Taxation Law Assignment: Fringe Benefits and Capital Gains Analysis

VerifiedAdded on 2023/03/23

|12

|2978

|100

Report

AI Summary

This assignment delves into Australian taxation law, specifically focusing on Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). It begins by explaining FBT, its applicability to non-cash benefits like company cars, and the calculation methods (statutory formula and operating cost). The assignment then shifts to CGT, defining capital gains and losses, distinguishing between short-term and long-term gains, and providing detailed calculations for various scenarios, including the sale of property, artwork, a yacht, and shares. The impact of forfeited deposits and interest deductibility on loans for share purchases is also examined. Finally, the assignment briefly discusses investing proceeds from asset sales into superannuation funds and the associated tax implications. Desklib provides similar solved assignments and study resources for students.

Australian Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1..................................................................................................................................3

Question 2..................................................................................................................................6

Part A.....................................................................................................................................6

Part B......................................................................................................................................9

Part C......................................................................................................................................9

References................................................................................................................................11

Question 1..................................................................................................................................3

Question 2..................................................................................................................................6

Part A.....................................................................................................................................6

Part B......................................................................................................................................9

Part C......................................................................................................................................9

References................................................................................................................................11

Question 1

In Australia, Fringe Benefits tax is a tax applied in accordance with provisions applied by the

Australian Taxation Office. It is the tax that is charged on the non-cash benefits provided by

the owner to its employees. However, for the applicability of the fringe benefits tax, it is

essential that benefit must be provided by the employer in terms of its employment.

Sometimes employer apart from salary or wages provides several benefits to employees. A

fringe benefit is the advantages provided by the employer to its employees in respect of the

employment (Butler, and Calcott, 2018). With this aspect, there are several fringe benefits

which are offered by the employer such as car fringe benefit, housing fringe benefit, property

fringe benefit, Loan Fringe benefits and many others (Cooper, 2018). This tax is paid by the

employer of the company. Moreover, it is charged even if any third party due to an

preparation of same with the employer provides the benefits to the employee. This tax is

distinct from the income tax,and it is computed on the taxable value of the fringe benefit. The

employer should compute the value of the fringe benefit as per the rules approved by the

government of Australia.

In the present case, it has been stated that the boss provides a car to its employee for personal

use. Thus, the same will be covered under the definition of the non-cash benefit provided by

the employer to its employee in respect of employment. Therefore the definition of the fringe

benefit is satisfied,and the tax should be paid by the employer.There are two methods for

computation of fringe benefits tax liability in case of the car provided by the employer to its

employees, such as the statutory formula method, and operating cost method.

Calculation of Fringe benefit value

Value of the benefit = Base Value of the car*statutory percentage *days vehicle available for

personal purpose/days in the year – contribution by the employee

In the given study

Base value of car = $ 18000

Statutory percentage* = 20%

Days vehicle was provided for personal use = 365

In Australia, Fringe Benefits tax is a tax applied in accordance with provisions applied by the

Australian Taxation Office. It is the tax that is charged on the non-cash benefits provided by

the owner to its employees. However, for the applicability of the fringe benefits tax, it is

essential that benefit must be provided by the employer in terms of its employment.

Sometimes employer apart from salary or wages provides several benefits to employees. A

fringe benefit is the advantages provided by the employer to its employees in respect of the

employment (Butler, and Calcott, 2018). With this aspect, there are several fringe benefits

which are offered by the employer such as car fringe benefit, housing fringe benefit, property

fringe benefit, Loan Fringe benefits and many others (Cooper, 2018). This tax is paid by the

employer of the company. Moreover, it is charged even if any third party due to an

preparation of same with the employer provides the benefits to the employee. This tax is

distinct from the income tax,and it is computed on the taxable value of the fringe benefit. The

employer should compute the value of the fringe benefit as per the rules approved by the

government of Australia.

In the present case, it has been stated that the boss provides a car to its employee for personal

use. Thus, the same will be covered under the definition of the non-cash benefit provided by

the employer to its employee in respect of employment. Therefore the definition of the fringe

benefit is satisfied,and the tax should be paid by the employer.There are two methods for

computation of fringe benefits tax liability in case of the car provided by the employer to its

employees, such as the statutory formula method, and operating cost method.

Calculation of Fringe benefit value

Value of the benefit = Base Value of the car*statutory percentage *days vehicle available for

