International Commerce Project: Fashion from Spain Sales Strategy

VerifiedAdded on 2023/05/30

|9

|1640

|160

Project

AI Summary

This project analyzes the global sales strategy for "Fashion from Spain", focusing on exporting fashion wear from Spain to Germany, Poland, and the United States. The project begins with a DAFO analysis (Strengths, Weaknesses, Opportunities, and Threats) of each target country, examining tax barriers, export regulations, and market entry challenges. It further details logistics and supply chain strategies, including transportation options and payment guarantees. The assignment also presents a financial plan, including sales and cash flow forecasts, and a depreciation schedule. The project concludes with a personalized advantage for the proposed model, emphasizing expansion into the United States and a detailed financial analysis to support the strategy. References to relevant sources are provided, and appendixes include detailed financial plans.

Running head: FINANCE/ INTERNATIONAL COMMERCE

International Commerce

Name of the Student

Name of the University

Author’s Note

International Commerce

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL COMMERCE

Table of Contents

Introduction..........................................................................................................................2

Global Sales strategy from Fashion from Spain..................................................................2

Taxes, barriers, to export, pros and cons per country......................................................2

Logistics and Supply Chain Strategy...............................................................................3

Guarantee service and payments.....................................................................................3

Supply Strategy of the company..........................................................................................3

Financing.............................................................................................................................3

Economic Targets and Turnover.........................................................................................3

Personalized advantage to the proposed model...................................................................4

Conclusion...........................................................................................................................4

References............................................................................................................................5

List of Appendix..................................................................................................................7

Table of Contents

Introduction..........................................................................................................................2

Global Sales strategy from Fashion from Spain..................................................................2

Taxes, barriers, to export, pros and cons per country......................................................2

Logistics and Supply Chain Strategy...............................................................................3

Guarantee service and payments.....................................................................................3

Supply Strategy of the company..........................................................................................3

Financing.............................................................................................................................3

Economic Targets and Turnover.........................................................................................3

Personalized advantage to the proposed model...................................................................4

Conclusion...........................................................................................................................4

References............................................................................................................................5

List of Appendix..................................................................................................................7

2INTERNATIONAL COMMERCE

Introduction

Fashion from Spain will export fashion wears from Spain to Deutschland and Poland in

Europe. The non-European nation selected for the study is U.S. The overall discussions of the

study will be based on developing a DAFO analysis. This analysis will compose of depicting the

strength, weakness, opportunities and threats of the selected countries.

Global Sales strategy from Fashion from Spain

Taxes, barriers, to export, pros and cons per country

The tax barriers in Germany is identified with few restrictions however the business is

well regulated by adherence to the legal requirement. In terms of taxes the country has a complex

tax laws for avoiding the critical errors. However, this business is seen with considering the

possible deductions and write-offs during the export. The main barriers need to be considered

with challenge relating to the tax and legal structures (World Business Culture 2018).

Poland on the other hand is depicted with dramatic transformation which are related to

the FDI and rapid globalization across the central European states. Between the period of 2004-

2013, the FDI in Poland was seen to be higher than three times in compare to 1989 to 2003. The

application of the tax barriers in the country is further depicted to be evident with retroactive

bank tax and a range of other levies.

The trade barriers in the U.S. are evident with the increase in the price and reduction in

the available quantities of the services and goods. Despite of this, the increasing measures of the

trade flows are the indicators of the positive economic health. In addition to this, production and

exchange with the country will be able to generate increased revenues. Moreover, the highest

Introduction

Fashion from Spain will export fashion wears from Spain to Deutschland and Poland in

Europe. The non-European nation selected for the study is U.S. The overall discussions of the

study will be based on developing a DAFO analysis. This analysis will compose of depicting the

strength, weakness, opportunities and threats of the selected countries.

Global Sales strategy from Fashion from Spain

Taxes, barriers, to export, pros and cons per country

The tax barriers in Germany is identified with few restrictions however the business is

well regulated by adherence to the legal requirement. In terms of taxes the country has a complex

tax laws for avoiding the critical errors. However, this business is seen with considering the

possible deductions and write-offs during the export. The main barriers need to be considered

with challenge relating to the tax and legal structures (World Business Culture 2018).

