Calculating FBT Liability and Reportable Fringe Benefits in Tax Law

VerifiedAdded on 2023/02/01

|10

|2155

|68

Homework Assignment

AI Summary

This tax law assignment analyzes the FBT liability of Logan Landscapes Pty Ltd for providing a dual-cab vehicle and reimbursing mobile phone expenses to its employee, Jackson. The solution calculates the taxable value of the car fringe benefit using both the statutory formula and the operating cost method, ultimately determining the lower value to be used. It also addresses the mobile phone expense payment, classifying it as an expense payment fringe benefit and calculating its taxable value. The assignment then calculates the total FBT payable, considering gross-up calculations. Finally, it determines whether Jackson has reportable fringe benefits, based on the total value of benefits received and the relevant thresholds, and determines the amount to be included on Jackson’s PAYG payment summary.

Tax Law

30 June 2019

Seminar Number 6 T1 2019

Question 1

Logan Landscapes Pty Ltd purchased a new Dual-cab vehicle for their employee Jackson to

use for both work and private purposes on 1 October 2018. The car cost $32,000 and they

paid an extra $4,600 to have a canopy installed at the time. The car was provided to Jackson

for his use (both work and private) from that date. Jackson was required to keep a logbook.

This showed that 9,000 km were travelled for a twelve week period during 1 October -

31 March 2019, and of these, 4,500 km were for business purposes.

Unfortunately in mid-January Jackson was involved in a traffic accident, which caused a

substantial amount of damage to the vehicle. The repairs cost $2,750 (which was covered by

insurance) and the car was off the road for 14 days while the repairs were being done.

Other expenses incurred by Logan Landscapes Pty Ltd relating to the vehicle were:

Registration & insurance $1,450 (for 12 months), which was paid on 1 October 2018

Fuel: $3,600

Jackson paid out $360 for petrol and oil to the local service station in respect of the vehicle,

and is able to substantiate these payments. Jackson also contributed to the car insurance by

paying $280 directly to Logan Landscapes.

Note that Logan Landscapes Pty Ltd is registered for GST and that where relevant the costs

mentioned above include GST.

Logan Landscapes Pty Ltd has elected to use the operating cost basis under section 10

FBTAA for the vehicle.

Logan Landscapes Pty Ltd also pays Telstra directly for Jacksons’ mobile phone expenses

from 1st October to 31 March which equates to $1,800 (inc GST) – as he uses his own mobile

phone for work purposes. Jackson estimates that 40% of his mobile phone use is for work

purposes.

Required:

(1) Work out whether Logan Landscapes Pty Ltd has a FBT liability in respect of

providing the vehicle and reimbursing Jackson for his mobile phone bill. If they

do, calculate how much that liability would be for the 2019 FBT year.

(2) Work out if Jackson would have a reportable fringe benefit in respect of the

vehicle provided to him and the mobile phone reimbursement from Logan

Landscapes.

1

30 June 2019

Seminar Number 6 T1 2019

Question 1

Logan Landscapes Pty Ltd purchased a new Dual-cab vehicle for their employee Jackson to

use for both work and private purposes on 1 October 2018. The car cost $32,000 and they

paid an extra $4,600 to have a canopy installed at the time. The car was provided to Jackson

for his use (both work and private) from that date. Jackson was required to keep a logbook.

This showed that 9,000 km were travelled for a twelve week period during 1 October -

31 March 2019, and of these, 4,500 km were for business purposes.

Unfortunately in mid-January Jackson was involved in a traffic accident, which caused a

substantial amount of damage to the vehicle. The repairs cost $2,750 (which was covered by

insurance) and the car was off the road for 14 days while the repairs were being done.

Other expenses incurred by Logan Landscapes Pty Ltd relating to the vehicle were:

Registration & insurance $1,450 (for 12 months), which was paid on 1 October 2018

Fuel: $3,600

Jackson paid out $360 for petrol and oil to the local service station in respect of the vehicle,

and is able to substantiate these payments. Jackson also contributed to the car insurance by

paying $280 directly to Logan Landscapes.

Note that Logan Landscapes Pty Ltd is registered for GST and that where relevant the costs

mentioned above include GST.

Logan Landscapes Pty Ltd has elected to use the operating cost basis under section 10

FBTAA for the vehicle.

Logan Landscapes Pty Ltd also pays Telstra directly for Jacksons’ mobile phone expenses

from 1st October to 31 March which equates to $1,800 (inc GST) – as he uses his own mobile

phone for work purposes. Jackson estimates that 40% of his mobile phone use is for work

purposes.

Required:

(1) Work out whether Logan Landscapes Pty Ltd has a FBT liability in respect of

providing the vehicle and reimbursing Jackson for his mobile phone bill. If they

do, calculate how much that liability would be for the 2019 FBT year.

(2) Work out if Jackson would have a reportable fringe benefit in respect of the

vehicle provided to him and the mobile phone reimbursement from Logan

Landscapes.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

Group One

ISSUE (1) – Is Logan Landscapes Pty Ltd liable for FBT on the vehicle provided to

Jackson?

STEP 1 – Is there a fringe benefit?