personal purpose/days in the year – contribution by the employee

In the given study

Base value of car = $ 18000

Statutory percentage* = 20%

Days vehicle was provided for personal use = 365

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

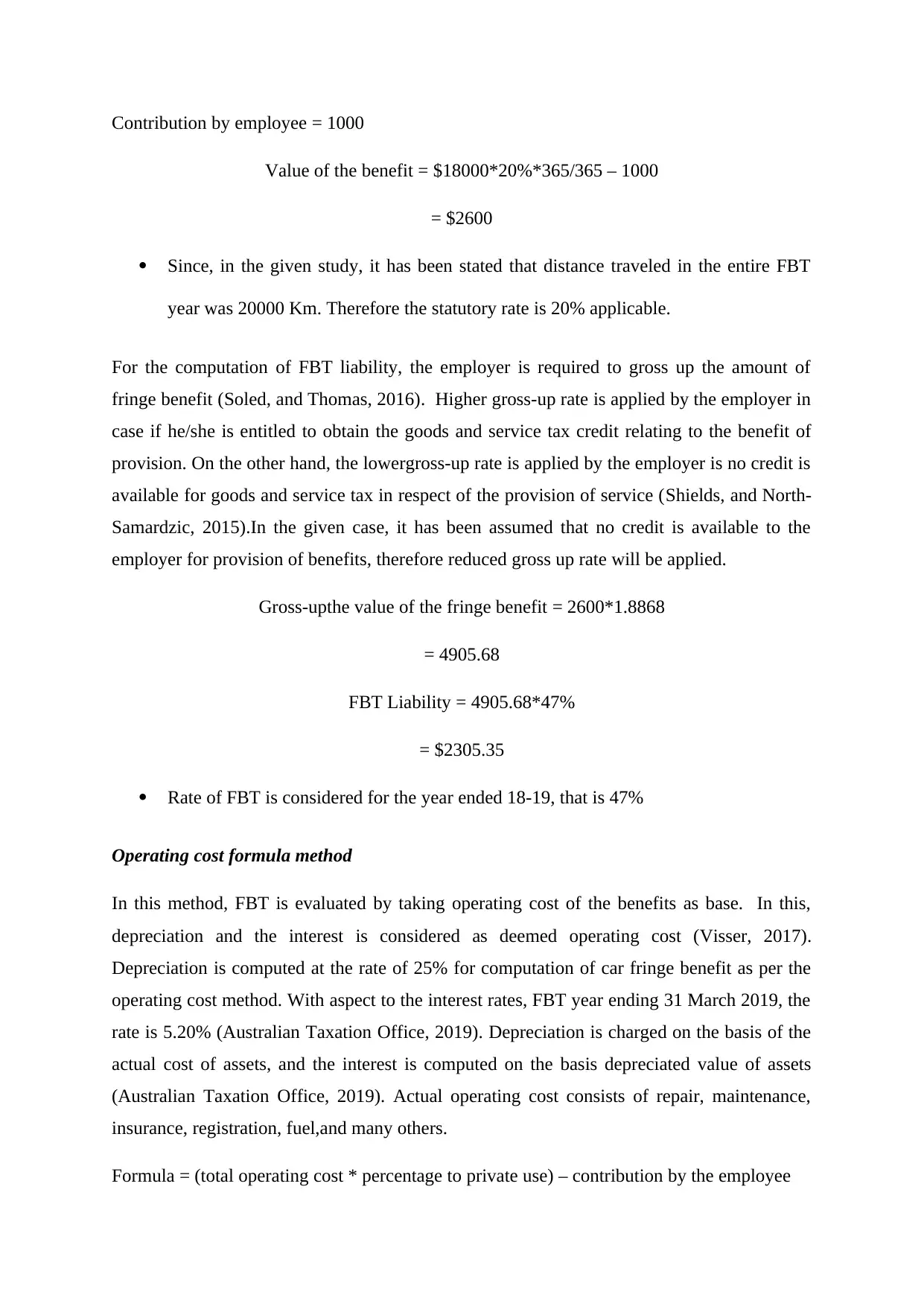

Contribution by employee = 1000

Value of the benefit = $18000*20%*365/365 – 1000

= $2600

Since, in the given study, it has been stated that distance traveled in the entire FBT

year was 20000 Km. Therefore the statutory rate is 20% applicable.

For the computation of FBT liability, the employer is required to gross up the amount of

fringe benefit (Soled, and Thomas, 2016). Higher gross-up rate is applied by the employer in

case if he/she is entitled to obtain the goods and service tax credit relating to the benefit of

provision. On the other hand, the lowergross-up rate is applied by the employer is no credit is

available for goods and service tax in respect of the provision of service (Shields, and North-

Samardzic, 2015).In the given case, it has been assumed that no credit is available to the

employer for provision of benefits, therefore reduced gross up rate will be applied.

Gross-upthe value of the fringe benefit = 2600*1.8868

= 4905.68

FBT Liability = 4905.68*47%

= $2305.35

Rate of FBT is considered for the year ended 18-19, that is 47%

Operating cost formula method

In this method, FBT is evaluated by taking operating cost of the benefits as base. In this,

depreciation and the interest is considered as deemed operating cost (Visser, 2017).

Depreciation is computed at the rate of 25% for computation of car fringe benefit as per the

operating cost method. With aspect to the interest rates, FBT year ending 31 March 2019, the

rate is 5.20% (Australian Taxation Office, 2019). Depreciation is charged on the basis of the

actual cost of assets, and the interest is computed on the basis depreciated value of assets

(Australian Taxation Office, 2019). Actual operating cost consists of repair, maintenance,

insurance, registration, fuel,and many others.

Formula = (total operating cost * percentage to private use) – contribution by the employee

Value of the benefit = $18000*20%*365/365 – 1000

= $2600

Since, in the given study, it has been stated that distance traveled in the entire FBT

year was 20000 Km. Therefore the statutory rate is 20% applicable.

For the computation of FBT liability, the employer is required to gross up the amount of

fringe benefit (Soled, and Thomas, 2016). Higher gross-up rate is applied by the employer in

case if he/she is entitled to obtain the goods and service tax credit relating to the benefit of

provision. On the other hand, the lowergross-up rate is applied by the employer is no credit is

available for goods and service tax in respect of the provision of service (Shields, and North-

Samardzic, 2015).In the given case, it has been assumed that no credit is available to the

employer for provision of benefits, therefore reduced gross up rate will be applied.