Poland on the other hand is depicted with dramatic transformation which are related to

the FDI and rapid globalization across the central European states. Between the period of 2004-

2013, the FDI in Poland was seen to be higher than three times in compare to 1989 to 2003. The

application of the tax barriers in the country is further depicted to be evident with retroactive

bank tax and a range of other levies.

The trade barriers in the U.S. are evident with the increase in the price and reduction in

the available quantities of the services and goods. Despite of this, the increasing measures of the

trade flows are the indicators of the positive economic health. In addition to this, production and

exchange with the country will be able to generate increased revenues. Moreover, the highest

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL COMMERCE

tariff in the country are evident with the products such as agriculture, textiles, and footwear.

Hence, in terms of the fashion wear the company has increased scope of operations.

Logistics and Supply Chain Strategy

The logistics requirement in Deutschland and Poland can be accommodated with Rail,

Road and Air transportation. However, the in the Non-European country the most suitable mode

of transportation is shipping. The available shipping options needs to be considered with the

United Parcel Service of America Inc., FedEx Corporation, Hapag-Lloyd., COSCO, Hanjin.,

NYK Line and CMA CGM (Austrade.gov.au 2018).

Guarantee service and payments

The guarantees pertaining to the EU rules needs to be identified with good or a service

online provided can be cancelled and returned within 14 days (Your Europe – Citizens 2018). On

the contrary, the guarantee for the service payment are more flexible in U.S., which may go up to

3 months in case payment is postponed (Tax Foundation 2018).

Supply Strategy of the company

The Lead time and possible cost for the individual countries are stated as follows:

