Financial Report: Analysis of Faux Fashion Limited Performance

VerifiedAdded on 2022/03/29

|19

|3701

|34

Report

AI Summary

This report provides a comprehensive financial analysis of Faux Fashion Limited, examining its annual accounts, including income statements, and key financial ratios. It delves into costing and pricing strategies, comparing current costing methods with alternative approaches like activity-based costing, and evaluating their pros and cons. The report further explores variance analysis, comparing budgeted and actual performance for April and May, and offers recommendations based on the findings. It also assesses capital expenditure (capex) using methods like payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). Finally, the report covers budgeting, including budget and cash flow forecasts, providing a holistic view of Faux Fashion Limited's financial health and performance.

“Faux Fashion Limited” Words: 2500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

List of Tables.............................................................................................................................................3

1) Review of Annual Accounts.............................................................................................................4

a) Purpose of Financial Statements................................................................................................4

b) Analysis of Income Statement.....................................................................................................4

c) Overview of accounting fundamentals.......................................................................................6

2) Costing and Pricing...........................................................................................................................9

a) Cost for single men’s black Faux leather jacket.......................................................................9

b) Total production overheads and calculation of an alternative total cost................................9

c) Difference between current costing and alternative total cost method and the pros and

cons of the two alternative approaches.............................................................................................9

3) Variance Analysis...........................................................................................................................11

a) Budget for April (using experienced labour)............................................................................11

b) Budget for May (using apprentice labour)................................................................................12

c) Recommendation........................................................................................................................13

4) Capex Appraisal..............................................................................................................................14

a) Payback Period...........................................................................................................................14

b) Accounting rate of return (ARR)................................................................................................14

c) Net Present Value (NPV)...........................................................................................................15

d) Internal Rate of return (IRR)......................................................................................................15

5. Budgeting.........................................................................................................................................17

a) Budget Forecast..........................................................................................................................17

b) Cash flow forecast......................................................................................................................18

References..............................................................................................................................................20

List of Tables.............................................................................................................................................3

1) Review of Annual Accounts.............................................................................................................4

a) Purpose of Financial Statements................................................................................................4

b) Analysis of Income Statement.....................................................................................................4

c) Overview of accounting fundamentals.......................................................................................6

2) Costing and Pricing...........................................................................................................................9

a) Cost for single men’s black Faux leather jacket.......................................................................9

b) Total production overheads and calculation of an alternative total cost................................9

c) Difference between current costing and alternative total cost method and the pros and

cons of the two alternative approaches.............................................................................................9

3) Variance Analysis...........................................................................................................................11

a) Budget for April (using experienced labour)............................................................................11

b) Budget for May (using apprentice labour)................................................................................12

c) Recommendation........................................................................................................................13

4) Capex Appraisal..............................................................................................................................14

a) Payback Period...........................................................................................................................14

b) Accounting rate of return (ARR)................................................................................................14

c) Net Present Value (NPV)...........................................................................................................15

d) Internal Rate of return (IRR)......................................................................................................15

5. Budgeting.........................................................................................................................................17

a) Budget Forecast..........................................................................................................................17

b) Cash flow forecast......................................................................................................................18

References..............................................................................................................................................20

List of Tables

Table 1: Income Statement.....................................................................................................................5

Table 2: Ratio analysis.............................................................................................................................5

Table 3: Working capital cycle................................................................................................................7

Table 4: Liquidity Ratio.............................................................................................................................7

Table 5: Cost per unit...............................................................................................................................9

Table 6: Total cost under AAA costing...................................................................................................9

Table 7: Original budget.........................................................................................................................11

Table 8: Actual budget...........................................................................................................................11

Table 9: Flex budget...............................................................................................................................11

Table 10: Variance analysis..................................................................................................................12

Table 11: Actual Budget (May).............................................................................................................13

Table 12: Variance analysis (May).......................................................................................................13

Table 13: NPV.........................................................................................................................................15

Table 14: Budget Forecast....................................................................................................................17

Table 15: Cash Flow Forecast..............................................................................................................18

Table 1: Income Statement.....................................................................................................................5

Table 2: Ratio analysis.............................................................................................................................5

Table 3: Working capital cycle................................................................................................................7

Table 4: Liquidity Ratio.............................................................................................................................7

Table 5: Cost per unit...............................................................................................................................9

Table 6: Total cost under AAA costing...................................................................................................9

Table 7: Original budget.........................................................................................................................11

Table 8: Actual budget...........................................................................................................................11

Table 9: Flex budget...............................................................................................................................11

Table 10: Variance analysis..................................................................................................................12

Table 11: Actual Budget (May).............................................................................................................13

Table 12: Variance analysis (May).......................................................................................................13

Table 13: NPV.........................................................................................................................................15

Table 14: Budget Forecast....................................................................................................................17

Table 15: Cash Flow Forecast..............................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1) Review of Annual Accounts

a) Purpose of Financial Statements

Financial statements are prepared at the end of the financial year and are published for

the general public so that the investors can get the idea about the performance of a

company. There are four common financial statements which are income statement,

statement of financial position, statement of cash flows and statement of changes in

equity (Healy and Palepu, 2012).

a. Income Statement: Income statement identifies the profit and loss of a company

by subtracting revenues and expenses. It is helpful for the analysis of change in

income of the organization over the financial year (Brigham and Houston, 2012).

b. Statement of Financial position: This financial statement highlights the assets,

liabilities and equity held by a company. It is useful in identifying the liquidity risk

which can have an impact on the investing side of a company (Brigham and

Houston, 2012).

c. Statement of Cash flow: Statement of cash flow defines the inflow and outflow

of cash by dividing the function of the entities into operating activities, financing

activities and investing activities. Positive cash flows are said to have a good

impact on the stakeholders (Brigham and Houston, 2012).

d. Statement of Changes in equity: This statement identifies the changes in

equity side of the company by showing the impact of reserves, retained earnings

and any increased investments by the shareholders. It is helpful in identifying the

confidence if the investors ob a company (Brigham and Houston, 2012).