Gross-upthe value of the fringe benefit = 2600*1.8868

= 4905.68

FBT Liability = 4905.68*47%

= $2305.35

Rate of FBT is considered for the year ended 18-19, that is 47%

Operating cost formula method

In this method, FBT is evaluated by taking operating cost of the benefits as base. In this,

depreciation and the interest is considered as deemed operating cost (Visser, 2017).

Depreciation is computed at the rate of 25% for computation of car fringe benefit as per the

operating cost method. With aspect to the interest rates, FBT year ending 31 March 2019, the

rate is 5.20% (Australian Taxation Office, 2019). Depreciation is charged on the basis of the

actual cost of assets, and the interest is computed on the basis depreciated value of assets

(Australian Taxation Office, 2019). Actual operating cost consists of repair, maintenance,

insurance, registration, fuel,and many others.

Formula = (total operating cost * percentage to private use) – contribution by the employee

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the given case total operating cost is as follows

Table 1 Computation of operating cost

Particulars Amount in $

Repair 3300

Insurance 2200

Fuel 990

Depreciation* 4500

Interest** 936

Total Operating Cost 11926

*Depreciation = 18000*25%

= 4500

*Interest = 18000*5.20%

= 936

Taxable Value = $11926*30% -1000

= $2577.8

It is given that, car is used 70% for business, and therefore the private use of car is 30%

(100% 30 %).

Gross up value = 2577.8*1.8868

= $4863.79

FBT Liability = $4863.79*47%

= $2285.98

Summary

Table 2 FBT Liability

Particulars Amount in $

FBT Liability as per the statutory method $2305.28

Table 1 Computation of operating cost

Particulars Amount in $

Repair 3300

Insurance 2200

Fuel 990

Depreciation* 4500

Interest** 936

Total Operating Cost 11926

*Depreciation = 18000*25%

= 4500

*Interest = 18000*5.20%

= 936

Taxable Value = $11926*30% -1000

= $2577.8

It is given that, car is used 70% for business, and therefore the private use of car is 30%

(100% 30 %).

