FASB's Disclosure and Framework: Interim Reporting Project Report

VerifiedAdded on 2022/08/22

|11

|3470

|32

Report

AI Summary

This report provides a comprehensive analysis of the Financial Accounting Standards Board (FASB) project titled "Disclosure and Framework: Disclosures-Interim Reporting." The report begins with an executive summary outlining the project's objective, which is to improve the effectiveness of information disclosure in financial statements and associated notes. It then delves into the project's history, background, and current status, highlighting the FASB's goal of enhancing the clarity and conciseness of information communicated according to Generally Accepted Accounting Principles (GAAP). The report discusses the proposed changes in four key areas: fair value measurement, compensation-retirement benefits, income taxes, and inventory. It explains the rationale behind these changes, emphasizing the aim to make disclosures more effective, useful, and flexible while minimizing the volume of required information. The report further explores the effects of comments from entities and individuals on reporting requirements. A research log and annotated bibliography are included. Finally, the report assesses the impact of the proposed changes on relevant stakeholders, concluding with a summary of the project's implications.

Running head: INTERMEDIATE ACCOUNTING

Intermediate Accounting

Name of the Student

Name of the University

Author’s Note

Intermediate Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERMEDIATE ACCOUNTING

Executive Summary

The key purpose of this report is to provide description and other associated information on

the FASB’s project named Disclosure and Framework: Disclosures-Interim Reporting. The

outcome of the analysis of this report shows that increasing the effectiveness of disclosure of

information in the financial statements associated notes is the main aim of the Board to

introduce these changes. The main implication is that the introduction of these changes have

created both positive and negative impacts on the stakeholders associated with the business

organizations.

Executive Summary

The key purpose of this report is to provide description and other associated information on

the FASB’s project named Disclosure and Framework: Disclosures-Interim Reporting. The

outcome of the analysis of this report shows that increasing the effectiveness of disclosure of

information in the financial statements associated notes is the main aim of the Board to

introduce these changes. The main implication is that the introduction of these changes have

created both positive and negative impacts on the stakeholders associated with the business

organizations.

2INTERMEDIATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Project History, Background and Status....................................................................................3

Discussion on the Proposed Changes and Reason for Changes.................................................4

Effects of Comments on Reporting Requirements.....................................................................5

Research Log..............................................................................................................................5

Annotated Bibliography.............................................................................................................6

Relevant Stakeholders and the Impacts of Proposed Changes on each of Them.......................7

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Table of Contents

Introduction................................................................................................................................3

Project History, Background and Status....................................................................................3

Discussion on the Proposed Changes and Reason for Changes.................................................4

Effects of Comments on Reporting Requirements.....................................................................5

Research Log..............................................................................................................................5

Annotated Bibliography.............................................................................................................6

Relevant Stakeholders and the Impacts of Proposed Changes on each of Them.......................7

Conclusion..................................................................................................................................7

References..................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERMEDIATE ACCOUNTING

Introduction

The main aim of the Financial Accounting Standards Board (FASB) is the

establishment as well as improvement of the standards and practices of financial accounting

reporting for guiding and educating the public that includes financial standards issuers,

auditors, investors and others users of the financial statements. It is also the responsibility of

FASB to assess whether there is any need for the introduction of any financial reporting

standard for strengthening the practice of financial reporting. The presence of many ongoing

projects can be seen under the supervision of FASB. This report taken an honest attempt of

analyzing and evaluating the different aspects associated with one of the major ongoing

projects of FASB that is Disclosure and Framework: Disclosures-Interim Reporting. There

are certain objectives of this report. This report first discusses about the history, background

and status of this particular project of FASB. The next part discusses about the proposed

changes in the ongoing project along with the reason for recommending these changes. The

next parts discuses about the usefulness of SEC 10-K comments on this project. This report

also involves in preparing a research log and annotated bibliography. The last part discusses

about the impact of the proposed changes on different groups of relevant stakeholders of the

business organizations.

Project History, Background and Status

The main objective as well as main attention of this disclosure framework projects is

to bring improvement in the efficiency of disclosures in the financial statements associated

notes through the facilitation of clear and concise communication of the information needed

by Genially Accepted Accounting Principles (GAAP) and this GAAP has major importance

to the users of the financial statements of the business organizations (fasb.org, 2020).

A proposed concepts Statement of FASB was issued by the FASB, Conceptual

Framework for Financial Reporting – Chapter 8: Notes to Financial Statements on March 4,

2014. The same was finalized by the board on August 28, 2018 Chapter 8 of Concepts

Statements 8 and this identified a wide range of potential information in order to take into

account by the Board at the time to make decisions on the disclosure necessities for a specific

FASB Accounting Standards Codification Topic (fasb.org, 2020). From this wide set, a

narrower set of disclosure will be identified by the Board about that particular Topic that is

required based on the particular assessment and evaluation that whether the expected benefits

of the business organizations delivering the information provided adequate justification to the

expected costs. The main utilization of the Chapter 8 of Concepts Statement 8 can be seen by

the Board as a part of the procedure to establish the requirements of disclosure in the

accounting standards along with the assessment and evaluation of the present requirements of

disclosure in case and when those requirements are considered by the Board (fasb.org, 2020).