‘Fringe benefit’ is defined in s_____136 of ____ FBTAA. There are five elements to a fringe

benefit:

(i) There must be a benefit – (apply to the facts) ______Jackson is able to use car

for private purpose. Hence, benefit accrues to employee _____________________

(ii) Provided during the year – (apply to the facts) __1st October, 2018 to 31st March,

2019_________________________

(iii) By an employer, associate, or third party arranger or other relevant person –

(apply to the facts) Employer, Logan Landscape Pty

Limited___________________________

(iv) To an employee or an associate – (apply to the facts) ______Employee,

Jackson_____________________

(v) In respect of the employment of the employee –(apply to the facts) _______In

respect of employment as Jackson is employee of Logan Landscape Pty Limited

____________________

Yes or No, a fringe benefit exists.

What kind of fringe benefit is it?

Subsection ______1 of Section 7____ FBTAA a car benefit arises on any day, if:

In respect of employment

–(apply to the facts) _a car has been held by Jackson for both private and

business use. Further, the car has been provided by

employer__________________________

A car

“Car” is defined in s ____136_____to mean

_______________________________a motor car, station wagon, panel van, utility

truck or similar vehicle or any other form of road vehicle designed to carry a load of

less than 1 tonne or fewer than 9 passengers.

(Commonwealth Numbered Acts, 2019)

Is held by an employer or associate or third party provider AND

(apply to the facts) _has been made available for private use of employee, Jackson

during the concerned year.__________________________

Is applied to or available for the private use of an employee or associate

2

30 June 2019

Group One

ISSUE (1) – Is Logan Landscapes Pty Ltd liable for FBT on the vehicle provided to

Jackson?

STEP 1 – Is there a fringe benefit?

‘Fringe benefit’ is defined in s_____136 of ____ FBTAA. There are five elements to a fringe

benefit:

(i) There must be a benefit – (apply to the facts) ______Jackson is able to use car

for private purpose. Hence, benefit accrues to employee _____________________

(ii) Provided during the year – (apply to the facts) __1st October, 2018 to 31st March,

2019_________________________

(iii) By an employer, associate, or third party arranger or other relevant person –

(apply to the facts) Employer, Logan Landscape Pty

Limited___________________________

(iv) To an employee or an associate – (apply to the facts) ______Employee,

Jackson_____________________

(v) In respect of the employment of the employee –(apply to the facts) _______In

respect of employment as Jackson is employee of Logan Landscape Pty Limited

____________________

Yes or No, a fringe benefit exists.

What kind of fringe benefit is it?

Subsection ______1 of Section 7____ FBTAA a car benefit arises on any day, if:

In respect of employment

–(apply to the facts) _a car has been held by Jackson for both private and

business use. Further, the car has been provided by

employer__________________________

A car

“Car” is defined in s ____136_____to mean

_______________________________a motor car, station wagon, panel van, utility

truck or similar vehicle or any other form of road vehicle designed to carry a load of

less than 1 tonne or fewer than 9 passengers.

(Commonwealth Numbered Acts, 2019)

Is held by an employer or associate or third party provider AND

(apply to the facts) _has been made available for private use of employee, Jackson

during the concerned year.__________________________

Is applied to or available for the private use of an employee or associate

2

Tax Law

30 June 2019

“Private use” includes any use which is _____not used in the course of producing

assessable income _______________________________________________ of

the employee: s 136(1)

apply to the facts) _Car has been used for private purpose by Jackson and not for

exclusive use of business__________________________

___________________________

Therefore the car provided to Jackson by Logan Landscapes Pty Ltd is a car fringe benefit

as per s7(1) FBTAA 1986 because: _the same is provided by an employer to employee and is