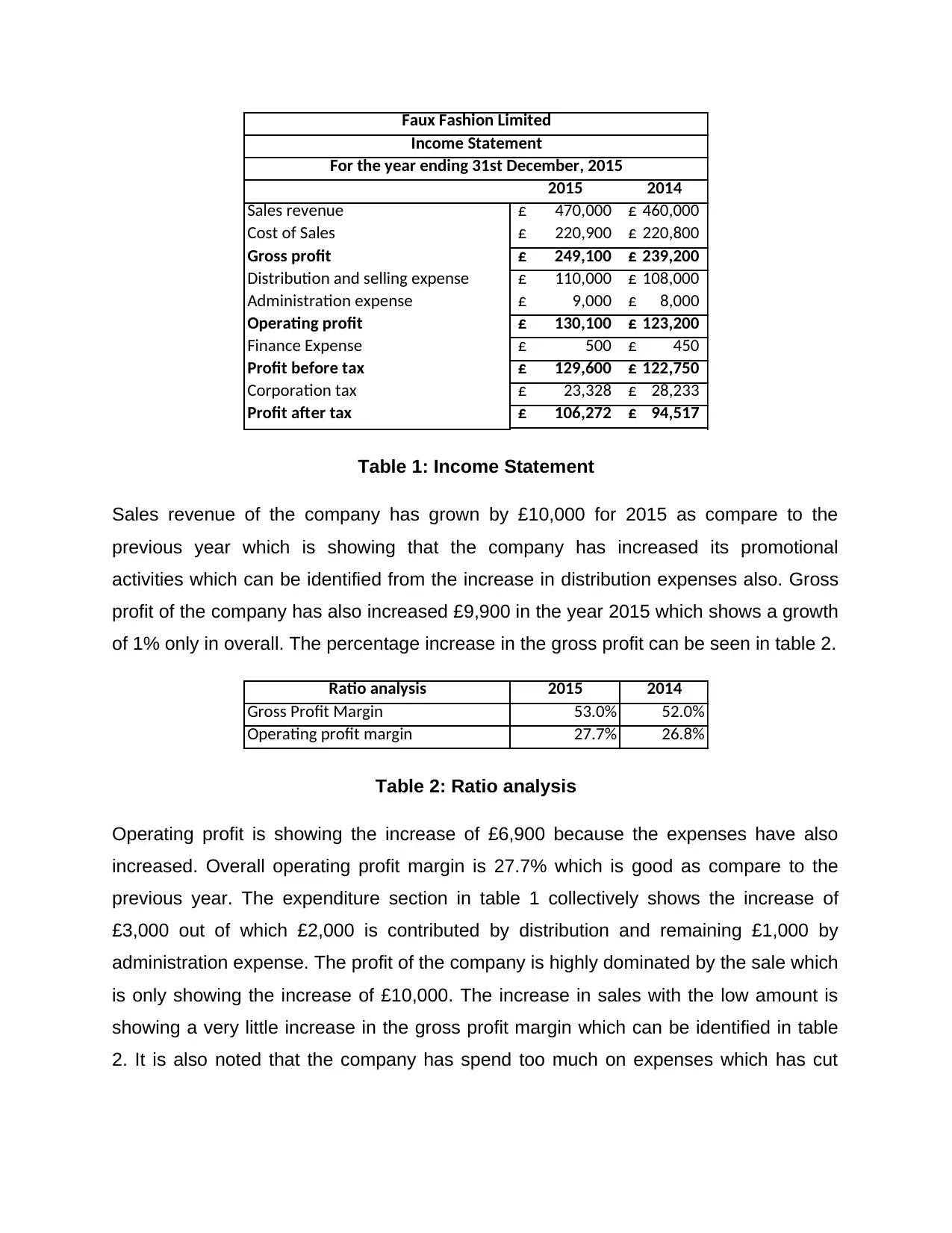

b) Analysis of Income Statement

The income statement of the Faux fashion Limited is shown in the table 1.

a) Purpose of Financial Statements

Financial statements are prepared at the end of the financial year and are published for

the general public so that the investors can get the idea about the performance of a

company. There are four common financial statements which are income statement,

statement of financial position, statement of cash flows and statement of changes in

equity (Healy and Palepu, 2012).

a. Income Statement: Income statement identifies the profit and loss of a company

by subtracting revenues and expenses. It is helpful for the analysis of change in

income of the organization over the financial year (Brigham and Houston, 2012).

b. Statement of Financial position: This financial statement highlights the assets,

liabilities and equity held by a company. It is useful in identifying the liquidity risk

which can have an impact on the investing side of a company (Brigham and

Houston, 2012).

c. Statement of Cash flow: Statement of cash flow defines the inflow and outflow

of cash by dividing the function of the entities into operating activities, financing

activities and investing activities. Positive cash flows are said to have a good

impact on the stakeholders (Brigham and Houston, 2012).

d. Statement of Changes in equity: This statement identifies the changes in

equity side of the company by showing the impact of reserves, retained earnings

and any increased investments by the shareholders. It is helpful in identifying the

confidence if the investors ob a company (Brigham and Houston, 2012).

b) Analysis of Income Statement

The income statement of the Faux fashion Limited is shown in the table 1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2014

Sales revenue 470,000£ 460,000£

Cost of Sales 220,900£ 220,800£

Gross profit 249,100£ 239,200£

Distribution and selling expense 110,000£ 108,000£

Administration expense 9,000£ 8,000£

Operating profit 130,100£ 123,200£

Finance Expense 500£ 450£

Profit before tax 129,600£ 122,750£

Corporation tax 23,328£ 28,233£

Profit after tax 106,272£ 94,517£

Faux Fashion Limited

Income Statement

For the year ending 31st December, 2015

Table 1: Income Statement

Sales revenue of the company has grown by £10,000 for 2015 as compare to the

previous year which is showing that the company has increased its promotional

activities which can be identified from the increase in distribution expenses also. Gross

profit of the company has also increased £9,900 in the year 2015 which shows a growth

of 1% only in overall. The percentage increase in the gross profit can be seen in table 2.