Prior to the finalization of the Chapter 8 of Concepts Statement 8, the Board took the

decision of testing the concepts in the proposed Chapter 8 and enhance the effectiveness of

the requirements of disclosure in four major topic. These topic are 1) Fair value measurement

that falls under Section 820-10-50, 2) Compensation-Retirement Benefits which can be seen

in Section 715-20-50, 3 Income taxes under Section 740-10-50 and 4) Inventory under

Section 330-10-50. In addition of these, the Board is assessing and evaluating the

requirements of interim requirements with the aim to modify them for increasing the overall

effectiveness of financial reporting (fasb.org, 2020).

The Board has taken the decision of adding high-value principle to Topic 270, Interim

Reporting, for the purpose of interim disclosure on the parts of SEC Regulations S-X that

were removed along with Rule 10-01, Interim Financial Statements. The Board has also taken

Introduction

The main aim of the Financial Accounting Standards Board (FASB) is the

establishment as well as improvement of the standards and practices of financial accounting

reporting for guiding and educating the public that includes financial standards issuers,

auditors, investors and others users of the financial statements. It is also the responsibility of

FASB to assess whether there is any need for the introduction of any financial reporting

standard for strengthening the practice of financial reporting. The presence of many ongoing

projects can be seen under the supervision of FASB. This report taken an honest attempt of

analyzing and evaluating the different aspects associated with one of the major ongoing

projects of FASB that is Disclosure and Framework: Disclosures-Interim Reporting. There

are certain objectives of this report. This report first discusses about the history, background

and status of this particular project of FASB. The next part discusses about the proposed

changes in the ongoing project along with the reason for recommending these changes. The

next parts discuses about the usefulness of SEC 10-K comments on this project. This report

also involves in preparing a research log and annotated bibliography. The last part discusses

about the impact of the proposed changes on different groups of relevant stakeholders of the

business organizations.

Project History, Background and Status

The main objective as well as main attention of this disclosure framework projects is

to bring improvement in the efficiency of disclosures in the financial statements associated

notes through the facilitation of clear and concise communication of the information needed

by Genially Accepted Accounting Principles (GAAP) and this GAAP has major importance

to the users of the financial statements of the business organizations (fasb.org, 2020).

A proposed concepts Statement of FASB was issued by the FASB, Conceptual

Framework for Financial Reporting – Chapter 8: Notes to Financial Statements on March 4,

2014. The same was finalized by the board on August 28, 2018 Chapter 8 of Concepts

Statements 8 and this identified a wide range of potential information in order to take into

account by the Board at the time to make decisions on the disclosure necessities for a specific

FASB Accounting Standards Codification Topic (fasb.org, 2020). From this wide set, a

narrower set of disclosure will be identified by the Board about that particular Topic that is

required based on the particular assessment and evaluation that whether the expected benefits

of the business organizations delivering the information provided adequate justification to the

expected costs. The main utilization of the Chapter 8 of Concepts Statement 8 can be seen by

the Board as a part of the procedure to establish the requirements of disclosure in the

accounting standards along with the assessment and evaluation of the present requirements of

disclosure in case and when those requirements are considered by the Board (fasb.org, 2020).

Prior to the finalization of the Chapter 8 of Concepts Statement 8, the Board took the

decision of testing the concepts in the proposed Chapter 8 and enhance the effectiveness of

the requirements of disclosure in four major topic. These topic are 1) Fair value measurement

that falls under Section 820-10-50, 2) Compensation-Retirement Benefits which can be seen

in Section 715-20-50, 3 Income taxes under Section 740-10-50 and 4) Inventory under

Section 330-10-50. In addition of these, the Board is assessing and evaluating the

requirements of interim requirements with the aim to modify them for increasing the overall

effectiveness of financial reporting (fasb.org, 2020).

The Board has taken the decision of adding high-value principle to Topic 270, Interim

Reporting, for the purpose of interim disclosure on the parts of SEC Regulations S-X that

were removed along with Rule 10-01, Interim Financial Statements. The Board has also taken

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERMEDIATE ACCOUNTING

the initiative of discussing the approach of the staffs towards the project and has provided

direction to the staffs that they need to perform research for the purpose of reassessing the

requirements of disclosure associated with interim reporting. As per current status of the

project, it needs to be mentioned that the staffs of the Board will develop a high-level

principle for interim reporting and will involve in performing research and outreach.

Moreover, as per the recent update on January 7, 2020, the project is in the stage of

preliminary negotiations; and the forthcoming stages include exposure draft, exposure

comment period, exposure draft re-deliberations and final standard. There is only one stage

that has been completed which is added to agenda (fasb.org, 2020).