Deutschland- 30 Days, $ 190,000

Poland-30 Days, $ 228,000

U.S.- 45 Days, $ 120,000

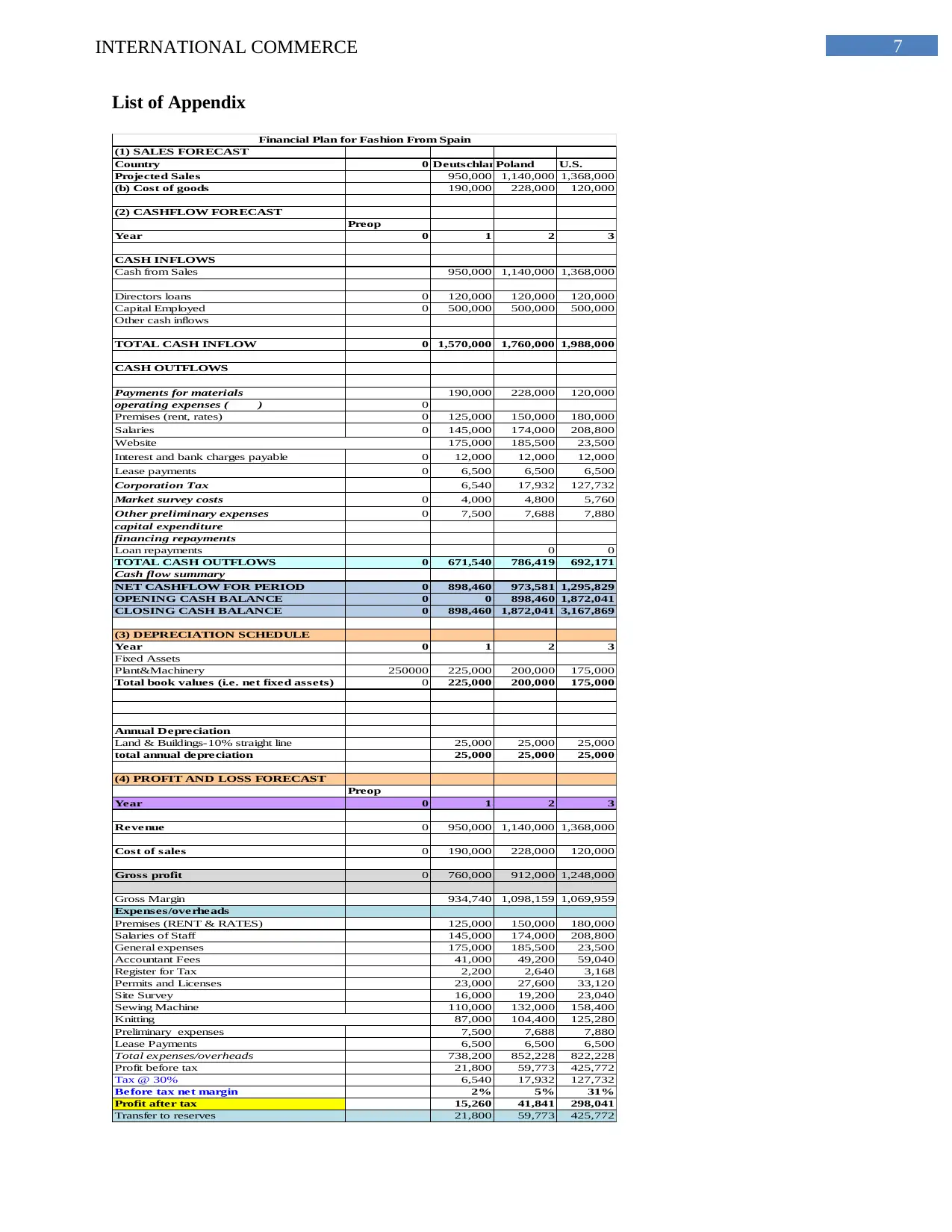

Financing

Refer to appendix

tariff in the country are evident with the products such as agriculture, textiles, and footwear.

Hence, in terms of the fashion wear the company has increased scope of operations.

Logistics and Supply Chain Strategy

The logistics requirement in Deutschland and Poland can be accommodated with Rail,

Road and Air transportation. However, the in the Non-European country the most suitable mode

of transportation is shipping. The available shipping options needs to be considered with the

United Parcel Service of America Inc., FedEx Corporation, Hapag-Lloyd., COSCO, Hanjin.,

NYK Line and CMA CGM (Austrade.gov.au 2018).

Guarantee service and payments

The guarantees pertaining to the EU rules needs to be identified with good or a service

online provided can be cancelled and returned within 14 days (Your Europe – Citizens 2018). On

the contrary, the guarantee for the service payment are more flexible in U.S., which may go up to

3 months in case payment is postponed (Tax Foundation 2018).

Supply Strategy of the company

The Lead time and possible cost for the individual countries are stated as follows:

Deutschland- 30 Days, $ 190,000

Poland-30 Days, $ 228,000

U.S.- 45 Days, $ 120,000

Financing

Refer to appendix

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL COMMERCE

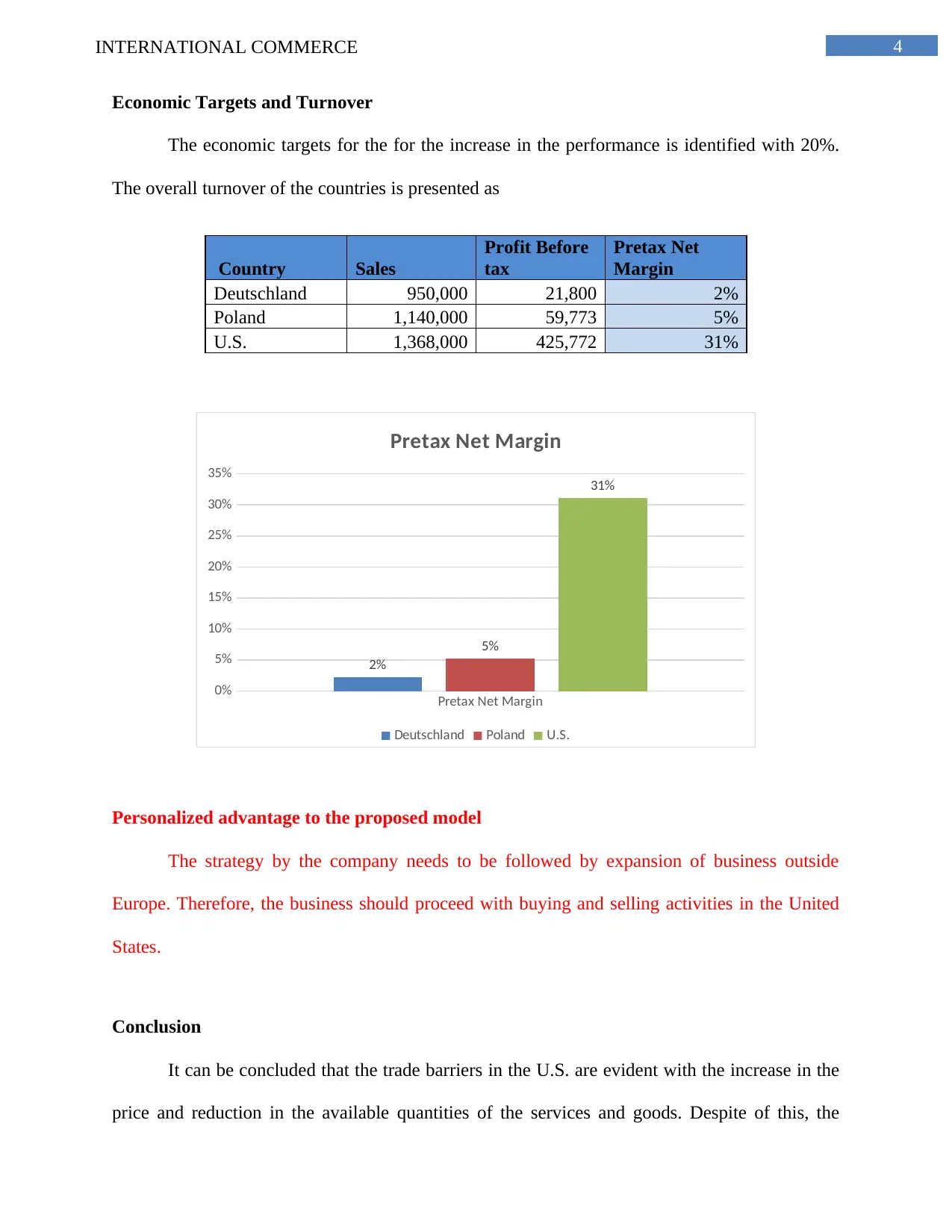

Economic Targets and Turnover

The economic targets for the for the increase in the performance is identified with 20%.

The overall turnover of the countries is presented as

Country Sales

Profit Before

tax

Pretax Net

Margin

Deutschland 950,000 21,800 2%

Poland 1,140,000 59,773 5%

U.S. 1,368,000 425,772 31%

Pretax Net Margin

0%

5%

10%

15%

20%

25%

30%

35%

2%

5%

31%

Pretax Net Margin

Deutschland Poland U.S.

Personalized advantage to the proposed model

The strategy by the company needs to be followed by expansion of business outside

Europe. Therefore, the business should proceed with buying and selling activities in the United

States.

Conclusion

It can be concluded that the trade barriers in the U.S. are evident with the increase in the

price and reduction in the available quantities of the services and goods. Despite of this, the

Economic Targets and Turnover

The economic targets for the for the increase in the performance is identified with 20%.

The overall turnover of the countries is presented as

Country Sales

Profit Before

tax

Pretax Net

Margin

Deutschland 950,000 21,800 2%

Poland 1,140,000 59,773 5%

U.S. 1,368,000 425,772 31%

Pretax Net Margin

0%

5%

10%

15%

20%

25%

30%

35%

2%

5%

31%

Pretax Net Margin

Deutschland Poland U.S.

Personalized advantage to the proposed model

The strategy by the company needs to be followed by expansion of business outside

Europe. Therefore, the business should proceed with buying and selling activities in the United

States.

Conclusion

It can be concluded that the trade barriers in the U.S. are evident with the increase in the

price and reduction in the available quantities of the services and goods. Despite of this, the

5INTERNATIONAL COMMERCE

increasing measures of the trade flows are the indicators of the positive economic health. In

addition to this, the expansion of the business in the U.S. will to higher customer and revenue.