used for private purpose of the employee_____________________________

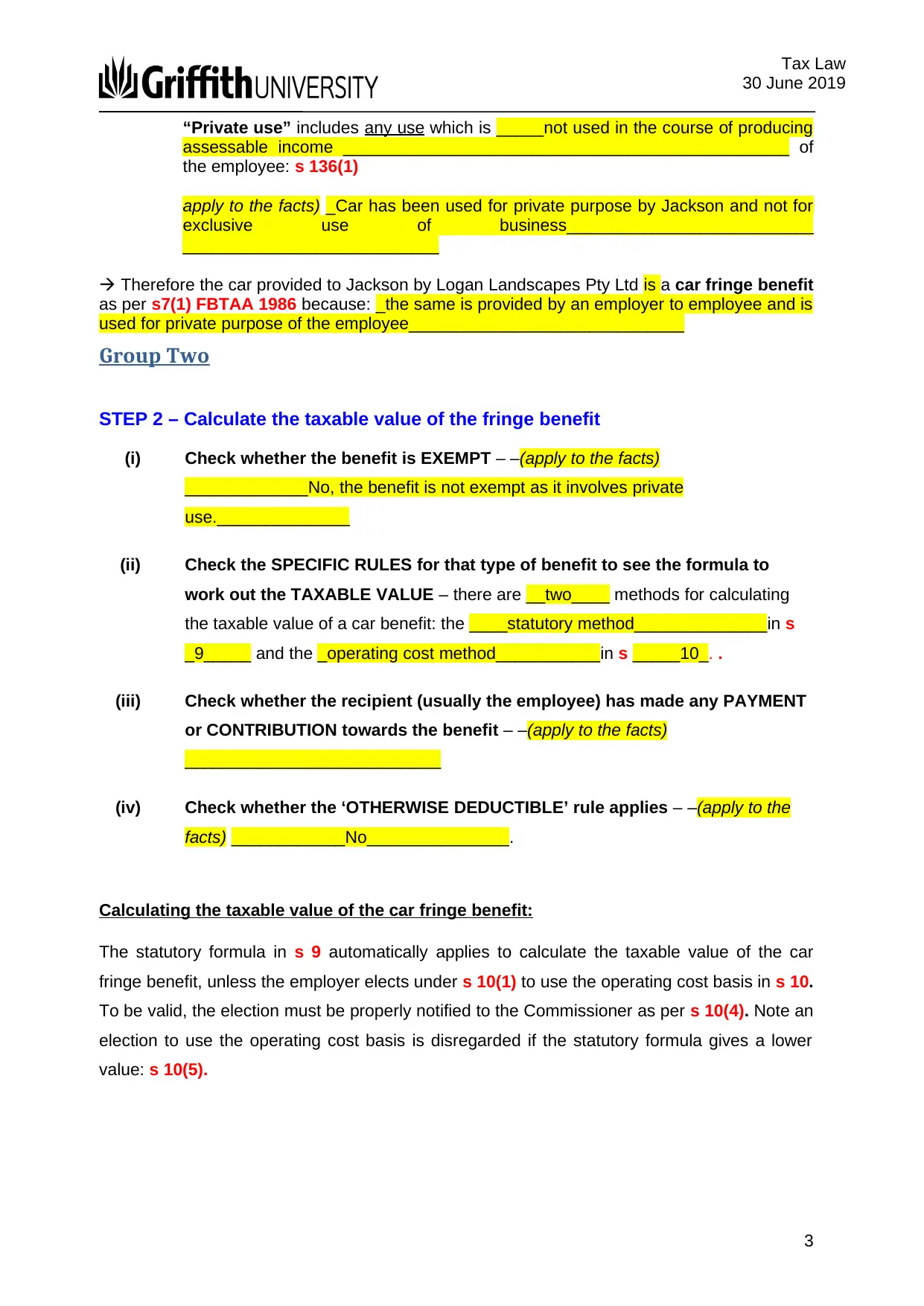

Group Two

STEP 2 – Calculate the taxable value of the fringe benefit

(i) Check whether the benefit is EXEMPT – –(apply to the facts)

_____________No, the benefit is not exempt as it involves private

use.______________

(ii) Check the SPECIFIC RULES for that type of benefit to see the formula to

work out the TAXABLE VALUE – there are __two____ methods for calculating

the taxable value of a car benefit: the ____statutory method______________in s

_9_____ and the _operating cost method___________in s _____10_. .

(iii) Check whether the recipient (usually the employee) has made any PAYMENT

or CONTRIBUTION towards the benefit – –(apply to the facts)

___________________________

(iv) Check whether the ‘OTHERWISE DEDUCTIBLE’ rule applies – –(apply to the

facts) ____________No_______________.

Calculating the taxable value of the car fringe benefit:

The statutory formula in s 9 automatically applies to calculate the taxable value of the car

fringe benefit, unless the employer elects under s 10(1) to use the operating cost basis in s 10.

To be valid, the election must be properly notified to the Commissioner as per s 10(4). Note an

election to use the operating cost basis is disregarded if the statutory formula gives a lower

value: s 10(5).

3

30 June 2019

“Private use” includes any use which is _____not used in the course of producing

assessable income _______________________________________________ of

the employee: s 136(1)

apply to the facts) _Car has been used for private purpose by Jackson and not for

exclusive use of business__________________________

___________________________

Therefore the car provided to Jackson by Logan Landscapes Pty Ltd is a car fringe benefit

as per s7(1) FBTAA 1986 because: _the same is provided by an employer to employee and is

used for private purpose of the employee_____________________________

Group Two

STEP 2 – Calculate the taxable value of the fringe benefit

(i) Check whether the benefit is EXEMPT – –(apply to the facts)

_____________No, the benefit is not exempt as it involves private

use.______________

(ii) Check the SPECIFIC RULES for that type of benefit to see the formula to

work out the TAXABLE VALUE – there are __two____ methods for calculating

the taxable value of a car benefit: the ____statutory method______________in s

_9_____ and the _operating cost method___________in s _____10_. .

(iii) Check whether the recipient (usually the employee) has made any PAYMENT

or CONTRIBUTION towards the benefit – –(apply to the facts)

___________________________

(iv) Check whether the ‘OTHERWISE DEDUCTIBLE’ rule applies – –(apply to the

facts) ____________No_______________.

Calculating the taxable value of the car fringe benefit:

The statutory formula in s 9 automatically applies to calculate the taxable value of the car

fringe benefit, unless the employer elects under s 10(1) to use the operating cost basis in s 10.

To be valid, the election must be properly notified to the Commissioner as per s 10(4). Note an

election to use the operating cost basis is disregarded if the statutory formula gives a lower

value: s 10(5).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

As Logan Landscapes Pty Ltd made an election to use the operating cost basis method, we

will need to calculate the taxable value under both methods to see which method gives

the lower value.

