on further level the payment timings

of remaining liabilities which will be highly dependable in analysis of working capital in which

there will be clear indication related to payment of outstanding obligation. The company will be

able to make the proper variability and analysis of debtors. This will helps in ageing the accounts

receivable report and also with the help of short term-time buckets. There will be consideration

of revisitation of clients which is having the consideration of paying and amount due date which

will have involvement of correct assessment in potential incoming and cash flows. The

e4ffcetive system of the working capital make the analysis to determine and evaluate areas that

require attention in order to maintain profitability and liquidity. This will not only help company

to meet out financial obligations but also assist the management to improve the earnings of the

business.

3. Analysis of annual cash flow of both the companies.

Definitions -

Cash flow margin ratio is helps in measuring the operating objectivities in percentage of the

generalized revenue from the given sales.

Cash flow coverage ratio it helps in indicating the firm capacity's which is paying the amount of

the principal along with interest around the due date.

Current liabilities' coverage ratio it helps in measuring the level of realizing between the level

of generalizing cash from the current liabilities of the company.

the acquirement of the funds on term basis which is performed in aversion types of the

organization. The company will be able to make the plan to shift additional cash into long term

investment vehicles. This will help the company in longer term in taking the decision and

consideration ODF all aspects which will have the maximization operation. This will have the

lead to the maintenance of the level of operation which are smooth in nature a support the

company in order to have the level of improbability and crabbing as well. The company will be

ensured by effectiveness in managing proper level if accounts payables and management of

stock.

Heiniken

The company can have the use of the account payable repost to have the proper division of

the variant accounts payable into the next 30 days bucket in having the proper level of evaluation

of the liquidity available with company. On the other hand on further level the payment timings

of remaining liabilities which will be highly dependable in analysis of working capital in which

there will be clear indication related to payment of outstanding obligation. The company will be

able to make the proper variability and analysis of debtors. This will helps in ageing the accounts

receivable report and also with the help of short term-time buckets. There will be consideration

of revisitation of clients which is having the consideration of paying and amount due date which

will have involvement of correct assessment in potential incoming and cash flows. The

e4ffcetive system of the working capital make the analysis to determine and evaluate areas that

require attention in order to maintain profitability and liquidity. This will not only help company

to meet out financial obligations but also assist the management to improve the earnings of the

business.

3. Analysis of annual cash flow of both the companies.

Definitions -

Cash flow margin ratio is helps in measuring the operating objectivities in percentage of the

generalized revenue from the given sales.

Cash flow coverage ratio it helps in indicating the firm capacity's which is paying the amount of

the principal along with interest around the due date.

Current liabilities' coverage ratio it helps in measuring the level of realizing between the level

of generalizing cash from the current liabilities of the company.