Ratio analysis 2015 2014

Gross Profit Margin 53.0% 52.0%

Operating profit margin 27.7% 26.8%

Table 2: Ratio analysis

Operating profit is showing the increase of £6,900 because the expenses have also

increased. Overall operating profit margin is 27.7% which is good as compare to the

previous year. The expenditure section in table 1 collectively shows the increase of

£3,000 out of which £2,000 is contributed by distribution and remaining £1,000 by

administration expense. The profit of the company is highly dominated by the sale which

is only showing the increase of £10,000. The increase in sales with the low amount is

showing a very little increase in the gross profit margin which can be identified in table

2. It is also noted that the company has spend too much on expenses which has cut

Sales revenue 470,000£ 460,000£

Cost of Sales 220,900£ 220,800£

Gross profit 249,100£ 239,200£

Distribution and selling expense 110,000£ 108,000£

Administration expense 9,000£ 8,000£

Operating profit 130,100£ 123,200£

Finance Expense 500£ 450£

Profit before tax 129,600£ 122,750£

Corporation tax 23,328£ 28,233£

Profit after tax 106,272£ 94,517£

Faux Fashion Limited

Income Statement

For the year ending 31st December, 2015

Table 1: Income Statement

Sales revenue of the company has grown by £10,000 for 2015 as compare to the

previous year which is showing that the company has increased its promotional

activities which can be identified from the increase in distribution expenses also. Gross

profit of the company has also increased £9,900 in the year 2015 which shows a growth

of 1% only in overall. The percentage increase in the gross profit can be seen in table 2.

Ratio analysis 2015 2014

Gross Profit Margin 53.0% 52.0%

Operating profit margin 27.7% 26.8%

Table 2: Ratio analysis

Operating profit is showing the increase of £6,900 because the expenses have also

increased. Overall operating profit margin is 27.7% which is good as compare to the

previous year. The expenditure section in table 1 collectively shows the increase of

£3,000 out of which £2,000 is contributed by distribution and remaining £1,000 by

administration expense. The profit of the company is highly dominated by the sale which

is only showing the increase of £10,000. The increase in sales with the low amount is

showing a very little increase in the gross profit margin which can be identified in table

2. It is also noted that the company has spend too much on expenses which has cut

down the operating profit margin from 53% to only 27.7% which is only 52% of the gross

profit margin.

c) Overview of accounting fundamentals

Profit and cash are different in nature. Although they at times considered similar, but

there is a core difference between them. Profit of a firm is calculated after the deduction

of expenses from the sales amount and is reported in the income statement. It is useful

for the stakeholders attraction towards the company and fro the stability in the market

(Bodie, Kane and Marcus, 2014). However, cash is the amount which is hold by a

company for the continuation of its operational activities and is reported in the current

assets side of the financial position. Positive amount of cash is necessary because

negative amount of cash for too long can create a risk of liquidity (Weil, Schipper and

Francis, 2013).

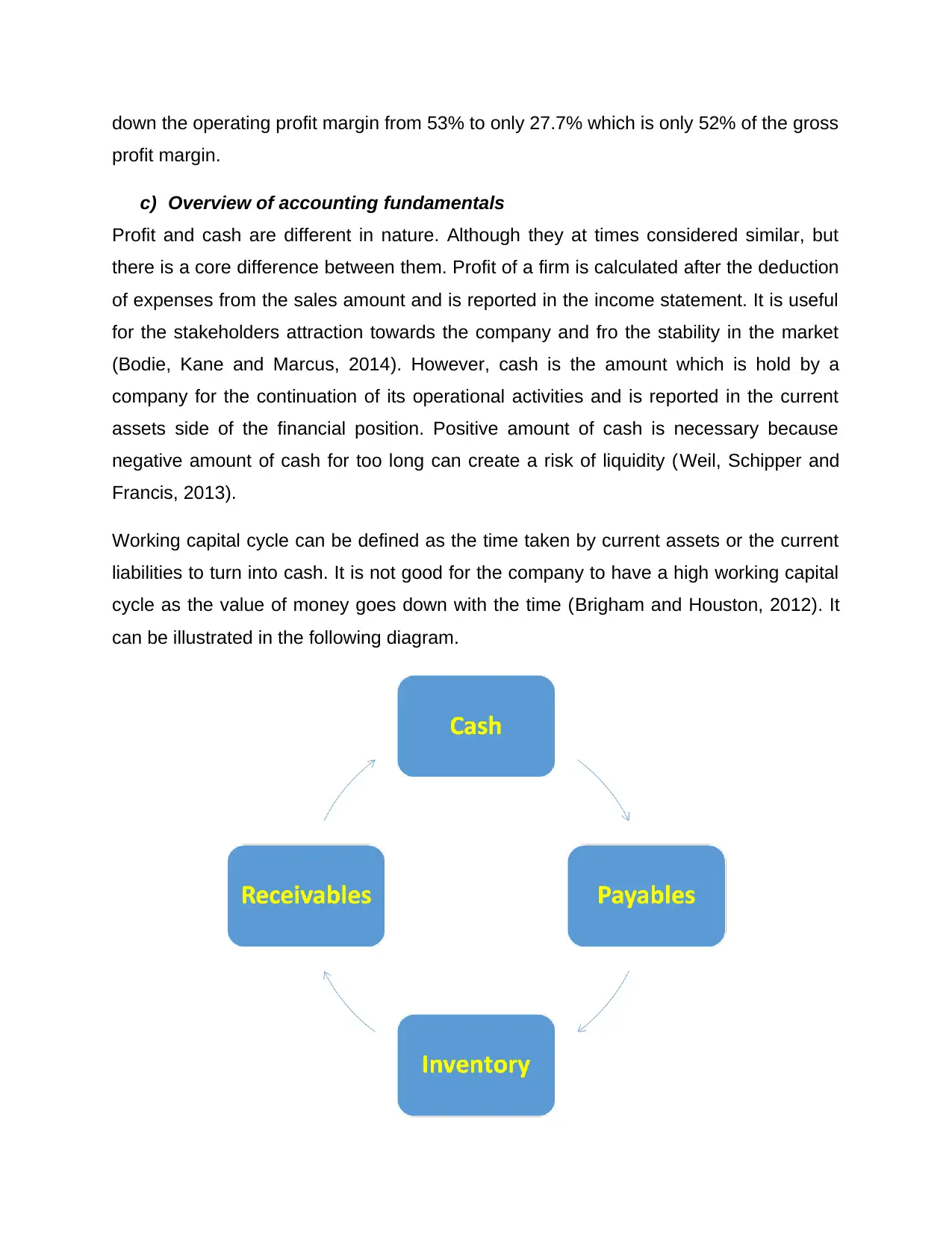

Working capital cycle can be defined as the time taken by current assets or the current

liabilities to turn into cash. It is not good for the company to have a high working capital

cycle as the value of money goes down with the time (Brigham and Houston, 2012). It

can be illustrated in the following diagram.

profit margin.

c) Overview of accounting fundamentals

Profit and cash are different in nature. Although they at times considered similar, but

there is a core difference between them. Profit of a firm is calculated after the deduction

of expenses from the sales amount and is reported in the income statement. It is useful

for the stakeholders attraction towards the company and fro the stability in the market

(Bodie, Kane and Marcus, 2014). However, cash is the amount which is hold by a

company for the continuation of its operational activities and is reported in the current

assets side of the financial position. Positive amount of cash is necessary because

negative amount of cash for too long can create a risk of liquidity (Weil, Schipper and

Francis, 2013).