Discussion on the Proposed Changes and Reason for Changes

As per the disclosure project, proposed changes will be brought in four areas which

are measurement of fair value, compensation – retirement plan, inventory and income taxes.

Measurement of Fair Value (Section 820-10-50) – There are four requirements of

disclosure that will be removed; they are the sum of and reason for transfer between Level 1

and Level 2 of the fair value order, the policy for transfer timing between levels, Level 3

valuation process and change in gains and losses for non-public entities that has not been

realized yet (fasb.org, 2020). Apart from this, there will be modification of three disclosure

requirements; they are disclosure requirement of a non-public entity regarding transfer into

and out of Level 3 fair value hierarchy, disclosure requirement of an entity of the timing of

insolvency of an investee’s assets along with the date of restriction from redemption and the

requirement for communicating information on the measurement uncertainty. The

requirements of disclosure that will be added include alterations in unrealized gains and

losses and the range as well as weighted average of major unobservable inputs (fasb.org,

2020).

Compensation—Retirement Benefits (Section 715-20-50) – There are six specific

disclosures that will be removed from the current standard; they are the amount of accrued

other comprehensive income predictable to be recognized, the amount and timing of plan

assets predictable to be returned to the employer, disclosure requirement associated with the

June 2001 alterations to the Japanese Welfare Pension Insurance Law, disclosures associated

with related party about the sum of future annual benefits, opening balance reconciliation of

plan assets measured for the non-public entities and the impact of 1% point change in

expected health care cost for public entities. The disclosures that will be added include the

weighted average interest crediting rates for each balance plans and a clarification of the

details for key gains and losses associated to the change in benefit plans (fasb.org, 2020).

Income taxes (Section 740-10-50) – There will be the addition of certain new disclosures for

all the entities; they are explanation of an enacted change in taxation law, income or loss

from continuing operation before the disaggregation of the payment of income tax expenses,

income tax expenses from continuing operation, disaggregation of the payment of income

taxes between domestic and foreign, an explanation of situations that are responsible for

changes in assertions about the identified investments and the aggregate of cash, marketable

securities and cash equivalent held by foreign subsidiaries. The disclosures that will be added

include settlements by using present deferred tax assets, the line items included in the

statement of financial position, the explanation on the amount of recognized valuation

allowance and the total amount of unrecognized tax benefits (fasb.org, 2020).

Inventory (Section 330-10-50) – There are certain additional disclosures that will be

required in the existing standard for the purpose of additional disclosure; they are

disaggregation of inventory by components, disaggregation of inventory by base of

the initiative of discussing the approach of the staffs towards the project and has provided

direction to the staffs that they need to perform research for the purpose of reassessing the

requirements of disclosure associated with interim reporting. As per current status of the

project, it needs to be mentioned that the staffs of the Board will develop a high-level

principle for interim reporting and will involve in performing research and outreach.

Moreover, as per the recent update on January 7, 2020, the project is in the stage of

preliminary negotiations; and the forthcoming stages include exposure draft, exposure

comment period, exposure draft re-deliberations and final standard. There is only one stage

that has been completed which is added to agenda (fasb.org, 2020).

Discussion on the Proposed Changes and Reason for Changes

As per the disclosure project, proposed changes will be brought in four areas which

are measurement of fair value, compensation – retirement plan, inventory and income taxes.

Measurement of Fair Value (Section 820-10-50) – There are four requirements of

disclosure that will be removed; they are the sum of and reason for transfer between Level 1

and Level 2 of the fair value order, the policy for transfer timing between levels, Level 3

valuation process and change in gains and losses for non-public entities that has not been

realized yet (fasb.org, 2020). Apart from this, there will be modification of three disclosure

requirements; they are disclosure requirement of a non-public entity regarding transfer into

and out of Level 3 fair value hierarchy, disclosure requirement of an entity of the timing of

insolvency of an investee’s assets along with the date of restriction from redemption and the

requirement for communicating information on the measurement uncertainty. The

requirements of disclosure that will be added include alterations in unrealized gains and

losses and the range as well as weighted average of major unobservable inputs (fasb.org,

2020).

Compensation—Retirement Benefits (Section 715-20-50) – There are six specific

disclosures that will be removed from the current standard; they are the amount of accrued

other comprehensive income predictable to be recognized, the amount and timing of plan

assets predictable to be returned to the employer, disclosure requirement associated with the

June 2001 alterations to the Japanese Welfare Pension Insurance Law, disclosures associated

with related party about the sum of future annual benefits, opening balance reconciliation of

plan assets measured for the non-public entities and the impact of 1% point change in

expected health care cost for public entities. The disclosures that will be added include the

weighted average interest crediting rates for each balance plans and a clarification of the

details for key gains and losses associated to the change in benefit plans (fasb.org, 2020).