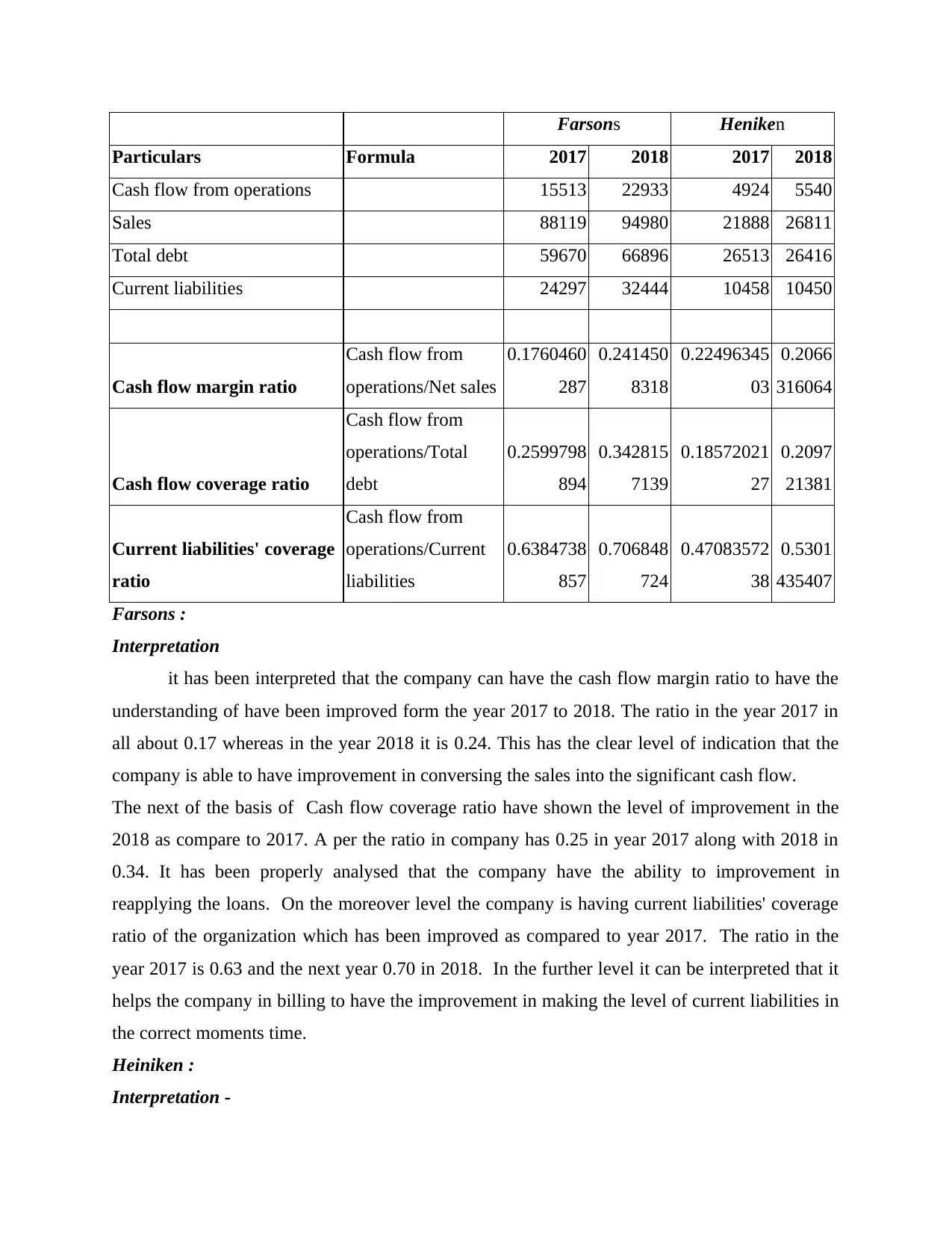

Farsons Heniken

Particulars Formula 2017 2018 2017 2018

Cash flow from operations 15513 22933 4924 5540

Sales 88119 94980 21888 26811

Total debt 59670 66896 26513 26416

Current liabilities 24297 32444 10458 10450

Cash flow margin ratio

Cash flow from

operations/Net sales

0.1760460

287

0.241450

8318

0.22496345

03

0.2066

316064

Cash flow coverage ratio

Cash flow from

operations/Total

debt

0.2599798

894

0.342815

7139

0.18572021

27

0.2097

21381

Current liabilities' coverage

ratio

Cash flow from

operations/Current

liabilities

0.6384738

857

0.706848

724

0.47083572

38

0.5301

435407

Farsons :

Interpretation

it has been interpreted that the company can have the cash flow margin ratio to have the

understanding of have been improved form the year 2017 to 2018. The ratio in the year 2017 in

all about 0.17 whereas in the year 2018 it is 0.24. This has the clear level of indication that the

company is able to have improvement in conversing the sales into the significant cash flow.

The next of the basis of Cash flow coverage ratio have shown the level of improvement in the

2018 as compare to 2017. A per the ratio in company has 0.25 in year 2017 along with 2018 in

0.34. It has been properly analysed that the company have the ability to improvement in

reapplying the loans. On the moreover level the company is having current liabilities' coverage

ratio of the organization which has been improved as compared to year 2017. The ratio in the

year 2017 is 0.63 and the next year 0.70 in 2018. In the further level it can be interpreted that it

helps the company in billing to have the improvement in making the level of current liabilities in

the correct moments time.

Heiniken :

Interpretation -

Particulars Formula 2017 2018 2017 2018

Cash flow from operations 15513 22933 4924 5540

Sales 88119 94980 21888 26811

Total debt 59670 66896 26513 26416

Current liabilities 24297 32444 10458 10450

Cash flow margin ratio

Cash flow from

operations/Net sales

0.1760460

287

0.241450

8318

0.22496345

03

0.2066

316064

Cash flow coverage ratio

Cash flow from

operations/Total

debt

0.2599798

894

0.342815

7139

0.18572021

27

0.2097

21381

Current liabilities' coverage

ratio

Cash flow from

operations/Current

liabilities

0.6384738

857

0.706848

724

0.47083572

38

0.5301

435407

Farsons :

Interpretation

it has been interpreted that the company can have the cash flow margin ratio to have the

understanding of have been improved form the year 2017 to 2018. The ratio in the year 2017 in

all about 0.17 whereas in the year 2018 it is 0.24. This has the clear level of indication that the

company is able to have improvement in conversing the sales into the significant cash flow.