Gross up value = 2577.8*1.8868

= $4863.79

FBT Liability = $4863.79*47%

= $2285.98

Summary

Table 2 FBT Liability

Particulars Amount in $

FBT Liability as per the statutory method $2305.28

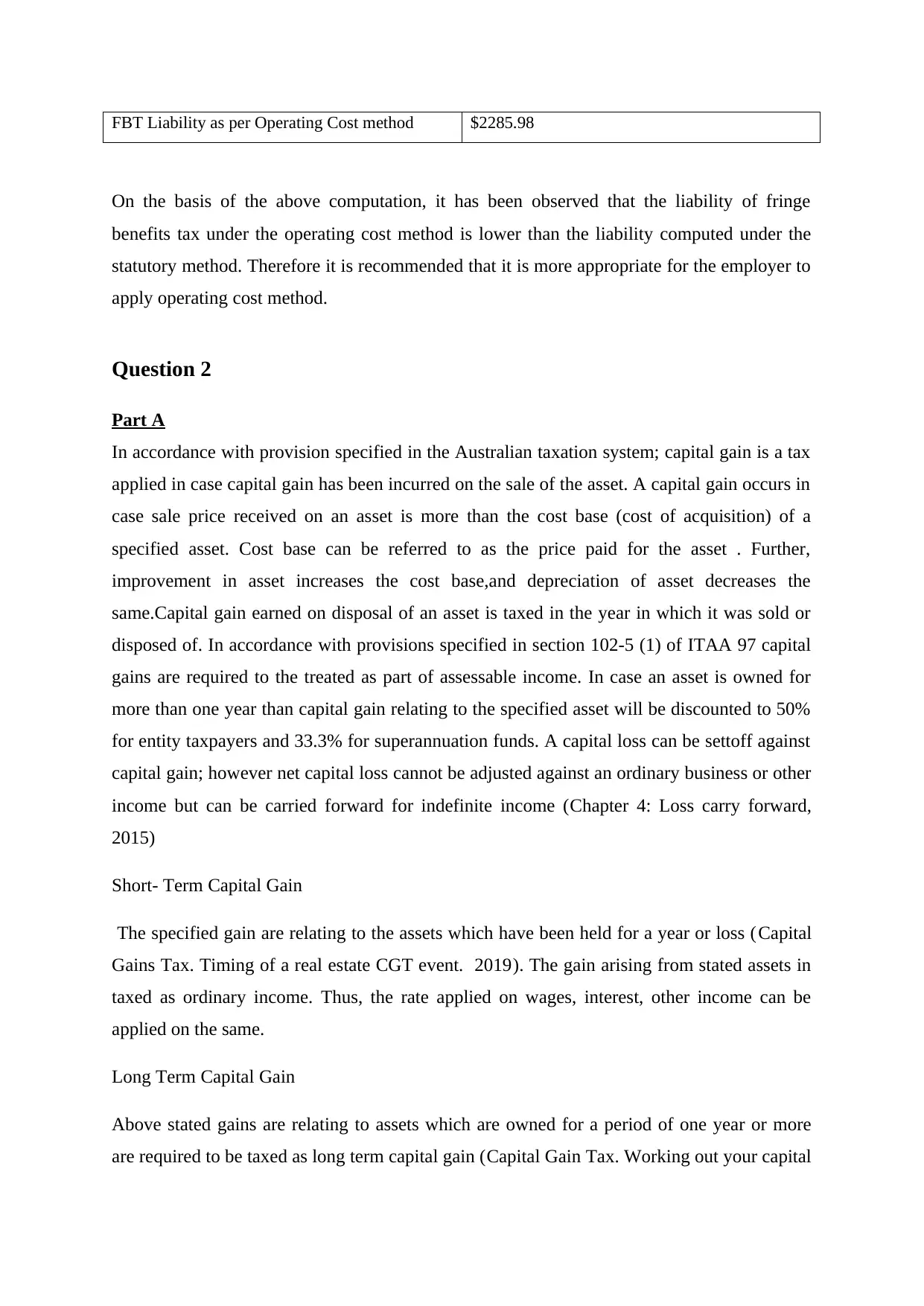

FBT Liability as per Operating Cost method $2285.98

On the basis of the above computation, it has been observed that the liability of fringe

benefits tax under the operating cost method is lower than the liability computed under the

statutory method. Therefore it is recommended that it is more appropriate for the employer to

apply operating cost method.

Question 2

Part A

In accordance with provision specified in the Australian taxation system; capital gain is a tax

applied in case capital gain has been incurred on the sale of the asset. A capital gain occurs in

case sale price received on an asset is more than the cost base (cost of acquisition) of a

specified asset. Cost base can be referred to as the price paid for the asset . Further,

improvement in asset increases the cost base,and depreciation of asset decreases the

same.Capital gain earned on disposal of an asset is taxed in the year in which it was sold or

disposed of. In accordance with provisions specified in section 102-5 (1) of ITAA 97 capital

gains are required to the treated as part of assessable income. In case an asset is owned for

more than one year than capital gain relating to the specified asset will be discounted to 50%

for entity taxpayers and 33.3% for superannuation funds. A capital loss can be settoff against

capital gain; however net capital loss cannot be adjusted against an ordinary business or other

income but can be carried forward for indefinite income (Chapter 4: Loss carry forward,

2015)

Short- Term Capital Gain

The specified gain are relating to the assets which have been held for a year or loss (Capital

Gains Tax. Timing of a real estate CGT event. 2019). The gain arising from stated assets in

taxed as ordinary income. Thus, the rate applied on wages, interest, other income can be

applied on the same.

Long Term Capital Gain

Above stated gains are relating to assets which are owned for a period of one year or more

are required to be taxed as long term capital gain (Capital Gain Tax. Working out your capital

On the basis of the above computation, it has been observed that the liability of fringe

benefits tax under the operating cost method is lower than the liability computed under the

statutory method. Therefore it is recommended that it is more appropriate for the employer to

apply operating cost method.

Question 2

Part A

In accordance with provision specified in the Australian taxation system; capital gain is a tax

applied in case capital gain has been incurred on the sale of the asset. A capital gain occurs in

case sale price received on an asset is more than the cost base (cost of acquisition) of a

specified asset. Cost base can be referred to as the price paid for the asset . Further,

improvement in asset increases the cost base,and depreciation of asset decreases the

same.Capital gain earned on disposal of an asset is taxed in the year in which it was sold or

disposed of. In accordance with provisions specified in section 102-5 (1) of ITAA 97 capital

gains are required to the treated as part of assessable income. In case an asset is owned for

more than one year than capital gain relating to the specified asset will be discounted to 50%

for entity taxpayers and 33.3% for superannuation funds. A capital loss can be settoff against

capital gain; however net capital loss cannot be adjusted against an ordinary business or other

income but can be carried forward for indefinite income (Chapter 4: Loss carry forward,

2015)

Short- Term Capital Gain

The specified gain are relating to the assets which have been held for a year or loss (Capital

Gains Tax. Timing of a real estate CGT event. 2019). The gain arising from stated assets in

taxed as ordinary income. Thus, the rate applied on wages, interest, other income can be

applied on the same.

Long Term Capital Gain

Above stated gains are relating to assets which are owned for a period of one year or more

are required to be taxed as long term capital gain (Capital Gain Tax. Working out your capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gain, 2018). The specified gains are taxed at more favorable tax rates. These rates variates

from 0% to 20% in accordance with the income of the taxpayer.