Income taxes (Section 740-10-50) – There will be the addition of certain new disclosures for

all the entities; they are explanation of an enacted change in taxation law, income or loss

from continuing operation before the disaggregation of the payment of income tax expenses,

income tax expenses from continuing operation, disaggregation of the payment of income

taxes between domestic and foreign, an explanation of situations that are responsible for

changes in assertions about the identified investments and the aggregate of cash, marketable

securities and cash equivalent held by foreign subsidiaries. The disclosures that will be added

include settlements by using present deferred tax assets, the line items included in the

statement of financial position, the explanation on the amount of recognized valuation

allowance and the total amount of unrecognized tax benefits (fasb.org, 2020).

Inventory (Section 330-10-50) – There are certain additional disclosures that will be

required in the existing standard for the purpose of additional disclosure; they are

disaggregation of inventory by components, disaggregation of inventory by base of

5INTERMEDIATE ACCOUNTING

measurement, changes in the balances of inventory that have no relation with the purchase,

manufacture and sale of inventory, a qualitative explanation of the cost types that are

capitalized into inventory, the impacts of last-in, first-out (LIFO) liquidations on income and

the additional of the cost of LIFO inventory method (fasb.org, 2020).

Reason for the Change – The key reason for the introduction of the above-mentioned

changes is to bring improvement in the efficiency of disclosures in the financial statements

related notes for the public and private businesses along with the not-for-profit organizations.

Through the clear communication of information that has major importance to the users of

the financial statements, these changes make the disclosure more effective and useful. These

changes are allowing more discretion and flexibility in the application of present and future

relevant requirements for disclosure on the basis of the specific situations. At the same time,

these provide the business organizations with flexibility in the process of financial reporting.

Minimize the increased volume of necessary disclosure can be considered as another major

aim of these changes (fasb.org, 2020).

Effects of Comments on Reporting Requirements

Comment letters are the letters submitted by the entities and individuals in response to

the requests for public comment on the proposal of new accounting standards or the

amendments in financial standards. The main purpose of these comments can be seen in

providing assistance to the issuing company to make information in the registration statement

clear, free from irregularity and transparent before the final issue of the new financial

reporting standard or the amendments in an existing financial reporting standard. This same

can be seen in this particular FASB project of Disclosure and Framework associated with

interim reporting. For example, First Alliance Bank and The Commercial Bank of Grayson

commented on the project of Interim Disclosure about Fair Value of Financial Instrument.

First Alliance Bank did not support these amendments proposed by FASB on disclose of fair

value as they urged for more discussion regarding the issue (fasb.org, 2020). On the other

hand, The Commercial Bank of Grayson recommended to exempt the non-publicly traded

companies from this requirement on quarterly basis. Therefore, it can be seen that through the

issue of these comments, various individuals and organizations may request the board to

provide more supplemental information so that better understanding on the disclosures or

revised disclosures can be obtained. Therefore, it can be said that the comments have created

a positive impact on the projects of FASB (fasb.org, 2020).

