Dominic's Tax Obligations: FBT, Capital Gains, and Deductions

VerifiedAdded on 2023/01/11

|7

|1299

|55

Project

AI Summary

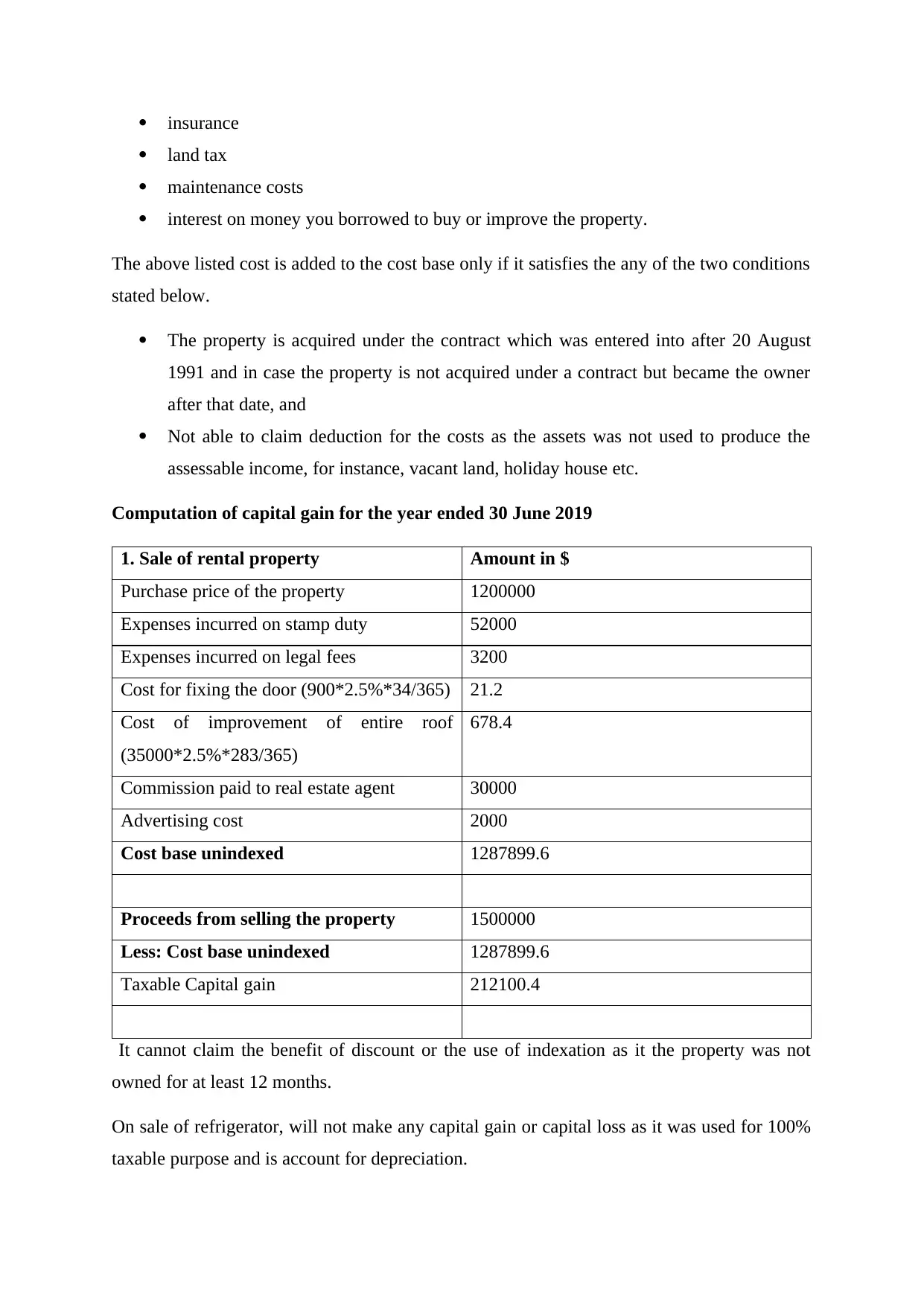

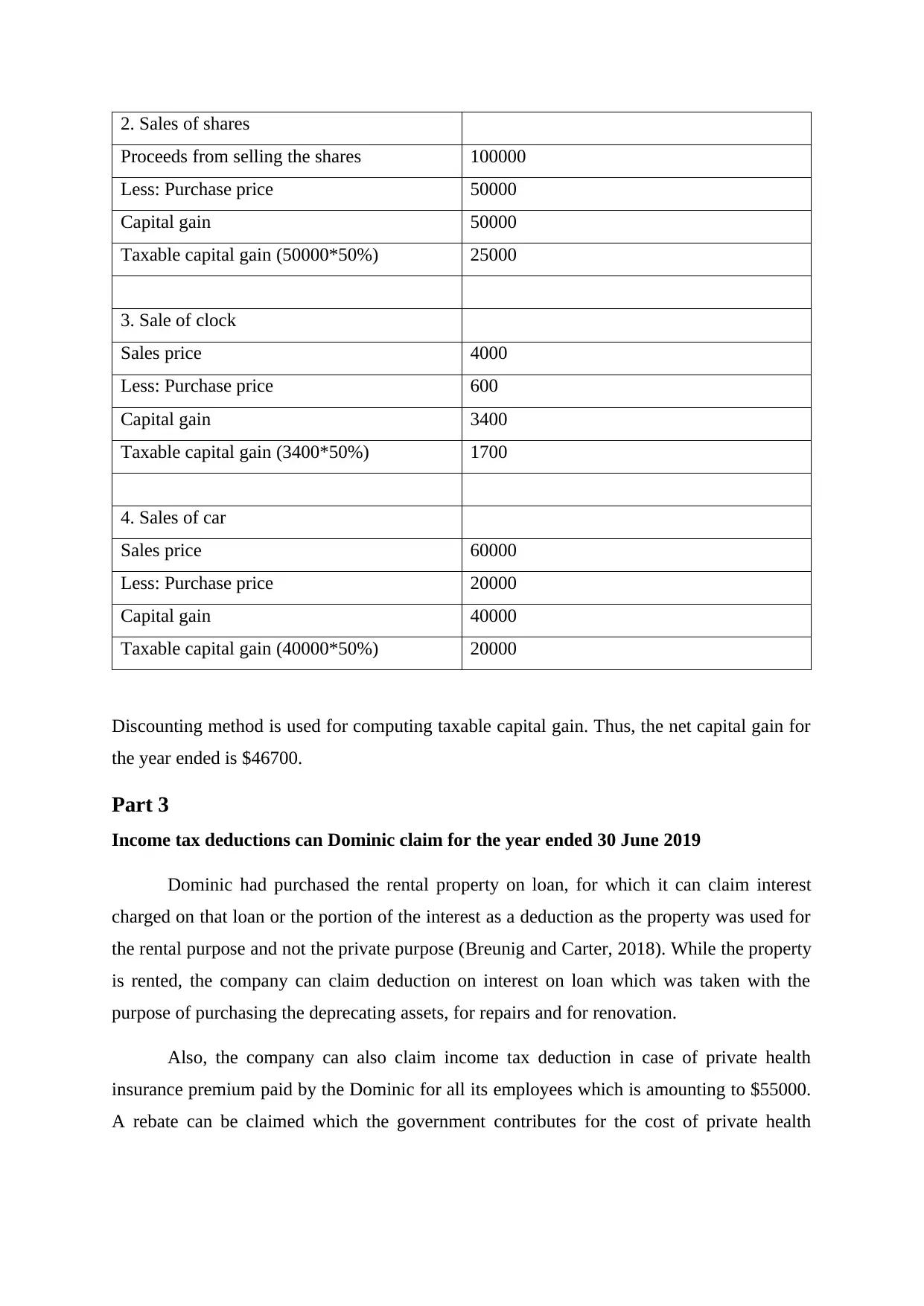

This project analyzes Dominic's tax obligations for the year ended 31 March 2019 and 30 June 2019. Part 1 focuses on Fringe Benefits Tax (FBT) calculations, comparing the statutory and operating cost methods for a company vehicle, concluding that the operating cost method results in a lower taxable value. Part 2 addresses Dominic's net capital gain or loss, calculating capital gains from the sale of a rental property, shares, a clock, and a car, ultimately determining a net capital gain for the year. Part 3 examines income tax deductions Dominic can claim, including interest on a loan for the rental property and deductions for private health insurance premiums paid for employees. The project references relevant books and journals to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.