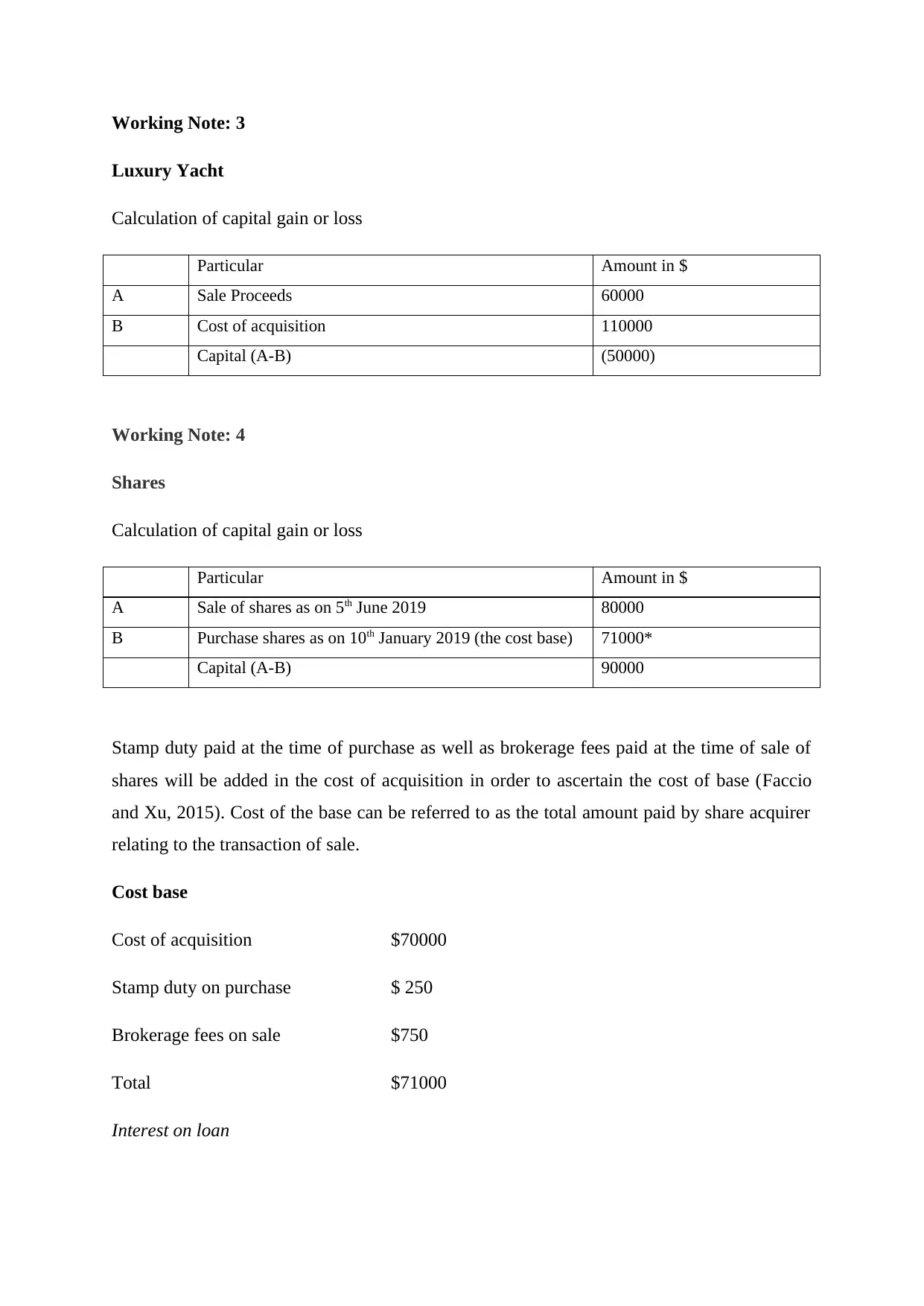

Working Note: 1

Sale of a house located at Doncaster (a suburb of Melbourne)

In accordance with taxation ruling, 1999/19 CGT which provides specification relating to the

accounting treatment of forfeited deposits in case the seller receives deposit by purchase and

same is forfeited by him. Further, the judgment of case law Josephine Binns v. the U.S., 385

F.2d 159 (6th Cir. 1967) relating to the decision of tax treatment for federal income tax

purpose can be applied in the present case. In the case of Josephine Binns, the issue rose

relating to the sale agreement in which he agreed to sell 26000 shares of a company at the

rate $43 per share. $ 75000 was paid as a down payment for the same. The stock was

delivered and placed in escrow. However, after the end of week purchase stated that he is not

able to complete the transaction and purchaser forfeited the amount received as a deposit. It

was concluded that the amount of forfeited is required to be accounted for as ordinary income

as the sale has not been completed. Thus, it can be assessed that as there is no sale or

exchange transaction and hence no recognition of capital gain or loss .

In the presentcase, as Daniel Ray forfeited the amount received at the time of auction from

the purchaser as he was not able to continue the transaction. Thus, the same will be treated as

ordinary income instead of capital gains. The amount paid to the real estate agent as sales

commission can be deducted as an expense against the amount which has been forfeited and

accounted as ordinary income.

Working Note: 2

An artistic piece of painting

Calculation of capital gain or loss

Particular Amount in $

A Sale Proceeds 125000

B Cost of acquisition 15000

Capital (A-B) 110000

from 0% to 20% in accordance with the income of the taxpayer.

Working Note: 1

Sale of a house located at Doncaster (a suburb of Melbourne)

In accordance with taxation ruling, 1999/19 CGT which provides specification relating to the

accounting treatment of forfeited deposits in case the seller receives deposit by purchase and

same is forfeited by him. Further, the judgment of case law Josephine Binns v. the U.S., 385

F.2d 159 (6th Cir. 1967) relating to the decision of tax treatment for federal income tax

purpose can be applied in the present case. In the case of Josephine Binns, the issue rose

relating to the sale agreement in which he agreed to sell 26000 shares of a company at the

rate $43 per share. $ 75000 was paid as a down payment for the same. The stock was

delivered and placed in escrow. However, after the end of week purchase stated that he is not

able to complete the transaction and purchaser forfeited the amount received as a deposit. It

was concluded that the amount of forfeited is required to be accounted for as ordinary income

as the sale has not been completed. Thus, it can be assessed that as there is no sale or

exchange transaction and hence no recognition of capital gain or loss .