The next of the basis of Cash flow coverage ratio have shown the level of improvement in the

2018 as compare to 2017. A per the ratio in company has 0.25 in year 2017 along with 2018 in

0.34. It has been properly analysed that the company have the ability to improvement in

reapplying the loans. On the moreover level the company is having current liabilities' coverage

ratio of the organization which has been improved as compared to year 2017. The ratio in the

year 2017 is 0.63 and the next year 0.70 in 2018. In the further level it can be interpreted that it

helps the company in billing to have the improvement in making the level of current liabilities in

the correct moments time.

Heiniken :

Interpretation -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It has been analysed that the cash flow margining have the reduced the form year 2017 to

year 2018. The company have the decreased point 0.20 in year 2018 as compare to 2017. This

has had the clear indication that companies has reduced capabilities which is converting the sales

amount into cash inflow.

Moreover, there us the conclusion that the cash flow coverage ratio has been increased in

year 2017 as per yer2018. In year 2017, the ratio was 0.18 as compared to year 2017 in which the

cash flow coverage ratio was 0.20.

On the further level the current liabilities' coverage ratio of Heiniken have been found at

increasing level in the year 2018 as compared to the vales of the year 2017. In the year 2017 the

ratio was .40 as on the other hand ratio has increased up-to 0.53 in 2018. Form this it can be

concluded that the company is able to produce the sufficient level of cash flow in paying the

outstanding level of liabilities to the various parties.

CONCLUSION

From the repost it can be concluded that the various ratio vertical and horizontal analysis

has help in making the proper level of understanding in make the level of interpretation in proper

decision-making of the business. The company Farsons as be compared to be more effective as

to its competitors. The working capital has been considered as the calculation of variance

between the current assess the company and the current liabilities. The company have the

consideration of the different types of working capital which are considered as the temporary and

permanent, gross and net working capital. On the other hand the analysis of the both companies

in making the proper level of interpretation to have the proper development of the prorogation in

having the level of understanding in different business aspects.

year 2018. The company have the decreased point 0.20 in year 2018 as compare to 2017. This

has had the clear indication that companies has reduced capabilities which is converting the sales

amount into cash inflow.

Moreover, there us the conclusion that the cash flow coverage ratio has been increased in

year 2017 as per yer2018. In year 2017, the ratio was 0.18 as compared to year 2017 in which the

cash flow coverage ratio was 0.20.

On the further level the current liabilities' coverage ratio of Heiniken have been found at

increasing level in the year 2018 as compared to the vales of the year 2017. In the year 2017 the

ratio was .40 as on the other hand ratio has increased up-to 0.53 in 2018. Form this it can be

concluded that the company is able to produce the sufficient level of cash flow in paying the

outstanding level of liabilities to the various parties.

CONCLUSION

From the repost it can be concluded that the various ratio vertical and horizontal analysis

has help in making the proper level of understanding in make the level of interpretation in proper

decision-making of the business. The company Farsons as be compared to be more effective as

to its competitors. The working capital has been considered as the calculation of variance

between the current assess the company and the current liabilities. The company have the

consideration of the different types of working capital which are considered as the temporary and

permanent, gross and net working capital. On the other hand the analysis of the both companies

in making the proper level of interpretation to have the proper development of the prorogation in

having the level of understanding in different business aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Ağca, Ş. and Mozumdar, A., 2017. Investment–Cash Flow Sensitivity: Fact or Fiction?. Journal

of Financial and Quantitative Analysis, 52(3), pp.1111-1141.

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate Finance, 30,

pp.98-113.

Baldacchino, P.J., Vella, C. and Grima, S., 2019. The Corporate Governance Code and

Compliance by Maltese Listed Companies. International Journal of Economics &

Business Administration (IJEBA), 7(2), pp.71-90.

Billiard, E., 2016. Lost in tradition: an attempt to go beyond labels, taking Maltese food practices

as a primary example. In Eating Traditional Food (pp. 62-80). Routledge.

Camin, F., Bontempo, L., Perini, M. and Piasentier, E., 2016. Stable isotope ratio analysis for

assessing the authenticity of food of animal origin. Comprehensive Reviews in Food

Science and Food Safety, 15(5), pp.868-877.

Campbell, D., 2015. Investigating the need for an EAP: a case study (Bachelor's thesis,

University of Malta).

Hatanaka, M., Yokoyama, Y., Ogawa, N.O., Miyairi, Y., Clark, G. and Ohkouchi, N., 2017.

Paleodiet study based on isotopic ratio analysis of bone collagen from Malagasy extinct

species.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of

Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Pais, M.A. and Gama, P.M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance, 11(3), pp.341-358.

Petruzzo, P., Gazarian, A., Kanitakis, J., Parmentier, H., Guigal, V., Guillot, M., Vial, C.,

Dubernard, J.M., Morelon, E. and Badet, L., 2015. Outcomes after bilateral hand

allotransplantation: a risk/benefit ratio analysis. Annals of surgery, 261(1), pp.213-220.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Short, C.A., 2017. The Recovery of Natural Environments in Architecture: Air, Comfort and

Climate. Routledge.