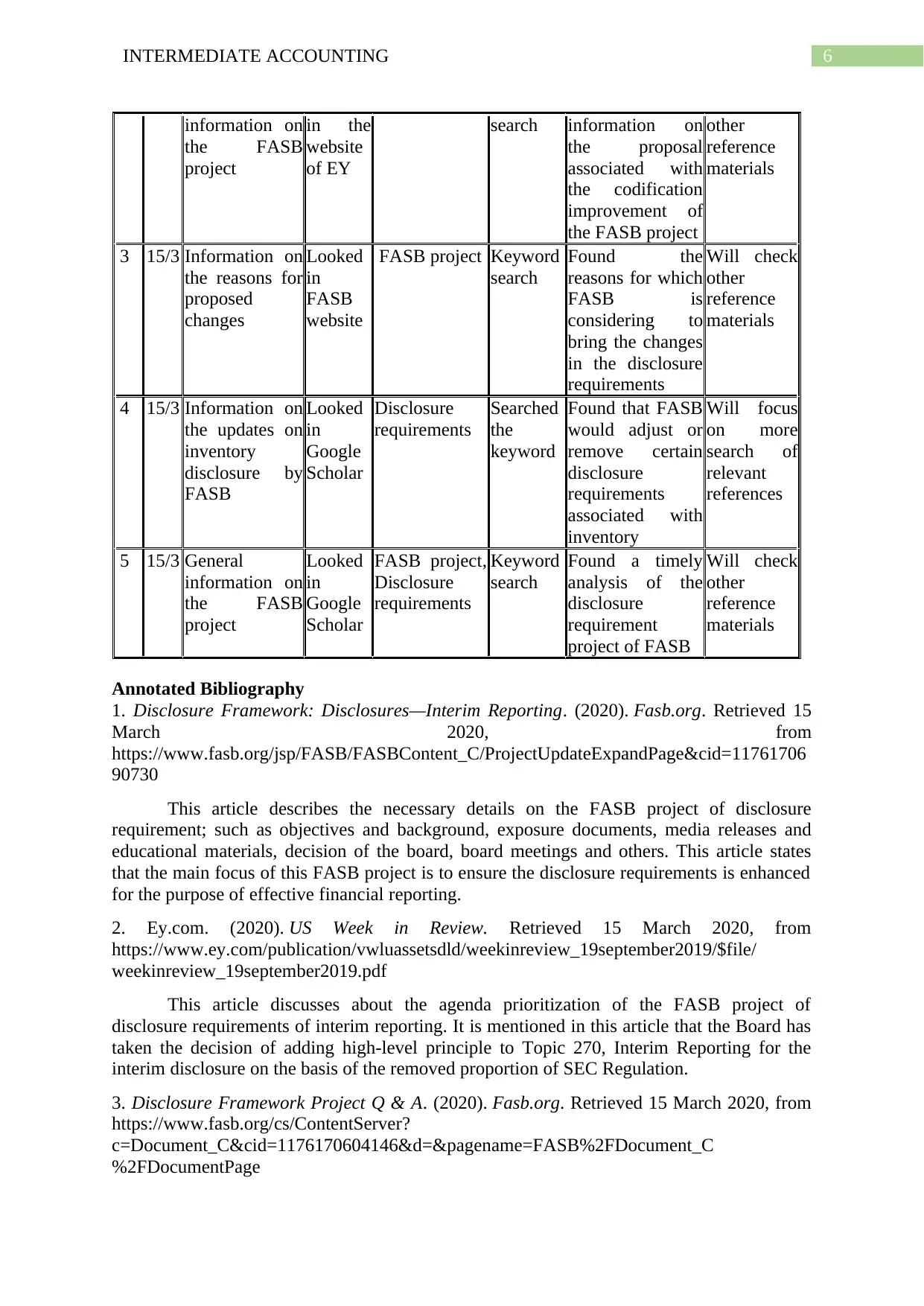

Research Log

No

.

Dat

e

Question

Pursuing,

Information

Sought,

Rationale for

Search

Tool or

Source

Used

Concepts or

Keywords,

Terms,

Phrases

Search

Strategy

Results Decision,

Action,

Next Step

1 15/3 History and

background of

the project

Looked

in

FASB

website

Interim

reporting,

disclosure

requirement

Keyword

search

Found

information on

the objective,

history,

background and

current status of

the project

Will check

other

references

2 15/3 General Looked FASB project Keyword Found Will check

measurement, changes in the balances of inventory that have no relation with the purchase,

manufacture and sale of inventory, a qualitative explanation of the cost types that are

capitalized into inventory, the impacts of last-in, first-out (LIFO) liquidations on income and

the additional of the cost of LIFO inventory method (fasb.org, 2020).

Reason for the Change – The key reason for the introduction of the above-mentioned

changes is to bring improvement in the efficiency of disclosures in the financial statements

related notes for the public and private businesses along with the not-for-profit organizations.

Through the clear communication of information that has major importance to the users of

the financial statements, these changes make the disclosure more effective and useful. These

changes are allowing more discretion and flexibility in the application of present and future

relevant requirements for disclosure on the basis of the specific situations. At the same time,

these provide the business organizations with flexibility in the process of financial reporting.

Minimize the increased volume of necessary disclosure can be considered as another major

aim of these changes (fasb.org, 2020).

Effects of Comments on Reporting Requirements

Comment letters are the letters submitted by the entities and individuals in response to

the requests for public comment on the proposal of new accounting standards or the

amendments in financial standards. The main purpose of these comments can be seen in

providing assistance to the issuing company to make information in the registration statement

clear, free from irregularity and transparent before the final issue of the new financial

reporting standard or the amendments in an existing financial reporting standard. This same

can be seen in this particular FASB project of Disclosure and Framework associated with

interim reporting. For example, First Alliance Bank and The Commercial Bank of Grayson

commented on the project of Interim Disclosure about Fair Value of Financial Instrument.

First Alliance Bank did not support these amendments proposed by FASB on disclose of fair

value as they urged for more discussion regarding the issue (fasb.org, 2020). On the other

hand, The Commercial Bank of Grayson recommended to exempt the non-publicly traded

companies from this requirement on quarterly basis. Therefore, it can be seen that through the

issue of these comments, various individuals and organizations may request the board to

provide more supplemental information so that better understanding on the disclosures or

revised disclosures can be obtained. Therefore, it can be said that the comments have created

a positive impact on the projects of FASB (fasb.org, 2020).

Research Log

No

.