In the presentcase, as Daniel Ray forfeited the amount received at the time of auction from

the purchaser as he was not able to continue the transaction. Thus, the same will be treated as

ordinary income instead of capital gains. The amount paid to the real estate agent as sales

commission can be deducted as an expense against the amount which has been forfeited and

accounted as ordinary income.

Working Note: 2

An artistic piece of painting

Calculation of capital gain or loss

Particular Amount in $

A Sale Proceeds 125000

B Cost of acquisition 15000

Capital (A-B) 110000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

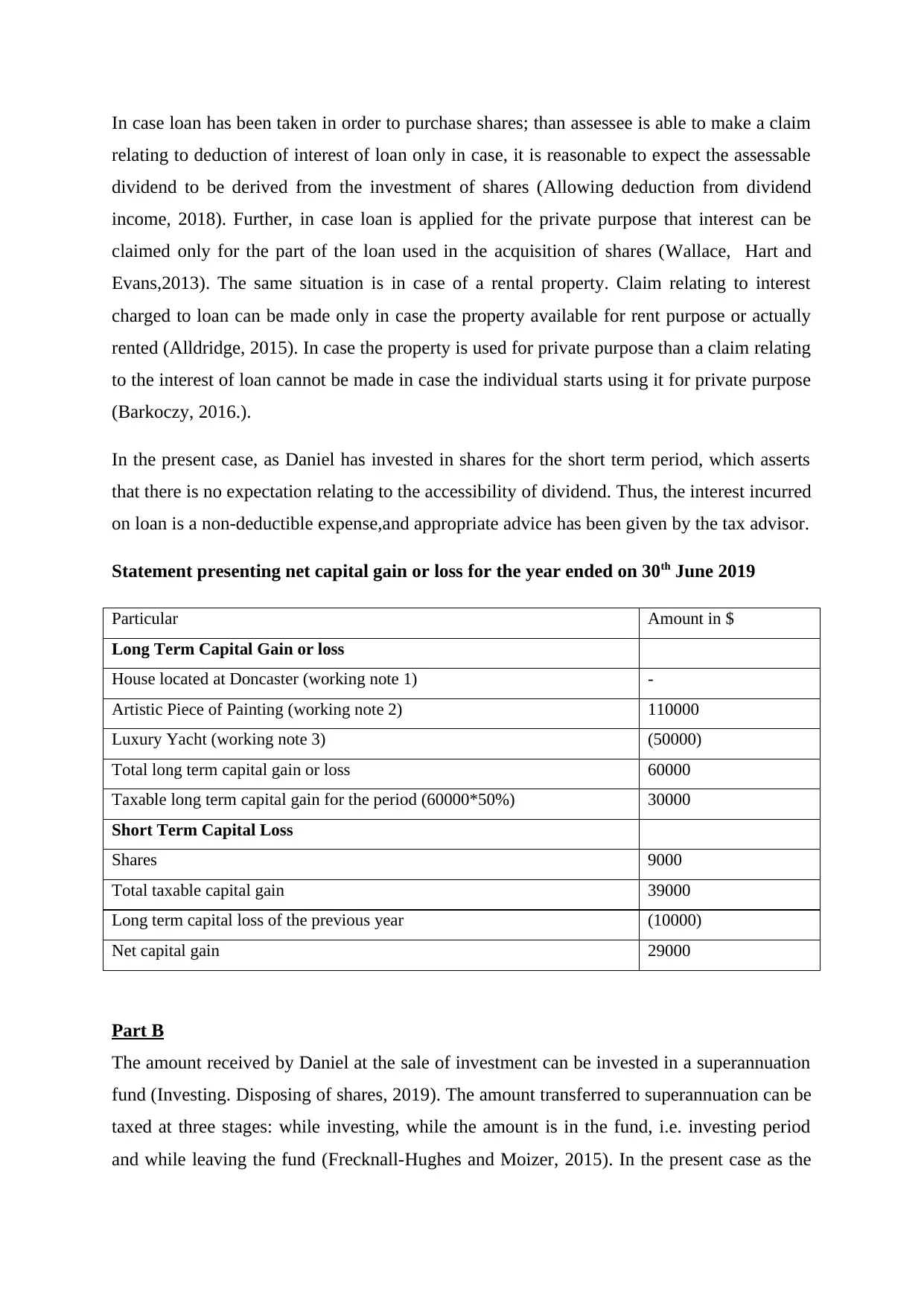

Working Note: 3

Luxury Yacht

Calculation of capital gain or loss

Particular Amount in $

A Sale Proceeds 60000

B Cost of acquisition 110000

Capital (A-B) (50000)

Working Note: 4

Shares

Calculation of capital gain or loss

Particular Amount in $

A Sale of shares as on 5th June 2019 80000

B Purchase shares as on 10th January 2019 (the cost base) 71000*

Capital (A-B) 90000

Stamp duty paid at the time of purchase as well as brokerage fees paid at the time of sale of

shares will be added in the cost of acquisition in order to ascertain the cost of base (Faccio

and Xu, 2015). Cost of the base can be referred to as the total amount paid by share acquirer

relating to the transaction of sale.