The buying and selling of the fashion wears should be proceeded in the U.S.

References

Austrade.gov.au. (2018). Doing business - Tariffs and regulations – United States of America –

For Australian exporters - Austrade . [online] Available at:

https://www.austrade.gov.au/Australian/Export/Export-markets/Countries/United-States-of-

America/Doing-business/Tariffs-and-regulations [Accessed 23 Nov. 2018].

Tax Foundation. (2018). The Impact of Trade and Tariffs on the United States | Tax Foundation.

[online] Available at: https://taxfoundation.org/impact-trade-tariffs-united-states/ [Accessed 23

Nov. 2018].

World Business Culture. 2018. Barriers to Entry in Germany | World Business Culture. [online]

Available at: https://www.worldbusinessculture.com/country-profiles/germany/market-entry/

barriers-to-entry/ [Accessed 23 Nov. 2018].

Your Europe - Citizens. 2018. Guarantees: repairs, replacements, refunds. [online] Available at:

https://europa.eu/youreurope/citizens/consumers/shopping/guarantees-returns/index_en.htm

[Accessed 23 Nov. 2018].

increasing measures of the trade flows are the indicators of the positive economic health. In

addition to this, the expansion of the business in the U.S. will to higher customer and revenue.

The buying and selling of the fashion wears should be proceeded in the U.S.

References

Austrade.gov.au. (2018). Doing business - Tariffs and regulations – United States of America –

For Australian exporters - Austrade . [online] Available at:

https://www.austrade.gov.au/Australian/Export/Export-markets/Countries/United-States-of-

America/Doing-business/Tariffs-and-regulations [Accessed 23 Nov. 2018].

Tax Foundation. (2018). The Impact of Trade and Tariffs on the United States | Tax Foundation.

[online] Available at: https://taxfoundation.org/impact-trade-tariffs-united-states/ [Accessed 23

Nov. 2018].

World Business Culture. 2018. Barriers to Entry in Germany | World Business Culture. [online]

Available at: https://www.worldbusinessculture.com/country-profiles/germany/market-entry/

barriers-to-entry/ [Accessed 23 Nov. 2018].

Your Europe - Citizens. 2018. Guarantees: repairs, replacements, refunds. [online] Available at:

https://europa.eu/youreurope/citizens/consumers/shopping/guarantees-returns/index_en.htm

[Accessed 23 Nov. 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL COMMERCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL COMMERCE

List of Appendix

(1) SALES FORECAST

Country 0 DeutschlandPoland U.S.