Dat

e

Question

Pursuing,

Information

Sought,

Rationale for

Search

Tool or

Source

Used

Concepts or

Keywords,

Terms,

Phrases

Search

Strategy

Results Decision,

Action,

Next Step

1 15/3 History and

background of

the project

Looked

in

FASB

website

Interim

reporting,

disclosure

requirement

Keyword

search

Found

information on

the objective,

history,

background and

current status of

the project

Will check

other

references

2 15/3 General Looked FASB project Keyword Found Will check

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERMEDIATE ACCOUNTING

information on

the FASB

project

in the

website

of EY

search information on

the proposal

associated with

the codification

improvement of

the FASB project

other

reference

materials

3 15/3 Information on

the reasons for

proposed

changes

Looked

in

FASB

website

FASB project Keyword

search

Found the

reasons for which

FASB is

considering to

bring the changes

in the disclosure

requirements

Will check

other

reference

materials

4 15/3 Information on

the updates on

inventory

disclosure by

FASB

Looked

in

Google

Scholar

Disclosure

requirements

Searched

the

keyword

Found that FASB

would adjust or

remove certain

disclosure

requirements

associated with

inventory

Will focus

on more

search of

relevant

references

5 15/3 General

information on

the FASB

project

Looked

in

Google

Scholar

FASB project,

Disclosure

requirements

Keyword

search

Found a timely

analysis of the

disclosure

requirement

project of FASB

Will check

other

reference

materials

Annotated Bibliography

1. Disclosure Framework: Disclosures—Interim Reporting. (2020). Fasb.org. Retrieved 15

March 2020, from

https://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdateExpandPage&cid=11761706

90730

This article describes the necessary details on the FASB project of disclosure

requirement; such as objectives and background, exposure documents, media releases and

educational materials, decision of the board, board meetings and others. This article states

that the main focus of this FASB project is to ensure the disclosure requirements is enhanced

for the purpose of effective financial reporting.

2. Ey.com. (2020). US Week in Review. Retrieved 15 March 2020, from

https://www.ey.com/publication/vwluassetsdld/weekinreview_19september2019/$file/

weekinreview_19september2019.pdf

This article discusses about the agenda prioritization of the FASB project of

disclosure requirements of interim reporting. It is mentioned in this article that the Board has

taken the decision of adding high-level principle to Topic 270, Interim Reporting for the

interim disclosure on the basis of the removed proportion of SEC Regulation.

3. Disclosure Framework Project Q & A. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=Document_C&cid=1176170604146&d=&pagename=FASB%2FDocument_C

%2FDocumentPage

information on

the FASB

project

in the

website

of EY

search information on

the proposal

associated with

the codification

improvement of

the FASB project

other

reference

materials

3 15/3 Information on

the reasons for

proposed

changes

Looked

in

FASB

website

FASB project Keyword

search

Found the

reasons for which

FASB is

considering to

bring the changes

in the disclosure

requirements

Will check

other

reference

materials

4 15/3 Information on

the updates on

inventory

disclosure by

FASB

Looked

in

Scholar

Disclosure

requirements

Searched

the

keyword

Found that FASB

would adjust or

remove certain

disclosure

requirements

associated with

inventory

Will focus

on more

search of

relevant

references

5 15/3 General

information on

the FASB

project

Looked

in

Scholar

FASB project,

Disclosure

requirements

Keyword

search

Found a timely

analysis of the

disclosure

requirement

project of FASB

Will check

other

reference

materials

Annotated Bibliography

1. Disclosure Framework: Disclosures—Interim Reporting. (2020). Fasb.org. Retrieved 15

March 2020, from

https://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdateExpandPage&cid=11761706

90730

This article describes the necessary details on the FASB project of disclosure

requirement; such as objectives and background, exposure documents, media releases and

educational materials, decision of the board, board meetings and others. This article states

that the main focus of this FASB project is to ensure the disclosure requirements is enhanced

for the purpose of effective financial reporting.

2. Ey.com. (2020). US Week in Review. Retrieved 15 March 2020, from

https://www.ey.com/publication/vwluassetsdld/weekinreview_19september2019/$file/

weekinreview_19september2019.pdf

This article discusses about the agenda prioritization of the FASB project of

disclosure requirements of interim reporting. It is mentioned in this article that the Board has

taken the decision of adding high-level principle to Topic 270, Interim Reporting for the

interim disclosure on the basis of the removed proportion of SEC Regulation.

3. Disclosure Framework Project Q & A. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=Document_C&cid=1176170604146&d=&pagename=FASB%2FDocument_C

%2FDocumentPage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERMEDIATE ACCOUNTING

This article describes the main reasons and motives of the FASB Board for bringing

the amendments in the disclosure requirements. This article also discusses about the decision

process of Board related to these disclosure requirements. This also discusses about the

volume of the financial statement disclosures.

4. Orrell, M., & Tian-Lee, J. (2012). Accounting Roundup.

This article describes the proposed updates of the FASB Board to the disclosure

requirements of inventory. As per this article, FASB discusses about the proposed

modification or elimination of certain requirements of disclosure associated with inventory

with the aim to establish new requirements.