** Note all figures are rounded up or down for the sake of simplicity **

4

30 June 2019

As Logan Landscapes Pty Ltd made an election to use the operating cost basis method, we

will need to calculate the taxable value under both methods to see which method gives

the lower value.

** Note all figures are rounded up or down for the sake of simplicity **

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

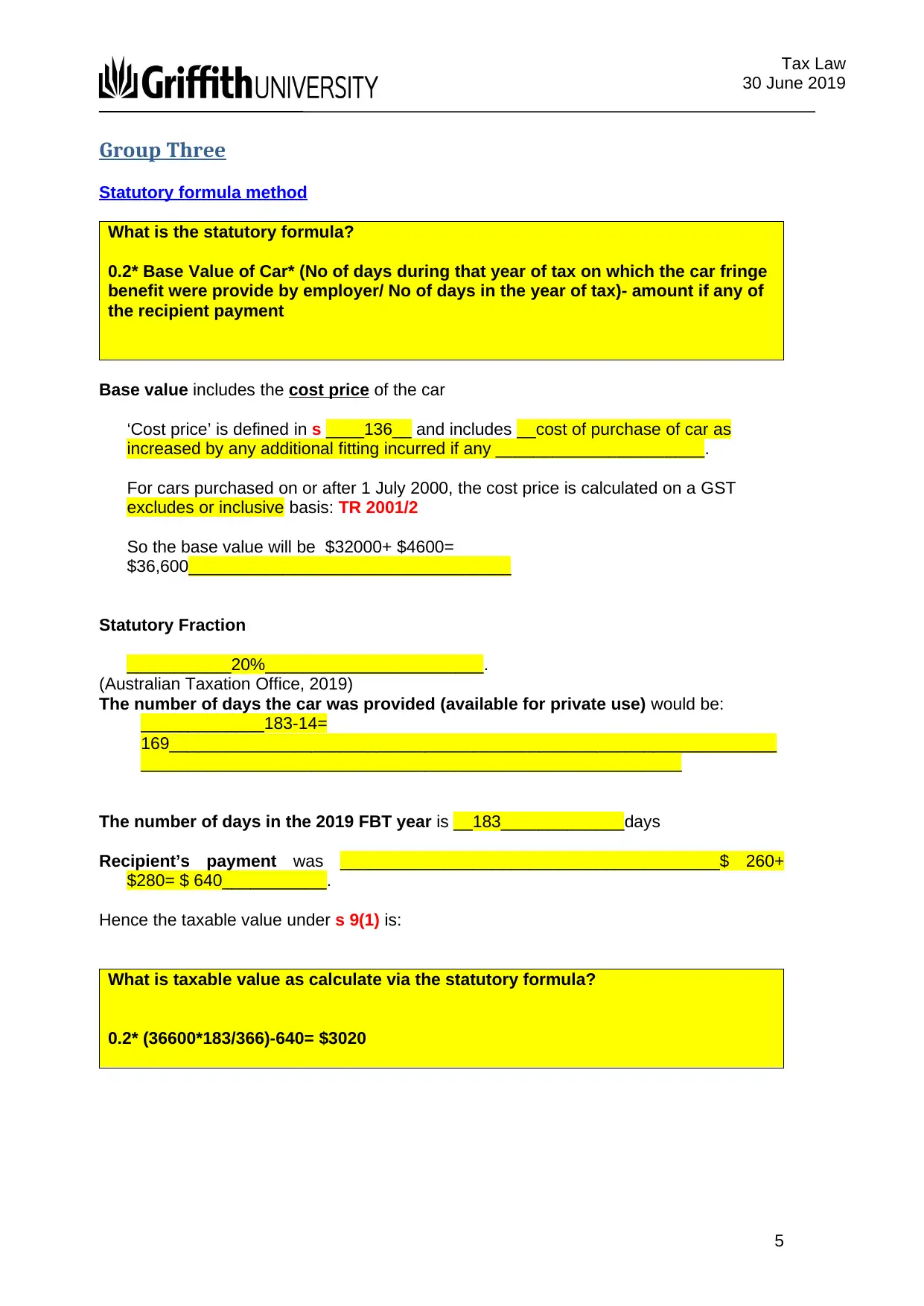

Group Three

Statutory formula method

What is the statutory formula?

0.2* Base Value of Car* (No of days during that year of tax on which the car fringe

benefit were provide by employer/ No of days in the year of tax)- amount if any of

the recipient payment

Base value includes the cost price of the car

‘Cost price’ is defined in s ____136__ and includes __cost of purchase of car as

increased by any additional fitting incurred if any ______________________.

For cars purchased on or after 1 July 2000, the cost price is calculated on a GST

excludes or inclusive basis: TR 2001/2

So the base value will be $32000+ $4600=

$36,600__________________________________

Statutory Fraction

___________20%_______________________.

(Australian Taxation Office, 2019)

The number of days the car was provided (available for private use) would be:

_____________183-14=

169________________________________________________________________

_________________________________________________________

The number of days in the 2019 FBT year is __183_____________days

Recipient’s payment was ________________________________________$ 260+

$280= $ 640___________.