Working capital cycle can be defined as the time taken by current assets or the current

liabilities to turn into cash. It is not good for the company to have a high working capital

cycle as the value of money goes down with the time (Brigham and Houston, 2012). It

can be illustrated in the following diagram.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

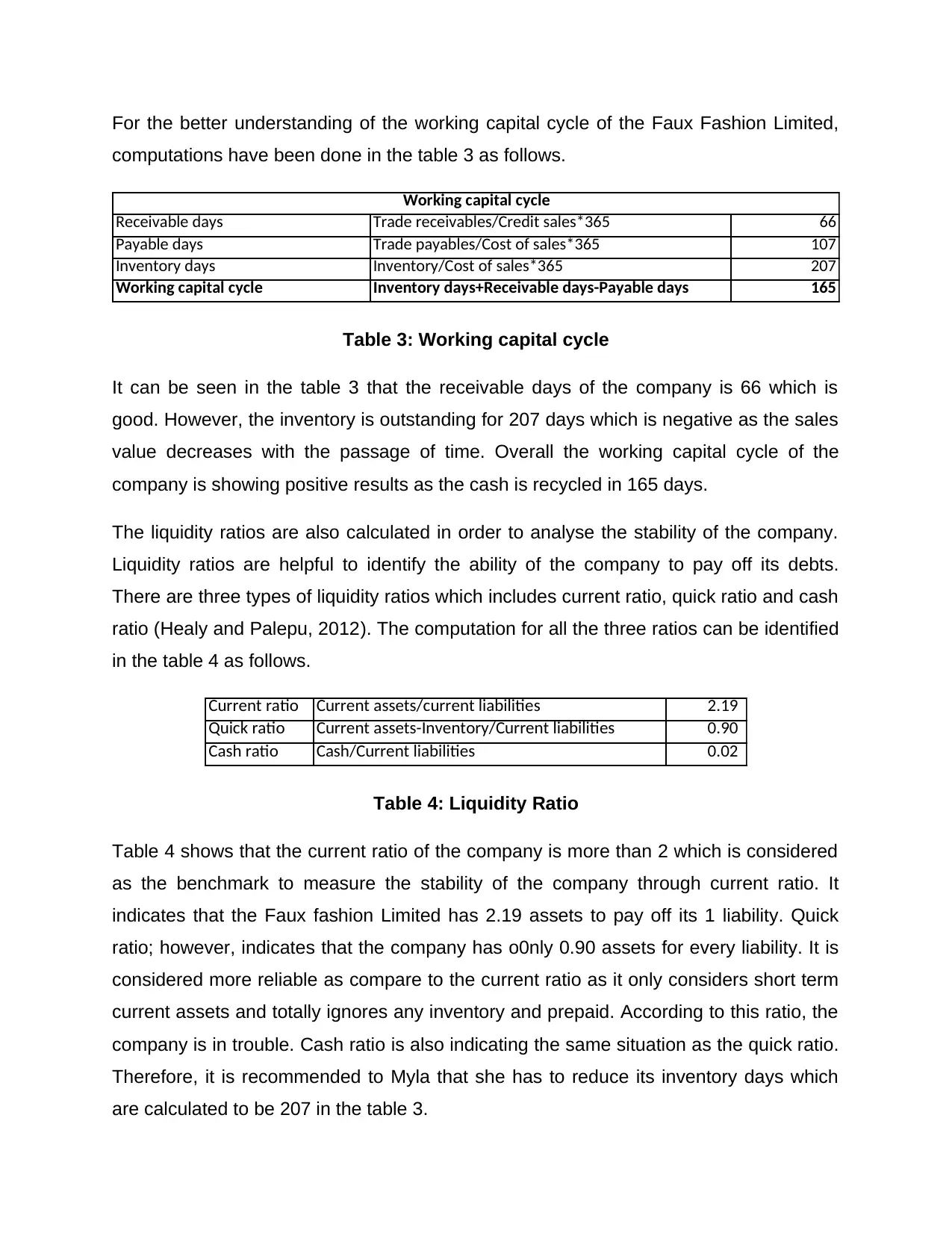

For the better understanding of the working capital cycle of the Faux Fashion Limited,

computations have been done in the table 3 as follows.

Receivable days Trade receivables/Credit sales*365 66

Payable days Trade payables/Cost of sales*365 107

Inventory days Inventory/Cost of sales*365 207

Working capital cycle Inventory days+Receivable days-Payable days 165

Working capital cycle

Table 3: Working capital cycle

It can be seen in the table 3 that the receivable days of the company is 66 which is

good. However, the inventory is outstanding for 207 days which is negative as the sales

value decreases with the passage of time. Overall the working capital cycle of the

company is showing positive results as the cash is recycled in 165 days.

The liquidity ratios are also calculated in order to analyse the stability of the company.

Liquidity ratios are helpful to identify the ability of the company to pay off its debts.

There are three types of liquidity ratios which includes current ratio, quick ratio and cash

ratio (Healy and Palepu, 2012). The computation for all the three ratios can be identified

in the table 4 as follows.

Current ratio Current assets/current liabilities 2.19

Quick ratio Current assets-Inventory/Current liabilities 0.90

Cash ratio Cash/Current liabilities 0.02

Table 4: Liquidity Ratio

Table 4 shows that the current ratio of the company is more than 2 which is considered

as the benchmark to measure the stability of the company through current ratio. It

indicates that the Faux fashion Limited has 2.19 assets to pay off its 1 liability. Quick

ratio; however, indicates that the company has o0nly 0.90 assets for every liability. It is

considered more reliable as compare to the current ratio as it only considers short term

current assets and totally ignores any inventory and prepaid. According to this ratio, the

company is in trouble. Cash ratio is also indicating the same situation as the quick ratio.

Therefore, it is recommended to Myla that she has to reduce its inventory days which

are calculated to be 207 in the table 3.

computations have been done in the table 3 as follows.