5. Bakarich, K. M., Hossain, M., & Weintrop, J. (2019). Different time, different tone:

Company life cycle. Journal of Contemporary Accounting & Economics, 15(1), 69-86.

This particular article provides an appropriate assessment of the disclosure

requirements of FASB Board related to Disclosure Framework Project which aim in

increasing the overall effectiveness of the financial reporting mechanism of the business

organizations. This also facilitates in better communication of the financial information of the

companies through the financial statements.

Relevant Stakeholders and the Impacts of Proposed Changes on each of Them

There are different stakeholder groups that will be impacted by the proposed changes

in the disclosure requirements of interim reporting by FASB. They are as below:

Board of Directors – The Board of Directors of the companies will be impacted as they will

be necessary for adhering to the new requirements which will consume both effort and

financial resources.

Investors – The investors will be beneficial as they will be able in obtaining more accurate

and precise financial information of the companies on timely manner which will be helpful in

investment decision-making process (Ferretti, 2016).

Banks and other Financial Institutions – Bank and other financial institutions will be

negatively affects as they will have to bear additional costs for providing additional

information through disclosure requirements.

Auditors – The auditors will be beneficial as disclosure requirements under interim reporting

would lead to provide more information to the auditors that will be helpful in audit

engagement in the audit client organizations.

Small Organizations – This will not be beneficial for the small business organizations as the

provision for interim reporting would cost them more in the absence of any additional

benefits. This would affect their financial reporting related operations (Ferretti, 2016).

Conclusion

It can be seen from the above analysis that the main aim of the FASB project of

disclosure requirement of interim reporting is to enhance efficiency of disclosures in the

financial statements related notes. There are four areas where the proposed additions or

eliminations in disclosure requirements will be applied; they are fair value measurement,

compensation and retirement benefits, income taxes and inventory. The above discussion also

shows that reduction in the volume of disclosures in financial reporting is another crucial

reason for these changes in the existing standards. There are certain stakeholders who will be

impacted by the introduction of these changes related to disclosure requirements; they are

This article describes the main reasons and motives of the FASB Board for bringing

the amendments in the disclosure requirements. This article also discusses about the decision

process of Board related to these disclosure requirements. This also discusses about the

volume of the financial statement disclosures.

4. Orrell, M., & Tian-Lee, J. (2012). Accounting Roundup.

This article describes the proposed updates of the FASB Board to the disclosure

requirements of inventory. As per this article, FASB discusses about the proposed

modification or elimination of certain requirements of disclosure associated with inventory

with the aim to establish new requirements.

5. Bakarich, K. M., Hossain, M., & Weintrop, J. (2019). Different time, different tone:

Company life cycle. Journal of Contemporary Accounting & Economics, 15(1), 69-86.

This particular article provides an appropriate assessment of the disclosure

requirements of FASB Board related to Disclosure Framework Project which aim in

increasing the overall effectiveness of the financial reporting mechanism of the business

organizations. This also facilitates in better communication of the financial information of the

companies through the financial statements.

Relevant Stakeholders and the Impacts of Proposed Changes on each of Them

There are different stakeholder groups that will be impacted by the proposed changes

in the disclosure requirements of interim reporting by FASB. They are as below:

Board of Directors – The Board of Directors of the companies will be impacted as they will

be necessary for adhering to the new requirements which will consume both effort and

financial resources.

Investors – The investors will be beneficial as they will be able in obtaining more accurate

and precise financial information of the companies on timely manner which will be helpful in

investment decision-making process (Ferretti, 2016).

Banks and other Financial Institutions – Bank and other financial institutions will be

negatively affects as they will have to bear additional costs for providing additional

information through disclosure requirements.

Auditors – The auditors will be beneficial as disclosure requirements under interim reporting

would lead to provide more information to the auditors that will be helpful in audit

engagement in the audit client organizations.

Small Organizations – This will not be beneficial for the small business organizations as the

provision for interim reporting would cost them more in the absence of any additional

benefits. This would affect their financial reporting related operations (Ferretti, 2016).

Conclusion

It can be seen from the above analysis that the main aim of the FASB project of

disclosure requirement of interim reporting is to enhance efficiency of disclosures in the

financial statements related notes. There are four areas where the proposed additions or

eliminations in disclosure requirements will be applied; they are fair value measurement,

compensation and retirement benefits, income taxes and inventory. The above discussion also

shows that reduction in the volume of disclosures in financial reporting is another crucial

reason for these changes in the existing standards. There are certain stakeholders who will be

impacted by the introduction of these changes related to disclosure requirements; they are

8INTERMEDIATE ACCOUNTING

Board of Directors, investors, banks and other financial institutions, auditors and small

business organizations.