Cost base

Cost of acquisition $70000

Stamp duty on purchase $ 250

Brokerage fees on sale $750

Total $71000

Interest on loan

Luxury Yacht

Calculation of capital gain or loss

Particular Amount in $

A Sale Proceeds 60000

B Cost of acquisition 110000

Capital (A-B) (50000)

Working Note: 4

Shares

Calculation of capital gain or loss

Particular Amount in $

A Sale of shares as on 5th June 2019 80000

B Purchase shares as on 10th January 2019 (the cost base) 71000*

Capital (A-B) 90000

Stamp duty paid at the time of purchase as well as brokerage fees paid at the time of sale of

shares will be added in the cost of acquisition in order to ascertain the cost of base (Faccio

and Xu, 2015). Cost of the base can be referred to as the total amount paid by share acquirer

relating to the transaction of sale.

Cost base

Cost of acquisition $70000

Stamp duty on purchase $ 250

Brokerage fees on sale $750

Total $71000

Interest on loan

In case loan has been taken in order to purchase shares; than assessee is able to make a claim

relating to deduction of interest of loan only in case, it is reasonable to expect the assessable

dividend to be derived from the investment of shares (Allowing deduction from dividend

income, 2018). Further, in case loan is applied for the private purpose that interest can be

claimed only for the part of the loan used in the acquisition of shares (Wallace, Hart and

Evans,2013). The same situation is in case of a rental property. Claim relating to interest

charged to loan can be made only in case the property available for rent purpose or actually

rented (Alldridge, 2015). In case the property is used for private purpose than a claim relating

to the interest of loan cannot be made in case the individual starts using it for private purpose

(Barkoczy, 2016.).

In the present case, as Daniel has invested in shares for the short term period, which asserts

that there is no expectation relating to the accessibility of dividend. Thus, the interest incurred

on loan is a non-deductible expense,and appropriate advice has been given by the tax advisor.

Statement presenting net capital gain or loss for the year ended on 30th June 2019

Particular Amount in $

Long Term Capital Gain or loss

House located at Doncaster (working note 1) -

Artistic Piece of Painting (working note 2) 110000

Luxury Yacht (working note 3) (50000)

Total long term capital gain or loss 60000

Taxable long term capital gain for the period (60000*50%) 30000

Short Term Capital Loss

Shares 9000

Total taxable capital gain 39000

Long term capital loss of the previous year (10000)

Net capital gain 29000

Part B

The amount received by Daniel at the sale of investment can be invested in a superannuation

fund (Investing. Disposing of shares, 2019). The amount transferred to superannuation can be

taxed at three stages: while investing, while the amount is in the fund, i.e. investing period

and while leaving the fund (Frecknall-Hughes and Moizer, 2015). In the present case as the

relating to deduction of interest of loan only in case, it is reasonable to expect the assessable

dividend to be derived from the investment of shares (Allowing deduction from dividend

income, 2018). Further, in case loan is applied for the private purpose that interest can be

claimed only for the part of the loan used in the acquisition of shares (Wallace, Hart and

Evans,2013). The same situation is in case of a rental property. Claim relating to interest

charged to loan can be made only in case the property available for rent purpose or actually

rented (Alldridge, 2015). In case the property is used for private purpose than a claim relating

to the interest of loan cannot be made in case the individual starts using it for private purpose

(Barkoczy, 2016.).

In the present case, as Daniel has invested in shares for the short term period, which asserts

that there is no expectation relating to the accessibility of dividend. Thus, the interest incurred

on loan is a non-deductible expense,and appropriate advice has been given by the tax advisor.

Statement presenting net capital gain or loss for the year ended on 30th June 2019

Particular Amount in $

Long Term Capital Gain or loss

House located at Doncaster (working note 1) -

Artistic Piece of Painting (working note 2) 110000

Luxury Yacht (working note 3) (50000)

Total long term capital gain or loss 60000

Taxable long term capital gain for the period (60000*50%) 30000

Short Term Capital Loss

Shares 9000

Total taxable capital gain 39000

Long term capital loss of the previous year (10000)

Net capital gain 29000

Part B

The amount received by Daniel at the sale of investment can be invested in a superannuation

fund (Investing. Disposing of shares, 2019). The amount transferred to superannuation can be

taxed at three stages: while investing, while the amount is in the fund, i.e. investing period

and while leaving the fund (Frecknall-Hughes and Moizer, 2015). In the present case as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount invested in a superannuation fund is personal contribution than same will be not

taxed while they are transferred in the super fund. In the presentcase, as Daniel is making an

investment in order to plan his retirement, this amount will be withdrawn only after he turns

to 60. Thus, it is the best option for Daniel as the amount will withdrawn by a person having

after attaining age of 60 years, it will not be taxed.

Part C

In the presentcase, long term capital gain has occurred. However, in case capital loss would

have occurred than treatment of same would have been dependent on the nature of capital

loss,i.e. whether it is long term capital loss or short term capital loss (Barkoczy.,2016).

Australian taxation law allows carrying forward a loss for an indefinite period but at their

nominal amount only (Losses. How to claim a tax loss, 2019). Thus, in case capital loss has

been incurred as an investor (selling the asset after holding it for minimum one year) than

individual will be able to set off the same against existing capital gain as well as can carry

forward to offset against future capital gains.

taxed while they are transferred in the super fund. In the presentcase, as Daniel is making an

investment in order to plan his retirement, this amount will be withdrawn only after he turns

to 60. Thus, it is the best option for Daniel as the amount will withdrawn by a person having

after attaining age of 60 years, it will not be taxed.