Hence the taxable value under s 9(1) is:

What is taxable value as calculate via the statutory formula?

0.2* (36600*183/366)-640= $3020

5

30 June 2019

Group Three

Statutory formula method

What is the statutory formula?

0.2* Base Value of Car* (No of days during that year of tax on which the car fringe

benefit were provide by employer/ No of days in the year of tax)- amount if any of

the recipient payment

Base value includes the cost price of the car

‘Cost price’ is defined in s ____136__ and includes __cost of purchase of car as

increased by any additional fitting incurred if any ______________________.

For cars purchased on or after 1 July 2000, the cost price is calculated on a GST

excludes or inclusive basis: TR 2001/2

So the base value will be $32000+ $4600=

$36,600__________________________________

Statutory Fraction

___________20%_______________________.

(Australian Taxation Office, 2019)

The number of days the car was provided (available for private use) would be:

_____________183-14=

169________________________________________________________________

_________________________________________________________

The number of days in the 2019 FBT year is __183_____________days

Recipient’s payment was ________________________________________$ 260+

$280= $ 640___________.

Hence the taxable value under s 9(1) is:

What is taxable value as calculate via the statutory formula?

0.2* (36600*183/366)-640= $3020

5

Tax Law

30 June 2019

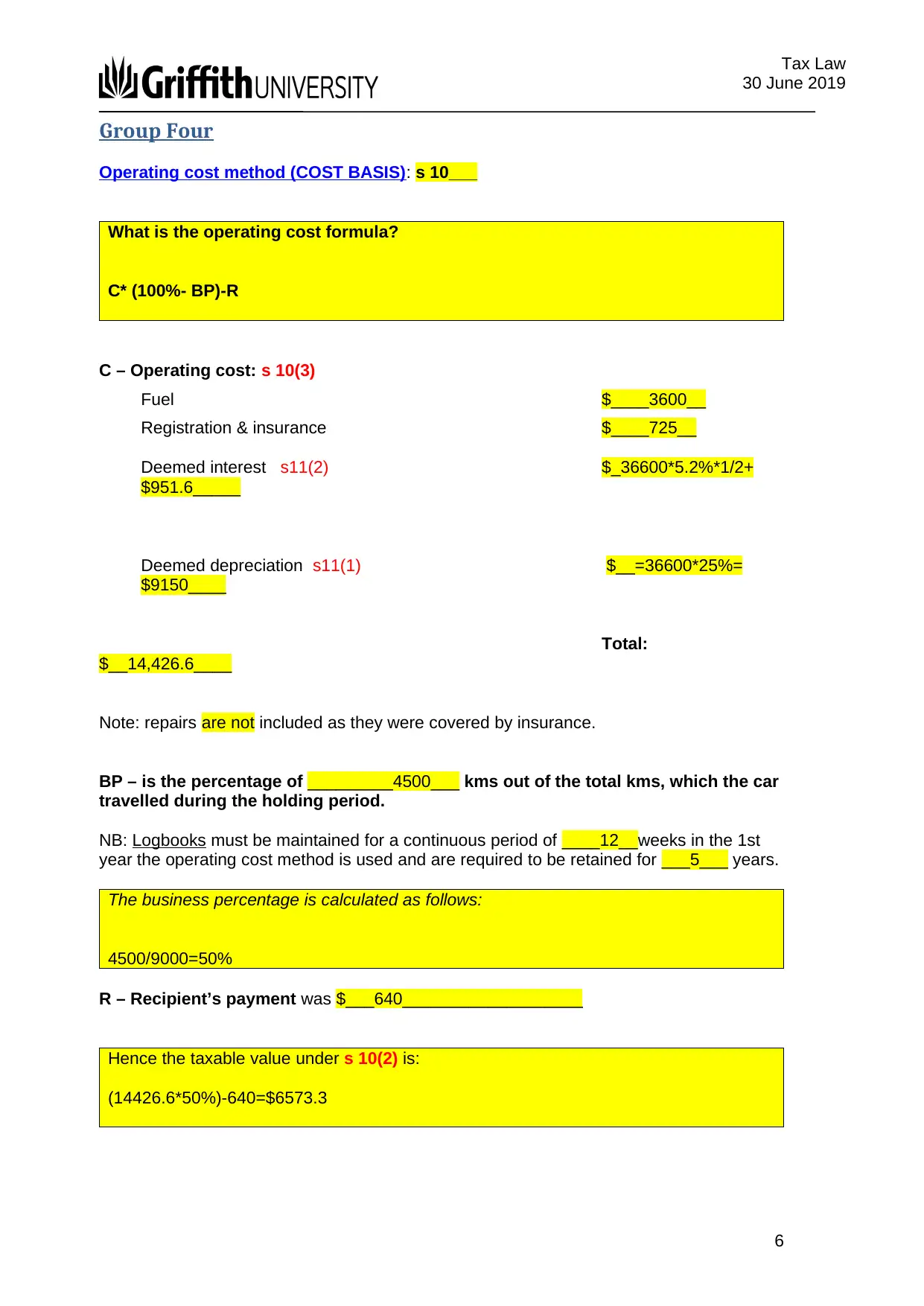

Group Four

Operating cost method (COST BASIS): s 10___

What is the operating cost formula?