Projected Sales 950,000 1,140,000 1,368,000

(b) Cost of goods 190,000 228,000 120,000

(2) CASHFLOW FORECAST

Preop

Year 0 1 2 3

CASH INFLOWS

Cash from Sales 950,000 1,140,000 1,368,000

Directors loans 0 120,000 120,000 120,000

Capital Employed 0 500,000 500,000 500,000

Other cash inflows

TOTAL CASH INFLOW 0 1,570,000 1,760,000 1,988,000

CASH OUTFLOWS

Payments for materials 190,000 228,000 120,000

operating expenses ( ) 0

Premises (rent, rates) 0 125,000 150,000 180,000

Salaries 0 145,000 174,000 208,800

175,000 185,500 23,500

Interest and bank charges payable 0 12,000 12,000 12,000

Lease payments 0 6,500 6,500 6,500

Corporation Tax 6,540 17,932 127,732

Market survey costs 0 4,000 4,800 5,760

Other preliminary expenses 0 7,500 7,688 7,880

capital expenditure

financing repayments

Loan repayments 0 0

TOTAL CASH OUTFLOWS 0 671,540 786,419 692,171

Cash flow summary

NET CASHFLOW FOR PERIOD 0 898,460 973,581 1,295,829

OPENING CASH BALANCE 0 0 898,460 1,872,041

CLOSING CASH BALANCE 0 898,460 1,872,041 3,167,869

(3) DEPRECIATION SCHEDULE

Year 0 1 2 3

Fixed Assets

Plant&Machinery 250000 225,000 200,000 175,000

Total book values (i.e. net fixed assets) 0 225,000 200,000 175,000

Annual Depreciation

Land & Buildings-10% straight line 25,000 25,000 25,000

total annual depreciation 25,000 25,000 25,000

(4) PROFIT AND LOSS FORECAST

Preop

Year 0 1 2 3

Revenue 0 950,000 1,140,000 1,368,000

Cost of sales 0 190,000 228,000 120,000

Gross profit 0 760,000 912,000 1,248,000

Gross Margin 934,740 1,098,159 1,069,959

Expenses/overheads

Premises (RENT & RATES) 125,000 150,000 180,000

Salaries of Staff 145,000 174,000 208,800

General expenses 175,000 185,500 23,500

Accountant Fees 41,000 49,200 59,040

Register for Tax 2,200 2,640 3,168

Permits and Licenses 23,000 27,600 33,120

Site Survey 16,000 19,200 23,040

Sewing Machine 110,000 132,000 158,400

87,000 104,400 125,280

Preliminary expenses 7,500 7,688 7,880

Lease Payments 6,500 6,500 6,500

Total expenses/overheads 738,200 852,228 822,228

Profit before tax 21,800 59,773 425,772

Tax @ 30% 6,540 17,932 127,732

Before tax net margin 2% 5% 31%

Profit after tax 15,260 41,841 298,041

Transfer to reserves 21,800 59,773 425,772

Website

Knitting

Financial Plan for Fashion From Spain

List of Appendix

(1) SALES FORECAST

Country 0 DeutschlandPoland U.S.