Part C

In the presentcase, long term capital gain has occurred. However, in case capital loss would

have occurred than treatment of same would have been dependent on the nature of capital

loss,i.e. whether it is long term capital loss or short term capital loss (Barkoczy.,2016).

Australian taxation law allows carrying forward a loss for an indefinite period but at their

nominal amount only (Losses. How to claim a tax loss, 2019). Thus, in case capital loss has

been incurred as an investor (selling the asset after holding it for minimum one year) than

individual will be able to set off the same against existing capital gain as well as can carry

forward to offset against future capital gains.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals

Alldridge, P., 2015. Tax avoidance, tax evasion, money laundering,and the problem of

‘offshore.’ Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Barkoczy, S., 2016. Core tax legislation and study guide. OUP Catalogue.New York

Butler, C.,andCalcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Faccio, M. &Xu, J.(2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis. 50(03). Pp.277-300.

Frecknall-Hughes, J.,andMoizer, P., 2015. Assessing the quality of services provided by UK

tax practitioners. eJournal of Tax Research, 13(1), p.51.

Shields, J.,and North-Samardzic, A., 2015. 10 Employee benefits. Managing Employee

Performance and Reward: Concepts, Practices, Strategies, p.218.

Soled, J.A.,and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

Visser, A., 2017. Tax and employee transport. Tax Breaks Newsletter, 2017(376), pp.8-8.

Wallace, M., Hart, G.,and Evans, C., 2013. An evaluation of the contribution of Justice Hill

to the provisions for the taxing of capital gains in Australia. Austl. Tax F., 28, p.123.

Online

Allowing deduction from dividend income. 2018. Available through

<https://www.ato.gov.au/Forms/You-and-your-shares-2018/?page=11>. [Accessed on 16th

May 2019]

Australian Taxation Office, 2019.Fringe Benefits Tax – rates and thresholds . (online).

Available through<https://www.ato.gov.au/rates/fbt/?page=1#Fringe_benefits_tax_rates>

[Accessed on 16th May 2019]

Books and Journals

Alldridge, P., 2015. Tax avoidance, tax evasion, money laundering,and the problem of

‘offshore.’ Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Barkoczy, S., 2016. Core tax legislation and study guide. OUP Catalogue.New York

Butler, C.,andCalcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Faccio, M. &Xu, J.(2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis. 50(03). Pp.277-300.

Frecknall-Hughes, J.,andMoizer, P., 2015. Assessing the quality of services provided by UK

tax practitioners. eJournal of Tax Research, 13(1), p.51.

Shields, J.,and North-Samardzic, A., 2015. 10 Employee benefits. Managing Employee

Performance and Reward: Concepts, Practices, Strategies, p.218.

Soled, J.A.,and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

Visser, A., 2017. Tax and employee transport. Tax Breaks Newsletter, 2017(376), pp.8-8.

Wallace, M., Hart, G.,and Evans, C., 2013. An evaluation of the contribution of Justice Hill

to the provisions for the taxing of capital gains in Australia. Austl. Tax F., 28, p.123.

Online

Allowing deduction from dividend income. 2018. Available through

<https://www.ato.gov.au/Forms/You-and-your-shares-2018/?page=11>. [Accessed on 16th

May 2019]

Australian Taxation Office, 2019.Fringe Benefits Tax – rates and thresholds . (online).

Available through<https://www.ato.gov.au/rates/fbt/?page=1#Fringe_benefits_tax_rates>

[Accessed on 16th May 2019]

Capital Gain Tax. Working out your capital gain. 2018. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 16th May 2019].

Capital Gains Tax. Timing of a real estate CGT event. 2019. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/Timing-

of-a-real-estate-CGT-event/>. [Accessed on 16th May 2019]

Chapter 4: Loss carry forward. 2015. Available through

<https://treasury.gov.au/publication/business-tax-working-group-final-report-on-the-tax-

treatment-of-losses/final-report-on-the-tax-treatment-of-losses/chapter-4-loss-carry-forward>.

[Accessed on 16th May 2019].

Investing. Disposing of shares. 2019. Available through

<https://www.ato.gov.au/individuals/investing/investing-in-shares/disposing-of-shares/>.

[Accessed on 16th May 2019].

Losses. How to claim a tax loss. 2019. Available through

<https://www.ato.gov.au/General/Losses/How-to-claim-a-tax-loss/>. [Accessed on 16th May

2019]

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 16th May 2019].

Capital Gains Tax. Timing of a real estate CGT event. 2019. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/Timing-

of-a-real-estate-CGT-event/>. [Accessed on 16th May 2019]

Chapter 4: Loss carry forward. 2015. Available through

<https://treasury.gov.au/publication/business-tax-working-group-final-report-on-the-tax-

treatment-of-losses/final-report-on-the-tax-treatment-of-losses/chapter-4-loss-carry-forward>.

[Accessed on 16th May 2019].

Investing. Disposing of shares. 2019. Available through

<https://www.ato.gov.au/individuals/investing/investing-in-shares/disposing-of-shares/>.

[Accessed on 16th May 2019].

Losses. How to claim a tax loss. 2019. Available through

<https://www.ato.gov.au/General/Losses/How-to-claim-a-tax-loss/>. [Accessed on 16th May

2019]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.