Weber, M., 2018. Cash flow duration and the term structure of equity returns. Journal of

Financial Economics, 128(3), pp.486-503.

Ağca, Ş. and Mozumdar, A., 2017. Investment–Cash Flow Sensitivity: Fact or Fiction?. Journal

of Financial and Quantitative Analysis, 52(3), pp.1111-1141.

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate Finance, 30,

pp.98-113.

Baldacchino, P.J., Vella, C. and Grima, S., 2019. The Corporate Governance Code and

Compliance by Maltese Listed Companies. International Journal of Economics &

Business Administration (IJEBA), 7(2), pp.71-90.

Billiard, E., 2016. Lost in tradition: an attempt to go beyond labels, taking Maltese food practices

as a primary example. In Eating Traditional Food (pp. 62-80). Routledge.

Camin, F., Bontempo, L., Perini, M. and Piasentier, E., 2016. Stable isotope ratio analysis for

assessing the authenticity of food of animal origin. Comprehensive Reviews in Food

Science and Food Safety, 15(5), pp.868-877.

Campbell, D., 2015. Investigating the need for an EAP: a case study (Bachelor's thesis,

University of Malta).

Hatanaka, M., Yokoyama, Y., Ogawa, N.O., Miyairi, Y., Clark, G. and Ohkouchi, N., 2017.

Paleodiet study based on isotopic ratio analysis of bone collagen from Malagasy extinct

species.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of

Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Pais, M.A. and Gama, P.M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance, 11(3), pp.341-358.

Petruzzo, P., Gazarian, A., Kanitakis, J., Parmentier, H., Guigal, V., Guillot, M., Vial, C.,

Dubernard, J.M., Morelon, E. and Badet, L., 2015. Outcomes after bilateral hand

allotransplantation: a risk/benefit ratio analysis. Annals of surgery, 261(1), pp.213-220.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Short, C.A., 2017. The Recovery of Natural Environments in Architecture: Air, Comfort and

Climate. Routledge.

Weber, M., 2018. Cash flow duration and the term structure of equity returns. Journal of

Financial Economics, 128(3), pp.486-503.

APPENDIX

Vertical analysis

Particulars 2015 2016 2017 2018

Cost of Sales -62.75% -61.65% -60.92% -60.98%

Gross Profit 37.25% 38.35% 39.08% 39.02%

Selling and Dist.

Cost -12.40% -11.82% -12.16% -10.88%

Adm. Exp. -12.13% -12.88% -12.34% -12.70%

Other operational

exp. -0.47% -0.31% 0.00% 0.00%

Operating profit 12.24% 13.34% 14.58% 15.44%

Finance income 0.02% 0.02% 0.01% 0.00%

Finance costs -1.86% -1.60% -1.67% -1.27%

PBT 10.40% 11.75% 12.92% 14.17%

Tax income 6.59% 1.01% 0.53% 1.00%

Profit for the

year from

continuing

operations 16.99% 12.76% 13.46% 15.17%

Discontinued

operations -6.88% 0.28% 0.31% -0.68%

Profit 10.11% 13.04% 13.77% 14.49%

Horizontal analysis

Particulars 2016 2017 2018

Revenue 8.62% 2.42% 7.79%

Cost of Sales 6.71% 1.21% 7.89%

Gross Profit 11.84% 4.37% 7.62%

Vertical analysis

Particulars 2015 2016 2017 2018

Cost of Sales -62.75% -61.65% -60.92% -60.98%

Gross Profit 37.25% 38.35% 39.08% 39.02%

Selling and Dist.

Cost -12.40% -11.82% -12.16% -10.88%

Adm. Exp. -12.13% -12.88% -12.34% -12.70%

Other operational

exp. -0.47% -0.31% 0.00% 0.00%

Operating profit 12.24% 13.34% 14.58% 15.44%

Finance income 0.02% 0.02% 0.01% 0.00%

Finance costs -1.86% -1.60% -1.67% -1.27%

PBT 10.40% 11.75% 12.92% 14.17%

Tax income 6.59% 1.01% 0.53% 1.00%

Profit for the

year from

continuing

operations 16.99% 12.76% 13.46% 15.17%

Discontinued

operations -6.88% 0.28% 0.31% -0.68%

Profit 10.11% 13.04% 13.77% 14.49%

Horizontal analysis

Particulars 2016 2017 2018

Revenue 8.62% 2.42% 7.79%

Cost of Sales 6.71% 1.21% 7.89%

Gross Profit 11.84% 4.37% 7.62%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.