C* (100%- BP)-R

C – Operating cost: s 10(3)

Fuel $____3600__

Registration & insurance $____725__

Deemed interest s11(2) $_36600*5.2%*1/2+

$951.6_____

Deemed depreciation s11(1) $__=36600*25%=

$9150____

Total:

$__14,426.6____

Note: repairs are not included as they were covered by insurance.

BP – is the percentage of _________4500___ kms out of the total kms, which the car

travelled during the holding period.

NB: Logbooks must be maintained for a continuous period of ____12__weeks in the 1st

year the operating cost method is used and are required to be retained for ___5___ years.

The business percentage is calculated as follows:

4500/9000=50%

R – Recipient’s payment was $___640___________________

Hence the taxable value under s 10(2) is:

(14426.6*50%)-640=$6573.3

6

30 June 2019

Group Four

Operating cost method (COST BASIS): s 10___

What is the operating cost formula?

C* (100%- BP)-R

C – Operating cost: s 10(3)

Fuel $____3600__

Registration & insurance $____725__

Deemed interest s11(2) $_36600*5.2%*1/2+

$951.6_____

Deemed depreciation s11(1) $__=36600*25%=

$9150____

Total:

$__14,426.6____

Note: repairs are not included as they were covered by insurance.

BP – is the percentage of _________4500___ kms out of the total kms, which the car

travelled during the holding period.

NB: Logbooks must be maintained for a continuous period of ____12__weeks in the 1st

year the operating cost method is used and are required to be retained for ___5___ years.

The business percentage is calculated as follows:

4500/9000=50%

R – Recipient’s payment was $___640___________________

Hence the taxable value under s 10(2) is:

(14426.6*50%)-640=$6573.3

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

Logan Landscapes Pty Ltd election to use the operating cost method would be

____disregarded______ as the statutory formula gives a lower taxable value:

s_10(5)________:.