Board of Directors, investors, banks and other financial institutions, auditors and small

business organizations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERMEDIATE ACCOUNTING

References

Bakarich, K. M., Hossain, M., & Weintrop, J. (2019). Different time, different tone:

Company life cycle. Journal of Contemporary Accounting & Economics, 15(1), 69-

86.

Disclosure Framework Project Q & A. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=Document_C&cid=1176170604146&d=&pagename=FASB%2FDocument_C

%2FDocumentPage

Disclosure Framework: Disclosures—Interim Reporting. (2020). Fasb.org. Retrieved 15

March 2020, from

https://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdateExpandPage&cid=11

76170690730

Disclosure Framework—Disclosure Review: Defined Benefit Plans (Post Issuance

Summary). (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179028&d=&pagename=FASB

%2FFASBContent_C%2FCompletedProjectPage

Disclosure Framework—Disclosure Review: Fair Value Measurement (Post- Issuance

Summary. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179766&d=&pagename=FASB

%2FFASBContent_C%2FCompletedProjectPage

Ey.com. (2020). US Week in Review. Retrieved 15 March 2020, from

https://www.ey.com/publication/vwluassetsdld/weekinreview_19september2019/$file

/weekinreview_19september2019.pdf

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818340673&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=50818&blobheadervalue1=filename

%3D53594.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818341181&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=72377&blobheadervalue1=filename

%3D53617.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818463699&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=15801&blobheadervalue1=filename

%3D53573.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818463588&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

References

Bakarich, K. M., Hossain, M., & Weintrop, J. (2019). Different time, different tone:

Company life cycle. Journal of Contemporary Accounting & Economics, 15(1), 69-

86.

Disclosure Framework Project Q & A. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=Document_C&cid=1176170604146&d=&pagename=FASB%2FDocument_C

%2FDocumentPage

Disclosure Framework: Disclosures—Interim Reporting. (2020). Fasb.org. Retrieved 15

March 2020, from

https://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdateExpandPage&cid=11

76170690730

Disclosure Framework—Disclosure Review: Defined Benefit Plans (Post Issuance

Summary). (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179028&d=&pagename=FASB

%2FFASBContent_C%2FCompletedProjectPage

Disclosure Framework—Disclosure Review: Fair Value Measurement (Post- Issuance

Summary. (2020). Fasb.org. Retrieved 15 March 2020, from

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179766&d=&pagename=FASB

%2FFASBContent_C%2FCompletedProjectPage

Ey.com. (2020). US Week in Review. Retrieved 15 March 2020, from

https://www.ey.com/publication/vwluassetsdld/weekinreview_19september2019/$file

/weekinreview_19september2019.pdf

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818340673&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=50818&blobheadervalue1=filename

%3D53594.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818341181&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=72377&blobheadervalue1=filename

%3D53617.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818463699&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=15801&blobheadervalue1=filename

%3D53573.pdf&blobcol=urldata&blobtable=MungoBlobs

Fasb.org. (2020). Retrieved 15 March 2020, from https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175818463588&blobheader=applicatio

n%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERMEDIATE ACCOUNTING

Disposition&blobheadervalue2=36811&blobheadervalue1=filename

%3D53569.pdf&blobcol=urldata&blobtable=MungoBlobs

Ferretti, V. (2016). From stakeholders analysis to cognitive mapping and Multi-Attribute

Value Theory: An integrated approach for policy support. European Journal of

Operational Research, 253(2), 524-541.

Orrell, M., & Tian-Lee, J. (2012). Accounting Roundup.

Proposed Accounting Standards Update—Inventory (Topic 330): Disclosure Framework—

Changes to the Disclosure Requirements for Inventory. (2020). Fasb.org. Retrieved 15

March 2020, from https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176168748657&acceptedDisclaimer=true

Proposed ASU—Income Taxes (Topic 740) Disclosure Framework—Changes to the

Disclosure Requirements for Income Taxes. (2020). Fasb.org. Retrieved 15 March

2020, from https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176168335332&acceptedDisclaimer=true

Disposition&blobheadervalue2=36811&blobheadervalue1=filename

%3D53569.pdf&blobcol=urldata&blobtable=MungoBlobs

Ferretti, V. (2016). From stakeholders analysis to cognitive mapping and Multi-Attribute

Value Theory: An integrated approach for policy support. European Journal of

Operational Research, 253(2), 524-541.

Orrell, M., & Tian-Lee, J. (2012). Accounting Roundup.

Proposed Accounting Standards Update—Inventory (Topic 330): Disclosure Framework—

Changes to the Disclosure Requirements for Inventory. (2020). Fasb.org. Retrieved 15

March 2020, from https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176168748657&acceptedDisclaimer=true

Proposed ASU—Income Taxes (Topic 740) Disclosure Framework—Changes to the

Disclosure Requirements for Income Taxes. (2020). Fasb.org. Retrieved 15 March

2020, from https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176168335332&acceptedDisclaimer=true

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.