Receivable days Trade receivables/Credit sales*365 66

Payable days Trade payables/Cost of sales*365 107

Inventory days Inventory/Cost of sales*365 207

Working capital cycle Inventory days+Receivable days-Payable days 165

Working capital cycle

Table 3: Working capital cycle

It can be seen in the table 3 that the receivable days of the company is 66 which is

good. However, the inventory is outstanding for 207 days which is negative as the sales

value decreases with the passage of time. Overall the working capital cycle of the

company is showing positive results as the cash is recycled in 165 days.

The liquidity ratios are also calculated in order to analyse the stability of the company.

Liquidity ratios are helpful to identify the ability of the company to pay off its debts.

There are three types of liquidity ratios which includes current ratio, quick ratio and cash

ratio (Healy and Palepu, 2012). The computation for all the three ratios can be identified

in the table 4 as follows.

Current ratio Current assets/current liabilities 2.19

Quick ratio Current assets-Inventory/Current liabilities 0.90

Cash ratio Cash/Current liabilities 0.02

Table 4: Liquidity Ratio

Table 4 shows that the current ratio of the company is more than 2 which is considered

as the benchmark to measure the stability of the company through current ratio. It

indicates that the Faux fashion Limited has 2.19 assets to pay off its 1 liability. Quick

ratio; however, indicates that the company has o0nly 0.90 assets for every liability. It is

considered more reliable as compare to the current ratio as it only considers short term

current assets and totally ignores any inventory and prepaid. According to this ratio, the

company is in trouble. Cash ratio is also indicating the same situation as the quick ratio.

Therefore, it is recommended to Myla that she has to reduce its inventory days which

are calculated to be 207 in the table 3.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2) Costing and Pricing

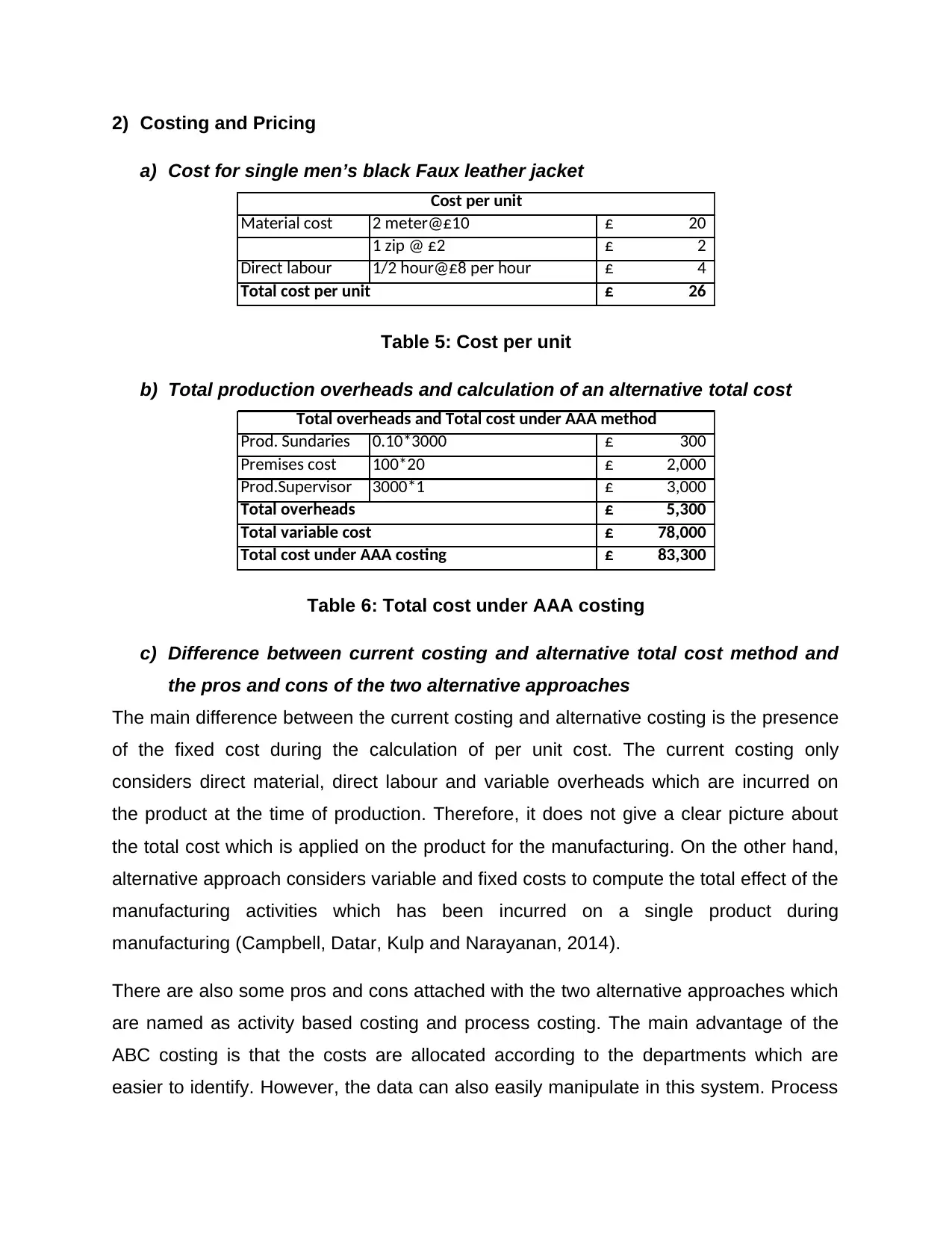

a) Cost for single men’s black Faux leather jacket

Material cost 2 meter@£10 20£

1 zip @ £2 2£

Direct labour 1/2 hour@£8 per hour 4£

26£

Cost per unit

Total cost per unit

Table 5: Cost per unit

b) Total production overheads and calculation of an alternative total cost

Prod. Sundaries 0.10*3000 300£

Premises cost 100*20 2,000£

Prod.Supervisor 3000*1 3,000£

5,300£

78,000£

83,300£Total cost under AAA costing

Total overheads and Total cost under AAA method

Total overheads

Total variable cost

Table 6: Total cost under AAA costing

c) Difference between current costing and alternative total cost method and

the pros and cons of the two alternative approaches

The main difference between the current costing and alternative costing is the presence

of the fixed cost during the calculation of per unit cost. The current costing only

considers direct material, direct labour and variable overheads which are incurred on

the product at the time of production. Therefore, it does not give a clear picture about

the total cost which is applied on the product for the manufacturing. On the other hand,

alternative approach considers variable and fixed costs to compute the total effect of the

manufacturing activities which has been incurred on a single product during

manufacturing (Campbell, Datar, Kulp and Narayanan, 2014).