Projected Sales 950,000 1,140,000 1,368,000

(b) Cost of goods 190,000 228,000 120,000

(2) CASHFLOW FORECAST

Preop

Year 0 1 2 3

CASH INFLOWS

Cash from Sales 950,000 1,140,000 1,368,000

Directors loans 0 120,000 120,000 120,000

Capital Employed 0 500,000 500,000 500,000

Other cash inflows

TOTAL CASH INFLOW 0 1,570,000 1,760,000 1,988,000

CASH OUTFLOWS

Payments for materials 190,000 228,000 120,000

operating expenses ( ) 0

Premises (rent, rates) 0 125,000 150,000 180,000

Salaries 0 145,000 174,000 208,800

175,000 185,500 23,500

Interest and bank charges payable 0 12,000 12,000 12,000

Lease payments 0 6,500 6,500 6,500

Corporation Tax 6,540 17,932 127,732

Market survey costs 0 4,000 4,800 5,760

Other preliminary expenses 0 7,500 7,688 7,880

capital expenditure

financing repayments

Loan repayments 0 0

TOTAL CASH OUTFLOWS 0 671,540 786,419 692,171

Cash flow summary

NET CASHFLOW FOR PERIOD 0 898,460 973,581 1,295,829

OPENING CASH BALANCE 0 0 898,460 1,872,041

CLOSING CASH BALANCE 0 898,460 1,872,041 3,167,869

(3) DEPRECIATION SCHEDULE

Year 0 1 2 3

Fixed Assets

Plant&Machinery 250000 225,000 200,000 175,000

Total book values (i.e. net fixed assets) 0 225,000 200,000 175,000

Annual Depreciation

Land & Buildings-10% straight line 25,000 25,000 25,000

total annual depreciation 25,000 25,000 25,000

(4) PROFIT AND LOSS FORECAST

Preop

Year 0 1 2 3

Revenue 0 950,000 1,140,000 1,368,000

Cost of sales 0 190,000 228,000 120,000

Gross profit 0 760,000 912,000 1,248,000

Gross Margin 934,740 1,098,159 1,069,959

Expenses/overheads

Premises (RENT & RATES) 125,000 150,000 180,000

Salaries of Staff 145,000 174,000 208,800

General expenses 175,000 185,500 23,500

Accountant Fees 41,000 49,200 59,040

Register for Tax 2,200 2,640 3,168

Permits and Licenses 23,000 27,600 33,120

Site Survey 16,000 19,200 23,040

Sewing Machine 110,000 132,000 158,400

87,000 104,400 125,280

Preliminary expenses 7,500 7,688 7,880

Lease Payments 6,500 6,500 6,500

Total expenses/overheads 738,200 852,228 822,228

Profit before tax 21,800 59,773 425,772

Tax @ 30% 6,540 17,932 127,732

Before tax net margin 2% 5% 31%

Profit after tax 15,260 41,841 298,041

Transfer to reserves 21,800 59,773 425,772

Website

Knitting

Financial Plan for Fashion From Spain

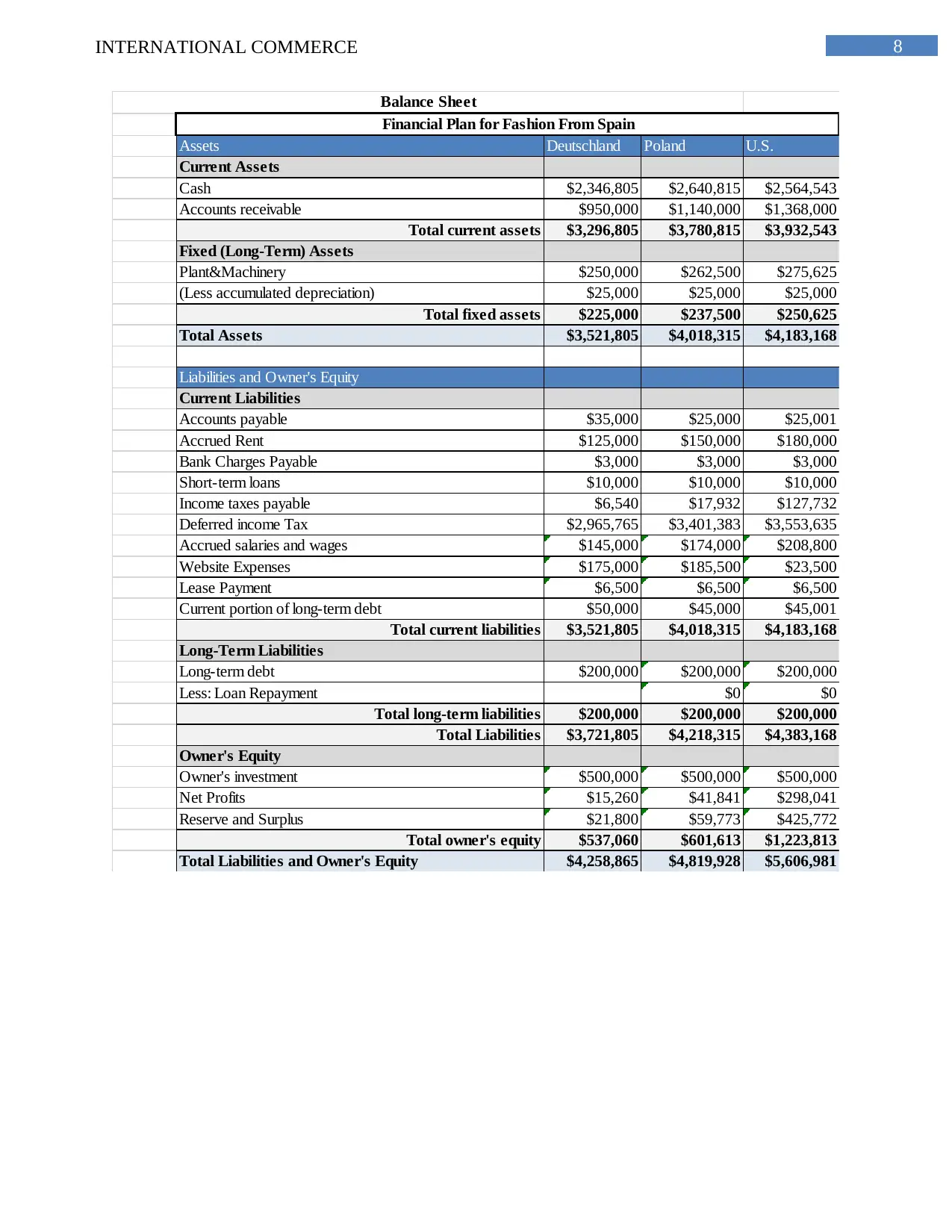

8INTERNATIONAL COMMERCE

Assets Deutschland Poland U.S.