7

30 June 2019

Logan Landscapes Pty Ltd election to use the operating cost method would be

____disregarded______ as the statutory formula gives a lower taxable value:

s_10(5)________:.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

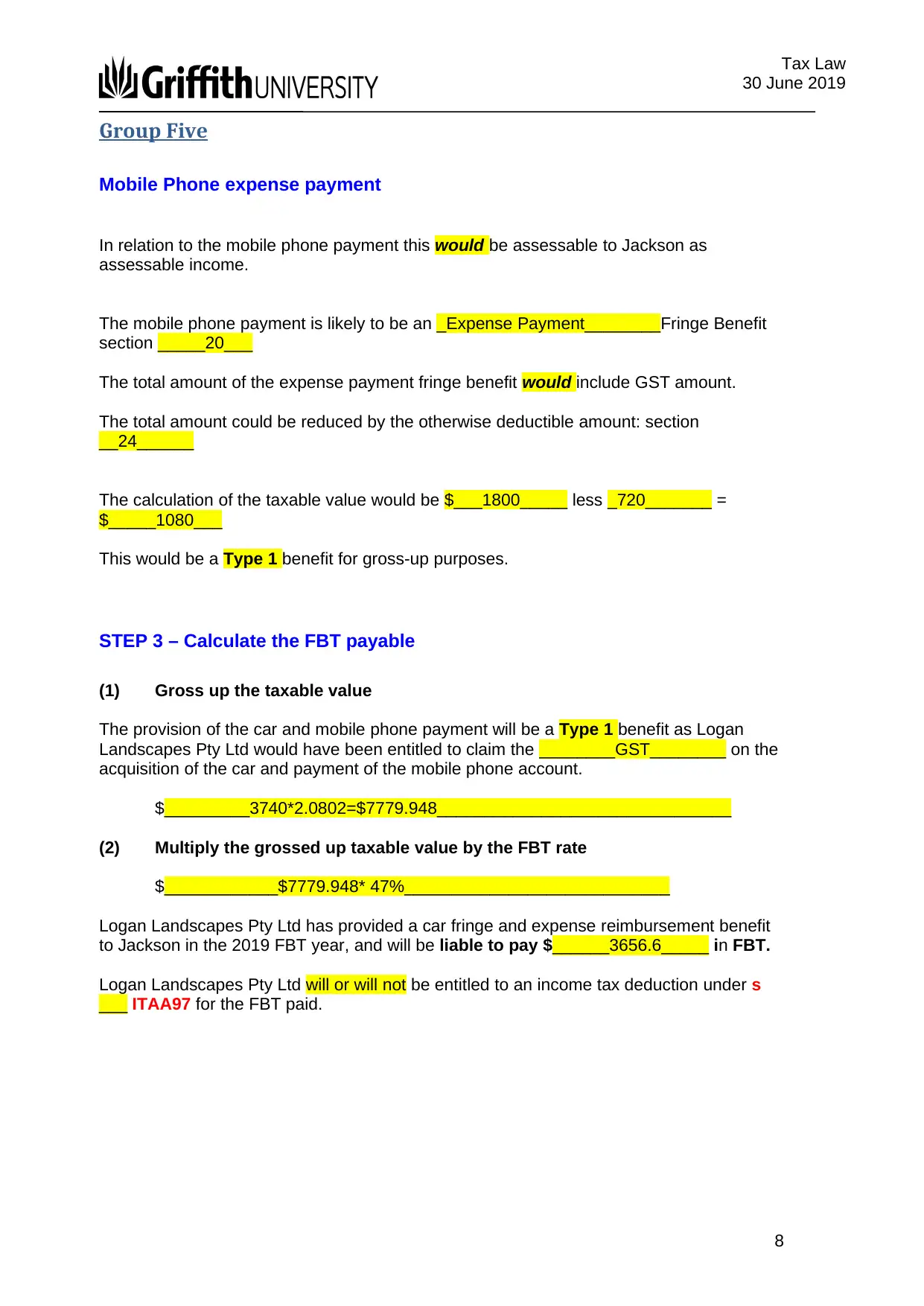

Group Five

Mobile Phone expense payment

In relation to the mobile phone payment this would be assessable to Jackson as

assessable income.

The mobile phone payment is likely to be an _Expense Payment________Fringe Benefit

section _____20___

The total amount of the expense payment fringe benefit would include GST amount.

The total amount could be reduced by the otherwise deductible amount: section

__24______

The calculation of the taxable value would be $___1800_____ less _720_______ =

$_____1080___

This would be a Type 1 benefit for gross-up purposes.

STEP 3 – Calculate the FBT payable

(1) Gross up the taxable value

The provision of the car and mobile phone payment will be a Type 1 benefit as Logan

Landscapes Pty Ltd would have been entitled to claim the ________GST________ on the

acquisition of the car and payment of the mobile phone account.

$_________3740*2.0802=$7779.948_______________________________

(2) Multiply the grossed up taxable value by the FBT rate

$____________$7779.948* 47%____________________________

Logan Landscapes Pty Ltd has provided a car fringe and expense reimbursement benefit

to Jackson in the 2019 FBT year, and will be liable to pay $______3656.6_____ in FBT.

Logan Landscapes Pty Ltd will or will not be entitled to an income tax deduction under s

___ ITAA97 for the FBT paid.

8

30 June 2019

Group Five

Mobile Phone expense payment

In relation to the mobile phone payment this would be assessable to Jackson as

assessable income.

The mobile phone payment is likely to be an _Expense Payment________Fringe Benefit

section _____20___

The total amount of the expense payment fringe benefit would include GST amount.

The total amount could be reduced by the otherwise deductible amount: section

__24______

The calculation of the taxable value would be $___1800_____ less _720_______ =

$_____1080___

This would be a Type 1 benefit for gross-up purposes.

STEP 3 – Calculate the FBT payable

(1) Gross up the taxable value

The provision of the car and mobile phone payment will be a Type 1 benefit as Logan

Landscapes Pty Ltd would have been entitled to claim the ________GST________ on the

acquisition of the car and payment of the mobile phone account.

$_________3740*2.0802=$7779.948_______________________________

(2) Multiply the grossed up taxable value by the FBT rate

$____________$7779.948* 47%____________________________

Logan Landscapes Pty Ltd has provided a car fringe and expense reimbursement benefit

to Jackson in the 2019 FBT year, and will be liable to pay $______3656.6_____ in FBT.

Logan Landscapes Pty Ltd will or will not be entitled to an income tax deduction under s