There are also some pros and cons attached with the two alternative approaches which

are named as activity based costing and process costing. The main advantage of the

ABC costing is that the costs are allocated according to the departments which are

easier to identify. However, the data can also easily manipulate in this system. Process

a) Cost for single men’s black Faux leather jacket

Material cost 2 meter@£10 20£

1 zip @ £2 2£

Direct labour 1/2 hour@£8 per hour 4£

26£

Cost per unit

Total cost per unit

Table 5: Cost per unit

b) Total production overheads and calculation of an alternative total cost

Prod. Sundaries 0.10*3000 300£

Premises cost 100*20 2,000£

Prod.Supervisor 3000*1 3,000£

5,300£

78,000£

83,300£Total cost under AAA costing

Total overheads and Total cost under AAA method

Total overheads

Total variable cost

Table 6: Total cost under AAA costing

c) Difference between current costing and alternative total cost method and

the pros and cons of the two alternative approaches

The main difference between the current costing and alternative costing is the presence

of the fixed cost during the calculation of per unit cost. The current costing only

considers direct material, direct labour and variable overheads which are incurred on

the product at the time of production. Therefore, it does not give a clear picture about

the total cost which is applied on the product for the manufacturing. On the other hand,

alternative approach considers variable and fixed costs to compute the total effect of the

manufacturing activities which has been incurred on a single product during

manufacturing (Campbell, Datar, Kulp and Narayanan, 2014).

There are also some pros and cons attached with the two alternative approaches which

are named as activity based costing and process costing. The main advantage of the

ABC costing is that the costs are allocated according to the departments which are

easier to identify. However, the data can also easily manipulate in this system. Process

costing is helpful as the amount is allocated to the units according to the number of

processes from which the product passes. It is easy to use. However, the allocation is

done on the basis of equivalent units which can decrease the reliability of results (Bodie

et al, 2014).

processes from which the product passes. It is easy to use. However, the allocation is

done on the basis of equivalent units which can decrease the reliability of results (Bodie

et al, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) Variance Analysis

a) Budget for April (using experienced labour)

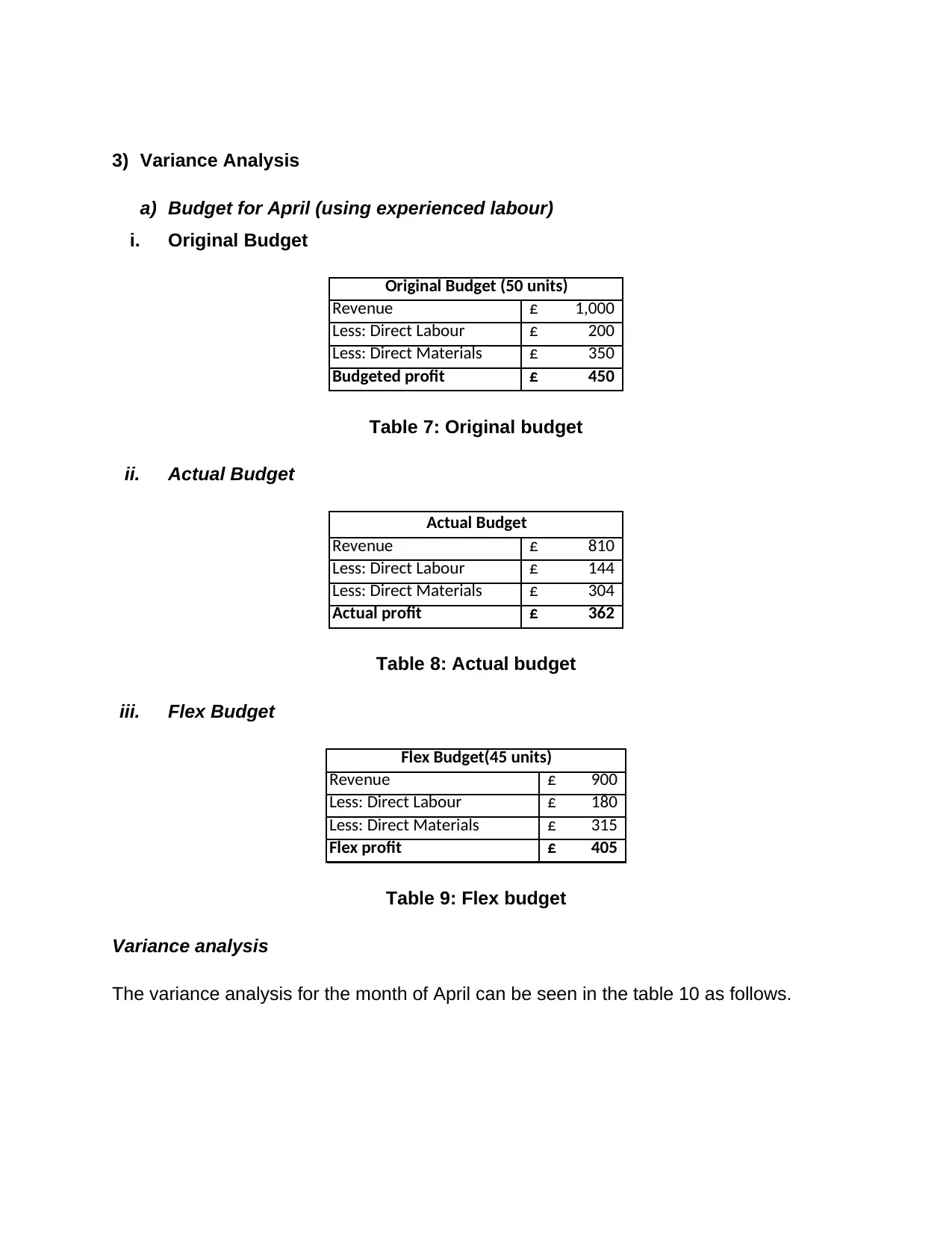

i. Original Budget

Revenue 1,000£

Less: Direct Labour 200£

Less: Direct Materials 350£

Budgeted profit 450£

Original Budget (50 units)