Current Assets

Cash $2,346,805 $2,640,815 $2,564,543

Accounts receivable $950,000 $1,140,000 $1,368,000

Total current assets $3,296,805 $3,780,815 $3,932,543

Fixed (Long-Term) Assets

Plant&Machinery $250,000 $262,500 $275,625

(Less accumulated depreciation) $25,000 $25,000 $25,000

Total fixed assets $225,000 $237,500 $250,625

Total Assets $3,521,805 $4,018,315 $4,183,168

Liabilities and Owner's Equity

Current Liabilities

Accounts payable $35,000 $25,000 $25,001

Accrued Rent $125,000 $150,000 $180,000

Bank Charges Payable $3,000 $3,000 $3,000

Short-term loans $10,000 $10,000 $10,000

Income taxes payable $6,540 $17,932 $127,732

Deferred income Tax $2,965,765 $3,401,383 $3,553,635

Accrued salaries and wages $145,000 $174,000 $208,800

Website Expenses $175,000 $185,500 $23,500

Lease Payment $6,500 $6,500 $6,500

Current portion of long-term debt $50,000 $45,000 $45,001

Total current liabilities $3,521,805 $4,018,315 $4,183,168

Long-Term Liabilities

Long-term debt $200,000 $200,000 $200,000

Less: Loan Repayment $0 $0

Total long-term liabilities $200,000 $200,000 $200,000

Total Liabilities $3,721,805 $4,218,315 $4,383,168

Owner's Equity

Owner's investment $500,000 $500,000 $500,000

Net Profits $15,260 $41,841 $298,041

Reserve and Surplus $21,800 $59,773 $425,772

Total owner's equity $537,060 $601,613 $1,223,813

Total Liabilities and Owner's Equity $4,258,865 $4,819,928 $5,606,981

Balance Sheet

Financial Plan for Fashion From Spain

Assets Deutschland Poland U.S.

Current Assets

Cash $2,346,805 $2,640,815 $2,564,543

Accounts receivable $950,000 $1,140,000 $1,368,000

Total current assets $3,296,805 $3,780,815 $3,932,543

Fixed (Long-Term) Assets

Plant&Machinery $250,000 $262,500 $275,625

(Less accumulated depreciation) $25,000 $25,000 $25,000

Total fixed assets $225,000 $237,500 $250,625

Total Assets $3,521,805 $4,018,315 $4,183,168

Liabilities and Owner's Equity

Current Liabilities

Accounts payable $35,000 $25,000 $25,001

Accrued Rent $125,000 $150,000 $180,000

Bank Charges Payable $3,000 $3,000 $3,000

Short-term loans $10,000 $10,000 $10,000

Income taxes payable $6,540 $17,932 $127,732

Deferred income Tax $2,965,765 $3,401,383 $3,553,635

Accrued salaries and wages $145,000 $174,000 $208,800

Website Expenses $175,000 $185,500 $23,500

Lease Payment $6,500 $6,500 $6,500

Current portion of long-term debt $50,000 $45,000 $45,001

Total current liabilities $3,521,805 $4,018,315 $4,183,168

Long-Term Liabilities

Long-term debt $200,000 $200,000 $200,000

Less: Loan Repayment $0 $0

Total long-term liabilities $200,000 $200,000 $200,000

Total Liabilities $3,721,805 $4,218,315 $4,383,168

Owner's Equity

Owner's investment $500,000 $500,000 $500,000

Net Profits $15,260 $41,841 $298,041

Reserve and Surplus $21,800 $59,773 $425,772

Total owner's equity $537,060 $601,613 $1,223,813

Total Liabilities and Owner's Equity $4,258,865 $4,819,928 $5,606,981

Balance Sheet

Financial Plan for Fashion From Spain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.