___ ITAA97 for the FBT paid.

8

Tax Law

30 June 2019

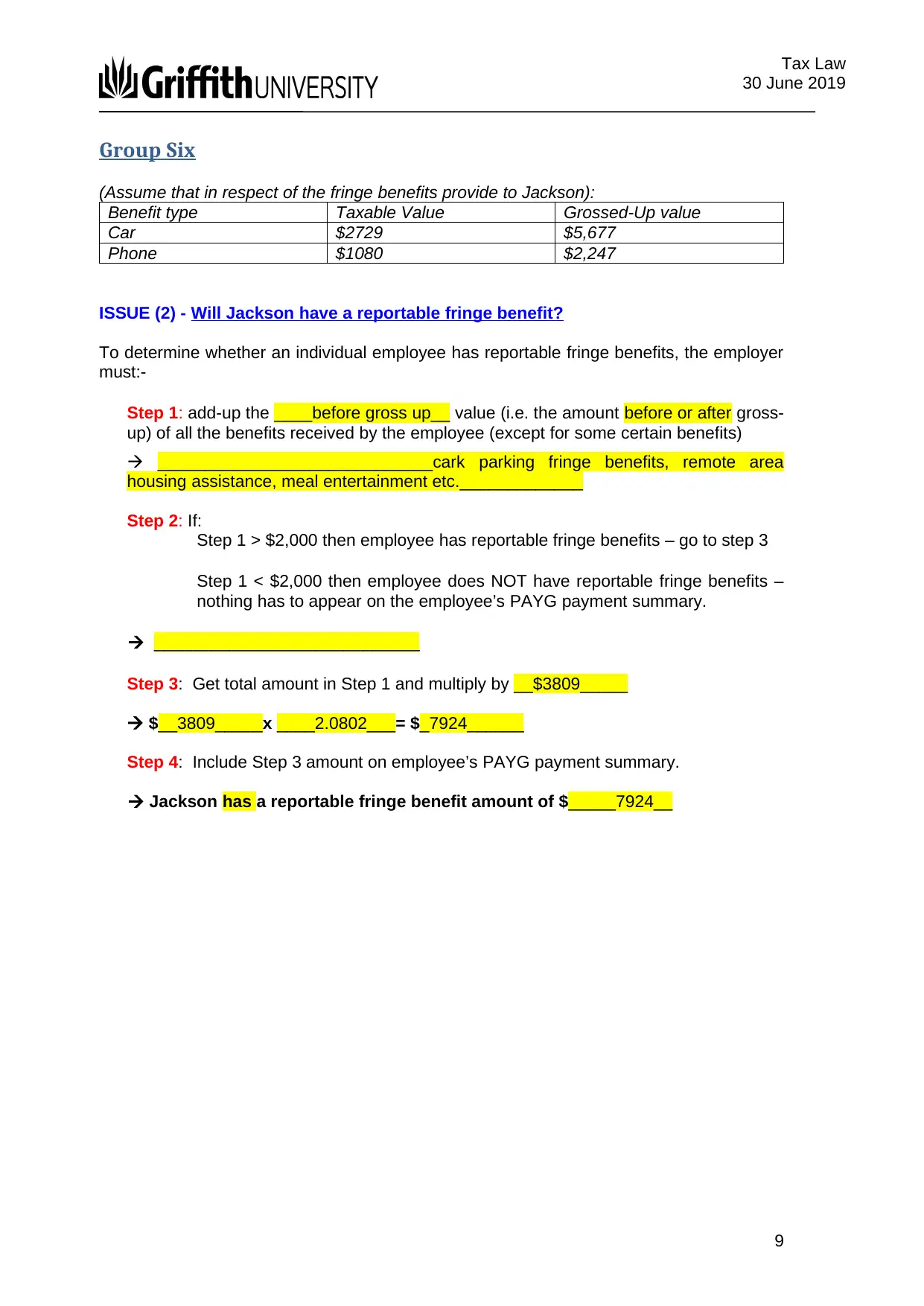

Group Six

(Assume that in respect of the fringe benefits provide to Jackson):

Benefit type Taxable Value Grossed-Up value

Car $2729 $5,677

Phone $1080 $2,247

ISSUE (2) - Will Jackson have a reportable fringe benefit?

To determine whether an individual employee has reportable fringe benefits, the employer

must:-

Step 1: add-up the ____before gross up__ value (i.e. the amount before or after gross-

up) of all the benefits received by the employee (except for some certain benefits)

_____________________________cark parking fringe benefits, remote area

housing assistance, meal entertainment etc._____________

Step 2: If:

Step 1 > $2,000 then employee has reportable fringe benefits – go to step 3

Step 1 < $2,000 then employee does NOT have reportable fringe benefits –

nothing has to appear on the employee’s PAYG payment summary.

____________________________

Step 3: Get total amount in Step 1 and multiply by __$3809_____

$__3809_____x ____2.0802___= $_7924______

Step 4: Include Step 3 amount on employee’s PAYG payment summary.

Jackson has a reportable fringe benefit amount of $_____7924__

9

30 June 2019

Group Six

(Assume that in respect of the fringe benefits provide to Jackson):

Benefit type Taxable Value Grossed-Up value

Car $2729 $5,677

Phone $1080 $2,247

ISSUE (2) - Will Jackson have a reportable fringe benefit?

To determine whether an individual employee has reportable fringe benefits, the employer

must:-

Step 1: add-up the ____before gross up__ value (i.e. the amount before or after gross-

up) of all the benefits received by the employee (except for some certain benefits)

_____________________________cark parking fringe benefits, remote area

housing assistance, meal entertainment etc._____________

Step 2: If:

Step 1 > $2,000 then employee has reportable fringe benefits – go to step 3

Step 1 < $2,000 then employee does NOT have reportable fringe benefits –

nothing has to appear on the employee’s PAYG payment summary.

____________________________

Step 3: Get total amount in Step 1 and multiply by __$3809_____

$__3809_____x ____2.0802___= $_7924______

Step 4: Include Step 3 amount on employee’s PAYG payment summary.

Jackson has a reportable fringe benefit amount of $_____7924__

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

References:

Australian Taxation Office. (2019, April 23). Fringe benefits tax - a guide for employers.

Retrieved from www.ato.gov.au: https://www.ato.gov.au/law/view/document?

DocID=SAV%2FFBTGEMP%2F00008

Commonwealth Numbered Acts. (2019, April 23). Retrieved from classic.austlii.edu.au:

http://classic.austlii.edu.au/au/legis/cth/num_act/fbtaa1986312/s136.html

10

30 June 2019

References:

Australian Taxation Office. (2019, April 23). Fringe benefits tax - a guide for employers.

Retrieved from www.ato.gov.au: https://www.ato.gov.au/law/view/document?

DocID=SAV%2FFBTGEMP%2F00008

Commonwealth Numbered Acts. (2019, April 23). Retrieved from classic.austlii.edu.au:

http://classic.austlii.edu.au/au/legis/cth/num_act/fbtaa1986312/s136.html

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.