Table 7: Original budget

ii. Actual Budget

Revenue 810£

Less: Direct Labour 144£

Less: Direct Materials 304£

Actual profit 362£

Actual Budget

Table 8: Actual budget

iii. Flex Budget

Revenue 900£

Less: Direct Labour 180£

Less: Direct Materials 315£

Flex profit 405£

Flex Budget(45 units)

Table 9: Flex budget

Variance analysis

The variance analysis for the month of April can be seen in the table 10 as follows.

a) Budget for April (using experienced labour)

i. Original Budget

Revenue 1,000£

Less: Direct Labour 200£

Less: Direct Materials 350£

Budgeted profit 450£

Original Budget (50 units)

Table 7: Original budget

ii. Actual Budget

Revenue 810£

Less: Direct Labour 144£

Less: Direct Materials 304£

Actual profit 362£

Actual Budget

Table 8: Actual budget

iii. Flex Budget

Revenue 900£

Less: Direct Labour 180£

Less: Direct Materials 315£

Flex profit 405£

Flex Budget(45 units)

Table 9: Flex budget

Variance analysis

The variance analysis for the month of April can be seen in the table 10 as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

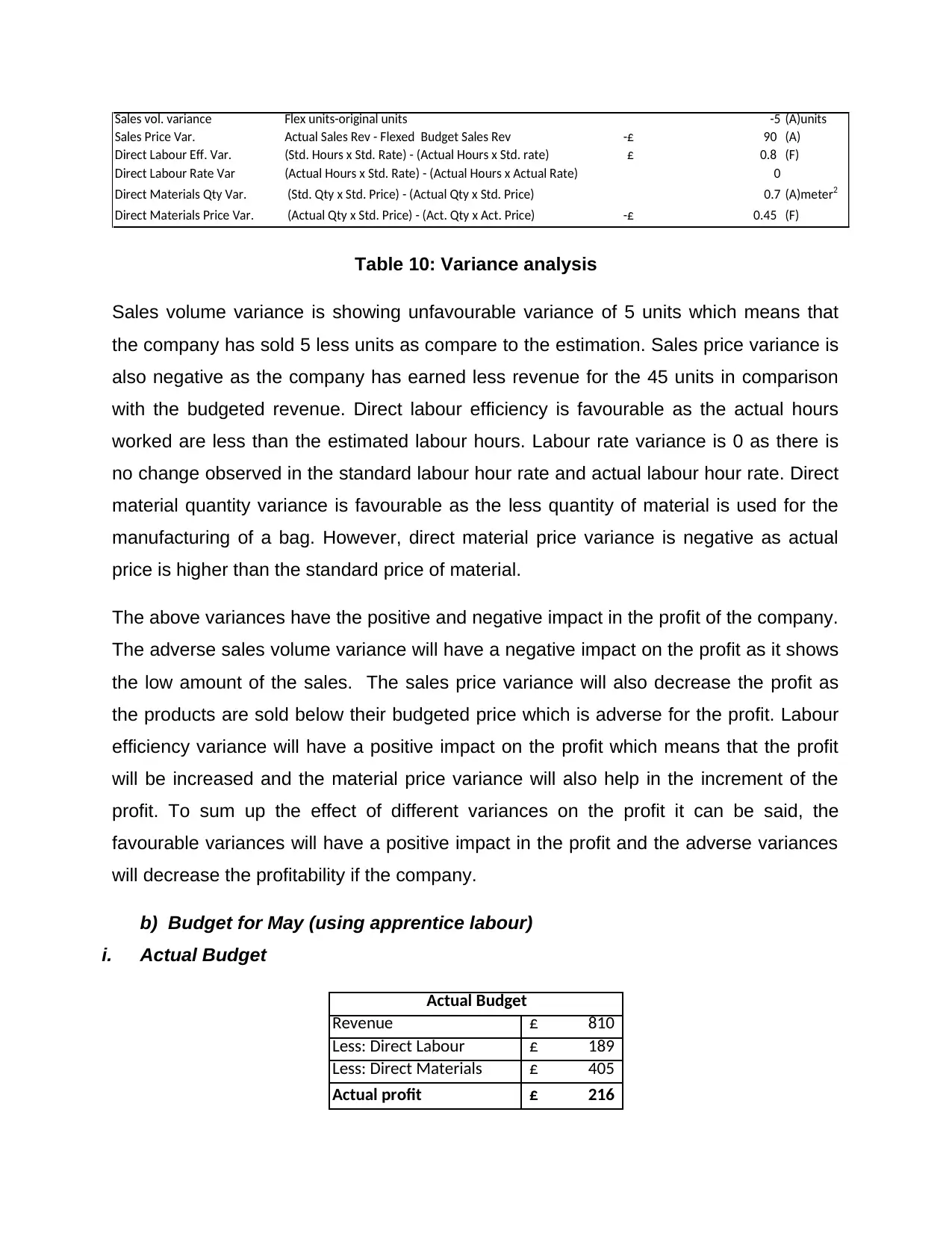

Sales vol. variance Flex units-original units -5 (A)units

Sales Price Var. Actual Sales Rev - Flexed Budget Sales Rev 90-£ (A)

Direct Labour Eff. Var. (Std. Hours x Std. Rate) - (Actual Hours x Std. rate) 0.8£ (F)

Direct Labour Rate Var (Actual Hours x Std. Rate) - (Actual Hours x Actual Rate) 0

Direct Materials Qty Var. (Std. Qty x Std. Price) - (Actual Qty x Std. Price) 0.7 (A)meter 2

Direct Materials Price Var. (Actual Qty x Std. Price) - (Act. Qty x Act. Price) 0.45-£ (F)

Table 10: Variance analysis

Sales volume variance is showing unfavourable variance of 5 units which means that

the company has sold 5 less units as compare to the estimation. Sales price variance is

also negative as the company has earned less revenue for the 45 units in comparison

with the budgeted revenue. Direct labour efficiency is favourable as the actual hours

worked are less than the estimated labour hours. Labour rate variance is 0 as there is

no change observed in the standard labour hour rate and actual labour hour rate. Direct

material quantity variance is favourable as the less quantity of material is used for the

manufacturing of a bag. However, direct material price variance is negative as actual

price is higher than the standard price of material.

The above variances have the positive and negative impact in the profit of the company.

The adverse sales volume variance will have a negative impact on the profit as it shows

the low amount of the sales. The sales price variance will also decrease the profit as

the products are sold below their budgeted price which is adverse for the profit. Labour

efficiency variance will have a positive impact on the profit which means that the profit

will be increased and the material price variance will also help in the increment of the

profit. To sum up the effect of different variances on the profit it can be said, the

favourable variances will have a positive impact in the profit and the adverse variances

will decrease the profitability if the company.

b) Budget for May (using apprentice labour)

i. Actual Budget

Revenue 810£

Less: Direct Labour 189£

Less: Direct Materials 405£

Actual profit 216£

Actual Budget

Sales Price Var. Actual Sales Rev - Flexed Budget Sales Rev 90-£ (A)

Direct Labour Eff. Var. (Std. Hours x Std. Rate) - (Actual Hours x Std. rate) 0.8£ (F)

Direct Labour Rate Var (Actual Hours x Std. Rate) - (Actual Hours x Actual Rate) 0

Direct Materials Qty Var. (Std. Qty x Std. Price) - (Actual Qty x Std. Price) 0.7 (A)meter 2

Direct Materials Price Var. (Actual Qty x Std. Price) - (Act. Qty x Act. Price) 0.45-£ (F)

Table 10: Variance analysis

Sales volume variance is showing unfavourable variance of 5 units which means that

the company has sold 5 less units as compare to the estimation. Sales price variance is

also negative as the company has earned less revenue for the 45 units in comparison

with the budgeted revenue. Direct labour efficiency is favourable as the actual hours

worked are less than the estimated labour hours. Labour rate variance is 0 as there is

no change observed in the standard labour hour rate and actual labour hour rate. Direct

material quantity variance is favourable as the less quantity of material is used for the

manufacturing of a bag. However, direct material price variance is negative as actual

price is higher than the standard price of material.

The above variances have the positive and negative impact in the profit of the company.

The adverse sales volume variance will have a negative impact on the profit as it shows

the low amount of the sales. The sales price variance will also decrease the profit as

the products are sold below their budgeted price which is adverse for the profit. Labour

efficiency variance will have a positive impact on the profit which means that the profit

will be increased and the material price variance will also help in the increment of the

profit. To sum up the effect of different variances on the profit it can be said, the

favourable variances will have a positive impact in the profit and the adverse variances

will decrease the profitability if the company.

b) Budget for May (using apprentice labour)

i. Actual Budget

Revenue 810£

Less: Direct Labour 189£

Less: Direct Materials 405£

Actual profit 216£

Actual Budget

Table 11: Actual Budget (May)

Variance analysis

The variance analysis for the month of May can be observed in the table 12 as follows.

Sales vol. variance Flex units-original units -5 (A)units

Sales Price Var. Actual Sales Rev - Flexed Budget Sales Rev 90-£ (A)

Direct Labour Eff. Var. (Std. Hours x Std. Rate) - (Actual Hours x Std. rate) 1.6-£ (A)

Direct Labour Rate Var (Actual Hours x Std. Rate) - (Actual Hours x Actual Rate) 1.4 (F)

Direct Materials Qty Var. (Std. Qty x Std. Price) - (Actual Qty x Std. Price) -1.4 (A)meter 2

Direct Materials Price Var. (Actual Qty x Std. Price) - (Act. Qty x Act. Price) 0.60-£ (A)

Table 12: Variance analysis (May)

In table 12 it can be seen that when the sales volume and sales price variance remains

same as of April. However, direct labour efficiency variance is now showing

unfavourable position because the actual hours are more than the standard hours.

Labour rate variance is showing favourable amount at per hour labour rate is cut down

from £8 to £6 in May. Direct material quantity variance is also unfavourable as the

actual quantity of the material used is increased in May. Direct material price variance is

also unfavourable as the actual price is increased as compare to the standard price of

material. The computed variances in the table 12 show some adverse and favourable

variances. It should be noted that all the favourable variances will increase the

profitability of the company which includes only direct labour rate variance. However, all

the remaining variances are adverse which decrease the profitability of the company.

c) Recommendation

There are certain factors which can have an impact on the different variances which

have been calculated in the above sections. Sales volume variance can be increased or

decreased with the number of units sold, sales price variance can be changed with the

change in the prices, labour efficiency and rate variance can be increased or decreased

with the change in labour hours or labour rate and similar case will be observed with the

material quantity and material price variance. It is recommended to Myla on the basis of

the above calculations that the experienced labour should be used in operations as the

profit is high and most of the variances are favourable also.

Variance analysis

The variance analysis for the month of May can be observed in the table 12 as follows.

Sales vol. variance Flex units-original units -5 (A)units

Sales Price Var. Actual Sales Rev - Flexed Budget Sales Rev 90-£ (A)

Direct Labour Eff. Var. (Std. Hours x Std. Rate) - (Actual Hours x Std. rate) 1.6-£ (A)

Direct Labour Rate Var (Actual Hours x Std. Rate) - (Actual Hours x Actual Rate) 1.4 (F)

Direct Materials Qty Var. (Std. Qty x Std. Price) - (Actual Qty x Std. Price) -1.4 (A)meter 2

Direct Materials Price Var. (Actual Qty x Std. Price) - (Act. Qty x Act. Price) 0.60-£ (A)

Table 12: Variance analysis (May)

In table 12 it can be seen that when the sales volume and sales price variance remains

same as of April. However, direct labour efficiency variance is now showing

unfavourable position because the actual hours are more than the standard hours.

Labour rate variance is showing favourable amount at per hour labour rate is cut down

from £8 to £6 in May. Direct material quantity variance is also unfavourable as the

actual quantity of the material used is increased in May. Direct material price variance is

also unfavourable as the actual price is increased as compare to the standard price of

material. The computed variances in the table 12 show some adverse and favourable

variances. It should be noted that all the favourable variances will increase the

profitability of the company which includes only direct labour rate variance. However, all

the remaining variances are adverse which decrease the profitability of the company.

c) Recommendation

There are certain factors which can have an impact on the different variances which

have been calculated in the above sections. Sales volume variance can be increased or

decreased with the number of units sold, sales price variance can be changed with the

change in the prices, labour efficiency and rate variance can be increased or decreased

with the change in labour hours or labour rate and similar case will be observed with the

material quantity and material price variance. It is recommended to Myla on the basis of

the above calculations that the experienced labour should be used in operations as the

profit is high and most of the variances are favourable also.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.